Saudi Arabia Health and Medical Insurance Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

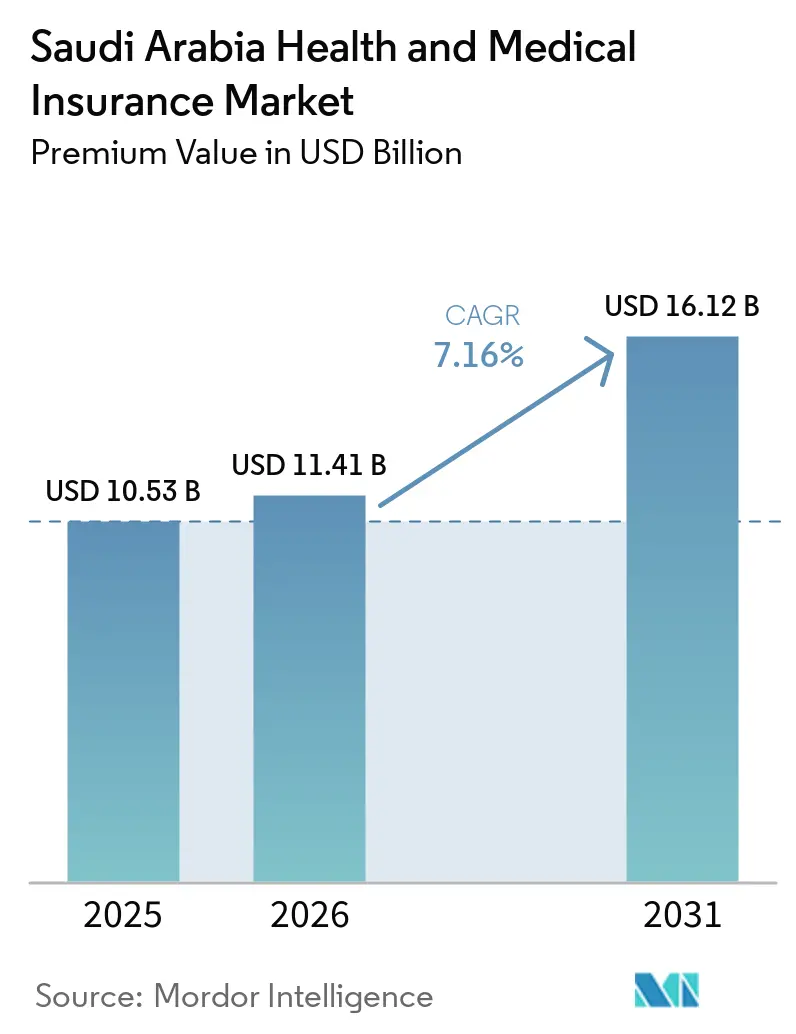

| Base Year Market Size (2025) | USD 10.53 Billion |

| Market Size (2026) | USD 11.41 Billion |

| Market Size (2031) | USD 16.12 Billion |

| Growth Rate (2026 - 2031) | 7.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Health and Medical Insurance Market Analysis by Mordor Intelligence

The Saudi Arabia Health And Medical Insurance Market size in terms of premium value was valued at USD 10.53 billion in 2025 and is estimated to grow from USD 11.41 billion in 2026 to reach USD 16.12 billion by 2031, at a CAGR of 7.16% during the forecast period (2026-2031).

Real-time e-claims through the NPHIES platform are improving settlement speeds, lowering denial rates, and reducing working-capital pressures for healthcare providers, enhancing overall operational efficiency. Digital distribution channels, including InsurTech platforms and aggregators, are expanding market access and reducing acquisition costs, particularly for SMEs and individual policyholders. The Sehhaty mobile health application has become a key component of the Kingdom’s digital healthcare ecosystem, providing appointment scheduling, teleconsultations, prescription management, and health tracking, with over 24 million users, around 68.5% of the population, illustrating high digital adoption and growing consumer comfort with mobile health solutions.[1]Alzghaibi H. et al., “Sehhaty Mobile Health Application in Saudi Arabia,” Frontiers in Medicine, frontiersin.org Regional growth is concentrated in Riyadh due to the presence of large corporations and Vision 2030 infrastructure projects, while other regions benefit from the pilgrimage economy and the privatization of health clusters. Silver-tier plans dominate policy uptake, but Bronze-tier plans are rapidly gaining traction among SMEs seeking cost-effective compliance with mandatory coverage requirements. The March 2024 regulatory consolidation under the Insurance Authority has streamlined approval cycles and centralized oversight, enabling insurers to allocate capital more efficiently into underserved market segments. [2]Saudi Gazette, “Health insurance powers transferred to Insurance Authority from Council of Health Insurance,” saudigazette.com.sa

Key Report Takeaways

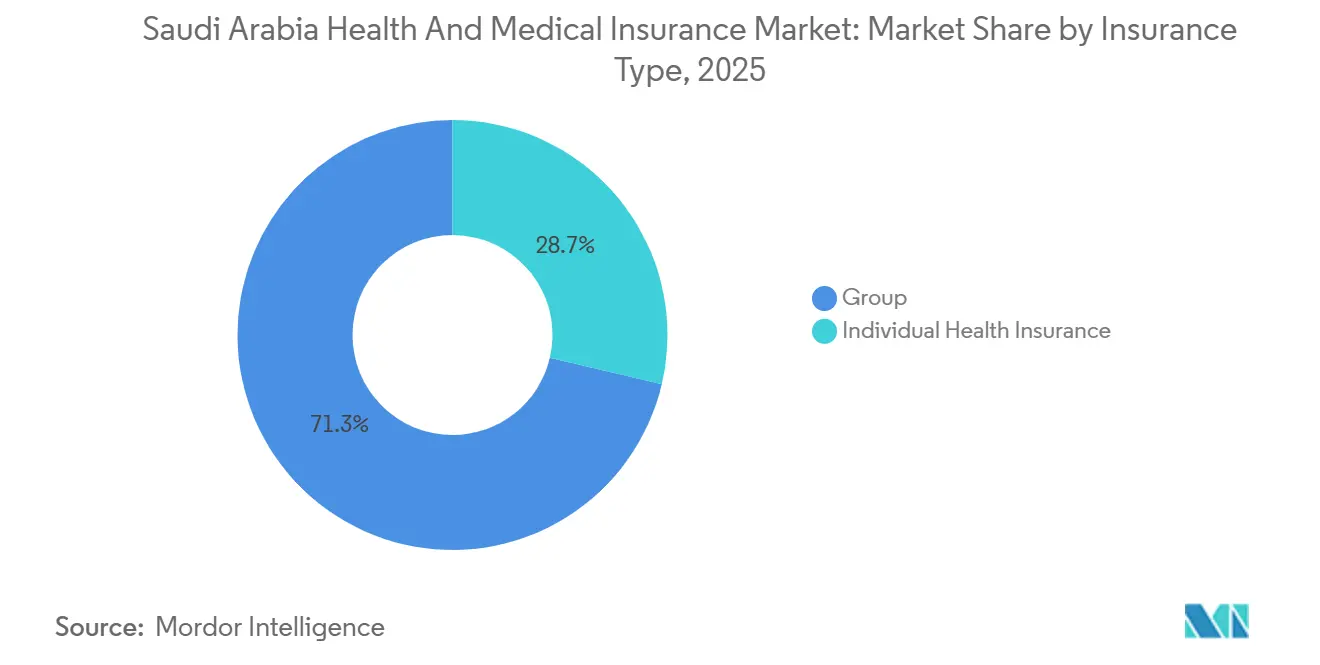

- By insurance type, group health led with 71.33% of the Saudi Arabian health and medical insurance market share in 2025, while individual policies are forecasted to expand at a 12.37% CAGR through 2031.

- By coverage type, inpatient cover accounted for 67.44% of the Saudi Arabian health and medical insurance market share in 2025, while wellness and telehealth add-ons are projected to grow at a 17.75% CAGR to 2031.

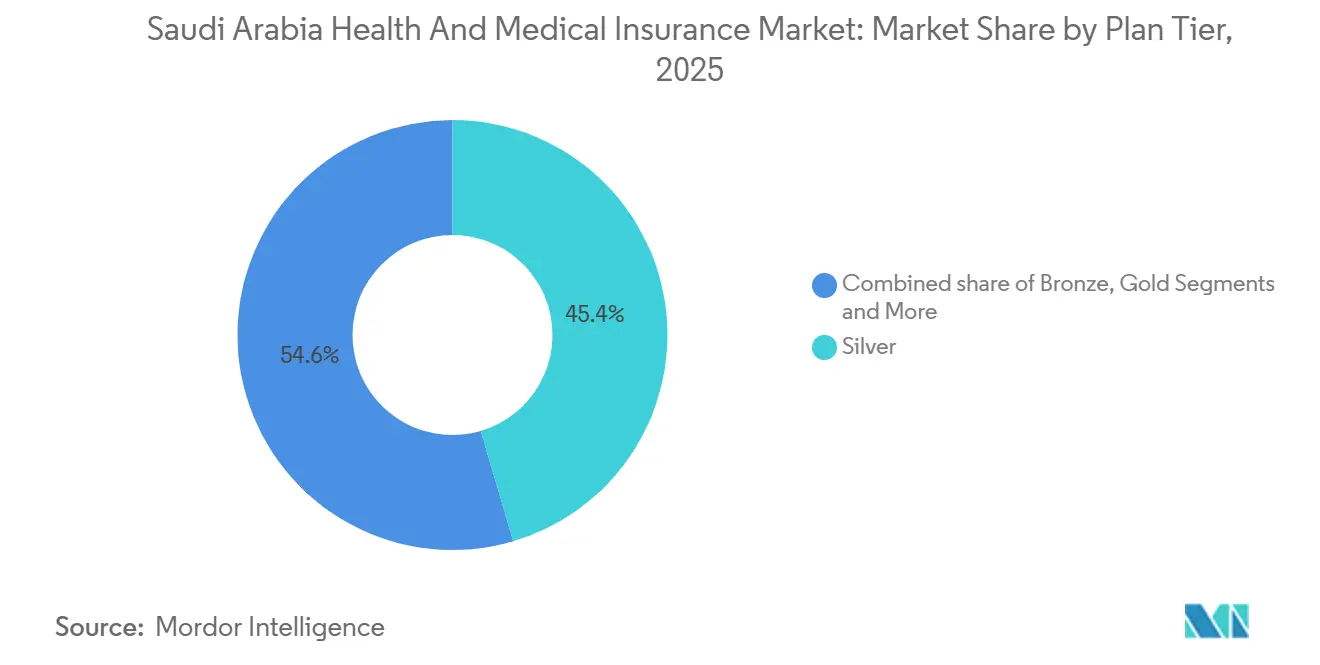

- By plan tier, silver plans held 45.44% of the Saudi Arabian health and medical insurance market share in 2025, while Bronze plans are set to grow at a 15.67% CAGR through 2031.

- By insurance model, co-operative Takaful accounted for 85.39% of the Saudi Arabian health and medical insurance market share in 2025, while conventional products are projected to grow at a 13.39% CAGR through 2031.

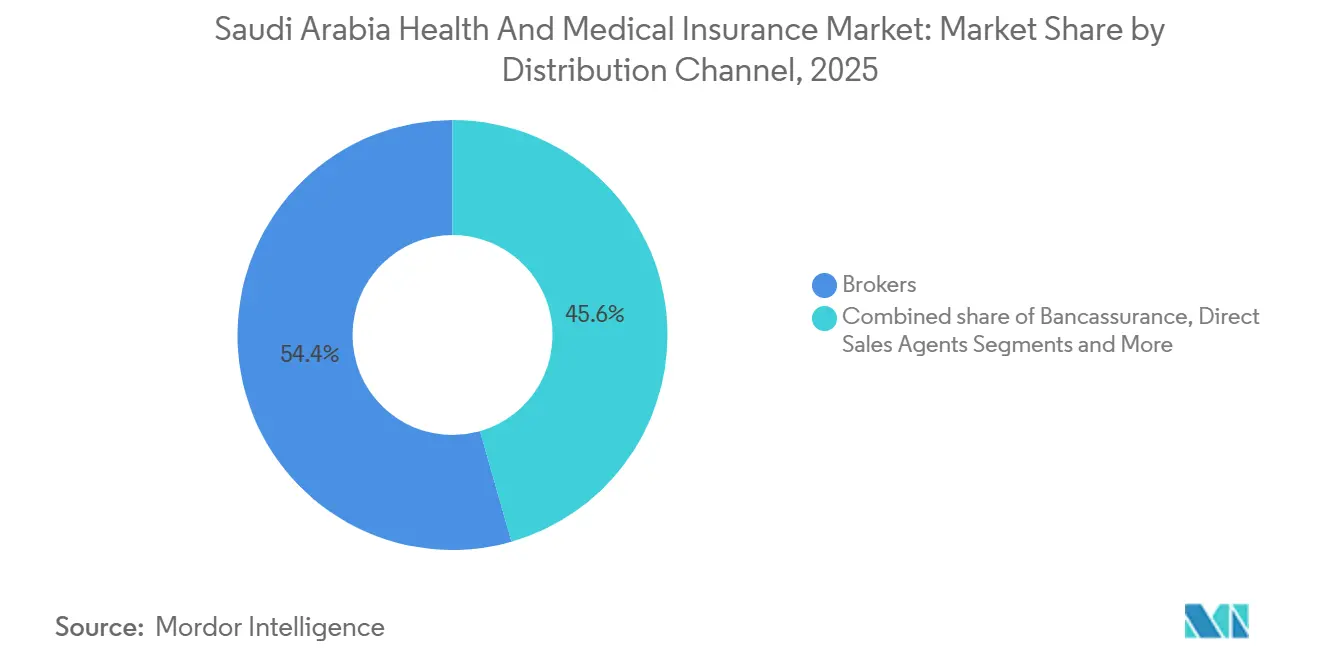

- By distribution channel, brokers led with 54.42% of the Saudi Arabia health and medical insurance market share in 2025, while digital aggregators are forecast to grow at a 22.38% CAGR through 2031.

- By end-user, large corporates accounted for 58.38% of the Saudi Arabia health and medical insurance market share in 2025, while SMEs are projected to grow at a 19.73% CAGR to 2031.

- By geography, the Central region captured 35.84% of the Saudi Arabia health and medical insurance market share in 2025, while the Western region is projected to expand at a 13.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Health and Medical Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NPHIES real-time e-claims mandate | +1.8% | National, strongest in Central and Western regions | Short term (≤ 2 years) |

| CHI value-based purchasing via AR-DRG bundles | +1.3% | National, early in Riyadh and Eastern Province | Medium term (2-4 years) |

| Compulsory dependent cover for private-sector Saudis | +1.5% | National, concentrated in Central, Western, and Eastern | Short term (≤ 2 years) |

| Vision 2030 SME expansion and micro-group demand | +1.2% | National, faster in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Rise of Digital Health Platforms (Sehhaty & Telehealth) | +1.4% | National, strongest in urban centers like Riyadh, Jeddah | Short term (≤ 2 years) |

| Regulatory consolidation under the Insurance Authority | +1.0% | National, immediate effect in all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

NPHIES Real-Time E-Claims Mandate Accelerates Insurer-Provider Adoption

The National Platform for Health Information Exchange Services (NPHIES) functions as a centralized digital gateway connecting healthcare providers, insurers, and TPAs to standardize and automate claims, eligibility, and authorization exchanges across the Kingdom. By enabling real‑time claim submission and adjudication through FHIR‑based messaging standards, NPHIES significantly reduces manual processing, accelerates reimbursement cycles, and improves accuracy by validating and forwarding electronic claims instantly to payers. This interoperability platform enhances data consistency and quality, lowers administrative costs, and increases first‑time acceptance rates, reducing denials and improving provider cash flow. NPHIES also supports instant eligibility checks and standardized data exchanges that simplify insurer workflows and cut turnaround times, fostering broader insurer adoption of digital claims processing. As a result, the mandate is reinforcing digital transformation across health insurers and providers, contributing to efficiency gains and smoother market operations in Saudi Arabia’s health insurance sector. [3]NPHIES, “HL7 FHIR Implementation Guide for NPHIES,” NPHIES, nphies.sa

CHI Value-Based Purchasing Through AR-DRG Bundles Spurs Richer Benefit Designs

The Council of Health Insurance (CHI) has been advancing the implementation of Australian Refined Diagnosis-Related Groups (AR‑DRG) as part of its broader value‑based healthcare strategy to replace traditional fee‑for‑service reimbursement with bundled, case‑based payments that better align cost with clinical value and outcomes. AR‑DRG classification and reimbursement mechanisms are designed to standardize provider billing, enhance cost transparency, and encourage efficient resource use, driving more sophisticated benefit designs that reward quality over volume. Early applications of AR‑DRG in public provider contracting demonstrated that claims can be more precisely weighted by case complexity, improving pricing accuracy and reducing unnecessary procedures, while workshops and phased market preparedness are accelerating adoption across insurers and providers. By supporting value‑based payment models, AR‑DRG fosters innovation in benefit packages and provider reimbursement strategies, ultimately elevating market competitiveness and incentivizing higher quality care within the Kingdom’s health insurance ecosystem. [4]Council of Health Insurance, “AR DRG White Paper,” CHI, chi.gov.sa

Compulsory Cover Extended to Dependents of Private-Sector Saudis Adds 3.2 Million Lives

The mandate requiring private-sector employers to enroll dependents of Saudi nationals has significantly increased the pool of insured lives, driving growth in the individual and family health insurance segment. Enrollment is concentrated in Bronze and Silver-tier plans, reflecting employer sensitivity to copays and network coverage, while premium adjustments remain within budget and below high-tier benchmarks to prevent migration to more expensive plans. The younger dependent demographic improves loss ratios, enhances claims stability, and supports more accurate reserve planning. Additionally, the Insurance Authority’s unified oversight has shortened approval timelines for dependent enrollments, facilitating market expansion and supporting the sector’s overall growth trajectory.

Vision 2030 SME Boom Lifts Micro-Group Policy Demand

Policies promoting entrepreneurship under Vision 2030 are expanding the SME base, driving demand for micro-group health coverage for small teams. Digital onboarding streamlines administrative processes, reducing paperwork and accelerating quote-to-bind cycles, which improves margins on smaller cases. Carriers are offering modular benefits managed via mobile apps, allowing business owners to adjust coverage—adding maternity or dental benefits when budgets allow and reducing coverage when headcount changes. The Insurance Authority’s supportive regulatory approach encourages responsible consolidation and enhanced service levels for SMEs, exemplified by mergers that created larger carriers focused on this segment. Additionally, government-backed fee returns and capital access programs are enabling more small businesses to offer formal health benefits, increasing market depth in the SME segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1 obesity drugs elevate annual claims pressure | -0.9% | National, the highest in Central and Western urban centers | Medium term (2-4 years) |

| Premium-ceiling circular limits repricing flexibility | -0.6% | National, affects all insurers | Long term (≥ 4 years) |

| Rising Chronic Disease Prevalence Increases Claims | -0.8% | National, strongest in urban and aging populations | Medium term (2-4 years) |

| Slow Adoption of Value-Based Reimbursement Models | -0.5% | National, early in Riyadh and Eastern Province | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GLP-1 Obesity Drugs Add USD 799.3 Million (SAR 3 Billion) Annual Claims Pressure

The growing adoption of GLP-1 therapies in private health coverage is creating additional cost pressures for insurers. Uptake varies across plan tiers, with higher-tier plans generally covering the therapy while lower-tier plans often exclude it, prompting some members to migrate to more comprehensive coverage. Insurers are responding with tighter underwriting for high-risk profiles and expanded prior authorization requirements, which can lengthen approval cycles and affect member experience. Preventive health programs promoted by the Ministry of Health aim to encourage lifestyle changes and primary care engagement, seeking to reduce reliance on expensive pharmacotherapy. To manage financial risk, carriers are increasing stop-loss thresholds and utilizing reinsurance for catastrophic claims. As GLP-1 adoption continues to rise, these factors collectively pose a challenge to claims stability and market profitability.

Premium-Ceiling Circular Limits Repricing Flexibility

Regulatory caps on annual premium increases constrain insurers’ ability to adjust pricing in line with rising medical costs. Multi-year corporate contracts face margin pressures until benefits can be repriced at renewal, creating income challenges during periods of cost escalation. Insurers respond by narrowing network options in lower-tier plans and steering members toward more cost-effective care settings, preserving savings without limiting essential access. Employers increasingly adopt administrative services-only arrangements to manage claims trends beyond the premium ceiling, shifting some risk while maintaining plan design flexibility. The Insurance Authority monitors stakeholder feedback and may adjust guidelines for higher-risk pools, but the premium cap continues to limit repricing flexibility. Collectively, these factors constrain profitability and strategic pricing in the Saudi health insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Dependent Mandate Reshapes Individual Growth

Group health coverage held 71.33% of 2025 premiums, and anchors employer benefits for large organizations across core sectors. Individual policies are expected to grow at a rate of 12.37% through 2031, as dependents of private-sector Saudis enter risk pools and freelancers seek portable coverage. Premiums for individual buyers tend to be higher than group rates due to distribution costs and risk selection considerations. Carriers mitigate adverse selection through health questionnaires and waiting periods, while encouraging preventive services to stabilize claims. Digital aggregators are expanding individual policy uptake in urban centers by providing instant quotes and lowering acquisition costs, making entry-level plans more accessible. The combination of regulatory compliance, risk pool expansion, and digital distribution is driving a structural shift in the Saudi health insurance market toward individualized offerings.

Group products remain critical for corporate compliance and expatriate workforce benefits, with renewals emphasizing network depth and digital claims capabilities. Employers are increasingly integrating dependent enrollments into plan hierarchies to balance coverage obligations with budget constraints. Individual buyers show growing interest in wellness-linked incentives that reward preventive screenings and promote healthier behaviors, helping control future claims. Insurers adjust underwriting by offering shorter waiting periods to remain competitive while maintaining actuarial prudence under regulatory rules on benefit exclusions. Digital platforms continue to refine user journeys, integrating NPHIES eligibility and claims checks at the point of sale to enhance conversion rates. Overall, the Saudi health insurance market is evolving toward a more digital, flexible, and wellness-focused structure that accommodates both group and individual needs.

By Coverage Type: Wellness Add-Ons Surge on Mobile Adoption

Inpatient coverage continues to dominate paid claims with 67.44% and serves as the core benefit for hospitalization limits, with plan designs aligned to mandated minimums. Wellness and telehealth add-ons are experiencing the fastest growth at 17.75% CAGR through 2031, reflecting the increasing use of mobile claims submission and strong engagement across national e-health platforms. Outpatient services occur more frequently than inpatient care but generate lower claim values, encouraging carriers to promote preventive care and virtual consultations. Maternity riders are gaining popularity in family policies as dependent enrollments increase, with pricing tiers adjusted according to the breadth of facility access. Bundled dental and optical benefits are enhancing retention in lower-tier plans by providing predictable value for routine services. Overall, the market is seeing a shift where add-ons complement core inpatient coverage to improve member satisfaction and loyalty.

Wellness benefits now extend to gym memberships, nutrition consultations, and mental health applications, with the highest activation among younger, digitally engaged adults. Telehealth services are improving access in regions with fewer specialists, supporting network adequacy, and reducing physical clinic congestion during peak periods. Critical-illness riders with lump-sum payouts are increasingly included in group plans, helping employers differentiate benefits in competitive talent markets. Insurers continue to refine benefit tiers to balance affordability and network coverage while preparing for broader digital adoption. The combination of traditional inpatient coverage with targeted add-ons is enhancing the overall member experience. These innovations are helping carriers strengthen plan loyalty and maintain engagement across both individual and group segments of the Saudi health insurance market.

By Plan Tier: Bronze Policies Gain on SME Cost Sensitivity

Silver plans hold the largest share at 45.44% and balance copays with broad network access that includes a high share of licensed facilities across major cities. Bronze plans are growing the fastest with 15.67% CAGR through 2031, as SMEs seek plans that meet minimum compliance requirements while managing payroll and benefit costs. Gold plans primarily serve multinational organizations that require access to top-tier facilities and second-opinion services for complex medical cases. Platinum plans target executives needing concierge-level care and medical evacuation, maintaining a smaller, specialized market share. Administrative services-only arrangements act as quasi-tiers for large employers who manage claims directly while retaining control over benefit design. Overall, tier adoption reflects both affordability considerations and targeted benefits for different employer segments.

Regulatory standards on minimum benefits and network adequacy continue to guide tier design, with carriers publishing access ratios for major cities. Bronze plan growth is fueled by the expansion of SMEs under national programs that promote entrepreneurship and private-sector hiring. Silver retains its leadership by balancing cost and network breadth, which is critical for employers recruiting across diverse labor markets. High-tier plans maintain differentiation through faster scheduling and bundled provider networks as AR-DRG implementation advances. The tier mix demonstrates a stable core while entry-level plans gain momentum to meet compliance needs and SME budgets. Collectively, this dynamic supports a market structure that accommodates both regulatory requirements and diverse organizational needs.

By Insurance Model: Conventional Products Narrow Takaful’s Lead

Takaful retains an 85.39% share as a culturally grounded model that emphasizes pooled contributions and surplus distribution to participants. Conventional health insurance offerings are growing steadily as the unified regulator streamlines approvals, allowing faster product cycles that appeal to multinational employers. Larger Takaful providers report improved revenue mix and lower costs as domestic retrocession capacity expands. Conventional plans attract global employers seeking simpler master agreements and easier alignment across Gulf operations. Hybrid products that combine Takaful governance with conventional reinsurance are emerging as a bridge category, appealing to younger buyers in the Saudi market. The evolving mix reflects both cultural preference and growing demand for products aligned with international standards.

The Insurance Authority continues to consult on product standards to formalize hybrid categories, facilitating faster innovation and more competitive plan designs. As coding readiness for DRG bundles improves, carriers increasingly align their model choice with network performance, pairing financing structures with provider quality. Conventional products are well-positioned to gain share among multinationals due to reinsurance capacity and cross-border administrative simplicity. Takaful carriers defend their market base through digital investments and strong ties to retail and SME segments that value surplus distribution. Market competition remains healthy, with regulatory clarity helping define categories and accelerate product approvals. Overall, both Takaful and conventional models coexist, providing diverse options for cultural and multinational preferences.

By Distribution Channel: InsurTech Platforms Disrupt Broker Dominance

Brokers lead at 54.42% because SME relationships and consultative services remain important to benefit selection and renewal negotiations. Digital aggregators are the fastest-growing channel with 22.38% CAGR through 2031, using price-comparison engines and API-driven enrollment to lower acquisition costs and shorten sales cycles. Bancassurance cross-sells health riders through bank branches, capitalizing on consumer finance and mortgage touchpoints. Direct sales teams focus on large RFPs, offering customized benefits and service levels to secure margins over standard plans. Corporate in-house negotiations maintain a steady share, allowing large employers to manage benefits internally at scale. Overall, distribution channels are evolving to balance traditional advisory roles with technology-enabled convenience and efficiency.

Regulators mandate standardized benefit summaries on digital platforms to improve transparency and align with national financial sector objectives. This increases price discovery and plan comparison capabilities for both consumers and employers, while shifting competition toward performance metrics like claims turnaround time. Integration with NPHIES allows digital platforms to pre-authorize elective procedures during the shopping process, reducing decision windows and improving conversion rates. Brokers adapt by offering risk management advisory services to maintain a share in complex group accounts and multi-site employers. Technology is streamlining quoting, enrollment, and post-sale support, reducing friction across all channels. The combined effect is a distribution landscape that blends traditional expertise with digital efficiency, driving growth and customer engagement.

By End-User: SME Segment Outpaces Corporations

Large corporates account for 58.38% of premiums as major sectors carry large insured employee bases and contract with carriers that offer deep networks and digital service. SMEs are the growth engine, projected to grow at a 19.73% CAGR through 2031, as entrepreneurship programs and fee-return initiatives lift formalization and benefits adoption in smaller firms. Expatriate coverage remains a significant component, shaping benefit design according to sector risk and regional workforce distribution. Expansion of dependent coverage for Saudi nationals in private roles is prompting employers to review plan tiers and contribution structures. Government employees who purchase supplemental coverage remain a smaller but profitable segment due to favorable risk profiles and low incidence of claims fraud. Overall, corporates provide stability while SMEs drive growth and diversification in the Saudi health insurance market.

Self-employed professionals and freelancers are seeking flexible plans that accommodate fluctuating headcounts in startups and contract-based roles across major cities. Carriers respond with income-verified products that lower premiums for eligible applicants and enhance portability across projects. Retail and hospitality employers often choose narrow-network bronze plans to align coverage with workforce demographics and control costs while remaining compliant. Innovative benefits targeting gig and platform workers represent a growing opportunity as sectors like logistics and services expand. The end-user mix is diversifying as SMEs and flexible work arrangements demand tailored coverage that is simple to administer and digitally accessible. These trends are reshaping the market toward adaptable, tech-enabled solutions for a broadening range of users.

Geography Analysis

The Central region, anchored by Riyadh, accounted for 35.84% of 2025 health insurance premiums, benefiting from the concentration of large employers and national projects that boost insured positions across contractors and professional services. Growth is expected to accelerate as megaproject labor demand rises, favoring premium-tier coverage for specialized expatriate roles and higher average annual premiums per life. Riyadh hosts a large share of licensed insurers’ headquarters, enabling direct negotiations and lowering distribution costs compared with brokered channels. Public-private partnership models in the region privatize health clusters and manage risk through capitated contracts with stop-loss protection for complex cases. Digital adoption peaks in Central Saudi Arabia, as fintech and e-government users submit a higher share of claims via mobile apps than the national average.

The Western region, encompassing Makkah and Medina, is projected to grow at a 13.84% rate through 2031, driven by the pilgrimage economy and healthcare capacity expansion to support visitor coverage. Seasonal demand dynamics during Hajj create liquidity needs, prompting insurers to maintain higher reserves for claims in peak quarters. Jeddah’s commercial base leans toward silver and bronze plans, reflecting the prevalence of SMEs that prioritize value, convenience, and price transparency. Investments in hospitals and bed capacity are easing prior constraints, allowing shorter stays for common procedures and improving service efficiency. Telehealth is expanding in the West to manage seasonal spikes, reducing pressure on physical clinics and ensuring continuity of care for both residents and visitors.

The Eastern Province is growing, anchored by energy and industrial sectors that favor strong corporate plans and high-performing networks. Growth is forecast at 8.9% through 2031, above the national average, as industrial diversification and new job creation increase insured populations and plan turnover. DRG coding readiness in the region is ahead of national averages, reducing reimbursement delays and improving loss ratios through network optimization. Northern and Southern regions, in contrast, hold smaller market shares and face network adequacy challenges, prompting temporary regulatory leniency. Telehealth is helping bridge access gaps in these regions, providing a pathway to higher penetration as new hospital projects come online throughout the decade.

Competitive Landscape

The Saudi Arabian health and medical insurance market shows moderate concentration, with a few leading carriers holding a significant share of premiums, while numerous other licensed insurers compete for the remainder of the market. Carriers are focusing on three key themes in 2026, which are network optimization with DRG-ready providers, mobile-first claims to reduce administrative costs, and vertical integration through telehealth. New entrants are raising industry standards with digital underwriting journeys and real-time eligibility checks, speeding decision-making and improving conversion among younger clients. Real-time claims adjudication reduces denials and reserve requirements, freeing capital for product innovation and selective contracting with high-performing facilities. Employers and individuals increasingly compare carriers using published turnaround metrics and benefit summaries, shifting competition toward measurable performance and user experience.

Scale advantages benefit larger carriers, which can negotiate more favorable reinsurance terms and absorb compliance costs more efficiently than mid-tier firms. A 2025 merger created a larger competitor targeting SMEs, with the expanded capital base enabling growth in digital distribution and data analytics. Leading insurers are investing in predictive analytics to identify at-risk members and deploy care management programs, lowering total medical costs per managed member and enhancing renewal value. Integration with NPHIES APIs allows carriers to complete authorizations quickly, improving service levels and reducing avoidable denials during pre-authorization. The market is positioned for further M&A activity, as compliance requirements and technology investments favor larger platforms that can spread fixed costs efficiently.

Strategic moves in 2025 reinforced carriers’ leadership in large account management through contracts with government-linked entities and national champions in utilities, airlines, and foreign service. One insurer launched a digital health platform combining telemedicine and prescription delivery, reducing call-center volumes and improving operational efficiency within months. Bupa Arabia undertook a corporate restructuring to optimize capital allocation and align its legal structure with regulatory standards. MedGulf secured a major national contract, rebalanced solvency metrics, and integrated a large merger that expanded both capital and market scope. The competitive landscape remains dynamic, as carriers continue balancing growth with disciplined underwriting and transparent service metrics under regulatory oversight.

Saudi Arabia Health and Medical Insurance Industry Leaders

Bupa Arabia for Cooperative Insurance

Tawuniya (The Company for Cooperative Insurance)

MedGulf (Mediterranean & Gulf Cooperative Insurance & Reinsurance)

Al Rajhi Company for Cooperative Insurance (Al Rajhi Takaful)

Saudi Arabian Cooperative Insurance Company (SAICO)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Khedmah, Oman’s digital payments and services platform, launched in app medical insurance services in partnership with Dhofar Insurance. This offering allows users to access a range of medical insurance products directly through the Khedmah platform, including coverage for individuals, families, SMEs, domestic workers, and employee health plans, enhancing digital access to essential health insurance and compliance solutions across the Sultanate.

- October 2025: Buruj Cooperative Insurance merged with Mediterranean and Gulf Insurance & Reinsurance (Medgulf). Medgulf issued 33,157,894 new shares to Buruj’s shareholders, absorbing all Buruj assets, liabilities, and contracts. The merger enhances scale and competitiveness in Saudi Arabia’s insurance sector, with Baker McKenzie advising Buruj legally.

- September 2025: Bupa Arabia received the Saudi Insurance Authority’s non-objection to restructure by demerging its insurance business into a new wholly owned subsidiary. The transaction is subject to shareholder approval, with closing planned in Q1 2026.

- March 2025: Bupa Arabia for Cooperative Insurance launched Saudi Arabia’s first “No Pre‑Approvals” health insurance program, allowing insured members to receive outpatient medical treatment directly without submitting or waiting for prior insurance approvals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabia health and medical insurance market as the total gross written premiums collected by licensed insurers for policies covering inpatient, outpatient, pharmaceutical, and wellness benefits delivered inside the Kingdom, plus mandatory cross-border emergency cover.

Scope exclusion: We exclude cover sold by foreign insurers to Saudi residents while traveling.

Segmentation Overview

- By Insurance Type

- Individual Health Insurance

- Group Health Insurance

- By Coverage Type

- Inpatient Cover

- Outpatient Cover

- Maternity Cover

- Dental Cover

- Optical Cover

- Critical-Illness Riders

- Wellness/Telehealth Add-ons

- By Plan Tier

- Bronze

- Silver

- Gold

- Platinum

- Employer Self-Funded (ASO)

- By Insurance Model

- Co-operative (Takaful)

- Conventional

- By Distribution Channel

- Insurance Brokers

- Bancassurance

- Direct Sales Agents

- Digital Aggregators & InsurTech Platforms

- Corporate In-house Sales

- By End-User

- SMEs

- Large Corporates

- Expatriates

- Saudi Nationals in Private Sector

- Government Employees (Supplemental)

- Self-Employed / Individual Citizens

- By Region

- Central (Riyadh)

- Western (Makkah & Medina)

- Eastern Province

- Northern Region

- Southern Region

Detailed Research Methodology and Data Validation

Primary Research

We complemented desk work with interviews and surveys of underwriting managers, benefit brokers, large providers, and digital aggregators across Riyadh, Jeddah, and Dammam. These conversations let us validate average claim severity, sense demand for new telehealth riders, and stress test our working assumptions.

Desk Research

We began by pulling time series on premiums, enrollment, and claims from the Council of Health Insurance, the Saudi Central Bank insurance statistics, and the General Authority for Statistics, which anchor volumes and average policy values. We then reviewed rule changes, including CHI premium ceiling circulars and the nphies real-time e-claims mandate, to map regulatory inflection points, and we mined peer-reviewed work in the Saudi Medical Journal and WHO health accounts for disease and cost trends.

Our analysts also dissected insurer filings on Tadawul, investor decks, and press releases, and we tapped D&B Hoovers for carrier revenue splits, plus Dow Jones Factiva for merger and contract news. The sources cited here are illustrative; numerous additional publications and datasets informed data collection, validation, and clarification.

Market-Sizing & Forecasting

Our base year value, reported by Mordor Intelligence, is rebuilt through a top-down premium pool approach that multiplies insured lives by average written premium, each calibrated with CHI and SAMA releases. Supplier roll-ups of selected insurers and sampled average selling price by plan tier act as a bottom-up sense check.

Key variables in the model include expatriate employment, population growth, mandatory coverage rollouts, medical inflation, digital channel share, and claim frequency. We project each driver with multivariate regression and scenario analysis, then weight outputs to yield a forecast. Data gaps are bridged with interpolations reviewed with sector experts before adoption.

Data Validation & Update Cycle

Before sign-off, our outputs run variance checks against health spending series and undergo multi-layer analyst review. Reports refresh annually, and we reopen models mid-cycle when material regulations, mega contracts, or cost shocks surface. A final sweep before publication ensures clients receive the latest view.

Why Mordor's Saudi Arabia Health & Medical Insurance Baseline Inspires Confidence

We note that published estimates often diverge because firms pick different scopes, reference years, or refresh rhythms.

Key gaps arise from whether expatriate dependents are counted, how takaful surplus income is treated, use of written versus earned premiums, and the weight models assign to rising telehealth riders.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.03 B (2025) | Mordor Intelligence | |

| USD 7.80 B (2024) | Regional Consultancy A | Excludes micro-group schemes and wellness add-ons |

| USD 7.80 B (2024) | Global Consultancy B | Uses constant 2022 FX rate, omits takaful surplus |

| USD 36.17 B (2024) | Trade Journal C | Aggregates personal accident and critical illness products |

The comparison shows that Mordor's disciplined scope selection, mixed-method modeling, and timely refresh deliver a balanced, transparent baseline that decision makers can trace to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size and growth outlook for the Saudi Arabia health and medical insurance market?

The Saudi Arabia health and medical insurance market size is USD 11.41 billion in 2026 and is projected to reach USD 16.12 billion by 2031 at a 7.16% CAGR.

Which coverage areas are expanding fastest within Saudi Arabia health and medical insurance?

Wellness and telehealth add-ons are growing at a 17.75% trajectory with digital claims adoption and wider use of e-health platforms across the country.

How is regulation shaping insurer growth in Saudi Arabia health and medical insurance?

A unified Insurance Authority and the NPHIES real-time e-claims system shorten approvals, speed adjudication, and support value-based purchasing under AR-DRG bundles.

Which customer segments are driving demand in Saudi Arabia health and medical insurance?

SMEs are the fastest-growing end-user cohort at 19.73% as entrepreneurship programs expand, while individual policies rise with the dependent enrollment mandate.

What is the role of digital channels in Saudi Arabia health and medical insurance?

Brokers lead share, but digital aggregators are expanding at a 22.38% growth pace with price comparisons, API enrollment, and standardized benefit displays required by regulation.

Which regions account for the largest premiums in Saudi Arabia health and medical insurance?

The central region leads with 35.84% of 2025 premiums, while the Western region shows the fastest growth profile at a 13.84% CAGR through 2031.

Page last updated on: