Photomedicine Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

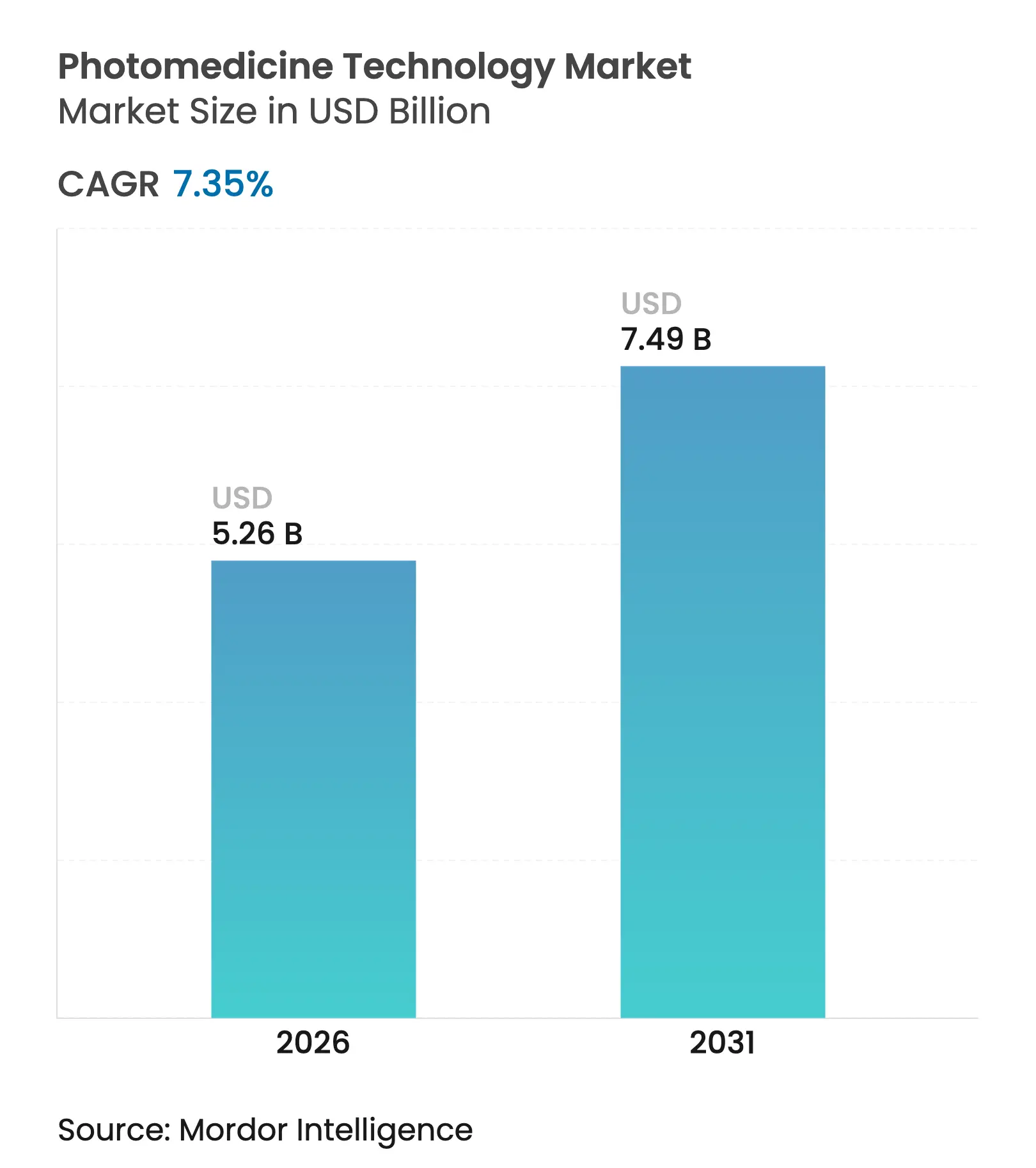

| Market Size (2026) | USD 5.26 Billion |

| Market Size (2031) | USD 7.49 Billion |

| Growth Rate (2026 - 2031) | 7.35 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Photomedicine Technology Market Analysis by Mordor Intelligence

Photomedicine technology market size in 2026 is estimated at USD 5.26 billion, growing from 2025 value of USD 4.90 billion with 2031 projections showing USD 7.49 billion, growing at 7.35% CAGR over 2026-2031. The market’s trajectory is underpinned by rapid progress in laser engineering, growing clinical validation of non-thermal modalities, and steady regulatory support that lowers adoption barriers across multiple care settings. Advances such as AI-guided dosimetry, closed-loop feedback, and wireless dual-light delivery elevate therapeutic precision while reducing operator variability, allowing providers to treat broader patient profiles with improved outcomes. The competitive landscape shows measured consolidation. Alcon’s pending acquisition of LumiThera for the FDA-cleared Valeda photobiomodulation platform and the Cynosure–Lutronic merger illustrate a strategic rush toward portfolio breadth and differentiated IP in AI-enabled systems.

Key Report Takeaways

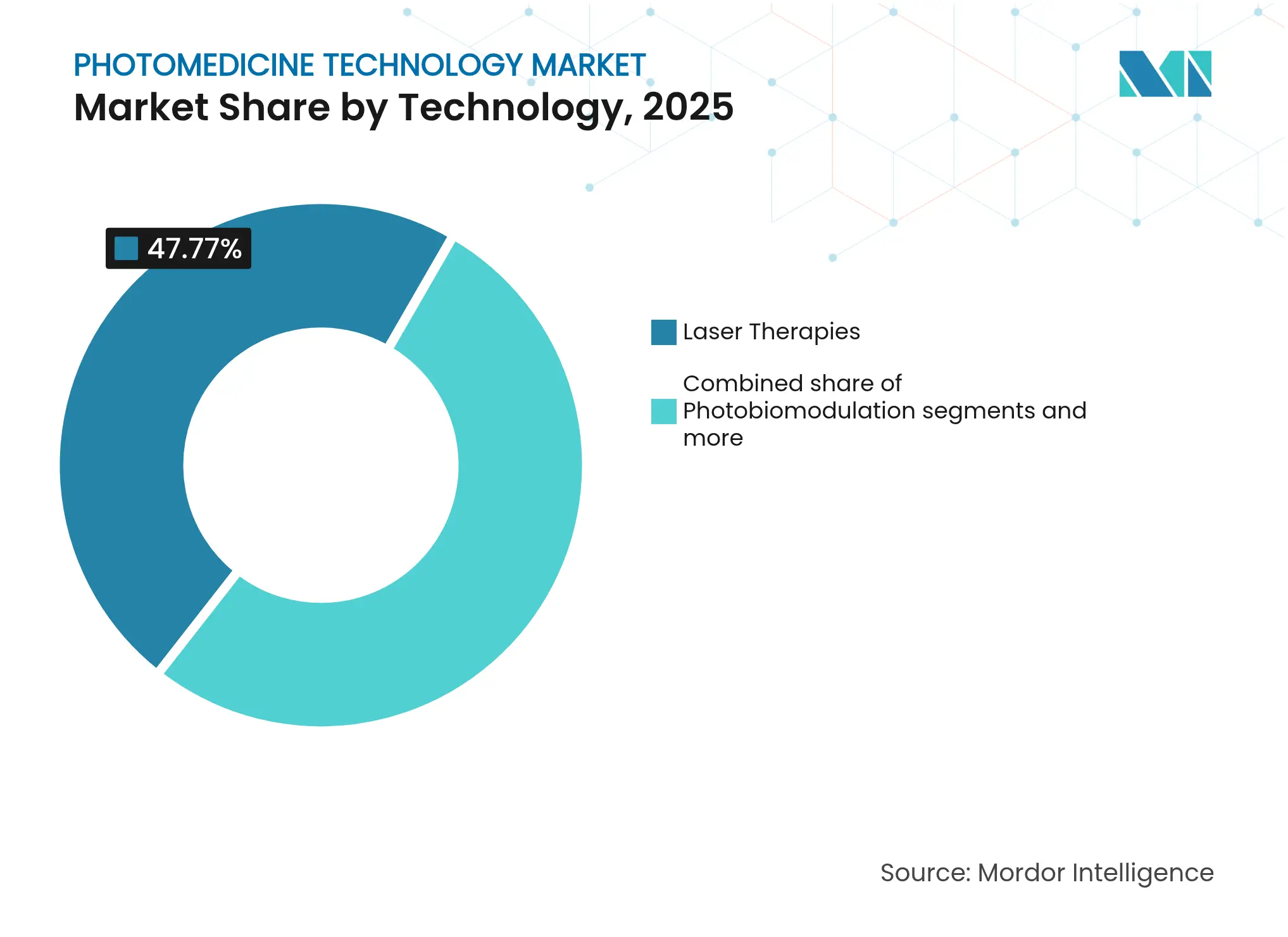

- By technology, laser therapies led with 47.77% of the photomedicine technology market share in 2025; photobiomodulation is projected to expand at an 7.85% CAGR to 2031.

- By application, dermatology and aesthetics accounted for 40.78% of the photomedicine technology market size in 2025, while oncology PDT is advancing at an 8.02% CAGR.

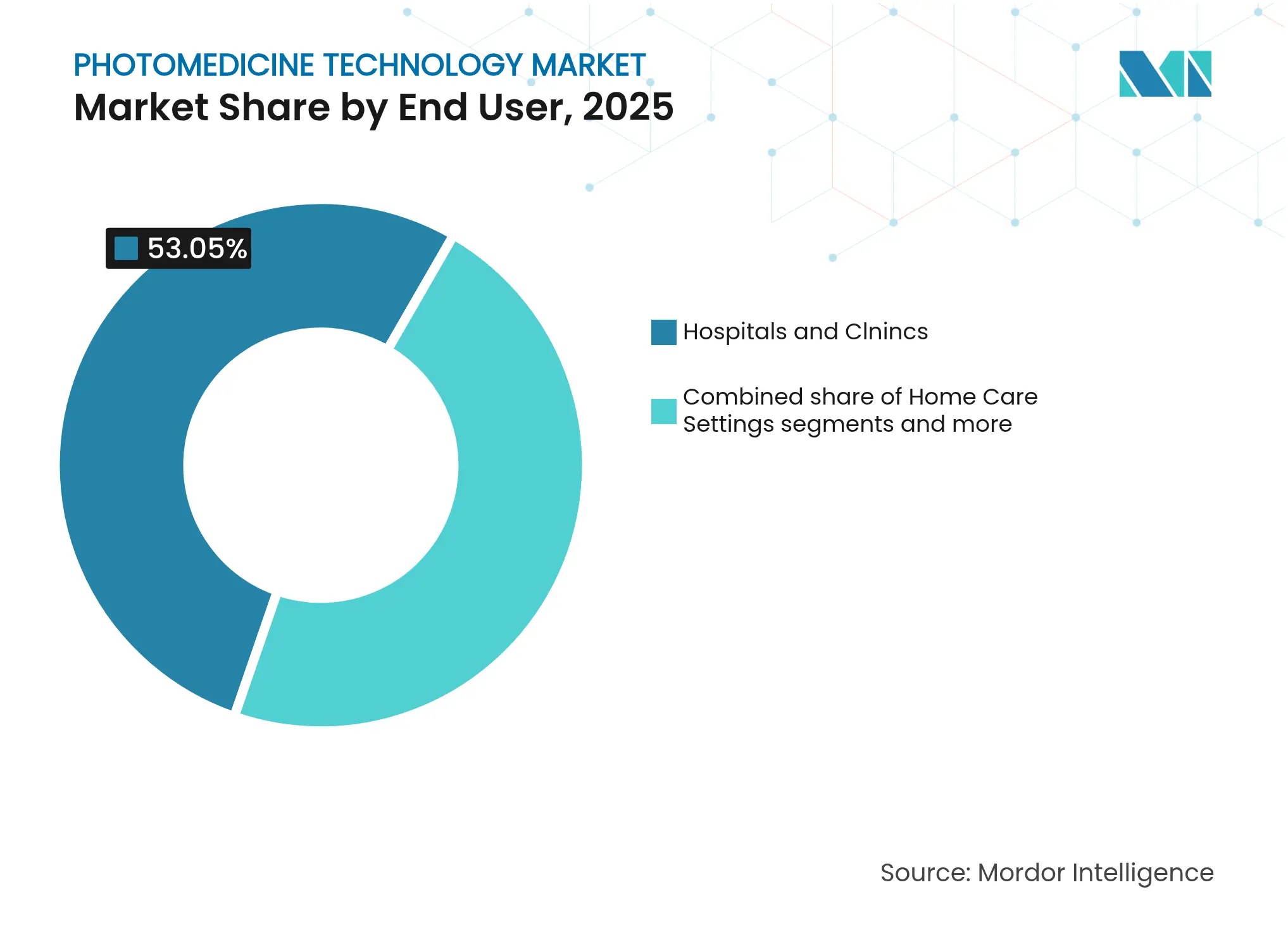

- By end user, hospitals and clinics commanded 53.05% share of the photomedicine technology market size in 2025; home-care settings record the highest forecast CAGR at 8.12%.

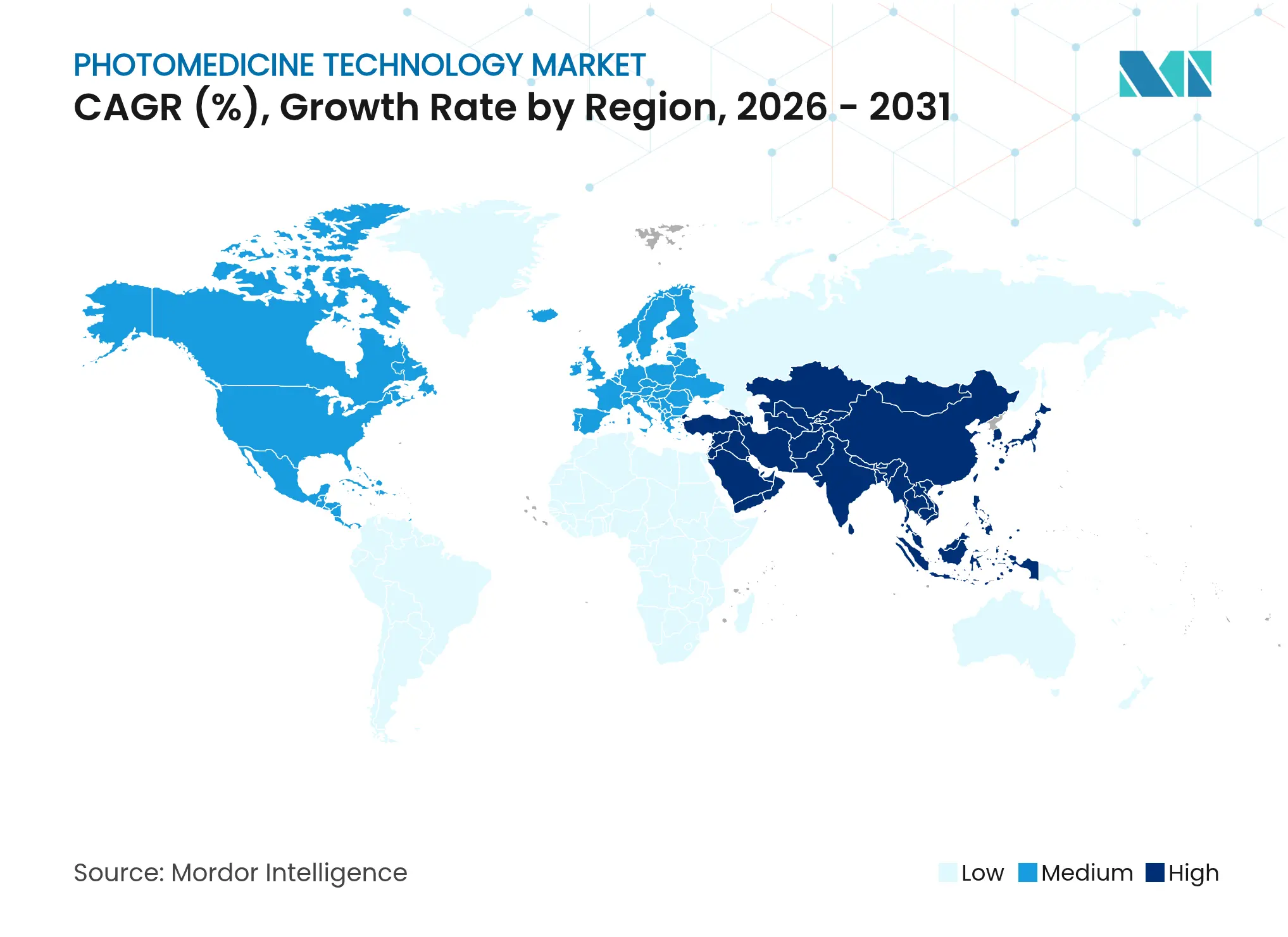

- By geography, North America captured 38.88% of the photomedicine technology market share in 2025; Asia-Pacific exhibits the fastest regional CAGR at 8.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photomedicine Technology Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for non-invasive aesthetic procedures Rising demand for non-invasive aesthetic procedures | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Global, with concentration in North America & Europe | Impact Timeline:Medium term (2-4 years) |

Technological advancements in laser & LED platforms Technological advancements in laser & LED platforms | +1.8% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) | |||

Growing prevalence of dermatological disorders & cancers Growing prevalence of dermatological disorders & cancers | +1.5% | Global, with higher impact in aging populations | Long term (≥ 4 years) | |||

Expanding adoption in pain management therapies Expanding adoption in pain management therapies | +1.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) | |||

Surge in at-home phototherapy devices with tele-health support Surge in at-home phototherapy devices with tele-health support | +1.4% | North America initially, global expansion | Short term (≤ 2 years) | |||

AI-driven dosimetry & closed-loop feedback integration AI-driven dosimetry & closed-loop feedback integration | +1.0% | North America & Europe, selective APAC markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Non-Invasive Aesthetic Procedures

Consumer preference for minimal-downtime treatments continues to elevate energy-based platforms over surgical alternatives. FDA authorization of Biofrontera’s RhodoLED XL lamp for actinic keratosis in July 2024 supplied dermatology clinics with a large-area red-light source that reduces chair time and pain scores. Clinical trials confirm photodynamic therapy achieves 90.9% lesion clearance, strengthening patient confidence and enabling cross-selling of cosmetic and therapeutic sessions within the same practice. Equipment makers leverage this dual-purpose demand by bundling multiple handpieces and subscription-based disposables, supporting predictable revenue while maximizing device utilization.

Technological Advancements in Laser & LED Platforms

Next-generation systems feature multi-wavelength emitters, AI-assisted dosimetry, and wireless operation. A 2024 Nature study detailed a sequential dual-light implant that programs PDT by toggling photosensitizer activation in vivo, achieving deeper tumor necrosis without thermal injury. Concurrently, self-calibrating OCT-SLO imaging reached 2.41-µm resolution, enabling real-time feedback loops that modulate fluence based on tissue absorption. Such closed-loop platforms transition photomedicine from manual adjustment to algorithm-driven precision, boosting efficacy and lowering adverse-event incidence.

Growing Prevalence of Dermatological Disorders & Cancers

Aging populations and UV exposure are expanding the addressable base for actinic keratosis, basal-cell carcinoma, and early prostate cancer. Medicare now reimburses dermatologist-administered PDT, lowering out-of-pocket costs and strengthening clinic economics. Parallel oncology trials using SpectraCure’s P18 interstitial fiber and verteporfin show promising ablation of localized prostate tumors, extending photomedicine beyond cutaneous lesions. Such broadened indications underpin long-run revenue visibility for device makers.

Expanding Adoption in Pain Management Therapies

Photobiomodulation (PBM) offers a drug-free alternative amid opioid stewardship initiatives. A 2024 triple-blind RCT reported systemic PBM shortened ICU stays and restored muscle strength, highlighting its utility beyond localized treatment. Veterinary clinics, where roughly 40% now employ laser therapy, further validate cross-species anti-inflammatory effects, reinforcing clinician confidence for human rehabilitation settings.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital cost of advanced equipment High capital cost of advanced equipment | -0.8% | Global, more pronounced in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Global, more pronounced in emerging markets | Impact Timeline:Medium term (2-4 years) |

Stringent safety regulations & approval timelines Stringent safety regulations & approval timelines | -0.6% | Global, with regional variations in severity | Long term (≥ 4 years) | |||

Lack of reimbursement for novel photobiomodulation protocols Lack of reimbursement for novel photobiomodulation protocols | -0.5% | Primarily North America & Europe | Medium term (2-4 years) | |||

Limited clinical evidence for hybrid multi-wavelength devices Limited clinical evidence for hybrid multi-wavelength devices | -0.4% | Global, affecting premium device segments | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital Cost of Advanced Equipment

Multi-wavelength platforms with AI circuitry command list prices surpassing USD 500,000, straining budgets of mid-size practices in Latin America, Southeast Asia, and rural U.S. counties. Pay-per-use SaaS models such as Modulight’s cloud-connected lasers lower entry hurdles yet may inflate lifetime cost and tie facilities to long-term service contracts. Budget constraints thus prolong replacement cycles and slow penetration into secondary care facilities.

Stringent Safety Regulations & Approval Timelines

While ensuring patient welfare, the FDA’s 2023 draft guidance on PBM devices mandates biocompatibility, dosimetry, and usability evidence, lengthening 510(k) timelines by 12-18 months for start-ups with limited clinical budgets[1]Source: CDRH, “Draft Guidance on Photobiomodulation Devices,” fda.gov . Japan’s evolving conditional approval framework similarly introduces uncertainty around post-market surveillance obligations, prompting some innovators to prioritize CE-mark markets first. Such regulatory opacity raises capital needs and delays global roll-outs.

Segment Analysis

By Technology: Laser Dominance Faces Photobiomodulation Challenge

Laser therapies accounted for 47.77% of 2025 revenue within the photomedicine technology market. Their clinical breadth ranges from CO₂ resurfacing to femtosecond ophthalmic surgery. Conversely, photobiomodulation is accelerating at an 7.85% CAGR, supported by LED arrays that deliver sub-thermal fluence for systemic pain and muscle recovery. LED platforms, cheaper and easier to operate, widen adoption among nursing homes and sports clinics. PDT maintains a specialized niche in oncology, especially when paired with next-generation photosensitizers.

Growing clinician familiarity with multi-wavelength consoles—capable of 670 nm, 810 nm, 980 nm, and 1,064 nm pulses—enables protocol personalization. The photomedicine technology market size for dual-modality laser-LED systems is forecast to expand alongside AI-embedded handpieces that auto-titrate dose. Automated fiber coupling cuts set-up time by 20%, enhancing per-hour case throughput. Integrated imaging further converges diagnosis and therapy, offering vendors differentiated value propositions.

Note: Segment shares of all individual segments available upon report purchase

By Application: Oncology PDT Accelerates Beyond Aesthetic Leadership

Dermatology and aesthetics remained the revenue anchor in 2025, delivering 40.78% share as photorejuvenation and scar revision procedures stayed resilient even amid payer scrutiny. Yet oncology PDT’s 8.02% CAGR signals a pivot toward systemic disease states with larger reimbursement envelopes. Early-stage prostate and glioma trials highlight improved margin control and minimal systemic toxicity.

The photomedicine technology market size for ophthalmology is bolstered by Valeda’s dry AMD clearance, a landmark that introduces visual-function improvement where pharmaceutical options remain limited. Pain-management and wound-healing sub-segments also expand as providers adopt whole-body PBM chambers to tackle fibromyalgia and diabetic ulcers. Dental and veterinary niches benefit from gingival healing outcomes that cut antibiotic use by 30%, supporting cross-disciplinary revenue streams.

By End User: Home Care Disrupts Traditional Clinical Models

Hospitals and clinics controlled 53.05% revenue in 2025, leveraging integrated imaging, anesthesia, and reimbursement chains. However, home-care settings are posting the swiftest gains at 8.12% CAGR, catalyzed by Zerigo’s UVB handhelds and Bluetooth-linked treatment logs. The photomedicine technology market size for remote devices will likely triple by 2030 as telehealth parity laws mandate insurer coverage for virtual supervision.

Dermatology-only centers still thrive by bundling loyalty programs and membership plans that guarantee repeat sessions for acne, melasma, and photoaging. Veterinary clinics, capturing household spending on companion animals, validate PBM efficacy and provide incremental revenue that offsets seasonality in elective human procedures.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America’s 38.88% stake reflects Medicare coverage for PDT and vibrant venture funding for AI-guided lasers. Top U.S. centers such as Memorial Sloan Kettering are trialing interstitial PDT for urologic tumors, reinforcing academic-industry collaboration. Device makers benefit from CPT code stability that shields margins against pricing pressure.

Asia-Pacific exhibits the highest 8.66% CAGR, driven by Japan’s PMDA fast-track and China’s broadened National Reimbursement Drug List that now includes domestic photosensitizers. Medical-tourism hubs in Thailand and South Korea market bundled aesthetic packages combining laser resurfacing with LED therapy, luring international clientele seeking cost savings without quality trade-offs.

Europe remains steady as CE-mark compliance allows rapid migration from clinical pilot to commercial deployment, especially in Germany, France, and the Nordics. The EU’s Medical Device Regulation (MDR) introduces post-market surveillance overhead, yet local manufacturers have leveraged notified-body familiarity to maintain rollout cadence.

Emerging regions, South America, Middle East, and Africa, gain traction via private dermatology chains and mobile clinic deployments, although high capital costs temper growth. Government-funded tele-dermatology pilots in Brazil illustrate how cloud-linked PBM devices can reach remote populations at a fraction of hospital-based care costs.

Competitive Landscape

Market Concentration

Industry concentration is moderate, with top quintile vendors controlling an estimated half of global revenue, a level that supports healthy competition while enabling meaningful R&D scale. Alcon’s bid for LumiThera underscores strategic appetite for vision-care franchises. Cynosure-Lutronic’s merger pools over 500 active U.S. and Korean patents, creating a one-stop aesthetic portfolio.

IRIDEX’s USD 10 million capital infusion targets footprint expansion for MicroPulse glaucoma lasers, while BTL’s ExoTMS launch illustrates adjacency moves into neuromodulation. Emerging players emphasize AI differentiation, with start-ups using multimodal AI for automatic treatment planning and claiming 20% dose-optimization gains over rule-based software. Veterinary-focused suppliers, such as Companion Animal Health, seize white space by repurposing PBM carts for small-animal dentistry and orthopedic pain management.

Strategic alliances between manufacturers and telehealth providers fuel subscription models that bundle hardware, firmware updates, and virtual consultations, generating recurring revenue and deep data pools that refine algorithms. Intellectual property intensity remains high; more than 1,300 photomedicine-related patents were filed globally in 2024, signaling sustained innovation barriers for late entrants.

Photomedicine Technology Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Alcon agreed to acquire LumiThera and its FDA-cleared Valeda photobiomodulation system, targeting the 200 million-patient dry AMD segment

- March 2025: IRIDEX raised USD 10 million from Novel Inspiration International to scale MicroPulse platforms for retinal disease.

Table of Contents for Photomedicine Technology Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising demand for non-invasive aesthetic procedures

- 4.2.2Technological advancements in laser & LED platforms

- 4.2.3Growing prevalence of dermatological disorders & cancers

- 4.2.4Expanding adoption in pain management therapies

- 4.2.5Surge in at-home phototherapy devices with tele-health support

- 4.2.6AI-driven dosimetry & closed-loop feedback integration

- 4.3Market Restraints

- 4.3.1High capital cost of advanced equipment

- 4.3.2Stringent safety regulations & approval timelines

- 4.3.3Lack of reimbursement for novel photobiomodulation protocols

- 4.3.4Limited clinical evidence for hybrid multi-wavelength devices

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Technology

- 5.1.1Laser Therapies

- 5.1.2LED Therapy

- 5.1.3Photodynamic Therapy

- 5.1.4Photobiomodulation (Low-Level Laser)

- 5.1.5Ultraviolet B Phototherapy

- 5.1.6Others

- 5.2By Application

- 5.2.1Dermatology & Aesthetics

- 5.2.2Oncology (PDT)

- 5.2.3Ophthalmology

- 5.2.4Pain Management & Musculoskeletal

- 5.2.5Wound Healing

- 5.2.6Dental Applications

- 5.2.7Others

- 5.3By End User

- 5.3.1Hospitals & Clinics

- 5.3.2Specialized Dermatology & Aesthetic Centers

- 5.3.3Home Care Settings

- 5.3.4Veterinary Clinics

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4South Korea

- 5.4.3.5Australia

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1GCC

- 5.4.5.2South Africa

- 5.4.5.3Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Koninklijke Philips N.V.

- 6.3.2Johnson & Johnson

- 6.3.3Lumenis Ltd.

- 6.3.4Candela Corporation

- 6.3.5BTL Industries

- 6.3.6Cynosure, LLC

- 6.3.7IRIDEX Corporation

- 6.3.8THOR Photomedicine Ltd

- 6.3.9Biolitec AG

- 6.3.10Alma Lasers (Sisram Medical)

- 6.3.11Cutera, Inc.

- 6.3.12Aspen Laser Systems, LLC

- 6.3.13Archimed

- 6.3.14Fotona d.o.o.

- 6.3.15Carl Zeiss Meditec AG

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Photomedicine Technology Market Report Scope

As per the scope of the report, photomedicine is a branch of medicine that deals with the application of light with respect to health and disease. The report on the photomedicine technology market includes the range of products and services being used by (but not limited to) hospitals, clinics, organizations, and individuals for healthcare therapies.

The photomedicine technology market is segmented by application (aesthetics and dermatology, dental procedures, oncology, ophthalmology, pain management, wound healing, and other applications) and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.