Market Overview

| Study Period | 2020 - 2031 |

|---|---|

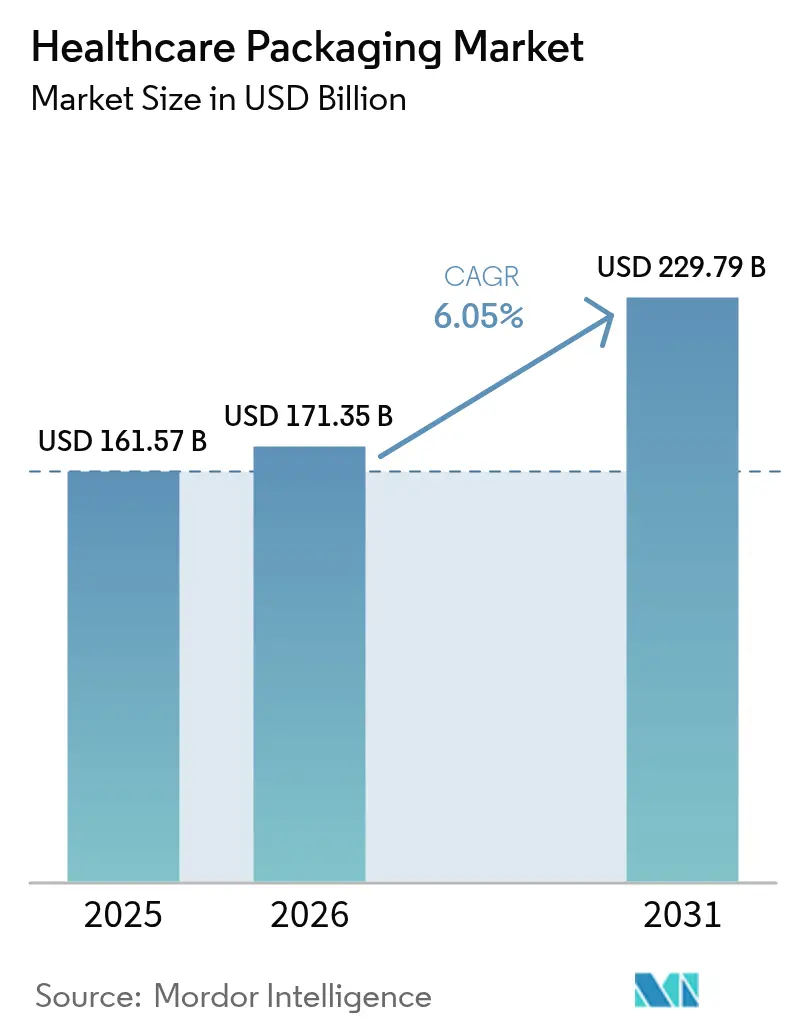

| Market Size (2026) | USD 171.35 Billion |

| Market Size (2031) | USD 229.79 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

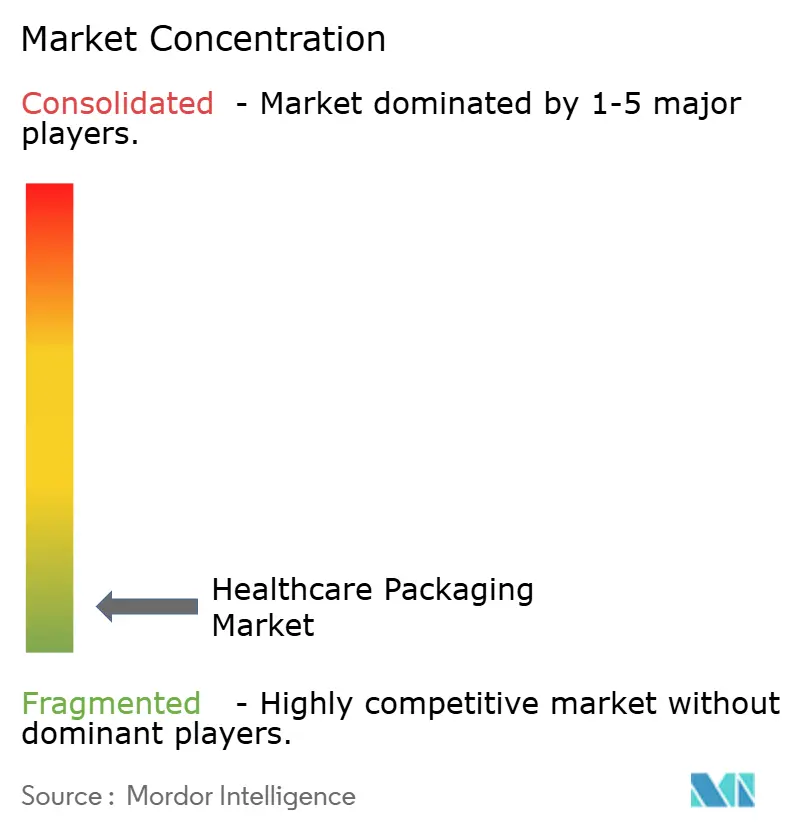

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Packaging Market Analysis by Mordor Intelligence

The healthcare packaging market size is expected to grow from USD 161.57 billion in 2025 to USD 171.35 billion in 2026 and is forecast to reach USD 229.79 billion by 2031 at 6.05% CAGR over 2026-2031. Accelerated demand for biologics, rapid expansion of home-care treatment models, and tightening serialization rules anchor this upward trajectory. Demographic momentum is evident as the over-65 cohort now outnumbers youth in Europe, intensifying needs for user-friendly, senior-safe packs. In parallel, pharmaceutical brand owners prioritize traceable, tamper-evident designs to curb counterfeits, while smart sensors embedded in primary packs enhance therapy adherence. Sustainability regulations in the European Union and select U.S. states are pushing brand owners toward recyclable mono-material structures without compromising barrier protection. Volatile polymer feedstock pricing and constrained medical-grade glass capacity remain cost headwinds, but ongoing investment in regional production hubs is cushioning supply risk.

Key Report Takeaways

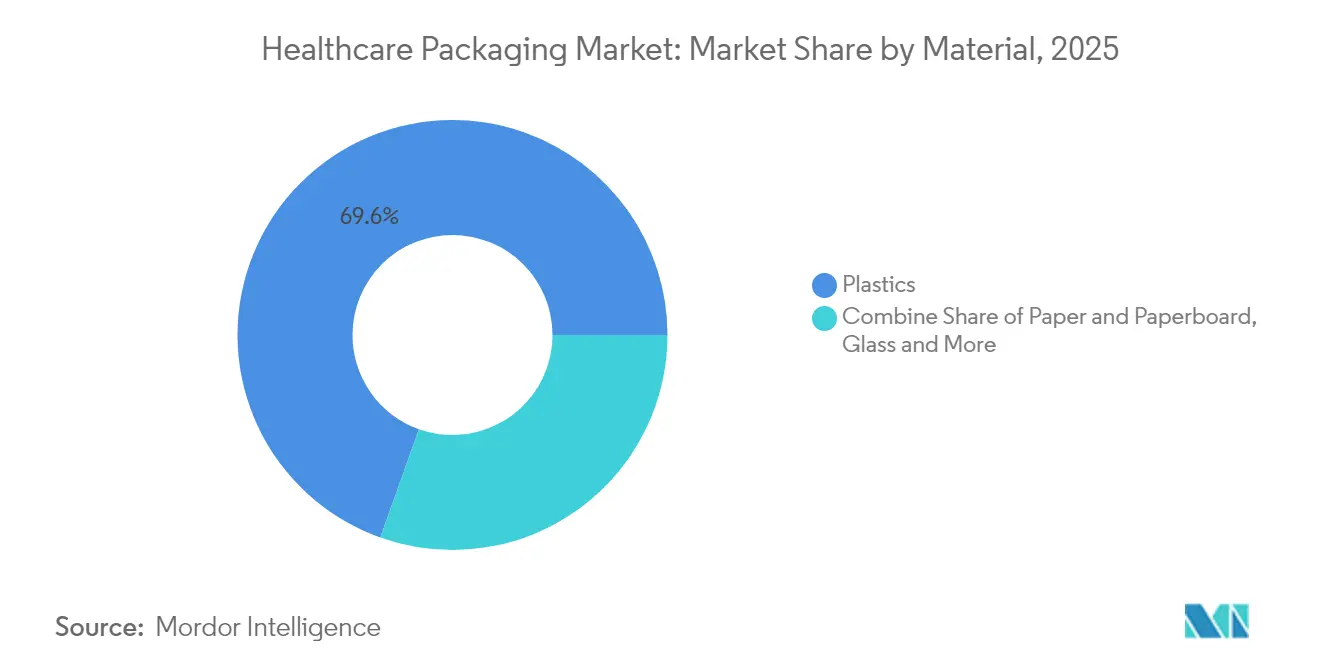

- By material, plastics led with 69.55% of healthcare packaging market share in 2025; glass is forecast to expand at a 9.88% CAGR through 2031.

- By product type, bottles and containers accounted for 39.78% of the healthcare packaging market size in 2025, while blister packs are projected to grow at an 8.29% CAGR to 2031.

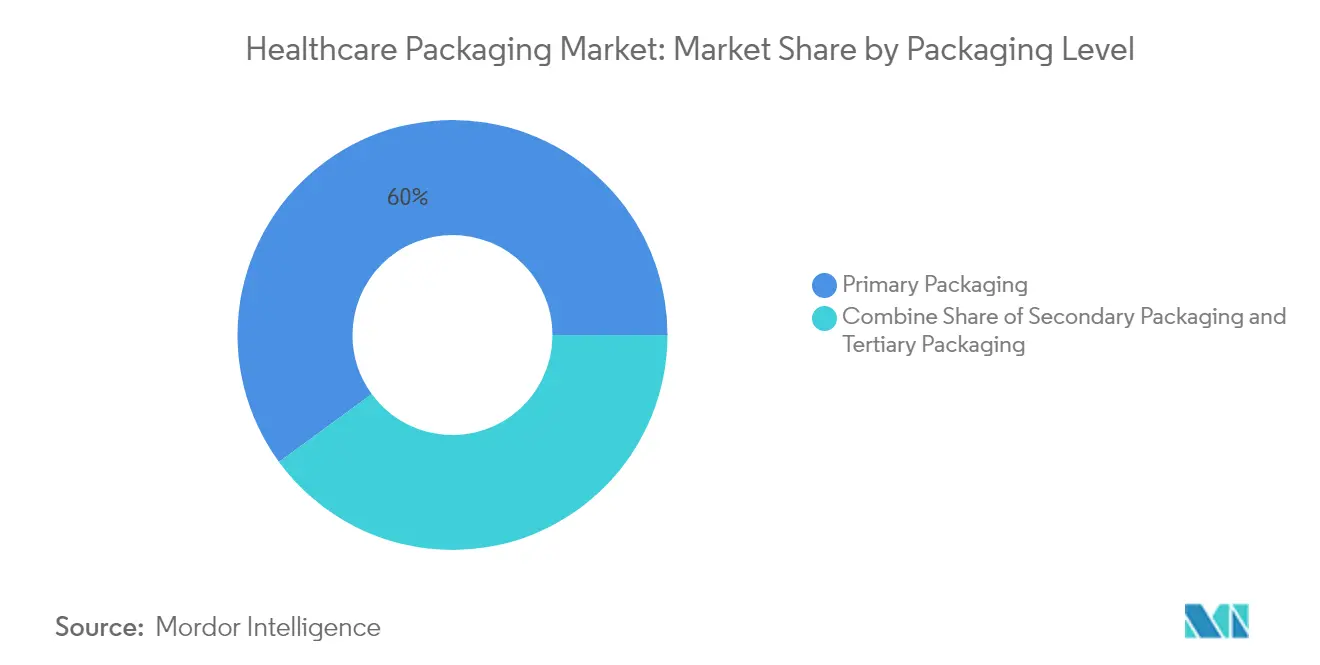

- By packaging level, primary packaging captured 60.05% share of the healthcare packaging market in 2025; tertiary packaging is advancing at an 7.78% CAGR through 2031.

- By geography, North America held 36.10% share of the healthcare packaging market in 2025, whereas Asia-Pacific is set for a 8.94% CAGR through 2031.

- By end-user, pharmaceutical manufacturing commanded 36.35% of the healthcare packaging market size in 2025, while nutraceuticals & OTC products are poised for 9.12% CAGR growth to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Healthcare Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand surge in self-care and home-diagnostic devices | +1.8% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Serialization and anti-counterfeit mandates | +1.2% | Global, led by US DSCSA and EU FMD implementation | Short term (≤ 2 years) |

| Aging population and chronic-disease prevalence | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Sustainability-driven material substitution | +0.9% | EU and North America core, spill-over to APAC | Medium term (2-4 years) |

| Cryogenic packaging for cell and gene therapies | +0.7% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Smart packs with RFID/NFC for adherence tracking | +0.4% | Developed markets initially, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand Surge in Self-Care and Home-Diagnostic Devices

Annual med-tech capital spending on diabetes care devices hit USD 7.09 billion in 2024, with USD 2.7 billion earmarked for continuous glucose monitors that require retail-ready sterile packaging. [1]Scitodate, “Diabetes Care Devices Deep-Dive,” scitodate.com BD’s PIVO Pro and MiniDraw launches show how brands now spec tamper-proof pouches sized for mail-order fulfillment while ensuring hospital-grade sterility. Medtronic’s FDA-cleared InPen-Simplera Smart MDI system underscores that packaging must protect not only the drug but also the embedded electronics and companion apps. The healthcare packaging market, therefore, pivots toward child-resistant yet senior-friendly closures, multi-layer cavities for sensors, and QR-enabled instructions that match telehealth workflows. Intensified home-care adoption keeps the healthcare packaging market on a robust growth arc.

Serialization and Anti-Counterfeit Mandates

Full enforcement of the U.S. DSCSA in November 2024 triggered up to 30% error rates in data exchanges, risking daily quarantines of 110,000 packs when codes mis-match.Cardinal Health’s turnkey serialization service pipeline grew as drug makers outsourced coding, aggregation, and validation steps. BD’s iDFill RFID syringe shows that embedding identifiers at the primary level lets companies dispense with secondary labels and accelerate line speeds. European FMD rules requiring dual human- and machine-readable codes further push the healthcare packaging market toward digital infrastructure investment. Suppliers able to bundle hardware, software, and validated cloud services gain share as serialization complexity mounts.

Aging Population and Chronic-Disease Prevalence

Multiple chronic conditions among U.S. adults climbed from 21.8% in 2013 to 27.1% in 2023, with the sharpest rise in young adults. West Pharmaceutical Services already derives 73% of proprietary-product sales from self-injection platforms that must ship in ergonomic, senior-safe trays. Caretech’s SmartPack integrates audio prompts and pill verification, reducing dosing errors among arthritis patients. These trends ensure the healthcare packaging market continues to develop larger fonts, tactile cues, and anti-slip surfaces that address declining dexterity without adding material weight.

Sustainability-Driven Material Substitution

The European Union’s Packaging and Packaging Waste Regulation mandates recyclability for all packs by 2030, although exemptions for contact-sensitive medical items are under review. [2]European Commission, “New EU Regulation Promotes the Procurement of Sustainable Packaging,” green-forum.ec.europa.eu Amcor’s AmFiber Performance Paper, newly protected by an EU patent, balances fiber-based structure with pharmaceutical-grade barrier layers. A life-cycle comparison showed polyethylene pouches emit 70% less CO₂-equivalent than glass or aluminum, complicating the “all-paper” narrative. TekniPlex now offers blister films with 30% post-consumer recycled content, hitting EU circularity targets without needing drug-formulation re-qualification. California’s SB 54 sets a 65% recycling rate by 2032 but presently exempts prescription drug packs, highlighting the regulatory patchwork that forces global brands to engineer modular designs. Green mandates, therefore, reshape the healthcare packaging market’s material mix and cost structure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petro-based resin price volatility | -0.8% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Complex multi-jurisdictional waste-disposal rules | -0.6% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Medical-grade glass capacity bottlenecks | -0.4% | Global, with supply concentration in Europe and Asia | Medium term (2-4 years) |

| Cyber-security risks in connected packaging | -0.3% | Developed markets with advanced healthcare IT | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Petro-based Resin Price Volatility

The shutdown of LyondellBasell’s Houston refinery and the commissioning of Formosa’s new polypropylene plant tightened propylene supply, with Argus expecting double-digit price hikes in 2025. Engineering-resin costs climbed again in March 2025, eroding converter margins. Healthcare brands tied to FDA-validated material codes cannot switch resins quickly, so smaller converters face liquidity crunches. The healthcare packaging market sees larger players using long-term hedging and multi-sourcing to blunt volatility, while they evaluate higher-barrier mono-PP laminates that permit down-gauging without risking barrier failure.

Complex Multi-Jurisdictional Waste-Disposal Rules

Arizona caps medical-waste storage at 90 days, whereas California mandates full cradle-to-grave plans, pushing pack designs toward double-lined, puncture-resistant tubs that add cost and weight. Federal 49 CFR 173.197 further requires rigid, leak-proof secondary containment during transit. [3]U.S. Department of Transportation, “49 CFR 173.197,” ecfr.gov Stericycle notes that 40 U.S. states adopted the Hazardous Waste Generator Improvements Rule in 2024, effectively raising documentation overhead for converters. The result is a healthcare packaging market where smaller firms must over-engineer packs for the strictest jurisdiction, limiting innovation and increasing minimum order quantities. Recyclers warn that current bio-hazard labeling laws hamper closed-loop schemes, despite life-cycle studies showing a 30% CO₂ reduction if medical plastics are mechanically recycled rather than incinerated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Glass Innovation Outpaces Plastic Volume

Plastics continued to account for 69.55% of healthcare packaging market share in 2025, reflecting unmatched cost efficiency and flexible processing windows. Conversely, glass is advancing at a 9.88% CAGR, buoyed by biologics that require zero-ion-leach containers. SCHOTT Pharma’s USD 371 million North Carolina plant will add 401 jobs and expand borosilicate syringe capacity for GLP-1 injectables, evidencing long-term confidence in premium vials. The healthcare packaging market size for high-value glass formats—vials, cartridges, syringes—will expand as mRNA, gene-editing, and cell therapies exit the clinic.

Advanced plastics retain dominance in inhalers, flexible IV bags, and ophthalmic droppers, but PFAS restrictions on certain fluoropolymer coatings force resin formulators to develop new barrier chemistries. Hybrid solutions, such as TekniPlex’s clear recyclable blister laminate, combine PET with EVOH to reach moisture-vapour-transmission targets traditionally reserved for foil. Paperboard is making headway in secondary wraps thanks to EU recyclability mandates, yet its penetration into primary drug contact layers remains limited. Metals continue to serve pressurized drug delivery aerosols, but propellant phase-out in European markets is opening white-space for algae-based biomaterials now in early testing. Collectively, raw-material diversification positions the healthcare packaging market for a nuanced landscape where therapeutic class determines container of choice.

By Product Type: Blister Innovation Drives Growth

Bottles and containers retained a 39.78% slice of the healthcare packaging market in 2025, but blister packs are sprinting ahead with an 8.29% CAGR. Amcor’s recycle-ready AmSky system substitutes PVC with HDPE, reducing greenhouse-gas emissions by 70% yet keeping the barrier specs demanded for moisture-sensitive antihypertensive tablets. Compliance blister cards featuring NFC tags now capture ingestion events, feeding adherence dashboards for clinicians. Vials and ampoules remain compulsory for lyophilized APIs, although Stevanato’s EZ-fill platform allowed Nipro to commercialize D2F ready-to-fill glass vials that cut change-over time by 80%.

Cartridges paired with wearable injectors are pivoting toward 8-mm thin-wall cannulas to handle high-viscosity biologics. Pouches have become the go-to for direct-to-consumer diagnostics kits, enabling low-profile letter-box shipping formats. The “other” category is swelling as smart packs embed desiccant pouches with RFID sensors that alert pharmacists when humidity excursions occur. Ultimately, the healthcare packaging market embraces a form-factor hierarchy where each format’s role is dictated by molecule sensitivity, dosage regimen, and emerging e-commerce fulfilment norms.

By Packaging Level: Tertiary Gains From Supply Chain Focus

Primary packs captured 60.05% of healthcare packaging market size in 2025 due to strict pharmacopoeia compliance, but tertiary layers post an 7.78% CAGR through 2031, propelled by cold-chain and serialization investment. Gerresheimer’s USD 180 million Georgia expansion couples injection-molding with in-house carton erection to shorten order-to-ship windows. Modern tertiary shippers integrate phase-change materials for 120-hour temperature hold and have IoT beacons that log real-time GPS and shock data.

Secondary cartons serve as the aggregation node where unique identifiers are linked to the primary level. Brands gravitate toward peel-and-seal QR flaps that reveal tamper activity without knives. Direct-to-patient distribution, now commonplace among specialty pharmacies, pushes tertiary packs to adopt gift-box aesthetics to improve unboxing experiences for consumer-facing therapies. The healthcare packaging industry leverages this trend to upsell value-added logistics kits bundled with validated lane data, ensuring that Korea-bound biologics meet 2-8 °C thresholds even during flight delays. Robust interoperability across packaging levels safeguards data integrity, vital for DSCSA verification.

By End-User: Nutraceuticals Capitalize on Wellness Trends

Pharmaceutical manufacturers still own 36.35% of healthcare packaging market share, yet the nutraceutical and OTC channel is sprinting at a 9.12% CAGR as preventive-health spending grows. Dietary-supplement brands request shelf-appeal tweaks like metallic inks and micro-embossed seals, but must still navigate child-resistant closure mandates. Medical-device OEMs, especially in cardiac monitoring, require ESD-safe, sterile trays that protect both circuitry and biocompatibility coatings.

Home-health companies order multi-dose roll-stock pouches pre-labeled for voice assistants that remind seniors to take pills. Hospitals prioritize single-use sterility barriers compliant with AAMI TIR22 for point-of-care compounding. The healthcare packaging industry thus juggles divergent regulatory loads, customizing print runs down to lot-level QR codes for tele-pharmacy while maintaining EU MDR paperwork stacks for class III devices. Constantly widening end-user demands guarantee long-run opportunities for converters able to master micro-segment production economics.

Geography Analysis

North America controlled 36.10% of healthcare packaging market share in 2025, supported by FDA serialization rules that compel high-margin coding equipment. Supply-chain turbulence persists; 80% of providers expect shortages to intensify, adding up to USD 3.5 million in annual costs for medium-sized systems. BD’s USD 2.5 billion domestic capacity build underscores a reshoring logic that protects the healthcare packaging market from trade disruptions. However, tariffs on medical devices now reaching 25% incentivize converters to dual-source tooling from Mexico and Canada.

Asia-Pacific is the fastest-growing region, charting a 8.94% CAGR on the back of generics expansion and public-health funding in India, China, and ASEAN. Amcor’s acquisition of Phoenix Flexibles doubled its cleanroom lamination capacity in India, demonstrating commitment to localize supply. Japan’s Health 2025 expo spotlighted regenerative-medicine packaging that demands cryo-validated vials. TOPPAN and DNP showcased fiber-based sterile packs, signaling a regional tilt toward circular materials. Europe maintains strong throughput despite regulatory churn. The upcoming recyclability mandate challenges legacy multilayer foils, yet drives R&D funding for bio-based barrier layers. Germany captures disproportionate share of glass syringe output, but capacity constraints spur investments in Spain and the Czech Republic. Middle East & Africa continue to expand basic generic drug plants in Saudi Arabia and Egypt, opening greenfield demand for GMP-grade films. South America posts mid-single-digit growth; Brazil’s ANVISA introduced e-leaflets that lower carton size, trimming logistics costs. Collectively these dynamics widen the healthcare packaging market size across every continent while diversifying the risk portfolio for multinational converters.

Regulatory Landscape

Healthcare packaging is shaped by overlapping product-safety, traceability, and transport rules, which influence label formats, coding requirements, and validated materials. In the United States, DSCSA-driven serialization continues to tighten operational requirements across primary, secondary, and tertiary packs, and FDA actions are also standardizing identifiers: in March 2026, FDA issued a Final Rule revising National Drug Code (NDC) format and drug label barcode requirements to move FDA-assigned NDCs to a uniform 12-digit format. This change increases the need for label and artwork updates, barcode verification, and system readiness across pharma packaging lines and downstream distribution.

In Europe, compliance is increasingly split across anti-tamper and environmental obligations. The EU Falsified Medicines Directive (FMD) safety-features framework keeps unique identifiers and tamper-evidence controls central for prescription medicines, while the Packaging and Packaging Waste Regulation (PPWR, Regulation (EU) 2025/40) moves recyclability and packaging management requirements toward a common EU baseline, with an application date of 12 August 2026. Parallel standardization efforts also affect packaging operations globally, including the publication of ISO 16791:2026 for international machine-readable coding of medicinal product package identifiers and the advancement of ISO/FDIS 11607-3 (final approval phase in April 2026) for process development in packaging for terminally sterilized medical devices.

Competitive Landscape

The healthcare packaging market remains fragmented. Global majors pursue a three-pronged strategy: scale capacity, enter smart-pack niches, and lock in sustainability credentials. Gerresheimer’s Bormioli acquisition adds Italian glass and elastomer lines to its footprint, elevating it to the second-largest sterile-syringe player. SCHOTT Pharma’s alliance with Stevanato expands polymer-syringe options, hedging against glass shortages. Amcor’s planned all-stock merger with Berry Global would create a USD 25 billion revenue entity, setting off a possible wave of antitrust concessions in flexible films.

Digital entrants differentiate by embedding NFC tags and IoT chips; Gerresheimer’s Gx Cap tablet bottle beams adherence data to clinical-trial dashboards. Thermo Fisher Scientific’s integrated cryogenic pack-and-ship service adds another layer of competition as CROs bundle logistics under single contracts. Sustainability messaging is now a credential: SGD Pharma gained Gold EcoVadis status, helping win biopharma bids that score environmental factors. Cyber-security expertise also weighs heavily; Schreiner MediPharm offers crypto-chips compliant with IEC 62443, assuaging hospital IT teams wary of ransomware threats. Competitive dynamics, therefore, hinge less on unit price and more on digital traceability, quality systems, and ESG disclosures, with mid-tier firms expected to consolidate or form alliances to survive.

Healthcare Packaging Industry Leaders

Gerresheimer AG

West Pharmaceutical Services Inc.

Schott AG

Stölzle-Oberglas GmbH

SGD SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Capacity localization and higher-value capability build-outs are creating a clearer gap for suppliers that can deliver validated sterile barriers, reliable labeling, and compliant materials at scale. In January 2026, SCHOTT Pharma inaugurated expanded vial production in Lebanon, Pennsylvania through a USD 60 million investment supported by BARDA, targeting domestic supply of standard and sterile ready-to-use glass vials, a key constraint point for biologics and injectable therapies. In flexible and device-oriented packaging, Amcor opened a USD 35 million healthcare packaging coating facility in Subang Jaya, Malaysia in April 2026, adding air-knife coating capability aligned with sterile medical device packaging requirements, and it also added healthcare packaging capacity through an investment in Sira, Karnataka, India (June 2026). Together, these moves point to opportunities around regional redundancy, shorter lead times, and tighter control of sterile quality systems for global brand owners.

Regulatory and operational change loads are also shifting demand toward packaging providers that can combine compliance tooling with digital workflows. PPWR becomes applicable on 12 August 2026, prompting redesign activity around recyclability and material choices in the EU, while pharma change-control expectations under FDA and EMA frameworks keep the bar high for pack modifications that could affect product quality. This combination supports demand for mono-material and recycled-content structures that minimize re-qualification burden, alongside serialization-ready print and inspection systems. Smart packaging adoption (NFC/RFID) in authentication, tracking, and adherence adds another layer of need for converters and component suppliers that can validate data integrity, cybersecurity, and machine-readability without slowing high-speed lines.

Recent Industry Developments

- July 2026: West Pharmaceutical Services completed the sale and transfer of the manufacturing and supply rights for its SmartDose 3.5 mL On-Body Delivery System and associated Tempe, Arizona operations to AbbVie. The transaction changes Wests exposure to on-body delivery manufacturing, while AbbVie gains direct control of an established capability set tied to combination-product packaging and drug delivery execution.

- May 2025: Gerresheimer completed an approximately EUR 100 million expansion and modernization project at its Lohr site, including a new oxy-hybrid glass melting furnace. The upgrade strengthens medical-glass output and supports customers seeking more resilient, lower-emission supply for vials and other pharma-grade containers.

- May 2024: Gerresheimer commenced an approximately EUR 166 million (about USD 180 million) expansion of medical systems production capacities in Peachtree City, Georgia, adding new buildings and planning for more than 400 new jobs. The investment increases North American capacity for high-growth medical systems that rely on precision components and compliant packaging formats for drug delivery and self-administration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers packaging used to protect, store, and distribute healthcare products, including medicines, medical devices, and related supplies, across primary, secondary, and tertiary packaging levels. Values are captured in revenue terms at the market level.

Scope exclusions: We exclude non-healthcare consumer packaging and general logistics services that sit outside packaging material and packaging conversion.

Segmentation Overview

- By Material

- Glass

- Plastics

- Paper and Paperboard

- Metals and Foils

- By Product Type

- Bottles and Containers

- Vials and Ampoules

- Cartridges and Pre-filled Syringes

- Blister Packs

- Pouches and Bags

- Other ProductType

- By Packaging Level

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

- By End-user

- Pharmaceutical Manufacturing

- Medical-Device OEMs

- Nutraceuticals and OTC

- Home-Healthcare Providers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping demand signals that reliably move packaging volumes, then converting those signals into value using publicly visible price and mix indicators. References we use include US FDA packaging and labeling guidance, US Pharmacopeia (USP) standards, EU packaging and waste directives, World Bank and OECD macro indicators, and UN Comtrade trade statistics for materials such as plastics, paperboard, and glass.

We also review annual reports, investor presentations, earnings transcripts, and reputable press coverage to track capacity additions, resin and glass cost movements, and changes in pharmaceutical output and medical device shipments. Where it helps sanity-check the player landscape and shipment direction, we use paid subscriptions for company financials and intelligence, news and financials, patent databases, and an import-export shipment-level database. These sources are not exhaustive, and many other public documents were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on packaging format mix, average selling price movement, and the pace of regulatory-led upgrades such as serialization, tamper evidence, and child-resistant features. We spoke with converters, material suppliers, distributors, and healthcare brand owners across APAC, EMEA, and the Americas, so regional differences in materials, compliance requirements, and adoption timing could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 13% | APAC: 48% |

| Mid tier: 49% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 20% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where healthcare output and treated volumes are translated into packaging demand, then filtered through packaging intensity by format and level (primary, secondary, and tertiary). To keep the numbers grounded, we corroborate totals using selective bottom-up approximations such as sampled supplier revenue roll-ups, channel checks on format shares, and volume-times-average-price checks for high-visibility packs like vials, ampoules, blisters, and bottles.

Inputs that matter in this market include pharmaceutical production growth by region, medical device shipment trends, the shift toward biologics and injectables that changes container and closure needs, mix changes between rigid and flexible packs, and the pass-through pattern of resin, paperboard, and glass pricing. In places where direct volume data is patchy, gaps are handled by using proxy indicators like trade flows of key materials and conversion capacity utilization, then rechecking those proxy assumptions through interviews.

For forecasting, scenario analysis is used to reflect differences in regulation timing and material substitution. The scenarios are anchored to variables that experts consistently referenced, including home-care growth, senior-friendly packaging uptake, and compliance-driven relabeling cycles. Assumptions are kept simple enough to explain and replicate without relying on private transaction data.

Data Validation & Update Cycle

Outputs are checked against independent signals such as regional healthcare manufacturing growth, material trade direction, and visible capacity announcements, so the model does not drift away from practical supply and demand. When an input creates a sharp jump, the variance is flagged, the driver is revalidated, and the underlying assumption is revisited before sign-off.

A multi-step internal review is followed so calculations, units, and currency conversions are consistent across regions and years. If primary feedback conflicts with desk direction, we re-contact sources and re-run sensitivities to identify which assumption is creating the spread. Reports are refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery check so clients receive the latest updated view.

Mordor Intelligence's Healthcare Packaging Market Estimate Compared With Other Published Estimates

Published market sizes for healthcare packaging can look far apart, even when they sound like they cover the same space. The difference usually comes from what is counted as packaging, the base year used, and how price and mix changes are carried through the forecast.

Some external estimates bundle narrower sustainability-only packaging subsets, or they fold in services and adjacent supply chain activities that do not sit inside packaging conversion revenue. Mordor Intelligence counts primary, secondary, and tertiary healthcare packaging formats across materials and end users, and it keeps the value model tied to packaging products rather than downstream logistics or broad sustainability program definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 161.57 B (2025) | |

| Industry Research House A | USD 143.96 B (2024) | Uses a different base year and growth window, and the lower value can also reflect a product and application mix that is benchmarked more heavily to historic pricing without fully carrying forward compliance-driven upgrades. |

| Sustainability Databook B | USD 43.13 B (2023) | Represents a narrower slice focused on recycled, reusable, and degradable packaging themes, which excludes large parts of mainstream healthcare packaging formats and materials that still dominate spending. |

The table shows that year choice and scope choices explain most of the spread before the forecasting technique comes into play. By keeping inclusions explicit and linking the totals to observable healthcare output, packaging format intensity, and realistic price progression, we end up with a market value that is easier to audit and repeat.

Key Questions Answered in the Report

What is the current size of the healthcare packaging market?

The healthcare packaging market stands at USD 171.35 billion in 2026 and is projected to reach USD 229.79 billion by 2031.

Which material dominates healthcare packaging?

Plastics hold 69.55% market share, although glass formats are expanding fastest at a 9.88% CAGR through 2031.

Why are blister packs growing quicker than bottles?

Blister packs offer unit-dose accuracy, stronger tamper evidence, and seamless integration with serialization codes, driving their 8.29% CAGR to 2031.

Which region is the fastest-growing market for healthcare packaging?

Asia-Pacific leads with a 8.94% CAGR, propelled by generic-drug manufacturing growth and government healthcare investments.

How are sustainability regulations influencing packaging design?

EU and California mandates require recyclable or high-recycled-content packs by 2030-2032, prompting brand owners to adopt mono-material laminates and fiber-based barriers.

What technologies are shaping smart healthcare packaging?

Integrated RFID/NFC labels, real-time temperature sensors, and software dashboards that track adherence and transit conditions are becoming mainstream features.

Page last updated on: