Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

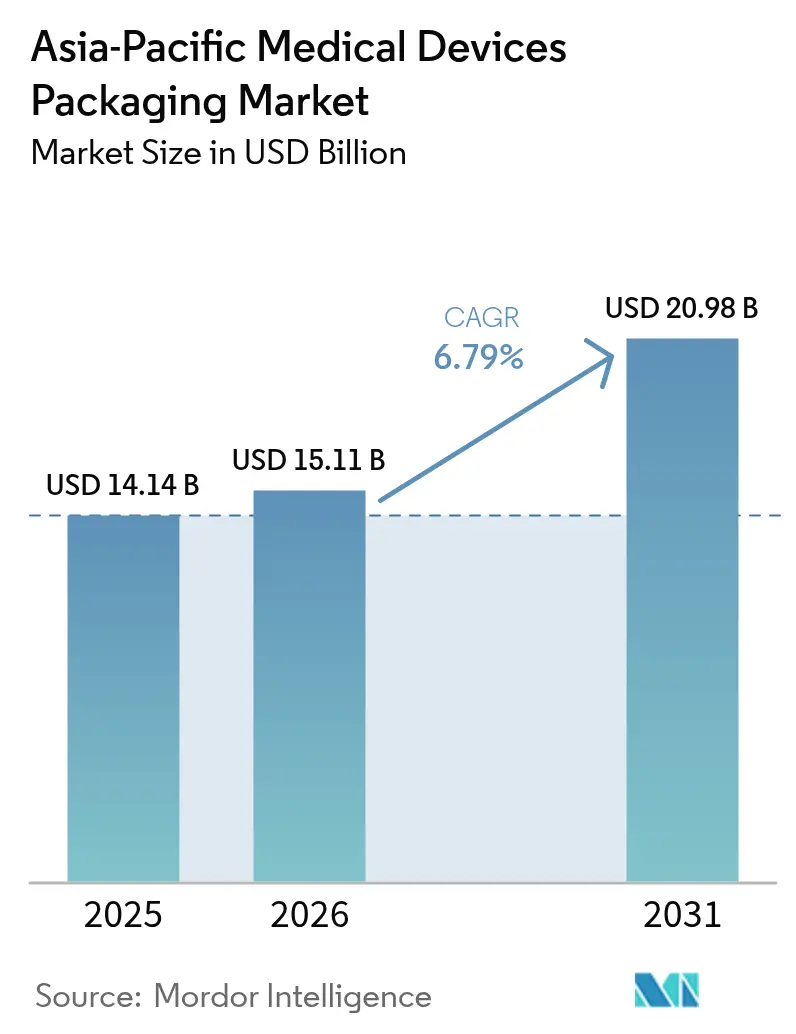

| Base Year Market Size (2025) | USD 14.14 Billion |

| Market Size (2026) | USD 15.11 Billion |

| Market Size (2031) | USD 20.98 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

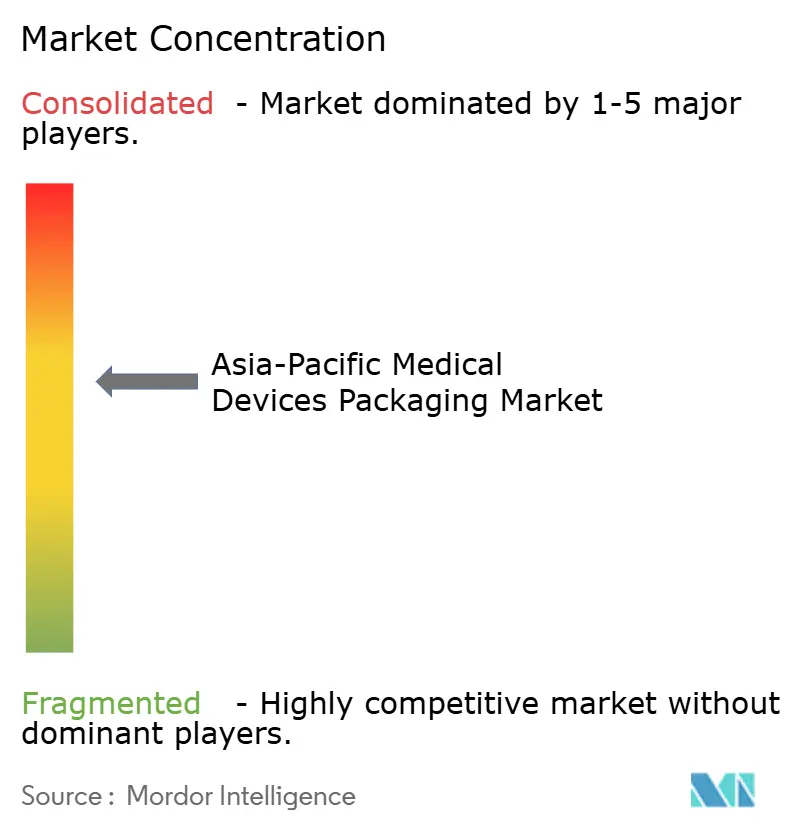

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Medical Devices Packaging Market Analysis by Mordor Intelligence

The Asia-Pacific medical devices packaging market size in 2026 is estimated at USD 15.11 billion, growing from 2025 value of USD 14.14 billion with 2031 projections showing USD 20.98 billion, growing at 6.79% CAGR over 2026-2031. Factory relocation toward Southeast Asia and India, demographic shifts that favor home-based care, and stricter sterility rules are reshaping sourcing patterns. Multinational device makers now co-locate packaging lines next to assembly plants so they can cut freight bills, compress lead times, and gain tariff relief. Hospitals have started specifying validated sterile-barrier systems as a condition of tender eligibility, narrowing supplier lists to converters with ISO 11607 credentials. At the same time, procurement teams award bonus points for circular-economy attributes such as bio-based plastics, recycled board, and tamper-evident outer cartons, encouraging converters to blend bio-resins or adopt mono-material laminates that simplify disposal.

Key Report Takeaways

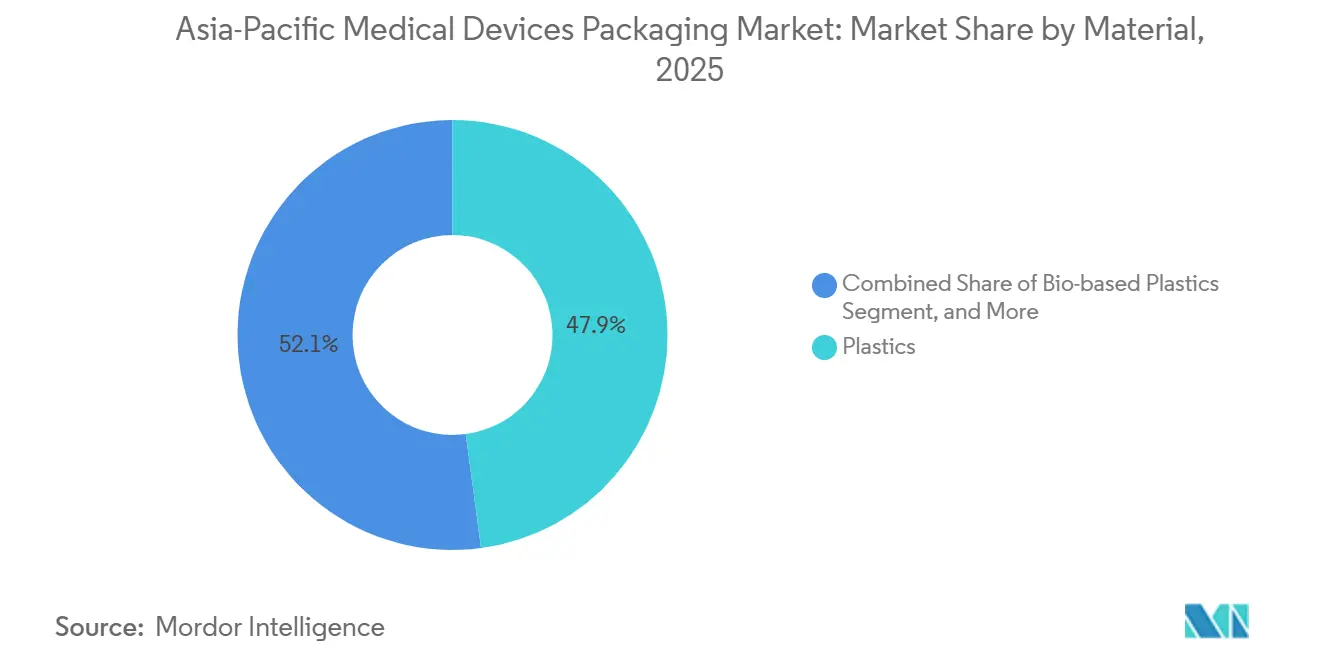

- By material, plastics led with a 47.88% revenue share in 2025, while bio-based plastics are set to grow at a 7.74% CAGR through 2031.

- By product type, pouches and bags accounted for 31.36% of the Asia-Pacific medical devices packaging market share in 2025, whereas blister packs is forecast to post a 7.72% CAGR by 2031.

- By application, sterile packaging accounted for 56.32% of the Asia-Pacific medical devices packaging market in 2025, and active/smart packaging is advancing at a 7.29% CAGR through 2031.

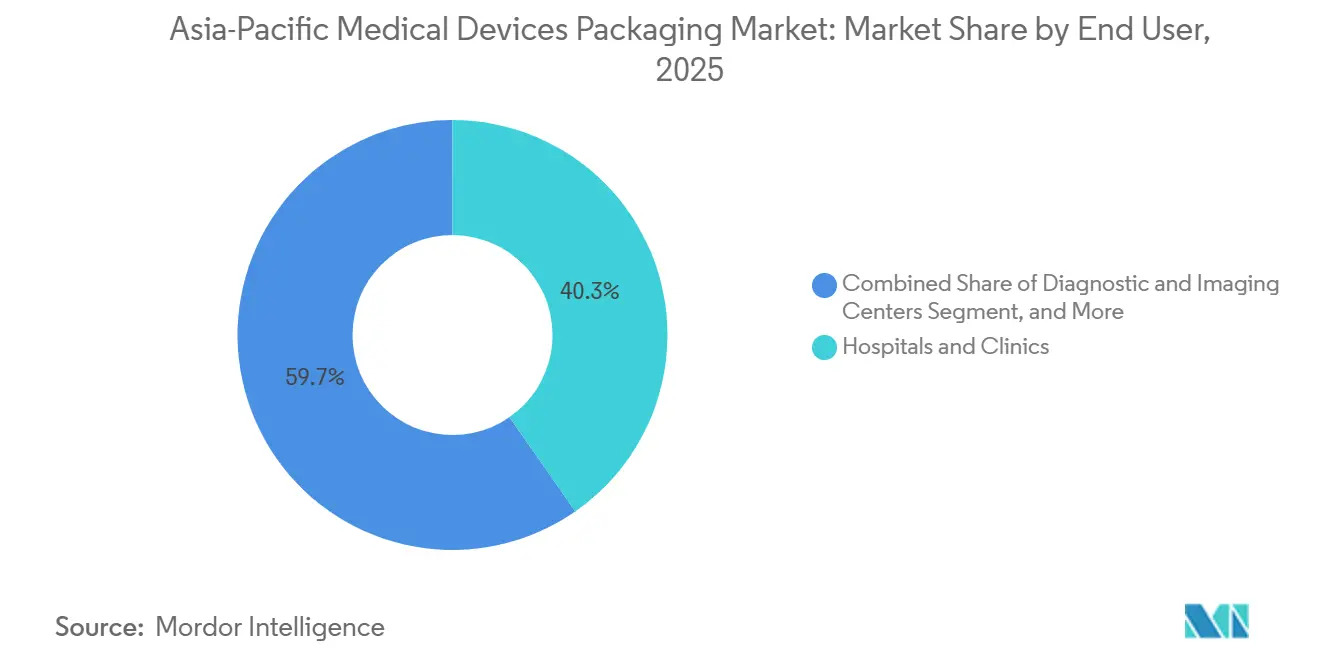

- By end user, hospitals and clinics held 40.33% of spending in 2025, while home healthcare is projected to expand at 7.43% through 2031.

- By packaging level, primary packaging captured 59.12% of revenue in 2025, while secondary packaging is projected to expand at a 7.31% CAGR through 2031.

- By geography, China commanded 34.77% of revenue in 2025, whereas India is expected to record the highest regional CAGR of 7.93% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Medical Devices Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Asia-Pacific Medical-Device Manufacturing Hub | +1.8% | China, India, Southeast Asia, South Korea | Medium term (2–4 years) |

| Growing Demand for Sterile Barrier Systems | +1.5% | Japan, Australia, South Korea, China | Short term (≤ 2 years) |

| Increasing Healthcare Expenditure and Aging Demographics | +1.3% | Japan, South Korea, Australia, China | Long term (≥ 4 years) |

| Stringent Regulatory Norms Mandating Tamper-Evident Packs | +0.9% | ASEAN, India, China | Medium term (2–4 years) |

| Rise of Direct-to-Patient E-Commerce Deliveries | +0.7% | Urban China, India, Southeast Asia | Short term (≤ 2 years) |

| Integration of Smart Sensors and Digital Tracking | +0.6% | Japan, South Korea, Australia, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Expansion of Asia-Pacific Medical-Device Manufacturing Hub

Multinational device makers accelerated capital spending in Malaysia, Thailand, Vietnam, and India after 2024 to hedge against single-country risk. The build-out of Class II and Class III assembly plants pulled packaging converters into adjoining industrial parks, allowing just-in-time delivery of sterile trays and pouches. India’s production-linked incentive scheme defrays clean-room capital costs, letting suppliers hit ISO 13485 standards without prohibitive debt loads. Co-location trims ocean-freight exposure, lowers inventory risk, and shortens design-change cycles, so converters win business on speed rather than solely on price. European and North American suppliers that rely on exports face margin pressure unless they also invest locally.

Growing Demand for Sterile Barrier Systems

Regulators across Asia-Pacific adopted ISO 11607-1:2019 and ISO 11607-2:2019, making validated sterile-barrier systems non-negotiable for most Class II and III devices.[1]Association of Southeast Asian Nations, “Medical Device Regulatory Harmonization Initiatives,” asean.org Hospitals refuse shipments that lack documented microbial-barrier performance, pushing sterile formats above half of regional volume. Although ethylene oxide remains the dominant sterilant, gamma and e-beam gained traction where environmental agencies curbed EO emissions. Film makers introduced polyethylene and polypropylene grades with improved radiation stability, preventing seal brittleness and extractables formation. Converters with in-house peel-strength and porosity labs enjoy a technical moat because low-cost rivals cannot fund validation equipment.

Increasing Healthcare Expenditure and Aging Demographics

High-income economies such as Japan, Australia, and South Korea spent more than 8% of GDP on health services by 2025.[2]Central Drugs Standard Control Organisation, “Tamper-Evident Packaging Guidelines for Medical Devices,” cdsco.gov.in With 30% of Japan’s population already over 65 years, demand surged for home-use devices packaged in easy-open pouches and large-font cartons. China’s expanding middle class bought diagnostic wearables that require tamper-evident packs to deter counterfeits. Insurers favor outpatient care to free up hospital beds, so chronic-care devices ship directly to residences, boosting volumes for single-use sterile packaging. Procurement teams increasingly score vendors on total cost of ownership, which now includes waste-disposal fees, making lightweight or recyclable packs a strategic differentiator.

Stringent Regulatory Norms Mandating Tamper-Evident Packs

Counterfeiting triggered serialization mandates in China and tamper-evident seal rules in India by 2025.[3]Central Drugs Standard Control Organisation, “Tamper-Evident Packaging Guidelines for Medical Devices,” cdsco.gov.in Regulators are harmonizing device codes, but implementation differs by country, creating compliance complexity. Converters invested in holographic labels, breakable seals, and barcode printers to enable OEMs to trace units across borders. Larger suppliers with enterprise systems that feed national databases gain share because smaller firms struggle with IT integration. Although added packaging features raise per-unit costs, OEMs absorb them to avoid warranty claims and reputational damage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Polymer-Resin Prices | -1.2% | Global, acute in Southeast Asia | Short term (≤ 2 years) |

| Cost-Reduction Pressure from Device OEMs | -0.9% | China, India, Southeast Asia | Medium term (2–4 years) |

| Weak Recycling Infrastructure for Multi-Material Packs | -0.5% | ASEAN, India, partly Japan and South Korea | Long term (≥ 4 years) |

| ASEAN ISO-11607 Harmonization Delays | -0.4% | Southeast Asia cross-border trade | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polymer-Resin Prices

Crude-oil swings and naphtha outages pushed polyethylene and polypropylene spot prices higher between 2024 and 2026. Converters on annual fixed-price contracts saw margin compression, especially in import-dependent Southeast Asia. Some firms trialed sugarcane-based polyethylene to hedge against petrochemical shocks, but bio-resins still cost 20-30% more than fossil grades. Virgin resin remains mandatory for primary sterile packs, so recycled blends appear mainly in outer cartons. Dual-sourcing across regions mitigates supply risk but adds complexity to OEM qualification audits.

Cost-Reduction Pressure from Device OEMs

Hospitals cap reimbursements, so OEMs demand 3-5% yearly price cuts from suppliers. Converters respond with lean manufacturing, predictive maintenance, and scrap-rate dashboards, yet resin inflation often wipes out gains. Scale matters: larger firms pool resin procurement and centralize design services, while small converters become acquisition targets. The squeeze slows adoption of value-added features such as RFID tags unless required by regulation or bundled into premium devices where patient-safety ROI is clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bio-Based Polymers Gain Traction

Plastics accounted for 47.88% of revenue in 2025, underscoring the dominance of polyethylene, polypropylene, and PET films in sterile pouches and thermoformed trays. The Asia-Pacific medical devices packaging market size for bio-based plastics is projected to rise at a 7.74% CAGR through 2031 as hospital scorecards elevate sustainability metrics. Early adopters blend sugarcane-derived polyethylene into multilayer films, maintaining seal integrity while lowering fossil-carbon footprints. Paperboard remains common in secondary cartons because it prints well and is widely recycled, yet humidity limits its role in primary barriers. Aluminum foil and composite laminates protect oxygen-sensitive implants but pose recycling challenges, an issue likely to intensify as extended producer responsibility fees spread across the Asia-Pacific.

Suppliers with validated bio-resin portfolios win specifications faster because OEMs avoid the cost of re-qualifying entire packaging systems. Glass continues to dominate pre-filled syringe and vial formats, but cyclic olefin copolymer is emerging for breakage-sensitive applications. Multilayer films that combine polyethylene for sealability, PET for puncture resistance, and aluminum for barrier control satisfy ISO 11607 performance tests, yet they complicate downstream material separation. Regulators are signalling a preference for mono-material solutions, giving an edge to converters investing in recyclable structures.

By Product Type: Pouches Dominate, Smart Formats Blister Accelerate

Pouches and bags delivered 31.36% of product-type revenue in 2025, reflecting their versatility across orthopedic, cardiovascular, and diagnostic devices. Rigid thermoformed trays guard delicate scopes and implants, while cartons enable shelf stacking and branding in retail pharmacy channels. The Asia-Pacific medical devices packaging market will see blister packs formats grow at 7.72% CAGR, led by oxygen-scavenger sachets and RFID-embedded labels that validate cold-chain compliance. Hospital buyers value time-temperature indicators that change color when shipments exceed preset thresholds, allowing ward staff to quarantine suspect lots instantly.

Adoption of smart components remains clustered in Japan, South Korea, and Australia, where reimbursement frameworks compensate for higher material costs. In China and India, OEMs restrict sensor use to high-value biologics or cardiac implants where recall risk is elevated. Converters that bundle software dashboards with packaging sensors are carving out service revenue streams, although data-standard fragmentation across national regulators still limits cross-border scalability.

By Application: Sterile Packaging Leads, Active Systems Emerge

Sterile formats accounted for 56.32% of application revenue in 2025 and anchor the Asia-Pacific medical devices packaging market, as most Class II and III devices must arrive contamination-free. Non-sterile packs, covering blood-pressure cuffs and stethoscopes, increasingly adopt tamper seals after counterfeit incidents in urban e-commerce channels. Active and smart systems will advance at a 7.29% CAGR to 2031 as infection-control committees demand documented evidence that barrier integrity survived transport. Oxygen absorbers and desiccant layers now come pre-sealed inside pouches, eliminating manual insertion that once slowed line speeds.

Digital tracking elements such as NFC chips enable OEMs to capture post-market data, including drop counts and temperature curves, which feed reliability analysis. Regulators such as Japan’s Pharmaceuticals and Medical Devices Agency encourage serialization, giving additional impetus to hybrid electronic-packaging designs. Cost remains a hurdle; therefore, vendors prioritize high-margin segments such as cardiac rhythm devices, diagnostic reagents, and biologic injectables for early rollouts.

By End User: Hospitals Anchor Demand, Home Healthcare Surges

Hospitals and clinics took 40.33% of 2025 revenue, driven by bulk purchases of sterile procedure kits and surgical trays. Procurement contracts bundle packaging performance metrics, waste-disposal fees, and vendor response times, pushing converters to adopt life-cycle costing models. Diagnostic and imaging centers specify light-barrier laminates to protect contrast agents and reagent cartridges, promoting innovation in pigmented PET films. Home healthcare demand will grow at a 7.43% CAGR, propelled by aging populations across Japan, South Korea, and Australia who manage chronic conditions outside hospitals.

Packaging must be user-friendly for elderly end users, so peel-open pouches include tactile notches and large-print instructions. Contract manufacturing and sterilization organizations (CMSOs) emerge as influential buyers because startups outsource assembly and sterilization, ordering validated packaging in high-volume rolls. The World Health Organization projects the 65-and-older cohort will exceed 25% of the population in several Asia-Pacific markets by 2030. Packaging for these devices increasingly incorporates instructional graphics and color-coded labeling to reduce user error, boosting patient safety.

By Packaging Level: Primary Dominates, Secondary Gains Share

Primary packs, including pouches, trays, and blisters, captured 59.12% of revenue in 2025. ISO 11607 compliance makes them the technical heart of any sterile-barrier system. Secondary packs will grow at 7.31% CAGR as e-commerce channels multiply individual parcel shipments, requiring tamper-evident outer cartons, corner cushioning, and QR codes for doorstep authentication. The Asia-Pacific medical devices packaging market for tertiary pallets is modest but growing, as RFID-enabled stretch wrap helps 3PLs track returns and recalls.

Converters that offer integrated primary-secondary bundles help OEMs avoid compatibility conflicts and reduce validation cycles. Branding considerations now matter because patients unbox products at home; graphics teams collaborate with packaging engineers to balance clinical sterility with consumer aesthetics. Smart-label pilots on outer cartons allow caregivers to scan lot codes with smartphones, closing data loops on temperature excursions or delivery delays.

Geography Analysis

China led with a 34.77% revenue share in 2025, thanks to vertically integrated clusters in Guangdong and Jiangsu where molding, thermoforming, and ethylene-oxide sterilization coexist in single parks. National Medical Products Administration rules expanded serialization to more device classes in 2025, pushing demand for barcode-ready labels and enterprise integrations. While foreign OEMs diversify sourcing, domestic consumption of diagnostic wearables and home-use therapeutics keeps volumes robust, sustaining local demand for tamper-evident cartons and validated pouches.

India is poised for the fastest growth at 7.93% CAGR through 2031. Production-linked incentives reimburse up to 25% of clean-room capex, enticing converters to co-locate with device plants in Hyderabad, Ahmedabad, and Bengaluru. The Central Drugs Standard Control Organisation’s 2025 order requiring tamper-evident packs for Class C and D devices accelerates investment in holographic labeling lines. Price sensitivity remains intense, so converters lean on automation and lean cell layouts to meet OEM cost targets while hitting ISO 13485 metrics.

Japan’s market, though smaller in absolute value, sets technology benchmarks. The Pharmaceuticals and Medical Devices Agency mandated track-and-trace compliance ahead of many peers, giving smart-label suppliers a testing ground. South Korea and Australia mirror Japan’s demographic challenges and regulatory rigor, particularly on cold-chain biologics. Australia’s Therapeutic Goods Administration fully aligned packaging requirements with ISO 11607 in 2025, simplifying multi-country compliance for suppliers. Rest-of-Asia-Pacific nations such as Thailand and Vietnam benefit from medical-tourism clinics and regional trade pacts that slash duties on packaging inputs, driving greenfield investments in pouch and tray lines.

Competitive Landscape

The Asia-Pacific medical devices packaging market features moderate fragmentation. Global majors such as Amcor, Sonoco, and Sealed Air run ISO-14644 clean rooms in China, Malaysia, and Australia, leveraging global resin procurement and automated inspection. Regional specialists like SteriPack, Technipaq, and Oliver Healthcare differentiate on quick-turn prototypes and low-volume specialty runs that global giants often decline. Dual-sourcing policies adopted by OEMs after 2024 distribute volume between a tier-one multinational and a regional backup, diluting single-supplier risk.

Strategic moves center on sustainable materials, active-packaging patents, and digital traceability. Amcor invested USD 50 million in Suzhou during 2026 to add thermoforming and in-house validation, positioning for relocations out of coastal China to inland hubs. Sonoco bought a Malaysian converter in 2025, granting instant access to Southeast Asian CMSOs. Sealed Air launched sugarcane-based polyethylene film in 2025 in Australia, betting that bio-resin premiums will shrink as scale builds.

Mid-tier contenders pursue ISO 13485 certification as a ticket into higher-margin sterile formats. Mergers and acquisitions have accelerated because small firms cannot absorb validation costs or enterprise IT upgrades needed for serialization. Patent filings in sensor-embedded films by 3M and DuPont hint at future competition that transcends commodity laminate price wars. Winning suppliers will combine clean-room capacity, testing labs, and data integration, translating technical moats into multiyear supply agreements.

Asia-Pacific Medical Devices Packaging Industry Leaders

Amcor Plc

DuPont de Nemours, Inc.

Sonoco Products Company

Oliver Healthcare Packaging

West Pharmaceutical Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Amcor committed USD 50 million to expand its Suzhou, China, medical-packaging plant, adding thermoforming, automated pinhole detection, and ISO 14644 clean-room capacity.

- November 2025: Sonoco acquired a Malaysia-based sterile-packaging converter, strengthening its footprint in Southeast Asian device clusters.

- September 2025: Gerresheimer opened a USD 40 million glass-vial line in Pune, India, targeting pre-filled vaccine syringes with automated cosmetic-defect inspection.

- July 2025: West Pharmaceutical Services partnered with a Japanese OEM to co-develop NFC-enabled smart packaging for cold-chain compliance, aiming for mid-2026 commercialization.

Asia-Pacific Medical Devices Packaging Market Report Scope

The Asia-Pacific Medical Devices Packaging Market Report is Segmented by Material (Plastics, Paper and Paperboard, Metals and Foils, Glass, Bio-based Plastics), Product Type (Pouches and Bags, Trays and Containers, Boxes and Cartons, Blister Packs, Other Product Types), Application (Sterile Packaging, Non-sterile Packaging, Active/Smart Packaging), End User (Hospitals and Clinics, Diagnostic and Imaging Centers, Home Healthcare, Contract Manufacturing and Sterilization Organization), Packaging Level (Primary, Secondary, Tertiary), and Geography (China, Japan, India, South Korea, Australia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Plastics |

| Paper and Paperboard |

| Metals and Foils |

| Glass |

| Bio-based Plastics |

By Product Type

| Pouches and Bags |

| Trays and Containers |

| Boxes and Cartons |

| Blister Packs |

| Other Product Types |

By Application

| Sterile Packaging |

| Non-sterile Packaging |

| Active / Smart Packaging |

By End User

| Hospitals and Clinics |

| Diagnostic and Imaging Centers |

| Home Healthcare |

| Contract Manufacturing and Sterilization Organization |

By Packaging Level

| Primary |

| Secondary |

| Tertiary |

By Country

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Material | Plastics |

| Paper and Paperboard | |

| Metals and Foils | |

| Glass | |

| Bio-based Plastics | |

| By Product Type | Pouches and Bags |

| Trays and Containers | |

| Boxes and Cartons | |

| Blister Packs | |

| Other Product Types | |

| By Application | Sterile Packaging |

| Non-sterile Packaging | |

| Active / Smart Packaging | |

| By End User | Hospitals and Clinics |

| Diagnostic and Imaging Centers | |

| Home Healthcare | |

| Contract Manufacturing and Sterilization Organization | |

| By Packaging Level | Primary |

| Secondary | |

| Tertiary | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large will the Asia-Pacific medical devices packaging market be by 2031?

It is forecast to reach USD 20.98 billion by 2031, growing at a 6.79% CAGR from 2026.

Which material segment is expanding the fastest?

Bio-based plastics are projected to grow at 7.74% as hospitals reward low-carbon packaging.

Why are smart and active packaging formats gaining traction?

Hospitals want real-time sterility and cold-chain data, so RFID labels and oxygen-scavenger sachets are now specified for high-value devices.

What drives India’s outperformance in growth?

Production-linked incentives, tamper-evident mandates, and multinational OEM diversification lift India’s CAGR to 7.93% through 2031.

How are converters coping with resin-price volatility?

They adopt dual-sourcing, trial sugarcane-based polyethylene, and negotiate index-linked contracts to shield margins.

What capabilities differentiate leading packaging suppliers?

ISO 13485 clean rooms, in-house sterile-barrier validation, and enterprise IT that feeds national serialization databases give a decisive edge.

Page last updated on: