Perfumes and Deodorants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

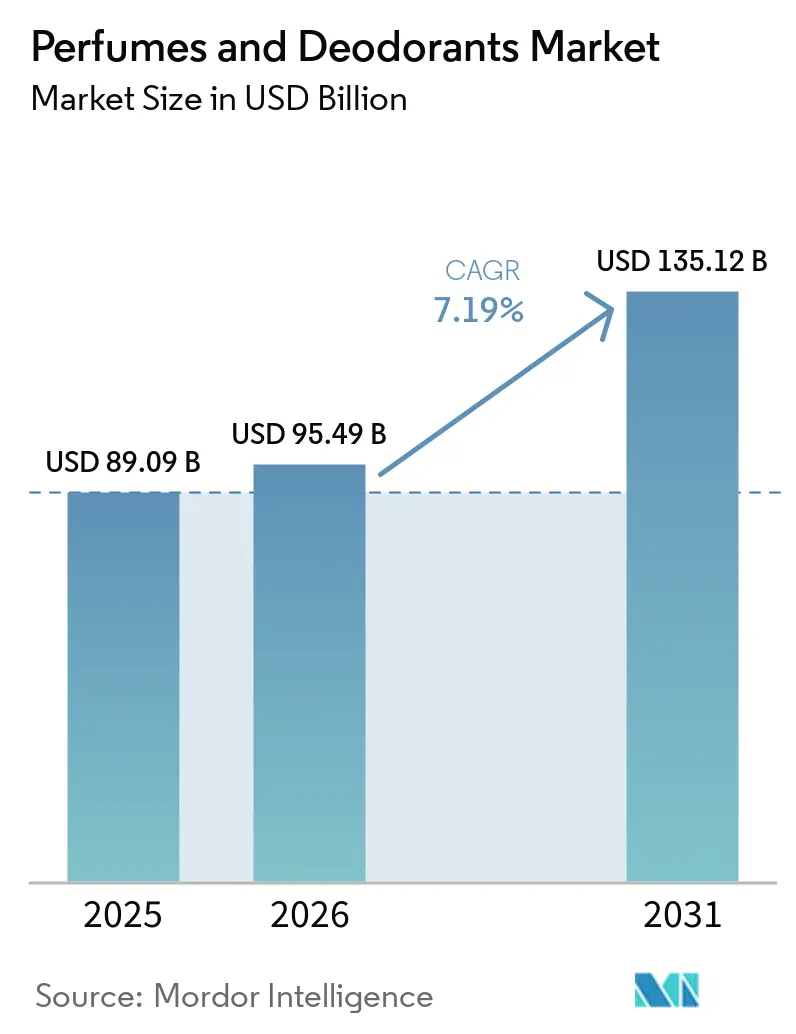

| Market Size (2026) | USD 95.49 Billion |

| Market Size (2031) | USD 135.12 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

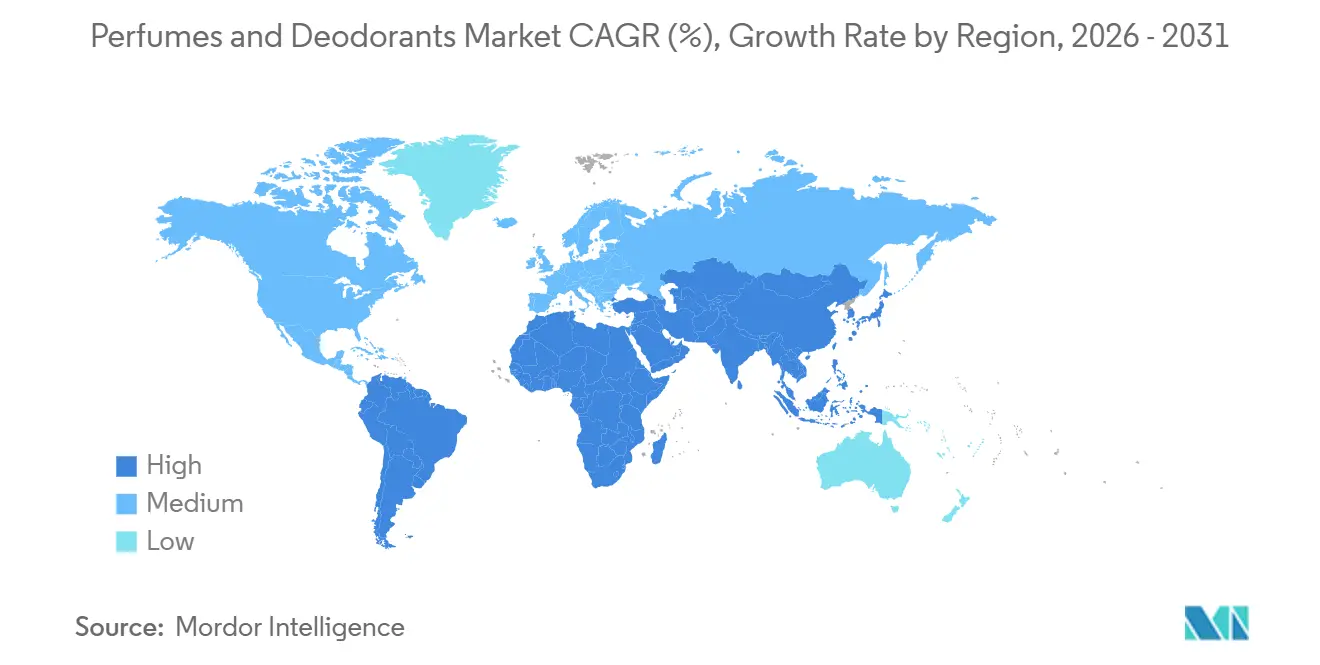

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

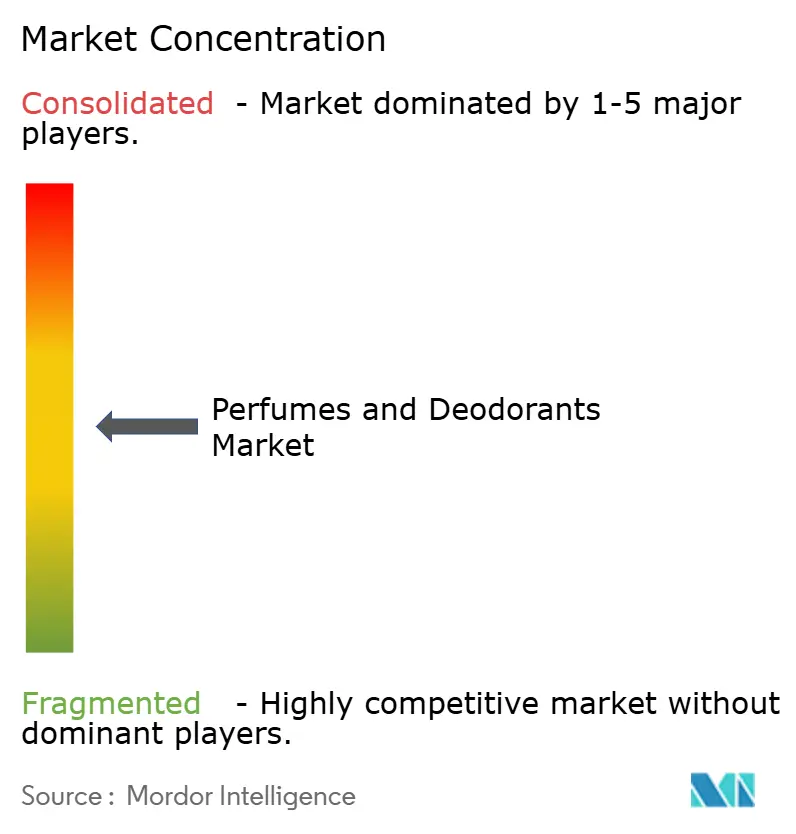

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Perfumes and Deodorants Market Analysis by Mordor Intelligence

The perfumes and deodorants market is projected to grow significantly, increasing from USD 89.08 billion in 2025 to USD 95.49 billion in 2026 and reaching USD 135.12 billion by 2031. This growth represents a compound annual growth rate (CAGR) of 7.19% during the forecast period of 2026-2031. The market's expansion is driven by changing consumer habits, with fragrances and deodorants now a daily routine rather than an occasional activity. Consumers across income levels are increasingly purchasing these products, driven by dual factors: maintaining hygiene and expressing individuality. Brands are evolving their strategies to cater to these demands by focusing on premium products, offering refillable packaging, and creating formulations that combine fragrance with skincare benefits. Digital platforms are playing a crucial role in product discovery, while travel retail and gender-neutral products are emerging as new growth opportunities. Companies that can adapt to these challenges by managing compliance costs, innovating product offerings, and maintaining strong customer engagement are expected to secure a long-term competitive edge.

Key Report Takeaways

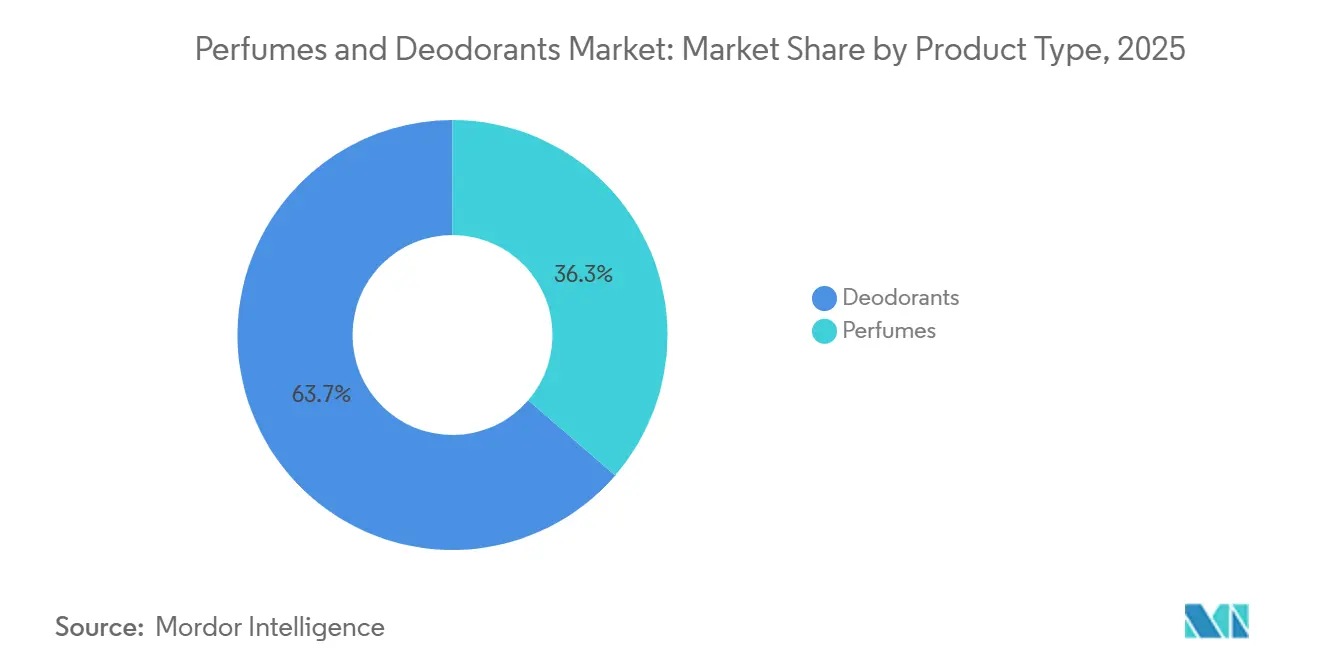

- By product type, deodorants led with 63.67% revenue share in 2025, while perfumes are projected to expand at an 8.82% CAGR through 2031.

- By ingredient source, synthetic and conventional formulations held 85.36% of revenue in 2025, while natural and organic products are forecast to grow at an 8.14% CAGR through 2031.

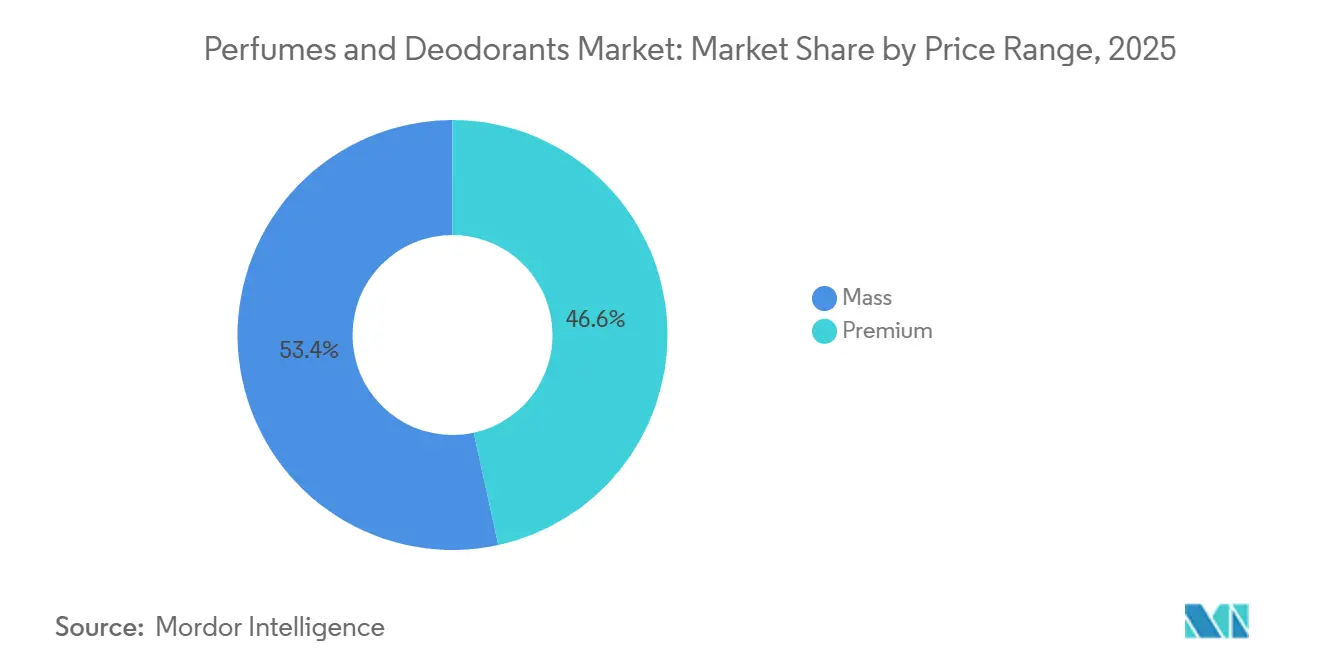

- By price range, mass products accounted for 53.42% of revenue in 2025, while premium and luxury products are expected to grow at an 8.47% CAGR through 2031.

- By end user, women held 67.44% of revenue in 2025, while men are projected to record the fastest growth at an 8.86% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets retained a 41.68% share in 2025, while online retail stores are forecast to advance at an 8.63% CAGR through 2031.

- By geography, North America accounted for 33.56% of revenue in 2025, while Asia-Pacific is expected to post the fastest regional growth at an 8.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Perfumes and Deodorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer focus on personal grooming and hygiene | +2.1% | Global, concentrated in Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Increasing investment by brands in personalized and AI-driven fragrance recommendations | +1.3% | North America, Europe, South Korea, United Arab Emirates | Medium term (2–4 years) |

| Expanding adoption of ethical and traceable fashion products | +0.8% | Europe, North America, Asia-Pacific core | Long term (≥ 4 years) |

| Continuous product innovation in long-lasting, multifunctional, and skin-friendly formulations | +0.9% | Global | Medium term (2–4 years) |

| Popularity of celebrity, designer, and niche fragrance brands | +1.2% | North America, Europe, Middle East and Africa, Asia-Pacific | Short term (≤ 2 years) |

| Growing travel retail and duty-free fragrance sales | +1.0% | Global, with early gains in Dubai, Singapore, Hainan | Short to medium term |

| Source: Mordor Intelligence | |||

Rising consumer focus on personal grooming and hygiene

The perfumes and deodorants market is being driven by increasing awareness of personal grooming, hygiene, and self-care. Consumers are now making deodorants and fragrances a regular part of their daily routines to stay fresh and boost confidence. This shift is evident in both developed and emerging markets, fueled by growing participation in social events, professional engagements, and fitness activities. To meet these evolving demands, companies are focusing on innovative products and packaging. For example, in November 2025, Amcor launched its Shadow roll-on deodorant packaging, which uses less plastic, is recyclable, and offers customization options for beauty and personal care brands. Such advancements not only enhance product appeal but also address consumers' rising preference for sustainable, convenient solutions.

Expanding adoption of ethical and traceable fashion products

Consumers are increasingly favoring ethical, sustainable, and traceable fashion products, boosting demand for alpaca apparel and accessories globally. Shoppers now prioritize transparency in how fibers are sourced, how products are made, and their environmental impact. This shift is pushing brands to improve supply chain traceability and adopt responsible sourcing practices. Alpaca fiber fits well with this trend due to its natural, biodegradable, and durable properties. A report by NSF in March 2025 highlighted that 74% of consumers value organic ingredients in personal care products, reflecting a broader preference for sustainability and ethical sourcing across various lifestyle categories[1]Source: NSF Org, "74% of Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org. As a result, demand for alpaca apparel and accessories produced with ethical, sustainable practices is expected to grow steadily worldwide.

Growing travel retail and duty-free fragrance sales

The growth of travel retail and duty-free channels is driving the perfumes and deodorants market. With international travel on the rise, more consumers are being exposed to premium and luxury fragrance brands at airports, travel hubs, and duty-free stores, where fragrances are among the most popular purchases. The World Travel & Tourism Council (WTTC) reported that the global Travel & Tourism sector contributed a record USD 11.6 trillion to global GDP in 2025, reflecting the strong recovery and growth in travel activities[2]Source: World Travel & Tourism Council, "Travel & Tourism Sees Best Year Ever and Emerges as the World’s Fastest Growing Sector, Outpacing the Global Economy in 2025", wttc.org. To cater to this demand, brands are innovating with products tailored for travelers. For example, in June 2024, Eze Perfumes introduced 18ml travel-friendly fragrances, offering convenient and portable options for consumers. As global travel continues to expand, these retail channels are expected to remain critical for introducing new fragrances, driving impulse purchases, and boosting premium brand growth.

Popularity of celebrity, designer, and niche fragrance brands

The rising demand for celebrity, designer, and niche fragrance brands is driving significant growth in the perfumes and deodorants market. Consumers are increasingly drawn to fragrances that offer a sense of exclusivity, unique scents, and compelling brand stories, enabling smaller, specialized brands to compete with established players. Social media platforms, celebrity endorsements, and direct-to-consumer sales channels are playing a key role in boosting brand visibility and consumer interest. For example, in July 2024, Sniff and Whiff introduced a line of luxury perfumes endorsed by celebrities, catering to consumers looking for premium fragrances inspired by famous personalities and lifestyle trends. Such initiatives demonstrate how celebrity partnerships and unique brand positioning are shaping consumer preferences and driving market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations governing fragrance ingredients and chemical formulations | -0.5% | Europe, North America, Global spill-over | Medium term (2–4 years) |

| Concerns regarding skin irritation, allergies, and sensitivity to fragrance ingredients | -0.3% | Europe, North America | Medium to long term |

| Sales of imitation fragrances at lower price points are intensifying competitive pressure | -0.4% | Global | Short term (≤ 2 years) |

| Use of aerosol propellants and packaging materials is raising environmental concerns | -0.3% | North America, Europe | Medium to long term |

| Source: Mordor Intelligence | |||

Stringent regulations governing fragrance ingredients and chemical formulations

Strict regulations on fragrance ingredients, chemical formulations, and product labeling are slowing the growth of the global perfumes and deodorants market. Governments and regulatory bodies in key markets are enforcing tougher rules to ensure ingredient safety, disclose allergens, and improve transparency for consumers. These changes are driving up compliance costs for manufacturers. For instance, the European Commission's Regulation (EU) 2023/1545 mandates more detailed allergen labeling, requiring companies to update packaging and product details across their portfolios[3]Source: European Commission, "Document 32023R1545", eur-lex.europa.eu. Similarly, the International Fragrance Association (IFRA) 51st Amendment imposes stricter limits on certain fragrance ingredients, forcing manufacturers to reformulate products to meet the new standards. These evolving regulations not only increase production and development costs but also extend the time required for product approvals.

Sales of imitation fragrances at lower price points are intensifying competitive pressure

The growing presence of imitation and fragrance-inspired products is intensifying competition in the global perfumes and deodorants market. These products mimic the scent profiles of premium and luxury fragrances but are sold at much lower prices, appealing to budget-conscious consumers and diminishing the exclusivity of original brands. This trend poses significant challenges for high-end fragrance manufacturers, as their success relies heavily on brand reputation, authenticity, and product uniqueness. Additionally, counterfeit products are becoming more prevalent, further complicating the market landscape. For example, in May 2026, Thai authorities arrested an individual in Bangkok for allegedly selling fake luxury perfumes online while falsely advertising them as genuine branded items. Such incidents highlight the growing difficulty for established brands to safeguard their intellectual property, maintain consumer trust, and differentiate themselves in a market crowded with low-cost alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Deodorant Volume Leads, Perfume Value Accelerates

In 2025, deodorants accounted for 63.67% of the perfumes and deodorants market, making them the leading product segment. Their widespread use in daily personal care routines across various age groups drives this dominance. Factors such as increasing awareness of personal hygiene, rapid urbanization, and the availability of deodorants at different price points contribute to their steady demand. Manufacturers are enhancing product offerings with features like long-lasting protection, skin-friendly ingredients, and multi-purpose applications, further boosting their popularity among consumers.

Perfumes are projected to be the fastest-growing segment, with a CAGR of 8.82% from 2026 to 2031. This growth is fueled by rising consumer interest in premium and niche fragrances that offer unique and personalized scent experiences. Higher disposable incomes, the expansion of online fragrance sales, and the influence of social media and celebrity endorsements are key factors driving demand. Moreover, frequent product innovations and the growing perception of fragrances as a lifestyle statement and a form of self-expression are expected to sustain the segment's growth during the forecast period.

By Ingredient Source: Synthetic Scale Persists, Natural Growth Accelerates

Synthetic and conventional formulations accounted for 85.36% of the perfumes and deodorants market revenue in 2025, establishing themselves as the leading formulation types. These formulations dominate due to their cost efficiency, reliable fragrance performance, and ability to deliver long-lasting scents at scale. They also provide manufacturers with greater flexibility in creating diverse fragrances, making them a preferred choice for mass-market products. As a result, companies continue to rely on synthetic ingredients to meet high consumer demand while maintaining competitive pricing.

Natural and organic formulations are projected to grow at the fastest rate, with a CAGR of 8.14% during the 2026–2031 period. This growth is driven by rising consumer preference for products with transparent ingredients, sustainability, and clean-label attributes. Many consumers now prioritize fragrances and deodorants free from synthetic chemicals, parabens, and artificial additives, especially in premium and wellness-focused segments. To cater to this demand, brands are expanding their natural product offerings and investing in plant-based ingredients and eco-friendly formulations.

By Price Range: Mass Commands the Market, Premium Grows Fastest

In 2025, mass-market products accounted for 53.42% of the perfumes and deodorants market revenue, making them the top-performing price segment. Their popularity stems from their affordability, easy availability, and widespread distribution through supermarkets, convenience stores, pharmacies, and online platforms. These products are designed for everyday use, leading to frequent purchases and high sales volumes. Ongoing product innovations and marketing campaigns have further boosted their adoption in both developed and emerging regions.

Premium and luxury products are expected to grow at a CAGR of 8.47% during the 2026–2031 period, making them the fastest-growing price segment. This growth is fueled by rising disposable incomes, a growing preference for unique and exclusive fragrances, and increasing demand for personalized scent options. Luxury brands benefit from features like premium packaging, niche formulations, and strong brand identity, which attract aspirational consumers. Furthermore, the expansion of online luxury retail and the influence of social media on fragrance discovery are anticipated to sustain demand throughout the forecast period.

By End User: Women's Share Remains Dominant, Men's Closes the Gap

In 2025, women accounted for 67.44% of global revenue in the perfumes and deodorants market, making them the largest consumer group. This dominance is attributed to frequent product usage, a broader range of fragrance options, and a strong focus on personal grooming and beauty. Companies are actively launching diverse scent collections, premium products, and specialized formulations to cater to female preferences. The rising emphasis on self-care and wellness continues to drive this segment's growth, solidifying its leading position in the market.

The men’s segment is projected to grow at the fastest rate, with a CAGR of 8.86% during the 2026–2031 period. Increasing awareness of personal grooming, higher spending on lifestyle products, and the availability of male-specific fragrances are key factors fueling this growth. Brands are expanding their offerings with premium, sports-inspired, and long-lasting products tailored to male consumers. Furthermore, evolving social attitudes toward grooming and the influence of digital marketing are expected to boost demand in the men’s segment throughout the forecast period.

By Distribution Channel: Physical Scale Holds, Digital Channel Accelerates

Supermarkets and hypermarkets accounted for 41.68% of the perfumes and deodorants market revenue in 2025, making them the top distribution channel. These outlets dominate due to their wide product selection, strong brand presence, and convenience as one-stop shopping destinations. Consumers benefit from the ability to compare various brands, fragrances, and prices in a single location. Promotional offers, attractive in-store displays, and their widespread availability make these retail formats a preferred choice for many buyers.

Online retail stores are expected to grow at the fastest rate, with a projected CAGR of 8.63% during 2026–2031. This growth is driven by increasing internet access, rising smartphone usage, and a growing preference for hassle-free shopping. E-commerce platforms provide customers with access to a diverse range of products, competitive pricing, and the convenience of reading reviews and receiving personalized recommendations. Furthermore, the rise of digital marketing, social media campaigns, and direct-to-consumer strategies is anticipated to further boost online sales of perfumes and deodorants during the forecast period.

Geography Analysis

North America held the largest share of the perfumes and deodorants market in 2025, accounting for 33.56%. This dominance is attributed to high consumer spending on personal care products, a robust retail infrastructure, and the widespread popularity of premium fragrances and deodorants. The United States leads the region, driven by continuous product innovations, celebrity-endorsed launches, and a growing online retail sector. Canada and Mexico are also key contributors, as global brands expand their presence in these markets.

The Asia-Pacific region is expected to witness the fastest growth in the perfumes and deodorants market, with a projected CAGR of 8.38% through 2031. Factors such as rapid urbanization, increasing disposable incomes, and heightened awareness of personal grooming are fueling this growth. The expanding middle-class population and evolving lifestyle preferences are boosting demand for both affordable deodorants and premium fragrances. Furthermore, the rise of modern retail and e-commerce platforms is making these products more accessible to consumers across the region.

Europe remains a significant market for perfumes and deodorants, supported by its strong fragrance heritage and a loyal consumer base. Countries like France, Germany, the United Kingdom, Italy, and Spain continue to dominate in fragrance consumption and innovation. The demand for luxury and premium fragrances remains robust, aided by well-established retail networks and travel retail channels. Meanwhile, South America and the Middle East & Africa are emerging as important markets, driven by increasing fragrance adoption, cultural preferences, and growing investments from international brands.

Competitive Landscape

The perfumes and deodorants market is consolidated with a few key players, including L'Oréal S.A., The Procter & Gamble Company, Unilever PLC, CHANEL Limited, and LVMH Moët Hennessy Louis Vuitton SE. These companies hold a significant market share due to their wide product ranges, strong brand reputations, and well-established distribution networks across various regions. They cater to both premium and mass-market segments, offering products that appeal to diverse consumer preferences. Their large-scale production capabilities and substantial marketing efforts give them a competitive edge in the market.

Competition in the market is shaped by factors such as expanding product portfolios, focusing on premium products, and acquiring strategic brands. Leading companies are investing heavily in their fragrance divisions, introducing high-end products to meet the growing demand for luxury and niche fragrances. At the same time, smaller, independent brands are gaining traction by offering unique scents, personalized options, and engaging younger consumers. This has created a competitive landscape where both large-scale operations and distinctive branding play crucial roles in achieving success.

Innovation is a key driver of growth in the perfumes and deodorants market. Companies are focusing on developing new products, such as whole-body deodorants, sustainable packaging, and formulations made with natural ingredients. Refillable packaging and eco-friendly solutions are also gaining popularity among consumers. While emerging brands leverage digital platforms to enter the market, established players benefit from their robust supply chains, regulatory expertise, and ability to make long-term investments. These strengths help major companies maintain their leadership positions in the evolving market.

Perfumes and Deodorants Industry Leaders

-

L'Oréal S.A.

-

The Procter & Gamble Company

-

Unilever PLC

-

CHANEL Limited

-

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Unilever expanded its whole-body deodorant portfolio in the United Kingdom by introducing new Dove products intended for use beyond underarm applications. This launch aligned with the company's strategy to meet the increasing consumer demand for holistic personal care and odor protection solutions.

- January 2026: Dove launched its first refillable anti-perspirant range, featuring reusable cases and interchangeable refills. This initiative aimed to promote more sustainable deodorant usage while ensuring 72-hour sweat and odor protection.

- December 2025: LVMH Luxury Ventures acquired a minority stake in niche fragrance house BDK Parfums to support the brand’s global expansion and enhance its position in the rapidly growing luxury fragrance market.

- July 2025: Rexona collaborated with lifestyle personality Martha Stewart to introduce its Whole Body Deodorant in Australia, accompanied by a marketing campaign emphasizing comprehensive body odor protection beyond conventional underarm use.

Global Perfumes and Deodorants Market Report Scope

Perfumes and deodorants are fragrance products that enhance personal hygiene and grooming by providing pleasant scents and controlling body odor. The global perfumes and deodorants market comprises product type, ingredient source, price range, end user, distribution, and geography. Based on product type, the market is classified into perfumes and deodorants. Based on ingredient source, the market is classified into natural/organic and synthetic/conventional. Based on price range, the market is classified into mass and premium/luxury. Based on end user, the market is classified into men, women, and unisex. Based on distribution channel, the market is classified into supermarkets/hypermarkets, drugstores and pharmacies, specialty stores, online retail stores, and other distribution channels. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Perfumes | Parfum/Extrait de Parfum |

| Eau de Parfum | |

| Eau de Toilette | |

| Eau de Cologne | |

| Deodorants | Spray Deodorants |

| Roll-On Deodorants | |

| Stick Deodorants | |

| Others |

| Natural/Organic |

| Synthetic/Conventional |

| Mass |

| Premium/Luxury |

| Men |

| Women |

| Unisex |

| Supermarkets/Hypermarkets |

| Drugstores and Pharmacies |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Perfumes | Parfum/Extrait de Parfum |

| Eau de Parfum | ||

| Eau de Toilette | ||

| Eau de Cologne | ||

| Deodorants | Spray Deodorants | |

| Roll-On Deodorants | ||

| Stick Deodorants | ||

| Others | ||

| By Ingredient Source | Natural/Organic | |

| Synthetic/Conventional | ||

| By Price Range | Mass | |

| Premium/Luxury | ||

| By End User | Men | |

| Women | ||

| Unisex | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Drugstores and Pharmacies | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected size of global perfumes and deodorants by 2031?

The global perfumes and deodorants market is forecast to reach USD 135.12 billion by 2031, rising from USD 95.49 billion in 2026, projected to grow at a 7.19% CAGR over 2026-2031.

Which product category is larger, deodorants or perfumes?

Deodorants are larger by current revenue and held 63.67% share in 2025, while perfumes are growing faster with a projected 8.82% CAGR through 2031.

Why is Asia-Pacific important for future growth?

Asia-Pacific is the fastest-growing region, projected to grow at 8.38% CAGR through 2031, supported by urbanization, rising middle-class spending, and wider personal grooming adoption.

Which sales channel is expanding the fastest?

Online retail stores are the fastest-growing channel, projected to grow at an 8.63% CAGR through 2031, helped by convenience buying, larger digital assortments, and brand storytelling.

Page last updated on: