Pet Accessories Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

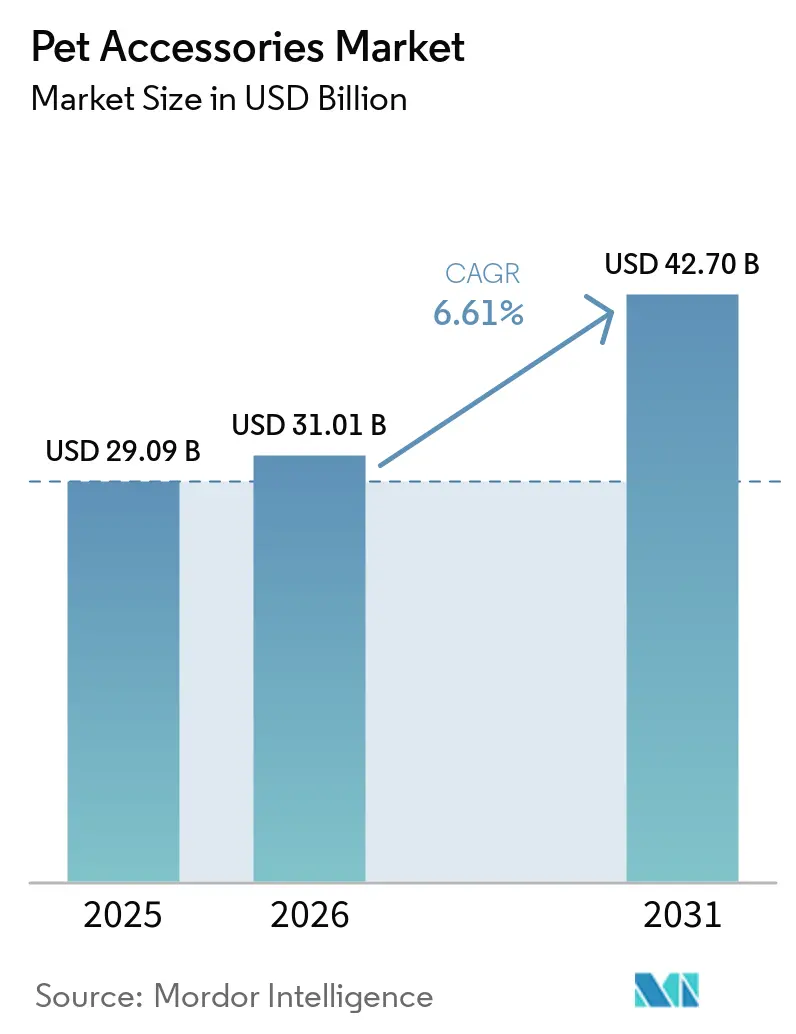

| Market Size (2026) | USD 31.01 Billion |

| Market Size (2031) | USD 42.70 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

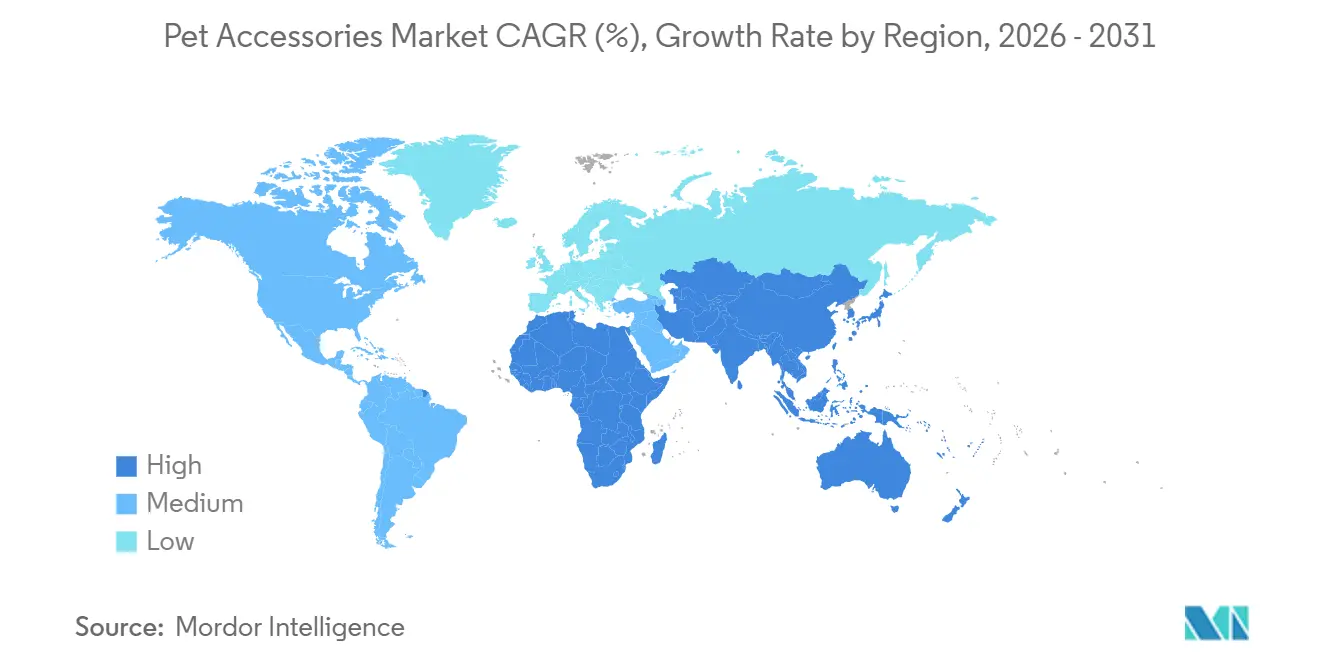

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Accessories Market Analysis by Mordor Intelligence

The pet accessories market size was valued at USD 29.09 billion in 2025 and is projected to grow from USD 31.01 billion in 2026 to USD 42.70 billion by 2031, at a CAGR of 6.61% between 2026 and 2031. According to the American Pet Products Association (APPA), 95 million households in the United States owned at least one pet in 2025, in which dog-owning households accounted for 53%, while cat-owning households reached 39%, both at multi-decade highs. This larger base of pet owners drives consistent spending, as an increasing number of owners treat pets as family members, making accessory purchases more akin to routine care than to discretionary spending. The market is also evolving beyond basic utility, with wellness, connected devices, and design influencing product development, merchandising, and pricing strategies. E-commerce, digital discovery, and subscription-based sales models are expanding access to innovation-driven stock-keeping units. However, private-label competition and compliance costs are contributing to steady, rather than rapid, market growth. Competitive differentiation is increasingly focused on connected collars, smart housing solutions, and recurring digital services, which create switching costs that extend beyond the physical products themselves.

Key Report Takeaways

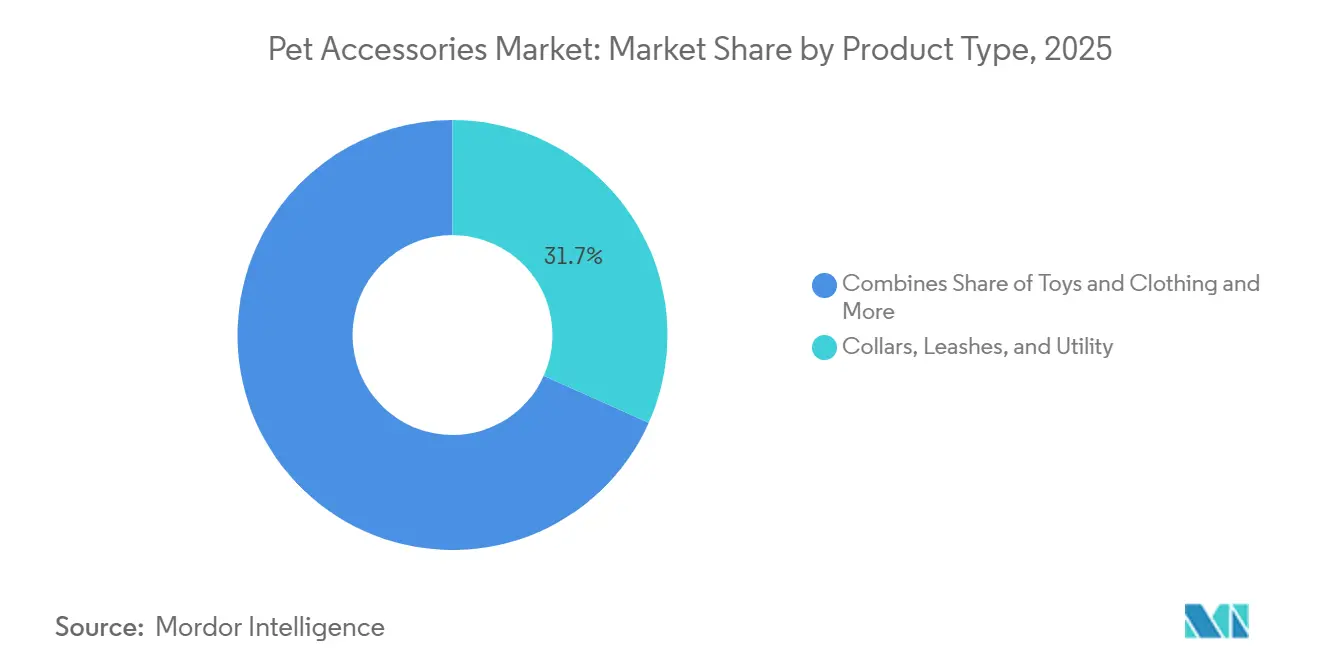

- By product type, the pet accessories market share for the collars, leashes, and utility segment held the largest 31.7% in 2025, while the pet accessories market size for the toys and clothing segment is forecast to expand at the fastest 8.7% CAGR from 2026 to 2031.

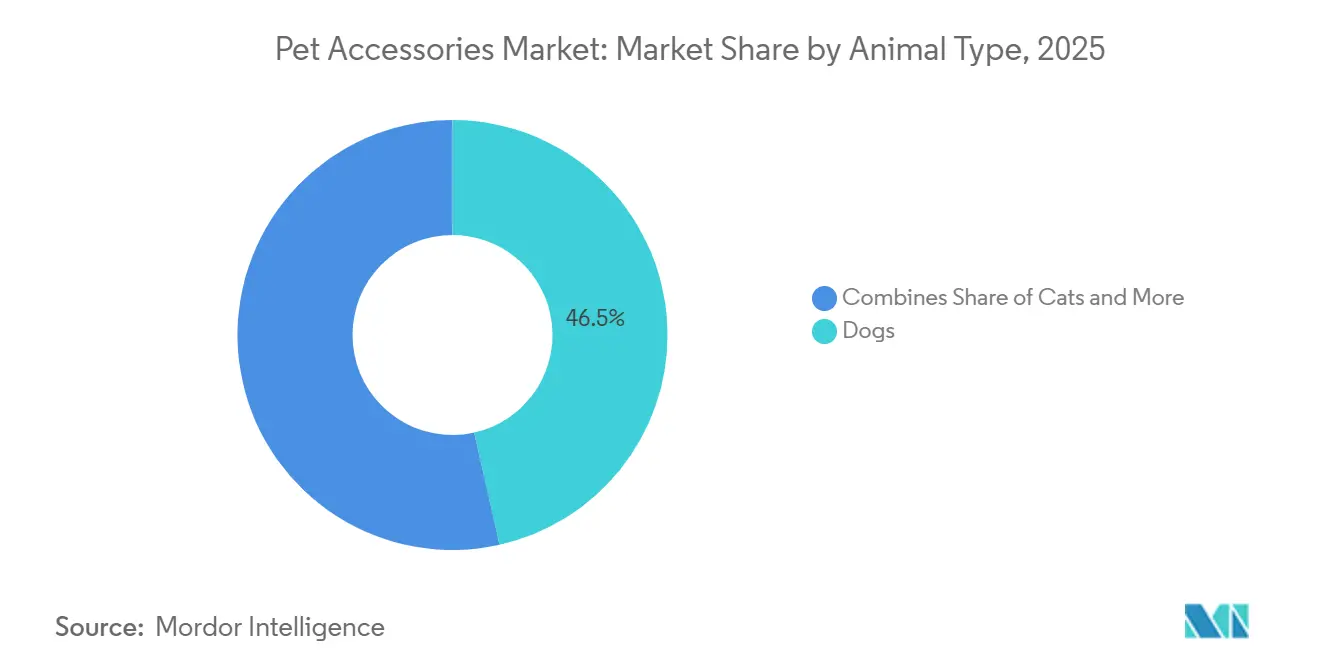

- By animal type, dogs accounted for the largest 46.5% share in 2025, while the pet accessories market for cats recorded the fastest CAGR at 7.6% from 2026 to 2031.

- By geography, the pet accessories market in North America was the largest at 39.4% share in 2025, while the Asia-Pacific market is advancing at the fastest 9.1% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pet Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership and pet humanization | +2.1% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Higher spending on pet health, hygiene, and comfort | +1.5% | North America and Europe | Medium term (2-4 years) |

| E-commerce and omnichannel convenience | +1.2% | Global | Short term (≤ 2 years) |

| Premiumization in design-led and functional accessories | +1.0% | North America and Europe | Medium term (2-4 years) |

| Indoor-cat enrichment upgrade cycle | +0.6% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Pet-inclusive mobility and travel accessory demand | +0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership and Pet Humanization

The pet accessories market is experiencing growth driven by an increasing pet population and stronger emotional bonds between pet owners and their animals. As pets become more integrated into family life, spending on accessories focused on comfort, enrichment, safety, and personalization is rising. This trend is particularly notable in Germany, one of Europe's largest pet markets. According to the Industrieverband Heimtierbedarf (IVH) and Zentralverband Zoologischer Fachbetriebe Deutschlands (ZZF), 43% of households in Germany owned at least one pet in 2025. A substantial and engaged pet-owning population sustains steady demand for accessories, while the ongoing trend of pet humanization promotes higher expenditure on premium and lifestyle-oriented products.

Higher Spending on Pet Health, Hygiene, and Comfort

Increased spending on pet health, hygiene, and comfort is driving growth in the pet accessories market, as consumers increasingly prefer premium products that emphasize wellness and daily care. According to the American Pet Products Association (APPA), spending in the United States pet industry on supplies, live animals, and over-the-counter medicine reached USD 34.4 billion in 2024, while veterinary care and product sales totaled USD 41.0 billion[1]Source: American Pet Products Association, “Industry Trends & Stats,” American Pet Products Association, americanpetproducts.org. This rising focus on pet well-being is boosting demand for premium accessories, including orthopedic bedding, calming products, wearable devices, grooming items, and hygiene products, across the pet accessories market.

E-commerce and Omnichannel Convenience

Digital retail is a significant growth driver for the pet accessories market, enhancing product accessibility and streamlining the purchasing process for consumers. Online platforms allow pet owners to compare products, explore new brands, and access a broader range of accessories than what is typically available in physical stores. According to Korea Bizwire, online channels accounted for 64% of pet product purchases in South Korea in 2024, demonstrating the strong adoption of digital commerce among pet owners. As e-commerce capabilities expand, the pet accessories market benefits from greater product visibility, convenience, and customer engagement across both basic and premium categories.

Premiumization in Design-led and Functional Accessories

Premiumization is driving revenue growth in the pet accessories market as pet owners prioritize products that blend style, quality, and functionality. There is increasing demand for accessories that offer enhanced durability, personalized designs, and technology-enabled features to improve pet comfort and convenience. This trend is further evident in the rising engagement with premium pet care ecosystems. According to the FY25 Preliminary Results of Pets at Home Group Plc, published on the London Stock Exchange, the Pets Club loyalty program reached 8.2 million active members in fiscal year 2025, demonstrating strong consumer interest in premium pet-related products and services. As owners focus more on quality and unique experiences, spending on premium accessories continues to grow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-price sensitivity and trade-down behavior | -1.1% | Global, strongest in Europe and emerging markets | Short term (≤ 2 years) |

| Regulatory and product safety compliance complexity | -0.8% | North America and Europe | Long term (≥ 4 years) |

| SKU-level testing burden across electronics, textiles, and chemical-contact items | -0.5% | Global, concentrated among Chinese exporters and cross-border sellers | Medium term (2-4 years) |

| Fast copycat cycles and private-label crowding | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium-price Sensitivity and Trade-down Behavior

The pet accessories market demonstrates resilience but remains vulnerable to budget constraints among lower- and middle-income households. During periods of cautious discretionary spending, consumers tend to prioritize essential products such as pet food and healthcare over non-essential accessories. According to data from Japan's Cabinet Office, the Consumer Confidence Index declined to 32.2 in April 2026, down 1.1 points from the previous month, reflecting weak consumer sentiment and constrained household spending. In such circumstances, pet owners are likely to delay purchases of premium accessories or opt for lower-cost alternatives, thereby extending replacement cycles and limiting value growth in discretionary product categories.

Regulatory and Product Safety Compliance Complexity

Regulatory and product safety compliance challenges are constraining growth in the pet accessories market, as manufacturers face increasingly stringent testing, certification, and documentation requirements across various jurisdictions. The United States Consumer Product Safety Commission (CPSC) issued a final rule in January 2025 mandating the electronic filing of compliance certificates for regulated consumer products at the point of United States Customs entry. This rule is set to be implemented as mandatory starting July 8, 2026 [2]Source: Consumer Product Safety Commission, “Certificates of Compliance,” Federal Register, federalregister.gov. These enhanced compliance procedures are driving up operational and administrative costs for pet accessory manufacturers, especially for those managing extensive imported product portfolios that include electronics, chemical-contact materials, and connected devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safety Utility Leads, Toys Accelerate

The collars, leashes, and utility segment held the largest share of the pet accessories market, accounting for 31.7% in 2025. This segment benefits from consistent replacement demand and widespread adoption among dog and cat owners, particularly for products such as harnesses, travel accessories, identification tags, and smart collars. Utility-focused products are gaining popularity as consumers increasingly prioritize safety, monitoring, and convenience in pet care. Additionally, demand is driven by the use of premium materials and ergonomic designs that enhance durability and comfort. The segment enjoys strong retail presence across supermarkets, pet specialty stores, and e-commerce platforms, ensuring stable recurring purchases from both new and existing pet owners.

The toys and clothing segment of the pet accessories market is projected to grow at the fastest CAGR of 8.7% through 2031. This growth is fueled by increasing pet humanization and a growing preference for enrichment-oriented and lifestyle products. Items such as seasonal apparel, interactive toys, calming products, and customized accessories are becoming part of routine discretionary spending rather than occasional purchases. Social media influence and the expansion of digital commerce are further driving product discovery and impulse buying. Manufacturers are addressing these trends by introducing themed collections, multifunctional designs, and premium product offerings that integrate entertainment, wellness, and aesthetics, catering to both mass-market and premium consumer segments.

By Animal Type: Dogs Anchor Revenue, Cats Deliver Growth

The pet accessories market share for dogs accounted for the largest 46.5% in 2025. This dominance is attributed to higher ownership rates and broader activity-based usage patterns, leading to significant spending on collars, leashes, travel carriers, training products, and outdoor accessories. Consumers also spend more frequently on replacement and premium utility products for dogs than on those for other companion animals. The demand is further supported by large product assortments, active lifestyle positioning, and the growing adoption of wearable and connected accessories. Retailers and brands prioritize dog-focused categories due to stronger cross-selling opportunities across grooming, mobility, wellness, and travel-related product ecosystems.

The pet accessories market size for cats is projected to grow at the fastest CAGR at 7.6% from 2026 to 2031. This growth is driven by increasing urban pet ownership and rising consumer spending on indoor enrichment, safety, and comfort products. Cat owners are expanding their purchases to include a wider range of accessories such as harnesses, climbing systems, calming products, interactive toys, and smart feeding solutions. Product innovation tailored to compact living spaces and premium indoor experiences is further driving consumer adoption. E-commerce platforms play a significant role in supporting category growth through targeted merchandising, subscription offerings, and direct-to-consumer brands specializing in feline-focused products and connected home pet care solutions.

By Distribution Channel: Specialty Retail Leads, Online Channels Accelerate

Specialty stores accounted for the largest share of the pet accessories market, holding 37.3% in 2025. This channel remains strong due to its combination of knowledgeable staff, curated product assortments, and in-store services such as grooming, veterinary support, and training, which online-only formats have yet to replicate at scale. Supermarkets and hypermarkets continue to serve as secondary channels, particularly for repeat purchases of basic items like collars and standard feeding accessories. This trend is especially prominent in South America and Africa, where specialty retail infrastructure is still developing. Veterinary clinics and pharmacies are gaining relevance for health-related accessories, including orthopedic bedding and therapeutic harnesses.

The online channel is projected to grow at the fastest CAGR of 11.1% from 2026 to 2031. This growth is driven by factors such as subscription-based purchasing, algorithm-driven product discovery, and the preference of Generation Z and Millennial pet owners to initiate their shopping online. Digital platforms are not only capturing market share from physical retail but are also serving as launchpads for connected accessories and premium enrichment products. These products benefit from video demonstrations and user reviews, which influence purchasing decisions.

Geography Analysis

The pet accessories market share in North America was the largest at 39.4% in 2025. This dominance is attributed to high pet ownership rates, robust consumer spending, advanced omnichannel retail infrastructure, and established premiumization trends. Consumers in the United States and Canada are increasingly purchasing wellness-focused and technology-enabled accessories through digital and subscription-based channels. The wide availability of products across supermarkets, specialty retailers, and e-commerce platforms supports recurring replacement purchases. Additionally, market participants benefit from heightened awareness of pet comfort, safety, and enrichment products. The region remains highly competitive due to strong brand penetration and the rapid adoption of connected and premium pet accessory categories.

The pet accessories market size for Asia-Pacific is advancing at the fastest 9.1% CAGR from 2026 to 2031. Factors such as rising urbanization, higher disposable incomes, and growing pet ownership among younger consumers are driving demand for premium and lifestyle-oriented pet accessories in countries such as China, India, Japan, and South Korea. E-commerce and social commerce platforms are accelerating market penetration by enabling direct product discovery and influencer-driven purchasing behavior. Domestic brands are also expanding rapidly within mid-range and premium categories. The growing popularity of indoor pets, particularly cats, is boosting demand for enrichment, grooming, feeding, and smart accessory products in major metropolitan areas.

Europe remains a significant market for pet accessories, driven by established pet ownership trends and robust consumer spending on premium pet care products in countries such as Germany, the United Kingdom, France, and Italy. The region is experiencing growth in subscription-based and omnichannel retail models, which facilitate recurring purchases and enhance customer retention. According to Pets at Home Group Plc, the company’s Pets Club membership base reached 8.2 million active members in fiscal 2025 against 7.8 million in 2024, indicating increased consumer engagement through loyalty and subscription programs [3]Source: Pets at Home Group Plc, “Annual Report and Accounts 2025,” petsathomeplc.com. This development is bolstering consistent demand for pet accessories, wellness products, and connected pet care solutions across the European market.

Competitive Landscape

The market remains fragmented, with global consumer brands, pet specialty companies, and direct-to-consumer businesses competing across premium, utility, and connected accessory categories. Key players include Central Garden & Pet Company, PetSmart, LLC (BC Partners), Petco Health and Wellness Company, Inc., Spectrum Brands Holdings, Inc., and PetSafe Brands (CD&R). Companies are increasingly emphasizing smart products, wellness integration, and digital merchandising to enhance consumer retention and drive recurring purchases. Innovation is extending beyond traditional collars and toys to include connected feeders, wearable monitoring devices, orthopedic bedding, and subscription-based product ecosystems. E-commerce and omnichannel distribution capabilities are becoming critical competitive differentiators as consumers increasingly prefer online shopping and rapid delivery. Additionally, product customization and sustainability are gaining prominence in premium accessory categories.

Competitive intensity is escalating as companies enhance digital commerce capabilities and invest in premium, recurring-demand categories. According to Central Garden & Pet Company’s fiscal 2025 Form 10-K, Walmart accounted for 29% of the company’s pet segment sales in 2025, up from 27% in the last year. This shift underscores the growing significance of store retail purchasing behavior in pet-related product categories. Companies are increasingly focusing on proprietary brands, connected devices, and direct-to-consumer strategies to improve margins and foster customer loyalty. Digital engagement, fulfillment efficiency, and recurring purchasing ecosystems are becoming pivotal factors in shaping long-term competitive positioning.

Technology integration and premiumization are reshaping competition within connected and wellness-oriented accessory categories. Market participants are investing in artificial intelligence-enabled monitoring products, automated feeders, and app-connected pet care ecosystems to enhance differentiation. Companies specializing in digital pet care infrastructure are gaining traction as consumers prioritize convenience, health tracking, and personalized experiences. Simultaneously, established manufacturers are expanding their premium product portfolios by incorporating ergonomic designs, sustainable materials, and multifunctional accessories. Regulatory compliance, product safety testing, and omnichannel fulfillment capabilities are becoming increasingly critical as brands scale operations across North America, Europe, and Asia-Pacific markets.

Pet Accessories Industry Leaders

Central Garden & Pet Company

PetSmart, LLC (BC Partners)

Petco Health and Wellness Company, Inc.

Spectrum Brands Holdings, Inc.

PetSafe Brands (CD&R)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Central Garden & Pet Company established an 80/20 joint venture with Phillips Pet Food and Supplies by contributing its pet distribution business, which handled approximately 26,000 SKUs. This transaction aligns with the company’s strategy to prioritize higher-margin branded pet products and enhance e-commerce fulfillment capabilities.

- December 2025: Central Garden & Pet Company announced the acquisition of Champion Petfoods USA's assets as part of its strategy to enhance its premium pet product portfolio and broaden its distribution network within the United States pet accessories market.

- October 2025: Swedencare AB collaborated with zooplus SE to introduce the NaturVet supplement range across Europe via zooplus’ online pet retail platform. This partnership enhanced the availability of premium pet wellness and care products within the European pet accessories and health market.

Global Pet Accessories Market Report Scope

Pet accessories are products intended to enhance the comfort, safety, hygiene, training, travel, entertainment, and daily care of companion animals, including dogs, cats, birds, and small pets. These items include collars, leashes, toys, bedding, feeding accessories, grooming tools, apparel, carriers, and smart pet devices, all designed to enhance convenience and promote pet well-being.

The pet accessories market report is segmented by product type (toys and clothing, housing, bedding and feeding, collars, leashes, and utility, pet hygiene products, and other products), by animal type (dogs, cats, and other animals), by distribution channel (convenience stores, online channel, specialty stores, supermarkets/hypermarkets, and other channels), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Toys and Clothing |

| Housing, Bedding, and Feeding |

| Collars, Leashes, and Utility |

| Pet Hygiene Products |

| Others |

| Dogs |

| Cats |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Toys and Clothing | |

| Housing, Bedding, and Feeding | ||

| Collars, Leashes, and Utility | ||

| Pet Hygiene Products | ||

| Others | ||

| By Animal Type | Dogs | |

| Cats | ||

| Other Pets | ||

| By Distribution Channel | Convenience Stores | |

| Online Channel | ||

| Specialty Stores | ||

| Supermarkets/Hypermarkets | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the pet accessories market by 2031?

The pet accessories market is forecast to reach USD 42.7 billion by 2031.

Which region leads pet accessories demand today?

North America led with the largest market share of 39.4% in 2025, supported by high pet ownership, strong omnichannel retail, and high per-pet spending.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected 9.1% CAGR from 2026 to 2031, driven by rising pet adoption, digital retail, and stronger premium demand.

Which product category holds the largest share?

Collars, Leashes, and Utility was the largest product type in 2025 with a 31.7% market share.

Page last updated on: