Enterprise Mobile Application Development Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

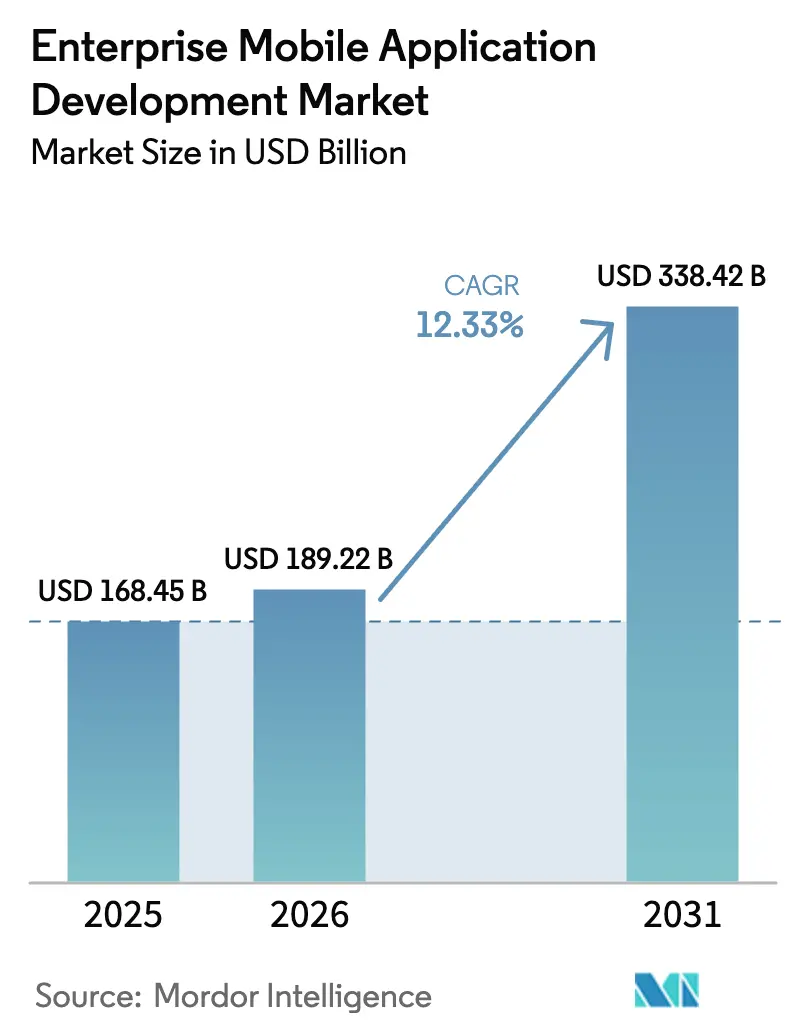

| Market Size (2026) | USD 189.22 Billion |

| Market Size (2031) | USD 338.42 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

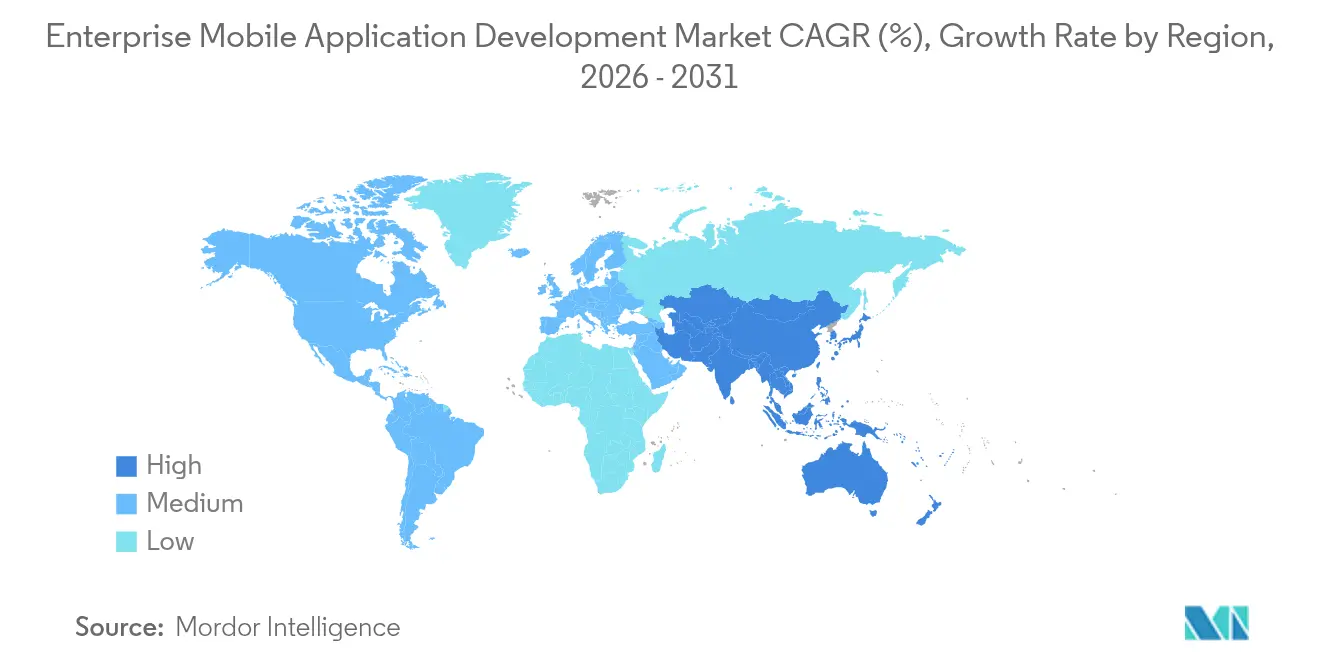

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Mobile Application Development Market Analysis by Mordor Intelligence

Enterprise Mobile Application Development market size in 2026 is estimated at USD 189.22 billion, growing from 2025 value of USD 168.45 billion with 2031 projections showing USD 338.42 billion, growing at 12.33% CAGR over 2026-2031. Widespread mobile-first mandates, fast-maturing cloud-native development platforms, and the surging popularity of low-code and no-code tooling continue to propel spending. Business leaders view mobile apps not as optional add-ons but as essential front ends for digitized processes, especially as bring-your-own-device (BYOD) programs accelerate. Cloud deployment dominates thanks to consumption-based pricing, automated scaling, and tight linkage with AI and analytics services. At the same time, developer skill shortages and tightening security expectations are amplifying demand for visual development environments that shorten delivery cycles without sacrificing governance. Competition remains moderate; established enterprise-software providers leverage their ecosystems, while specialist vendors differentiate through edge-AI features and accessibility compliance.

Key Report Takeaways

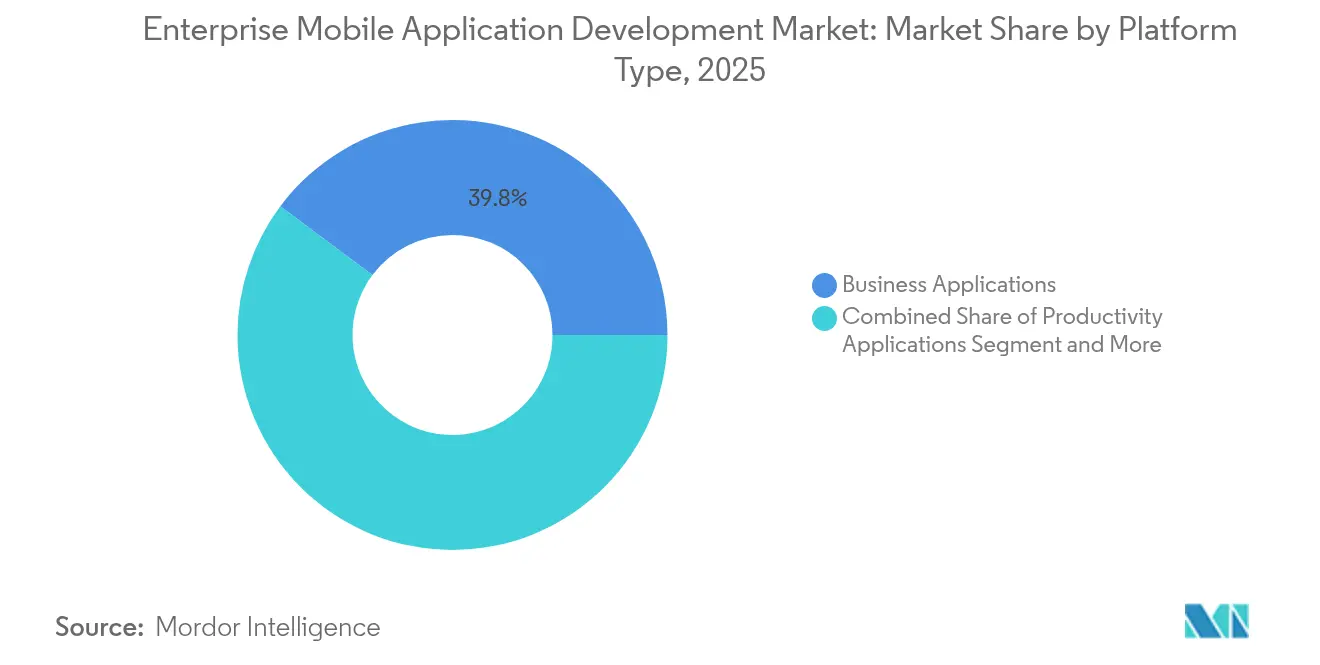

- By platform type, business applications led with 39.78% of the enterprise mobile application development market share in 2025, whereas field-service applications are projected to expand at a 15.02% CAGR through 2031.

- By deployment model, cloud solutions captured 67.92% revenue share in 2025 and are advancing at a 14.12% CAGR to 2031.

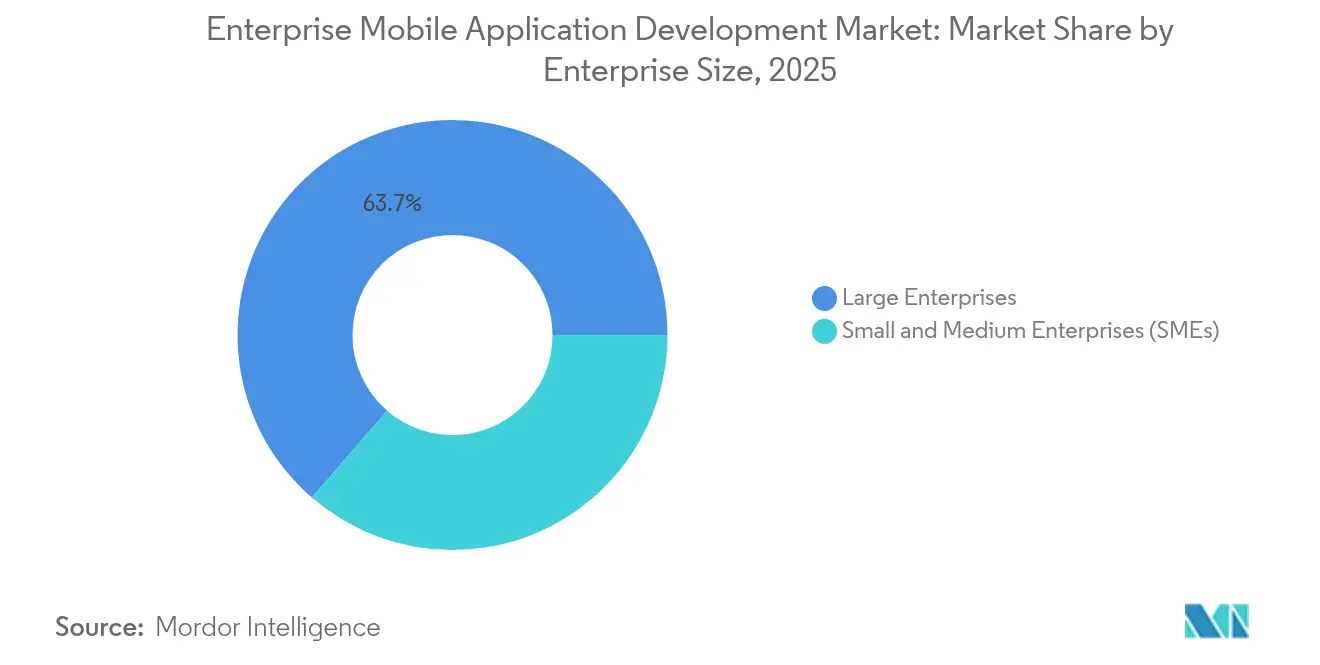

- By enterprise size, large enterprises accounted for 63.65% of the enterprise mobile application development market size in 2025, yet small and medium enterprises post the fastest growth at a 15.29% CAGR.

- By industry vertical, IT and telecommunications held a 28.22% share in 2025; retail and e-commerce are forecast to grow at a 14.35% CAGR through 2031.

- By geography, North America remained the largest region with a 37.95% share in 2025, while Asia-Pacific shows the highest 14.88% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Mobile Application Development Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of mobile devices and BYOD culture | +2.8% | Global, with strongest impact in North America and EU | Medium term (2-4 years) |

| Emergence of cloud-native MADP and mPaaS offerings | +2.1% | Global, particularly APAC and North America | Short term (≤ 2 years) |

| Surge in low-code/no-code platforms for faster time-to-value | +1.9% | Global, with early adoption in North America and EU | Short term (≤ 2 years) |

| Enterprise-wide digital-transformation mandates | +1.7% | Global, with accelerated adoption in APAC | Medium term (2-4 years) |

| Edge-AI inference enabling offline intelligent apps | +1.4% | North America and EU initially, expanding to APAC | Long term (≥ 4 years) |

| Accessibility-compliance (WCAG 3.0) modernisation push | +0.8% | North America and EU primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Mobile Devices and BYOD Culture

More than 80% of enterprises now permit employee-owned smartphones and tablets, turning personal devices into primary work terminals and expanding the addressable user base for internal mobile apps. [1]Menlo Security, “The key to securing BYOD access to applications and providing visibility,” menlosecurity.com Security investment has followed suit, with 84% of organizations boosting mobile protection budgets in 2024. Development teams are therefore prioritizing cross-platform frameworks that deliver consistent experiences across diverse hardware while integrating enterprise-grade identity controls. Zero-touch enrollment and remote-wipe capabilities are increasingly embedded, reducing IT overhead and enabling faster rollouts. As employees blur work-life usage patterns, intuitive consumer-style interfaces are becoming standard even for back-office functions. Collectively, these trends support the sustained expansion of the enterprise mobile application development market.

Emergence of Cloud-Native MADP and mPaaS Offerings

Cloud-native mobile application development platforms (MADP) and mobile platform-as-a-service (mPaaS) solutions shift development from resource-intensive on-premise stacks to elastic infrastructure. Alibaba Cloud’s mPaaS illustrated the model’s resilience when the 12306 ticketing app handled holiday traffic spikes without service degradation. [2]Alibaba Cloud, “mPaaS: Reconstructing User Experience with Technology,” alibabacloud.com Containerized microservices and API-first architectures provide modularity, allowing independent feature teams to release updates in hours rather than weeks. Enterprises also sidestep capital expenditure, paying only for consumed resources. The approach integrates naturally with DevOps pipelines and automated testing, further compressing release cycles. As a result, the enterprise mobile application development market is tilting decisively toward cloud deployment.

Surge in Low-Code/No-Code Platforms for Faster Time-to-Value

Analysts estimate low-code and no-code tools already account for over 65% of mobile-app development tasks, a figure Gartner expects to climb as citizen-developer programs mature. Visual drag-and-drop interfaces allow business users to assemble workflows, while IT teams embed connectors that enforce governance and security. Enterprises report 50–70% cycle-time reductions compared with hand-coding, enabling rapid prototyping of customer-facing features. Native integration with major SaaS platforms also minimizes custom API work. These efficiency gains are particularly attractive for small and medium enterprises chasing aggressive launch timelines, spurring additional growth in the enterprise mobile application development market.

Enterprise-Wide Digital-Transformation Mandates

Mobile apps sit at the heart of broader modernization efforts as companies digitize legacy processes. Asia-Pacific’s mobile economy added USD 880 billion to regional GDP in 2023, underscoring the macroeconomic stakes. Internal field-force automation, mobile ordering, and real-time inventory visibility are now baseline expectations. Regulators increasingly accept mobile records as compliant audit trails, further legitimizing app-centric workflows in healthcare and financial services. Senior leadership, therefore, allocates budget to platforms that blend low-code speed with robust integration hooks, reinforcing the virtuous cycle behind enterprise mobile application development market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and complexity of securing multi-platform apps | -1.8% | Global, particularly acute in regulated industries | Short term (≤ 2 years) |

| Shortage of skilled mobile developers | -1.5% | Global, most severe in North America and EU | Medium term (2-4 years) |

| Legacy back-end technical debt hindering composable architectures | -1.2% | Global, especially in established enterprises | Long term (≥ 4 years) |

| Energy-consumption scrutiny and sustainability mandates on SDKs | -0.7% | EU and North America primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Complexity of Securing Multi-Platform Apps

Threat actors increasingly exploit reverse-engineering and bot attacks to steal credentials or poison APIs, forcing enterprises to embed advanced attestation routines. Google’s Play Integrity API and Apple’s App Attest raise the security bar but require specialist skills, inflating project budgets. Regulated sectors add mandatory encryption and audit logging layers, compounding cost. While cross-platform frameworks boost productivity, they also widen the attack surface because identical vulnerabilities propagate across iOS and Android builds. Continuous monitoring and zero-trust architectures mitigate risk but demand ongoing investment, tempering short-term growth for the enterprise mobile application development market.

Shortage of Skilled Mobile Developers

Competition for experienced Kotlin, Swift, and cross-platform engineers remains intense. Salary surveys show compensation outpacing general IT averages as enterprises pursue parallel AI, 5G, and edge-computing initiatives. The talent crunch extends to UX designers and API-integration specialists who understand mobile constraints. Organizations plug gaps with offshore teams and by empowering citizen developers, yet onboarding and knowledge transfer lengthen schedules. Vendor platforms that embed code-generation and reusable templates partially offset the shortfall but cannot fully replace seasoned architects, creating a persistent drag on the enterprise mobile application development market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Business Applications Anchor Spending but Field-Service Apps Accelerate

Business applications represented 39.78% of 2025 revenue, underscoring their pivotal role in automating internal workflows across finance, HR, and supply-chain operations. Their dominance in the enterprise mobile application development market stems from deep integration with ERP and CRM back ends, enabling data-driven decision-making. Recent launches such as ServiceNow’s Connected Worker suite demonstrate how mobile dashboards support real-time manufacturing analytics. Field-service applications are, however, posting the fastest 15.02% CAGR as utilities and telecom operators equip remote technicians with AI-guided maintenance tools. Integration of 5G and edge-AI lets these apps operate offline while syncing nuanced sensor data upon reconnection.

Continuous rollout of private cellular networks amplifies field-service momentum by ensuring deterministic latency. Industrial IoT coupling further elevates use cases—from predictive maintenance to digital twins—sparking incremental license demand. Progressive web applications offer lightweight alternatives where device constraints or patchy coverage prevail. Consequently, field-service solutions are expected to narrow the revenue gap, fortifying future growth in the enterprise mobile application development market.

By Deployment Model: Cloud Gains Ground as the Default Choice

Cloud deployments captured 67.92% of global revenue in 2025 and are advancing at a 14.12% CAGR. Elastic scaling, zero-downtime updates, and the availability of managed AI services make the cloud the natural fit for enterprises seeking rapid iteration. Microsoft Azure reported 31% year-over-year growth in Q2 2025, with mobile workload expansion cited as a key contributor. The enterprise mobile application development market size for cloud solutions is forecast to widen further as container orchestration normalizes multi-cloud strategies.

On-premise models persist in financial services and public-sector agencies bound by data-sovereignty rules. Hybrid architectures, blending local processing with cloud analytics, give such organizations a compromise path. Edge nodes deployed within factories or retail branches allow real-time decisioning close to assets while synchronizing with centralized models. This flexibility helps minimize vendor lock-in and ensures that the enterprise mobile application development market remains diverse across deployment options.

By Enterprise Size: SMEs Leverage Democratized Tooling for Outsized Gains

Large enterprises held 63.65% of spending in 2025, reflecting entrenched ERP landscapes demanding sophisticated integration. They actively pilot low-code workbenches to accelerate departmental projects without diluting governance, maintaining a strong presence in the enterprise mobile application development market. Small and medium enterprises (SMEs), however, are expanding at 15.29% CAGR thanks to pay-as-you-go pricing and visual builders that mask backend complexity. The enterprise mobile application development market size for SMEs is projected to climb sharply as app-store distribution and cloud marketplaces lower acquisition barriers.

Citizen-developer initiatives inside larger firms also lift productivity—business analysts rapidly prototype dashboards while central IT institutes guardrails. For SMEs, outsourced development remains common, yet low-code tooling reduces vendor dependence over time. AI-assisted code generation embedded in modern platforms further levels the playing field, ensuring the enterprise mobile application development market benefits from broad-based participation.

By Industry Vertical: IT and Telecom Remain Lead Adopters while Retail Surges

IT and telecommunications companies accounted for 28.22% of 2025 revenue, acting as early adopters of emerging standards and microservice architectures. Their familiarity with network APIs accelerates the uptake of edge-AI toolkits and 5G-enabled slices, reinforcing leadership in the enterprise mobile application development market. Retail and e-commerce, meanwhile, post the highest 14.35% CAGR as firms craft frictionless omnichannel journeys. Progressive check-out flows, AR-based virtual try-ons, and real-time inventory views compel continuous investment.

Healthcare organizations deploy mobile telemetry for remote patient monitoring, aligning with telemedicine reimbursement frameworks. Manufacturing adopts connected-worker dashboards and augmented-reality maintenance guides, improving uptime. Financial institutions embed biometric authentication and AI-driven fraud analytics in mobile banking apps. These sector-specific imperatives collectively uphold upward momentum for the enterprise mobile application development market.

Geography Analysis

North America retained 37.95% revenue share in 2025, underpinned by deep enterprise-software spend, early 5G rollout, and stringent accessibility regulations. High cloud adoption and robust venture funding sustain a vibrant partner ecosystem. Europe follows with steady uptake, balancing GDPR compliance with innovation agendas; platforms offering built-in data-residency controls resonate strongly with EU buyers.

Asia-Pacific is the fastest-growing region at 14.88% CAGR, driven by government-backed digitalization programs and unparalleled smartphone penetration. India’s start-up base is projected to more than double by 2030, positioning the country as a global development hub. China’s advanced 5G coverage accelerates the use of AI-enhanced, device-side applications, keeping pressure on vendors to localize stacks. Southeast Asian economies employ mobile apps to leapfrog fixed-line limitations across payments, logistics, and public services. Latin America and the Middle East and Africa show emerging potential, especially where government smart-city projects mandate citizen-service apps. Cloud data-center expansions by hyperscalers reduce latency and have catalyzed regional developer communities. Collectively, these dynamics reinforce a geographically diversified expansion path for the enterprise mobile application development market.

Competitive Landscape

The market remains moderately fragmented. SAP’s cloud revenue grew 27% year-on-year to EUR 4,993 million in Q1 2025, underscoring its pivot toward mobile-centric SaaS. Microsoft’s Azure platform posted USD 40.9 billion Q2 2025 cloud revenue, with mobile workloads highlighted as growth catalysts. Salesforce launched AgentForce, an AI-driven platform attracting 3,000 paying customers within its first quarter.

Strategic acquisitions continue to reshape the field. Triton agreed to acquire Neptune Software, adding a low-code enterprise offering serving 800 customers. [4]Neptune Software, “Triton signs agreement to acquire Neptune Software,” neptune-software.com BP3 Global absorbed DarwinLabs to deepen OutSystems expertise. EPAM announced a USD 1.9 billion deal for NEORIS to expand nearshore delivery. These moves highlight investor appetite for platforms that compress development time while satisfying enterprise governance.

Edge-AI enablement, WCAG 3.0 compliance suites, and sustainability dashboards have emerged as new competitive vectors. Vendors embedding power-usage telemetry differentiate as ESG reporting gains board-level visibility. Likewise, extensible marketplaces offering pre-built connectors draw enterprises seeking faster integration. These dynamics collectively sustain innovation and competition within the enterprise mobile application development market.

Enterprise Mobile Application Development Industry Leaders

Microsoft Corporation

SAP SE

Oracle Corporation

IBM Corporation

Salesforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Google launched AI Edge Gallery, enabling Android devices to run Hugging Face models offline, with an iOS version in the pipeline.

- April 2025: SAP reported EUR 4,993 million cloud revenue in Q1 2025, up 27% year-over-year.

- April 2025: Salesforce closed FY 2025 with USD 10 billion Q4 revenue and unveiled AgentForce, its AI-driven development environment.

- January 2025: Microsoft disclosed USD 69.6 billion Q2 2025 revenue, with Azure and cloud services growing 31%.

- January 2025: Triton signed an agreement to acquire Neptune Software, expanding its low-code portfolio.

- January 2025: ServiceNow completed the acquisitions of 4Industry and EY’s Smart Daily Management application to strengthen connected-worker offerings.

- October 2024: BP3 Global acquired DarwinLabs to bolster low-code delivery capacity.

- October 2024: EPAM Systems agreed to acquire NEORIS, adding 4,700 professionals to its digital-transformation practice.

- September 2024: Salesforce announced a USD 1.9 billion cash deal to buy Own Co., enhancing cloud data-protection capabilities.

- September 2024: SAP closed its acquisition of WalkMe, integrating digital-adoption technology across its suite.

Global Enterprise Mobile Application Development Market Report Scope

Enterprise mobile application development focuses on creating custom software solutions for specific enterprise-grade organizations. These applications aim to streamline company workflows and boost employee productivity and are specially designed for internal organizational use.

The study tracks the revenue accrued through the sale of the enterprise mobile application development solutions by various players across the globe. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

Enterprise mobile application development market is segmented by platform type (business applications, consumer facing applications, productivity applications, field service applications), by deployment model (cloud, on-premise), by enterprises (small and medium enterprises, large enterprises), by industry vertical (BFSI, healthcare, manufacturing, retail, IT and telecom), by geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Business Applications |

| Consumer-Facing Applications |

| Productivity Applications |

| Field-Service Applications |

| Cloud |

| On-Premise |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Healthcare |

| Manufacturing |

| Retail and E-Commerce |

| IT and Telecommunications |

| Other Industry Verticals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Platform Type | Business Applications | ||

| Consumer-Facing Applications | |||

| Productivity Applications | |||

| Field-Service Applications | |||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Industry Vertical | BFSI | ||

| Healthcare | |||

| Manufacturing | |||

| Retail and E-Commerce | |||

| IT and Telecommunications | |||

| Other Industry Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the enterprise mobile application development market?

The market stands at USD 189.22 billion in 2026 and is projected to reach USD 338.42 billion by 2031.

Which deployment model holds the largest share?

Cloud deployment leads with 67.92% revenue share in 2025, driven by scalability and faster release cycles.

Which industry vertical is growing the fastest?

Retail and e-commerce shows the highest forecast CAGR at 14.35% through 2031 as brands pursue frictionless omnichannel experiences.

Why are low-code and no-code platforms important?

They already power more than 65% of development tasks, cutting delivery times by up to 70% and helping enterprises offset developer shortages.

Which region will see the fastest growth?

Asia-Pacific is projected to expand at a 14.88% CAGR, propelled by smartphone ubiquity and government-led digital-economy initiatives.

How are edge-AI capabilities influencing enterprise mobile apps?

On-device AI enables offline analytics and real-time guidance, enhancing field-service, retail, and manufacturing use cases while reducing latency and data-sovereignty concerns.

Page last updated on: