North America Medical Devices Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

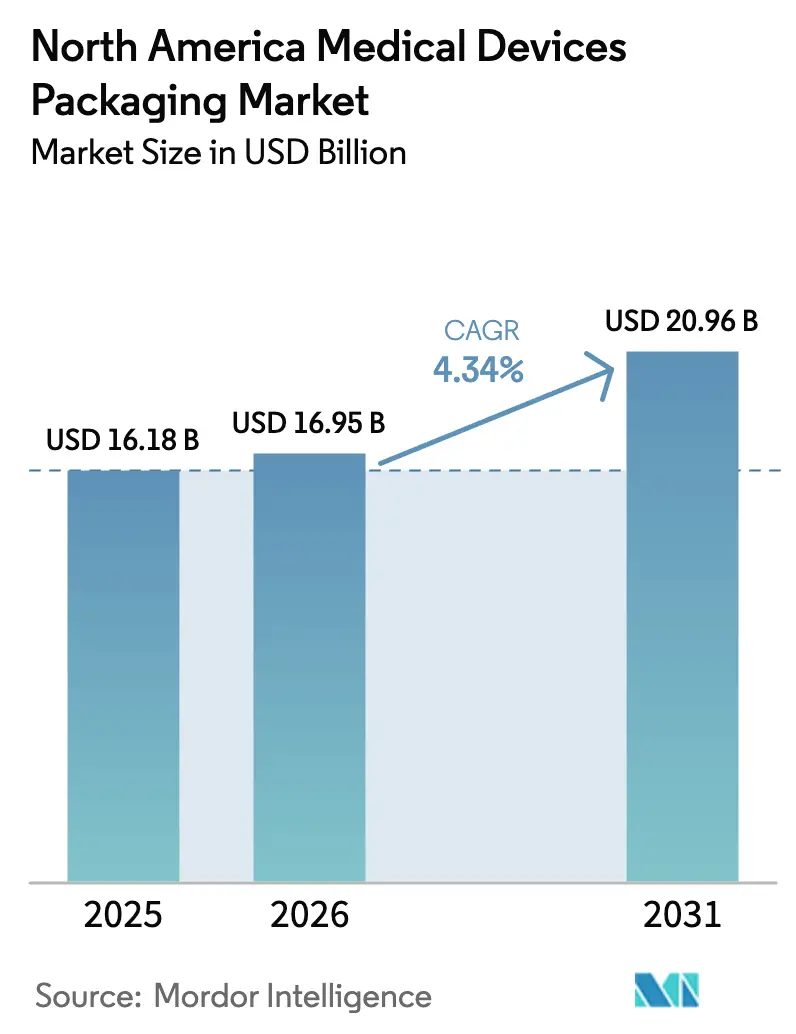

| Base Year Market Size (2025) | USD 16.18 Billion |

| Market Size (2026) | USD 16.95 Billion |

| Market Size (2031) | USD 20.96 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

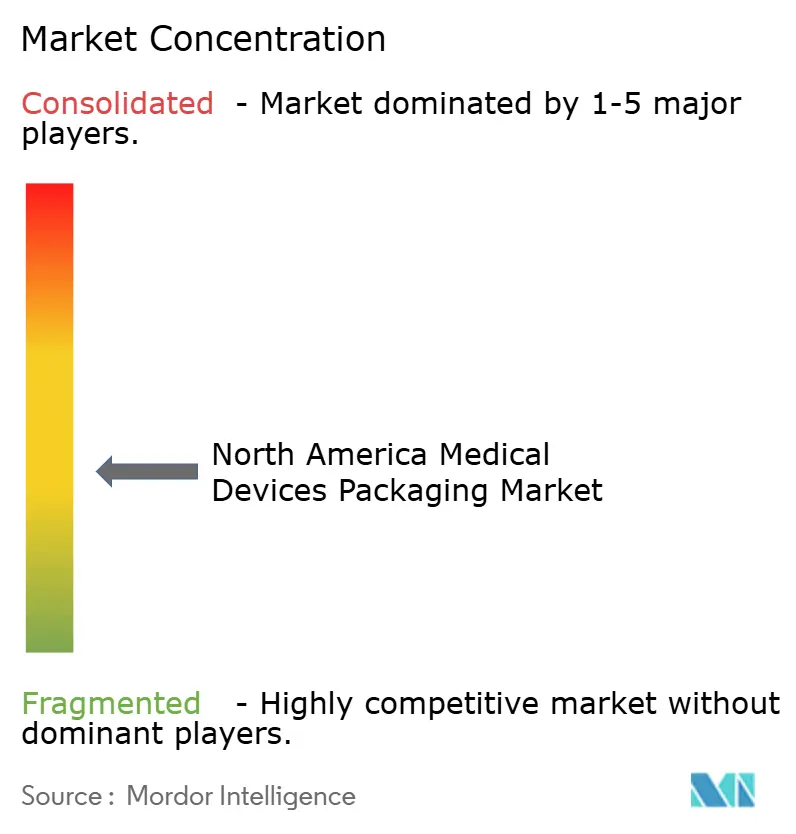

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Medical Devices Packaging Market Analysis by Mordor Intelligence

The North America Medical Devices Packaging Market size is expected to grow from USD 16.19 billion in 2025 to USD 16.95 billion in 2026 and is forecast to reach USD 20.96 billion by 2031 at 4.34% CAGR over 2026-2031.

Several forces underpin this trajectory: hospitals are restocking elective-procedure inventories, ambulatory surgery centers are embracing single-use instrument trays, and home-care operators are scaling direct-to-consumer diagnostic kits. Sterile formats retain a wide lead, yet non-sterile packs for wearable monitors are rising as tele-health reimbursement codes mature. Material dynamics are equally fluid, with plastics maintaining dominance but bio-based polymers gaining momentum as procurement teams embed carbon-footprint clauses into tender documents. Regulatory convergence around the U.S. Food and Drug Administration’s Quality Management System Regulation and the Environmental Protection Agency’s ethylene-oxide emission standards is reshaping capital allocation, favoring converters with in-house validation laboratories and digital traceability systems that can absorb higher compliance costs. As a result, price discipline has tightened, and strategic investments now skew toward securing resin supply, expanding clean-room capacity, and integrating smart sensors to safeguard cold-chain biologics.

Key Report Takeaways

- By product type, sterile packaging held 63.35% of the North America medical devices packaging market share in 2025, while non-sterile formats are the fastest-growing segment at a 4.93% CAGR to 2031.

- By packaging type, pouches and bags led with 37.21% revenue share in 2025, and bio-based polymer-based formats are set to expand at a 5.26% CAGR through 2031.

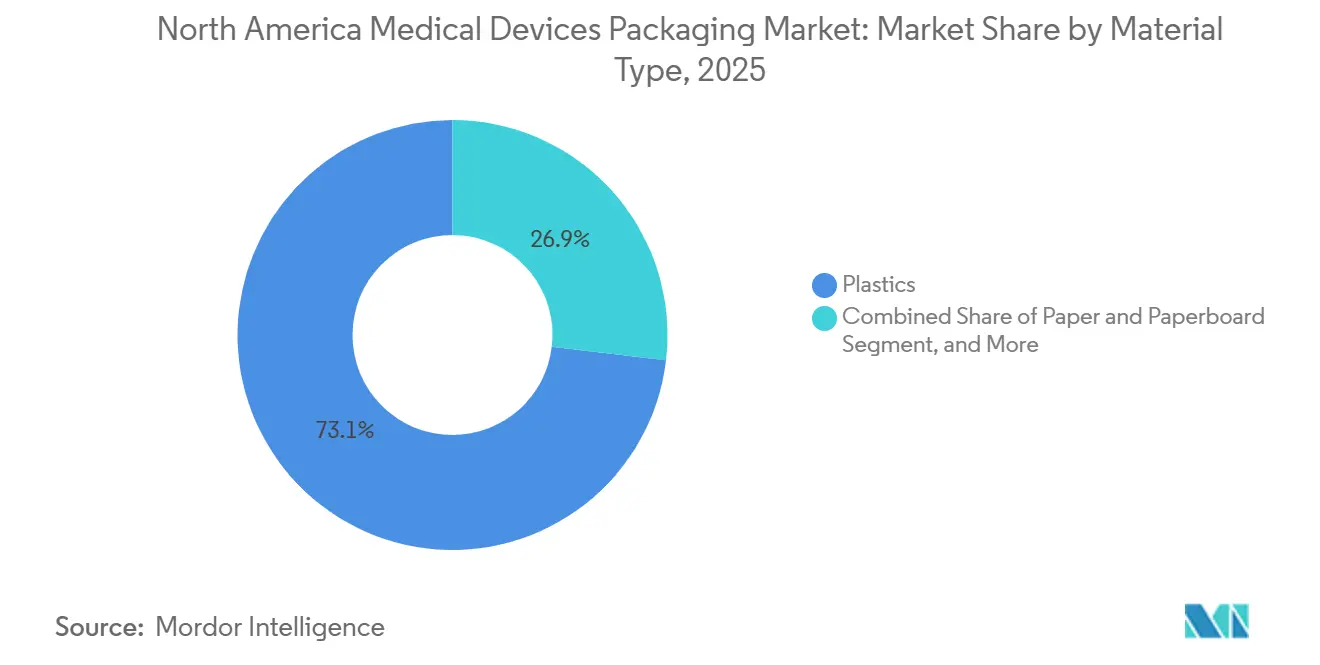

- By material type, plastics accounted for 73.12% of the North America medical device packaging market in 2025, whereas bio-based polymers posted the fastest growth at a 5.11% CAGR.

- By application, surgical and medical instruments commanded a 33.94% share in 2025, while wearable and home-care devices are advancing at a 5.64% CAGR to 2031.

- By geography, the United States dominated with 81.46% of regional spending in 2025, and Mexico is forecast to grow at a 4.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Medical Devices Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elective-Surgery Rebound Fuels Higher Procedure Volumes | +0.8% | United States and Canada, concentrated in ambulatory surgery centers | Short term (≤ 2 years) |

| Rapid Shift Toward Single-Use and Minimally-Invasive Devices | +1.1% | United States, expanding into Mexico as nearshoring scales | Medium term (2-4 years) |

| Growth in Home-Based Care and Tele-Health Kits | +0.9% | United States and Canada, rural and underserved urban corridors | Medium term (2-4 years) |

| FDA UDI and Traceability Mandates Tighten Sterility Demands | +0.6% | United States, with spillover compliance in Canada and Mexico | Long term (≥ 4 years) |

| Rise of Hospital Sustainability Tenders for Low-Carbon Packs | +0.5% | United States and Canada, led by integrated delivery networks | Long term (≥ 4 years) |

| Smart-Sensor Packs Enabling Cold-Chain Compliance | +0.4% | United States, concentrated in biologics logistics streams | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elective-Surgery Rebound Fuels Higher Procedure Volumes

Outpatient surgical volumes in the United States rose 6.2% year over year during 2025 as elective cases exceeded pre-pandemic baselines. Ambulatory centers prefer pre-sterilized, peel-open trays that remove reprocessing labor and cut infection risk. Orthopedic, ophthalmic, and cardiovascular specialties use high-barrier Tyvek pouches and segmented thermoformed trays to protect delicate instruments during transit. The Centers for Medicare & Medicaid Services expanded reimbursement coverage for 11 additional ambulatory procedures in January 2025, locking in visibility into demand for device makers.[1]Centers for Medicare and Medicaid Services, “CY 2025 Medicare Hospital Outpatient Prospective Payment System Final Rule,” cms.gov Suppliers are now pre-booking resin and lidding film 6 months in advance to avoid spot-market spikes that could disrupt tray production schedules. Logistics partners have responded by adding sterile handling zones inside regional distribution centers, keeping cycle times in line with tight surgical calendars.

Rapid Shift Toward Single-Use and Minimally-Invasive Devices

Minimally invasive instruments accounted for 62% of FDA 510(k) clearances in 2025, up 9 points from 2023. Custom trays must accommodate articulated jaws, flexible shafts, and multi-lumen catheters without allowing component migration. Intuitive Surgical shipped 379,000 single-use tools for its robotics platform in 2025, each wrapped in an individual sterile pouch that includes tamper-evident seals.[2]Source: Intuitive Surgical, “Fourth Quarter Earnings 2025,” isrg.intuitive.com Mexico’s Class II assembly lines expanded 18% the same year, feeding north-bound demand for validated pouches that meet ISO 11607 and FDA import rules. Converters are installing five-axis thermoformers that switch from deep-draw trays to flat pouches in under an hour, improving asset utilization. OEMs, meanwhile, are standardizing tray footprints across product families to lower tooling costs and simplify hospital stocking.

Growth in Home-Based Care and Tele-Health Kits

Remote patient monitoring enrolled 12.3 million Medicare beneficiaries in 2025, 34% above the prior year, as new reimbursement codes encouraged wider adoption. Abbott shipped 8.7 million FreeStyle Libre glucose monitors, each in a shock-resistant clamshell with QR-coded setup links. E-commerce parcel networks impose ASTM drop and compression tests that exceed hospital pallet norms, driving converters to integrate molded pulp inserts and corner crush stiffeners. Graphic design now highlights intuitive opening cues and step-by-step pictograms to reduce helpline calls. Returns management is emerging as a new packaging criterion, with resealable mailers enabling safe reverse logistics for sensor recycling. The cost per kit remains 30% to 40% below that of sterile hospital packs, supporting high-volume subscription models.

FDA UDI and Traceability Mandates Tighten Sterility Demands

Full UDI enforcement for Class I devices in September 2024 forced converters to add high-resolution inkjet coders and in-line barcode cameras. Each sterile pouch now carries serialized data tied to sterilization batch, resin lot, and distribution node for instant recall execution. West Pharmaceutical Services pegged the per-pouch serialization cost at USD 0.12 in 2025, after accounting for software fees and reduced line speed. Smaller converters without enterprise planning tools face steep onboarding costs, accelerating customer migration to vertically integrated suppliers. Hospitals leverage UDI data to automatically audit expiration dates, reducing shelf-stock write-offs. The next phase involves integrating NFC chips so clinicians can confirm sterility status with a smartphone tap, a feature already in pilot on high-value biologics cartons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Geographic Relevance |

|---|---|---|---|

| Escalating Cost of High-Barrier Medical-Grade Resins | -0.7% | United States and Canada, with pass-through pressure on Mexico-based converters | Short term (≤ 2 years) |

| Volatility in Ethylene-Oxide Sterilization Capacity | -0.5% | United States, centered in Illinois, California, and Georgia hubs | Medium term (2-4 years) |

| OEM Qualification Delays for Novel Sustainable Materials | -0.3% | United States and Canada, affecting sustainable procurement pilots | Long term (≥ 4 years) |

| Capital Intensity of ISO 11607 Validation Testing | -0.2% | United States, constraining small and mid-sized converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cost of High-Barrier Medical-Grade Resins

Medical-grade polyethylene and polypropylene traded at USD 1.85 to USD 2.10 per pound in late 2025, up 14% from 2024, owing to Gulf Coast cracker outages, bloomberg.com. High-barrier films with ethylene-vinyl alcohol add another 25% premium, squeezing converter margins. Amcor reported a 120-basis-point erosion in its 2025 medical-packaging segment, even after pass-through clauses that lag spot prices by up to 90 days. Smaller firms lacking hedging contracts are pivoting toward industrial markets or selling sterile lines altogether. Some OEMs are trialing thinner-gauge films to reduce resin mass per pack, but seal-strength validation often offsets the savings. In parallel, bio-based resin suppliers are negotiating volume-linked discounts to narrow the price gap and win early adopters.

Volatility in Ethylene-Oxide Sterilization Capacity

EPA emission rules finalized in April 2024 led several EtO plants to shut down for retrofits, stretching contract sterilization lead times from eight to fourteen weeks by mid-2025.[3]U.S. Environmental Protection Agency, “Ethylene Oxide Emissions Standards for Sterilization Facilities,” epa.gov Sterigenics spent USD 38 million on abatement gear and raised fees by 8% to 12% in January 2025. Device makers exploring gamma or e-beam alternatives face a 9- to 12-month revalidation under FDA guidance, dampening quick migration. Some converters are partnering with logistics firms to pre-book EtO slots and guarantee door-to-door cycle times. Regional health systems have begun stocking two months of safety inventory to avoid surgical delays, tying up working capital. Over the long term, new EtO chambers slated for Texas and Indiana could restore capacity, but permitting hurdles suggest relief will not arrive before 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sterile Formats Anchor Revenue, Non-Sterile Gains Momentum

Sterile packaging captured 63.35% of the North America medical devices packaging market share in 2025, reflecting hospital reliance on validated microbial barriers for implants, surgical tools, and diagnostic kits. The segment is expanding, although at a measured 4.34% pace, as validation costs rise under harmonized ISO 13485 rules. Non-sterile formats are scaling faster at a 4.93% CAGR, fueled by tele-health and home-care distribution that bypasses central sterilization. The introduction of remote patient monitoring reimbursement has already redirected substantial unit volumes into parcel channels. Sterile players are responding by shortening validation cycles with in-house labs, yet the cost differential remains significant, positioning non-sterile packs as the incremental growth engine for the North America medical devices packaging market.

Non-sterile proliferation does not spell contraction for sterile lines; rather, the internal mix is shifting. Single-use trays for minimally invasive platforms are advancing, while reusable device packs taper as infection-control committees push disposables. Converters that master both formats hedge cyclical swings, yet those concentrated solely in sterile production may face utilization pressure. The North America medical devices packaging market will therefore reward flexible operators capable of running high-speed pouching for consumer devices alongside ISO-class clean-rooms for surgical sets.

By Packaging Type: Pouches Remain Dominant, Bio-Based Polymers Disrupt Mix

Pouches and bags accounted for 37.21% of 2025 revenue, underscoring their efficiency, compatibility with automation, and wide sterilization window. Trays and clamshells serve complex instruments, while wraps, cartons, and specialty lids round out application-specific needs. Hospitals now evaluate carbon metrics in tenders, prompting converters to roll out recycled-content pouches. Amcor launched a 40% recycled polyethylene line in January 2025, winning a multi-year contract with a major integrated delivery network. Bio-based innovations flow fastest into pouches, which tolerate resin tweaks without jeopardizing seal performance.

Rigid trays still matter for articulated robotic tools, and investments such as Amcor’s USD 45 million Wisconsin expansion added 30% thermoforming capacity in 2024. Nonetheless, the improved environmental profile of flexible packs, plus freight savings from lower dimensional weight, positions pouches to capture the bulk of incremental gains within the North America medical devices packaging market during the forecast period.

By Material Type: Plastics Lead, Bio-Based Polymers Gain Traction

Plastics delivered 73.12% of value in 2025 thanks to proven biocompatibility, puncture resistance, and broad sterilization windows. Paper and paperboard add structural rigidity and printability for secondary packs, while metalized laminates secure moisture-sensitive diagnostics. Bio-based polymers, though only a niche, are rising at 5.11% and are central to hospital sustainability pledges. Group purchasing organizations that represent 4,200 facilities now allocate up to 15% of bid scoring to carbon impact, forcing converters to pilot polylactic acid and bio-polyethylene blends.[4]Healthcare Purchasing News, “GPOs Embed Sustainability Criteria in Medical Device Packaging Tenders,” hpnonline.com

Cost gaps persist. Bio-resins remain 40% to 60% above petrochemical equivalents, and ISO 10993 testing can add 18 months to commercialization schedules. Even so, DuPont’s 30% recycled-content Tyvek gained FDA acceptance in August 2025, proving that sustainable formulations can clear regulatory bars when major OEMs underwrite qualification costs. As economies of scale improve, bio-based penetration will progressively chip away at plastics’ hegemony in the North America medical devices packaging market.

By Application: Surgical Instruments Lead, Wearables Surge

Surgical and medical instruments accounted for 33.94% of demand in 2025, an unsurprising outcome given the volume of procedures and strict sterility requirements. These packs often combine rigid trays, peelable lids, and breathable Tyvek to withstand vacuum steam or ethylene oxide. Wearable and home-care devices, however, form the fastest-rising cohort with a 5.64% CAGR to 2031. Direct-to-consumer shipment, simplified opening features, and vivid graphic design frame their requirements, differentiating them sharply from hospital-bound trays. Abbott’s FreeStyle Libre roll-out illustrates the scale shift as millions of clamshells move through parcel networks each quarter.

Diagnostic substances depend on high-barrier films with desiccant inserts, while surgical appliances and supplies gravitate toward bulk wraps that facilitate central sterile processing. Dental and ophthalmic goods represent specialized niches demanding ultra-clean environments. Over the forecast horizon, remote monitoring incentives and outcomes-based reimbursement models will continue to lift wearable volumes, reinforcing their outsized influence on the evolution of the North America medical devices packaging market.

Geography Analysis

The United States generated 81.46% of regional revenue in 2025, supported by a USD 186 billion domestic device industry, 6,200 hospitals, and 5,900 ambulatory surgery centers that collectively pull vast quantities of validated pouches, trays, and cartons. FDA oversight, ISO 11607 adherence, and UDI serialization protocols converge to reward scale and technical depth, which explains why converters with in-house validation laboratories capture a disproportionate share. Regulatory alignment between the FDA’s February 2025 Quality Management System Regulation and ISO 13485 has tightened biocompatibility documentation, raising validation spend yet simultaneously driving innovation such as NFC-enabled Seal-ID labels rolled out by West Pharmaceutical Services.

Canada contributes a smaller, mid-single-digit share of the North America medical devices packaging market. Cross-border supply is facilitated by the Medical Device Single Audit Program, which spares converters from duplicate inspections. Packaging demand clusters around Ontario and Quebec, where domestic device assembly and distribution hubs reside. Population density and centralized procurement dampen per-capita consumption compared with the United States, yet steady investment in outpatient clinics maintains a stable baseline for converters serving Canadian clients.

Mexico is the breakout growth story, advancing at a 4.93% CAGR through 2031. Nearshoring has spurred multinational OEMs such as Medtronic and Boston Scientific to expand along the Baja California and Chihuahua corridors, stimulating local demand for ISO-11607-compliant pouches and trays. Still, most Mexican converters lack ISO 13485 certification, forcing OEMs to import pre-validated packs from the United States, which limits domestic value capture. The federal tax credit covering 30% of capital equipment purchased for clean-room upgrades, introduced in 2025, is set to narrow this capability gap. As certification levels climb, Mexico’s share of the North America medical devices packaging market should edge upward without displacing U.S. leadership.

Competitive Landscape

In North America, the top five suppliers, Amcor, Sonoco Products, DuPont, 3M, and West Pharmaceutical Services, command a notable 40% to 45% share of the installed capacity, indicating a moderate market concentration. These industry leaders are increasingly leaning towards strategies like vertical integration and capacity debottlenecking. For instance, Amcor's recent USD 45 million thermoforming expansion in Wisconsin not only boosted tray throughput by 30% but also introduced co-located clean rooms, significantly shortening validation cycles from 16 weeks to a mere 10. Meanwhile, in March 2025, West Pharmaceutical Services made headlines with its acquisition of a specialty film converter in Ontario, a move that not only secured a high-barrier laminate supply but also slashed lead times to 8 weeks.

Material innovation is becoming a pivotal factor in shaping industry rivalries. DuPont's collaboration with Olympus and Cook Medical on recycled-content Tyvek underscores the growing importance of sustainable substrates, which not only command price premiums but also align with hospital sustainability initiatives. On another front, 3M is making waves in the smart-sensor domain, introducing passive RFID indicators. These indicators ensure cold-chain integrity without compromising sterile barriers and are in line with the draft FDA guidance for cell therapies. While smaller converters are finding their footing by specializing in custom geometries, rapid prototyping, and biodegradable films, they're grappling with capital challenges, especially concerning ISO 11607 and UDI compliance, which are putting pressure on their margins.

These evolving dynamics suggest a landscape where larger, tech-savvy firms are poised to strengthen their foothold in the North American medical devices packaging market. In contrast, specialized challengers are carving out their space, emphasizing agility and eco-design to stay competitive.

North America Medical Devices Packaging Industry Leaders

Amcor plc

DuPont de Nemours, Inc.

Sonoco Products Co.

3M Company

West Pharmaceutical Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Amcor launched a 40% recycled-content polyethylene pouch validated for non-sterile wound-care dressings, winning a three-year supply contract with a major integrated delivery network committed to halving landfill waste by 2027.

- November 2025: West Pharmaceutical Services completed a USD 52 million clean-room expansion in Kinston, North Carolina, adding 120,000 square feet of ISO Class 7 space for high-barrier films used in pre-filled syringes and vials.

- September 2025: DuPont began commercial sales of Tyvek structures containing 30% post-consumer recycled content after FDA master-file acceptance, targeting hospitals with strict sustainability scorecards.

- July 2025: Sonoco Products acquired a thermoforming converter in Guadalajara, Mexico, adding 15 million trays of annual capacity and onboarding ISO 13485 clean rooms.

North America Medical Devices Packaging Market Report Scope

The North America Medical Devices Packaging Market Report is Segmented by Product Type (Sterile Packaging, Non-Sterile Packaging), Packaging Type (Pouches and Bags, Trays and Clamshells, Boxes and Cartons, Wraps and Films, Other Packaging Type), Material Type (Plastics, Paper and Paperboard, Metal, Bio-Based Polymers), Application (Diagnostic Substances, Surgical and Medical Instruments, Surgical Appliances and Supplies, Dental Equipment and Supplies, Ophthalmic Goods, Wearable and Home-Care Devices, Other Applications), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Sterile Packaging |

| Non-Sterile Packaging |

| Pouches and Bags |

| Trays and Clamshells |

| Boxes and Cartons |

| Wraps and Films |

| Other Packaging Type |

| Plastics |

| Paper and Paperboard |

| Metal |

| Bio-Based Polymers |

| Diagnostic Substances |

| Surgical and Medical Instruments |

| Surgical Appliances and Supplies |

| Dental Equipment and Supplies |

| Ophthalmic Goods |

| Wearable and Home-Care Devices |

| Other Applications |

| United States |

| Canada |

| Mexico |

| By Product Type | Sterile Packaging |

| Non-Sterile Packaging | |

| By Packaging Type | Pouches and Bags |

| Trays and Clamshells | |

| Boxes and Cartons | |

| Wraps and Films | |

| Other Packaging Type | |

| By Material Type | Plastics |

| Paper and Paperboard | |

| Metal | |

| Bio-Based Polymers | |

| By Application | Diagnostic Substances |

| Surgical and Medical Instruments | |

| Surgical Appliances and Supplies | |

| Dental Equipment and Supplies | |

| Ophthalmic Goods | |

| Wearable and Home-Care Devices | |

| Other Applications | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

Question

Answer

How large will packaging demand be for medical devices in North America by 2031?

The North America medical devices packaging market size is projected to reach USD 20.96 billion by 2031, with a 4.34% CAGR.

Which product format is growing fastest across the region?

Non-sterile packs, primarily serving home-care and tele-health devices, are forecast to grow at 4.93% per year through 2031.

Why are bio-based polymers gaining attention among hospitals?

Group purchasing organizations are now embedding carbon metrics into tenders, making bio-based polyethylene and polylactic acid more attractive despite current price premiums.

What impact do ethylene oxide regulations have on packaging lead times?

EPA emission rules prompted sterilization retrofits that lengthened EtO lead times to as much as fourteen weeks in 2025, pressuring device inventory models.

Which country offers the highest growth potential within North America?

Mexico is projected to advance at a 4.93% CAGR to 2031 as nearshoring expands Class II device assembly and stimulates local packaging capacity.

How concentrated is the supplier landscape?

The top five vendors hold roughly 40% to 45% of capacity, indicating moderate concentration and ongoing room for specialized challengers.

Page last updated on: