Audience Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

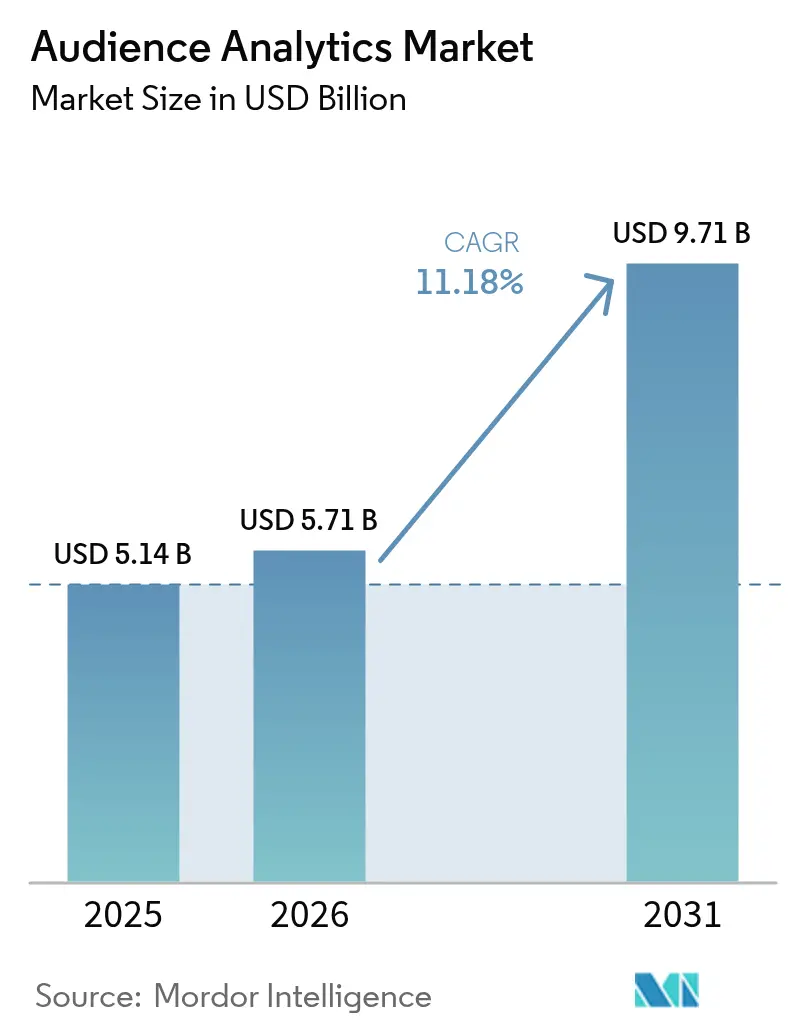

| Market Size (2026) | USD 5.71 Billion |

| Market Size (2031) | USD 9.71 Billion |

| Growth Rate (2026 - 2031) | 11.18% CAGR |

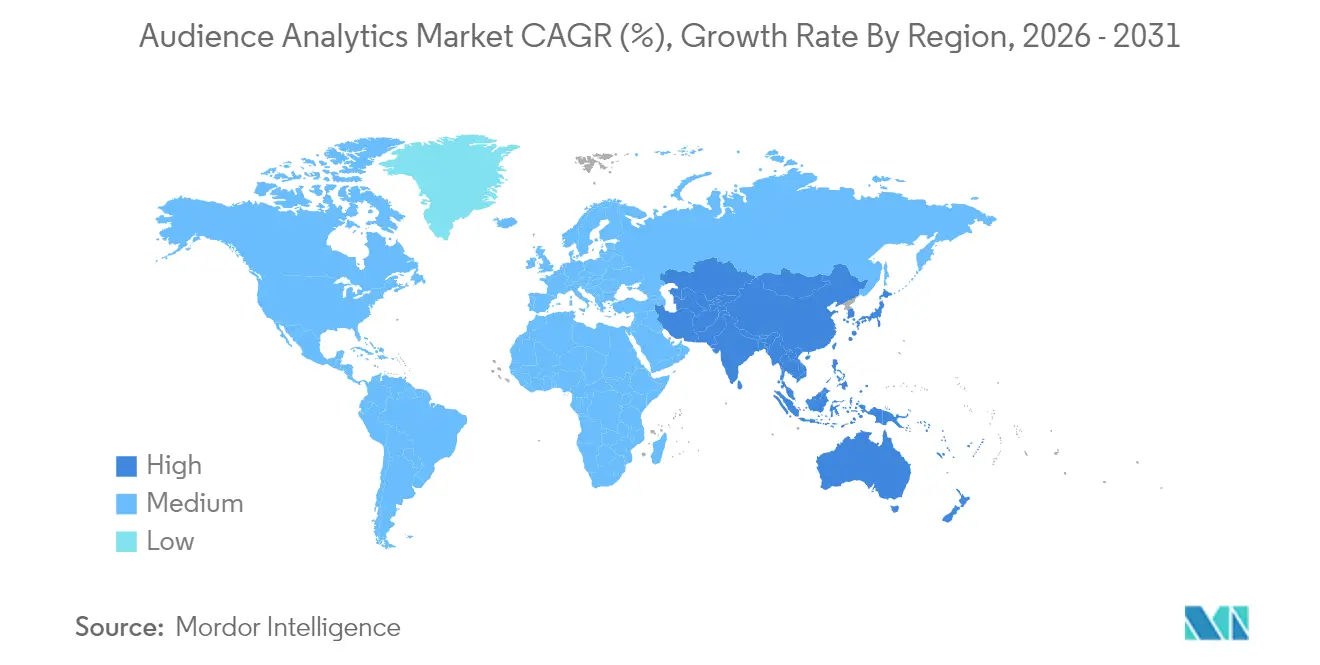

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

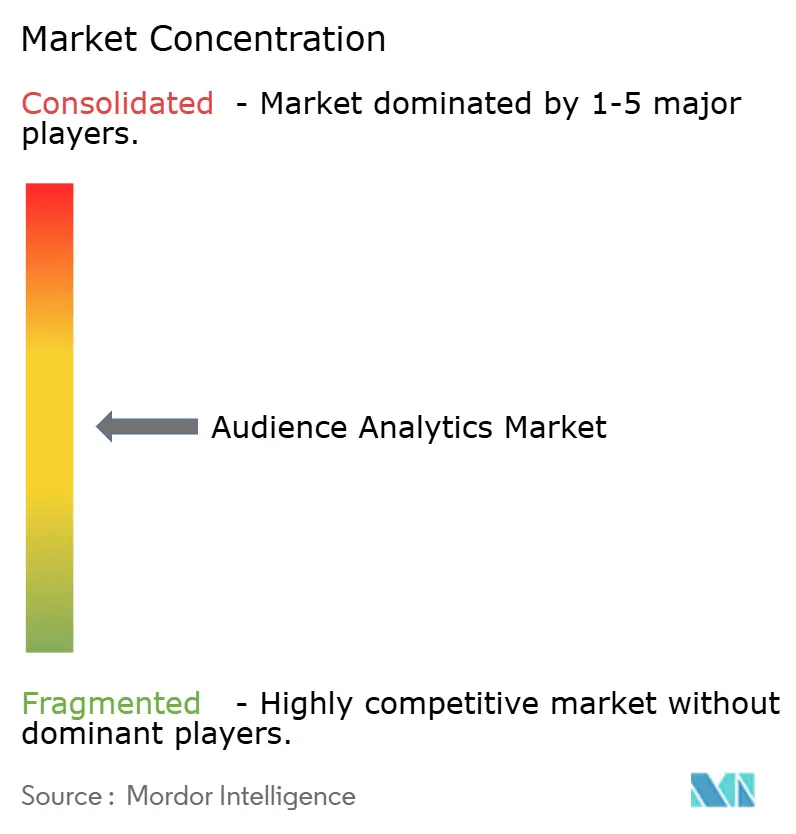

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Audience Analytics Market Analysis by Mordor Intelligence

The audience analytics market size was valued at USD 5.14 billion in 2025 and estimated to grow from USD 5.71 billion in 2026 to reach USD 9.71 billion by 2031, at a CAGR of 11.18% during the forecast period (2026-2031). Heightened demand for consent-based identity resolution, powerful AI toolkits, and the rapid monetisation of first-party data in retail media networks underpin this expansion. Organisations increasingly deploy real-time, edge-based analytics that protect privacy while generating actionable insights at the point of engagement. Solutions remain the largest revenue contributor, yet cloud-native services record the quickest growth as firms seek scalability and cost optimisation. Meanwhile, large enterprises dominate spending, but small and medium enterprises accelerate adoption thanks to no-code interfaces and consumption-based pricing models that lower entry barriers to sophisticated analytics.

Key Report Takeaways

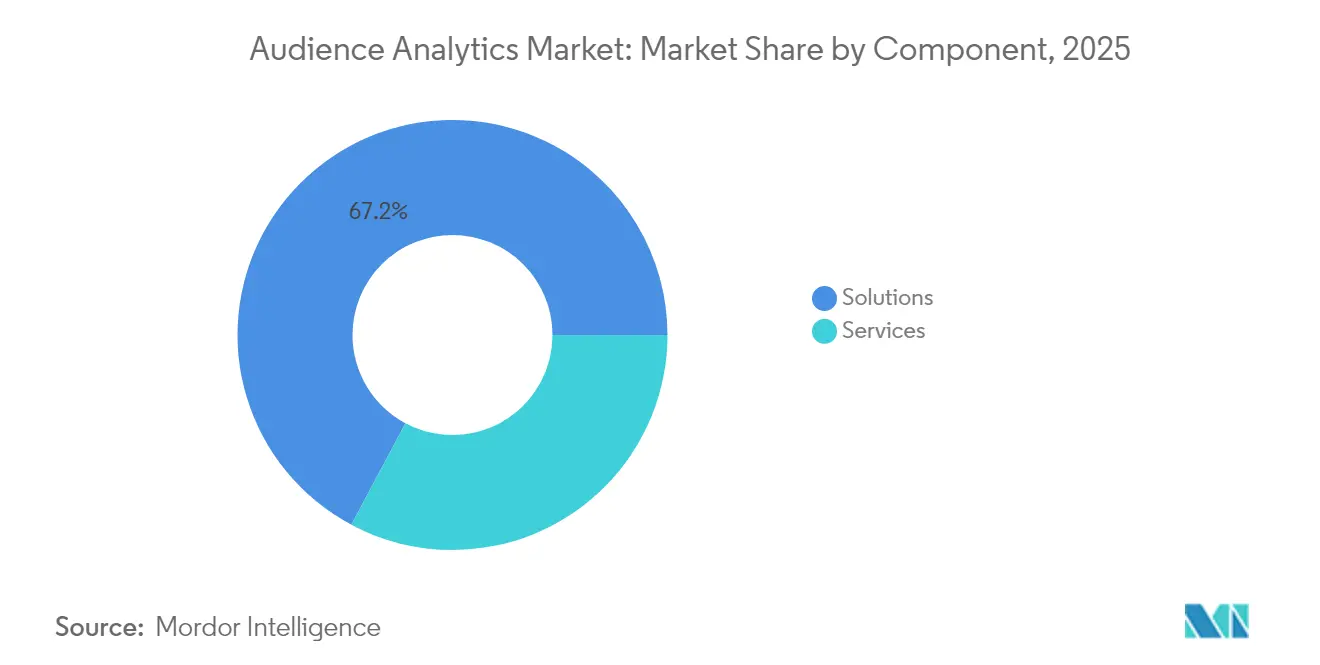

- By component, solutions retained 67.20% revenue share in 2025, while services are projected to grow at a 12.45% CAGR through 2031.

- By deployment mode, on-premises installations held 65.10% of the audience analytics market share in 2025; cloud deployments are forecast to expand at a 12.84% CAGR to 2031.

- By organisation size, large enterprises accounted for 70.50% of the audience analytics market size in 2025; SMEs record the highest projected CAGR at 12.32% to 2031.

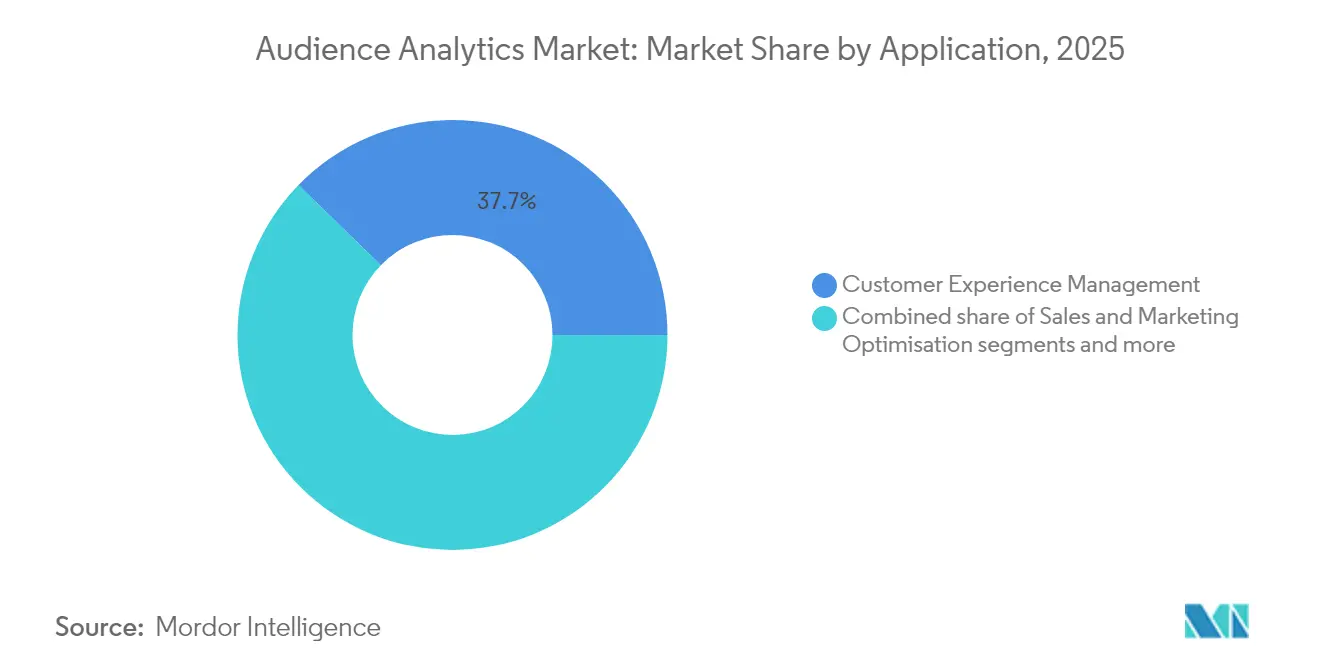

- By application, customer experience management led with 37.70% of the audience analytics market share in 2025, while fraud and risk analytics is advancing at an 11.62% CAGR to 2031.

- By end-user industry, media and entertainment contributed 35.60% of 2025 revenue; retail and e-commerce is forecast to grow at an 11.38% CAGR through 2031.

- By geography, North America commanded 39.90% of 2025 revenue; Asia-Pacific is progressing at a 11.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Audience Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in omnichannel first-party data collection | +2.1% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Surging adoption of AI/ML-powered predictive analytics | +1.8% | Global, with Asia-Pacific showing fastest implementation | Short term (≤ 2 years) |

| Media and entertainment shift to real-time audience monetisation | +1.4% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| Cookieless marketing pushes demand for consent-based identity graphs | +1.6% | Global, with GDPR and CPRA regions driving urgency | Short term (≤ 2 years) |

| Retail media networks scaling first-party shopper insights | +1.3% | North America leading, with Europe and APAC following | Medium term (2-4 years) |

| Edge analytics on devices enabling privacy-preserving insights | +1.2% | Global, with mobile-first markets in APAC accelerating | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Omnichannel First-Party Data Collection

Brands are rebuilding data architectures around owned interaction points, integrating in-store behaviour, mobile engagement, and connected-device signals. Retailers now operate sophisticated media networks that align physical and digital journeys, opening USD-level revenue channels once dominated by third-party data brokers. The ability to merge offline and online insights improves lifetime value modelling and elevates segmentation precision.

Surging Adoption of AI/ML-Powered Predictive Analytics

Machine-learning algorithms now underpin behavioural modelling, conversion prediction, and automated cohort creation across mainstream platforms. Google Analytics 4 and Adobe Experience Cloud showcase AI engines that slash insight latency from weeks to minutes while improving forecast accuracy by more than 30%[1]Adobe, “Introducing GenStudio Content Analytics,” business.adobe.com. Cloud delivery makes these functions accessible to mid-market firms previously constrained by infrastructure costs and talent shortages.

Media and Entertainment Shift to Real-Time Audience Monetisation

Streaming services and broadcasters combine panel and big-data streams to optimise content placement and dynamically price ads. Nielsen’s Big Data + Panel system fuses linear and streaming consumption metrics, enabling monetisation tactics that adapt instantly to engagement patterns. Audience feedback now informs production choices, merchandising, and interactive experiences across traditional and emerging channels.

Cookieless Marketing Pushes Demand for Consent-Based Identity Graphs

Marketers respond to cookie deprecation by investing in hashed-email IDs, contextual analysis, and location signals that respect privacy. Nielsen reports that three-quarters of marketers still depend on cookies, fuelling rapid migration to alternative identifiers and robust consent mechanisms. Vendors able to marry privacy compliance with insight depth gain competitive advantage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing privacy-first regulation (GDPR, CPRA, DMA) | -1.4% | Europe and California leading, expanding globally | Short term (≤ 2 years) |

| Data-engineering skill shortages among SME users | -1.1% | Global, with North America and Europe most affected | Medium term (2-4 years) |

| Rising cloud-compute costs for petabyte-scale analytics workloads | -0.8% | Global, with cloud-heavy regions experiencing higher impact | Medium term (2-4 years) |

| Fragmentation of identity solutions hinders interoperability | -0.9% | Global, with mature digital advertising markets most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Privacy-First Regulation

GDPR, CPRA, and the Digital Markets Act compel firms to re-engineer data flows, often diverting 15-20% of analytics budgets to compliance efforts. Privacy-preserving solutions, such as cookieless web analytics, reduce dependence on personal identifiers while sustaining behavioural insight quality. Vendors tout contextual targeting and edge processing to balance regulatory demands with commercial goals.

Data-Engineering Skill Shortages Among SME Users

A persistent talent gap hampers smaller enterprises that wish to operationalise advanced analytics pipelines. Industry surveys show businesses struggling to hire professionals who can deploy machine-learning models and manage privacy-centric data architecture. As a result, demand grows for managed services, no-code platforms, and packaged analytics that minimise technical overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Maintain Scale While Services Accelerate

Solutions generated 67.20% of 2025 revenue and remain the backbone of the audience analytics market. They comprise data-integration hubs, customer data platforms, and AI inference engines that enable cross-channel insight generation. Organisations invest heavily at the outset in scalable infrastructures, creating high switching costs and entrenched vendor relationships. Services, however, achieve a 12.45% CAGR as firms outsource expertise in identity resolution, model governance, and compliance auditing. Managed offerings deliver continuous optimisation and bridge the data-engineering talent gap, elevating overall project success rates.

The rise of analytics-as-a-service signals a strategic shift from perpetual licences to consumption-based engagements. Consultancies and system integrators package technology stacks with advisory support, ensuring business objectives drive implementation choices. As privacy regulation tightens, specialised services in consent management and edge deployment command premium pricing, accelerating the revenue mix transition toward recurring professional support.

By Deployment Mode: Cloud Gains Momentum Despite On-Premises Leadership

On-premises systems held 65.10% of the audience analytics market share in 2025, reflecting enduring concerns over data sovereignty and latency for high-volume streaming analyses. Sectors such as banking and government rely on self-hosted platforms to retain sensitive personally identifiable information. Nevertheless, cloud instances grow at a 12.84% CAGR as vendors implement region-specific encryption, sovereign-cloud options, and advanced compliance certifications. Adobe’s joint offering with AWS exemplifies tailored cloud solutions for real-time customer profiling.

Hybrid architectures surface as the prevailing model, retaining golden customer profiles on-premises while bursting compute-intensive workloads to the cloud. This arrangement curbs infrastructure capital expenditure and unlocks elastic processing for seasonal campaigns and sudden surges in data ingestion. The audience analytics market size represented by cloud deployments is forecast to overtake on-premises revenue in the post-2030 horizon as confidence in public-cloud security matures.

By Organisation Size: Democratised Analytics Fuels SME Uptake

Large enterprises spent the most in 2024, but SMEs register the highest growth rate at 12.32%. Cloud-native platforms and flexible subscription tiers remove historical capital barriers, enabling smaller brands to adopt product-analytics suites and basic AI forecasting. Vendors such as Amplitude embed step-by-step wizards and templated dashboards that condense deployment cycles into days, not months.

SME adoption is also driven by the imperative to personalise digital storefronts amid intensifying competition. Pay-as-you-go pricing aligns analytics investment with revenue, encouraging iterative experimentation instead of multi-year, fixed-fee contracts. Meanwhile, large enterprises continue to dominate the audience analytics market size for complex omnichannel orchestration initiatives that demand extensive data-cleansing and integration effort.

By Application: Customer Experience Leads; Fraud Analytics Surges

Customer experience management tools controlled 37.70% of 2025 revenue as every sector aligns growth objectives with end-to-end journey insight. Real-time personalisation engines amplify conversion rates and upsell potential, embedding analytics directly into engagement workflows. Fraud and risk analytics, advancing at 11.62% CAGR, responds to deepfake-enabled scams and synthetic-identity attacks that bypass rule-based detection. Behavioural biometrics and anomaly-detection models analyse velocity, device, and usage patterns to identify malicious activity without user friction.

Sales and marketing optimisation remains a mature yet evolving use case, integrating next-best-action logic powered by predictive intent signals. Competitive intelligence platforms sift public data and media consumption to benchmark brand performance. Finally, product and content development teams use engagement heatmaps and cohort analyses to guide feature roadmaps and storyline investment, tightening feedback loops between audience preference and creation.

By End-User Industry: Media and Entertainment Leads as Retail Accelerates

Media and entertainment organisations contributed 35.60% of 2025 revenue, leveraging cross-platform measurement to justify rising content budgets. Streaming providers refine release schedules and ad inventory pricing with real-time viewing analytics, while video-game studios track in-game behaviour to balance difficulty and monetisation elements. Retail and e-commerce, growing at an 11.38% CAGR, capitalise on first-party shopper data harvested from loyalty apps, click-and-collect services, and connected point-of-sale sensors.

Telecom carriers combine geospatial analytics and churn-propensity scoring to prioritise retention outreach. BFSI institutions monitor transaction fingerprints for fraud and personalise credit offers using audience analytics market insights. Healthcare entities apply privacy-preserving analytics to improve patient adherence and outreach, albeit under strict regulatory oversight. Government agencies employ usability analytics to streamline digital services and enhance citizen engagement.

Geography Analysis

North America held 39.90% revenue in 2025, anchored by a sophisticated advertising ecosystem, heavy technology investment, and early adoption of privacy-first tools. United States retailers such as Walmart and Target lead in retail media revenue generation, while Canada benefits from progressive privacy laws that nudge firms toward compliant analytics architectures. Mexico’s accelerating e-commerce adoption widens the regional user base for scalable, cloud-delivered insight engines.

Europe sits in a steady growth phase shaped by GDPR and the Digital Markets Act, which elevate demand for consent-based solutions that minimise personal data dependence. Germany and the United Kingdom endorse edge-processing pilots that keep data resident, reducing cross-border transfer complexity. France and Italy explore contextual targeting to maintain advertising efficiency. Independent vendors that can interoperate across multiple identity frameworks attract mid-market adopters seeking flexible compliance.

Asia-Pacific is the fastest-growing region at a 11.96% CAGR, supported by a USD 880 billion mobile economy and 1.8 billion mobile subscribers. China pioneers social commerce analytics that blend video, messaging, and payments, creating granular, real-time insight streams. India’s fintech boom expands transactional datasets, while Japan and South Korea integrate audience analytics into gaming ecosystems to optimise retention. Australia and New Zealand embrace enterprise analytics to support omnichannel retail and public-service modernisation. Rising smartphone penetration and government digital initiatives propel additional demand across Southeast Asia, reinforcing long-term momentum for the audience analytics market.

Competitive Landscape

The competitive field is moderately fragmented. Technology conglomerates such as Adobe, Google, and Microsoft offer integrated stacks that embed data collection, identity resolution, and AI orchestration within broader cloud suites. Specialist providers—including Nielsen, Amplitude, and Mixpanel—focus on media measurement, product analytics, and experimentation workflows, respectively, capturing share through domain depth and product-led uptake.

Strategic activity centres on three themes. First, AI-native capabilities accelerate insight generation; Adobe’s autonomous agents orchestrate experiences across channels without manual segmentation. Second, cross-platform measurement alliances, such as the Nielsen-LiveRamp collaboration, extend reach from linear TV to connected devices, providing unified attribution. Third, privacy-preserving innovation drives differentiation, with edge analytics firms promising compliance and cost savings by processing data on device.

Convergence and partnership remain common as vendors fill capability gaps. Cloud providers embed analytics functions directly into data-warehouse offerings, while systems integrators package vertical solutions for healthcare, retail, and public sector. Emerging challengers target ease of use, launching low-code orchestration and transparent pricing models that appeal to resource-constrained teams. The result is an ecosystem where no single player commands outsized dominance, yet brand scale and continuous innovation dictate competitive positioning.

Audience Analytics Industry Leaders

Oracle Corporation

Adobe Inc.

IBM Corporation

Google LLC

JCDecaux Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Adobe rolled out AI agents across Experience Cloud, enabling automated, cross-channel experience orchestration for real-time personalisation.

- March 2025: Adobe expanded GenStudio with Content Analytics to measure asset performance and streamline high-volume content workflows.

- January 2025: Nielsen announced a 3,000-person expansion in India, opening technology centres in Hyderabad and Gurgaon to support retail and gaming analytics offerings.

- December 2024: Adobe and Amazon Web Services extended their partnership, bringing Adobe Experience Platform to AWS for unified data management and AI-driven insights.

- November 2024: Amplitude posted Q3 2024 results with 9% ARR growth and launched “Amplitude Made Easy,” simplifying onboarding for product analytics customers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the audience analytics market as all software and related support services that collect, join, and algorithmically interpret first-, second-, and permitted third-party data to profile, segment, and predict audience behavior across digital and physical channels. Solutions that cover pure web traffic measurement, generic BI dashboards, or non-consented data scraping remain outside this boundary.

Scope Exclusion: Stand-alone web-analytics tools that lack identity resolution or advanced segmentation are excluded.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- On-premises

- Cloud

- By Organisation Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Application

- Sales and Marketing Optimisation

- Customer Experience Management

- Competitive/Media Intelligence

- Product and Content Development

- Fraud and Risk Analytics

- By End-user Industry

- Media and Entertainment

- Retail and eCommerce

- BFSI

- Telecom and IT

- Healthcare and Life Sciences

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

To ground secondary findings, we interviewed marketing technology architects, data-privacy officers, and CX leaders in North America, Europe, and Asia. Short surveys with regional system integrators and SaaS resellers helped us validate price points, deployment mix, and near-term demand triggers.

Desk Research

We began by mapping installed-base indicators and revenue pools from public sources such as the US Bureau of Economic Analysis, the Interactive Advertising Bureau, Eurostat, StatCan, and reports released by the World Federation of Advertisers. Annual reports, 10-Ks, and investor day decks from leading platform providers supplied channel-level adoption signals. Subscription databases that Mordor analysts access, D&B Hoovers for company financials, Dow Jones Factiva for deal flow, and Questel for patent intensity, added longitudinal depth. A wider scan of trade journals, patent filings, and tender notices completed the secondary picture. This list is illustrative; many other sources were reviewed for cross-checks and clarification.

Market-Sizing & Forecasting

Top-down sizing starts with global digital advertising and CRM spending, which is then filtered through audience-addressable share, solution penetration, and average license plus service fees. Select bottom-up checks, supplier roll-ups and sampled average selling price multiplied by active installations, tighten the range. Key variables include consent-based identity graph adoption, cloud migration rates, real-time analytics share, regulatory enforcement timelines, average cost per thousand addressable profiles, and macro advertising outlay. Forecasts rely on multivariate regression with scenario analysis, and the variable inputs are stress-tested with expert consensus before finalization. Gaps in granular spend data are bridged by weighted proxies from comparable martech sub-segments.

Data Validation & Update Cycle

Each draft model is peer-reviewed, variance-checked against independent benchmarks, and revisited whenever material events occur. Reports refresh annually, and just before delivery, an analyst performs a fresh validation pass so clients receive the latest view.

Why Mordor's Audience Analytics Baseline Commands Reliability

Published estimates can differ because firms pick unique scopes, input metrics, and refresh cadences.

Key gap drivers often include whether services revenue is counted, how adjacent web or social-media analytics are folded in, the currency year applied, and the aggressiveness of price-compression assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.14 B (2025) | Mordor Intelligence | - |

| USD 5.00 B (2024) | Regional Consultancy A | Excludes implementation services and uses narrow component scope |

| USD 6.30 B (2023) | Global Consultancy B | Includes broader social-media analytics and applies historical FX uplift |

The comparison shows that our disciplined scope selection, balanced top-down plus bottom-up validation, and yearly refresh give decision-makers a dependable starting point, while other figures swing wider due to either restrictive or overly inclusive assumptions.

Key Questions Answered in the Report

What is the current size of the audience analytics market?

The market is valued at USD 5.71 billion in 2026 and is forecast to reach USD 9.71 billion by 2031.

Which segment is growing fastest within the audience analytics market?

Cloud deployments exhibit the quickest expansion at a 12.84% CAGR as organisations shift workloads for scalability and cost efficiency.

Why are retail media networks important to audience analytics?

Retailers leverage first-party shopper data to create high-margin advertising channels, making audience analytics core to monetising these insights.

How do privacy regulations impact audience analytics adoption?

GDPR and CPRA drive investment in consent-based identity graphs and edge processing, adding compliance costs yet encouraging privacy-preserving innovation.

Which region offers the greatest growth potential?

Asia-Pacific leads with a projected 11.96% CAGR, propelled by a USD 880 billion mobile economy and expanding digital-first consumer base.

What role does AI play in modern audience analytics?

AI accelerates behavioural modelling and automated segmentation, reducing time-to-insight from weeks to minutes and improving predictive accuracy by 30% or more.

Page last updated on: