Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Peru Telecom Tower Market Report is Segmented by Ownership (Operator-Owned, Independent TowerCo, and More), Installation (Rooftop, Ground-Based), Fuel Type (Renewable-Powered, Grid/Diesel Hybrid), and Tower Type (Monopole, Lattice, Guyed, Stealth/Concealed). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Installed Base).

Market Overview

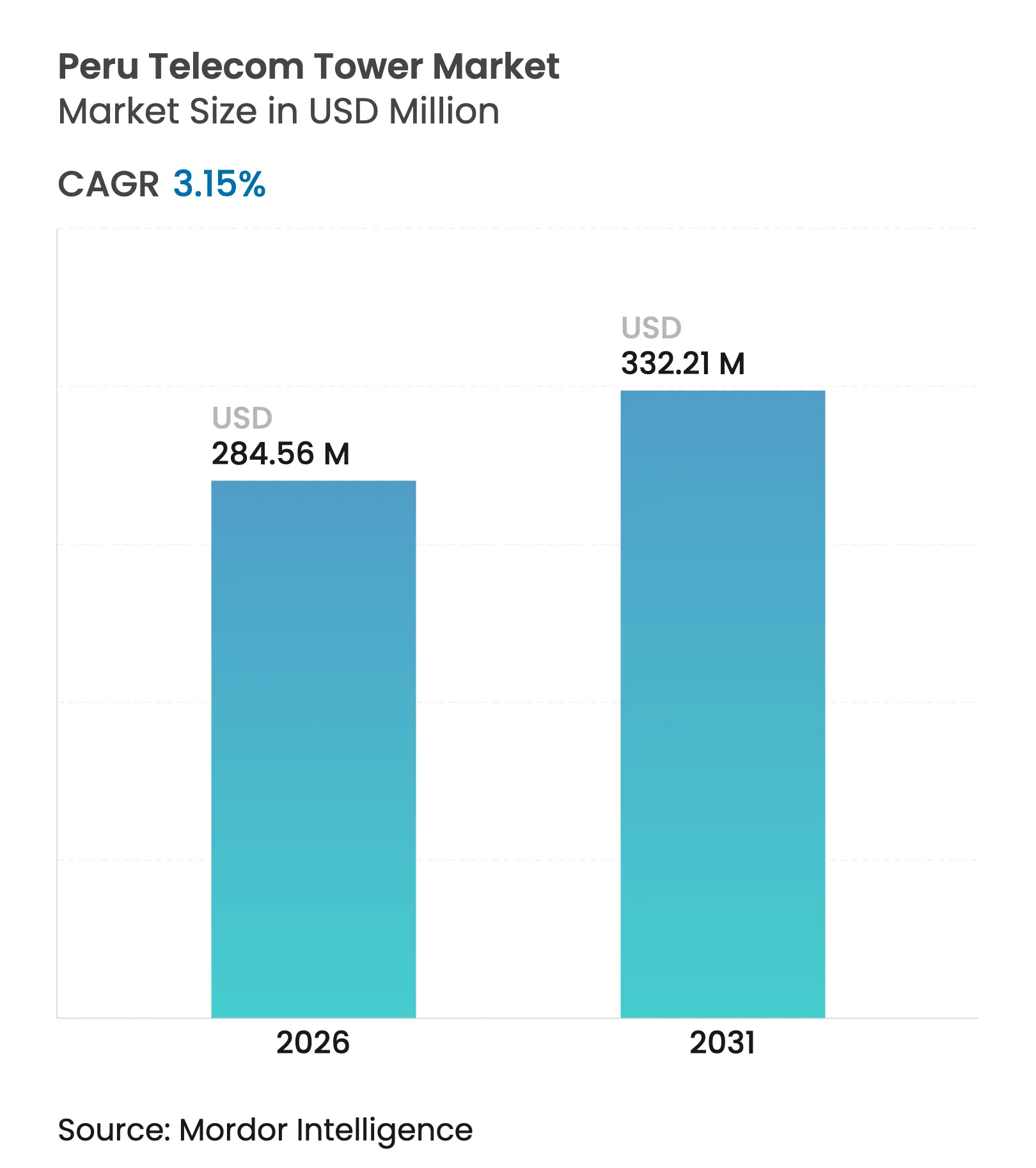

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 284.56 Million |

| Market Size (2031) | USD 332.21 Million |

| Growth Rate (2026 - 2031) | 3.15 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Continued densification in core urban zones, direct spectrum assignments for 5G, and tower sale-leaseback activity underpin steady capital deployment even as operators shift away from wide-area green-field builds. Independent TowerCos leverage neutral-host portfolios to accelerate co-location uptake, while renewable-powered hybrid sites gain traction as diesel logistics costs rise in remote provinces. Government-backed public-private partnership (PPP) pipelines and Open-RAN pilots further widen opportunities for low-cost coverage expansion. Currency volatility and a 180-220-day average municipal permit cycle temper rollout velocity but have not derailed overall investment momentum.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

4G/5G coverage obligations in 700 MHz and 3.5 GHz auctions 4G/5G coverage obligations in 700 MHz and 3.5 GHz auctions | +1.2% | National; early gains in Lima, Arequipa, Trujillo | Medium term (2–4 years) |

(~) % Impact on

CAGR Forecast

:

+1.2%

|

Geographic

Relevance

:

National; early gains in Lima, Arequipa,

Trujillo

|

Impact Timeline

:

Medium term (2–4 years)

|

National Fiber-Optic Backbone driving rural co-location demand National Fiber-Optic Backbone driving rural co-location demand | +0.8% | Rural Andes, Amazon, mining corridors | Long term (≥ 4 years) | |||

DAS and small-cell densification in Lima metropolitan area DAS and small-cell densification in Lima metropolitan area | +0.6% | Lima metro, secondary cities | Short term (≤ 2 years) | |||

Renewable-powered hybrid sites to cut diesel logistics costs Renewable-powered hybrid sites to cut diesel logistics costs | +0.4% | Remote Amazon basin, highland regions | Medium term (2–4 years) | |||

Tower sale-leaseback programs by regional MNOs (Entel, Bitel) Tower sale-leaseback programs by regional MNOs (Entel, Bitel) | +0.3% | Nationwide | Short term (≤ 2 years) | |||

Open-RAN pilots by OSIPTEL lowering entry barriers for MVNOs Open-RAN pilots by OSIPTEL lowering entry barriers for MVNOs | +0.2% | Urban clusters | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

4G/5G coverage obligations in 700 MHz and 3.5 GHz auctions

Direct spectrum assignment announced in March 2025 eliminates auction delays and lets operators redeploy capital from license fees to site builds. Coverage targets for 700 MHz and 3.5 GHz create immediate requirements for macro and infill infrastructure, especially in underserved rural districts. Vendors such as ZTE, contracted by Bitel for 1,000 antennas, have pre-positioned inventory to compress deployment timelines. Obligations stipulate service level milestones, compelling operators to accelerate tower upgrades or new-build programs to avoid penalties. The policy, therefore, injects predictable demand into the Peru telecom tower market, sustaining pipeline visibility for TowerCos.

National Fiber-Optic Backbone driving rural co-location demand

Internet Para Todos and Internexa have extended optical backhaul nodes delivering 10 Gbps in northern clusters, lowering transport costs at peripheral sites [1]BNamericas, “ISA's Internexa expands network in Peru eyeing mining, energy and carriers,” bnaméricas.com. Mining firms leverage Peru’s works-for-taxes scheme to finance additional spurs, anchoring traffic in sparsely populated areas. Fiber presence transforms previously single-tenant rural towers into multi-tenant assets, improving return profiles for independents. Government incentives encourage further backbone build-outs, positioning remote provinces for incremental co-location leases throughout the forecast window. This structural tailwind bolsters the Peru telecom tower market long-term.

DAS and small-cell densification in Lima metropolitan area

Macro sites in Lima have reached saturation, moving operators toward rooftop, DAS, and small-cell systems to manage traffic growth. QMC Telecom’s indoor system at the Faria Lima commercial hub showcases the rising preference for blended architecture [2]QMC Telecom, “Indoor Solutions: Faria Lima,” qmctelecom.com. Municipal height limits and aesthetic ordinances favor low-profile equipment, accelerating the adoption of monopoles and concealed designs. These dynamics feed a steady stream of urban infill contracts for TowerCos seeking diversification within the Peru telecom tower market. The uptick in rooftop leases also moderates permitting friction because existing structures often bypass full environmental reviews.

Renewable-powered hybrid sites to cut diesel logistics costs

Approved renewable projects totaling 2,155 MW create grid stability opportunities and bilateral power-purchase agreements that TowerCos can tap. Diesel transport costs in the Amazon frequently top USD 2 per liter, incentivizing hybrid solar-wind solutions such as Kliux micro-turbine arrays tailored for BTS loads [3]Kliux, “Renewable hybrid wind solar power system for telecommunication BTS,” kliux.com. Battery storage integration now meets 3-hour autonomy thresholds required by MNO SLAs. Renewable penetration, therefore, removes key operational risks and unlocks opex savings, elevating ROI for next-generation sites in the Peru telecom tower market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lengthy municipal permitting (average 180-220 days) Lengthy municipal permitting (average 180-220 days) | −0.9% | National; acute in Lima, Cuzco, Arequipa | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

−0.9%

|

Geographic

Relevance

:

National; acute in Lima, Cuzco, Arequipa

|

Impact

Timeline

:

Short term (≤ 2 years)

|

Anti-tower activism in Cuzco and Arequipa tourist corridors Anti-tower activism in Cuzco and Arequipa tourist corridors | −0.4% | Cuzco, Arequipa heritage zones | Medium term (2–4 years) | |||

Currency volatility vs. USD-denominated lease contracts Currency volatility vs. USD-denominated lease contracts | −0.3% | Nationwide | Short term (≤ 2 years) | |||

High cost of grid extension in Amazonia elevating capex High cost of grid extension in Amazonia elevating capex | −0.2% | Amazon basin, remote mining sites | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Lengthy Municipal Permitting

Average approval periods of 180-220 days inflate carrying costs and delay revenue recognition for TowerCos. Contraloria-flagged project paralyzes and illustrates systemic governance gaps that also affect telecom infrastructure. Aggreko’s ability to energize a high-altitude site in 45 days proves technical capacity exists, yet administrative hurdles remain the principal timeline bottleneck. Protracted permitting erodes NPV on marginal projects, prompting some operators to sequence builds conservatively, which suppresses near-term growth in the Peru telecom tower market.

Anti-tower activism in Cuzco and Arequipa tourist corridors

Tourism-driven municipalities impose stringent aesthetic standards that constrain traditional lattice or monopole placement near UNESCO heritage assets. Community push-back intensifies in Cuzco and Arequipa, prolonging consultations and inflating concealed-tower capex by 40-60%. Movistar’s pivot to fiber for 290,000 households in Arequipa reflects operator preference for less intrusive solutions [4]DPL News, “Perú | Más de 290 mil hogares de Arequipa ya pueden acceder a la fibra óptica de Movistar,” dplnews.com. While demand persists, activism reshapes site economics and tilts deployment toward costlier stealth formats, marginally dragging on the Peru telecom tower market CAGR.

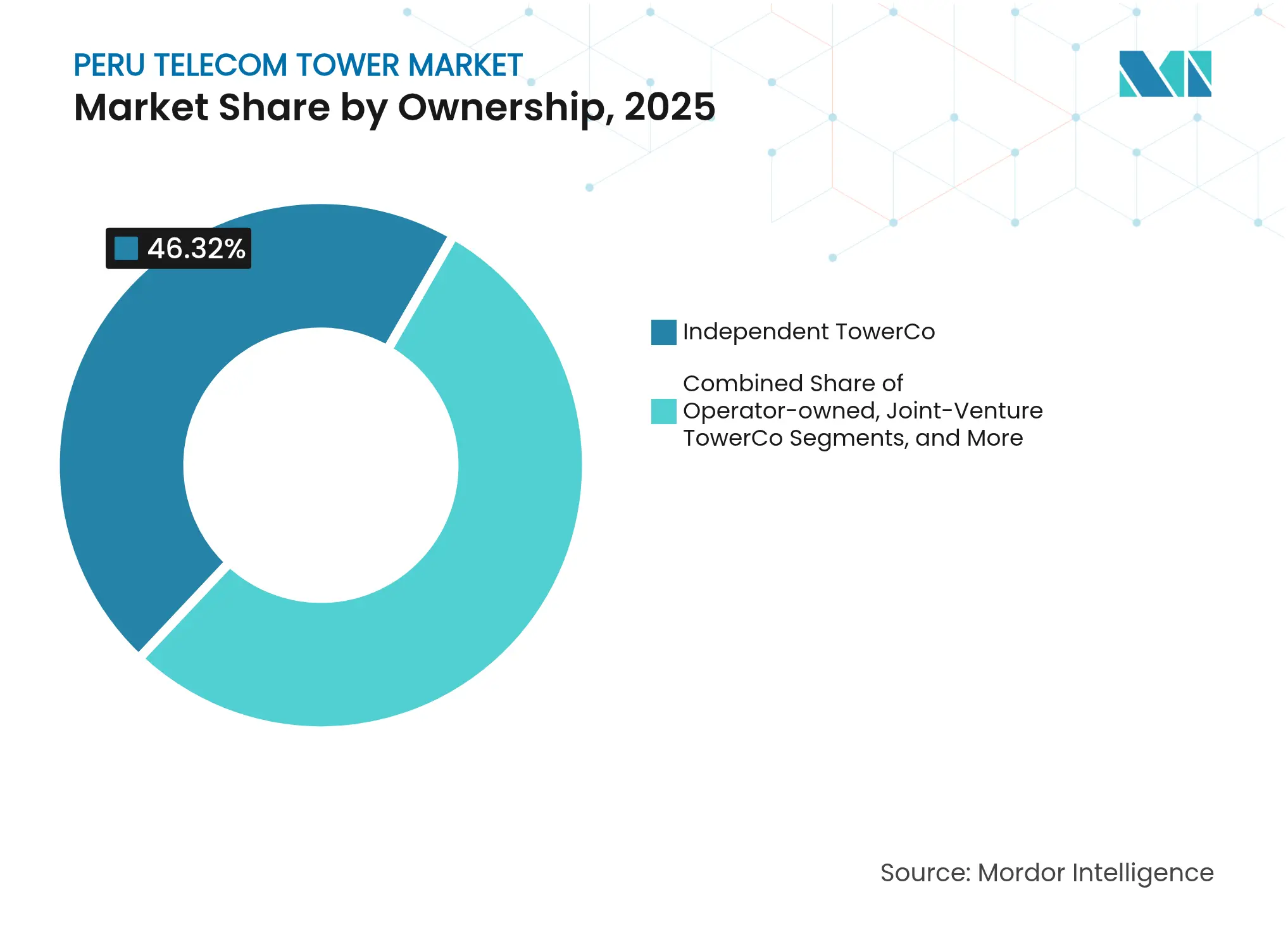

By Ownership: Independent TowerCos Sustain Structural Advantage

Independent TowerCos controlled 46.32% of active sites in 2025 and are expanding at a 5.18% CAGR, supported by neutral-host regulations and operator sale-leaseback programs that offload capex while preserving service-level flexibility. This stake equates to the single largest slice of the Peru telecom tower market size. Scale allows independents to spread fixed costs over multi-tenant leases, sharpening pricing power against MNO captive entities.

Joint-venture TowerCos are emerging to balance operator control with investor capital, particularly attractive for rural footprints where single-tenant economics remain thin. MNO captive portfolios persist in critical metro grids but show limited expansion beyond maintenance upgrades. As spectrum-driven densification continues, the Peru telecom tower market remains structurally favorable to independents capable of rapid build-to-suit delivery.

Note: Segment shares of all individual segments available upon report purchase

By Installation: Rooftop Uptick Offsets Ground-Based Saturation

Ground sites accounted for 78.06% of installations in 2025, equal to the bulk of Peru's telecom tower market share, yet urban land scarcity pushes operators toward rooftops. Rooftop deployments are growing at a 7.29% CAGR as Lima municipality approvals for vertical extensions outpace new land concessions. The Peru telecom tower market size for rooftop footprints is projected to expand steadily through 2031, buoyed by expedited permitting and lower site-prep costs.

Ground-based structures remain essential in mining corridors and Amazon outposts where coverage radii and terrain demand higher elevations. However, improved structural retrofits have narrowed the cost gap between reinforced rooftops and smaller ground monopoles, spurring substitution in secondary cities. Permit reforms targeting shorter clearance windows for adaptive reuse sites would further tilt momentum toward rooftop additions inside urban clusters.

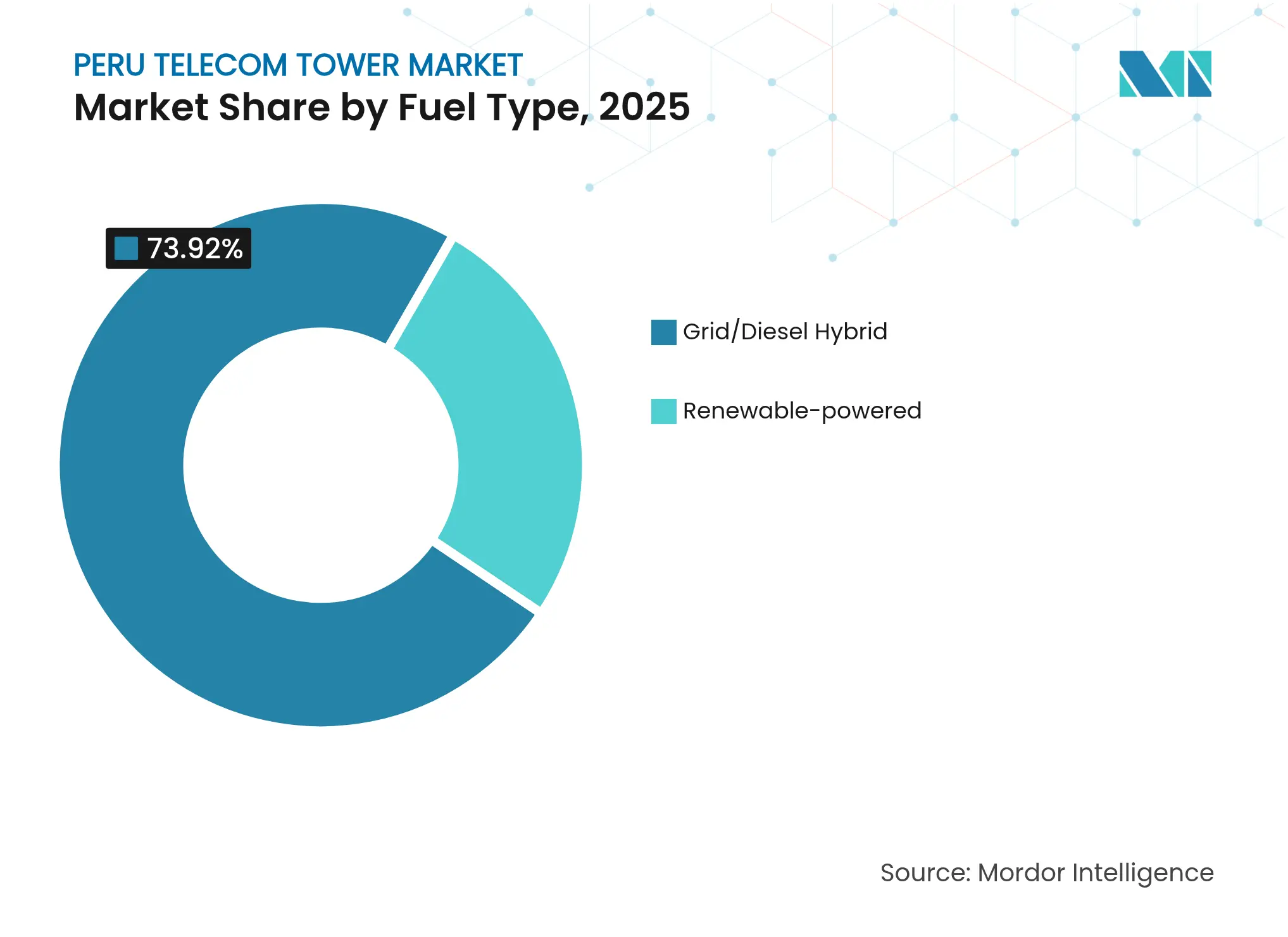

By Fuel Type: Renewable-Hybrid Solutions Gain Economic Credibility

Grid/diesel hybrids dominated 73.92% of the Peru telecom tower market size in 2025, a reflection of grid instability outside Lima. Yet renewable configurations exhibit the fastest 11.49% CAGR, propelled by declining battery costs and supplier learning curves. Diesel-logistics savings exceed USD 40,000 annually per remote site, yielding paybacks under five years.

Grid availability remains uneven, so hybrids buffer reliability risks while cutting emissions. TowerCos increasingly bundle renewable kits in build-to-suit contracts, shifting cost burdens to upfront capex but improving long-term EBITDA margins. As Peru’s utility-scale solar and wind assets come online, clean grid connections will proliferate, compressing diesel share further across the Peru telecom tower market.

Note: Segment shares of all individual segments available upon report purchase

By Tower Type: Monopoles Balance Cost and Community Acceptance

Monopoles held 40.53% of 2025 deployments, the largest slice of Peru's telecom tower market share, because their compact footprints align with municipal guidelines. Concealed variants grow at 9.22% CAGR, albeit from a low base, addressing heritage-site objections yet inflating structural expenses.

Lattice towers prevail in rugged provinces where altitude and load requirements supersede aesthetic concerns. Advances in composite materials now enable taller monopoles, pushing them into coverage roles previously reserved for lattice designs. Concealment demand will remain geographically concentrated but underscores a broader community-engagement imperative within the Peru telecom tower market.

The Lima metropolitan area commands around 34.68% of active sites and drives the highest tenancy ratios due to dense population clusters and robust commercial traffic. High rooftop penetration, mature fiber backhaul, and DAS deployments keep average revenue per site above the national mean, although permitting queues elongate delivery schedules.

Secondary coastal cities such as Arequipa, Trujillo, and Piura are the fastest-growing provincial hubs benefiting from mining investment and PPP infrastructure outlays. Movistar’s recent fiber push in Arequipa validates rising bandwidth demand, enabling TowerCos to lock in anchor tenants quickly. Grid reliability across these cities supports conventional power architectures, encouraging multi-tenant economics that reinforce the Peru telecom tower market expansion.

Amazon and Andean highland districts remain coverage white spaces characterized by complex terrain, sparse populations, and prohibitive grid extension costs. Internet Para Todos fiber spurs and satellite backhaul partnerships have reduced barriers, yet deployment still hinges on renewable-hybrid power packs and modular monopoles. As additional fiber nodes go live by 2026, the Peru telecom tower market should register incremental unit growth even in traditionally unserved territories.

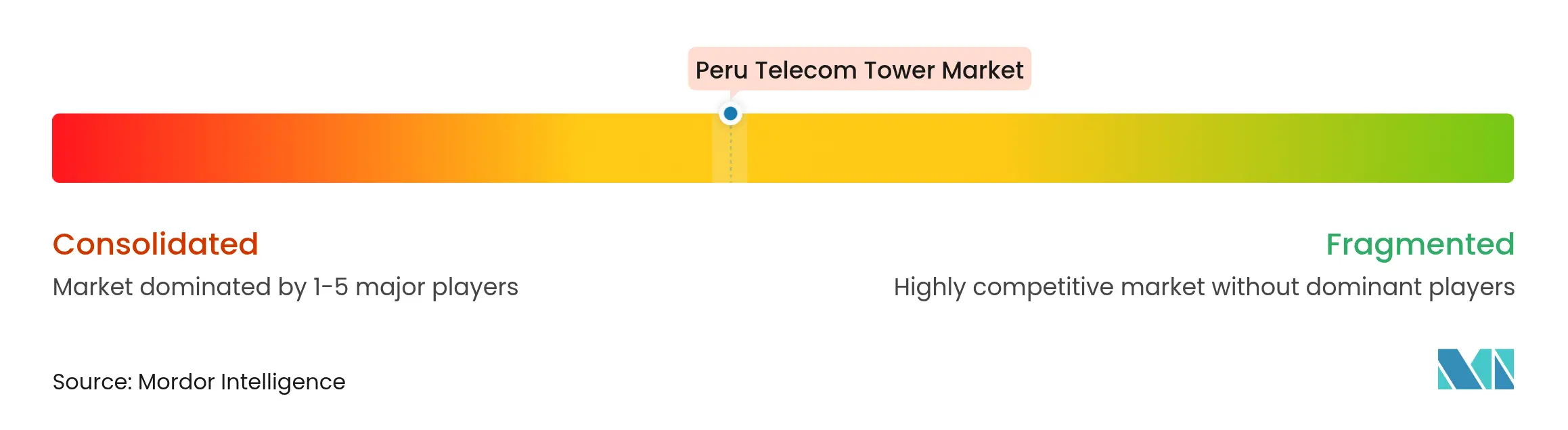

Market Concentration

The Peru telecom tower market exhibits moderate concentration. The competitive field hosts a balanced mix of global majors and regional specialists. American Tower and SBA Communications maintain radius-based portfolios clustered around Lima and Tier-2 coastal cities, capturing premium multi-tenant revenue streams. Phoenix Tower International and Andean Telecom Partners scale through sale-leaseback acquisitions, exemplified by ATP’s purchase of BTS Towers that added roughly 1,100 sites.

Competitive differentiation centers on speed-to-market, regulatory fluency, and sustainability credentials. Leaders deploy remote-monitoring SCADA, AI-driven energy optimization, and community-first engagement models to win municipal goodwill. Mid-tier players target regional strongholds or specialty verticals, such as mining or energy corridors, to avoid head-on competition.

Open-RAN pilots overseen by OSIPTEL could unlock disruptive entry points for agile newcomers, yet established incumbents defend their share through long-term master lease agreements and economies of scale.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The Report Covers Peru Telecom Tower Companies and the Market is Segmented by Ownership (Operator-Owned, Private-Owned, MNO Captive Sites), by Installation (Rooftop, Ground-Based), by Fuel Type (Renewable, Non-Renewable). The Market Sizes and Forecasts are Provided in Terms of Installed Base (in Thousand Units ) for all the Above Segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Deep-Dive Analysis of Feed Probiotics Across Key Regions

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.