Cardiac Mapping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

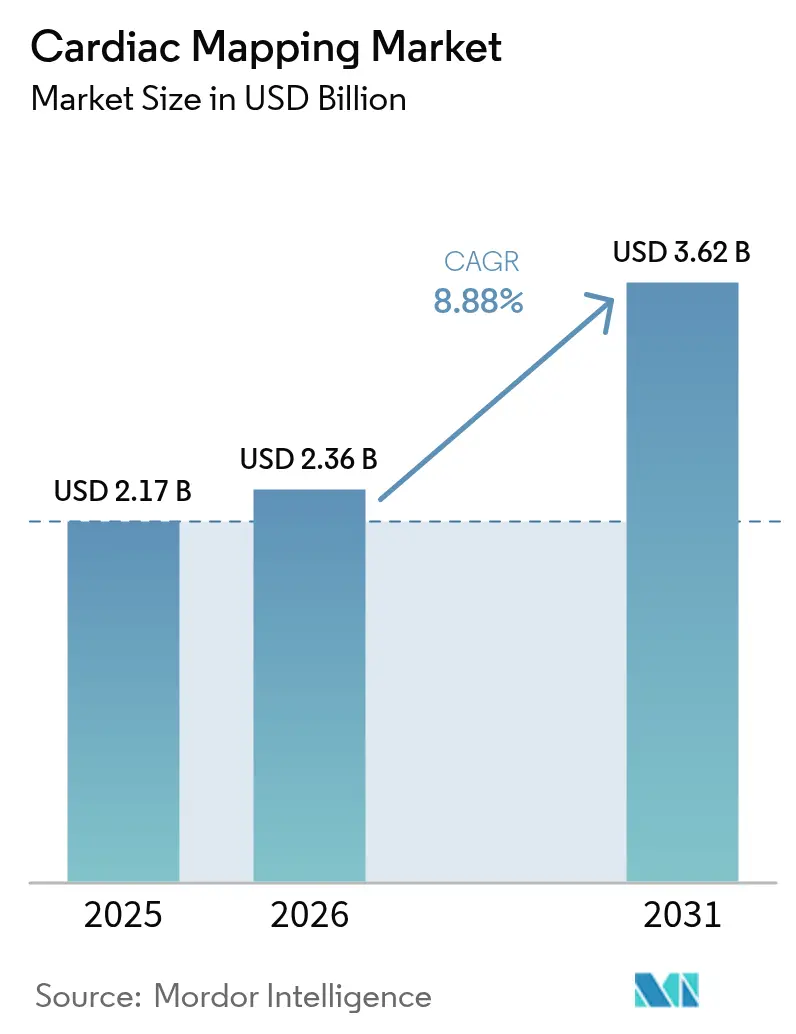

| Market Size (2026) | USD 2.36 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

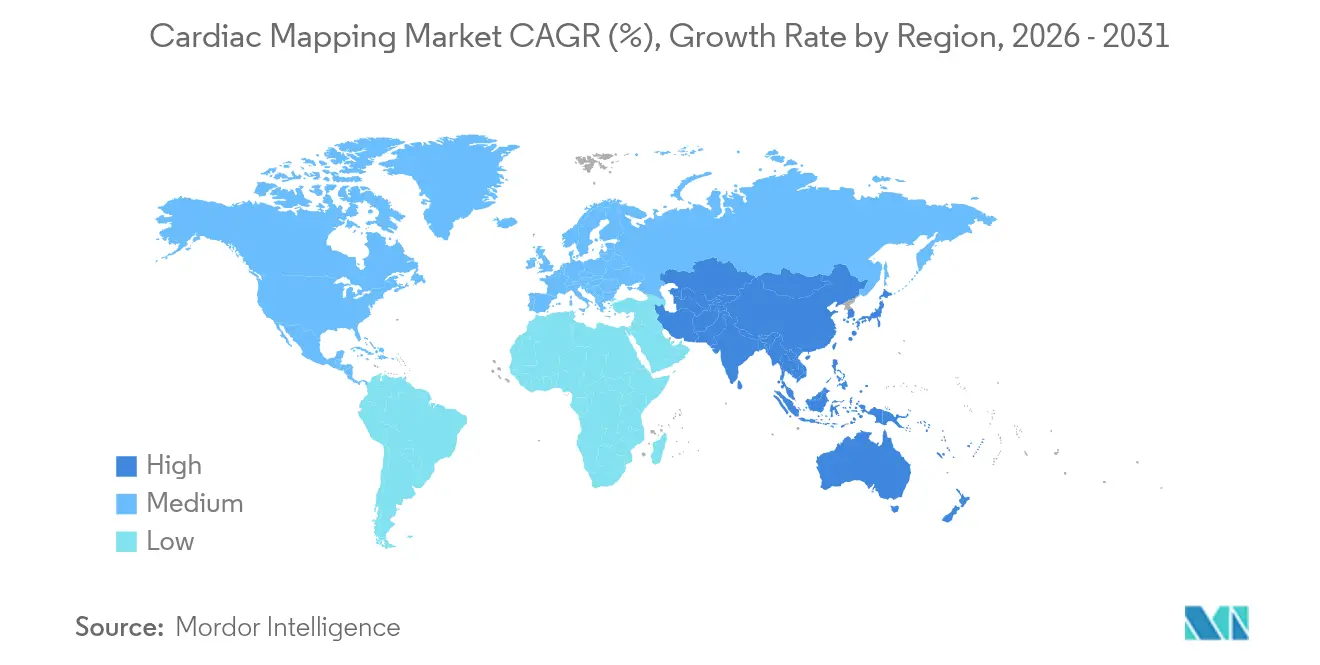

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

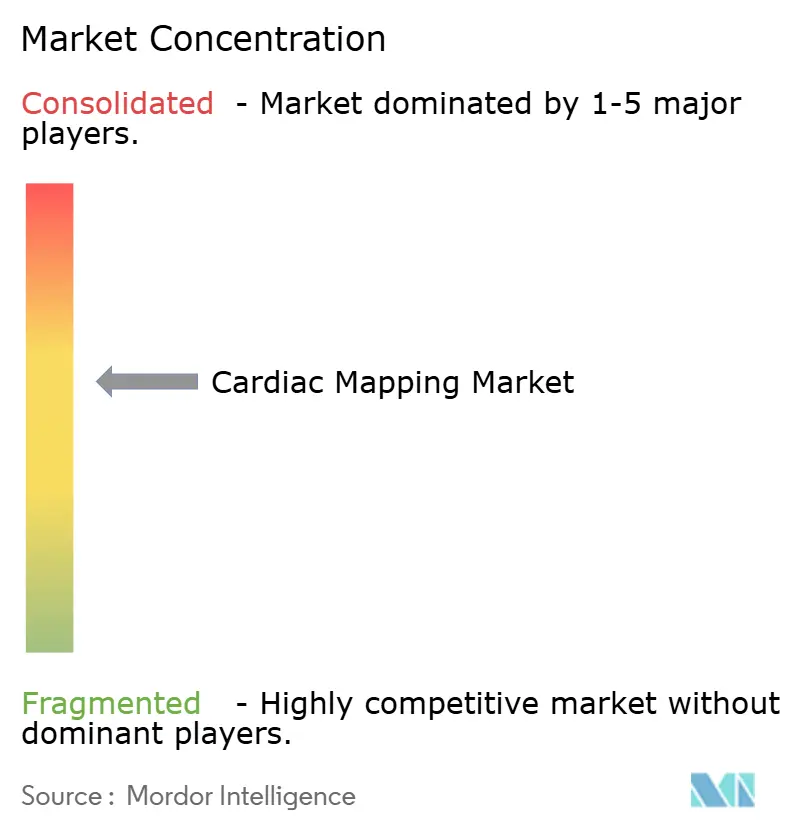

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Mapping Market Analysis by Mordor Intelligence

The cardiac mapping market size was valued at USD 2.17 billion in 2025 and estimated to grow from USD 2.36 billion in 2026 to reach USD 3.62 billion by 2031, at a CAGR of 8.88% during the forecast period (2026-2031). North America leads with 43.12% revenue share in 2024, yet Asia-Pacific delivers the fastest 9.54% CAGR as hospital networks add electrophysiology capacity and embrace artificial-intelligence-enabled platforms. Demand accelerates because atrial fibrillation affects more than 60 million people worldwide, compelling providers to adopt precision mapping systems that shorten procedures and cut readmissions. Contact technologies still command 64.23% share, but non-contact innovations are expanding at 10.43% CAGR on the back of ultrasound and body-surface algorithms that reduce fluoroscopy time. Competitive intensity has elevated since 2024 as manufacturers introduce dual-energy ablation and AI-guided navigation, while hospitals pivot toward same-day discharge models that trim per-case costs by EUR 850-1,301. Reimbursement headwinds—such as a 2.8% CMS conversion-factor cut for 2025—push administrators to extract higher throughput and verifiable outcomes from every device purchase.

Key Report Takeaways

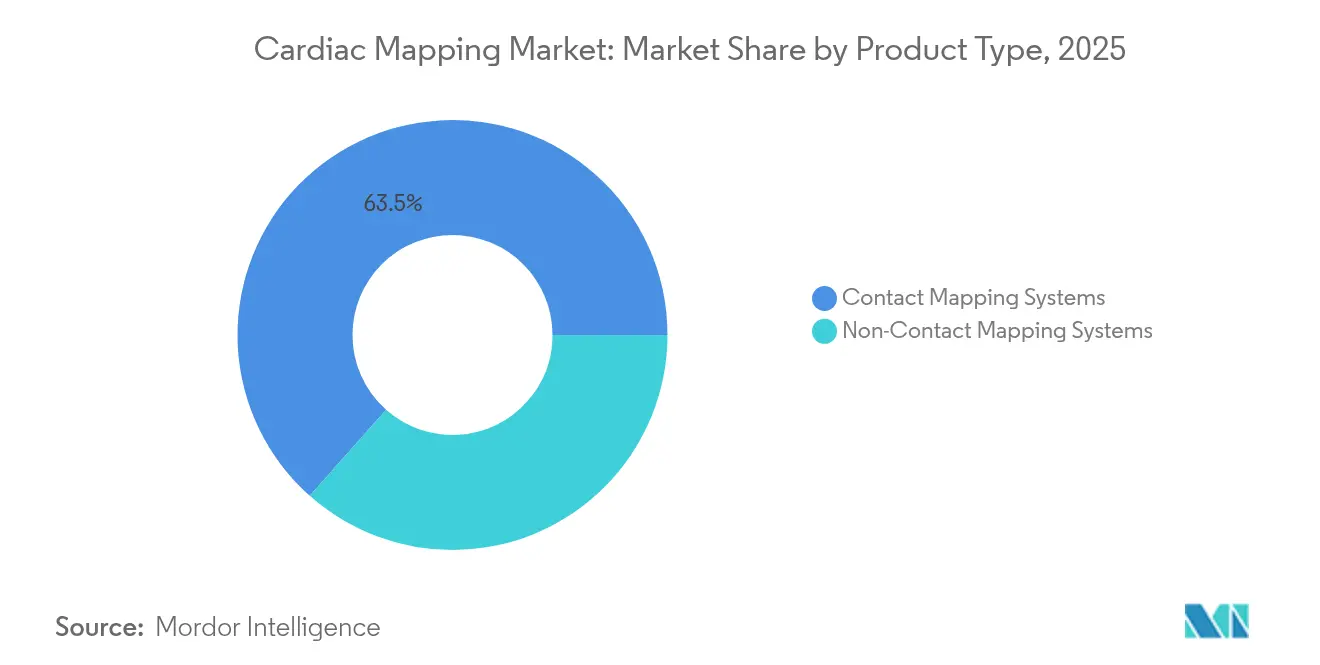

- By product type, contact mapping systems held 63.45% of the cardiac mapping market share in 2025, while non-contact platforms posted the fastest 10.12% CAGR through 2031.

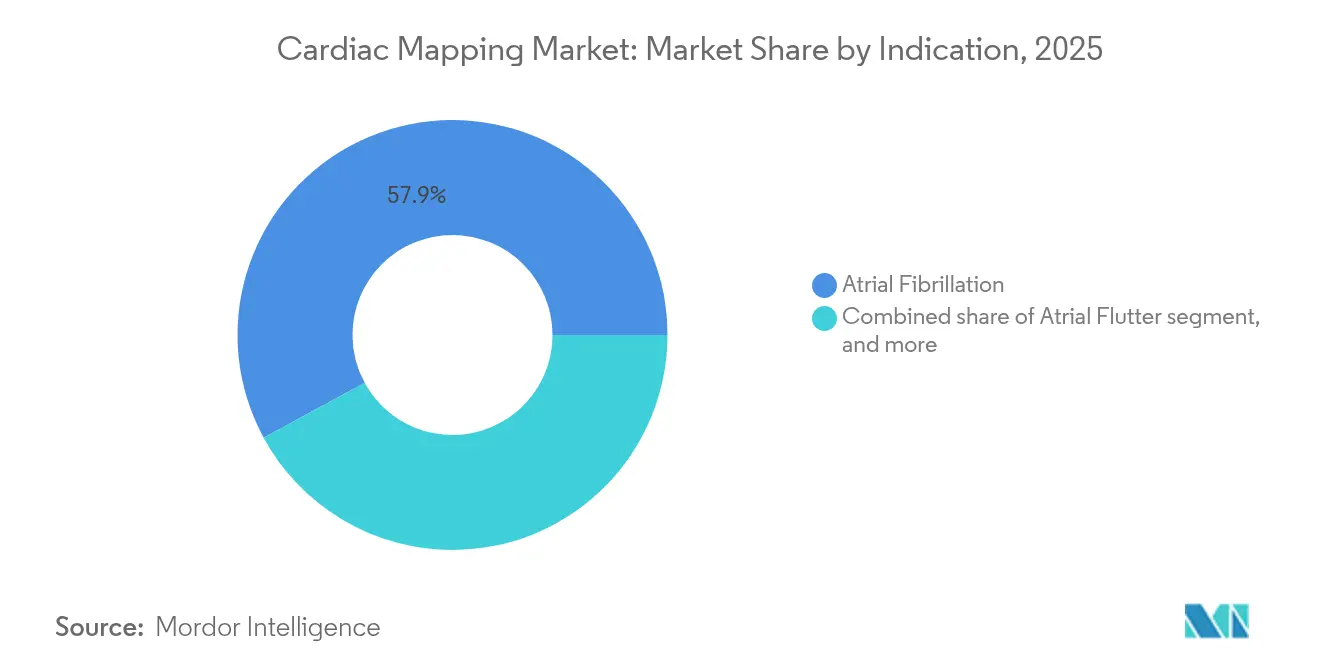

- By indication, atrial fibrillation accounted for 57.92% of the cardiac mapping market size in 2025; ventricular tachycardia is projected to expand at an 11.45% CAGR during 2026-2031.

- By end-user, tertiary hospitals led with 54.66% share in 2025, whereas ambulatory surgical centers are forecast to grow at an 11.25% CAGR to 2031.

- By geography, North America captured 42.55% revenue share in 2025; Asia-Pacific is advancing quickest at a 9.21% CAGR throughout the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cardiac Mapping Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of cardiovascular diseases | +2.1% | Global; strongest in North America & Asia-Pacific | Long term (≥4 years) |

| Advancements in electrophysiology mapping technologies | +1.8% | Global; led by North America & Europe | Medium term (2-4 years) |

| Increasing adoption of minimally invasive ablation procedures | +1.5% | Global; rapid uptake in Asia-Pacific | Medium term (2-4 years) |

| Favorable regulatory and reimbursement policies | +1.2% | North America & Europe | Short term (≤2 years) |

| Expansion of cardiac electrophysiology infrastructure in emerging markets | +1.0% | Asia-Pacific, Middle East & Africa | Long term (≥4 years) |

| Integration of artificial intelligence and cloud analytics in mapping workflows | +0.8% | Global; early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Cardiovascular Diseases

Atrial fibrillation prevalence doubled in South Korea from 1.1% to 2.2% of adults between 2013 and 2022, illustrating how aging populations and lifestyle factors magnify arrhythmia caseloads[1]Hyeon-Cheol Gwon, “AF Prevalence Trends in Korea,” International Journal of Arrhythmia, ijarrhythmia.org. Higher CHA₂DS₂-VASc scores and multiple comorbidities mean physicians need granular electrical roadmaps to guide targeted lesions. More than 9,500 clinicians attended Heart Rhythm 2024, underscoring infrastructural expansion and professional focus on electrophysiology. Emerging economies mirror this trajectory as cardiovascular disease incidence rises alongside urbanization. Hospitals therefore allocate larger capital budgets to high-density mapping consoles, ensuring readiness for a patient cohort that will persist for decades. The result is predictable, long-cycle demand that anchors the cardiac mapping market.

Advancements in Electrophysiology Mapping Technologies

Randomized evidence confirms technology gains: the TAILORED-AF study reported 88% 12-month freedom-from-AF when AI directed lesion sets, eclipsing the 70% rate for routine pulmonary vein isolation[2]TAILORED-AF Investigators, “AI-Guided Ablation Outcomes,” Nature Medicine, nature.com. Hardware moves in lockstep, with 64-electrode catheters embedding contact-force sensors that relay sub-gram accuracy in real time. Companies such as Volta Medical and GE Healthcare combine algorithmic mapping with established recording systems, creating integrated ecosystems. Pulsed field ablation shifts lesion creation from thermal to non-thermal energy, with trials documenting 100% acute PV isolation and minimal oesophageal impact. Continuous innovation imposes upgrade pressure on hospitals that wish to maintain competitive clinical outcomes and referral volumes. Consequently, capital budgets for mapping platforms remain resilient even in constrained reimbursement environments.

Increasing Adoption of Minimally Invasive Ablation Procedures

Health systems increasingly discharge ablation patients on the same day, a model proven non-inferior to overnight observation while improving satisfaction and resource utilization. Pulsed field ablation trims procedure time and reduces post-operative complications, reinforcing the shift toward outpatient pathways. Regulators back the trend; in 2024 the FDA cleared Boston Scientific’s FARAPULSE and Medtronic’s Affera systems, validating PFA safety and efficacy. As electrophysiologists gain familiarity with new energy sources and catheters, peer-to-peer diffusion accelerates adoption curves. The economic argument is decisive: independent analyses show cumulative savings of EUR 850-1,301 per patient compared with conventional thermal techniques. These clinical and financial advantages collectively enlarge the cardiac mapping market because every ablation relies on accurate electro-anatomical imaging.

Integration of Artificial Intelligence and Cloud Analytics in Mapping Workflows

Artificial intelligence transforms mapping consoles into predictive engines. Johns Hopkins researchers built an MRI-based model that predicted sudden cardiac death risk with nearly 90% accuracy. Real-time guidance further shortens procedures; algorithms terminated AF acutely in 40% of cases and kept 70% of patients arrhythmia-free over two years. Cloud connectivity allows every case to refine neural-network weights, improving performance on subsequent patients. Vendors such as Vektor Medical claim 23% shorter procedures and 18% higher lab throughput using AI-assisted localization. As reimbursement increasingly ties payment to quality metrics, AI-enhanced accuracy and efficiency create compelling value propositions that fuel equipment purchases.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled electrophysiologists | -1.4% | Global; most acute in emerging markets | Long term (≥ 4 years) |

| High capital and procedural costs | -1.1% | Global; strongest in price-sensitive markets | Medium term (2-4 years) |

| Cybersecurity and patient data privacy concerns | -0.9% | Global; heightened focus in developed markets | Short–medium term (≤ 4 years) |

| Semiconductor supply chain vulnerabilities | -0.7% | Global; most pronounced in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Electrophysiologists

Fellowship programs cannot match demand; US training pipelines deliver too few specialists according to the Journal of the American College of Cardiology. Emerging markets feel the pinch more acutely because hospital expansion outstrips staff growth. AdventHealth built an 8-month orientation curriculum covering 48 team members to accelerate in-house capability, yet the gap persists. Skill shortages delay utilization of installed systems and lengthen patient wait times. Vendors respond with automation and intuitive user interfaces to reduce learning curves. Health systems also explore tele-mentoring, yet credentialling and liability frameworks remain underdeveloped, extending the constraint’s long-term influence on the cardiac mapping market.

High Capital and Procedural Costs

Full-function mapping suites and pulsed field generators require large upfront outlays. Even though PFA cuts operating-room time, cost-effectiveness models can be marginal in price-sensitive environments, as detailed in Innovations in Cardiac Rhythm Management. Medicare’s 2.8% payment reduction for 2025 sharpens hospital focus on return-on-investment. Capital committees now demand clear data on reduced complications and shortened length of stay before approving purchases. Some suppliers offer value-based contracting where payment depends on achieving specific outcome benchmarks. The trend favors technologies that deliver measurable efficiency while avoiding incremental disposables that inflate per-case costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Contact Systems Dominate Despite Non-Contact Innovation

Contact platforms delivered 63.45% of the cardiac mapping market size in 2025 owing to widespread clinical familiarity, robust reimbursement, and improvements such as 64-electrode grids that yield sub-millimeter resolution. Abbott’s TactiCath catheter registers 0.3 gram precision that helps operators titrate energy safely. The segment’s momentum is fortified by integration with popular ablation generators, ensuring procedural continuity.

Non-contact modalities are advancing at a 10.12% CAGR because AI body-surface algorithms and ultrasound acoustical sensors can reconstruct 3-D chambers without extensive catheter manipulation, thereby reducing fluoroscopy exposure. Basket and multi-electrode arrays provide panoramic data that identifies extra-pulmonary triggers overlooked by point-by-point systems. Hybrid workflows merge contact accuracy for lesion validation with global non-contact scans that guide strategy, illustrating technology convergence that will sustain segment diversity within the cardiac mapping market.

By Indication: Atrial Fibrillation Leadership Faces VT Challenge

Atrial fibrillation represented 57.92% of the cardiac mapping market share during 2025 on the strength of a vast patient pool and standardized procedural pathways. Over 12 million Americans are projected to carry an AF diagnosis within ten years, guaranteeing steady procedural volumes. PFA platforms already post 88% arrhythmia-free survival at one year, enhancing position.

Ventricular tachycardia is growing fastest at 11.45% CAGR because substrate mapping innovations like the S3 technique raise long-term success to 77.9%. Although VT cases are fewer, they carry higher mortality risk, motivating tertiary centers to procure sophisticated 3-D systems that image intramural circuits. Personalised AI-guided maps now tailor lesions based on real-time conduction patterns, narrowing the efficacy gap between VT and AF treatments and expanding the cardiac mapping market size among high-acuity patients.

By End-User: Hospital Dominance Shifts Toward Ambulatory Care

Tertiary hospitals captured 54.66% revenue because they house multidisciplinary teams, hybrid operating rooms, and advanced imaging that underpin complex ablations. They act as reference sites where vendors launch upgrades and collect early-use data.

Ambulatory surgical centers are projected to grow at 11.25% CAGR since same-day discharge protocols have proven safe and cost-efficient. Portable consoles, simplified workflows, and regulatory discussion around ASC inclusion for catheter ablations accelerate this move. Electrophysiology labs embedded within community hospitals compete on volume efficiency, while academic institutes emphasize first-in-human trials that seed future upgrades. This care-setting diversification enlarges the cardiac mapping market by deploying systems beyond flagship institutions.

Geography Analysis

North America booked 42.55% revenue in 2025 thanks to mature reimbursement and early PFA clearances that encourage rapid technology refresh cycles. US centers participate in pivotal trials for dual-energy ablation and AI mapping, securing clinical leadership. Moderate growth through 2031 reflects saturation at top hospitals, though outpatient expansion offsets plateau effects.

Asia-Pacific delivers the highest 9.21% CAGR because cardiovascular disease burdens rise in tandem with economic growth. Fortis Healthcare’s USD 156 million expansion that adds AI-equipped cath labs typifies regional investment. Chinese device firms target FDA and CE pathways, intensifying price competition while broadening product availability. Japan, South Korea, and Australia leverage aging demographics and sophisticated insurance systems to adopt new modalities quickly.

Europe sustains incremental gains as payers scrutinize cost-utility yet reward proven innovations through harmonized regulatory channels. Germany, the United Kingdom, and France absorb most installations, while Italy and Spain emphasize regional equity in access. Brexit mildly disrupts supply chains but clinical collaboration endures. Middle East & Africa and South America form smaller bases yet offer long-run upside as public health budgets climb. Overall, diversified regional trajectories collectively reinforce global expansion of the cardiac mapping market.

Competitive Landscape

Biosense Webster, Abbott, Boston Scientific, and Medtronic anchor a moderately consolidated field where platform breadth and R&D scale drive share. Since 2024, the race to commercialize PFA and AI navigation spawned approvals like Medtronic’s Affera and Boston Scientific’s FARAPULSE, resetting competitive benchmarks. Collaborations flourish: Abbott links with iCardio.ai, while Volta Medical teams with GE Healthcare to embed machine learning into familiar consoles.

Acquisitions underline strategic urgency; Boston Scientific’s Cortex buy strengthens computational mapping for PFA catheters. Niche competitors such as Stereotaxis promote robotically navigated magnetic catheters, aiming at radiation-free precision. Vektor Medical markets purely computational arrhythmia localization that overlays any mapping system, allowing capital-light upgrades.

Price pressure and cybersecurity mandates—FDA released updated guidance in June 2025—drive convergence around secure, upgradable architectures. Vendors that showcase authenticated encryption, cloud update pathways, and proven reductions in procedure time improve tender success. Consequently, product differentiation hinges on measurable efficiency, integrated safety features, and flexible business models rather than hardware alone, shaping sustainable leadership in the cardiac mapping market.

Cardiac Mapping Industry Leaders

Medtronic Plc

Boston Scientific Corporation

Acutus Medical

Johnson & Johnson

Abbott

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Boston Scientific secured FDA approval for expanded FARAPULSE labeling covering persistent AF after the ADVANTAGE AF trial yielded an 85.3% success rate.

- June 2025: Abbott received CE Mark for the Volt Pulsed Field Ablation System, achieving 99.1% PV isolation on fewer energy applications.

- April 2025: Medtronic reported 88% arrhythmia-free survival from Sphere-360 single-shot PFA trials in paroxysmal AF patients.

- March 2025: Stereotaxis filed a 510(k) for the MAGiC Sweep robotically navigated high-density mapping catheter with 20 electrodes.

- November 2024: Johnson & Johnson MedTech obtained FDA clearance for the VARIPULSE PFA platform integrated with CARTO 3 mapping, reaching 85% primary effectiveness.

- October 2024: Medtronic won FDA approval for the dual-energy Affera Mapping and Ablation System with Sphere-9 catheter.

Global Cardiac Mapping Market Report Scope

As per the scope, cardiac mapping is an electrophysiology study that aims to understand the cause of heart rhythm problems like arrhythmia. Mapping the heart's electrical activity is critical for diagnosing and treating heart disease.

The cardiac mapping market is segmented by type, indication, and geography. By type, the market is segmented into contact cardiac mapping systems and non-contact cardiac mapping systems. By indication, the market is segmented into atrial fibrillation, atrial flutter, and other indications. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD) for the above segments.

| Contact Mapping Systems | Conventional RF Contact Catheters |

| Contact-Force Sensing Catheters | |

| High-Density Grid Catheters | |

| Non-Contact Mapping Systems | Basket & Multielectrode Arrays |

| Ultrasound / Acoustical Mapping | |

| AI-Based Body-Surface Mapping |

| Atrial Fibrillation |

| Atrial Flutter |

| Ventricular Tachycardia |

| Supraventricular Tachycardia |

| Tertiary Hospitals |

| Electrophysiology & Cath Labs |

| Ambulatory Surgical Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Contact Mapping Systems | Conventional RF Contact Catheters |

| Contact-Force Sensing Catheters | ||

| High-Density Grid Catheters | ||

| Non-Contact Mapping Systems | Basket & Multielectrode Arrays | |

| Ultrasound / Acoustical Mapping | ||

| AI-Based Body-Surface Mapping | ||

| By Indication | Atrial Fibrillation | |

| Atrial Flutter | ||

| Ventricular Tachycardia | ||

| Supraventricular Tachycardia | ||

| By End-User | Tertiary Hospitals | |

| Electrophysiology & Cath Labs | ||

| Ambulatory Surgical Centres | ||

| Academic & Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the cardiac mapping market be by 2031?

Forecasts place it at USD 3.62 billion, reflecting an 8.88% CAGR during 2026-2031.

Which region grows fastest for cardiac mapping technologies?

Asia-Pacific leads with a projected 9.21% CAGR through 2031 as hospitals expand electrophysiology capacity.

What segment currently dominates cardiac mapping systems?

Contact platforms held 63.45% share in 2025 due to clinician familiarity and broad reimbursement.

Which arrhythmia indication is expanding most rapidly?

Ventricular tachycardia procedures are set to rise at an 11.45% CAGR thanks to improved substrate mapping.

How does pulsed field ablation influence economics?

Analyses show EUR 850-1,301 savings per patient because of shorter procedure times and reduced complications.

Are outpatient settings gaining share in ablation volumes?

Yes, ambulatory surgical centers exhibit an 11.25% CAGR as same-day discharge protocols demonstrate clinical equivalence.

Page last updated on: