Penetration Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

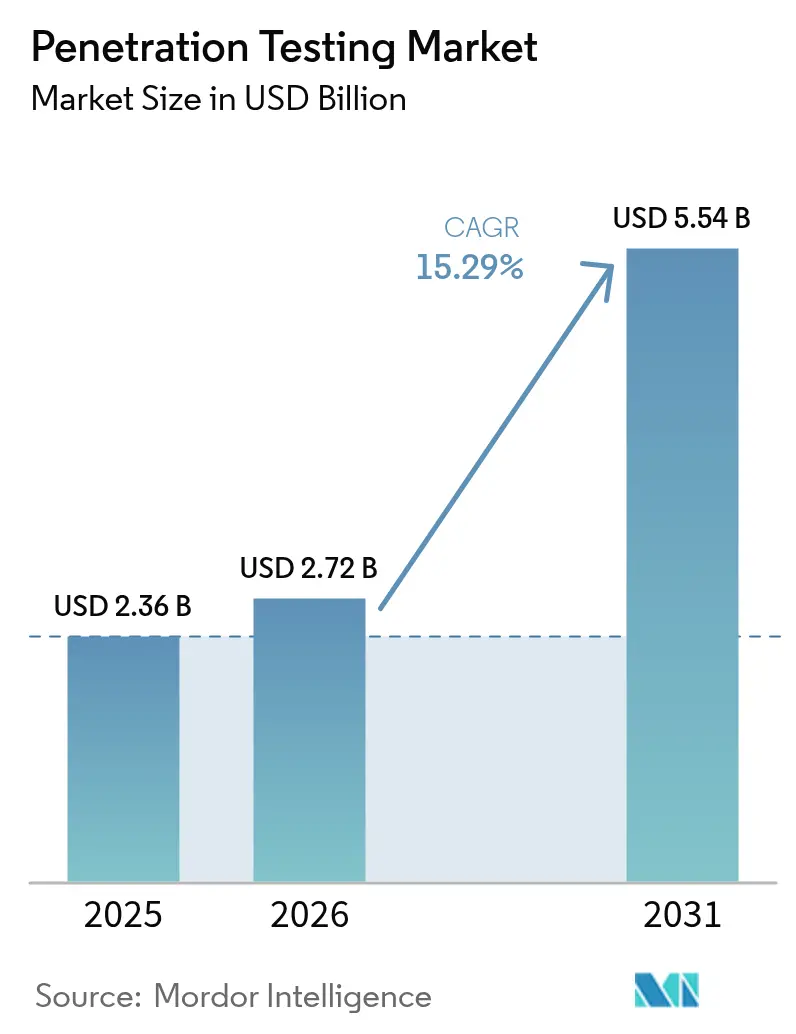

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 5.54 Billion |

| Growth Rate (2026 - 2031) | 15.29% CAGR |

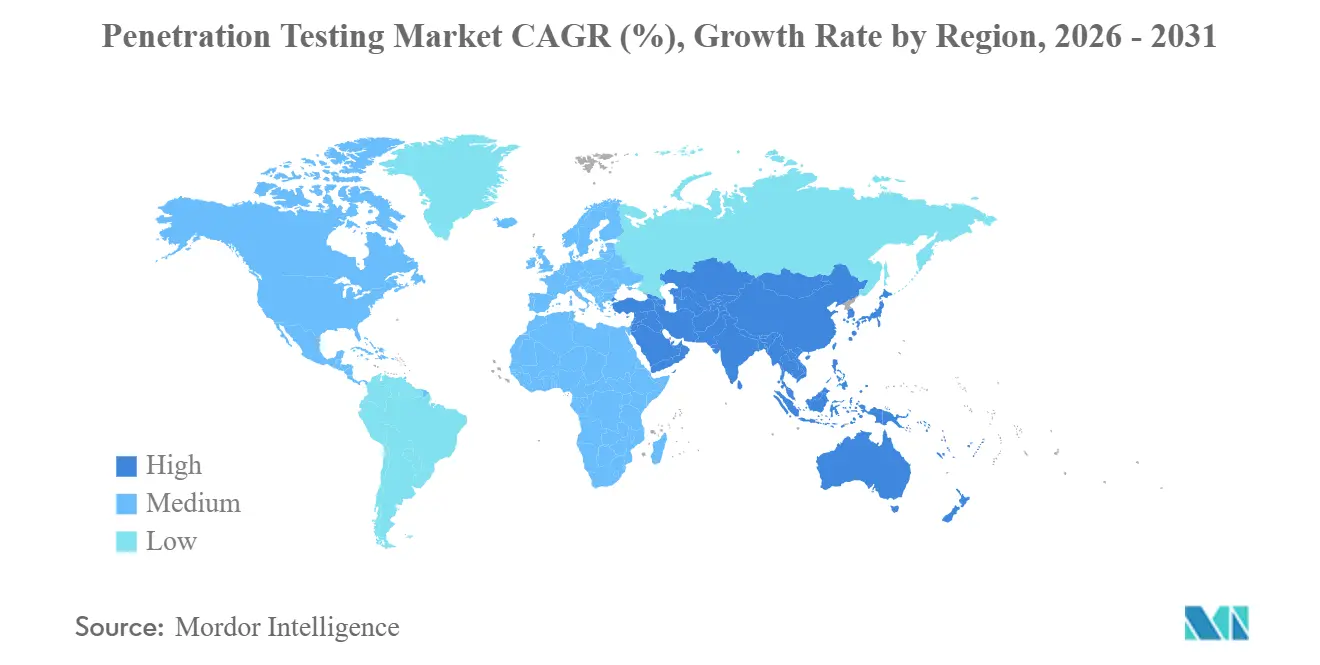

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

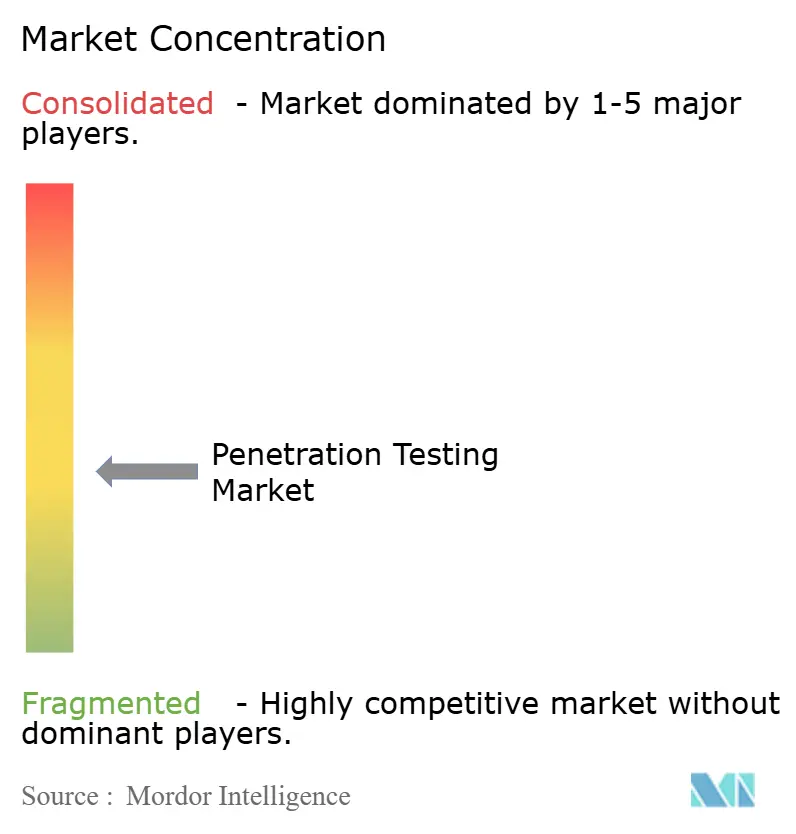

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Penetration Testing Market Analysis by Mordor Intelligence

The penetration testing market size is projected to expand from USD 2.36 billion in 2025 and USD 2.72 billion in 2026 to USD 5.54 billion by 2031, registering a CAGR of 15.29% between 2026 to 2031. Rapid adoption of cloud workloads, a sharp rise in generative-AI driven exploits, and compressed regulatory deadlines are moving penetration testing from ad-hoc audits to an always-on control. Enterprises now treat proactive validation as essential insurance against publicly disclosed vulnerabilities that adversaries weaponize within hours. Mandatory annual tests under HIPAA and PCI DSS version 4.0, along with the European Union’s Digital Operational Resilience Act and NIS2, have shortened internal decision cycles and lifted multi-year contract values. Vendors are responding with autonomous red-team agents that cut test duration from weeks to days, while integration with CI/CD pipelines enables developers to trigger tests at every commit. Competitive dynamics, therefore, favor platforms that combine continuous coverage, regulatory mapping, and granular reporting.

Key Report Takeaways

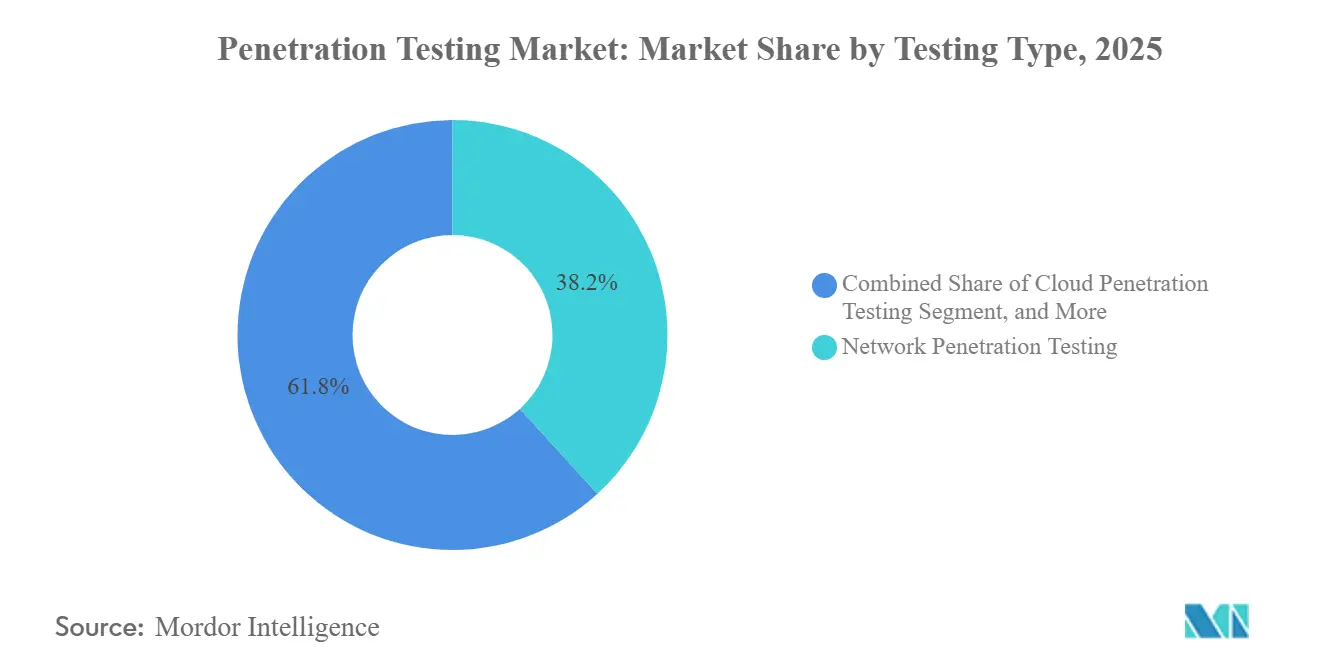

- By testing type, network assessments held 38.23% of penetration testing market share in 2025, while cloud penetration testing is forecast to expand at a 16.63% CAGR through 2031.

- By deployment model, on-premises solutions led with a 59.21% share in 2025, whereas cloud-based platforms are projected to grow at a 15.61% CAGR through 2031.

- By organization size, large enterprises accounted for 67.83% of penetration testing market share in 2025, yet small and medium enterprises are advancing at a 15.68% CAGR over the forecast period.

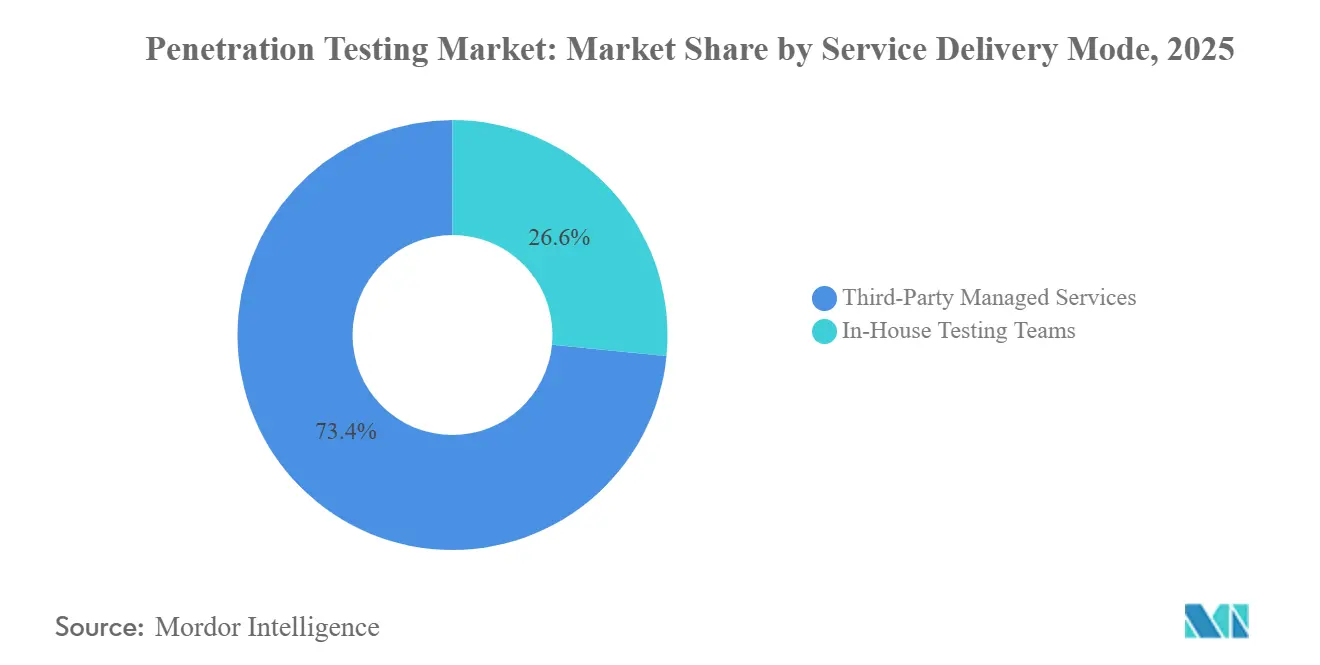

- By service delivery mode, third-party managed services captured a 73.44% share in 2025, while in-house teams are rising at a 15.64% CAGR through 2031.

- By end-user industry, banking, financial services, and insurance commanded 28.68% of penetration testing market share in 2025, but healthcare and life sciences are projected to expand at a 16.89% CAGR during 2026-2031.

- By geography, North America held a 38.27% share in 2025, whereas Asia-Pacific is the fastest-expanding region at a 16.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Penetration Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cybersecurity Risks Across Sectors | +3.8% | Global | Short term (≤ 2 years) |

| Increasing Demand for Security Assessments and Compliance Audits | +3.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government Mandates and Industry-Specific Regulations | +2.9% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| DevSecOps Pipelines Require Continuous Pen-Testing Integration | +2.4% | Core markets in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-Driven Autonomous Red Teaming Enables Continuous Validation | +1.8% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Software Bill of Materials Mandates Expand Supply-Chain Pentest Scope | +1.2% | North America, Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cybersecurity Risks Across Sectors

Public exploit kits now appear within hours of vulnerability disclosure, shrinking defenders’ reaction windows and forcing more frequent penetration tests.[1]CrowdStrike, “2026 Global Threat Report,” crowdstrike.com Dragos counted 26 threat groups actively probing operational technology in 2026, showing that industrial environments no longer enjoy obscurity or safety. After a coordinated attack on Poland’s energy grid, CISA urged quarterly testing for critical infrastructure operators, signaling regulatory impatience with annual testing cycles. A Pentera survey of 500 security leaders found 67% suffered at least one breach in the prior year and raised testing budgets to a median of USD 187,000, confirming that executives now treat proactive validation as insurance rather than an audit luxury. Together, these data points illustrate how escalating threat velocity directly expands demand for continuous penetration testing.

Increasing Demand for Security Assessments and Compliance Audits

Layered industry frameworks are stacking mandatory penetration-testing clauses, compelling organizations to synchronize multiple audits into one program. PCI DSS version 4.0, effective March 2025, requires annual testing for all merchants, plus segmentation and wireless assessments that were previously optional.[2]PCI Security Standards Council, “Payment Card Industry Data Security Standard 4.0,” pcisecuritystandards.org FDA pre-market guidance obliges medical-device makers to include test results in every submission and maintain post-market evidence, widening the scope beyond hospitals to their suppliers. FedRAMP 3.0 requires quarterly scanning and annual testing for federal cloud providers, with a draft 4.0 proposal to double the cadence for high-impact systems. New York’s amended 23 NYCRR 500 rule requires boards to review penetration-testing findings within 30 days, elevating tests from technical exercises to governance artifacts. These overlapping audits drive enterprises toward managed service providers that can map a single engagement to multiple rulebooks.

Government Mandates and Industry-Specific Regulations

Legislators are removing the discretion that once allowed firms to defer or down-scope offensive security work. Europe’s Digital Operational Resilience Act requires financial entities to conduct threat-led penetration tests at least every 3 years, with regulators empowered to order additional rounds after incidents.[3]European Union, “Regulation 2022/2554 Digital Operational Resilience Act,” eur-lex.europa.eu NIS2 extends similar duties across essential operators, harmonizing requirements for energy, transport, and health providers. In the United States, updated HIPAA Security Rule language now states that covered entities “must” conduct annual penetration testing, closing the loophole of risk-based discretion. The forthcoming Cyber Resilience Act obliges manufacturers of digital products to test before market entry, extending obligations to hardware suppliers that previously escaped scrutiny. As each statute takes effect, baseline demand for testing becomes insulated from macroeconomic swings.

DevSecOps Pipelines Require Continuous Pen-Testing Integration

Continuous deployment has rendered point-in-time audits obsolete, pushing offensive validation directly into code pipelines. Aikido Infinite lets developers trigger penetration tests on every commit inside GitHub, GitLab, or Bitbucket, returning exploitability verdicts in minutes. Bishop Fox added large-language-model tooling that drafts custom payloads within the integrated development environment, cutting manual research cycles. Rapid7’s InsightVM correlates vulnerability scans with confirmed exploit paths so teams can fix exploitable flaws before release candidates ship. These integrations shift purchasing criteria from report depth to API depth, favoring vendors that deliver autonomous agents, pipeline plug-ins, and remediation tickets in a single workflow. As a result, continuous penetration testing has become routine in modern software factories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage and High Cost of Skilled Testers | -1.4% | Global, acute in Asia-Pacific and Europe | Medium term (2-4 years) |

| Lack of Awareness Among SMEs | -1.1% | South America, Africa, Southeast Asia | Short term (≤ 2 years) |

| Ethical Constraints on Live Exploitation of Critical OT Environments | -0.8% | Energy, utilities, manufacturing worldwide | Long term (≥ 4 years) |

| Unclear Legal Liability in Multi-Jurisdiction Cloud Environments | -0.6% | Multi-cloud deployments across North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage and High Cost of Skilled Testers

Global demand for certified penetration testers far exceeds supply, driving up engagement fees and lengthening project queues. ISC2 found that 95% of organizations report cybersecurity staffing gaps, ranking offensive testing among the three hardest roles to fill. The United Kingdom still needed 11,200 additional cybersecurity workers in 2024, with offensive roles taking the longest to hire. Pass rates for advanced OSCP credentials remain below 50%, underscoring steep learning curves and slow growth in the talent pipeline. Enterprises, therefore, turn to automation for routine tasks, yet scoping, social engineering, and post-exploitation analysis still require human expertise. The persistent talent deficit caps service capacity and tempers market growth despite strong demand.

Lack of Awareness Among SMEs

Many small and medium enterprises underestimate the likelihood of breaches and treat penetration testing as a luxury rather than a necessity. A Nepalese study showed only 25% of SMEs had ever conducted a test, with 68% citing cost and 54% lacking methodological awareness. The UK National Cyber Security Centre reported that while 43% of small firms suffered incidents in 2024, just 19% had hired external testers, preferring basic vulnerability scans instead. Limited regulatory oversight in retail, hospitality, and professional services leaves few external pressures to change behavior. Although supply-chain rules like DORA and SBOM policies are starting to cascade requirements onto smaller vendors, knowledge gaps and budget constraints slow adoption. Consequently, SME inertia remains a drag on market penetration outside heavily regulated ecosystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Testing Type: Cloud Assessments Outpace Legacy Network Focus

Network assessments held a 38.23% market share in penetration testing in 2025, underscoring the continued priority of perimeter and lateral-movement defenses. Yet cloud penetration testing, propelled by multi-cloud adoption, is projected to advance at a 16.63% CAGR through 2031, making it the fastest-growing modality. The shift reflects container orchestration, serverless functions, and API-centric architectures that fall outside traditional network scopes. Bishop Fox expanded its CloudFox toolkit to Google Cloud Platform in 2026, signaling maturity in cloud-native testing methods. Mobile and web application tests are converging because adversaries frequently reuse API and credential-stuffing tactics across channels. Social-engineering exercises now simulate deepfake voice and video attacks, a trend made possible by generative AI. Wireless testing widens to cover Wi-Fi 6E and 5G private networks in factories and logistics hubs. IoT and operational technology assessments grow as industrial asset owners replicate production environments in sandboxes to avoid downtime.

The penetration testing market size for hybrid engagements that bundle network, cloud, and application scopes is growing, as buyers prefer a single contract that spans multiple frameworks. Vendors that offer unified dashboards and automated retesting win deals as compliance cycles tighten. Continuous validation expectations are rising quickly; Bishop Fox’s Cosmos AI claims a 40% reduction in assessment time, while HackerOne’s agentic service delivers findings within hours rather than days. These efficiency gains let security teams schedule more frequent tests without escalating budgets. As threat actors weaponize disclosed flaws in hours, enterprises gravitate toward modalities that confirm exploitability, not just vulnerability presence. Consequently, demand migrates from point-in-time network sweeps to always-on cloud and application probes that integrate directly into CI/CD pipelines.

By Deployment Model: Cloud Platforms Gain Ground on On-Premise Solutions

On-premises deployments commanded 59.21% of the penetration testing market share in 2025, as many regulated sectors still favor on-premises control. However, cloud-delivered platforms are set to grow at a 15.61% CAGR to 2031, fueled by elastic scaling and rapid feature updates that align with DevSecOps cycles. Aikido Infinite lets developers trigger penetration tests on every commit without provisioning servers, illustrating the operational ease of SaaS delivery. PCI DSS 4.0 clarified that cloud-based tests satisfy cardholder data rules, removing a lingering barrier. Hybrid environments now dominate enterprise architectures, so visibility into both cloud workloads and on-premise assets becomes essential.

The penetration testing market for on-prem tools remains resilient in air-gapped government and defense networks, where sovereignty rules block external connectivity. Even there, vendors ship virtual appliances that synchronize anonymized findings once links are available. For the broader market, subscription pricing moves expenditure from capital to operating budgets, simplifying approvals. Managed service providers increasingly bundle cloud testing dashboards with verbal readouts that satisfy board-level reporting. Buyers also cite quicker patch validation when test results are fed directly into ticketing systems via REST APIs. As continuous deployment normalizes, organizations view cloud delivery not as an option but as the default unless a statute forbids it.

By Organization Size: Supply-Chain Rules Accelerate SME Uptake

Large enterprises accounted for 67.83% of revenue in 2025, reflecting larger attack surfaces and stricter oversight. Yet the penetration testing market size for small and medium enterprises is projected to expand at a 15.68% CAGR, as regulations such as DORA obligate banks to vet third-party vendors. U.S. SBOM policies impose similar obligations on federal contractors, cascading tests down the supply chain. Automated platforms such as Pentera remove scoping complexity, letting mid-market firms launch tests without dedicated red-team staff.

Budget sensitivity still curbs SME adoption, with surveys showing cost and awareness as leading barriers. Vendors respond with entry-level tiers that bundle quarterly scans, penetration tests, and virtual CISO advisory for a single annual fee. As cyber-insurance carriers refuse coverage without evidence of offensive testing, boards at smaller firms begin to budget for it proactively. Large enterprises reinforce the shift by inserting penetration-test attestations in procurement contracts. Over time, marketplace portals may emerge where SMEs upload validated reports to bid for regulated projects, further institutionalizing testing.

By Service Delivery Mode: Managed Services Lead but In-House Teams Scale Fast

Third-party managed services captured a 73.44% share in 2025 because they consolidate scarce talent, tooling, and compliance mapping into turnkey engagements. In-house capabilities, however, are projected to rise at a 15.64% CAGR as platforms automate reconnaissance and exploitation chains. Rapid7 InsightVM now correlates scan data with confirmed exploit paths, enabling corporate red teams to focus on remediation rather than enumeration. Synopsys embeds exploit verification inside code reviews, letting developers close loops without waiting for external testers.

The penetration testing market share for managed services stays dominant in high-risk scenarios that demand niche expertise, such as operational technology or physical intrusion drills. Talent scarcity drives hybrid models where an internal squad handles daily checks and outsources annual adversary simulations to boutique firms. AI agents absorb repetitive tasks, but human creativity remains vital for social engineering and post-exploitation analysis. Pricing models now tie service fees to remediation outcomes, aligning incentives. As continuous validation normalizes, buyers judge providers on integration depth, evidence quality, and speed rather than tester headcount.

By End-User Industry: Healthcare Momentum Outpaces BFSI Dominance

Banking, financial services, and insurance led with 28.68% market share in penetration testing in 2025, stabilized by Basel and PCI regimes. Healthcare and life sciences, however, are on track for the fastest 16.89% CAGR through 2031, following FDA guidance that made test evidence mandatory in pre-market device files. HIPAA now requires annual testing for covered entities, pushing hospitals and insurers alike to institutionalize offensive validation. Ransomware continues to pressure executive boards into approving larger budgets.

Government and defense spending climb to support zero-trust rollouts, while FedRAMP draft proposals call for semiannual tests for high-impact systems. Retail and e-commerce firms face stricter segmentation requirements under PCI DSS 4.0, driving demand for wireless and social engineering modules. Manufacturers and utilities accelerate operational technology assessments following CISA's recommendation of quarterly tests for critical infrastructure. Education, hospitality, and professional services begin engaging testers as supply-chain questionnaires require validation proof. Collectively, these trends expand the penetration testing market across verticals, but growth skews toward sectors where new statutes embed testing directly into core operating licenses.

Geography Analysis

North America commanded 38.27% penetration testing market share in 2025, anchored by mature regulatory frameworks such as HIPAA, PCI DSS 4.0, and FedRAMP that formalize annual or semiannual testing cadences. U.S. financial institutions bundle threat-led testing into operational resilience programs, while Canadian health-privacy statutes drive hospitals to adopt continuous validation. Mexico’s fast-growing fintech ecosystem also embeds penetration testing into cross-border payment licenses, widening regional demand. Venture funding is concentrated in Silicon Valley and Boston, allowing local platform vendors to iterate on AI agents that shorten test cycles for domestic clients. As a result, North America remains the reference market for new tooling and service models.

Asia-Pacific is forecast to expand its penetration testing market size at a 16.26% CAGR through 2031, the fastest regional trajectory. India’s 30% to 50% cyber-talent gap encourages enterprises to adopt automated platforms, while data-localization rules in China compel in-country testing of all systems that handle personal information. Japan’s revised Act on the Protection of Personal Information and South Korea’s critical infrastructure mandates further hardwire annual testing into corporate governance. Rapid digital-payment adoption in Indonesia and the Philippines underscores the need for validation for small merchants connecting to regional gateways. Together, these factors create a demand surge that helps global vendors justify in-region cloud PoPs and local language reporting.

Europe benefits from a compliance floor established by the Digital Operational Resilience Act, NIS2, and the forthcoming Cyber Resilience Act, which collectively elevate penetration testing from best practice to a legal duty. Germany’s BSI released sector playbooks for critical infrastructure in 2025, and France expanded its SecNumCloud framework to include mandatory testing for service providers. The United Kingdom’s National Cyber Security Centre recommends annual tests for any firm handling sensitive data, to keep post-Brexit standards aligned with continental norms. South America, the Middle East, and Africa are emerging as strong markets as Brazil’s data-protection law and Gulf national cyber programs embed offensive testing into licensing regimes. Overall geographic expansion is therefore paced by how quickly statutes migrate from guidance to enforcement across each jurisdiction.

Competitive Landscape

The market remains moderately fragmented, yet consolidation among platform vendors is accelerating. IBM, Palo Alto Networks, and Rapid7 integrate penetration testing into broader detection, response, and identity suites, leveraging their installed vulnerability-management bases to upsell autonomous red-team modules. Palo Alto Networks acquired QRadar SaaS in 2024, Chronosphere in 2026, and CyberArk in 2026, knitting SIEM, observability, and identity validation into a single subscription, thereby deepening stickiness among Fortune 500 buyers.

Specialist consultancies such as Bishop Fox, Offensive Security, IOActive, and NCC Group defend share through domain depth in operational technology, mobile, and social-engineering scenarios. Their engineers craft bespoke exploits, perform physical intrusion exercises, and deliver adversary simulation, areas where automated agents remain immature. NCC Group’s 2024 acquisition of Fox-IT expanded industrial-control capabilities, enabling sandboxed testing that avoids production downtime. Even so, pricing pressure rises as clients reserve boutique engagements for annual red-team events and rely on platforms for routine validation.

Automation-first disruptors HackerOne, Pentera, Cobalt.io, and Synack build a competitive edge on AI agents that compress reconnaissance, exploitation, and reporting from weeks to hours. HackerOne’s Agentic Penetration Testing as a Service continuously probes production endpoints and exports findings directly into ticketing systems, narrowing the remediation loop. Pentera focuses on mid-market enterprises, raising USD 60 million Series D funding in 2025 to scale an agent-less platform that executes safely in live networks. With efficiency becoming the core differentiator, vendor evaluations now weigh API depth, evidence granularity, and regulatory mapping higher than headcount, driving a strategic pivot from labor scale to software velocity across the competitive field.

Penetration Testing Industry Leaders

IBM Corporation

Rapid7 Inc.

Broadcom Inc.

FireEye Inc.

Veracode Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Palo Alto Networks completed the CyberArk acquisition to extend identity validation in zero-trust projects.

- February 2026: Bishop Fox launched Cosmos AI, an LLM-assisted application testing tool that trims assessment time by 40%.

- February 2026: Bishop Fox released CloudFox for Google Cloud Platform, rounding out coverage of all major hyperscalers.

- February 2026: CISA issued guidance urging quarterly penetration testing for industrial control systems after a Poland energy attack.

Global Penetration Testing Market Report Scope

The Penetration Testing Market Report is Segmented by Testing Type (Network Penetration Testing, Web Application Penetration Testing, Mobile Application Penetration Testing, Social Engineering Penetration Testing, Wireless Network Penetration Testing, Cloud Penetration Testing, Other Testing Types), Deployment Model (On-Premise, and Cloud-Based), Organization Size (Large Enterprises, and Small and Medium Enterprises), Service Delivery Mode (In-House Testing Teams, and Third-Party Managed Services), End-User Industry (Government and Defense, Banking, Financial Services and Insurance, IT and Telecom, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Energy and Utilities, Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Network Penetration Testing |

| Web Application Penetration Testing |

| Mobile Application Penetration Testing |

| Social Engineering Penetration Testing |

| Wireless Network Penetration Testing |

| Cloud Penetration Testing |

| Other Testing Types |

| On-Premise |

| Cloud-Based |

| Large Enterprises |

| Small and Medium Enterprises |

| In-House Testing Teams |

| Third-Party Managed Services |

| Government and Defense |

| Banking, Financial Services and Insurance |

| IT and Telecom |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Energy and Utilities |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Testing Type | Network Penetration Testing | ||

| Web Application Penetration Testing | |||

| Mobile Application Penetration Testing | |||

| Social Engineering Penetration Testing | |||

| Wireless Network Penetration Testing | |||

| Cloud Penetration Testing | |||

| Other Testing Types | |||

| By Deployment Model | On-Premise | ||

| Cloud-Based | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Service Delivery Mode | In-House Testing Teams | ||

| Third-Party Managed Services | |||

| By End-User Industry | Government and Defense | ||

| Banking, Financial Services and Insurance | |||

| IT and Telecom | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the penetration testing market projected to grow through 2031?

The market is expected to expand at a 15.29% CAGR from 2026 to 2031, reaching USD 5.54 billion in value.

Which testing type shows the strongest growth momentum?

Cloud penetration testing posts the highest trajectory at a 16.63% CAGR as serverless, container, and multi-cloud deployments widen the attack surface.

Why are healthcare organizations increasing their penetration testing budgets?

FDA guidance now requires device makers to include test evidence in submissions, while a surge in ransomware incidents drives boards to mandate annual assessments.

What is driving SME adoption of penetration testing?

Supply-chain rules under frameworks like DORA and SBOM compel smaller vendors to furnish test evidence to retain contracts with regulated buyers.

How are AI technologies changing penetration testing delivery?

Vendors embed large-language models and autonomous agents that automate reconnaissance, exploitation, and reporting, shrinking test cycles from weeks to days and enabling continuous validation.

Which region is growing the fastest in penetration testing adoption?

Asia-Pacific leads regional growth at a projected 16.26% CAGR due to digital payments expansion, data residency laws, and government cyber mandates.

Page last updated on: