Data Analytics Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.54 Billion |

| Market Size (2031) | USD 61.58 Billion |

| Growth Rate (2026 - 2031) | 33.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Analytics Outsourcing Market Analysis by Mordor Intelligence

The data analytics outsourcing market size was valued at USD 10.89 billion in 2025 and estimated to grow from USD 14.54 billion in 2026 to reach USD 61.58 billion by 2031, at a CAGR of 33.47% during the forecast period (2026-2031). Enterprises are accelerating the shift from capital-intensive on-premises analytics to variable operational-expense arrangements that tap specialized third-party expertise. Rapid growth in enterprise data volumes, early deployment of generative AI, and ever-stricter compliance mandates continue to pull demand toward external providers. At the same time, hybrid delivery models are reshaping sourcing decisions as firms balance cost savings with data-sovereignty obligations. Competitive intensity is rising because leading service providers are pouring resources into AI platforms, industry accelerators, and outcome-based commercial structures that link compensation to measurable business results.

Key Report Takeaways

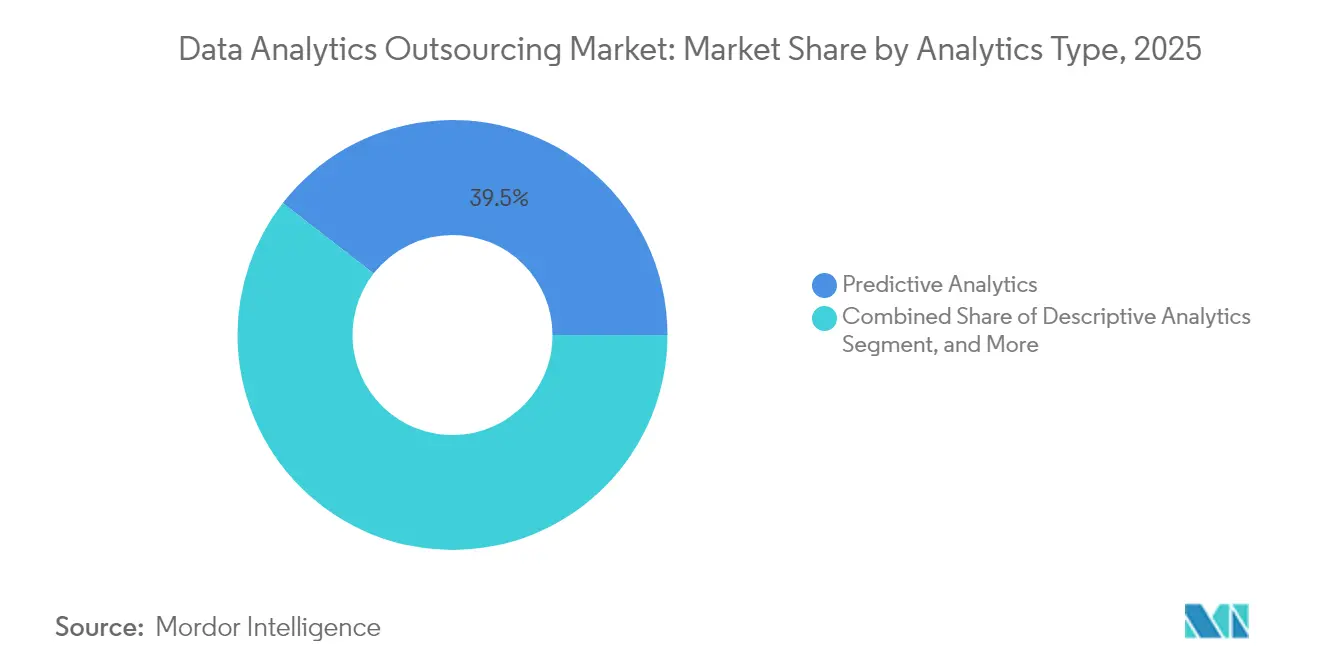

- By analytics type, predictive analytics led with 39.48% of the data analytics outsourcing market share in 2025. Prescriptive analytics is projected to expand at a 34.32% CAGR through 2031.

- By end-user industry, BFSI held 27.05% of the data analytics outsourcing market share in 2025; healthcare is set to grow at a 34.15% CAGR to 2031.

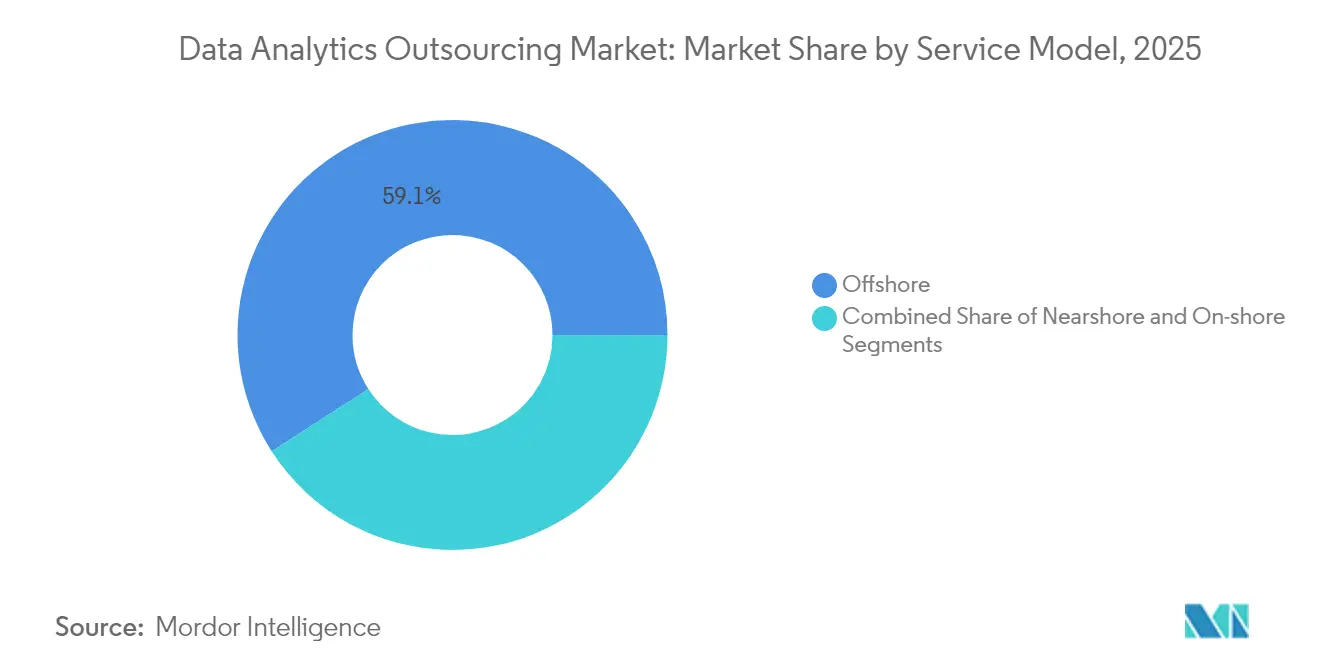

- By service model, offshore services accounted for 59.10% of the data analytics outsourcing market size in 2025, while nearshore delivery is advancing at a 34.88% CAGR through 2031.

- By organization size, large enterprises commanded 66.05% of demand in 2025; SMEs are forecast to rise at a 35.02% CAGR to 2031.

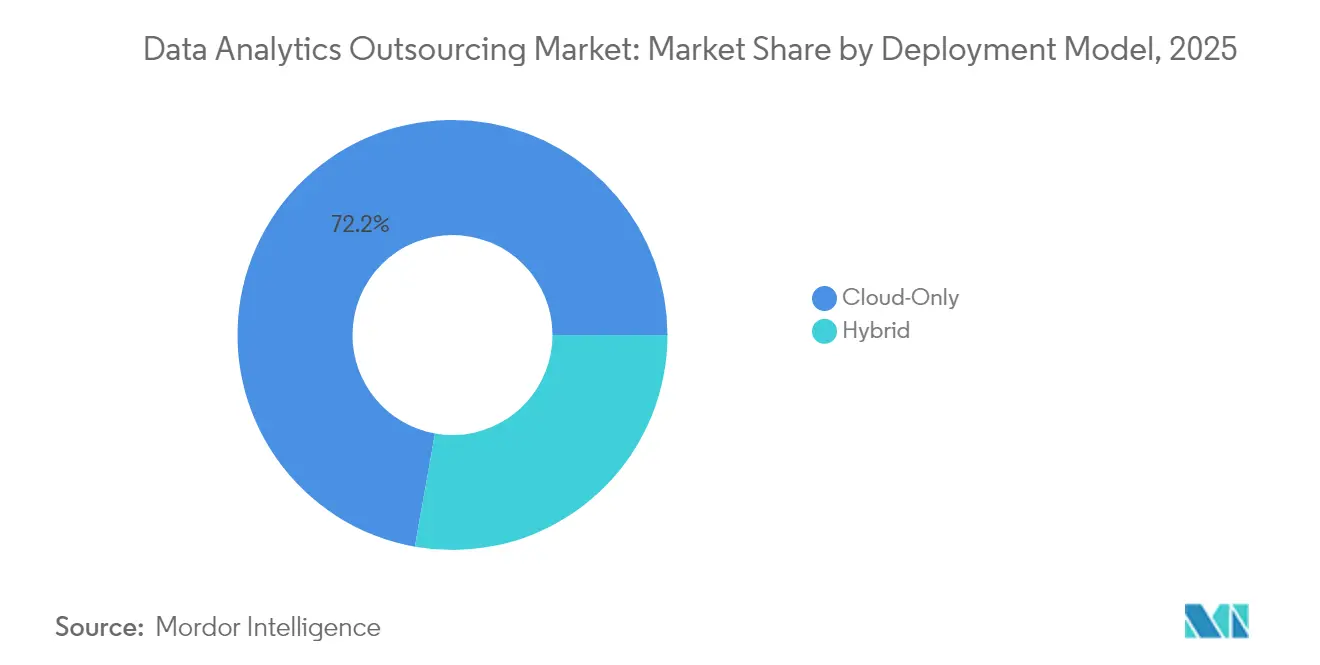

- By deployment model, cloud-only approaches captured 72.20% of the data analytics outsourcing market share in 2025, whereas hybrid cloud is growing at a 35.09% CAGR through 2031.

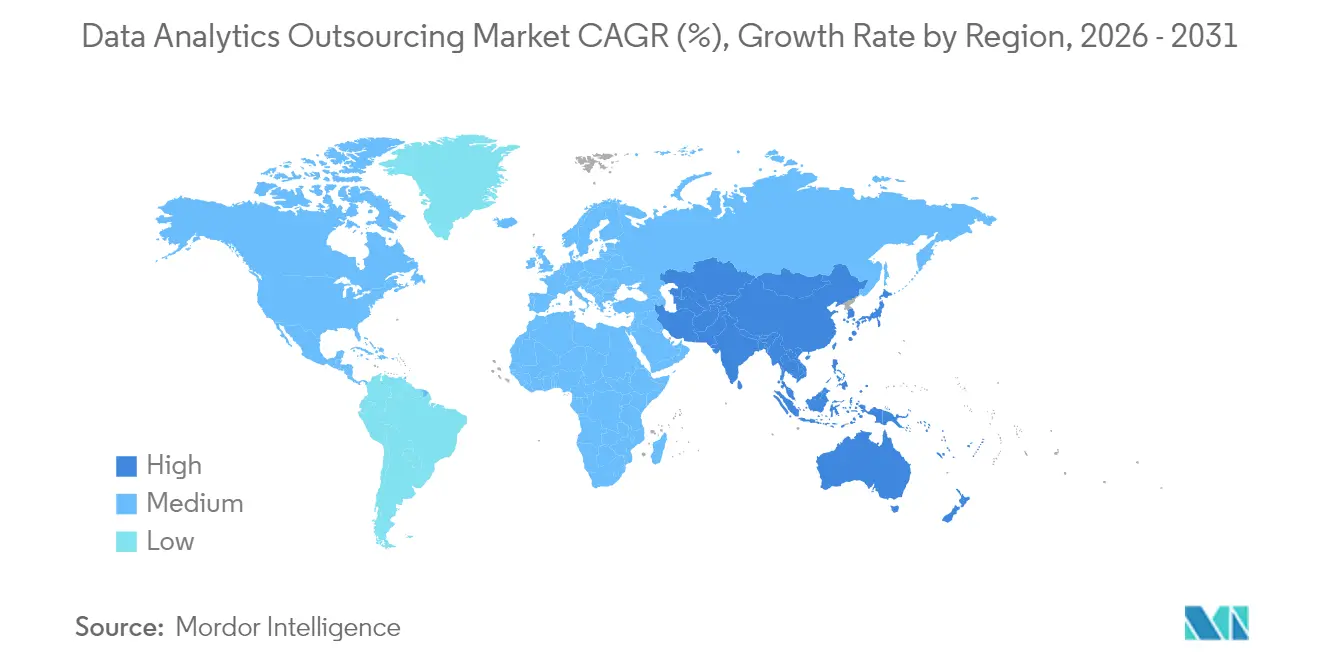

- North America retained 38.35% revenue share in 2025 and Asia Pacific is on track for a 34.62% CAGR through 2031.

- Accenture, IBM, Cognizant, and TCS collectively controlled an estimated 40.85% share of global outsourcing revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Analytics Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging enterprise data volumes and complexity | +6.5% | Global, with APAC leading growth | Medium term (2-4 years) |

| Need for near-real-time decision-making in omnichannel commerce | +5.8% | North America and EU primarily | Short term (≤ 2 years) |

| Cost-pressure to convert capex analytics stacks into variable opex | +4.2% | Global, strongest in cost-sensitive markets | Medium term (2-4 years) |

| BFSI shift to outcome-based pricing for fraud and risk analytics | +3.1% | North America, EU, select APAC | Long term (≥ 4 years) |

| Emerging Gen-AI copilots that compress insight-delivery cycles | +2.9% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Sovereign-cloud mandates triggering offshore/nearshore re-balancing | +1.8% | EU, select APAC countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Enterprise Data Volumes and Complexity

Global organizations now generate petabytes of structured, semi-structured, and unstructured data from mobile apps, IoT devices, and omnichannel touchpoints, overwhelming in-house processing capacity. Limited internal skills in data engineering and machine learning further hamper timeliness. Outsourcing partners address these gaps with pre-built ingestion pipelines, scalable cloud infrastructure, and industry-specific data models that shorten time to insight while lowering total cost of ownership. Many clients adopt pay-as-you-go data-as-a-service contracts that unlock variable pricing advantages, enabling redeployment of scarce capital toward core innovation initiatives.

Need for Near-Real-Time Decision-Making in Omnichannel Commerce

Digital shoppers expect instant personalization and seamless inventory visibility whether they engage on web, mobile, or physical channels. This expectation drives demand for analytics engines capable of processing event streams, updating recommendation algorithms, and triggering interventions within milliseconds. Building such low-latency stacks in-house requires large capital outlays in stream-processing platforms, in-memory databases, and edge servers. Specialist outsourcing vendors offer turnkey real-time analytics platforms, complete with 24×7 operations support, that let retailers and consumer brands go live quickly while converting fixed investments into variable fees tied to usage.

Cost Pressure to Convert Capex Analytics Stacks into Variable Opex

Finance teams increasingly treat on-premises analytics infrastructure as stranded capital because utilization rarely tracks peak sizing. Outsourcing swaps those fixed depreciation schedules for elastic consumption-based pricing that scales with business cycles. Many organizations report 40-60% reductions in total analytics spend after migrating workloads to managed service models. Savings accrue not only from infrastructure rationalization but from reduced talent acquisition costs because specialized data-science roles are provided as part of the service.

BFSI Shift to Outcome-Based Pricing for Fraud and Risk Analytics

Banks and insurers now prefer contracts in which providers’ compensation links directly to fraud-loss reduction, false-positive decline, or audit-readiness scores. The model aligns incentives and reinvests savings into advanced analytics experiments, creating a virtuous cycle of improvement. Providers that maintain large pools of anonymized transaction data can refine machine-learning models faster, delivering measurable value that strengthens multi-year relationships.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-residency and cross-border transfer regulations | -2.4% | EU, select APAC countries, emerging globally | Long term (≥ 4 years) |

| Talent attrition and wage inflation in India-centric delivery hubs | -1.7% | India, Philippines, other traditional offshore centers | Medium term (2-4 years) |

| Buyer concerns over LLM "model leakage" when outsourcing Gen-AI analytics | -1.9% | Global, strongest in regulated industries | Short term (≤ 2 years) |

| Vendor lock-in risk due to proprietary accelerators and templates | -1.3% | Global, particularly affecting enterprise clients | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Residency and Cross-Border Transfer Regulations

GDPR enforcement and forthcoming AI-specific statutes tighten rules on where citizen data can be stored and processed. Multinationals reassess vendor portfolios to ensure compliance documentation, secure connectivity, and geo-fencing capabilities. Outsourcing agreements now include detailed sub-processor disclosures and audit clauses, adding legal complexity that can slow deal cycles and raise costs for providers that lack certified local facilities.

Talent Attrition and Wage Inflation in India-Centric Delivery Hubs

High turnover rates among experienced data scientists and engineers drive double-digit salary increases, eroding the traditional labor-arbitrage advantage of mature offshore centers. Service providers fight back with aggressive upskilling budgets, automation of low-complexity tasks, and relocation of selective workloads to lower-cost Southeast Asian and Latin American geographies. Still, persistent churn risks project delays, knowledge loss, and higher service pricing, which may nudge buyers toward nearshore or hybrid models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Analytics Type: Prescriptive Analytics Drives Next-Generation Insights

Prescriptive tools translated 39.48% of total revenue into predictive models during 2025, yet their share continues to rise because enterprises increasingly demand recommendations rather than retrospective dashboards. The data analytics outsourcing market size for prescriptive solutions is projected to advance at a 34.32% CAGR over 2026-2031. Outsourcing partners differentiate by integrating scenario optimization engines with conversational AI, delivering decision automation that bypasses the need for specialized coding talent.

Generative AI further democratizes prescriptive analytics by allowing domain specialists to articulate business constraints in natural language, which engines then translate into optimization logic. Vendors embed frameworks that manage model governance, version control, and regulatory explainability, positioning themselves as partners in strategic decision making instead of report builders. As client expectations shift toward continuous improvement, providers bundle iterative model tuning and A/B testing into outcome-based contracts, ensuring value realization throughout the engagement lifecycle.

By End-User Industry: Healthcare Accelerates Beyond Traditional BFSI Leadership

BFSI retained 27.05% of data analytics outsourcing market share in 2025 owing to longstanding investment in credit-risk scoring, fraud detection, and regulatory reporting. Nonetheless, healthcare is climbing fastest with a 34.15% CAGR to 2031, propelled by telehealth adoption, electronic health record integration, and personalized medicine protocols. Providers offering HIPAA-compliant data lakes and pre-certified clinical analytics libraries enjoy a first-mover advantage.

Life-science firms increasingly outsource real-world evidence gathering and genomic sequencing analytics, creating high-margin opportunities for vendors with specialist domain expertise. Meanwhile, insurers partner with analytics firms to combine claims data and wearable sensor inputs, driving early-warning models that reduce hospitalization costs. As payers and providers converge around value-based care, demand rises for longitudinal patient-journey analytics that span clinical, behavioral, and social determinants of health data.

By Service Model: Nearshore Gains Momentum Amid Geopolitical Shifts

Offshore hubs delivered 59.10% of 2025 revenue, but clients are experimenting with nearshore engagement centers in Mexico, Poland, and Malaysia that provide cultural affinity and overlapping work hours. The data analytics outsourcing market size associated with nearshore services is on course for a 34.88% CAGR through 2031 as sovereign-cloud laws and geopolitical friction encourage geographic diversification.

Nearshore contracts typically bundle agile delivery pods that collaborate closely with client product teams, reducing rework and cycle times. Providers add bilingual capability centers and invest in local university partnerships to secure talent pipelines. Offshore locations remain critical for 24×7 operations and large-scale managed services, yet balanced portfolios that blend nearshore client engagement with offshore factory execution are becoming the norm.

By Organization Size: SME Adoption Accelerates Through Cloud Democratization

Large enterprises represented 66.05% of total spending in 2025 because they maintain centralized data offices and mature vendor-management functions. Nonetheless, SME contracts are forecast to grow at a 35.02% CAGR, reflecting cloud-native marketplaces that let smaller firms acquire advanced analytics on a subscription basis. Consumption models reduce upfront costs and let SMEs dial usage up or down alongside seasonal demand, making data-driven decision making attainable without dedicated internal data teams.

Providers cater to this segment with templatized data connectors, no-code model builders, and outcome-linked pricing that aligns spend with revenue impact. Because SMEs often lack legacy systems, deployments proceed faster, letting vendors showcase time-to-value metrics that strengthen reference pipelines in adjacent verticals such as retail, hospitality, and professional services.

By Deployment Model: Hybrid Cloud Balances Control with Scalability

Cloud-only workloads captured 72.20% of data analytics outsourcing market share in 2025 thanks to enterprise comfort with public-cloud resilience and native AI services. Yet hybrid architectures will be the fastest-growing choice, expanding at a 35.09% CAGR to 2031. Industry regulations and latency-sensitive edge scenarios motivate retention of specific datasets on private infrastructure while shifting compute-intensive training jobs to elastic cloud nodes.

Vendors differentiate by offering unified observability, automated workload placement, and policy-driven data-movement orchestration across private, public, and edge footprints. As hyperscale providers deploy industry-specific cloud regions, clients gain the flexibility to comply with residency laws without relinquishing access to state-of-the-art platform services.

Geography Analysis

North America generated 38.35% of 2025 revenue, reflecting the region’s deep enterprise technology budgets, mature regulatory frameworks, and early adoption of outcome-based vendor agreements. Fortune 500 multinationals rely on outsourced partners to manage data estates that underpin global operations while meeting Sarbanes-Oxley and HIPAA mandates. However, rising scrutiny of offshore labor practices and federal incentives for on-shore AI research push some workloads into Canadian and Mexican nearshore centers that offer both cultural proximity and bilingual talent.

Asia Pacific is the fastest-growing geography with a projected 34.62% CAGR between 2026 and 2031. Digital-government initiatives in India, smart-city rollouts in Southeast Asia, and large-scale manufacturing analytics programs in China all create fertile ground for data analytics outsourcing market expansion. Though India remains the primary delivery hub, emerging players in Vietnam and Indonesia secure specialized analytics work focused on AI annotation, edge computing, and domain-specific model testing. Digital-government initiatives in India, spearheaded by the national Digital India programme, are creating fertile ground for analytics-outsourcing growth across public-sector and commercial projects.

Europe’s trajectory is heavily shaped by GDPR enforcement and impending AI-risk regulations that heighten emphasis on data provenance and algorithmic transparency. Clients increasingly favor providers that can supply in-region data centers certified to European Cybersecurity Certification Scheme standards. Nearshore centers in Poland and Portugal attract investment because they blend EU compliance with cost advantages compared to Western European capitals. South America and the Middle East and Africa together account for a modest slice of current spending but display accelerating demand tied to national digital-economy plans and growing private-sector awareness of data-driven decision making.

Regulatory Landscape

Data analytics outsourcing is increasingly shaped by data-protection, cross-border transfer, and AI-governance requirements, and these expectations filter into vendor contracts, sub-processor disclosures, and audit rights. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) sets staged compliance obligations for high-risk AI systems, including conformity assessment, technical documentation, logging/traceability, and human oversight, with a key implementation threshold cited for August 2, 2026. Separately, European policymakers pursued refinements through a May 2026 provisional political agreement on the Digital Omnibus on AI, which reinforces the need for providers to operationalize governance controls alongside delivery scale.

Other jurisdiction-specific rules also reinforce localization and contractual discipline for outsourced analytics. In March 2026, Dubai issued Law No. (9) of 2026 regulating the outsourcing of government services, setting rules around contractor engagement, performance monitoring, and service quality standards, which increases compliance demands for vendors serving public-sector analytics programs. In India, the Digital Personal Data Protection (DPDP) Rules 2025 introduce a compliance clock referenced as running to November 13, 2026 for specific Data Processing Agreement clauses, pushing buyers and suppliers to update consent management and outsourced processing terms across global delivery models.

Competitive Landscape

The competitive field features a mix of global system integrators, IT-services majors, and AI-native boutiques. Accenture, TCS, IBM, and Cognizant collectively held an estimated 41% of 2024 revenue and continue to invest in proprietary AI platforms, industry accelerators, and global delivery expansion. Mid-tier specialists focus on niche capabilities such as computer-vision analytics for manufacturing or clinical-trial optimization for life sciences, carving out high-growth sub-segments.

Strategic moves in 2024 included Accenture’s launch of a USD 3 billion Data and AI investment program, IBM’s release of industry-specific Watson x assistants, and Cognizant’s acquisition of pattern-recognition startup Mobica to strengthen edge-analytics offerings. Accenture reported USD 65 billion in fiscal 2024 revenue and announced plans to double its AI workforce to 80,000 by 2026 while earmarking USD 6.6 billion for strategic acquisitions.[3]Accenture, “Annual Report 2024,” accenture.com

Pricing is shifting toward value-sharing structures that reward providers for tangible business outcomes such as fraud-loss reduction or inventory-turn improvement. Vendors able to integrate data engineering, model operations, and business-process change management in a single contract gain negotiating leverage, while pure-play staffing firms struggle to differentiate against platforms enriched with reusable IP and automation. M&A activity focuses on absorbing boutique AI labs that possess proprietary annotation tools, synthetic-data generators, or specialized LLM fine-tuning techniques.

Data Analytics Outsourcing Industry Leaders

Accenture PLC

Capgemini SE

Cognizant Technology Solutions Corp.

Genpact Ltd

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Outcome-based commercial models and platform-led delivery create whitespace for providers that can combine data engineering, MLOps, and measurable business KPIs into a single managed engagement, particularly in regulated industries that rely heavily on outsourced analytics, such as BFSI. The market is also creating demand for specialized governance and controls for generative AI analytics. Buyer concerns about LLM model leakage, alongside tightening AI compliance obligations, are pulling services for secure environments, logging, and traceability into managed offerings rather than bespoke in-house builds.

Geographic and delivery-model rebalancing also opens room for nearshore and in-region execution that meets data-sovereignty constraints while keeping cloud analytics programs moving quickly. This is reflected in vendors formalizing hyperscaler-aligned operating models and talent pools: Accenture formed dedicated business groups with Snowflake (December 2025) and Databricks (March 2026), and expanded European cloud-native data and analytics capability through the Keepler acquisition (April 2026). Together, these moves support an opportunity for providers to industrialize cloud-only delivery, the dominant deployment model in 2025, while offering hybrid patterns for sensitive datasets and public-sector workloads under tighter localization expectations.

Recent Industry Developments

- April 2026: Cognizant partnered with Google Cloud to bring agentic AI to retail customer experience, introducing an AI-powered contact center solution built on Gemini Enterprise. The launch strengthens Cognizant's packaged offerings for real-time, data-driven customer operations, and it supports outsourcing deals that combine analytics modernization with AI-assisted workflow automation.

- July 2025: Capgemini signed a definitive agreement to acquire WNS for USD 3.3 billion, expanding its intelligent operations portfolio with deeper analytics and AI-led delivery capability. The deal adds scale in outsourced data-driven business operations and broadens Capgemini's ability to deliver outcome-linked analytics programs across enterprise functions.

- June 2024: Deloitte announced a collaboration with Anthropic to bring trusted AI to commercial and government organizations, combining Deloitte's Trustworthy AI framework with the Claude model family and a plan to train more than 15,000 professionals. The partnership institutionalizes governance-focused GenAI delivery, reinforcing how provider talent programs and risk controls are becoming core differentiators in outsourced analytics engagements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues earned by third-party providers that deliver data analytics work for client organizations, including ongoing analytics operations and project-based assignments delivered remotely or on-site.

Scope exclusions: Excludes in-house analytics teams and internal shared-service centers that do not generate external vendor revenue.

Segmentation Overview

- By Analytics Type

- Descriptive Analytics

- Diagnostic Analytics

- Predictive Analytics

- Prescriptive Analytics

- By End-user Industry

- Retail and e-Commerce

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Manufacturing

- IT and Telecom

- Automotive and Transport

- Energy, Utilities and Oil-and-Gas

- Others (Media, Public Sector, etc.)

- By Service Model

- Offshore

- Nearshore

- On-shore

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Deployment Model

- Cloud-Only

- Hybrid Cloud

- By Geography

- North America

- United States

- Canada

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South-East Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

To build the base structure, we start with public statistics and definitions that help anchor the demand environment for outsourced analytics. Sources used include items such as US Bureau of Labor Statistics data on analytics and related roles, OECD and World Bank digital economy indicators, the International Telecommunication Union for connectivity measures, and Eurostat for enterprise ICT adoption patterns.

After that, the model is refined using company filings, annual reports, and investor presentations to understand service mix and regional exposure, followed by reputed press and association publications to cross-check major demand shifts. Where helpful, a paid subscription for company financials and news intelligence, and a paid patent database, are referenced to validate timelines and service-led investment signals. These desk sources are illustrative only, and many other public references were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the sizing logic with people who sell, buy, or manage outsourced analytics programs, including service providers, enterprise users, and channel partners. We also cover major regions so pricing, delivery mix (offshore, nearshore, on-site), and cloud-only versus hybrid delivery assumptions can be checked and then aligned with how contracts are actually written.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 51% |

| Mid tier: 50% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 15% | Managers: 59% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build that links enterprise analytics adoption and outsourcing penetration to spend capacity by region and major end users, and then converts that pool into revenue using typical contract mix and delivery models. The totals are corroborated with selective bottom-up checks such as sampled provider revenue splits, observed service-bundle pricing, and channel feedback on average deal sizes, which helps adjust the implied totals when gaps show up.

Key inputs used in the model include enterprise cloud-only versus hybrid usage patterns, offshore versus nearshore versus on-site delivery shares, analytics program maturity by industry, bill rate movement and utilization signals, and the pace of data platform modernization that pulls more work into managed services. When a bottom-up checkpoint is incomplete, missing slices are handled by using conservative ranges and then re-checking them with interview feedback before finalizing the roll-up.

For forecasting, scenario analysis is used because outsourcing budgets can shift quickly with cost pressure, AI tooling adoption, and security concerns. Growth paths are built for each region and major end-user group, and then reconciled so the final trajectory stays consistent with the demand indicators and expert expectations we gathered.

Data Validation & Update Cycle

Outputs are validated by comparing results against independent signals such as digital transformation spend direction, hiring and wage movement for analytics roles, and reported outsourcing pipeline commentary in public filings. If a region or industry shows an unusual jump, the assumptions are revisited, the math is rechecked, and follow-up outreach is triggered so we do not carry forward a one-off data point.

Before sign-off, the model and assumptions go through multi-step analyst reviews where variances are explained and documented in plain terms. The report is refreshed annually, and interim updates are made when material events change pricing, delivery capacity, or enterprise buying behavior. Right before delivery, a final review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Data Analytics Outsourcing Market Estimate Compared With Other Published Estimates

Published market values for data analytics outsourcing can look far apart because the included services, the year used as the starting point, and the way pricing is projected are not consistent across sources. In some cases, the same label is used, but the counted revenue streams are not the same.

Managed data platform operations and adjacent IT outsourcing items are common add-ons in other estimates, but they can inflate totals when they are blended into analytics work without a clear separation. Some sources also anchor on a different base year and then apply a single growth rate across regions, which can miss delivery mix changes and the impact of cloud-only versus hybrid delivery on contract value. Provider feedback on bill rates and utilization, along with region-wise currency timing, also matters because it shifts the converted USD totals from one publisher to another.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.54 B (2026) | |

| Global Research Publisher A | USD 18.00 B (2025) | Uses a broader scope that blends solutions and services and anchors the series on a different base year, which can pull in adjacent platform-related service revenue. |

| Industry Publisher B | USD 9.24 B (2023) | Starts earlier and may undercount newer hybrid delivery contracts and later-cycle enterprise adoption, which tends to lift the measured spend in subsequent years. |

The spread in values is mostly explained by what is counted as outsourcing revenue, and the year chosen to represent the current market. Excluding adjacent IT-managed services from the analytics-only revenue pool keeps Mordor Intelligence aligned to contracts where analytics work is the paid deliverable, and that makes the total easier to trace back to delivery mix, pricing, and adoption inputs.

Key Questions Answered in the Report

How large is the data analytics outsourcing market in 2026?

The market is valued at USD 14.54 billion in 2026 and is projected to grow rapidly through 2031.

What CAGR is expected for data-analytics outsourcing through 2031?

The forecast indicates a 33.47% CAGR between 2026 and 2031.

Which region shows the fastest growth?

Asia Pacific is set to expand at a 34.62% CAGR owing to aggressive digital-transformation programs.

Why are hybrid-cloud deployments gaining traction?

Hybrid cloud balances regulatory control over sensitive data with the scalability of public-cloud analytics services.

Which industry will grow most quickly in outsourcing analytics?

Healthcare is projected to post a 34.15% CAGR on the back of personalized-medicine and clinical-analytics use cases.

Page last updated on: