Sterile Medical Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

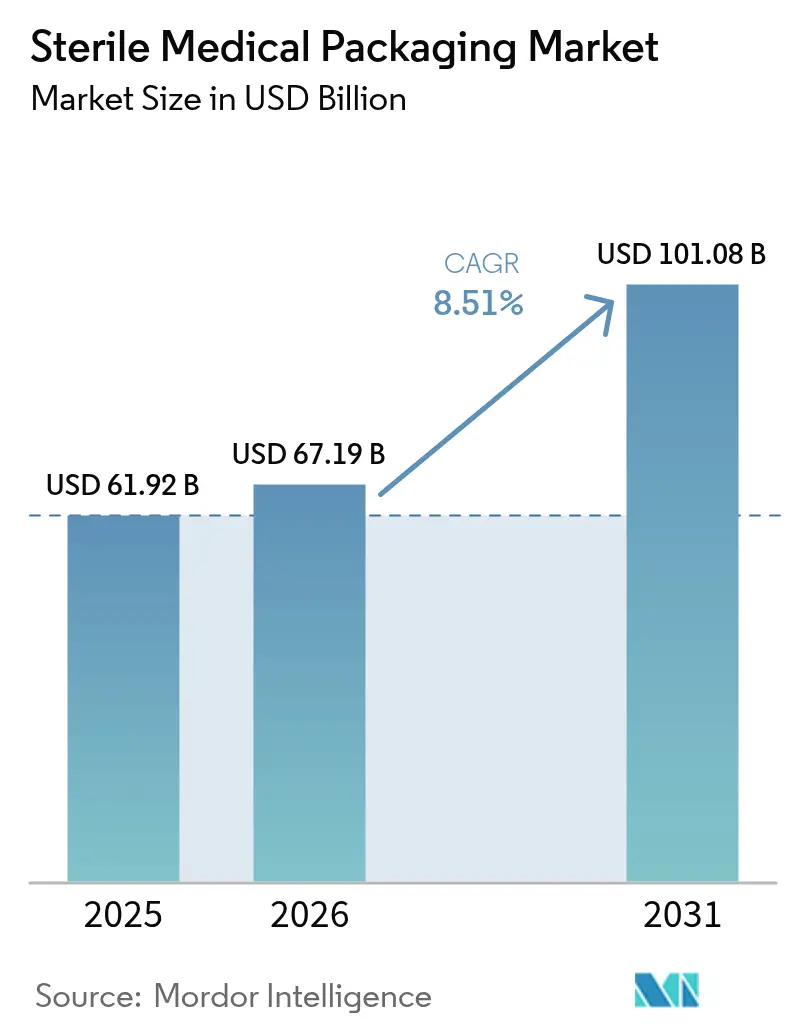

| Market Size (2026) | USD 67.19 Billion |

| Market Size (2031) | USD 101.08 Billion |

| Growth Rate (2026 - 2031) | 8.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterile Medical Packaging Market Analysis by Mordor Intelligence

The sterile medical packaging market size is projected to be USD 61.92 billion in 2025, USD 67.19 billion in 2026, and reach USD 101.08 billion by 2031, growing at a CAGR of 8.51% from 2026 to 2031. Persistent infection-control mandates, accelerated biologics commercialization, and rapid material innovation are pushing pharmaceutical buyers to upgrade from legacy packs to high-barrier, recyclable solutions. Tightening alignment with ISO 11607 revisions, the February 2026 U.S. Quality Management System Regulation, and parallel European Union requirements are eliminating older lines that cannot deliver end-to-end traceability, which, in turn, is lifting average selling prices. Resin volatility remains a swing factor, yet converters that backward-integrated into compounding have shielded margins and preserved capacity commitments. Finally, the near-shoring of contract sterilization hubs inside major life-science corridors has shortened order-to-sterilize cycles, enabling just-in-time pack supply and curbing logistics risk for hospital networks and drug sponsors.

Key Report Takeaways

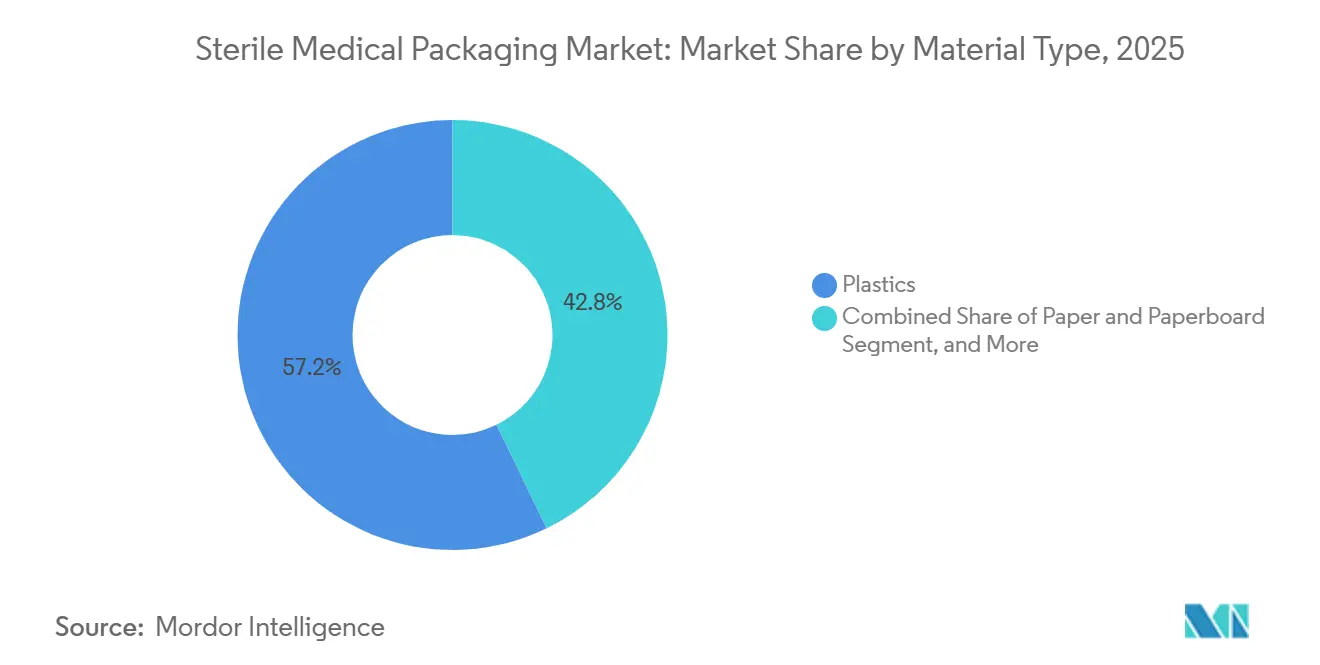

- By material type, plastics led the sterile medical packaging market with 57.23% share in 2025, while paper and paperboard are projected to expand at a 9.34% CAGR through 2031.

- By product type, pouches and bags commanded 29.37% revenue share in 2025, whereas pre-filled syringes and inhalers are forecast to record a 10.11% CAGR through 2031.

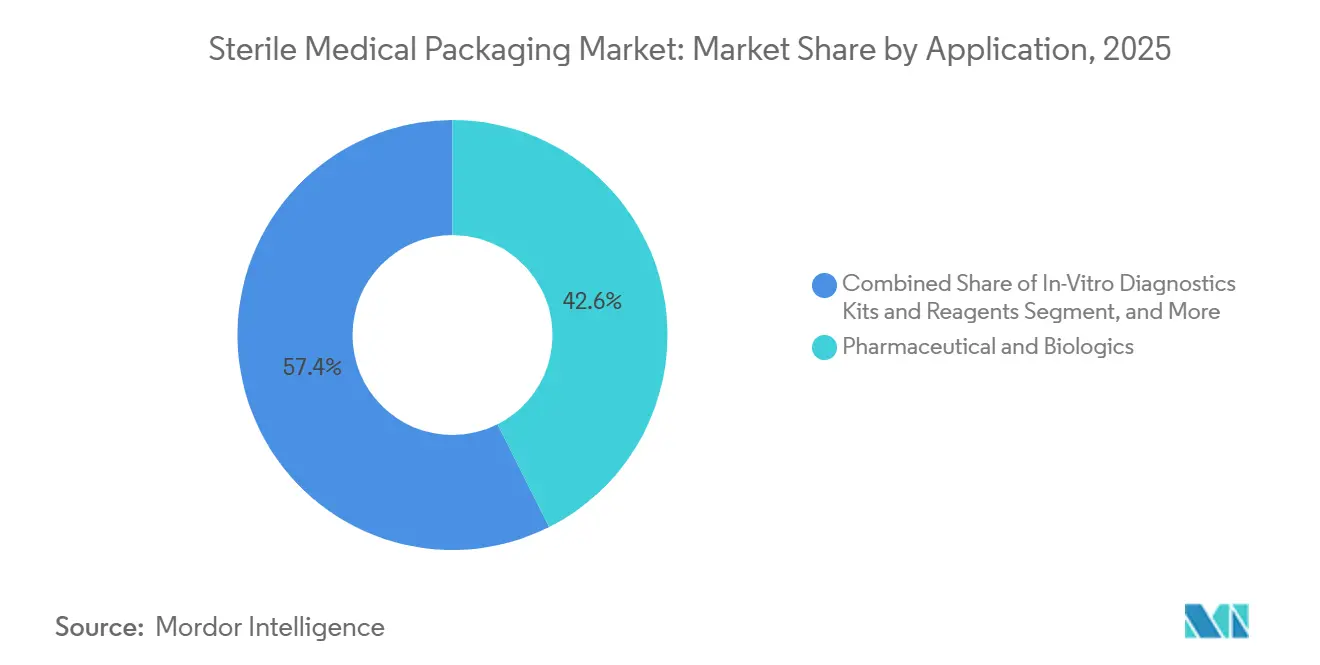

- By application, pharmaceuticals and biologics accounted for 42.58% of the sterile medical packaging market in 2025, yet in-vitro diagnostics kits and reagents are advancing at a 9.53% CAGR through 2031.

- By sterilization method, radiation accounted for 38.91% of revenue share in 2025, but low-temperature plasma and ozone processes are set to grow at a 9.57% CAGR through 2031.

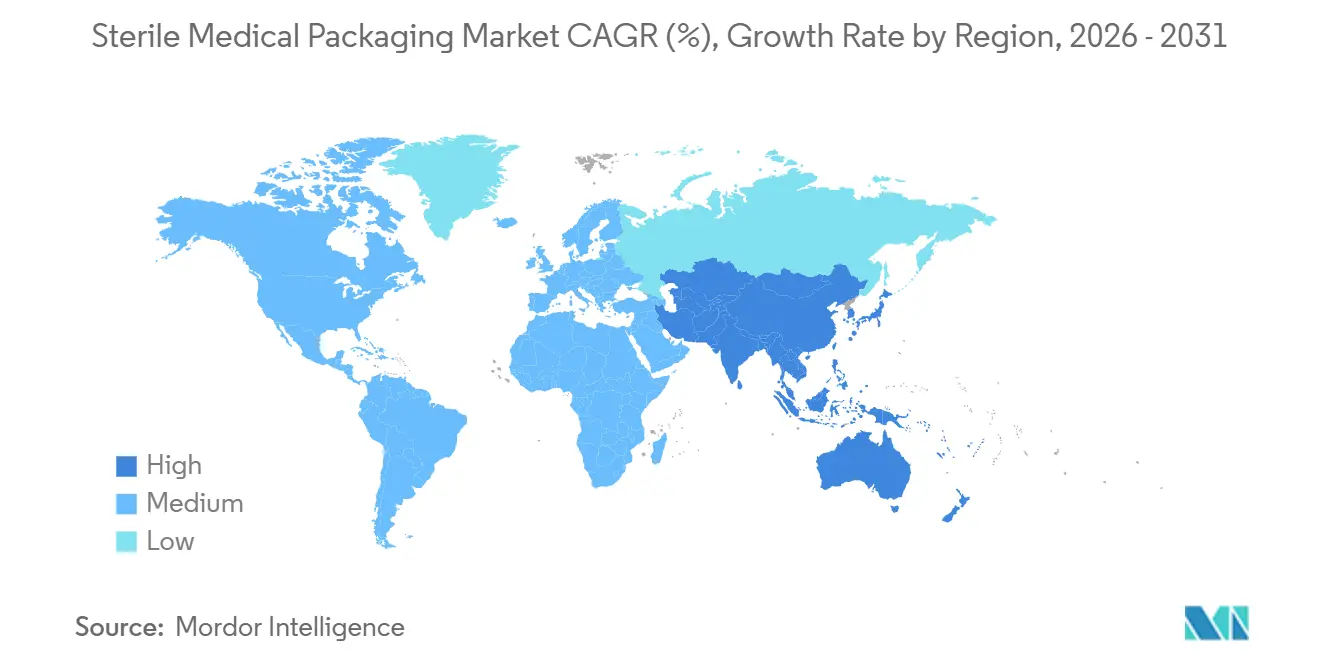

- By geography, North America dominated with 39.42% revenue share in 2025, and Asia-Pacific is predicted to be the fastest-growing region at 9.61% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sterile Medical Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Infection-Control Regulations and Standards | +2.1% | Global, with early enforcement in North America and Europe | Medium term (2-4 years) |

| Rise in Surgical Volumes and Chronic Disease Burden | +1.8% | Global, concentrated in Asia-Pacific and North America | Long term (≥ 4 years) |

| Boom in Biologics and Injectables Needing High-Integrity Packs | +1.6% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Rapid Material Innovations in High-Barrier Recyclable Plastics and Papers | +1.3% | Europe and North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Near-Shoring of Sterilization-as-a-Service Hubs near Pharma Clusters | +0.9% | North America and Europe | Short term (≤ 2 years) |

| AI-Driven Container-Closure Integrity Inspection and Digital Twins | +0.8% | North America and Europe, pilot deployments in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Infection-Control Regulations and Standards

Global agencies are closing loopholes in sterile‐barrier validation, forcing converters to adopt risk-based seal-strength testing and real-time leak detection that align with the latest ISO 11607 amendments.[1]International Organization for Standardization, “ISO 11607 Packaging For Terminally Sterilized Medical Devices,” iso.org The U.S. Quality Management System Regulation, effective February 2026, hard-codes ISO 13485:2016 practices into federal law and elevates documentation parity with Europe. Hospitals now demand packaging that simultaneously satisfies FDA 21 CFR 820 and European Union Medical Device Regulation 2017/745, a dual burden many mid-tier firms cannot meet. Upcoming ISO 11607-3, scheduled for late 2026, will require full process-development trace files, which favor vertically integrated suppliers with in-house microbiology labs. Collectively, these moves raise entry barriers and boost spending on inline inspection systems, cementing the growth outlook for incumbent leaders.

Rise in Surgical Volumes and Chronic Disease Burden

Worldwide surgical procedures climbed to 421 million in 2024, a 4.2% jump that mirrors aging demographics and broader insurance coverage in middle-income nations.[2]World Health Organization, “Global Health Estimates 2024,” who.int India’s National Health Mission recorded a 9% year-over-year increase in elective orthopedic cases during 2025, each needing roughly a dozen individually wrapped sterile components. China’s Healthy China 2030 plan funded 1,200 new surgical centers through 2025, all of which specify ISO-compliant sterile packs for every consumable. Minimally invasive and robotic techniques intensify packaging complexity because delicate tools require custom thermoform cavities and anti-static coatings that corrugated cartons cannot provide. Rising procedure counts, coupled with higher specification depth, are therefore amplifying both unit and value demand.

Boom in Biologics and Injectables Needing High-Integrity Packs

Biologic approvals hit 87 in 2025, up from 72 the prior year, and most favor pre-filled syringes or autoinjectors that demand airtight container-closure systems.[3]United States Food and Drug Administration, “Quality Management System Regulation,” fda.gov Novo Nordisk and Eli Lilly shipped more than 40 million GLP-1 autoinjectors in 2024 alone, underscoring the volume swing toward ready-to-use injectables. These formats rely on cyclic-olefin polymer barrels or Type I glass paired with fluoropolymer-coated stoppers that pass helium-leak and vacuum-decay tests, excluding commodity suppliers. The European Medicines Agency now requires extractables and leachables studies for every advanced-therapy medicinal product, stretching validation timelines by up to 9 months. While rigorous, the new standards lock in long-term supply contracts for converters able to meet the higher bar.

Rapid Material Innovations in High-Barrier Recyclable Plastics and Papers

Amcor’s AmPrima Plus mono-material polyethylene, launched in 2024, delivers sub-1 cc/m²/day oxygen transmission while remaining curbside recyclable. Dow’s 2025 RETAIN modifier lets converters blend up to 50% post-consumer recycled polyethylene without losing seal integrity, a breakthrough that helps pharmaceutical clients hit the European Union’s 30% recycled-content rule for 2030. Sonoco’s EnviroFlex Paper passes ISO 11607 peel tests and composts within 90 days, providing a fiber-based option for sterile pouches. A 2025 survey showed 62% of packaging managers now rate recyclability equal to microbial-barrier performance, a steep jump from 38% in 2023. These advances are accelerating substrate swaps, boosting order books for innovators that can balance sterility and sustainability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Resin Pricing and Supply-Chain Shocks | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Multi-Jurisdiction Regulatory Complexity and Compliance Costs | -0.9% | Global, concentrated in firms serving North America, Europe, and Asia-Pacific simultaneously | Medium term (2-4 years) |

| Legislative Push for Minimum Recycled Content Risking Pack Integrity | -0.7% | Europe and select North American states | Medium term (2-4 years) |

| Shortage of Ethylene-Oxide Capacity amid Emission Curbs | -0.6% | North America, spillover to Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Resin Pricing and Supply-Chain Shocks

U.S. polypropylene spot prices jumped 18% between January and April 2025 after unplanned cracker outages, then slid 12% by year-end, leaving converters whipsawed on raw-material costs. Medical-grade polyethylene traded at a 20% premium over commodity resin all year, while force majeure events in Europe stretched lead times for thermoform sheet from 4 to 9 weeks. To hedge, Tekni-Plex bought a 25% stake in a Texas polypropylene compounder, but smaller firms lack the balance sheets for such vertical plays. Currency swings further complicated procurement, as a weaker U.S. dollar made euro-denominated resin 8% more expensive. The net result is margin compression that could slow investment in new capacity.

Multi-Jurisdiction Regulatory Complexity and Compliance Costs

Converters that ship globally face overlapping rules from the FDA, European MDR, China’s NMPA, and Japan’s PMDA, each demanding unique documentation and post-market surveillance. A 2025 PwC study found that average annual compliance spend for mid-size firms was USD 2.3 million, or roughly 4-6% of revenue. The February 2026 U.S. QMSR transition alone is expected to consume up to 12,000 labor hours per packaging line for retraining, supplier audits, and procedure updates. Divergent sterilization standards add further drag; Europe accepts overkill validation while China insists on lot-by-lot bioburden tests, forcing dual pathways that stretch launches by several months. High overhead and timeline risk are therefore nudging smaller converters to exit cross-border markets, consolidating share with large incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastics Lead, But Paper Gains Ground

Plastics retained a 57.23% revenue share in 2025 as polypropylene and polyethylene underpinned thermoform trays and flexible pouches that tolerate gamma and e-beam sterilization. This dominance accounted for USD 38.5 billion of the sterile medical packaging market. Yet paper and paperboard, benefiting from EU recyclability mandates, are recording a 9.34% CAGR and are on course to lift their slice of the sterile medical packaging market by 2031. Rigid cyclic-olefin polymer formats are eroding glass's share in injectables, while bio-based polyethylene derived from sugarcane offers identical barrier performance and a 70% reduction in carbon, though supply remains limited.

Converters pivoting toward paper-poly laminates are winning pilot awards from European pharma groups aiming for 30% recycled content compliance. In contrast, PVC shrinkage continues as hospital systems blocklist phthalates, pressuring legacy IV-bag programs. Polymer price turbulence has accelerated testing of mono-material films that streamline recycling streams and insulate buyers from volatility in styrene and vinyl prices. Overall, substrate diversification supports resilient volume growth while achieving sustainability milestones.

By Product Type: Innovation Fuels Pre-Filled Syringe Expansion

Pouches and bags accounted for 29.37% of 2025 revenue, driven by high-throughput form-fill-seal operations for surgical wraps and diagnostics sachets. Pre-filled syringes and inhalers, however, are slated to climb at a 10.11% CAGR, adding more than USD 10 billion to the sterile medical packaging market size by 2031. Autoinjector demand for GLP-1 agonists illustrates the leap, with capacity additions across North Macedonia and the United States.

Blister packs and thermoform trays remain essential for unit-dose orals and orthopedic kits, respectively, while vial and ampoule programs innovate with thinner borosilicate glass to reduce breakage. Elastomeric stoppers coated with fluoropolymers are now table stakes for advanced therapies, elevating component ASPs. Edge-seal technologies that trim peel-force variance by 35% are differentiating tray suppliers and translating into fewer line stoppages for device OEMs.

By Application: IVD Momentum Outpaces Biologics Base

Pharmaceutical and biologics lines supplied 42.58% of 2025 demand, anchored by insulin analogs, anticoagulants, and monoclonal antibodies, which favor cold-chain pouches and glass syringes that deliver airtight container-closure integrity. Yet in vitro diagnostics kits are sprinting ahead at a 9.53% CAGR, driven by pharmacy-based respiratory panels and metabolic screens that require ambient-stable, single-use packs. This shift adds incremental volume without cannibalizing drug formats, enlarging the sterile medical packaging market.

Surgical-instrument programs continue to demonstrate significant growth and remain a robust segment within the mid-tier category. At the same time, medical implants are increasingly utilizing high-density polyethylene (HDPE) and cyclic-olefin copolymer trays, which are specifically designed to withstand gamma and ethylene oxide (EtO) sterilization processes. Furthermore, the impending full enforcement of Europe’s In Vitro Diagnostic (IVD) Regulation in 2025 introduces stringent requirements for serialization and traceability. These regulatory developments are compelling reagent brands to partner with converters that possess advanced capabilities in digital printing and data-matrix technology.

By Sterilization Method: Plasma And Ozone Capture Share From EtO

Radiation techniques captured 38.91% of revenue in 2025, but capacity limitations for cobalt-60 and growing concerns about EtO residues are steering buyers toward low-temperature plasma and ozone, forecast to rise 9.57% annually. Plasma's residue-free characteristics significantly reduce the required aeration time, thereby lowering the overall cycle costs. This efficiency also supports hospitals in achieving their sustainability objectives by promoting environmentally responsible practices.

Thermal autoclaves remain indispensable for metal instruments and glassware, though the risk of polymer deformation limits their scope. Hydrogen-peroxide vapor units, rolling out across European biologics hubs, further squeeze EtO volumes. Materials science is increasingly focusing on ensuring that polypropylene and polyethylene films preserve their clarity and maintain seal integrity when subjected to plasma exposure, thereby facilitating the development of new conversion processes.

Geography Analysis

North America accounted for 39.42% of the sterile medical packaging market share in 2025, underpinned by dense drug-manufacturing corridors in New Jersey, North Carolina, Massachusetts, and California, which now sit within 200 kilometers of at least one contract sterilization hub. Near-shoring has trimmed order-to-sterilize lead times from eight days to less than four, allowing hospital networks to shift toward just-in-time inventory models that cut holding costs by roughly 20%. Implementation of the 2026 Quality Management System Regulation is expected to retire sub-scale facilities that cannot finance ISO 13485 upgrades, concentrating the regional sterile medical packaging market size in fewer, larger plants. Resin volatility remains a headwind, but converters that backward-integrated into compounding have insulated margins and preserved capacity commitments. Midwestern states are also offering tax credits for recycled-content infrastructure, accelerating the adoption of mono-material polyethylene pouches that align with circular-economy targets.

Europe shows slower top-line expansion yet remains the proving ground for recyclable barrier substrates and low-residue sterilization methods. Germany’s EUR 1 billion (USD 1.07 billion) sovereignty fund is drawing clean-room builds to Brandenburg and Saxony, while Switzerland’s Basel-based hydrogen-peroxide hub now processes 10 million packs per quarter for adjacent Roche and Novartis campuses. The European Union Packaging and Packaging Waste Regulation’s 30% recycled-content requirement for 2030 is prompting pharma brands to pilot paper-poly lamination and 50% post-consumer resin films. France, Spain, and Italy remain net importers of high-integrity trays, but local sterilizers are scaling up plasma chambers to offset capped ethylene oxide quotas. Brexit-related divergence has added documentation layers for U.K. shipments, nudging some U.S. converters to serve continental customers from Irish plants instead.

Asia-Pacific is the growth engine, with the region forecast to expand at a 9.61% CAGR through 2031 as China and India pour incentive funds into domestic sterile capacity. China’s National Medical Products Administration cleared 42 pre-filled syringe lines between 2024-2025, and Healthy China 2030 investments financed 1,200 new surgical centers that specify ISO-compliant barrier packs. India’s INR 15 billion (USD 180 million) Production-Linked Incentive scheme is fast-tracking clean-room builds for catheter trays, diagnostic kits, and orthopedic implant wraps. Japan and South Korea are piloting AI-enabled seal-inspection sandboxes that shorten validation by two months, giving regional innovators a technology edge. Brazil, Mexico, the United Arab Emirates, and South Africa add incremental upside as revised sterile-packaging codes unlock access for multinational suppliers.

Competitive Landscape

The competitive field is moderately concentrated; the top five converters, Amcor, DuPont, West Pharmaceutical Services, Gerresheimer, and Sonoco, controlled roughly 40% of the sterile medical packaging market share in 2025, granting them scale-based purchasing leverage but still leaving room for niche specialists. Scale leaders are doubling down on vertical integration, with Amcor owning resin compounding and film extrusion lines that buffer against polypropylene price swings, while DuPont’s Luxembourg Tyvek expansion lifted capacity by 20% in late 2025. Innovation-centric firms such as Nelipak and Oliver channel 6-8% of sales into R and D, rolling out proprietary edge-seal and barrier-coating technologies that command double-digit price premiums. Patent activity is intense; West filed 14 U.S. patents on fluoropolymer-coated stoppers in 2024-2025, and Aptar secured IP for low-grip child-resistant closures. Regulatory tightening around ISO 13485 compliance post-2026 is expected to trim the long tail of sub-scale players, nudging the concentration ratio toward the 45% mark by decade’s end.

Technology partnerships are emerging as new moats. Körber Pharma’s AI vision platform, now live on 12 lines, cuts false rejects by 40% and has persuaded drug sponsors to sole-source with converters that embed the system. Siemens and Riverside Medical Packaging demonstrated a closed-loop quality pilot that adjusts sealing-jaw pressure in real time, achieving a 99.7% first-pass yield and reducing rework labor by half. Contract sterilizers such as Nelson Labs and STERIS are integrating upstream by offering pre-sterilized thermoform trays, a strategy that compresses the supply chain and puts pricing pressure on traditional converters. Financial buyers have noticed the stability of pharma-linked revenue streams; private-equity ownership now accounts for roughly 18% of global sterile-packaging capacity, up from 12% three years ago. Debt-funded roll-ups could accelerate if resin pricing stabilizes and free cash flow expands.

Sustainability credentials are fast becoming a tie-breaker in request-for-proposal cycles. Paper-poly hybrids that pass ISO 11607 peel tests and disintegrate in 90 days won early contracts with three European drug majors in 2025. Mono-material polyethylene solutions with 50% post-consumer resin landed multiyear supply agreements with two top-10 generic firms, contingent on achieving 98% line speed versus incumbent films. Firms lacking seasoned ESG reporting teams are already missing out on bids, as pharma customers assign 10-15% of tender scores to carbon metrics. Collectively, technology leadership, vertical integration, and verifiable sustainability performance are shaping the next wave of consolidation and defining the competitive chessboard through 2031.

Sterile Medical Packaging Industry Leaders

Amcor plc

DuPont de Nemours Inc.

Wipak Group

Steripack Group

Placon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The U.S. Food and Drug Administration Quality Management System Regulation took effect, mandating ISO 13485:2016 compliance for all device packaging suppliers.

- January 2026: Gerresheimer announced a EUR 120 million (USD 128 million) expansion in Skopje to add 150 million pre-filled syringe units, integrating AI vision systems and digital twins.

- December 2025: Amcor launched AmPrima Renew, a 50% PCR polyethylene pouch that meets ISO 11607 seal tests and EU recycled-content rules.

- November 2025: West Pharmaceutical Services added 25,000 square meters of cleanroom space in Waterford, Ireland, for NovaPure and Daikyo elastomer production, with commercial output slated for Q2 2026.

Global Sterile Medical Packaging Market Report Scope

The Sterile Medical Packaging Market Report is Segmented by Material Type (Plastics, Paper and Paperboard, Glass, Other Material Types), Product Type (Thermoform Trays, Sterile Bottles and Containers, Pouches and Bags, Blister Packs, Vials and Ampoules, Pre-Filled Syringes and Inhalers, Wraps and Lids, Sterile Closures and Stoppers), Application (Pharmaceutical and Biologics, Surgical and Medical Instruments, In-Vitro Diagnostics Kits and Reagents, Medical Implants and Disposables, Other Applications), Sterilization Method (Chemical, Radiation, Thermal, Low-Temperature Plasma and Ozone, Aseptic/Filtration-Based), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Plastics | Polypropylene |

| Polyethylene | |

| Polyethylene-Terephthalate Glycol | |

| Polyvinyl Chloride | |

| Polystyrene | |

| Other Plastics | |

| Paper and Paperboard | |

| Glass | |

| Other Material Types |

| Thermoform Trays |

| Sterile Bottles and Containers |

| Pouches and Bags |

| Blister Packs |

| Vials and Ampoules |

| Pre-Filled Syringes and Inhalers |

| Wraps and Lids |

| Sterile Closures and Stoppers |

| Pharmaceutical and Biologics |

| Surgical and Medical Instruments |

| In-Vitro Diagnostics Kits and Reagents |

| Medical Implants and Disposables |

| Other Applications |

| Chemical |

| Radiation |

| Thermal |

| Low-Temperature Plasma and Ozone |

| Aseptic/Filtration-Based |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Plastics | Polypropylene | |

| Polyethylene | |||

| Polyethylene-Terephthalate Glycol | |||

| Polyvinyl Chloride | |||

| Polystyrene | |||

| Other Plastics | |||

| Paper and Paperboard | |||

| Glass | |||

| Other Material Types | |||

| By Product Type | Thermoform Trays | ||

| Sterile Bottles and Containers | |||

| Pouches and Bags | |||

| Blister Packs | |||

| Vials and Ampoules | |||

| Pre-Filled Syringes and Inhalers | |||

| Wraps and Lids | |||

| Sterile Closures and Stoppers | |||

| By Application | Pharmaceutical and Biologics | ||

| Surgical and Medical Instruments | |||

| In-Vitro Diagnostics Kits and Reagents | |||

| Medical Implants and Disposables | |||

| Other Applications | |||

| By Sterilization Method | Chemical | ||

| Radiation | |||

| Thermal | |||

| Low-Temperature Plasma and Ozone | |||

| Aseptic/Filtration-Based | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast value of the sterile medical packaging market by 2031?

The sterile medical packaging market is projected to reach USD 101.08 billion by 2031.

Which material segment is growing fastest?

Paper and paperboard packaging is expanding at a 9.34% CAGR through 2031 as sustainability mandates tighten.

Why are pre-filled syringes gaining share?

Rising adoption of GLP-1 agonists and biologics favors ready-to-use injectables that improve dosing accuracy and patient adherence.

How will the new U.S. regulations affect suppliers?

The February 2026 Quality Management System Regulation, aligned with ISO 13485:2016, compels converters to upgrade quality systems or exit the market.

Which region is expected to grow most quickly?

Asia-Pacific is forecast to post a 9.61% CAGR through 2031, buoyed by Chinese and Indian manufacturing incentives.

What sterilization methods are displacing ethylene oxide?

Low-temperature plasma, ozone, and hydrogen-peroxide vapor processes are gaining traction because they avoid EtO residue and face fewer emission limits.

Page last updated on: