Cybersecurity Consulting Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 21.57 Billion |

| Market Size (2030) | USD 35.29 Billion |

| Growth Rate (2025 - 2030) | 10.35% CAGR |

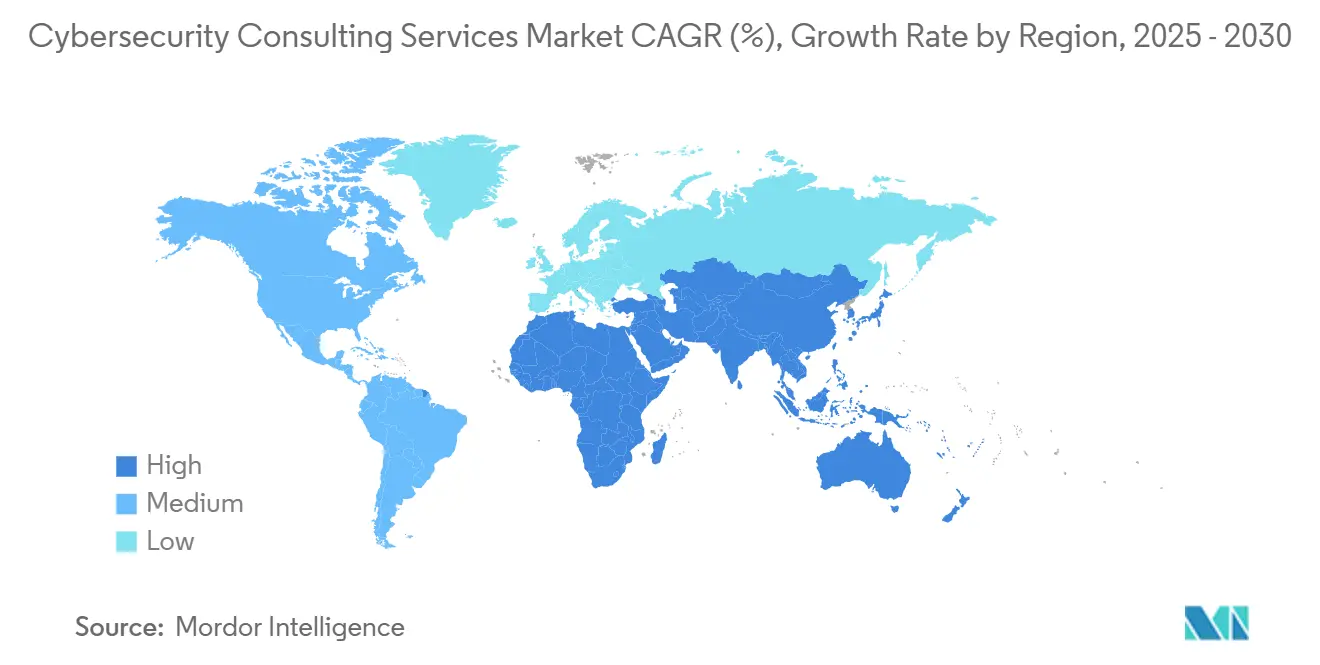

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cybersecurity Consulting Services Market Analysis by Mordor Intelligence

The Cybersecurity consulting services market size stands at USD 21.57 billion in 2025 and is forecast to reach USD 35.29 billion by 2030, growing at a 10.35% CAGR. This expansion reflects enterprises’ acknowledgment that in-house teams cannot independently address modern threat sophistication. Demand accelerates as the EU NIS2 directive and the U.S. Cybersecurity Maturity Model Certification oblige organizations to formalize risk oversight, while cyber-talent scarcity and AI-driven attack vectors reinforce outsourcing needs.[1]Vivek Krishnan, “The new math: Solving cryptography in an age of quantum,” Deloitte Insights, deloitte.com Growing investor scrutiny of cyber-resilience disclosures and the push for zero-trust adoption further elevate spending. Meanwhile, insurers increasingly tie coverage to professional security assessments, widening the client base for the Cybersecurity consulting services market.[2]PwC, “Managed Services and AI: Transforming cybersecurity and risk mitigation,” pwc.com

Key Report Takeaways

- By service type, strategic security consulting led with a 45% Cybersecurity consulting services market share in 2024; managed detection and response readiness consulting is projected to expand at a 16.8% CAGR through 2030.

- By client industry, banking, financial services, and insurance commanded 28% of the Cybersecurity consulting services market size in 2024, while healthcare is advancing at a 15.2% CAGR through 2030.

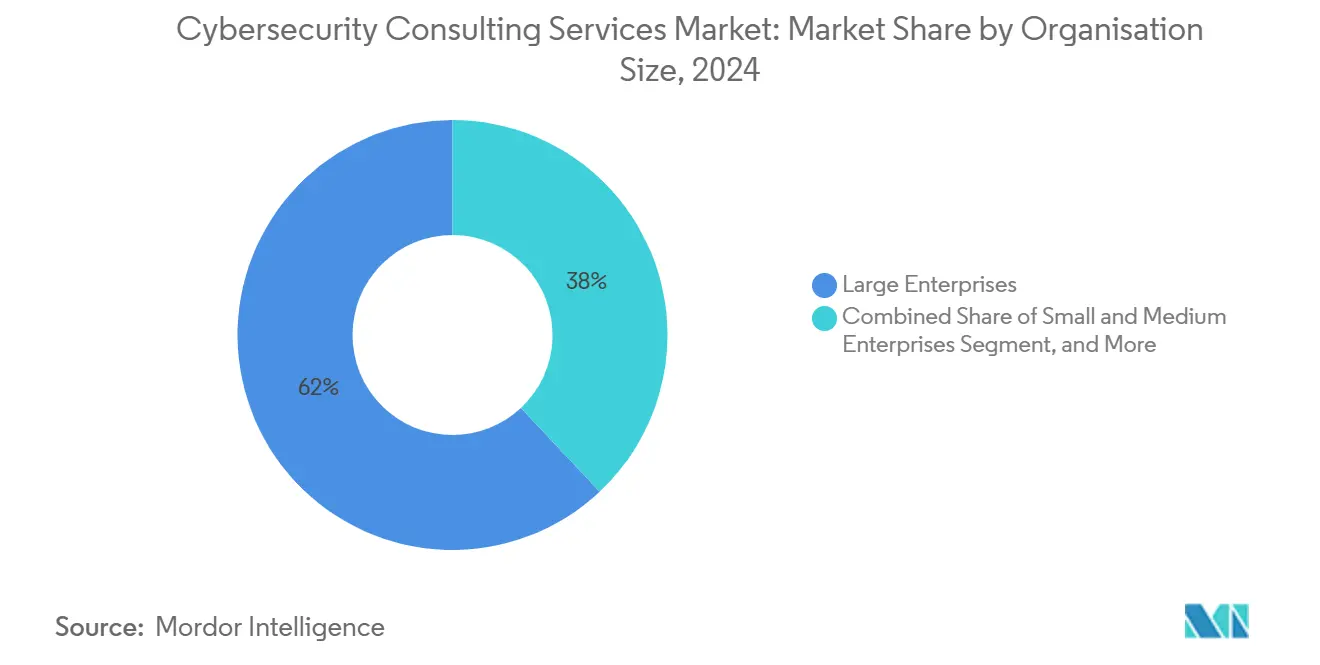

- By organization size, large enterprises held 62% revenue share of the Cybersecurity consulting services market in 2024, yet small and medium enterprises posted the fastest growth at a 14.9% CAGR to 2030.

- By engagement model, project-based advisory engagements retained 48% share of the Cybersecurity consulting services market size in 2024; outcome-based and risk-sharing contracts are rising at a 15.5% CAGR through 2030.

- By geography, North America led with 42.5% Cybersecurity consulting services market share in 2024, whereas Asia-Pacific exhibits the highest regional CAGR at 14.2% until 2030.

Global Cybersecurity Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating frequency and sophistication of cyber-attacks | +2.80% | Global, with concentrated impact in North America and Europe | Short term (≤ 2 years) |

| Tightening global data-protection regulations | +2.10% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Cloud-migration and hybrid-IT complexity | +1.90% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Cyber-talent shortage driving outsourcing | +1.70% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| ESG-linked cyber-resilience disclosure mandates | +1.20% | Europe and North America, emerging in APAC | Long term (≥ 4 years) |

| Cyber-insurance underwriting requirements | +0.80% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Attack Frequency and Sophistication

AI-enabled ransomware platforms, deepfake social engineering, and supply-chain intrusions have redefined risk posture expectations. Seventy-four percent of enterprises now deem AI critical for detection, pushing demand for behavioural analytics and threat-intel integration consulting. Ransomware-as-a-Service democratizes advanced tactics once reserved for nation-states, prompting board-level investment in proactive threat hunting. Meanwhile, a 431% surge in supply-chain attacks since 2024 requires third-party security validation programs delivered by specialized consultants.[3]Elliott Davis, “Top 10 Cybersecurity Trends for 2025,” elliottdavis.com

Tightening Global Data-Protection Regulations

NIS2 extends mandatory controls across 18 critical sectors and imposes 24-hour breach reporting, heightening the need for integrated legal and technical guidance. The U.S. SEC now obliges public issuers to disclose material incidents within four business days, spurring incident-response and materiality assessment consulting. China’s Data Security Law and Personal Information Protection Law add localized mandates, compelling multinationals to engage region-specific expertise that balances cross-border data transfer with domestic compliance.[4]Coro Cybersecurity, “Guide to FERPA Compliance for Schools,” coro.net

Cloud-Migration and Hybrid-IT Complexity

Zero-trust architecture will reach 80% enterprise adoption by 2025, generating consulting demand for identity-centric controls, micro-segmentation, and conditional access policies. Ninety-five percent of cloud breaches stem from customer misconfigurations, underscoring advisory needs for secure configuration baselines. Containerized workloads add new attack surfaces, and the convergence of operational technology with cloud requires consultants versed in industrial control system defense.

Cyber-Talent Shortage Driving Outsourcing

The 3.5 million global shortfalls in qualified practitioners propel uptake of virtual CISO subscriptions priced between USD 5,000 and USD 25,000 monthly. Scarcity in cloud-security architects and incident-response experts sustains premium rates, while co-managed SOC models become mainstream to blend internal visibility with external execution. Consulting firms now bundle automation tooling to offset human gaps and deliver faster detection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise IT budget compression | -1.40% | Global, with acute impact in Europe and emerging markets | Short term (≤ 2 years) |

| DIY automation reducing external spend | -0.90% | North America and Europe, with technology-forward enterprises | Medium term (2-4 years) |

| Generative-AI commoditising basic assessments | -0.70% | Global, with early adoption in North America | Medium term (2-4 years) |

| IT/OT convergence blurring accountability | -0.50% | Global, concentrated in manufacturing and energy sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise IT Budget Compression

Macroeconomic uncertainty drives closer scrutiny of consulting spend, delaying non-essential assessments and favouring bundled vendor relationships to cut overhead. Outcome-based contracts rise as buyers seek demonstrable risk reduction, pressuring firms to align fees with security performance. Subscription vCISO models gain favour as cost-effective leadership substitutes, yet overall revenue per client may fall, challenging profitability.

Generative-AI Commoditizing Basic Assessments

AI-driven platforms automate vulnerability scans and policy checks once billable to junior consultants. While reducing routine revenue, these tools free capacity for higher-margin advisory in AI governance and algorithmic bias mitigation. Consulting workflows accelerate, shrinking project timelines and pushing firms to compete on strategic value rather than labour hours.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Strategic Consulting Anchors Growth

Strategic security consulting accounted for 45% of the Cybersecurity consulting services market in 2024, reflecting enterprises’ reliance on governance, risk, and compliance frameworks that align with multijurisdictional regulations. Technical security services such as penetration testing maintain solid demand as internal teams find it cost-prohibitive to retain niche expertise.

The managed detection and response consulting niche leads growth at a 16.8% CAGR, supported by recognition that SIEM tools alone cannot combat advanced persistent threats. Zero-trust design projects increase as identity-centric models replace perimeter defenses, and cloud and hybrid-IT security engagements multiply amid multi-cloud complexity. Incident response and digital forensics remain resilient, buoyed by regulatory breach-report deadlines and cyber-insurance claim investigations.

By Client Industry Vertical: Healthcare Accelerates Past Banking

Banking, financial services, and insurance held 28% of the Cybersecurity consulting services market share in 2024, thanks to mature budgets and established compliance regimes. Government clients continue to invest under critical-infrastructure mandates.

Healthcare delivers the fastest expansion at a 15.2% CAGR through 2030 as ransomware and connected device vulnerabilities expose patient safety risks. Manufacturing also rises as operational technology security becomes critical for production continuity and supply-chain resilience.

By Organization Size: SMEs Drive Unexpected Growth

Large enterprises with over 5,000 employees contributed 62% of 2024 revenue, leveraging complex needs that demand multi-disciplinary consulting teams. Mid-market companies sustain steady growth, motivated by insurance prerequisites and governance policies.

Small and medium enterprises register a 14.9% CAGR to 2030. Insurers now require professional assessments for coverage renewals, prompting SMEs to seek affordable frameworks and virtual CISO subscriptions. Even start-ups allocate a budget for baseline controls to secure funding and meet customer due diligence checks.

By Consulting Engagement Model: Outcomes Replace Deliverables

Project-based advisory engagements retained 48% market share in 2024, preferred for discrete compliance projects and penetration tests with a fixed scope. Retainer staffing supplements internal gaps, especially during peak audit seasons.

Outcome-based contracts grow at 15.5% CAGR, aligning fees with measurable risk-reduction metrics. Subscription models for vCISO and on-demand advisory appeal to resource-constrained firms requiring continuous guidance without full-time leadership. Co-managed SOC engagements bridge strategy and execution, reflecting a hybrid approach to talent scarcity.

Geography Analysis

North America commanded 42.5% Cybersecurity consulting services market share in 2024, propelled by federal mandates such as CMMC for defense contractors and SEC incident-disclosure rules. The United States remains the largest revenue contributor, while Canada’s critical-infrastructure regulations and Mexico’s manufacturing digitization sustain regional momentum.

Europe maintains strong demand through GDPR and NIS2 compliance workloads that span 18 critical sectors. Germany’s industrial automation, the United Kingdom’s financial reforms, and Nordic innovation adoption together drive consulting opportunities. The regional threat landscape intensifies following geopolitical conflict, accelerating spending on supply-chain and critical-infrastructure security.

Asia-Pacific posts the highest CAGR at 14.2% to 2030. Singapore’s financial regulations, India’s data-protection law, and China’s Personal Information Protection Law oblige enterprises to procure local expertise. Japan and South Korea focus on OT security for advanced manufacturing, while ASEAN nations implement new frameworks that open green-field consulting demand.

Competitive Landscape

The Cybersecurity consulting services market is moderately fragmented. Big Four consultancies together hold about 35% revenue, leveraging enterprise relationships and cross-discipline capabilities. Specialized firms such as Optiv, NCC Group, and Mandiant dominate advanced technical niches like red team testing and threat intelligence.

Technology integration defines competitive edge: leading providers embed AI-augmented threat-detection platforms to increase efficiency and scalability. Investments in quantum-safe cryptography, AI governance, and OT security diversify service portfolios and command premium pricing.

Partnership ecosystems expand, evidenced by Deloitte-Google Cloud and Microsoft Security Copilot alliances that integrate generative AI into advisory offerings. Niche players differentiate through sector-specific expertise, for example, healthcare data-privacy consulting or energy OT hardening.

Cybersecurity Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

Accenture plc

International Business Machines Corporation

PricewaterhouseCoopers International Limited

Ernst & Young Global Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: QBE Insurance Group partnered with multiple cybersecurity consulting firms to enhance cyber-risk assessment for commercial underwriting.

- May 2025: Microsoft expanded its Security Copilot platform with generative AI for incident-response automation.

- April 2025: NIST released final post-quantum cryptography standards, spurring migration consulting.

- March 2025: Deloitte formed a strategic alliance with Google Cloud to embed generative AI in security consulting.

Global Cybersecurity Consulting Services Market Report Scope

| Strategic Security Consulting (Advisory, GRC) |

| Technical Security Services (Pen-Test, Red/Blue Team) |

| Cloud and Hybrid-IT Security Consulting |

| Zero-Trust Architecture Consulting |

| Incident Response and Digital Forensics |

| Managed Detection and Response / XDR Readiness |

| OT / ICS Security Consulting |

| Privacy and Data-Protection Compliance (GDPR, CCPA, etc.) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Government and Public Services |

| Manufacturing and Industrial |

| Energy, Utilities and Mining |

| Retail, e-Commerce and Consumer Goods |

| Telecommunications and Media |

| Transportation and Logistics |

| Education and Non-Profit |

| Large Enterprises (?5 000 FTE) |

| Mid-Market (500 - 4 999 FTE) |

| Small Enterprises (100 - 499 FTE) |

| Micro and Start-ups (More than 100 FTE) |

| Project-based Advisory (Fixed-scope) |

| Multi-year Retainer (Staff-Aug / Co-sourcing) |

| Managed Services / Co-managed SOC |

| Outcome-based / Risk-sharing Contracts |

| Subscription vCISO and On-demand Advisory |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Nordics (Sweden, Norway, Denmark, Finland) | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman) |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Service Type | Strategic Security Consulting (Advisory, GRC) | |

| Technical Security Services (Pen-Test, Red/Blue Team) | ||

| Cloud and Hybrid-IT Security Consulting | ||

| Zero-Trust Architecture Consulting | ||

| Incident Response and Digital Forensics | ||

| Managed Detection and Response / XDR Readiness | ||

| OT / ICS Security Consulting | ||

| Privacy and Data-Protection Compliance (GDPR, CCPA, etc.) | ||

| By Client Industry Vertical | Banking, Financial Services and Insurance (BFSI) | |

| Healthcare and Life Sciences | ||

| Government and Public Services | ||

| Manufacturing and Industrial | ||

| Energy, Utilities and Mining | ||

| Retail, e-Commerce and Consumer Goods | ||

| Telecommunications and Media | ||

| Transportation and Logistics | ||

| Education and Non-Profit | ||

| By Organisation Size | Large Enterprises (?5 000 FTE) | |

| Mid-Market (500 - 4 999 FTE) | ||

| Small Enterprises (100 - 499 FTE) | ||

| Micro and Start-ups (More than 100 FTE) | ||

| By Consulting Engagement Model | Project-based Advisory (Fixed-scope) | |

| Multi-year Retainer (Staff-Aug / Co-sourcing) | ||

| Managed Services / Co-managed SOC | ||

| Outcome-based / Risk-sharing Contracts | ||

| Subscription vCISO and On-demand Advisory | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics (Sweden, Norway, Denmark, Finland) | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman) | |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How fast is the Cybersecurity consulting services market expected to grow to 2030?

It is forecast to advance at a 10.35% CAGR, rising from USD 21.57 billion in 2025 to USD 35.29 billion by 2030.

Which service type will expand the quickest over the next five years?

Managed detection and response readiness consulting is projected to post a 16.8% CAGR as enterprises pivot to proactive threat hunting.

Why is healthcare generating heightened consulting demand?

A surge in ransomware targeting patient data plus connected medical device vulnerabilities is driving a 15.2% CAGR in healthcare engagements.

What region offers the strongest growth opportunity for providers?

Asia-Pacific leads with a 14.2% CAGR through 2030 thanks to rapid digitization and evolving regulatory frameworks.

How are small and medium enterprises influencing service uptake?

SMEs post the highest growth at 14.9% CAGR, spurred by insurer mandates for professional security assessments and cost-effective vCISO subscriptions.

What engagement model is gaining traction with buyers?

Outcome-based and risk-sharing contracts are expanding at a 15.5% CAGR as clients seek measurable security improvements.

Page last updated on: