Germany Semiconductor Foundry Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 2.48 Billion |

| Market Size (2030) | USD 6.80 Billion |

| Growth Rate (2025 - 2030) | 22.00% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Semiconductor Foundry Market Analysis by Mordor Intelligence

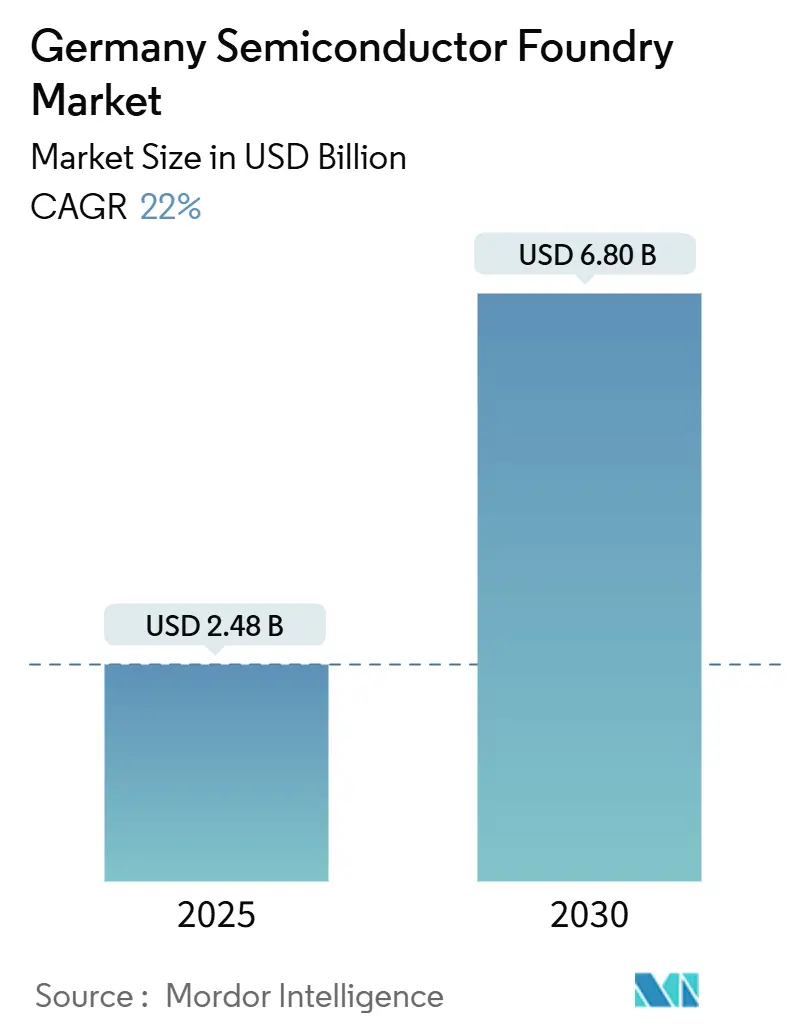

The German semiconductor foundry market size stands at USD 2.48 billion in 2025 and is forecast to reach USD 6.8 billion by 2030, reflecting a 22.0% CAGR over the period. The upsurge is attributable to EU Chips Act subsidies, large-scale joint ventures, and a decisive pivot toward advanced 16 nm and sub-10 nm technologies that underpin automotive electrification, edge AI, and high-performance computing. Pure-play operators are scaling aggressively, while integrated device manufacturers (IDMs) allocate fresh capacity to external customers, expanding the accessible pool of cutting-edge production. The Dresden-Magdeburg corridor has assumed hub status for Europe’s supply chain, offering critical labor density and logistics efficiencies that shorten time-to-volume. Export-control ambiguity and grid upgrades temper near-term momentum, but policy continuity and incremental renewable-energy integration act as balancing forces for sustained expansion.[1]European Commission, “Commission approves €5 billion German State aid measure to support ESMC in setting up a new semiconductor manufacturing facility,” EC.EUROPA.EU

Key Report Takeaways

- By application, automotive led with 41.4% revenue share in 2024, while high-performance computing is projected to post a 28.3% CAGR to 2030, making it the fastest-growing use case.

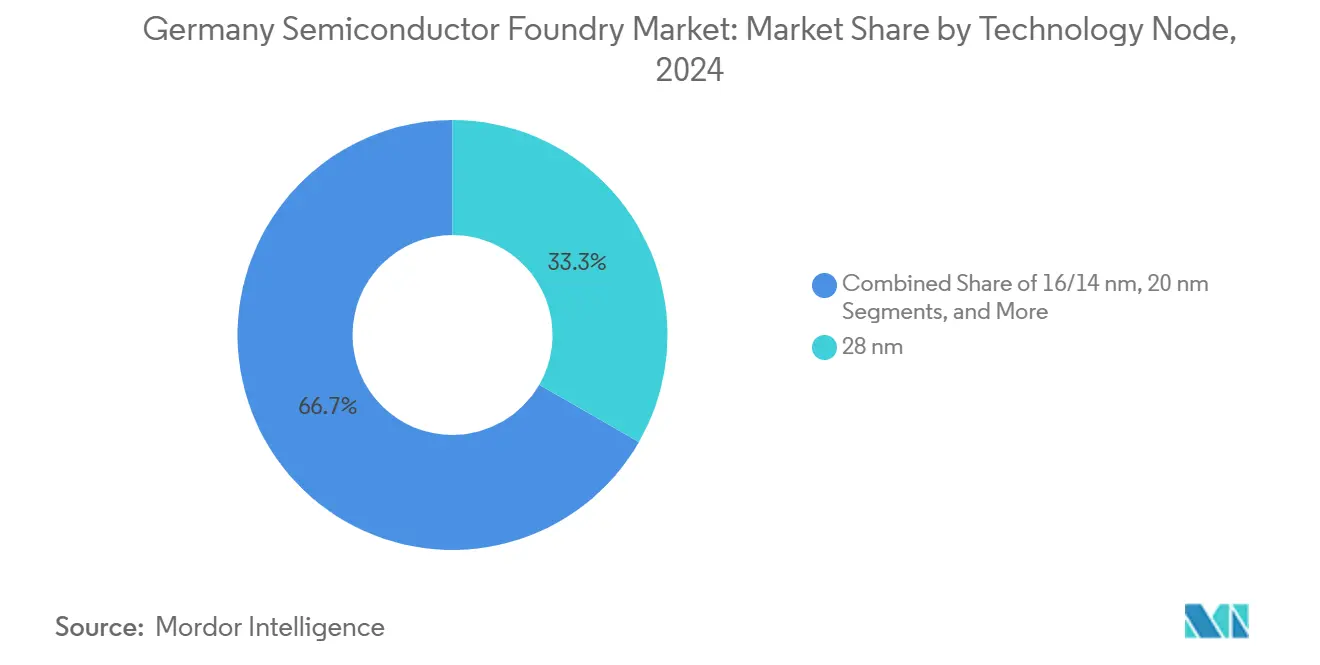

- By technology node, 28 nm accounted for 33.3% of the German semiconductor foundry market share in 2024; 10/7/5 nm and below are positioned to grow at a 30.3% CAGR through 2030.

- By wafer size, 300 mm commanded 52.5% share of the German semiconductor foundry market size in 2024 and is forecast to expand at a 24.2% CAGR up to 2030.

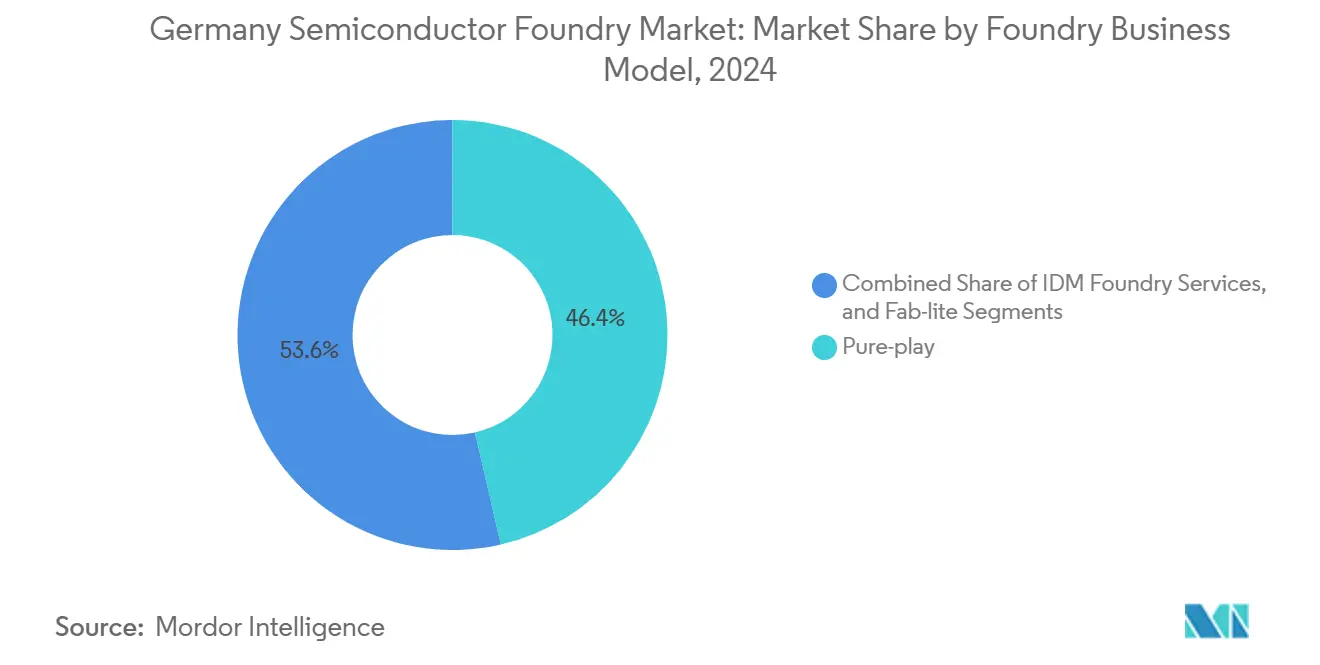

- By business model, pure-play foundries held 46.4% of the German semiconductor foundry market share in 2024, and the segment is advancing at a 24.2% CAGR through 2030.

Competitive positioning in Germany includes both locally based firms and those operating across multiple regions. The market landscape in the global semiconductor foundry industry research shows how these players are arranged internationally.

Germany Semiconductor Foundry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive electrification accelerates demand for 28 nm and 16 nm nodes | +6.8% | Dresden–Magdeburg corridor; spillover to Bavaria | Medium term (2-4 years) |

| EU Chips Act subsidies compress capital cost hurdles | +5.2% | Germany, concentrated in Saxony and Saarland | Short term (≤ 2 years) |

| Surging AI/edge inference creates new 7 nm-and-below volumes | +4.1% | Global demand; localized production in Dresden | Long term (≥ 4 years) |

| Silicon-Saxony talent cluster reduces cycle time | +2.9% | Saxony, extending to Thuringia | Medium term (2-4 years) |

| Power-device migration to 300 mm GaN and SiC lines | +2.3% | Germany-wide, focus on Dresden and Hamburg | Long term (≥ 4 years) |

| Tier-1 OEMs’ strategic inventories shift foundry sourcing onshore | +1.7% | Germany and the broader EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive Electrification Accelerates Demand for 28 nm and 16 nm Nodes

Electric vehicles now embed USD 1,500–2,000 worth of semiconductors per unit versus USD 500 in combustion models, propelling sustained demand for 28 nm and 16 nm process technologies that consolidate multiple control functions onto domain controllers. German OEMs are standardizing centralized E/E architectures that favor fusion chips, enabling one device to manage ADAS, infotainment, and drivetrain logic and improving bill-of-materials efficiency. ESMC’s upcoming Dresden fab aligns production ramps with this demand profile, underwritten by EUR 5 billion (USD 5.65 billion) in state aid that lowers entry barriers for ancillary Tier-1 suppliers. Proximity to automotive plants reduces logistics risk and mitigates the multi-billion-dollar shortages experienced during 2021–2023. Infineon’s migration toward 300 mm SiC production strengthens cost competitiveness for next-generation powertrain modules.[2]Press Office, “Infineon reaches next milestone on 200 mm silicon carbide roadmap,” INFINEON.COM

EU Chips Act Subsidies Compress Capital Cost Hurdles

The EU has earmarked EUR 43 billion (USD 48.6 billion) to seed semiconductor sovereignty, cutting effective capital intensity for new German fabs from 70–80% of revenue to roughly 40–50%. Key approvals include EUR 5 billion (USD 5.65 billion) for ESMC and EUR 1 billion (USD 1.13 billion) for Infineon’s Smart Power Fab, both contingent on open-foundry access that widens the user base beyond automotive majors. Temporary budget freezes in late 2024 highlighted political risk but were followed by a EUR 2 billion (USD 2.26 billion) supplemental package that reaffirmed commitment. The structure jointly funds pilot lines and workforce programs, ensuring research institutions and SMEs can prototype on the same nodes that scale into volume, strengthening the German semiconductor foundry market.

Surging AI/Edge Inference Creates New 7 nm-and-Below Volumes

AI accelerators are migrating from data centers to edge devices, including autonomous vehicles and factory robots. German institutes such as Fraunhofer IPMS partner with GlobalFoundries on 22FDX-based neuromorphic demonstrators, reducing inference power budgets by orders of magnitude. The Scale4Edge initiative builds RISC-V-compatible toolchains that lower NRE costs for localized AI plumbing. Dresden-based SEMRON has secured EUR 7.3 million (USD 8.25 million) to develop 3D stacked chips that multiply compute density, aligning with demand for real-time inference in smart-mobility ecosystems. FinFET and N-well engineering at 7 nm boost clock speeds while keeping thermal envelopes within ADAS module thresholds.[3]Research Group, “ANDANTE – AI for New Devices and Technologies at the Edge,” FRAUNHOFER.DE

Silicon-Saxony Talent Cluster Reduces Cycle Time

Silicon Saxony houses more than 81,000 microelectronics employees and 3,600 companies, providing a deep labor reservoir that shortens ramp-up cycles compared with greenfield locations in other EU regions. TU Dresden funnels engineering graduates directly into fabs while chamber-of-commerce programs accelerate technician retraining. TSMC will tap GlobalFoundries alums to shorten its Dresden start-up curve, shrinking expected learning phases. Although software and consulting firms bid aggressively for STEM talent, targeted apprenticeship incentives and EU-funded reskilling schemes partially offset wage pressure. The cluster effect—tight supplier footprint, specialized maintenance crews, and shared clean-room protocols—reduces cycle time and defects per wafer, reinforcing Germany's semiconductor foundry market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labour shortages in the Dresden/Magdeburg corridor | −3.4% | Saxony and Saxony-Anhalt | Short term (≤ 2 years) |

| Build-out delays from utility-grid bottlenecks | −2.8% | Eastern Germany, particularly Dresden and Magdeburg | Medium term (2-4 years) |

| Margin pressure from legacy-node price erosion | −1.9% | Germany-wide | Long term (≥ 4 years) |

| Export-control uncertainty on advanced lithography tools | −1.6% | Germany-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labour Shortages in Dresden/Magdeburg Corridor

An estimated 62,000 semiconductor-related vacancies existed in 2024, with the metal-and-electrical sector reporting 110,000 open roles across Germany. Intel’s Magdeburg project illustrates the gap: 3,000 new positions versus a pipeline producing only a pair of technicians, forcing extensive in-house training and international recruitment. High-wage software firms intensify competition, elevating average clean-room salaries and inflating operating costs. Demographics compound the constraint as senior experts approach retirement, accelerating knowledge attrition. Immigration reforms aim to widen talent inflow, but onboarding and language-training lead times blunt quick relief.

Build-Out Delays from Utility-Grid Bottlenecks

A single advanced fab can draw 1 GW of electricity, yet eastern Germany’s grid remains under strain from the national energy transition and the fallout from the Russia-Ukraine conflict. Renewable integration requires new transmission lines and storage that involve lengthy permitting cycles. Semiconductor expansion may therefore proceed in phased modules until sub-stations and redundant feeders come online. In the interim, operators secure backup generation and craft purchasing agreements for carbon-neutral power to align with EU sustainability norms, adding complexity and capital to project schedules.[4]Nikos Tsafos, “Energy Considerations at the Dawn of Strategic Manufacturing,” CSIS.ORG

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Node: Advanced Nodes Drive Future Growth

In 2024, the 28 nm process led with 33.3% share of the German semiconductor foundry market. The tier balances performance and cost for powertrain controllers and sensor hubs. The German semiconductor foundry market size for 10/7/5 nm and below is forecast to grow at a 30.3% CAGR on rising AI inference and next-generation zonal architectures. Strategic collaborations with equipment vendors ensure earlier tool deliveries that compress time-to-yield. Adoption of chiplet architectures further reduces large-die risk while leveraging mature nodes for I/O functions.

The 16/14 nm bracket serves as a bridge, offering FinFET power savings without the EUV exposure of sub-10 nm flows, making it attractive for safety-critical automotive compute. Legacy 65 nm and above continue in battery-management ICs yet earn lower ASPs, pressuring margins. Integration of advanced packaging, including fan-out and 3D stacking, allows heterogeneous integration that prolongs the life of established nodes. This positioning enhances overall asset utilization across fabs and supports balanced revenue diversification within the German semiconductor foundry market.

By Wafer Size: 300 mm Dominance Accelerates

The 300 mm category held 52.5% of the German semiconductor foundry market share in 2024 and is projected to log a 24.2% CAGR to 2030. Migration delivers 2.3× more dies per wafer versus 200 mm, cutting unit cost while facilitating advanced lithography. The German semiconductor foundry market size for 300 mm substrates benefits from Infineon’s EUR 5 billion (USD 5.65 billion) Smart Power Fab and Nexperia’s USD 200 million Hamburg upgrade, which aligns wide-bandgap production with automotive electrification.

Sub-150 mm wafers persist in legacy analog, MEMS, and specialty devices where depreciation is complete and changeover savings are marginal. Hybrid lines add 200 mm SiC as an intermediate step, but industry roadmaps converge on full 300 mm for GaN and SiC by late-decade. Larger wafers also streamline automation and enable higher cleanliness classes, key for defect density targets in safety-critical applications.

By Foundry Business Model: Pure-Play Leadership Strengthens

Pure-play players accounted for a 46.4% share in 2024 and outpaced the market at a 24.2% CAGR to 2030. Customers value the design-manufacturing firewall, assured capacity commitments, and multiparty benchmarking inherent in the model. The German semiconductor foundry market size tied to pure-play contracts grows as Bosch, BMW, and VW migrate from ad-hoc wafer agreements toward structured long-term supply deals.

IDM foundry services remain important for niche power devices and analog front ends, leveraging internal IP to offer application-specific process variants. Fab-lite companies outsource leading-edge wafers while retaining back-end and specialty in-house lines, preserving capital flexibility. Subsidy parity debates, triggered by GlobalFoundries’ protest over TSMC’s incentives, underscore competitive pressure within the pure-play camp and may shape future funding frameworks.

By Application: Automotive Leadership with HPC Acceleration

Automotive held 41.4% revenue share in 2024, reflecting Germany’s industrial focus and OEM re-shoring strategy. High-performance computing is the fastest riser, tracking a 28.3% CAGR on the back of edge-AI use cases in autonomous driving and industrial analytics. The German semiconductor foundry market size for HPC chips benefits from combined AI inference and power-efficient packaging, enabling system consolidation that lowers vehicle weight and board complexity.

Consumer electronics and communication maintain steady baseline volumes, important for fab loading but less so for margin optimization. Industrial and IoT leverage Industry 4.0 investments that require real-time control and sensor aggregation, often fabricated on 40/28 nm processes. Emerging medical, aerospace, and renewable-power converters widen the customer mix, stabilizing order books and reducing cyclicality tied to any single sector.

Geography Analysis

The German semiconductor foundry market derives strategic depth from the Dresden–Magdeburg corridor, which hosts ESMC’s EUR 10 billion (USD 11.3 billion) fab, Infineon’s Smart Power Fab, and GlobalFoundries’ existing cluster. More than 81,000 employees support 3,600 companies, delivering dense supplier networks and coordinated logistics that compress cycle times. Dresden’s mature clean-room ecosystem and training infrastructure allow quick ramp-ups relative to alternate EU sites.

Bavaria and Baden-Württemberg complement eastern capacity with design hubs and specialized fabs. KIT’s Chipdesign House will add research programs and a new Master’s curriculum by 2027, sharpening local IP creation and keeping tape-outs within Germany. Munich’s critical mass of EDA vendors and OSAT partners supports front-end-to-back-end coherence and enables rapid prototyping for Tier-1 suppliers.

Within the broader EU context, Germany captures roughly one-third of European semiconductor value and leads export volumes. The target of 20% global production share by 2030 hinges on Germany sustaining policy and grid upgrades. Improved export-control coordination with Brussels mitigates tool-access risks. Neighboring Ireland and the Netherlands retain niche competencies in photonics and EUV tool assembly, but Germany’s integrated manufacturing-design base and automotive anchor customers secure its primacy in regional capacity allocation.

Mordor Intelligence tracks the semiconductor foundry market with additional country-level coverage spanning Taiwan, Japan, Singapore, South Korea, China, United States, Malaysia, and Israel, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competition centers on process leadership, subsidy allocation, and automotive intimacy. TSMC’s European Semiconductor Manufacturing Company introduces cutting-edge FinFET capability and benefits from EUR 5 billion (USD 5.65 billion) in aid, challenging GlobalFoundries’ long-held incumbency. GlobalFoundries leverages 25 years of Dresden know-how and proprietary 22FDX processes, but seeks subsidy parity to finance 12 nm extensions. Infineon and Bosch wield IDM expertise in power semiconductors, offering customers differentiated process recipes validated to automotive AEC-Q100 standards.

Technology roadmaps converge on wide-bandgap materials and advanced packaging. Infineon’s rollout of 200 mm SiC products underscores first-mover advantage in high-voltage electrification. Nexperia’s Hamburg investment extends SiC and GaN capacity and strengthens supply chains for inverter modules. X-FAB keeps high-volume 6-inch SiC lines active for niche industrial demand, demonstrating parallel technology stacks in a single geography.

Collaborative models proliferate as talent constraints force pooling resources. EV Group and Fraunhofer IZM-ASSID expand wafer-bonding programs for quantum devices that need sub-micron alignment accuracy. The incremental emergence of specialized RISC-V design houses promises to widen the customer set for open foundry lanes, but margin compression in legacy nodes imposes operational discipline to sustain profitability in lower-ASP tiers.

Germany Semiconductor Foundry Industry Leaders

-

GlobalFoundries Inc. (Fab 1 Dresden)

-

X-FAB Silicon Foundries SE

-

Infineon Technologies AG – Foundry Services

-

Robert Bosch GmbH (Foundry)

-

European Semiconductor Manufacturing Company (ESMC) GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Infineon Technologies received final funding approval for its Smart Power Fab in Dresden, securing EUR 1 billion (USD 1.13 billion) under IPCEI ME/CT; production will commence in 2026.

- August 2025: TSMC broke ground on its EUR 10 billion (USD 11.3 billion) ESMC facility in Dresden, targeting 40,000 wpm at 28/22 nm and 16/12 nm nodes by late 2027.

- July 2025: Germany expanded export controls on low-temperature CMOS and dry-etch tools, increasing licensing hurdles for semiconductor equipment shipments.

- June 2025: Nexperia announced a USD 200 million upgrade at Hamburg to add SiC and GaN production lines for power devices.

Germany Semiconductor Foundry Market Report Scope

| 10/7/5 nm and below |

| 16/14 nm |

| 20 nm |

| 28 nm |

| 45/40 nm |

| 65 nm and above |

| 300 mm |

| 200 mm |

| <150 mm |

| Pure-play |

| IDM Foundry Services |

| Fab-lite |

| Consumer Electronics and Communication |

| Automotive |

| Industrial and IoT |

| High-Performance Computing (HPC) |

| Other Applications |

| By Technology Node | 10/7/5 nm and below |

| 16/14 nm | |

| 20 nm | |

| 28 nm | |

| 45/40 nm | |

| 65 nm and above | |

| By Wafer Size | 300 mm |

| 200 mm | |

| <150 mm | |

| By Foundry Business Model | Pure-play |

| IDM Foundry Services | |

| Fab-lite | |

| By Application | Consumer Electronics and Communication |

| Automotive | |

| Industrial and IoT | |

| High-Performance Computing (HPC) | |

| Other Applications |

Key Questions Answered in the Report

How large is the German semiconductor foundry market in 2025?

The German semiconductor foundry market size is USD 2.48 billion in 2025 and is projected to grow to USD 6.8 billion by 2030.

Which application contributes the most revenue?

Automotive applications generated 41.4% of revenue in 2024, reflecting Germany’s strong vehicle manufacturing base.

What process node is expanding fastest?

The 10/7/5 nm-and-below segment is expanding at a 30.3% CAGR through 2030 due to AI and centralized vehicle architectures.

Why is the Dresden–Magdeburg corridor strategic?

The corridor clusters fabs, suppliers, and 81,000 skilled workers, reducing cycle time and logistics costs.

How do EU subsidies impact capital intensity?

Chips Act incentives cut capital intensity from 70–80% of revenue to 40–50%, making German fabs globally competitive.

What limits near-term capacity expansion?

Skilled-labor shortages and utility-grid bottlenecks reduce ramp-up speed and add incremental capital expense.

Page last updated on: