Finance And Accounting Outsourcing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

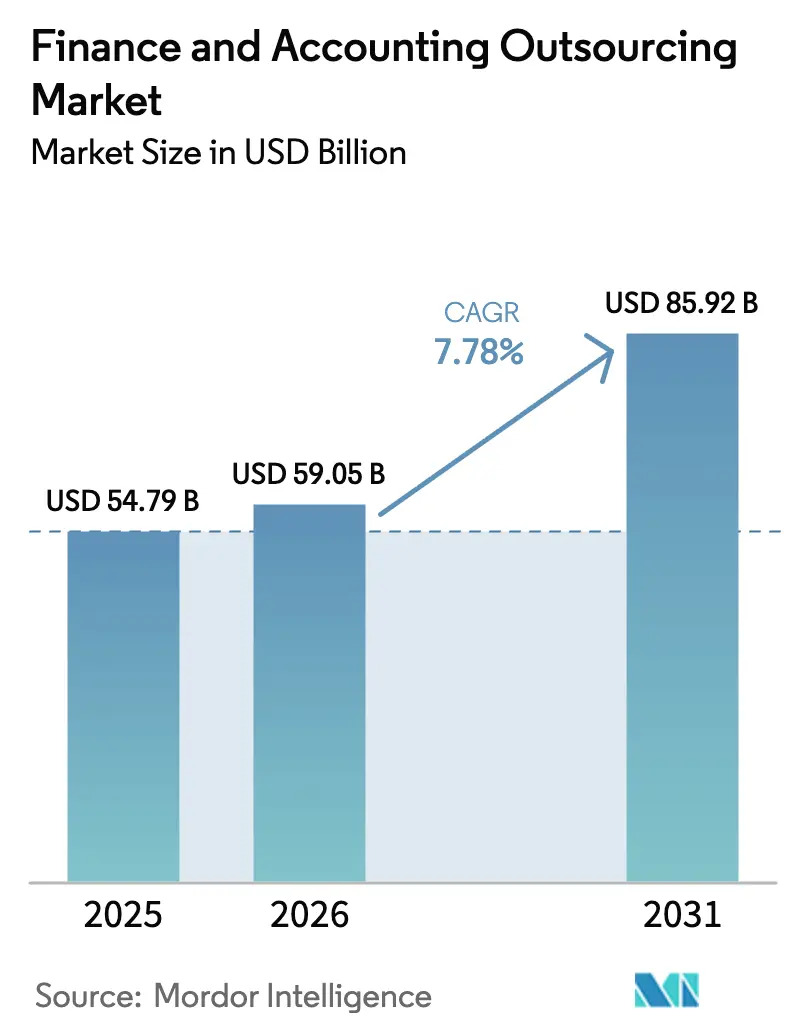

| Market Size (2026) | USD 59.05 Billion |

| Market Size (2031) | USD 85.92 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

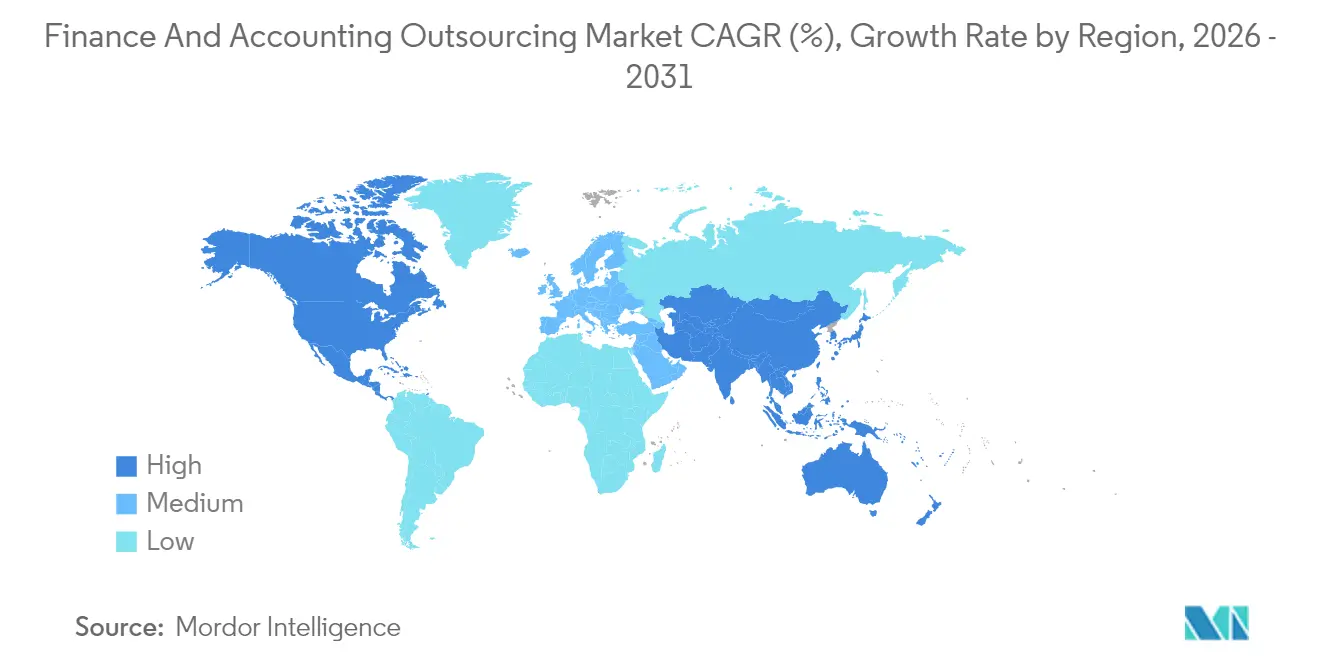

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Finance And Accounting Outsourcing Market Analysis by Mordor Intelligence

The finance and accounting outsourcing market size is expected to grow from USD 54.79 billion in 2025 to USD 59.05 billion in 2026 and is forecast to reach USD 85.92 billion by 2031 at 7.78% CAGR over 2026-2031. Rapid automation of routine bookkeeping, growing acceptance of outcome-based contracts, and stricter rules around ESG and global tax reform guide this upward path. Vendors combine artificial intelligence, analytics, and domain talent to offer real-time insights that replace traditional labor–arbitrage models. North America keeps its lead as digital finance adoption rises, while Asia-Pacific grows fastest as multinational companies expand Global Capability Centres. Buyers of every size now evaluate providers on cyber-resilience, data-sovereignty alignment, and demonstrable business results, which raises entry barriers for purely cost-driven competitors.

Key Report Takeaways

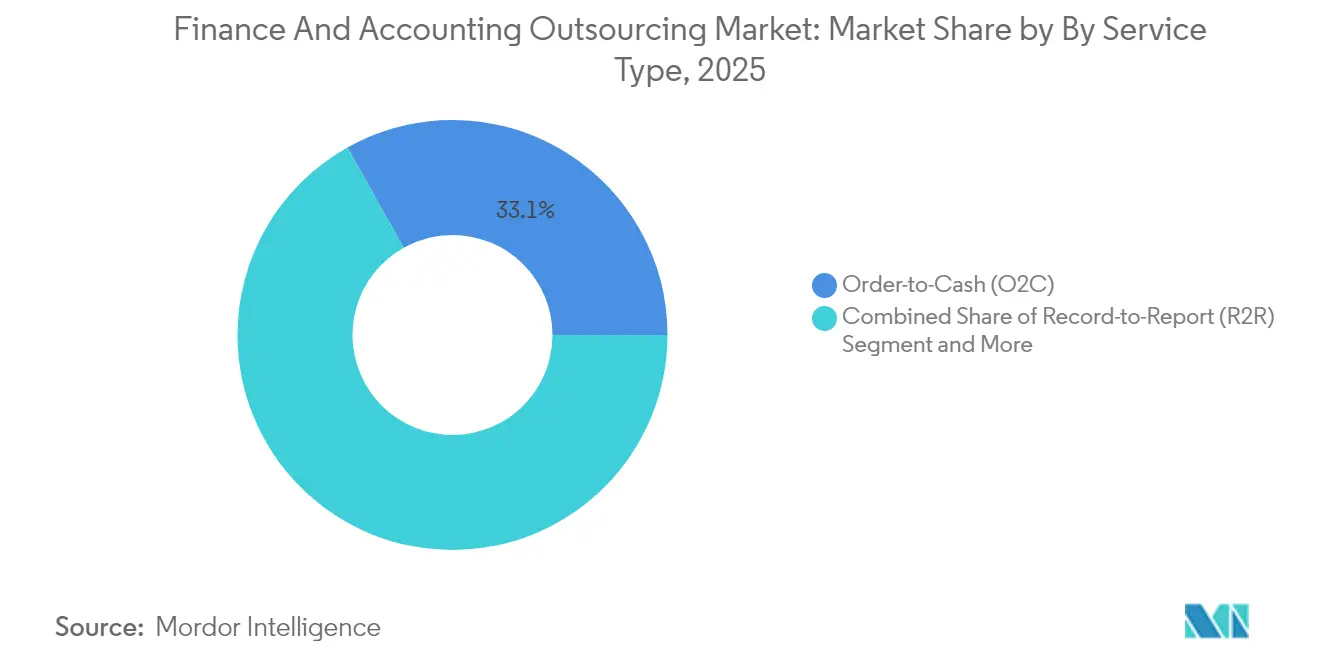

- By service type, multi-process engagements held 33.12% of the finance and accounting outsourcing market share in 2025; order-to-cash processes are set to expand at an 8.22% CAGR through 2031.

- By enterprise size, large enterprises accounted for 64.02% share of the finance and accounting outsourcing market size in 2025, while the SME segment is forecast to grow at 8.93% CAGR to 2031.

- By industry vertical, manufacturing contributed 28.15% revenue share in 2025; healthcare and life sciences are projected to rise at an 11.02% CAGR over the same period.

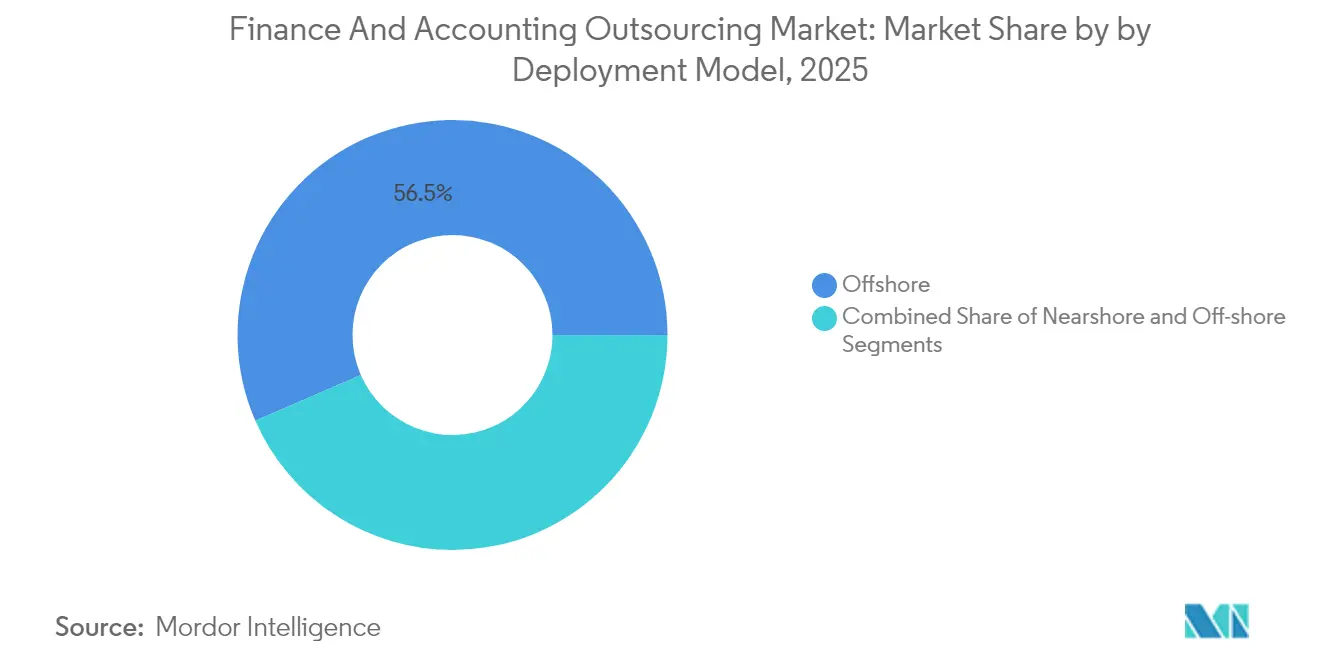

- By Deployment Model, offshore contributed 56.53% revenue share in 2025: Near-shore is projected to rise at a 9.66% CAGR over the same period.

- By the Contract Model, Multi-process contributed 33.86% revenue share in 2025; it is projected to rise at a 7.45% CAGR over the same period.

- By Geography, North America led with 40.88% of the finance and accounting outsourcing market share in 2025, whereas Asia-Pacific is expected to post a 8.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Finance And Accounting Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-reduction and talent-access imperative | +1.8% | Global with emphasis on North America and Europe | Short term (≤ 2 years) |

| Automation and AI infusion in FAO workflows | +2.1% | Global led by Asia-Pacific and North America | Medium term (2-4 years) |

| Outcome-based pricing and value-partnership models | +1.2% | North America and Europe expanding to Asia-Pacific | Medium term (2-4 years) |

| ESG / non-financial reporting compliance push | +1.4% | Europe and North America with spillover to Asia-Pacific | Long term (≥ 4 years) |

| BEPS 2.0-driven demand for tax expertise | +0.9% | Global with concentration in multinational hubs | Long term (≥ 4 years) |

| Cloud-ERP migrations demanding real-time analytics | +1.3% | Global with early uptake in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-reduction and talent-access imperative

Retirement-driven shortages and declining CPA enrolment tighten domestic supply of accountants, prompting firms to tap offshore talent pools. United States buyers often pivot to India where deep technical skills and professional certifications remain plentiful. A mid-size manufacturer reported savings of 25% to 45% after shifting end-to-end accounting services to an Indian provider while still accessing more than 400 qualified accountants. Beyond labor savings, offshore teams grant expertise in ESG disclosure and BEPS compliance that is scarce locally. Demand is particularly strong among manufacturers who must manage complex cost accounting and international tax structures. The scale of the talent gap—estimated at 300,000 open roles by 2025—keeps the finance and accounting outsourcing market on a steady expansion path.

Automation and AI infusion in FAO workflows

Intelligent automation has moved beyond invoice capture into anomaly detection, predictive forecasting, and self-healing reconciliation. One leading AI platform secured USD 34 million to build agents that cut bookkeeping time by 30% for a United States CPA firm. In another case, a global healthcare outsourcer doubled productivity and hit 99.5% accuracy on correspondence by integrating robotic process automation with natural-language models. Manufacturers such as Siemens have reached more than 90% touchless handling of delivery notes with annual benefits exceeding EUR 5 million[1]“Siemens Automates Delivery-Note Processing With AI,” DeepOpinion, deepopinion.ai.These gains free finance teams to focus on advisory work and encourage clients to negotiate value-linked contracts instead of hourly billing.

Outcome-based pricing and value-partnership models

CFOs increasingly favor fee structures tied to receivables cycle reduction, compliance accuracy, or working-capital release. A logistics platform documented a 37% fall in days sales outstanding—down from 35 days to 22 days—after a provider reorganized its order-to-cash workflow

[2]Veryable Cuts DSO With Upflow Platform,” Upflow, upflow.io. Robust tracking tools allow both sides to agree on metrics, which lowers disputes and builds longer partnerships. Providers that combine analytics dashboards with process expertise differentiate in the finance and accounting outsourcing market because they can guarantee measurable outcomes rather than merely supply labor hours.

ESG / non-financial reporting compliance pushes

The European Union Corporate Sustainability Reporting Directive requires companies to publish granular ESG data from 2026. The rule covers more than 50,000 entities and demands disclosure against 1,100 distinct data points. Many organizations lack the systems and skill sets to collect, validate, and audit such information. Outsourcing partners that already manage financial close processes extend into sustainability accounting by layering materiality assessment, carbon-footprint tracking, and stakeholder reporting services. AI-enabled extraction tools further cut manual effort and boost data confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cyber-risk concerns | -1.1% | Global with emphasis on Europe and North America | Short term (≤ 2 years) |

| Hidden transition costs and process complexity | -0.8% | Global affecting SMEs most | Short term (≤ 2 years) |

| Near-shore wage inflation eroding cost arbitrage | -0.6% | Latin America and Eastern Europe | Medium term (2-4 years) |

| Data-localisation regulations limiting offshoring | -0.7% | Global with varied regional intensity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-privacy and cyber-risk concerns

Rules like the United States safeguard measure that restricts sensitive data transfers to certain jurisdictions elevate compliance hurdles. European General Data Protection Regulation introduces fines that can reach 4% of global revenue, compelling providers to invest in encryption, zero-trust architecture, and location-specific data stores[3]US Tightens Controls on Sensitive Data Transfers,” Davis Polk, davispolk.com. Healthcare buyers face additional obligations under HIPAA, which often pushes them toward near-shore or on-shore centers. These requirements increase due diligence costs and lower the immediate savings once promised by offshore models, tempering adoption in highly regulated sectors.

Hidden transition costs and process complexity

Organizations sometimes underestimate the effort required to migrate fragmented ledgers, train offshore teams, and integrate cloud-ERP tools. Legal reviews, change-management programs, and middleware licenses raise the total bill and can consume over 30% of the initial budget if not planned precisely. Integration challenges intensify for companies with legacy mainframe finance systems or industry-specific regulatory checks. Smaller enterprises struggle most because internal project-management resources are limited, which delays value realization and can erode confidence in the finance and accounting outsourcing industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated solutions gain priority

Order-to-Cash (O2C) secured a 33.12% slice of finance and accounting outsourcing market share in 2025, confirming buyer preference for unified governance across accounts payable, receivable, and general ledger activities. This consolidation lowers vendor-management overhead and simplifies technology roll-outs. The finance and accounting outsourcing market size attached to multi-process deals is projected to advance steadily as clients seek platform-driven standardisation and analytics. Order-to-cash solutions will climb at an 8.22% CAGR through 2031 because economic uncertainty elevates cash-position monitoring. Demand for record-to-report remains resilient thanks to ongoing statutory reporting obligations, and financial planning and analysis services gain traction as boards ask finance teams for faster scenario modelling.

Adoption patterns vary by industry. Manufacturers use bundled services to align cost-accounting data with supply-chain planning, trimming reconciliation cycles. Healthcare providers outsource end-to-end revenue-cycle tasks, using analytics to flag denial trends and boost collection rates. AI accelerates reconciliation accuracy, pushing providers to commit to outcome metrics such as touchless-transaction percentages. Tax compliance work grows as BEPS 2.0 rules take effect, fuelling requests for specialised filing, audit-trail generation, and transfer-pricing analysis.

By Enterprise Size: Cloud platforms empower smaller firms

Large organizations captured 64.02% of finance and accounting outsourcing market size in 2025 by leveraging global shared-service footprints to achieve scale economies. They continue to pilot advanced analytics and autonomous close initiatives with tier-one vendors. Yet cloud ERP and plug-and-play APIs enable smaller businesses to tap the finance and accounting outsourcing market without large capital outlay. The SME segment is on course for a 8.93% CAGR, supported by subscription pricing and modular service catalogues that align cost with revenue cycles.

Providers tailor offerings to SME pain points such as bookkeeping accuracy, multistate payroll, and sales-tax compliance. Remote implementation toolkits cut change-over time, while chat-based advisory portals give smaller finance teams direct access to experts. Outcome-linked contracts appeal to entrepreneurs because fees scale with results, not input hours. For large organizations, geopolitical risk and data-residency mandates spur diversification of delivery locations, blending near-shore centers in Latin America with established Indian hubs.

By Industry Vertical: Healthcare surges under regulatory weight

Manufacturing retained 28.15% of finance and accounting outsourcing market share in 2025, reflecting its complex inventory costing, multi-currency operations, and growing investment in industrial automation. However, healthcare and life sciences will chart an 11.02% CAGR through 2031 as hospitals and pharmaceutical firms modernize revenue-cycle management and prepare for value-based care reimbursement. The finance and accounting outsourcing market size within healthcare includes tasks from claims adjudication to research-grant accounting, each governed by stringent privacy rules.

Banking, financial services, and insurance players maintain steady outsourcing levels because Basel IV, Solvency II, and IFRS-17 reporting changes require continuous updates. Retail and ecommerce clients seek order-and-payment reconciliation that spans multiple marketplaces, while energy utilities outsource project accounting for renewable-infrastructure builds. Vertically specialized delivery teams become critical differentiators as buyers value domain literacy over generic transaction processing.

By Deployment Model: Near-shore adoption rises

Offshore hubs such as India and the Philippines still provided 56.53% of service delivery in 2025, sustained by extensive capacity, English proficiency, and mature process frameworks. The near-shore model is projected to post a 9.66% CAGR through 2031 as data-localisation statutes and time-zone alignment gain prominence. North American firms increasingly sign statements of work with Latin American providers in Mexico and Colombia because proximity supports agile collaboration and cultural affinity.

Providers expand bilingual delivery teams and invest in customer-experience training to match on-shore quality. Wage inflation in popular near-shore cities narrows the cost gap, prompting vendors to differentiate with specialised analytics and sector-focused centres of excellence. Offshore players respond by establishing “follow-the-sun” models that pair India night shifts with United States day shifts to maintain responsiveness.

By Contract Model: Multi-process integration dominates value capture

Multi-process agreements made up 33.86% of engagements in 2025 and are expected to grow at 7.45% CAGR. Buyers prefer a single statement of work that covers procure-to-pay, order-to-cash, and record-to-report because data flows seamlessly across modules. Providers leverage common workflow engines and AI-powered reconciliation algorithms to unlock cross-process insights. The finance and accounting outsourcing market benefits when vendors can automate exception handling at the source rather than in downstream reports.

Single-process contracts remain entry vehicles, particularly where clients test a provider’s performance in accounts payable before expanding scope. Successful pilots often convert to multi-process renewals with outcome clauses covering net working capital and closing-cycle days. Shared gain-share structures encourage both parties to target continuous improvement and technology refresh.

Geography Analysis

North America commanded 40.88% of the finance and accounting outsourcing market in 2025. Enterprises there face high labour costs and rising attrition of certified accountants, which pushes demand for external partners with deep automation toolkits. United States buyers extend captive centres in Mexico and Costa Rica to mitigate data-sovereignty worries and enable Spanish-language support. Canada shows stable adoption among energy, mining, and public-sector entities that require bilingual documentation in English and French. Regulatory depth under Sarbanes-Oxley keeps internal-control outsourcing in focus, while SEC scrutiny on non-GAAP metrics encourages independent validation by third-party specialists.

Asia-Pacific will record the fastest 8.84% CAGR through 2031. India’s Global Capability Centres host more than 1.6 million finance professionals and push maturity from transactional processing to controlling and treasury analytics. The Philippines invests in advanced robotic-process-automation academies to graduate talent able to handle high-value tasks. Vietnam and Malaysia position themselves as specialty hubs for Japanese and Australian clients seeking cultural proximity and cost savings. Regional governments offer fiscal incentives and data-security frameworks that reassure multinational investors.

Europe balances cost and compliance pressures. Buyers often adopt a hub-and-spoke strategy that locates strategic finance close to headquarters while shifting volume work to Eastern Europe. Poland and Romania supply multilingual accountants who understand local GAAP and IFRS. The EU Corporate Sustainability Reporting Directive intensifies demand for outsourced ESG data management. Providers embed data centres within the European Economic Area to guarantee GDPR adherence. Brexit complexities stimulate finance-process offshoring by United Kingdom businesses to near-shore Ireland for Eurozone access.

Competitive Landscape

Competition remains moderate with a blend of global system integrators, specialised business-process outsourcers, and emerging AI-native challengers. Accenture, Tata Consultancy Services, Wipro, and Genpact leverage scale economies, extensive domain playbooks, and large automation partnerships to anchor multi-year contracts. Mid-tier firms focus on industry specialization and partner ecosystems. For instance, one niche provider concentrates on ESG reporting, aligning its data-collection engine with the European Sustainability Reporting Standards.

Technology ownership has become a primary battleground. AI vendors that automate invoice coding or anomaly detection license their engines to multiple outsourcers, lowering entry barriers. Some providers buy stakes in those platforms to lock exclusive rights. Strategic acquisitions escalate: a leading cloud accounting vendor secured a USD 2.5 billion payment-tech deal to embed end-to-end transaction services into its platform. Private-equity groups invest heavily, evidenced by a USD 2 billion valuation for a mid-market United States CPA firm, aiming to roll up regional practices into data-driven networks.

Client expectations pivot toward joint innovation roadmaps and transparent performance dashboards. Providers respond with outcome-based pricing, co-development of analytics use cases, and proof-of-concept sandboxes. Those unable to demonstrate tangible KPI improvement risk margin pressure and churn. The top five vendors collectively hold less than 45% of total revenue, leaving room for consolidation around technology assets and vertical depth.

Finance And Accounting Outsourcing Industry Leaders

Accenture plc

Genpact Limited

Tata Consultancy Services Limited

Infosys Limited

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Xero acquired fintech Melio for more than USD 2.5 billion to expand digital payment capabilities within its cloud accounting suite.

- May 2025: Thirteen firms merged under Sorren, backed by DFW Capital Partners, creating a USD 170 million revenue platform with operations across four countries.

- April 2025: Baker Tilly US and Moss Adams announced a USD 7 billion merger, targeting USD 6 billion annual revenue by 2030.

- April 2025: Earned Wealth bought Chahal and Associates, strengthening services for healthcare professionals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the finance and accounting outsourcing market as all fee-based contracts in which enterprises delegate core record-to-report, procure-to-pay, order-to-cash, financial planning and analysis, tax compliance, or payroll activities to third-party specialists; revenues from shared-service centers, captives, and purely software subscriptions are left out, so our numbers track only service fees that buyers actually pay to external vendors.

Scope exclusion: advisory projects such as ERP implementation or one-off audit support are not counted.

Segmentation Overview

- By Service Type

- Order-to-Cash (O2C)

- Procure-to-Pay (P2P)

- Record-to-Report (R2R)

- Financial Planning and Analysis (FPandA)

- Tax Processing and Compliance

- Payroll Outsourcing

- Other Services

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Manufacturing

- Healthcare and Life Sciences

- Information Technology and Telecommunications

- Retail and E-commerce

- Energy and Utilities

- Other Verticals

- By Deployment Model

- On-shore

- Near-shore

- Off-shore

- By Contract Model

- Multi-process FAO

- Single-process FAO

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed outsourcing buyers, tier-1 providers, and mid-size regional firms across North America, Europe, Asia-Pacific, and Latin America. These conversations tested rate cards, average full-time-equivalent (FTE) loads, cloud finance platform penetration, and compliance-driven demand swings, helping us correct desk-research blind spots before finalizing assumptions.

Desk Research

We began by harvesting public datasets such as U.S. Bureau of Labor Statistics wage files, UN Comtrade export codes for business-process services, OECD digital-services trade tables, and statements from bodies such as ACCA and IFAC, which anchor labor pools, pay scales, and regulatory pressure points. Company 10-Ks, investor decks, and reputable business dailies supplied contract values, near-shore openings, and automation adoption rates. Select paid sources, including D&B Hoovers for client counts and Dow Jones Factiva for deal flow, rounded out trend signals. This list is illustrative; dozens of other sources were screened for corroboration and clarity.

Market-Sizing & Forecasting

A top-down construct starts from national business-process-services revenue and separates the finance-and-accounting slice using provider disclosures and customs data; selective bottom-up checks sampled average selling price multiplied by deal volumes temper the totals. Variables such as CFO vacancy rates, labor cost differentials, RPA deployment counts, cross-border data-sovereignty laws, and SME cloud-ERP uptake feed a multivariate-regression forecast that extends to 2030. Gaps where supplier granularity is thin are bridged with validated penetration ratios from primary research.

Data Validation & Update Cycle

Outputs pass multi-step variance tests, peer reviews, and anomaly flags. Because market conditions evolve swiftly, reports refresh yearly and we trigger interim updates when material events, such as large M&A and regulatory shifts, arise. Just before delivery, an analyst re-checks every figure.

Why Mordor's Finance And Accounting Outsourcing Baseline Commands Reliability

Published estimates often differ; scope choices, exchange-rate cuts, and refresh timing explain most gaps.

Key gap drivers include some firms folding adjacent HR or procurement BPO into totals, others excluding payroll-only deals, and a few projecting uniform double-digit price inflation without cross-validating regional FTE rates, whereas Mordor's cadence and scope guard against such swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 54.79 B (2025) | Mordor Intelligence | - |

| USD 64.86 B (2024) | Global Consultancy A | Adds non-F&A BPO segments and applies single global ASP |

| USD 52.3 B (2024) | Industry Journal B | Omits payroll outsourcing and assumes muted SME adoption |

These contrasts show that our disciplined scope definition, mixed-method model, and annual refresh give decision-makers a balanced baseline they can trace back to transparent variables and reproducible steps.

Key Questions Answered in the Report

What is the current value of the finance and accounting outsourcing market?

The finance and accounting outsourcing market was valued at USD 59.05 billion in 2026 and is projected to reach USD 85.92 billion by 2031.

Which region leads the finance and accounting outsourcing market?

North America leads with 40.88% of 2025 revenue, driven by mature adoption and a widening talent gap.

Which service segment is growing fastest?

Order-to-cash outsourcing is set to grow at an 8.22% CAGR through 2031 as firms focus on cash-flow efficiency.

Why are SMEs accelerating outsourcing adoption?

Cloud ERP and subscription pricing reduce entry barriers, allowing SMEs to access professional finance capabilities while spreading costs as they scale.

How does AI influence outsourcing provider selection?

Buyers prioritise vendors that embed intelligent automation, predictive analytics, and outcome-based dashboards, which improve accuracy and shorten closing cycles.

What is the main risk associated with finance and accounting outsourcing?

Data-privacy regulations and cyber-risk exposure raise compliance costs and can limit offshoring options, especially for highly regulated industries.

Page last updated on: