Penetration Testing And Ethical Hacking Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

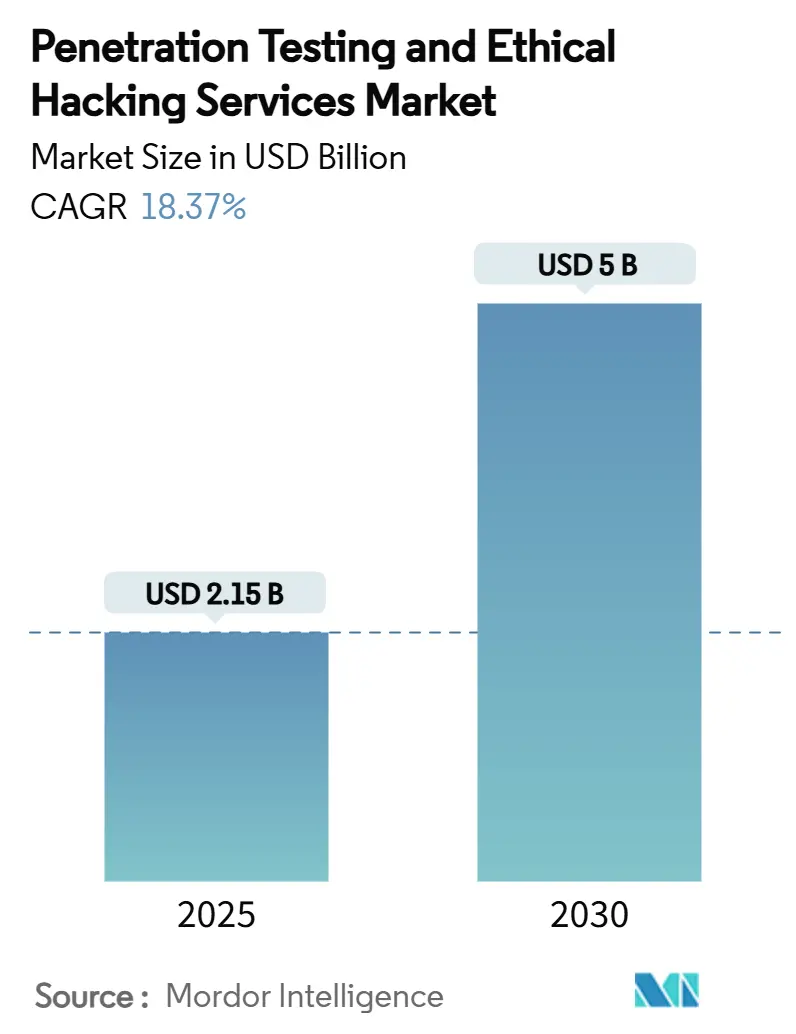

| Market Size (2025) | USD 2.15 Billion |

| Market Size (2030) | USD 5 Billion |

| Growth Rate (2025 - 2030) | 18.37% CAGR |

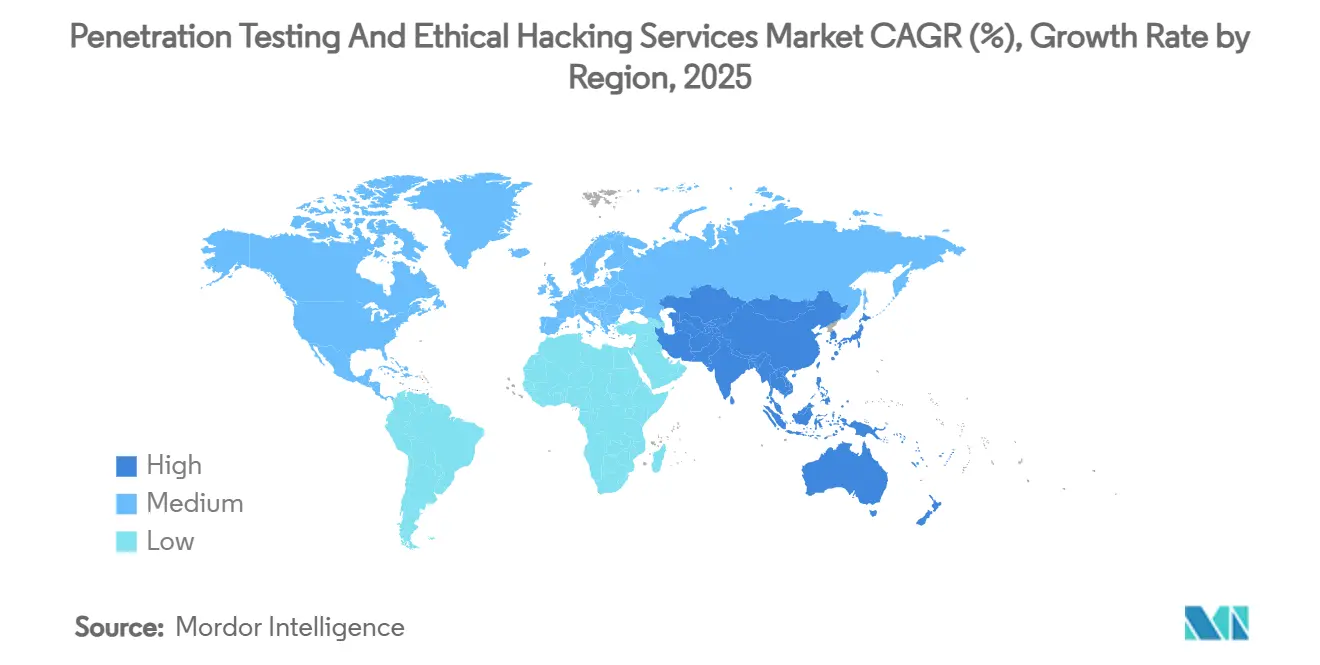

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

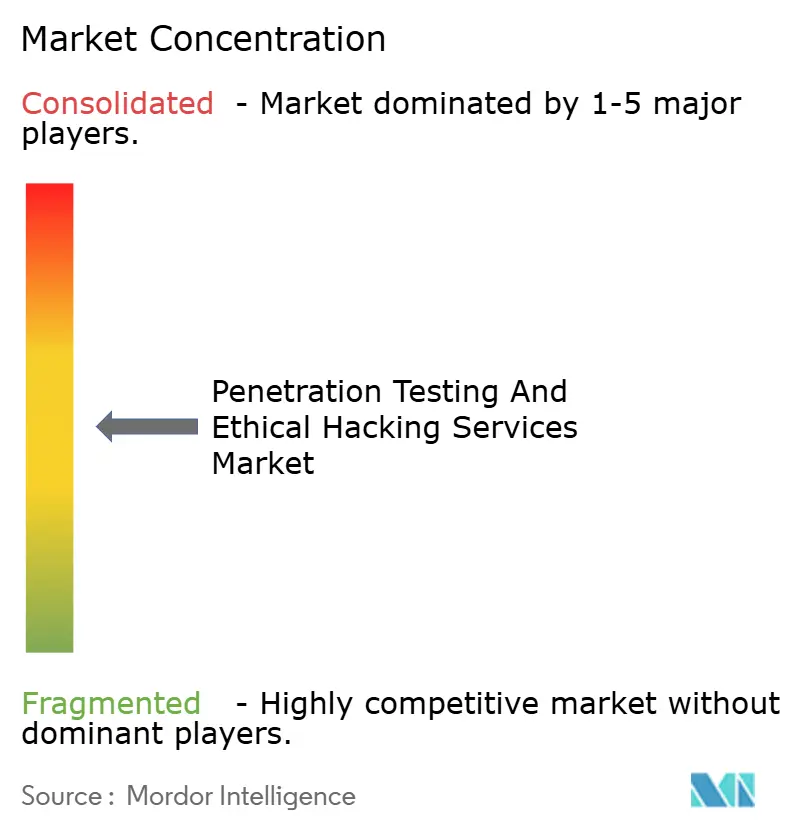

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Penetration Testing And Ethical Hacking Services Market Analysis by Mordor Intelligence

The Penetration Testing And Ethical Hacking Services Market size is USD 2.15 billion in 2025 and is forecast to reach USD 5.00 billion in 2030, advancing at an 18.37% CAGR. Heightened adversary sophistication, expanding regulatory obligations, and the migration of workloads into cloud and edge environments pivot security budgets toward proactive validation rather than reactive patching. Weaponized red-team tools such as Cobalt Strike and Metasploit accounted for nearly 50% of all malware activity in 2024, underscoring the need for continuous security testing that mirrors real-world attack chains. Mandatory frameworks—from PCI DSS 4.0 in payments to the European Union’s Digital Operational Resilience Act (DORA) in finance—formalize penetration testing as a compliance gate rather than a “best-effort” control. Simultaneously, AI-enabled purple-team platforms shorten test cycles and automate low-value tasks, freeing scarce ethical hackers for complex threat hunting. The Penetration Testing And Ethical Hacking Services Market, therefore, evolves from one-off engagements into subscription-based validation services integrated directly into CI/CD and DevSecOps pipelines.

Key Report Takeaways

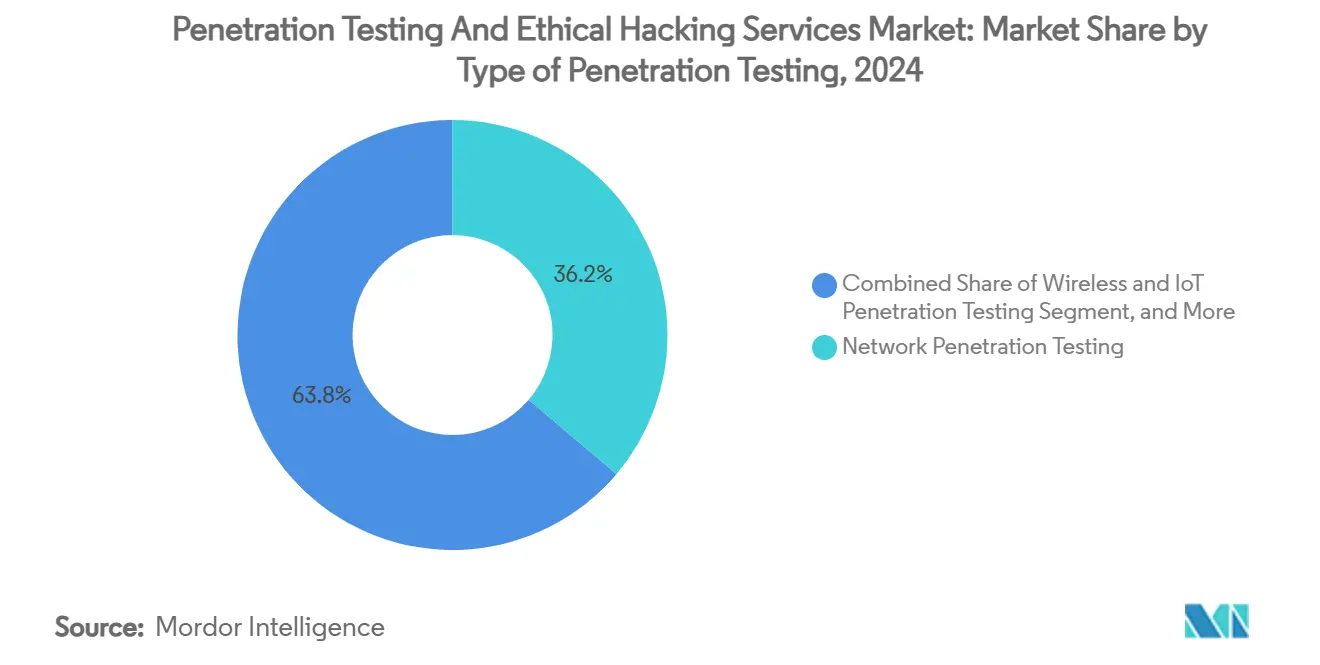

- By type of penetration testing, network testing led with 36.2% of the Penetration Testing And Ethical Hacking Services Market share in 2024, while cloud-configuration testing is set to expand at a 28.1% CAGR through 2030.

- By service model, consulting engagements held a 52.3% share of the Penetration Testing And Ethical Hacking Services Market size in 2024; Penetration Testing-as-a-Service (PTaaS) is projected to grow at a 29.1% CAGR to 2030.

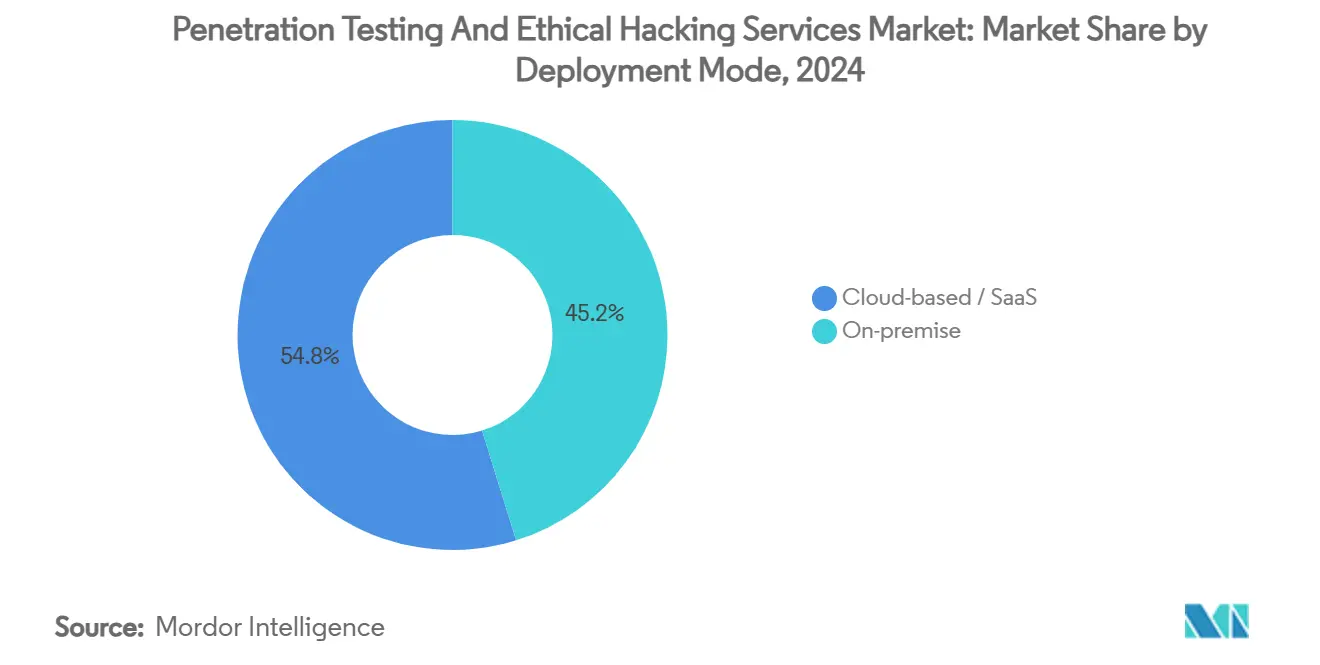

- By deployment, on-premise solutions accounted for 63.3% of the Penetration Testing And Ethical Hacking Services Market size in 2024, whereas cloud-based offerings are advancing at a 27.1% CAGR over the forecast period.

- By end-use, BFSI captured a 30.2% share of the Penetration Testing And Ethical Hacking Services Market size in 2024, while healthcare is forecast to grow at a 24.1% CAGR through 2030.

- By geography, North America commanded a 42.2% share in 2024; Asia-Pacific is the fastest-growing region at a 22.1% CAGR to 2030.

Global Penetration Testing And Ethical Hacking Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating sophistication and volume of cyber-attacks | +4.2% | Global, with concentrated impact in North America and Europe | Short term (≤ 2 years) |

| Mandatory compliance audits and cybersecurity regulations | +3.8% | Global, with regulatory leadership in the EU and North America | Medium term (2-4 years) |

| Surge in cloud, IoT, and edge deployments expanding attack surface | +3.5% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Board-level cyber-insurance underwriting requirements for independent testing | +2.1% | North America and the EU, emerging in the Asia-Pacific | Long term (≥ 4 years) |

| AI-enabled purple-teaming is accelerating continuous testing adoption | +2.8% | North America and Europe, early adoption in the Asia-Pacific | Short term (≤ 2 years) |

| Expansion of bug-bounty platforms legitimising crowdsourced testing | +1.9% | Global, with platform concentration in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication and Volume of Cyber-Attacks

Attackers increasingly repurpose legitimate red-team frameworks, compressing their time-to-breach and highlighting gaps in periodic audit schedules. AI-assisted recon tools map exposed assets at machine speed, enabling near real-time pivoting between vectors. Consequently, organizations adopt continuous Penetration Testing And Ethical Hacking Services Market offerings that embed assessments directly into DevOps pipelines, ensuring vulnerabilities are surfaced before code reaches production. Automated scanners now identify low-complexity flaws, allowing expert testers to invest effort into chained, logic-based exploits that mimic advanced persistent threats. This reallocation of human capital is crucial amid a global shortfall of 2.8 million cybersecurity professionals.

Mandatory Compliance Audits and Cybersecurity Regulations

Regulators have transitioned from recommending to mandating threat-led penetration testing, embedding it into supervisory review cycles across financial, healthcare, and critical-infrastructure sectors. PCI DSS 4.0 alone inserts 63 new requirements effective March 2024, pushing merchants to broaden test scope and frequency.[1]Andrew Vine, “The Impact of PCI DSS 4.0 on Organizational Penetration Testing Strategies,” Kroll, kroll.com DORA aligns European banks on common threat-led frameworks, reducing duplication for cross-border operations yet raising the bar for test rigor. G-7 guidelines further harmonize approaches, allowing multinational corporates to deploy standardised methodologies globally. These converging rules assure that the Penetration Testing And Ethical Hacking Services Market expands even in cyclical downturns because audit deadlines remain non-negotiable. Vendors able to map their deliverables to multiple frameworks simultaneously gain a competitive lift.

Surge in Cloud, IoT, and Edge Deployments Expanding Attack Surface

Cloud misconfiguration has overtaken endpoint exploitation as the leading breach root cause, prompting demand for specialised configuration reviews. Shared-responsibility models require tenants to secure workloads while providers protect the substrate, splitting accountability and complicating audit readiness. IoT deployments now exceed 19 billion connected devices, each contributing new protocol quirks and firmware-level flaws. Edge nodes further distribute compute and data, multiplying attack entry points. Frameworks such as PETIoT formalise device-centric testing procedures that account for hardware, radio, and cloud integrations. Consequently, cloud configuration and IoT testing fuel the fastest sub-segment growth inside the Penetration Testing And Ethical Hacking Services Market.

AI-Enabled Purple-Teaming Accelerating Continuous Testing Adoption

Machine-learning engines inside modern testing suites auto-prioritise exploit paths based on contextual risk, enabling red and blue teams to iterate rapidly in shared “purple” engagements. Predictive analytics recommend counter-measures while an attack is still unfolding, shortening the mean time to remediation. AI also analyses historical test data to suggest new scenarios tailored to a client’s architecture, creating bespoke playbooks without manual scripting. As a result, the Penetration Testing And Ethical Hacking Services Market sees demand shift toward platforms bundling continuous assessment, attack-surface management, and remediation orchestration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shortage of skilled ethical hackers | -2.8% | Global, with acute shortages in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| High cost of comprehensive tests for SMEs | -1.9% | Global, with a pronounced impact in developing economies | Medium term (2-4 years) |

| Price erosion from commoditised automated tooling | -1.5% | North America and Europe, spreading to the Asia-Pacific | Short term (≤ 2 years) |

| Cross-border legal uncertainty over "offensive" security work | -0.8% | Global, with regulatory complexity in the EU and the Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Skilled Ethical Hackers

Only 72% of cyber roles are currently filled worldwide, and offensive specialists comprise an even smaller slice of that workforce. High-demand verticals such as finance and technology compete aggressively for the same talent pool, inflating salaries and extending project lead times. In Asia-Pacific, where digital transformation is fastest, ethical-hacker deficits widen implementation gaps, compelling buyers to outsource to global PTaaS providers. Vendors leverage internal academies and apprenticeship programs to cultivate talent, yet ramp-up cycles remain lengthy, placing structural drag on Penetration Testing And Ethical Hacking Services Market capacity.

High Cost of Comprehensive Tests for SMEs

Full-scope penetration engagements range from USD 2,500 to USD 50,000 per cycle, whereas more than half of the world’s SMEs allocate under USD 500 annually to total cybersecurity spend.[2]Kenneth Webb, “Penetration Testing Costs: Pricing Models and Cost Factor,” Strike Graph, strikegraph.com Automated scanners lower entry barriers but often generate high false-positive rates, confusing resource-strapped IT teams. SME boards, therefore, postpone assessments until mandated by customers or insurers, leaving latent vulnerabilities unaddressed. Vendors respond with tiered PTaaS subscriptions, yet price remains the primary hurdle in emerging economies, dampening total addressable Penetration Testing And Ethical Hacking Services Market growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Penetration Testing: Cloud Configuration Overtakes Perimeter-Centric Approaches

Cloud configuration testing delivered the fastest 28.1% CAGR forecast, even though network testing still contributed the largest 36.2% slice of the Penetration Testing And Ethical Hacking Services Market share in 2024. Misconfigured identity roles, excessive permissions, and unchecked storage buckets now account for a growing proportion of breach root causes, prompting boards to prioritise cloud-specific audits. Continuous integration of configuration-drift detection inside PTaaS platforms means findings surface minutes after code commits, not months after annual reviews. Over the period, web and application testing maintain steady traction, supported by persistent digital-commerce expansion. Wireless and IoT testing rises as factories and hospitals connect asset fleets, driving niche demand for radio-frequency and protocol-fuzzing skills. Social-engineering assessments also gain salience because phishing exploits remain gateway vectors for multi-stage attacks. Vendors harmonise human-centric and technical tests within a single statement of work, reflecting an integrated view of organisational risk.

The Penetration Testing And Ethical Hacking Services Market size for cloud-configuration engagements is therefore projected to outstrip historical perimeter-oriented spending, signalling a pivot toward asset-centric validation. Frameworks such as PETIoT illustrate another growth node by formalising workflows for device firmware, mesh networking, and OTA update verification. Meanwhile, AI-focused testing methodologies look at data-poisoning, model-theft, and inference attacks, rounding out a segment mix that is far more heterogeneous than in 2024. Providers that develop repeatable methodologies for these emerging vectors will capture outsized wallet share as clients migrate beyond classic network assessments.

By Service Model: PTaaS Disrupts Consulting Dominance

Consulting retained 52.3% of 2024 revenue, yet PTaaS is expanding at a head-turning 29.1% CAGR. Buyers prize real-time dashboards, ticketing integration, and the ability to retest automatically once patches deploy. Continuous and managed testing options sit between pure PTaaS and project-based consulting, offering scheduled sprints alongside on-demand retesting. Vendors such as HackerOne leverage crowdsourced hacker communities to scale skill diversity, evidenced by a 200% jump in AI red-team bookings during Q2 2024.

As DevSecOps matures, enterprises consolidate around providers that can embed automated workflows into CI/CD pipelines while still supplying expert analysis for chained exploits. Consequently, the Penetration Testing And Ethical Hacking Services Market size attached to subscription service lines approaches parity with consulting revenues by decade-end. Providers unable to productise their know-how face margin compression as automated tooling commoditises basic test steps.

By Deployment Mode: Hybrid Security Architectures Shape Procurement

On-premises deployments held 63.3% revenue in 2024, reflecting regulatory directives and legacy environments where sensitive data must remain on-site. Yet cloud-hosted platforms, advancing at 27.1% CAGR, offer scalability, collaborative reporting, and automatic integration with cloud-native services. A hybrid model therefore prevails: enterprises run critical internal audits locally but consume specialised external tests—especially for cloud misconfiguration—through SaaS portals. Vendors integrate role-based access controls, encryption, and regional data centres to address sovereignty concerns, easing migration hesitancy.

The penetration testing industry now treats deployment flexibility as table stakes. Solutions expose APIs that feed results into SIEM, SOAR, and GRC systems, allowing stakeholders to track remediation within unified dashboards. Over time, this interoperability becomes a procurement criterion as important as technical depth, influencing vendor short-lists and contractual renewals.

By End-Use Industry: Healthcare Surges, BFSI Holds Anchor Position

BFSI contributed 30.2% of 2024 revenue thanks to stringent audit obligations, mature threat-intelligence programs, and generous security budgets. PCI DSS 4.0, SWIFT CSP, and cyber-insurance clauses oblige banks and processors to commission regular threat-led assessments, guaranteeing baseline demand irrespective of macro cycles. Healthcare, by contrast, expands at a 24.1% CAGR as electronic medical record integration and connected-medical-device adoption widen the attack canvas. Ransomware targeting of hospitals during pivotal care windows elevates board scrutiny, accelerating contract award cycles.

Retail and e-commerce maintain steady growth anchored by payment-data protection mandates, while energy and utilities invest to secure operational-technology networks that now interconnect with IT domains. Government and defence agencies, driven by national-security imperatives, continue to issue multi-year penetration-testing frameworks, though procurement remains lengthy. Overall, sectoral diversification cushions the Penetration Testing And Ethical Hacking Services Market against spending shocks in any single vertical.

Geography Analysis

North America commanded 42.2% revenue in 2024 on the back of early PTaaS adoption, deep consultant pools, and a venture-backed supplier ecosystem. North America’s Penetration Testing And Ethical Hacking Services Market dominance rests on regulatory maturity, robust venture funding, and concentrated talent availability. Federal mandates oblige critical-infrastructure operators to undergo red-team exercises, while private enterprises treat continuous validation as a prerequisite for cyber-insurance underwriting. The prevalence of weaponised open-source test kits in regional malware campaigns further galvanises the appetite for expert services. Investor enthusiasm remains high; private equity continues to court established vendors, driving a roll-up thesis that aims to blend consulting depth with platform scalability.

Asia-Pacific is the fastest-growing theatre, at 22.1% CAGR, lifted by double-digit expansion in cloud workloads, IoT deployments, and sovereignty-driven data-centre construction. Governments issue sector-specific cyber mandates—Singapore’s MAS TRM guidelines and Australia’s SOCI Act amendments are notable examples—that elevate demand for threat-led assessments. Yet talent scarcity hinders local supply, so multinational providers win contracts by offering remotely delivered PTaaS bolstered by regional data residency options. The Penetration Testing And Ethical Hacking Services Market, therefore, sees disproportionate growth in subscription over project revenue across the region.

Europe maintains a steady trajectory, catalysed by the Digital Operational Resilience Act, which formalises threat-led penetration testing within the financial value chain.[3]European Parliament and Council, “Official Journal L 333/2022,” europa.eu Harmonised guidance simplifies procurement for pan-EU banks, driving multi-country master-service agreements. Additionally, the G-7 Fundamental Elements provide a framework for global financial groups to align European and non-European entities under unified testing programs. Overall, Europe’s buyer emphasis on detailed reporting and remediation support favours vendors with strong consulting lineage, sustaining a balanced mix of platform and service revenues.

Competitive Landscape

The Penetration Testing And Ethical Hacking Services Market remains moderately fragmented: the top five vendors collectively command well under 60% revenue, yet consolidation momentum is unmistakable. HackerOne demonstrated the disruptive potential of crowdsourced platforms with a 200% spike in AI red-team bookings during Q2 2024, signaling buyer confidence in hybrid human-and-automation delivery models. Traditional players counter through acquisitions—Rapid7 integrated Noetic Cyber to broaden attack-surface visibility, while Tenable bought Vulcan Cyber for USD 150 million to fold exposure management into its stack.[4]Michael Novinson, “Tenable To Acquire Vulcan Cyber,” CRN, crn.com

Private-equity capital continues to pour in, attracted by recurring PTaaS revenue streams and cross-sell opportunities into vulnerability management and managed detection. Trustwave and Cybereason merged in February 2025 to craft a full-spectrum MDR provider that bundles penetration testing into wider service catalogs. Vendors differentiate through AI orchestration, vertical specialisation (healthcare, OT), and SLAs that guarantee fix-validation retests within days.

White-space opportunities persist in IoT device, edge node, and machine-learning model assurance domains, where legacy network testers possess limited expertise. Providers with deep firmware or data-science credentials can command premium rates, offsetting competitive price pressure on commoditised external-perimeter tests. Talent cultivation remains a strategic imperative: companies institute scholar-programs and simulator-based training to secure a pipeline of certified ethical hackers, mitigating the workforce bottleneck that could otherwise cap revenue growth.

Penetration Testing And Ethical Hacking Services Industry Leaders

Rapid7 Inc.

HackerOne Inc.

NCC Group plc

Qualys Inc.

Synack Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Trustwave and Cybereason completed their merger to create an expanded MDR provider with enhanced penetration testing capabilities.

- February 2025: Rapid7 launched the global PACT Partner Program, adding MSSP and Service Delivery specializations to broaden test-service reach.

- January 2025: Tenable acquired Vulcan Cyber for USD 150 million, integrating exposure management into its platform.

- October 2024: Rapid7 received buyout interest from Advent, Bain Capital, and EQT at valuations near USD 2.5 billion.

Global Penetration Testing And Ethical Hacking Services Market Report Scope

Penetration Testing And Ethical Hacking Services Market Report is Segmented by Type of Penetration Testing (Network, Web/Application, Wireless and IoT, Social Engineering Testing and Cloud Configuration Penetration Testing), Service Model (Consulting and One-Off Engagements, Managed/Continuous Pen-Test, and More), Deployment Mode (On-Premise, and Cloud-based/SaaS), End-Use Industry (BFSI, Healthcare and Life Sciences, IT and Telecom, Government and Defense, Retail and eCommerce and Energy and Utilities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa).

| Network Penetration Testing |

| Web / Application Penetration Testing |

| Wireless and IoT Penetration Testing |

| Social Engineering Testing |

| Cloud Configuration Penetration Testing |

| Consulting and One-off Engagements |

| Managed / Continuous Pen-Test (MSSP) |

| Pen-Testing-as-a-Service (PTaaS) |

| On-premise |

| Cloud-based / SaaS |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Government and Defense |

| Retail and eCommerce |

| Energy and Utilities |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type of Penetration Testing | Network Penetration Testing | ||

| Web / Application Penetration Testing | |||

| Wireless and IoT Penetration Testing | |||

| Social Engineering Testing | |||

| Cloud Configuration Penetration Testing | |||

| By Service Model | Consulting and One-off Engagements | ||

| Managed / Continuous Pen-Test (MSSP) | |||

| Pen-Testing-as-a-Service (PTaaS) | |||

| By Deployment Mode | On-premise | ||

| Cloud-based / SaaS | |||

| By End-Use Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| IT and Telecom | |||

| Government and Defense | |||

| Retail and eCommerce | |||

| Energy and Utilities | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the penetration testing market in 2025?

The penetration testing market size stands at USD 2.15 billion in 2025.

What growth rate is forecast for penetration testing through 2030?

Market value is projected to rise to USD 5.00 billion by 2030, equating to an 18.37% CAGR.

Which testing type is growing the fastest?

Cloud-configuration penetration testing leads with a 28.1% CAGR forecast.

Why is healthcare demand accelerating?

Hospitals digitising patient care and facing heightened ransomware threats are driving a 24.1% CAGR for healthcare penetration tests.

What service model is disrupting traditional consulting?

Penetration Testing-as-a-Service (PTaaS) is expanding at a 29.1% CAGR due to continuous validation needs.

Which region shows the highest growth momentum?

Asia-Pacific records the fastest regional expansion at 22.1% CAGR to 2030.

Page last updated on: