Chile Telecom Tower Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

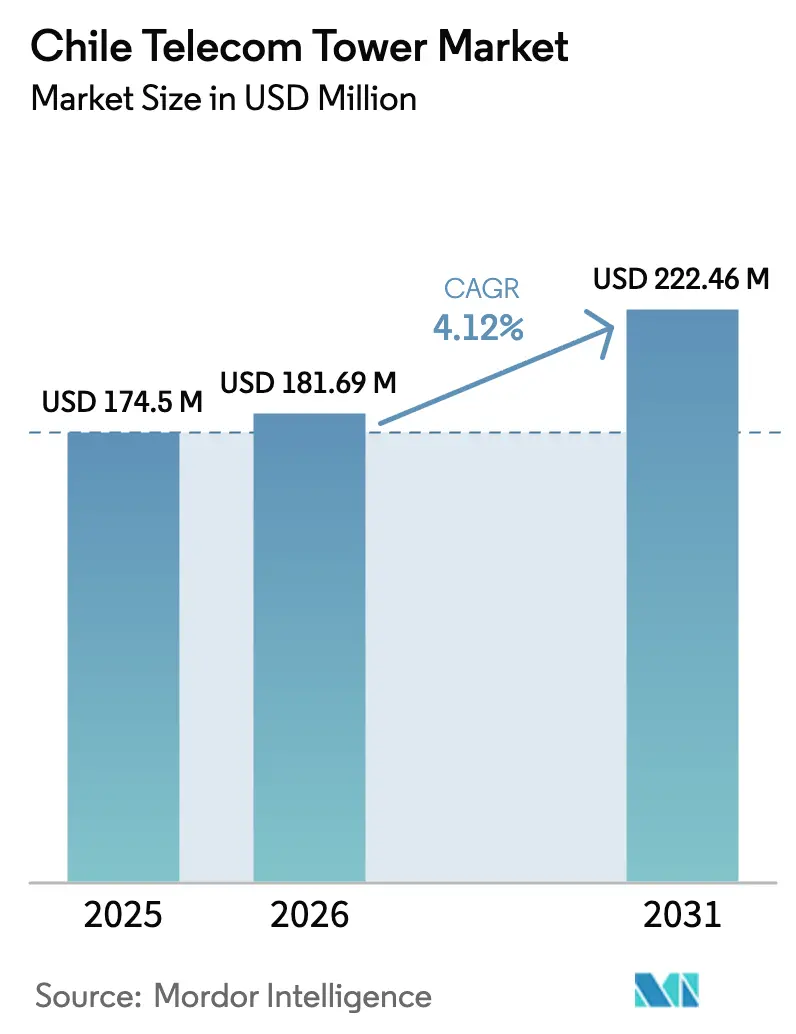

| Base Year Market Size (2025) | USD 174.5 Million |

| Market Size (2026) | USD 181.69 Million |

| Market Size (2031) | USD 222.46 Million |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

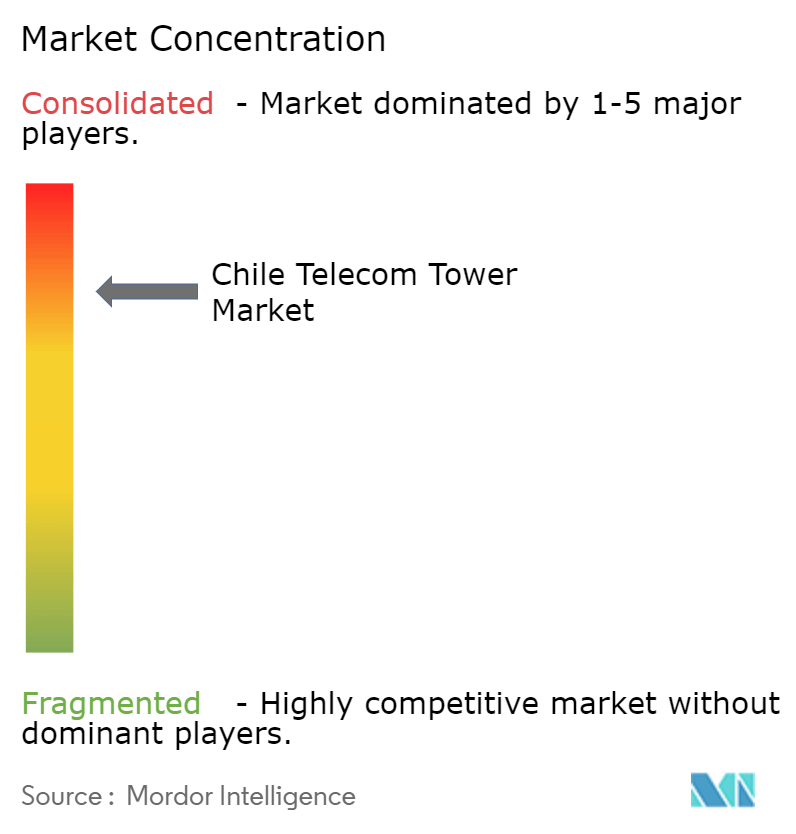

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Telecom Tower Market Analysis by Mordor Intelligence

The Chile Telecom Tower Market size was valued at USD 174.5 million in 2025 and estimated to grow from USD 181.69 million in 2026 to reach USD 222.46 million by 2031, at a CAGR of 4.12% during the forecast period (2026-2031).

Sustained network densification to support 5G coverage, operator migration to asset-light models, and robust submarine-cable investments underpin this steady expansion. Independent TowerCos now dominate ownership as operators monetize passive assets, while tower demand from private-LTE deployments in mining and port zones raises average lease rates. Rooftop installations, renewable-powered sites, and stealth structures are growing fastest, each benefiting from urban densification needs and stringent municipal aesthetics. At the same time, regulatory bottlenecks, land-lease inflation, and Chile’s seismic-design premiums continue to compress margins.

Key Report Takeaways

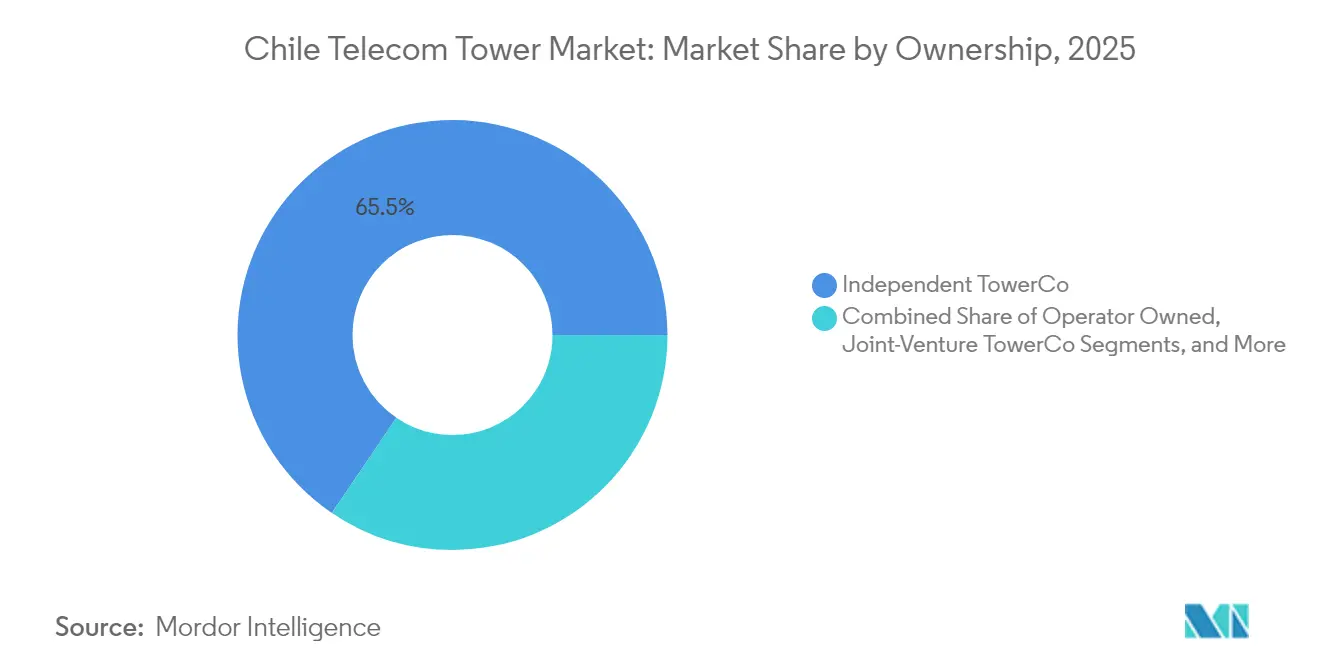

- By ownership, independent TowerCos led with 65.52% revenue share in 2025, and this segment is advancing at a 5.52% CAGR through 2031.

- By installation, ground-based structures held 55.72% of the Chile telecom towers market share in 2025, whereas rooftop deployments are projected to expand at 5.6% CAGR to 2031.

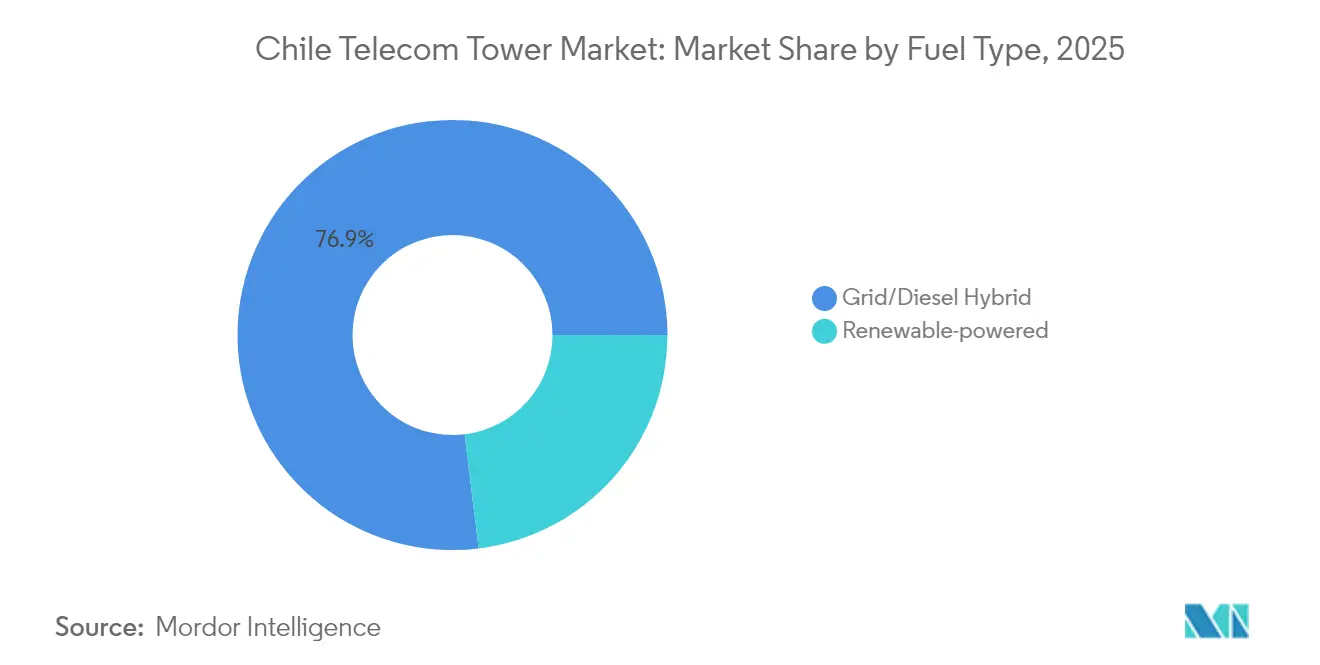

- By fuel type, grid/diesel hybrid sites accounted for 76.94% of the Chile telecom towers market size in 2025, while renewable-powered nodes are growing at an 17.62% CAGR over the same period.

- By tower type, monopoles captured 49.98% of revenue in 2025 and stealth towers are on track for a 7.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Telecom Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum-driven densification wave | +1.2% | National; early momentum in Santiago, Valparaíso | Medium term (2-4 years) |

| Rapid mobile-data consumption growth | +0.8% | National; urban centers | Short term (≤ 2 years) |

| Universal-service fibre and rural subsidies | +0.6% | Rural regions nationwide | Long term (≥ 4 years) |

| Enterprise private-LTE in mining & ports | +0.4% | Atacama, Valparaíso, Antofagasta | Medium term (2-4 years) |

| 700-site BTS pipeline from MNO carve-outs | +0.3% | National | Short term (≤ 2 years) |

| Cross-border fibre-to-tower backhaul | +0.2% | Central Chile; Argentina border | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G spectrum-driven densification wave

SUBTEL’s 5G coverage mandates require operators to triple or quadruple site density relative to 4G networks. Entel has earmarked USD 618 million for 2024 upgrades that include macro and small-cell sites to meet these obligations. Higher-frequency bands with limited propagation increase the value of rooftop and concealed locations that can enhance urban capacity. TowerCos benefit from mandated infrastructure sharing that boosts colocation ratios, raising tenancy revenue. As operators prioritize quick rollouts to secure first-mover advantage, build-to-suit agreements accelerate, shortening payback cycles for independent owners. [1]SUBTEL, “Plan Nacional de Espectro 5G,” subtel.cl

Rapid mobile-data consumption growth

Mobile data traffic in Chile has been expanding at more than 30% yearly, fueled by streaming, cloud workflows, and a near-saturated smartphone base. Urban congestion pushes operators to acquire additional tower slots and upgrade backhaul. In mining corridors, IoT telemetry and remote operations create continuous throughput demand that differs from consumer peak-hour patterns. This sustained usage growth keeps tower utilization high and supports incremental lease amendments for higher antenna loads. [2]Entel, “2024 Investment Plan,” entel.cl

Universal-service fibre and rural connectivity subsidies

Fondo de Desarrollo de las Telecomunicaciones (FDT) programs extend backbone fibre to remote areas yet still rely on wireless links for distribution in difficult terrain. The Curie and Humboldt submarine cables land in Valparaíso, requiring terrestrial towers for inland data distribution. Subsidized rural towers often operate on solar-hybrid power because of grid scarcity, aligning with national carbon goals. Government-backed contracts run longer terms and feature reliable payment schedules, improving cash-flow visibility for TowerCos that serve these zones.

Enterprise private-LTE in mining and ports

BHP, Codelco, and other miners are adopting private LTE networks to automate haulage and enhance safety, contracting bespoke towers with ruggedized designs. Lease rates in these industrial sites exceed nationwide averages because service-level guarantees are critical to production uptime. Nokia’s partnership with Claro for port connectivity shows MNOs pursuing enterprise verticals that demand dedicated infrastructure footprints. Multi-year agreements with expansion clauses provide TowerCos with stable, high-margin revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal permit bottlenecks (Ley 20.599) | -0.7% | National; most acute in Santiago | Short term (≤ 2 years) |

| High land-lease inflation | -0.5% | Santiago, Antofagasta | Medium term (2-4 years) |

| Direct-to-cell LEO satellites | -0.3% | Rural regions nationwide | Long term (≥ 4 years) |

| Seismic-resilience CAPEX premium | -0.2% | National; intensified in high-risk zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Municipal permit bottlenecks under Ley 20.599

Environmental assessments average 985 days, elevating capital carrying costs and discouraging smaller entrants. Multiple municipal agencies layer aesthetic and zoning conditions that particularly delay rooftop and stealth projects in dense districts. SUBTEL has begun digitizing approval workflows, yet uneven municipal adoption sustains unpredictability. Larger TowerCos mitigate this drag with dedicated regulatory teams and pre-negotiated design templates, while new entrants face steep compliance learning curves.

High land-lease inflation in Santiago and Antofagasta

Commercial land values in these high-demand zones have outpaced general inflation, squeezing operating margins. Mining-boom dynamics add volatility in Antofagasta, where industrial landlords push short lease cycles with steep escalators. TowerCos respond by bundling multi-site agreements and exploring co-location on existing structures to contain costs. Extended lease terms with cap-and-collar escalation clauses are becoming standard practice, though they reduce portfolio flexibility. [3]SUBTEL, “Ley de Antenas Implementation Report,” subtel.cl

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos consolidate the landscape

Independent TowerCos controlled 65.52% of revenue in 2025. Their portfolio scale and operational specialization enable lease-up ratios that surpass operator-owned assets, helping the segment grow at a 5.52% CAGR through 2031. The 2024 acquisition of 3,800 WOM sites by Phoenix Tower International highlighted the ongoing shift from captive ownership to professional infrastructure management. Joint-venture TowerCos allow MNOs to offload CAPEX while retaining some strategic influence, yet this model remains nascent. Operator-owned sites persist where rapid tactical builds or critical network control is essential, but the trend favors divestiture as balance-sheet discipline intensifies.

Lease-up economics attract private capital, and amortized build cost per tenant falls sharply when independent owners can secure second and third tenants. As a result, the Chile telecom towers market delivers predictable cash yields that align with infrastructure-fund return hurdles. Portfolio-level energy-efficiency upgrades and centralized maintenance further widen the cost gap against legacy captive assets. Taken together, ownership patterns will continue reinforcing TowerCo dominance while MNOs redirect resources toward spectrum and service innovation.

By Installation: Rooftop deployments accelerate urban coverage

Ground-based installations carried 55.72% of the Chile telecom towers market share in 2025, reflecting their role in national coverage grids. Yet rooftop nodes, projected to grow 5.6% annually to 2031, are critical for 5G capacity in Santiago’s high-rise corridors. Rooftop leases avoid some environmental scrutiny and shorten deployment cycles, although structural load assessments and landlord negotiations add new complexities. Lease pricing per tenant is higher because site counts remain constrained by building suitability, and proprietary rooftop portfolios can command premium valuations.

Ground sites remain indispensable for rural macro coverage and high-power broadcast functions. In mining belts, tall self-supporting towers integrate microwave backhaul and redundant power, supporting harsh-environment SLAs. Hybrid deployment models—ground macro for umbrella coverage and rooftop small cells for capacity—optimize network performance and drive multi-tier tenancy revenue across the Chile telecom towers market.

By Fuel Type: Renewable energy transforms power economics

Grid/diesel hybrid units accounted for 76.94% of the Chile telecom towers market size in 2025. Diesel redundancy is still vital for uptime, but fuel logistics in remote Andes and desert regions inflate opex. Solar-hybrid systems are gaining momentum at an 17.62% CAGR as Chile’s solar irradiation ranks among the world’s highest. TowerCos install modular photovoltaic arrays with lithium-ion storage to secure 99.5% availability while cutting diesel runs by up to 80%. Public sustainability goals and investor ESG mandates accelerate this transition.

Renewable adoption is also propelled by Chile’s carbon-tax framework, which prices diesel consumption into operational budgets. Energy-as-a-service providers guarantee performance and handle maintenance, mitigating technical risk for TowerCos. Larger portfolios gain scale advantages in equipment procurement and monitoring, reinforcing competitive positioning while advancing national decarbonization targets.

By Tower Type: Stealth solutions meet urban aesthetics

Monopoles held 49.98% of revenue in 2025 thanks to their cost efficiency, standard engineering, and relatively swift permitting. Stealth or concealed designs, however, are expanding at 7.21% CAGR as municipalities insist on minimal visual impact in heritage districts and tourist zones. These structures integrate antennas within streetlamps, chimneys, or architectural cladding, commanding lease premiums that offset higher fabrication costs.

Lattice towers remain essential where height and load capacity trump footprint and aesthetics, namely along inter-regional highways or power corridors. Guyed masts, although inexpensive, consume larger parcels and therefore see declining urban relevance. Emerging wooden and composite-fiber systems promise lighter weight and faster assembly, offering a potential middle path between standard monopoles and custom stealth formats.

Geography Analysis

The Santiago metropolitan area accounts for the largest concentration of active tenancies and yields the highest revenue per tower in the Chile telecom towers market. Dense high-rise clusters demand rooftop and short monopole installations that minimize visual intrusion while maximizing capacity. Colocation ratios in central Santiago average above two tenants per site, raising recurring revenue.

Northern mining corridors spanning Atacama and Antofagasta provinces represent the premium segment for specialized industrial towers. Enterprise contracts here bundle priority maintenance, ruggedized hardware, and high-throughput microwave backhaul. Average lease rates can exceed urban benchmarks because downtime directly impacts multimillion-dollar production schedules. Renewable-powered macro sites reduce diesel logistics costs across desert expanses that lack reliable grid feeds.

Southern regions, from Bío-Bío to Los Lagos, exhibit lower population density and higher deployment costs tied to mountainous terrain and forestry zones. Government rural-connectivity grants stimulate deployments that might otherwise be commercially marginal. Cross-border fibre routes near Paso Los Libertadores position central Chile as a redundancy hub for Argentine traffic, generating incremental tower demand along highways and rail corridors that parallel new fibre conduits.

Competitive Landscape

The market is moderately concentrated. American Tower, Phoenix Tower International, and SBA Communications collectively operate a majority share of active tenancies. Phoenix Tower’s 2024 WOM portfolio purchase materially expanded its footprint, signaling ample headroom for further operator carve-outs. American Tower leverages regional purchasing scale to standardize equipment and drive down maintenance costs, while SBA embeds advanced remote-monitoring to reduce truck rolls.

Regional specialist Andean Telecom Partners focuses on hybrid macro-tower and fibre offerings that cater to cross-border and multi-lat latency-sensitive applications. Torres Unidas targets rooftop and stealth assets that serve mid-tier MNOs seeking flexible urban capacity. Competitive differentiation increasingly turns on energy efficiency, speed-to-market, and regulatory navigation rather than mere asset count.

Strategic moves in 2024-2025 have tilted toward green-power retrofits and industrial-sector service bundles. TowerCos collaborate with solar integrators to lock in predictable opex and meet tenant sustainability metrics. Others pilot edge-compute cabinets at tower bases to capitalize on low-latency use cases. M&A appetite remains healthy because incremental scale still delivers cost synergies across maintenance, insurance, and network-operations control centers.

Chile Telecom Tower Industry Leaders

American Tower Chile

Phoenix Tower International Chile

Andean Telecom Partners

SBA Communications Chile

Torrecom

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: WOM Chile completed its exit from Chapter 11 bankruptcy with creditors taking controlling interest for USD 1.6 billion.

- February 2025: SUBTEL and CAF commissioned a feasibility study for a submarine cable from continental Chile to Antarctica, expected by Apr 2026.

- February 2025: Claro Chile began a nationwide mobile-network renewal program aimed at elevating customer experience.

- December 2025: OnNet Chile divested a portion of its FTTH network to CMB LV Digital Infra I, affecting 370,000 homes passed.

Chile Telecom Tower Market Report Scope

Telecom towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Chile telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO Captive sites), by installation (rooftop, and ground-based), and by fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of installed base (Thousand Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the Chile telecom towers market in 2026?

The market stands at USD 181.69 million in 2026 and is on track to reach USD 222.46 million by 2031.

What is the main growth driver for new tower builds?

Mandatory 5G coverage obligations that demand three to four times more sites than legacy 4G grids.

Which ownership model holds the largest share?

Independent TowerCos lead with 65.52% of revenue in 2025, reflecting operators’ shift to asset-light strategies.

Why are rooftop installations expanding quickly?

Urban densification and 5G small-cell requirements favor rooftop sites that shorten coverage gaps in high-rise districts.

How are TowerCos addressing power-cost inflation?

They are adopting solar-hybrid systems that cut diesel use and align with national carbon-reduction policies.

What restrains faster network expansion?

Lengthy municipal permitting under Ley 20.599 and steep land-lease inflation in Santiago and Antofagasta.

Page last updated on: