Outsourcing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.02 Trillion |

| Market Size (2031) | USD 1.35 Trillion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outsourcing Services Market Analysis by Mordor Intelligence

The Outsourcing Services Market size is projected to be at USD 0.94 trillion in 2025, USD 1.02 trillion in 2026, and reach USD 1.35 trillion by 2031, growing at a CAGR of 5.77% from 2026 to 2031. Enterprises are shifting from head-count-based billing to outcome-linked contracts that align provider compensation with client business metrics, a transition supported by the growing reliability of generative AI platforms. Data-residency mandates are splintering traditional global delivery models, compelling vendors to build micro-delivery hubs in Tier-2 cities while balancing higher compliance costs against lower wage bills. Wage inflation in legacy offshore hubs is narrowing historical cost advantages and intensifying competition from nearshore alternatives in South America and Eastern Europe. At the same time, zero-trust security frameworks are raising the technical bar for vendor qualification, favoring large providers with well-funded security operations.

Key Report Takeaways

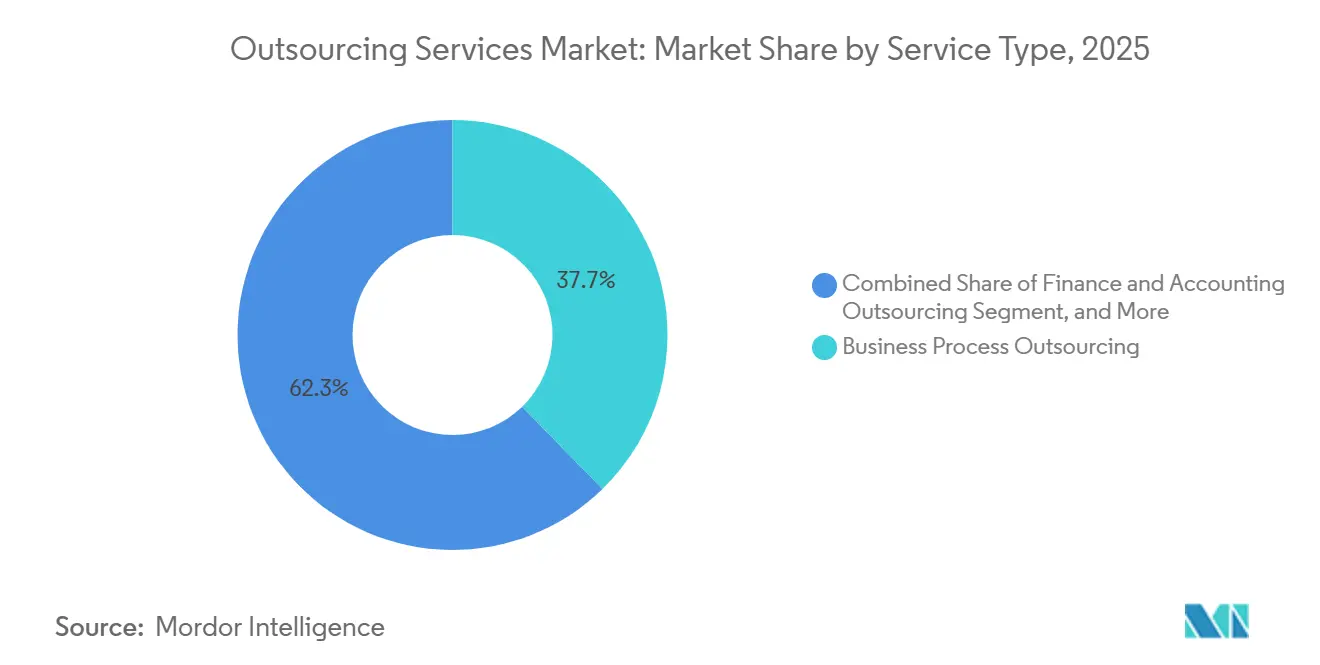

- By service type, business process outsourcing led with 37.72% of the outsourcing services market share in 2025, whereas knowledge process outsourcing is forecast to expand at a 6.11% CAGR between 2026 and 2031.

- By end-user industry, BFSI held 29.58% revenue share in 2025; healthcare is projected to grow at a 7.37% CAGR through 2031.

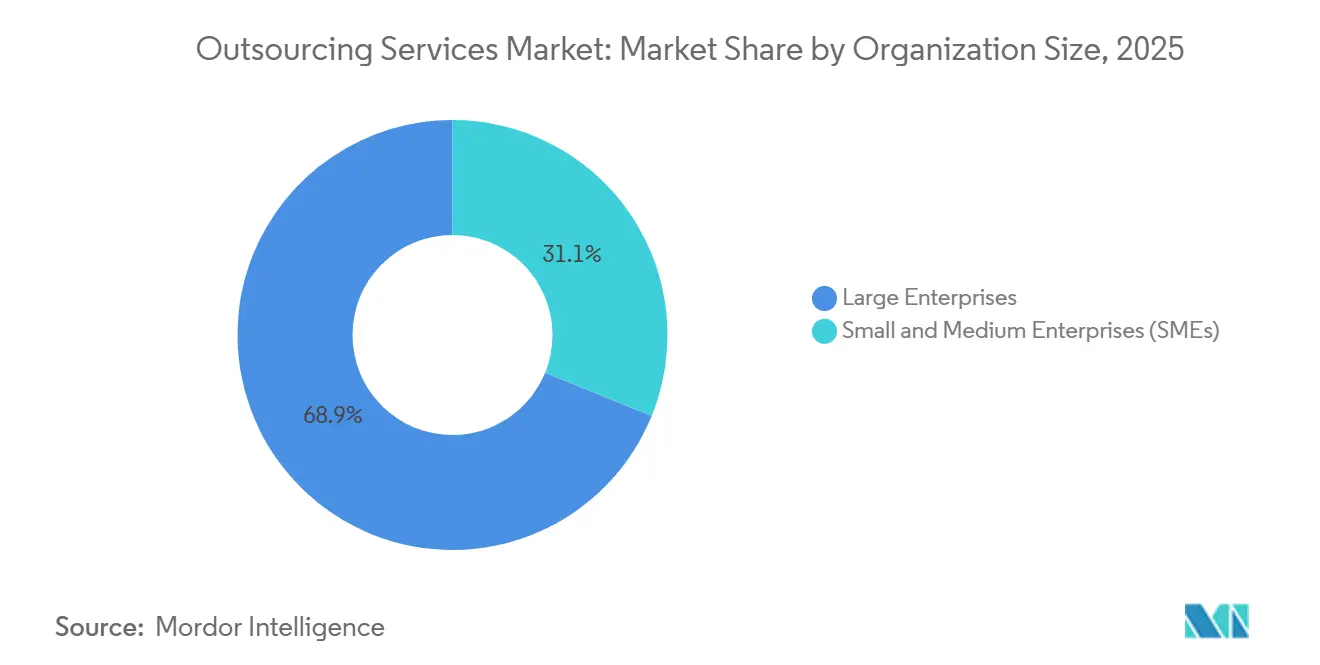

- By organisation size, large enterprises contributed 68.86% of spending in 2025, while small and medium enterprises are expected to advance at a 6.93% CAGR to 2031.

- By contract type, managed services captured 45.24% of value in 2025; project-based outsourcing is anticipated to climb at a 5.92% CAGR during the forecast period.

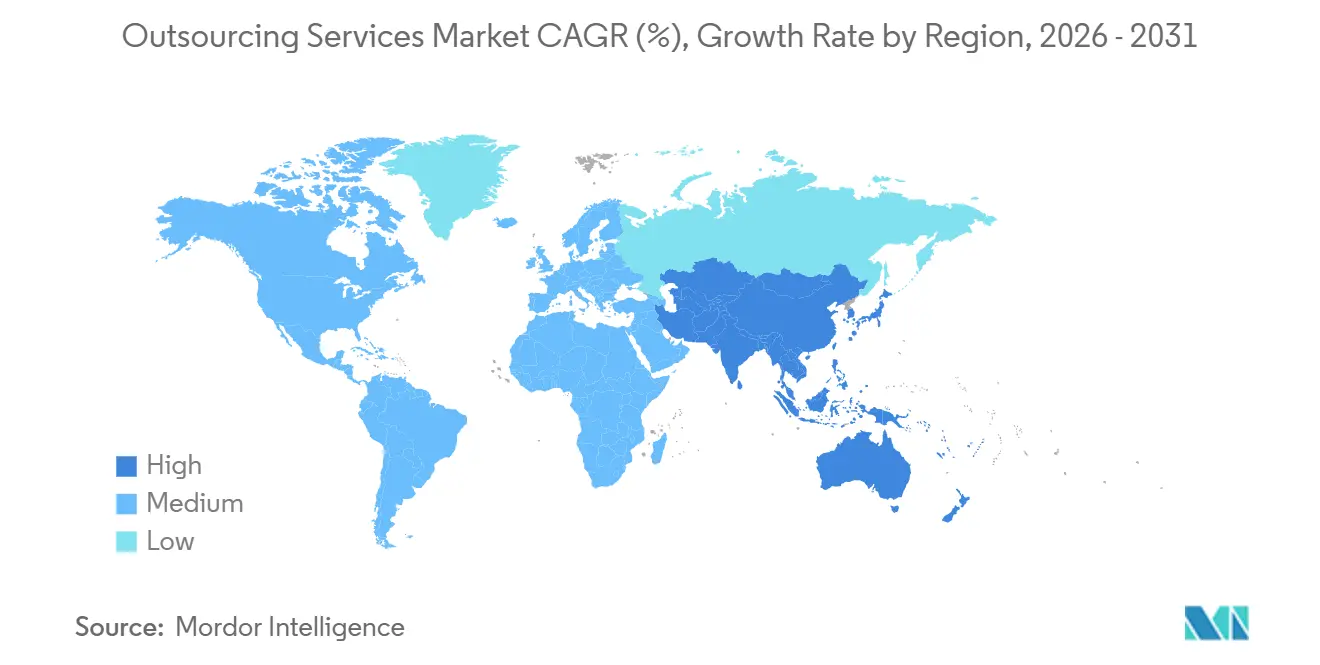

- By geography, North America retained 42.66% of 2025 revenue, whereas Asia Pacific is set to grow at a 7.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Outsourcing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cloud migration and virtualised infrastructure | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing demand for scalable and cost-efficient IT environments | +1.0% | Global, particularly Asia Pacific and Latin America | Short term (≤ 2 years) |

| Rise of outcome-based pricing models | +0.9% | North America and Europe, expanding to Asia Pacific | Medium term (2-4 years) |

| Cyber-resilient zero-trust framework adoption | +0.8% | Global, led by BFSI and Healthcare sectors | Long term (≥ 4 years) |

| Service-provider owned Gen-AI knowledge models (post-2026) | +0.7% | Global, early adoption in North America and India | Long term (≥ 4 years) |

| Near-shore micro-delivery centres in Tier-2 cities | +0.5% | Latin America, Eastern Europe, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud Migration and Virtualised Infrastructure

Cloud penetration reached 63% among Global 2000 companies by end-2025, fueling demand for partners that can orchestrate multi-cloud estates across Amazon Web Services, Microsoft Azure, and Google Cloud Platform. Virtualised infrastructure lets service providers spin up client-dedicated environments without large data-center investments, lowering barriers for mid-tier vendors and tightening price competition. Consumption-based billing aligns vendor incentives with utilization, motivating providers to optimize capacity rather than pass through fixed fees. Compliance audits under ISO 27001 and SOC 2 have become baseline requirements for cloud-enabled deals, creating additional service revenue for firms that maintain continuous assurance dashboards. North American and European enterprises are renegotiating legacy on-premises agreements as they shift entire application portfolios to cloud-native architectures, expanding the overall outsourcing services market opportunity.

Growing Demand for Scalable and Cost-Efficient IT Environments

Pay-as-you-go service catalogs now let Small and Medium Enterprises subscribe to discrete infrastructure, application management, and security modules without upfront capital outlays, widening the addressable market for outsourcing services. Total cost of ownership is eclipsing hourly rate comparisons, with buyers factoring in hidden costs such as time-zone coordination and prolonged knowledge transfer. Automation platforms enable providers to deliver 20%–30% cost reduction even when delivery teams sit in higher-wage countries, diminishing the historic primacy of offshoring. South American and Eastern European hubs are leveraging wage proximity, bilingual talent, and time-zone alignment to secure nearshore contracts from North American and European clients, reinforcing regional diversification.

Rise of Outcome-Based Pricing Models

Outcome-linked agreements represented 18% of new contracts in 2025, up from 11% in 2023. By pegging vendor fees to quantifiable results such as collections cycle time or revenue uplift, buyers shift delivery risk to providers, who in turn are investing in predictive analytics and process-mining tools to safeguard margins. Stripe observed a 23% boost in customer lifetime value for engagements transitioning from fixed-fee to outcome-based billing. Adoption is strongest in finance and accounting functions where metrics are easily benchmarked and monitored. Compliance frameworks such as GDPR and HIPAA constrain optimization levers, ensuring data protection principles are upheld even as vendors pursue aggressive performance gains.

Cyber-Resilient Zero-Trust Framework Adoption

Mandates such as the United States BOD 23-01 require federal agencies to implement zero-trust by 2025, and private firms are following the same roadmap.[1]CISA, “Zero Trust Maturity Model,” cisa.gov Gartner estimated 63% enterprise adoption for at least one critical workload in 2025, and projects more than 80% by 2028. Providers must now integrate seamlessly with client identity and access management, deploy micro-segmentation, and furnish real-time telemetry, raising entry barriers for smaller vendors. BFSI and Healthcare buyers accelerate zero-trust uptake because the average breach cost hit USD 4.88 million in 2024. The technical rigor required for continuous verification favors providers that operate mature security operations centers and maintain next-generation endpoint detection infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating data-localisation mandates | -0.6% | Europe, China, India, Brazil, with spillover to ASEAN | Medium term (2-4 years) |

| Wage-inflation volatility across key delivery hubs | -0.5% | India, Philippines, Eastern Europe | Short term (≤ 2 years) |

| Geopolitical friend-shoring limiting multi-shore models | -0.4% | North America and Europe sourcing decisions | Medium term (2-4 years) |

| Client shift to niche, specialist providers | -0.3% | Global, particularly in Healthcare and Life Sciences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Data Localisation Mandates

The European Union’s GDPR, China’s Personal Information Protection Law, India’s Digital Personal Data Protection Act 2023, and Brazil’s LGPD require personal data to remain inside national borders or be transferred under strict adequacy frameworks, fragmenting economies of scale in the outsourcing services market.[2]European Commission, “Data Protection in the EU,” ec.europa.eu Providers are racing to establish country-specific data centers, duplicating infrastructure expenditure and auditing costs. Multijurisdictional compliance raises contract complexity, slowing deal cycles and capping margin upside. Enterprises must now weigh jurisdiction-specific costs and risk exposure when choosing delivery locations, encouraging regionalized procurement strategies that disadvantage global arbitrage models.

Wage-Inflation Volatility Across Key Delivery Hubs

Compensation in India’s IT-BPM sector rose 10%–12% in 2024, mirrored by 8%–10% increases in the Philippines and 9%–11% in Eastern Europe, compressing provider margins in labor-intensive segments. The wage premium for artificial intelligence talent runs 40%–60% above traditional development roles, stretching payroll budgets for providers still reliant on manual processes. Vendors are automating Tier-1 support and reallocating human agents to exception handling, but this transition requires capital that mid-tier firms struggle to secure. Persistent wage spikes undermine long-term pricing commitments, prompting buyers to negotiate shorter contract terms or link rates to inflation indices, which adds revenue uncertainty for providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Knowledge Process Outsourcing Outpaces Transactional Work

Business Process Outsourcing controlled 37.72% of outsourcing services market share in 2025, yet Knowledge Process Outsourcing is forecast to expand at a 6.11% CAGR through 2031, the fastest among service families. Knowledge Process Outsourcing caters to analytics-heavy tasks such as clinical data review and regulatory submission drafting that cannot be commoditized easily, preserving pricing power. Information Technology Outsourcing remains the single largest contributor in absolute terms, but hyperscale cloud services are eroding traditional infrastructure management margins, pushing vendors toward higher-value cloud migration and modernization projects.

Generative AI amplifies the productivity of Knowledge Process Outsourcing by automating literature reviews and generating first-draft technical documents that human experts refine, enabling providers to deliver sophisticated outputs without proportionally scaling headcount. Business Process Outsourcing contracts focused on repetitive tasks face margin pressure because agent-assist AI can resolve customer queries and process invoices autonomously. Vendors in Information Technology Outsourcing are therefore expanding DevOps, containerization, and micro-services offerings to preserve relevance as enterprises migrate to cloud-native stacks.

By End-User Industry: Healthcare Surges on Regulatory Tailwinds

Banking, Financial Services, and Insurance captured 29.58% of 2025 spending, underpinned by open banking initiatives and heightened fraud-monitoring requirements that favor specialized service providers. Healthcare, however, is projected to be the fastest-growing vertical at 7.37% CAGR through 2031 as value-based reimbursement, telehealth expansion, and stringent billing accuracy rules drive demand for revenue-cycle management, medical coding, and telehealth back-office services.[3]Centers for Medicare and Medicaid Services, “Value-Based Programs,” cms.gov IT and Telecom enterprises are outsourcing network operations and software quality engineering to free internal resources for 5G and edge-computing priorities.

Healthcare adoption is boosted by HIPAA-mandated data-security frameworks that necessitate sophisticated compliance capabilities among vendors, which larger providers can more readily supply. Retail and E-commerce firms are ramping up outsourcing of supply-chain analytics and seasonal customer care, leveraging providers that can scale rapidly during peak shopping windows. Manufacturing and energy firms remain cautious due to legacy systems and union agreements but are exploring pilot engagements in predictive maintenance and asset-performance analytics to validate outsourcing efficacy.

By Organisation Size: Small and Medium Enterprises Embrace Modular Services

Large Enterprises represented 68.86% of 2025 revenue, reflecting complex operations that benefit from dedicated delivery teams and long-term frameworks. Small and Medium Enterprises are forecast to outpace the overall outsourcing services market at 6.93% CAGR, propelled by modular, click-to-activate service catalogs that lower contractual friction. Consumption-based pricing lets SMEs procure enterprise-grade security, backup, and help-desk capabilities without capital budgets, democratizing access to sophisticated technology.

Latin American and Southeast Asian SMEs are especially active, seeking bilingual support and region-specific payment schedules that align with local cash-flow constraints. Large Enterprises are diversifying vendor portfolios, engaging niche specialists for regulatory-intensive functions while retaining Tier-1 partners for global service desks. SMEs still face hurdles such as limited in-house vendor management expertise and heightened data security concerns, prompting providers to bundle onboarding assistance and transparent cost calculators to accelerate decision-making.

By Contract Type: Project-Based Engagements Test New Capabilities

Managed Services held 45.24% of 2025 contract value, reflecting enterprise preference for predictable monthly fees and outsourced accountability. Project-Based Outsourcing is projected to grow at 5.92% CAGR as organizations pilot new vendors on discrete digital transformation projects before committing to multi-year engagements. Staff Augmentation is losing share because it retains operational risk within the client organization and often proves more costly once supervision time is included.

Agile delivery frameworks favor short, iterative projects that align naturally with Project-Based Outsourcing structures, enabling clients to measure vendor performance quickly. Managed Services providers are embedding outcome-based metrics, such as transaction throughput and customer satisfaction, into service-level agreements, enhancing alignment but requiring investment in monitoring and continuous improvement platforms. Staff Augmentation remains viable for specialized, short-term skill gaps such as cloud security assessments or regulatory audits, though its share of total spend is shrinking.

Geography Analysis

North America held 42.66% of global outsourcing spending in 2025, underpinned by entrenched vendor relationships, regulatory comfort with cross-border data flows under frameworks such as the EU-US Data Privacy Framework, and the concentration of Fortune 500 headquarters in the United States and Canada.

Asia Pacific is poised to grow at 7.99% from 2026 to 2031, propelled by India's ambition to reach USD 254 billion in services exports and the Philippines' expansion into high-value voice and non-voice work that leverages its English proficiency and cultural affinity with Western buyers. Europe’s growth is moderated by strict data-localisation rules that encourage nearshore solutions in Poland, Romania, and the Czech Republic instead of offshore engagements in Asia, a trend that benefits Eastern Europe at the expense of India and the Philippines.

South America is rising as a time-zone-aligned nearshore alternative for North American buyers, with Mexico, Brazil, and Argentina investing in bilingual digital talent and fiber infrastructure. The Middle East and Africa remain nascent, though sovereign wealth funds in the United Arab Emirates and Saudi Arabia are financing captive centers focused on finance and human resources processing. Wage inflation of 10%-12% in India and similar levels in the Philippines are prompting providers to automate transactional workloads and focus on knowledge-intensive processes, preserving the outlook for outsourcing services market growth despite cost headwinds. Vietnam and Indonesia are positioning as overflow hubs, emphasizing English-language training and targeted incentives to attract service-delivery investment.

Competitive Landscape

The outsourcing services market is moderately consolidated; the top 10 providers control roughly most of global revenue, leaving ample room for regional specialists and born-digital challengers. Accenture, Tata Consultancy Services, and Cognizant each executed multiple acquisitions in the second half of 2025 to add Salesforce, ServiceNow, and data-engineering expertise. Smaller vertical specialists are capturing share in Healthcare and Life Sciences where domain knowledge trumps sheer scale. Technology capability is the primary battleground, with providers racing to build proprietary generative AI models that compress service-delivery cost while enhancing quality.

Nearshore vendors in South America and Eastern Europe are benefiting from friend-shoring preferences among North American and European clients seeking geopolitical alignment and real-time collaboration. Wage inflation in India and the Philippines is compressing Business Process Outsourcing margins, motivating providers to redeploy human agents to exception management and to invest in automation for Tier-1 inquiries. Regulatory compliance with ISO 27001, SOC 2, and GDPR has become table stakes, and smaller vendors that cannot fund annual audits risk exclusion from enterprise shortlists.

Emerging disruptors operate 100% in the cloud, eschew legacy on-premises assets, and use AI-driven delivery orchestration to sustain competitive pricing. The white-space opportunity lies in outcome-based contracts for SMEs, a segment historically overlooked by Tier-1 vendors due to high sales overhead relative to deal size. Providers that master templated, rapidly deployable outcome models stand to unlock incremental demand without proportionally increasing headcount.

Outsourcing Services Industry Leaders

Accenture PLC

Tata Consultancy Services Limited

Capgemini SE

Cognizant Technology Solutions Corporation

HCL Technologies Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Infosys acquired in-tech, a Germany-based automotive engineering firm, adding 2,500 embedded-software engineers to strengthen its software-defined vehicle portfolio.

- December 2025: Accenture bought Cientra, a United States data-engineering consultancy, to deepen real-time analytics expertise on AWS, Azure, and Google Cloud.

- November 2025: HCL Technologies completed a USD 1.8 billion purchase of Hewlett Packard Enterprise’s communications and media unit, adding 10,000 specialists in network transformation.

- November 2025: Cognizant acquired Belcan Engineering Group for USD 1.3 billion, securing 6,500 aerospace engineers skilled in digital twin technology.

- November 2025: Accenture absorbed AKOA, a French Salesforce consulting partner, gaining 200 certified professionals in Sales Cloud, Service Cloud, and Marketing Cloud.

Global Outsourcing Services Market Report Scope

The outsourcing services market study tracks the demand for outsourcing services such as business process outsourcing, information technology outsourcing, human resource outsourcing, knowledge process outsourcing, and other service types worldwide. The analysis is primarily based on the market insights captured through primary and secondary research.

The Outsourcing Services Market Report is Segmented by Service Type (Business Process Outsourcing, Information Technology Outsourcing, Human Resource Outsourcing, Knowledge Process Outsourcing, Finance and Accounting Outsourcing), End-User Industry (Banking Financial Services and Insurance, Healthcare, IT and Telecom, Retail and E-commerce, Other End-User Industries), Organisation Size (Large Enterprises, Small and Medium Enterprises), Contract Type (Staff Augmentation, Managed Services, Project-Based Outsourcing), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Business Process Outsourcing (BPO) |

| Information Technology Outsourcing (ITO) |

| Human Resource Outsourcing (HRO) |

| Knowledge Process Outsourcing (KPO) |

| Finance and Accounting Outsourcing (FAO) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| IT and Telecom |

| Retail and E-commerce |

| Other End-User Industries |

| Large Enterprises |

| Small and Medium Enterprises (SME) |

| Staff Augmentation |

| Managed Services |

| Project-Based Outsourcing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Business Process Outsourcing (BPO) | ||

| Information Technology Outsourcing (ITO) | |||

| Human Resource Outsourcing (HRO) | |||

| Knowledge Process Outsourcing (KPO) | |||

| Finance and Accounting Outsourcing (FAO) | |||

| By End-User Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare | |||

| IT and Telecom | |||

| Retail and E-commerce | |||

| Other End-User Industries | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium Enterprises (SME) | |||

| By Contract Type | Staff Augmentation | ||

| Managed Services | |||

| Project-Based Outsourcing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the outsourcing services market by 2031?

The market is expected to reach USD 1.35 trillion by 2031, growing at a 5.77% CAGR.

Which service category will grow fastest through 2031?

Knowledge Process Outsourcing is forecast to expand at a 6.11% CAGR as demand for analytics-heavy work rises.

Why is healthcare spending on outsourced services accelerating?

Regulatory shifts toward value-based reimbursement and telehealth back-office needs are driving a 7.37% CAGR in healthcare outsourcing.

How are data-localisation laws affecting vendor strategies?

Providers are building country-specific data centers, increasing infrastructure costs and reducing traditional scale efficiencies.

What role does generative AI play in outsourcing engagements?

Providers use generative AI to automate research, draft documents, and enhance service quality without proportionally increasing headcount.

Which regions are emerging as attractive nearshore alternatives?

Latin America and Eastern Europe are gaining share due to time-zone alignment, bilingual talent, and geopolitical compatibility.

Page last updated on: