Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

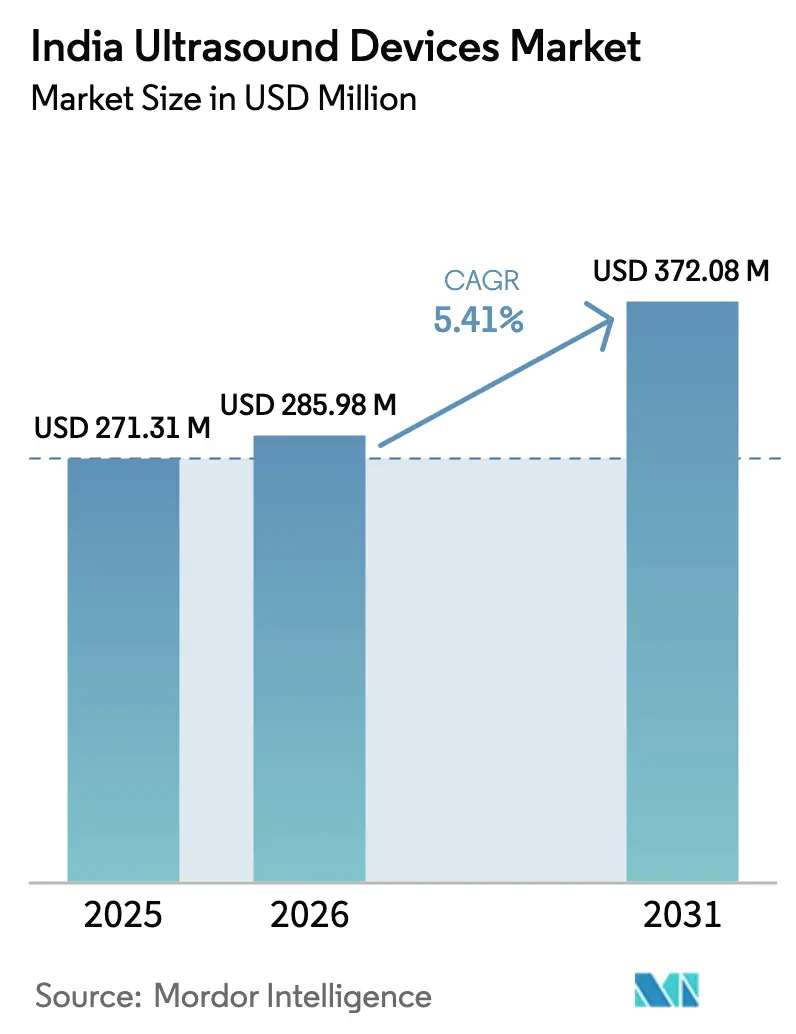

| Base Year Market Size (2025) | USD 271.31 Million |

| Market Size (2026) | USD 285.98 Million |

| Market Size (2031) | USD 372.08 Million |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Ultrasound Devices Market Analysis by Mordor Intelligence

The India Ultrasound Devices Market size was valued at USD 271.31 million in 2025 and estimated to grow from USD 285.98 million in 2026 to reach USD 372.08 million by 2031, at a CAGR of 5.41% during the forecast period (2026-2031).

Rising chronic-disease screening mandates, government incentives for local production, and rapid adoption of point-of-care imaging jointly sustain the expansion of the India ultrasound devices market. Multinational vendors accelerate localization through sizeable capital commitments, while indigenous manufacturers leverage the Production-Linked Incentive program to close capability gaps. Portable systems gain traction as 5G connectivity and tele-health platforms extend diagnostics into underserved districts, yet stringent CDSCO licensing and workforce shortages restrain near-term momentum. Overall, the India ultrasound devices market continues to benefit from policy-backed infrastructure spending that lifts public and private procurement across tier-1 and tier-2 cities.

Key Report Takeaways

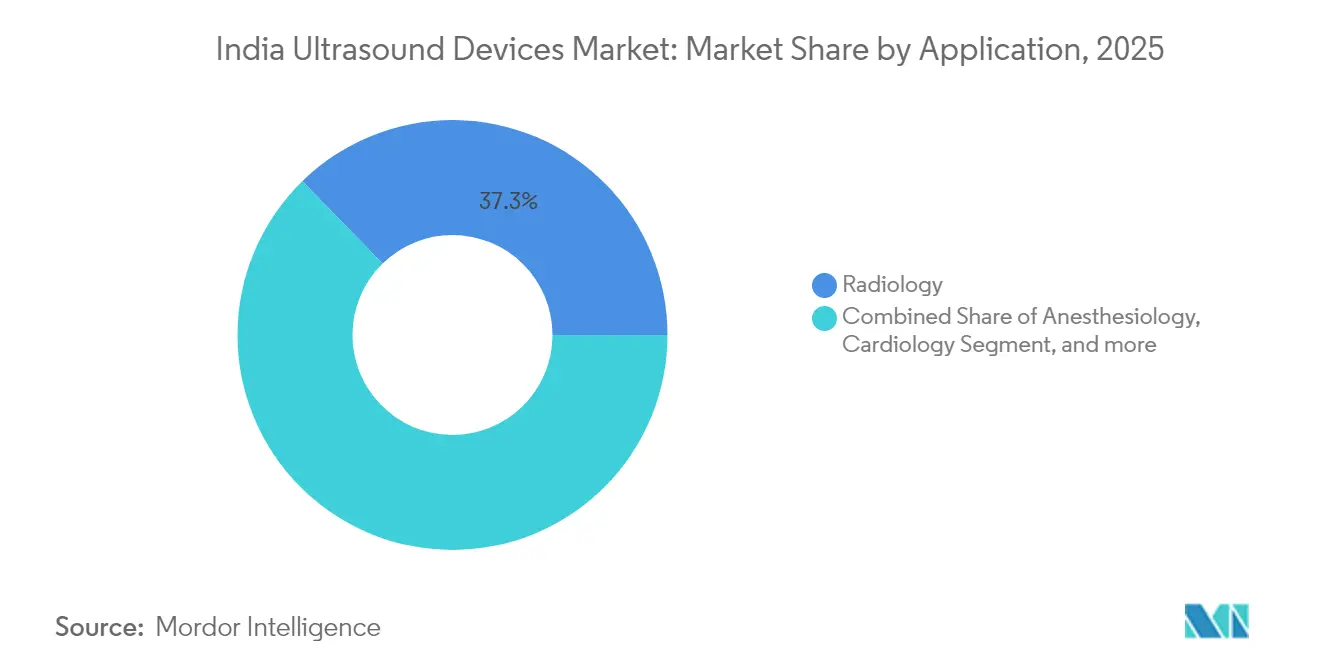

- By application, radiology led with 37.31% share of the India ultrasound devices market in 2025, while critical care posted the fastest 3.75% CAGR through 2031.

- By technology, 3D & 4D systems commanded 43.95% of the India ultrasound devices market size in 2025; high-intensity focused ultrasound is projected to grow at a 3.42% CAGR over 2026-2031.

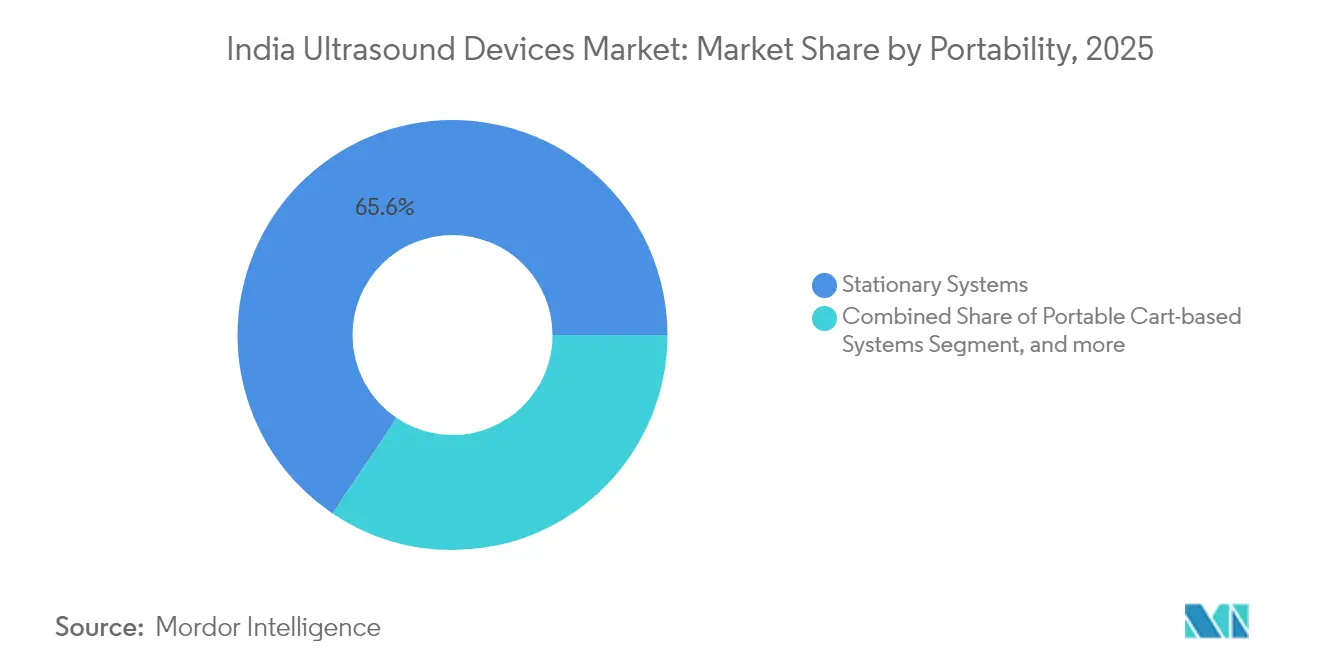

- By portability, stationary systems had a 65.58% share of the India ultrasound devices market in 2025, whereas handheld/pocket devices are advancing at a 4.63% CAGR to 2031.

- By end user, Hospitals held 52.34% share of the India ultrasound devices market in 2025, but Ambulatory Surgical Centres are forecast to expand at a 4.31% CAGR during the outlook period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic Diseases | +1.2% | National, higher in urban centers | Medium term (2-4 years) |

| Growing Awareness of Early Disease Detection | +0.9% | South & West India | Short term (≤ 2 years) |

| Expansion of Portable & Point-of-Care Ultrasound | +1.1% | Rural & semi-urban, North-East focus | Medium term (2-4 years) |

| Government Healthcare Initiatives | +0.8% | National, underserved regions | Long term (≥ 4 years) |

| Local Manufacturing & Product Innovation | +0.7% | Karnataka, Tamil Nadu, Gujarat | Long term (≥ 4 years) |

| Telemedicine & Remote Ultrasound Access | +0.6% | Rural North-East & Central India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases

One in four Indian adults screened at Apollo Hospitals in 2025 was hypertensive, and nearly the same proportion was diabetic, underscoring a silent epidemic that propels ultrasound from episodic diagnostic use to routine community screening.[1]Ministry of Health and Family Welfare, “NPCDCS Clinic Network Update 2025,” mohfw.gov.in NPCDCS clinics now operate across every state, embedding ultrasound into standardized protocols at primary centers.[2]Healthcare IT News, “AIIMS Delhi Oncology AI Project,” healthcareitnews.com Preventive-care financing under Ayushman Bharat further embeds structured reimbursement, while AIIMS Delhi’s oncology AI, trained on 500,000 images, exemplifies how artificial intelligence augments image interpretation and mitigates workforce gaps. The combined effect is sustained volume growth for portable units that reach urban outreach camps and rural wellness centers.

Growing Awareness of Early Disease Detection

The eSanjeevani tele-consult platform has served 340 million patients since 2021, integrating imaging referrals into virtual primary care and stimulating demand for systems that upload scans directly to cloud archives.[3]Invest India, “eSanjeevani Tele-consult Milestone,” investindia.gov.in Aster CMI Hospital’s 95%-accurate carpal-tunnel AI illustrates specialized ultrasound expansion beyond obstetrics. Hyderabad’s SMART DROP diabetic-retinopathy protocol proves how structured screening cascades into higher equipment utilization inside diabetes clinics. Ayushman Bharat reimbursement removes price friction, letting facilities deploy midrange scanners without delaying ROI, thereby accelerating the India ultrasound devices market.

Expansion of Portable & Point-of-Care Ultrasound

University of Cambridge research identified cultural and training barriers that suppress POCUS uptake, yet these constraints highlight lucrative niches for vendors that bundle remote coaching and AI-guided workflows. Siemens Healthineers’ ACUSON Maple, presented at AOCR 2025, combines battery operation, 5G uplink, and AI triage to address both metro ICUs and village health camps. Smartphone-linked handhelds from Clarius Mobile Health extend imaging to clinics lacking cart space or three-phase power, broadening reach among 25 million clinicians worldwide. Fujifilm SonoSite’s new Noida software hub reinforces local support and speeds India-specific firmware iterations.

Government Healthcare Initiatives

Union Budget 2025 raised health spending by 9.46% to INR 95,957.87 crore, financing diagnostics inside Health & Wellness Centres and subsidizing system purchases by district hospitals. The USD 400 million Production-Linked Incentive pool offsets capex for ultrasound assemblies that meet 50% domestic-value thresholds. Medical Device Parks in Himachal Pradesh and Tamil Nadu provide common utilities that cut overhead for vendors meeting India ultrasound devices market demand. National Medical Devices Policy 2023 targets USD 50 billion domestic output by 2030, anchoring long-term certainty for component suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Environment | -0.8% | National, higher on imports | Short term (≤ 2 years) |

| Shortage of Skilled Professionals | -0.6% | Rural & semi-urban | Long term (≥ 4 years) |

| High Cost of Advanced Systems | -0.7% | Tier-2/3 cities & rural | Medium term (2-4 years) |

| Infrastructure Gaps in Rural Areas | -0.5% | Central & North-East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Environment

CDSCO halted refurbished high-end imports in April 2024, citing safety, and its protracted MD-15 approvals encouraged several OEMs to divert assembly to Vietnam, delaying product refresh cycles in India. Although the National Single Window System aims to compress review times, compliance costs remain steep for start-ups. The 2024 marketing code further limits aggressive promotion but promises higher buyer trust long term.

Shortage of Skilled Professionals

Only one trained sonographer per 65,000 people serves rural clusters, restricting practical utilization once equipment arrives. New medical colleges will double graduate output by 2028, yet near-term shortages persist. GE HealthCare and NVIDIA’s autonomous scanning prototype can auto-position probes, easing operator dependence, while eSanjeevani offers remote consult layers that partially cover skill gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Expands Point-of-Care Adoption

Radiology anchored a 37.31% India ultrasound devices market share in 2025 as tertiary hospitals conducted comprehensive abdominal, obstetric, and vascular exams in centralized imaging suites. Critical Care posted the highest 3.75% CAGR, propelled by trauma protocols requiring bedside echo within 5 minutes of admission and by the India ultrasound devices market size growth inside emergency departments. Portable probes allied with AI decision support amplify throughput in ICU rounds and cardiac arrest calls. Gynecology/Obstetrics sustains double-digit volume as maternal-mortality reduction remains a policy target, whereas Musculoskeletal imaging gains visibility through sports-injury clinics that value quick tendon assessments.

Cardiology extends share through AI-enabled speckle-tracking that standardizes ejection-fraction calculation, and Urology leverages ultrasound guidance for minimally invasive stone retrieval. Rising diabetic vasculopathy drives vascular-segment growth, aided by handheld Doppler integration. Unified multi-application consoles, such as GE’s Versana Premier, allow smaller hospitals to span seven specialties with a single purchase, reducing capex while widening procedure menus.

By Technology: 3D & 4D Retain Lead amid AI-Powered Upgrades

3D & 4D platforms held 43.95% of the India ultrasound devices market in 2025, favored for obstetric bonding and surgical-planning clarity. The India ultrasound devices market size for these systems benefits from AI plug-ins that shorten fetal-anomaly scans to under 90 seconds. HIFU registers a 3.42% CAGR as non-invasive liver and prostate therapies receive wider reimbursement and specialist training centers multiply. Legacy 2D scanners persist in primary centers where budgets remain tight, while Color Doppler advances in cardiology and peripheral-artery workups. GE HealthCare’s USD 51 million Intelligent Ultrasound buyout infused ScanNav Assist into workflow, highlighting competition pivoting to AI-first differentiators.

Portable “other technologies” wrap in smartphone connectivity and edge-AI lesion detection, broadening reach where radiologists are scarce. GE and NVIDIA’s self-navigating prototype underpins a future where novice users capture diagnostic-grade imagery, easing the skilled-workforce choke point across the India ultrasound devices market share landscape.

By Portability: Hand-Held Momentum Closes Access Gaps

Stationary Systems delivered 65.58% of 2025 revenues, supporting advanced studies demanding high power and multi-probe switching. The India ultrasound devices market size for hand-held/pocket units grows 4.63% annually as district hospitals deploy them in outreach vans and community health camps. Cart-based systems bridge versatility and mobility inside surgical theaters and labor wards. Handheld makers like Clarius exploit smartphone ubiquity, selling probes that weigh under 200 grams yet stream DICOM over 5G, a match for tele-supervision workflows in the India ultrasound devices market.

Siemens’ ACUSON Maple tailors rugged casings and long-life batteries to withstand intermittent power in rural South Asia. Regulatory scrutiny remains equal to stationary consoles, compelling vendors to embed hardware-level safeguards. AI diagnostic modules bundled into handhelds lift exam confidence, cementing their role as first-touch tools across triage, obstetrics, and musculoskeletal clinics.

By End User: Ambulatory Centers Surge in Outpatient Era

Hospitals secured 52.34% 2025 share as apex institutions purchase premium scanners with elastography and contrast-enhanced modes. Ambulatory Surgical Centres register a 4.31% CAGR, reflecting payer preference for same-day procedures that lower cost of care inside the India ultrasound devices industry. Diagnostic Imaging Centres retain relevance by offering bulk exam contracts to insurers and corporates. Tele-health hubs, corporate clinics, and community wellness sites emerge as “other end users,” absorbing portable systems tied to eSanjeevani’s national platform.

Ayushman Bharat coverage of ultrasound-guided biopsies lifts throughput at small ambulatory sites, reducing referral leakage. GE’s Voluson Expert refresh accelerates obstetric throughput in high-volume outpatient maternity chains, underpinning revenue diversification. AI auto-measure packages on mid-tier consoles compress exam turnaround, adding strategic value for India ultrasound devices market penetration.

Geography Analysis

Southern India leads adoption due to manufacturing clusters in Karnataka and Tamil Nadu, where Trivitron operates nine factories and Siemens staged the AOCR 2025 showcase. Western India follows, boosted by Maharashtra’s sprawling hospital networks and Gujarat’s electronic component ecosystem, including a USD 2.7 billion semiconductor facility that promises domestic transducer chip supply. Northern India capitalizes on policy proximity, with AIIMS installing India’s first indigenous MRI and piloting advanced ultrasound AI suites. Eastern India climbs on West Bengal’s public-health emphasis, though infrastructure still lags western metros. Central India Madhya Pradesh and Chhattisgarh records steady gains as state schemes finance district-hospital upgrades. The North-East, although the smallest in value, outpaces all regions in growth, fueled by CMAAY and PMJAY cashless coverage that sets ultrasound as a baseline diagnostic. Tele-medicine bridges specialist scarcity, letting scans captured in Itanagar reach radiologists in Delhi within minutes, reinforcing equitable access across the India ultrasound devices market.

Telangana’s 35 NCD clinics, having already uncovered 28,000 new diabetes and hypertension patients, illustrate how state-specific programs spike local scanner demand. NPCDCS uniform protocols ensure procurement homogeneity across all 36 states, easing vendor tendering. Manufacturing benefits cluster south and west where supply chains and skilled labor are deeper; north and east skew toward consumption. Such regional asymmetries shape inventory planning and channel strategies for companies competing in the India ultrasound devices market.

Competitive Landscape

India's Ultrasound Devices Market is moderately competitive and consists of several major players. GE HealthCare, Siemens Healthineers, and Philips anchor the premium tier, each integrating AI suites that counteract operator shortages. Wipro GE’s INR 8,000 crore five-year pledge to scale local manufacturing and R&D underscores the premium players’ localization race. Trivitron leverages cost advantages from its Aloka ultrasound plant to undercut imports on mid-range carts.

Fujifilm SonoSite’s Noida hub develops AI algorithms that personalize settings for Indian body habitus, while considering probe assembly to meet PLI localization thresholds. Handheld challenger Clarius courts rural demand through smartphone-linked probes, whereas Shimadzu’s upcoming Karnataka plant hints at future diversification into medical imaging hardware. Refurbished-unit suppliers face shrinking share after CDSCO import curbs, tilting competitive leverage to firms meeting domestic content rules within the India ultrasound devices market.

India Ultrasound Devices Industry Leaders

Fujifilm Holdings Corporation

GE Healthcare

Siemens Healthineers AG

Koninklijke Philips N.V.

Mindray Medical International Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Telangana government launched 35 NCD clinics across 33 Government General Hospitals and two hospitals in Hyderabad, which have screened over 1.2 lakh individuals above 30 years old and identified 8,457 new cases of hypertension and 20,438 new cases of diabetes, demonstrating systematic early detection capabilities.

- February 2025: FUJIFILM SonoSite expanded its software development operations in Noida, India, focusing on AI applications and considering local manufacturing of ultrasound devices as part of its 'Make in India' strategy, leveraging India's skilled workforce and healthcare system to develop advanced technologies for global healthcare challenges.

- January 2025: Shimadzu Corporation announced plans to open a new analytical factory, Shimadzu Manufacturing India Private Limited (SMI), in Karnataka, India, with operations beginning in spring 2027, covering 40,000m2 and employing 50 people initially, with plans to expand into medical and industrial equipment manufacturing.

India Ultrasound Devices Market Report Scope

As per the scope of the report, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They are utilized for the assessment of various conditions in the kidney, liver, and other abdominal conditions. They are also widely used to treat chronic illnesses, which include ailments including diabetes, asthma, cancer, and heart disease. As a result, these devices have a variety of uses in the medical area, including both diagnostic imaging and therapeutic modality. India ultrasound devices market is segmented by application, technology, and type. By application market is segmented into anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, critical care, and other applications. By technology market is segmented into 2d ultrasound imaging, 3d and 4d ultrasound imaging, doppler imaging, and high-intensity focused ultrasound). By type market is segmented into stationary ultrasound and portable ultrasound. The report offers the value (in USD) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Hospitals |

| Diagnostic Imaging Centres |

| Ambulatory Surgical Centres |

| Other End Users |

By Region

| North India |

| South India |

| West India |

| East India |

| Central India |

| North-East India |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Hospitals |

| Diagnostic Imaging Centres | |

| Ambulatory Surgical Centres | |

| Other End Users | |

| By Region | North India |

| South India | |

| West India | |

| East India | |

| Central India | |

| North-East India |

Key Questions Answered in the Report

How large are ultrasound device sales in India in 2026?

Revenue stands at USD 285.98 million in 2026, with a projected rise to USD 372.08 million by 2031.

Which clinical area shows the fastest growth for ultrasound use?

Critical Care leads with a 3.75% CAGR through 2031, driven by emergency medicine and ICU protocols.

What is the expected growth rate for handheld ultrasound systems?

Hand-held/Pocket devices are forecast to expand at a 4.63% CAGR between 2026 and 2031.

How do government programs influence domestic production?

The USD 400 million Production-Linked Incentive plan reimburses up to 5% of local sales, prompting multinationals and Indian firms to scale India-based assembly lines.

What regulatory challenges do vendors face?

CDSCO approval timelines and a ban on refurbished high-end imports lengthen time-to-market and raise compliance costs.

Which regions are adopting point-of-care ultrasound fastest?

The North-East and Central states lead growth due to tele-medicine rollouts and targeted cashless-care schemes that reimburse diagnostic imaging.

Page last updated on: