Cambodia Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

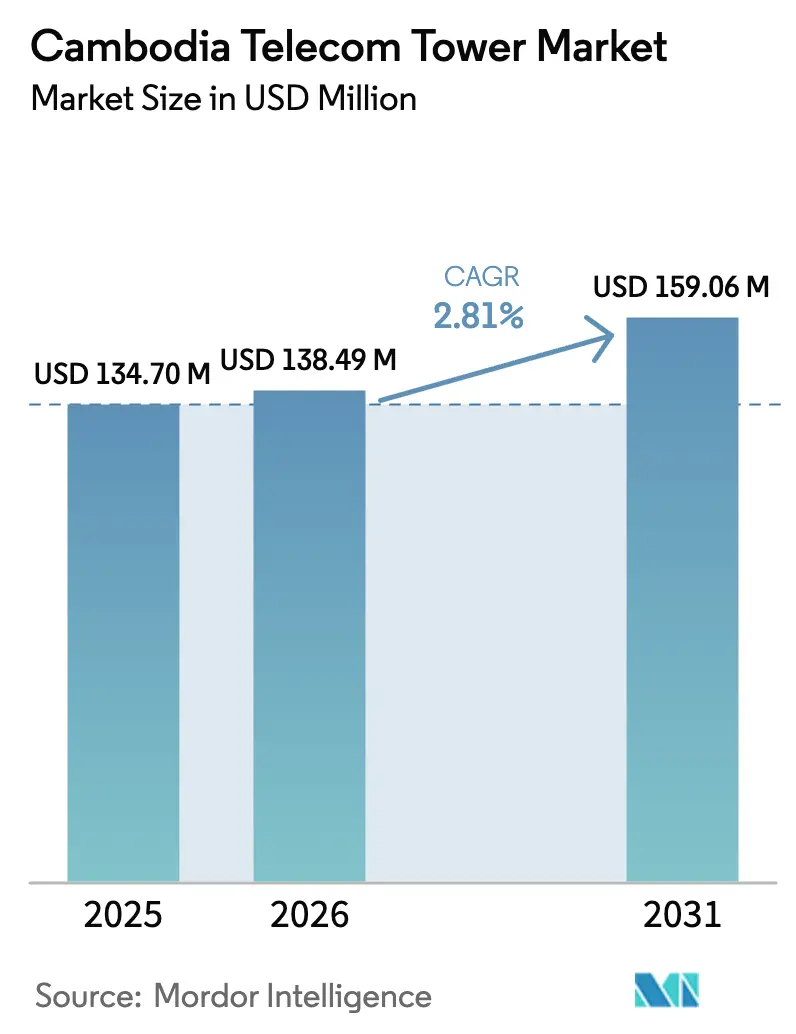

| Base Year Market Size (2025) | USD 134.70 Million |

| Market Size (2026) | USD 138.49 Million |

| Market Size (2031) | USD 159.06 Million |

| Growth Rate (2026 - 2031) | 2.81% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cambodia Telecom Tower Market Analysis by Mordor Intelligence

The Cambodia Telecom Tower Market size was valued at USD 134.70 million in 2025 and estimated to grow from USD 138.49 million in 2026 to reach USD 159.06 million by 2031, at a CAGR of 2.81% during the forecast period (2026-2031).

Sustained macro-economic growth, a young tech-savvy population, and rising smartphone adoption continue to fuel network investments, while government incentives ensure that tower assets remain pivotal to national digitalization plans. Operators are reallocating capital from bricks-and-mortar retail to network densification, increasing demand for multi-tenant sites that can host 4G upgrades and imminent 5G equipment. Independent tower companies now raise large volumes of long-term financing in international debt markets, easing balance-sheet pressure on mobile-network operators that must still fund spectrum fees. At the same time, solar-battery hybrid power solutions are becoming cost competitive, gradually reducing diesel-related operating risks and supporting environmental commitments.

Key Report Takeaways

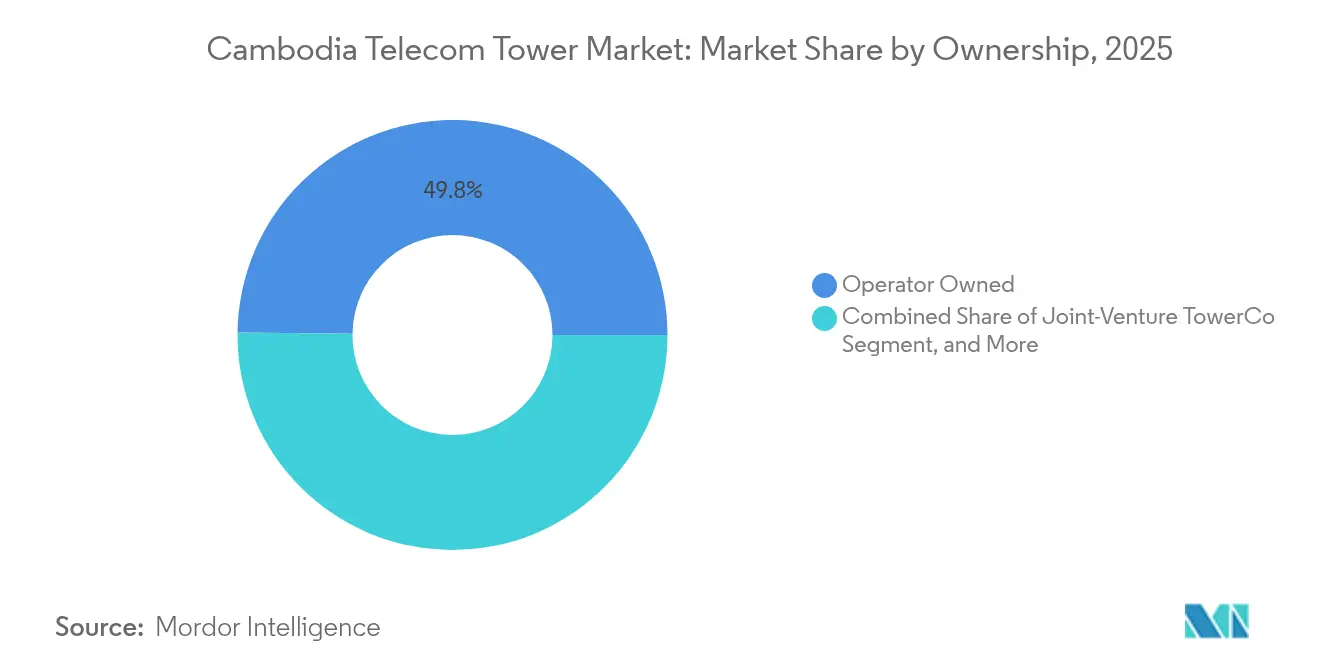

- By ownership, operator-held assets retained 49.82% of Cambodia telecom towers market share in 2025, while independent TowerCos are advancing at a 6.54% CAGR through 2031.

- By installation, ground-based structures captured 68.73% revenue share in 2025; rooftop deployments are forecast to expand at a 4.97% CAGR through 2031.

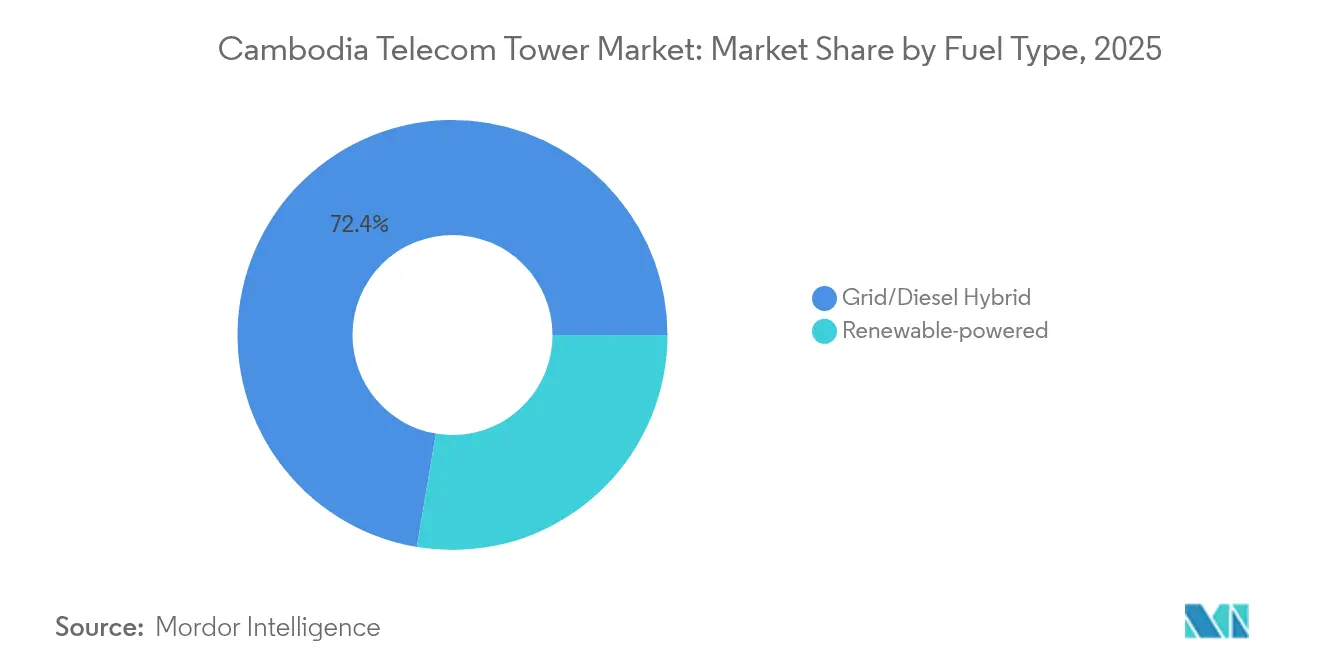

- By fuel type, grid-diesel hybrids accounted for 72.35% share of the Cambodia telecom towers market size in 2025 and renewable-powered sites are rising at a 10.29% CAGR to 2031.

- By tower type, lattice designs commanded 30.55% share of the Cambodia telecom towers market size in 2025 and stealth / concealed solutions are growing at a 7.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Cambodia Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 4G densification & 5G rollout financing surge | 1.5% | National, with urban concentration in Phnom Penh, Siem Reap, Sihanoukville | Medium term (2-4 years) |

| Rising mobile-data demand & smartphone uptake | 0.8% | National, strongest in urban centers | Short term (≤ 2 years) |

| Government "Digital Cambodia 2021-2035" infrastructure push | 0.4% | National, prioritizing rural connectivity | Long term (≥ 4 years) |

| MNO tower-asset divestment & new TowerCo capital inflows | 0.3% | National, concentrated in high-tenancy urban areas | Medium term (2-4 years) |

| Rural USO solar-micro-tower deployments | 0.2% | Rural areas, remote islands, demined regions | Long term (≥ 4 years) |

| Sub-marine cable landing hubs driving coastal colocation | 0.1% | Coastal regions, primarily Sihanoukville | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 4G Densification & 5G Rollout Financing Surge

Operators secured sizable credit lines, including Smart Axiata’s USD 50 million facility earmarked for 5G preparation, underscoring the capital intensity of next-generation upgrades. Urban cell sizes shrink by up to one-tenth under 5G, obliging network planners to triple site counts in downtown Phnom Penh. [1]Smart Axiata, “USD 50 Million Loan Agreement Signed,” smart.com.khStreamlined permits from the Ministry of Post and Telecommunications cut approval cycles to three months, lowering time-to-revenue for TowerCos. Robust steel lattice designs remain preferred because Cambodia’s monsoon climate demands high wind-load tolerance. Together these factors create predictable cash flows that appeal to global infrastructure funds entering the Cambodia telecom towers market.

Rising Mobile-Data Demand & Smartphone Uptake

Smartphone penetration surpassed 80% in 2024 and keeps climbing, pushing per-user data traffic to double-digit gigabyte levels each month. Metfone’s e-money platform posted 33% transaction growth, illustrating how digital services amplify bandwidth requirements. [2]Viettel Global, “FY 2024 Investor Presentation,” viettelglobal.vnVideo streaming peaks now strain urban macro cells, forcing operators to layer extra radios on existing lattice towers. Younger consumers—60% of Cambodians are under 30—make high-definition content and e-gaming integral to daily life, locking in structurally elevated data demand. Consequently, the Cambodia telecom towers market witnesses steady co-location orders that improve tenancy ratios for independent TowerCos.

Government “Digital Cambodia 2021-2035” Infrastructure Push

The Digital Cambodia blueprint earmarks public investment and incentives to close rural coverage gaps, assuring long-term policy support for new sites. Infrastructure-sharing mandates embedded in the plan enhance site utilization, lifting internal rates of return for third-party TowerCos. A dedicated fund under the Ministry finances backhaul and power upgrades in provinces where private cash flows remain thin. Clarity on right-of-way rules and transparent fee schedules reduce regulatory risk, making the Cambodia telecom towers market attractive to overseas investors.

MNO Tower-Asset Divestment & New TowerCo Capital Inflows

Operators increasingly monetize passive assets, mirroring regional patterns that unlocked billions elsewhere. edotco Cambodia, with group experience managing more than 55,000 sites, exemplifies globally benchmarked tower operations. Proceeds from sales backstop spectrum purchases, whereas TowerCos deploy fresh capital for site expansion. The stable inflation-linked lease model wins favor among pension and sovereign funds searching for predictable yields, injecting new liquidity into the Cambodia telecom towers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High diesel-power OPEX & fuel-price volatility | -0.6% | National, most severe in rural off-grid areas | Short term (≤ 2 years) |

| Complicated land-lease & permit processes | -0.4% | National, particularly challenging in rural and border areas | Medium term (2-4 years) |

| USD-denominated debt-service risk versus KHR revenue | -0.3% | National, affecting all leveraged tower operators | Medium term (2-4 years) |

| Security scrutiny of Chinese 5G RAN supply chain | -0.2% | National, concentrated in urban 5G deployment areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Diesel-Power OPEX and Fuel-Price Volatility

Petroleum imports rose 18% year-over-year to USD 1.663 billion during January–August 2024, inflating generator costs for roughly 40% of rural towers. Off-grid sites can spend triple the energy budget of grid-connected peers, eroding margins and complicating lease-rate negotiations. Seasonal floods disrupt fuel logistics, raising the specter of service outages. While solar-battery hybrids now approach break-even within seven years, the initial capex still constrains operators carrying USD-linked debt, reinforcing the near-term drag on the Cambodia telecom towers market.

Complicated Land-Lease and Permit Processes

Fragmented land-title records prolong negotiations, especially in provinces with informal tenure systems. Standard deployments can slip from the statutory three-month target to a year when multiple sign-offs are required at commune, district, and provincial levels. Foreign TowerCos cannot own land outright, forcing lease or joint-venture structures that add legal complexity and incremental cost. [3]Telecommunication Regulator of Cambodia, “Guidelines on Permit Procedures,” trc.gov.khSmaller firms lacking in-house regulatory teams find it tougher to scale, which tempers the immediate growth of the Cambodia telecom towers market despite robust demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Gain Momentum

Independent players grew revenue at 6.54% CAGR through 2031 even though operator portfolios still held 49.82% Cambodia telecom towers market share in 2025. The sale-and-lease-back model helps MNOs recycle capital into spectrum bids, while TowerCos push tenancy ratios past 1.8x on prime urban sites. edotco Cambodia applies predictive maintenance systems that cut downtime to under 0.5 hours per month, enhancing service-level agreements. Joint-venture structures also emerge, blending local permitting know-how with international funding to accelerate roll-outs.

Capital availability underpins this ownership shift. Domestic banks seldom fund long-dated infrastructure, yet global credit investors now accept Cambodia country risk, pricing 10-year paper near regional comparables. These flows support competitive bids for MNO portfolios, creating a deeper secondary market for passive assets. Consequently, the Cambodia telecom towers market sees quicker site acquisitions and more uniform engineering standards than during the early operator-built era.

By Installation: Rooftop Solutions Scale in Dense Cities

Ground-based masts retained 68.73% of 2025 revenue because rural coverage still relies on 40-60 meter lattice towers. However, rooftops are advancing at 4.97% CAGR as landlords in Phnom Penh and Sihanoukville strike multi-year lease packages bundled with building-management services. Rooftop permits are simpler, needing fewer environmental clearances, which trims cycle times by two months. Shorter 20-meter poles suffice for 5G small cells that aim for street-level signal quality.

The Cambodia telecom towers market benefits when operators offload rooftop scouting to specialized micro-TowerCos that aggregate rights across commercial malls and hotels. This aggregation cuts negotiation friction and ensures load-bearing audits comply with safety codes. For suburban coverage, ground sites remain optimal, but hybrid portfolios blending both installation types now define best-practice network architecture.

By Fuel Type: Solar Hybrids Start to Displace Diesel

Grid-diesel hybrids delivered 72.35% of 2025 revenue, reflecting historical grid unreliability. Yet renewable-powered towers post the fastest 10.29% CAGR through 2031 because average solar-panel prices fell below USD 0.20 per watt, halving since 2020. Solar irradiation of 4.5-5.0 kWh/m²/day allows 6 kW arrays to support 24/7 operations when coupled with lithium-ion storage. Pay-back periods now compress to under seven years, below typical concession tenures, boosting bankability.

Multilateral lenders co-finance rural solar conversions, bundling grants that cut equity requirements. Operators report carbon-footprint reductions surpassing corporate targets, strengthening ESG credentials vital to international investors. Even so, diesel remains indispensable for deep-rural backup because high-capacity batteries add weight and raise tower load considerations. Hence, the Cambodia telecom towers market is likely to operate dual-fuel models through the forecast horizon.

By Tower Type: Stealth Designs Meet Urban Rules

Lattice structures captured 30.55% revenue in 2025 owing to superior multi-tenant capacity. Urban planning committees increasingly mandate stealth or concealed formats, pushing that category to a 7.31% CAGR. Fake palm trees and integrated street-light poles help new sites win community acceptance in heritage precincts such as Siem Reap. Monopoles fill suburban coverage gaps where narrow road reserves constrain lattice footprints.

Advanced corrosion-resistant coatings mitigate Cambodia’s humid climate, extending life cycles to 30 years even for coastal installations exposed to salt spray. Guyed towers remain economical in provinces with abundant land, but the additional anchoring area limits adoption near expanding city fringes. Overall, varied tower formats enable operators to tailor solutions per site, reinforcing diversification within the Cambodia telecom towers market.

Geography Analysis

Phnom Penh hosts nearly 35% of national sites despite housing just 15% of the population, underscoring economic centralization. Coastal Preah Sihanouk benefits from Malaysia-Cambodia-Thailand submarine cable landings that raise bandwidth demand and enhance tenancy economics for colocation providers. Secondary cities such as Battambang and Siem Reap attract incremental investment on the back of tourism and agro-processing clusters, adding mid-height monopoles to local skylines.

Rural provinces challenge operators with sparse populations and low grid density. The Universal Service Obligation fund subsidizes tower builds on remote islands in Tonle Sap Lake, underwriting solar micro-tower pilots that showcase off-grid viability. Flood-prone Mekong Delta districts require elevated platform bases, raising capex per site by up to 12%. Border areas offer cross-border roaming traffic yet suffer from heritage land-mine contamination, necessitating specialized demining surveys prior to foundation works.

Northern highlands record the lowest tenancy but hold strategic value for future fiber corridors linking Laos and Vietnam. TowerCos therefore adopt portfolio strategies balancing high-yield urban sites with concession-supported rural builds, smoothing aggregated cash flows across the Cambodia telecom towers market.

Competitive Landscape

Market concentration remains moderate. edotco Cambodia leverages regional scale to secure bulk equipment discounts and deploy remote-monitoring IoT sensors that cut field visits by 15%. Local challenger Cam TowerLink differentiates on custom rooftop solutions bundled with property-management services, capturing mid-tier landlords. Global Tower Corporation entered in 2024 with a USD 19.97 million contract to erect 400 sites, signaling growing competitive intensity.

Strategic alliances are proliferating. Cellcard partners with solar integrators to retrofit diesel sites, whereas Smart Axiata explores neutral-host in-building systems for malls. Technology adoption—predictive analytics for structural health and AI-driven energy optimization—creates fresh differentiators. Rising compliance costs from tighter SIM registration rules imposed by TRC drive smaller firms to seek mergers, setting the stage for consolidation that could lift the Cambodia telecom towers market concentration in coming years.

Cambodia Telecom Tower Industry Leaders

EDOTCO (CAMBODIA) CO., LTD.

Metfone

Telemobile (Cambodia) Corporation

GLOBAL TOWER CORPORATION PTY LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: SpaceX Starlink delegation met Prime Minister Hun Manet to discuss satellite connectivity investments, hinting at future competition for terrestrial towers.

- March 2024: Smart Axiata appointed Ziad Shatara as CEO to steer 5G rollout.

- April 2024: JICA concluded a digital ecosystem assessment highlighting infrastructure gaps.

- March 2024: UNDP extended solar mini-grids supporting off-grid towers.

Cambodia Telecom Tower Market Report Scope

Telecom towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Cambodia telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO Captive sites), by installation (rooftop, and ground-based), and by fuel type (renewable and non-renewable). The Market Sizes and Forecasts are Provided in Terms of Installed Base (in Thousand Units) for all the Above Segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the Cambodia telecom towers market in 2026?

It is valued at USD 138.49 million in 2026 and is forecast to grow at a 2.81% CAGR to USD 159.06 million by 2031.

Which segment is expanding fastest within tower ownership?

Independent TowerCos show the highest growth with a 6.54% CAGR as operators divest passive assets to fund 5G spectrum.

Why are rooftop towers gaining traction?

Urban densification in Phnom Penh and Sihanoukville favors rooftop sites that avoid land acquisition, cutting deployment time and cost.

What is driving the shift toward renewable-powered towers?

Declining solar costs and government incentives make solar-battery hybrids commercially viable, especially for off-grid rural locations.

How does diesel price volatility impact tower operators?

Rising diesel costs inflate operating expenses at off-grid sites, prompting TowerCos to adopt solar hybrids to stabilize cash flows.

Who are the major competitive players in Cambodia?

Edotco Cambodia, Metfone, Smart Axiata, Cam TowerLink, and Global Tower Corporation together control the majority of active infrastructure.edotco Cambodia, Metfone, Smart Axiata, Cam TowerLink, and Global Tower Corporation together control the majority of active infrastructure.

Page last updated on: