In Vitro Lung Model Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

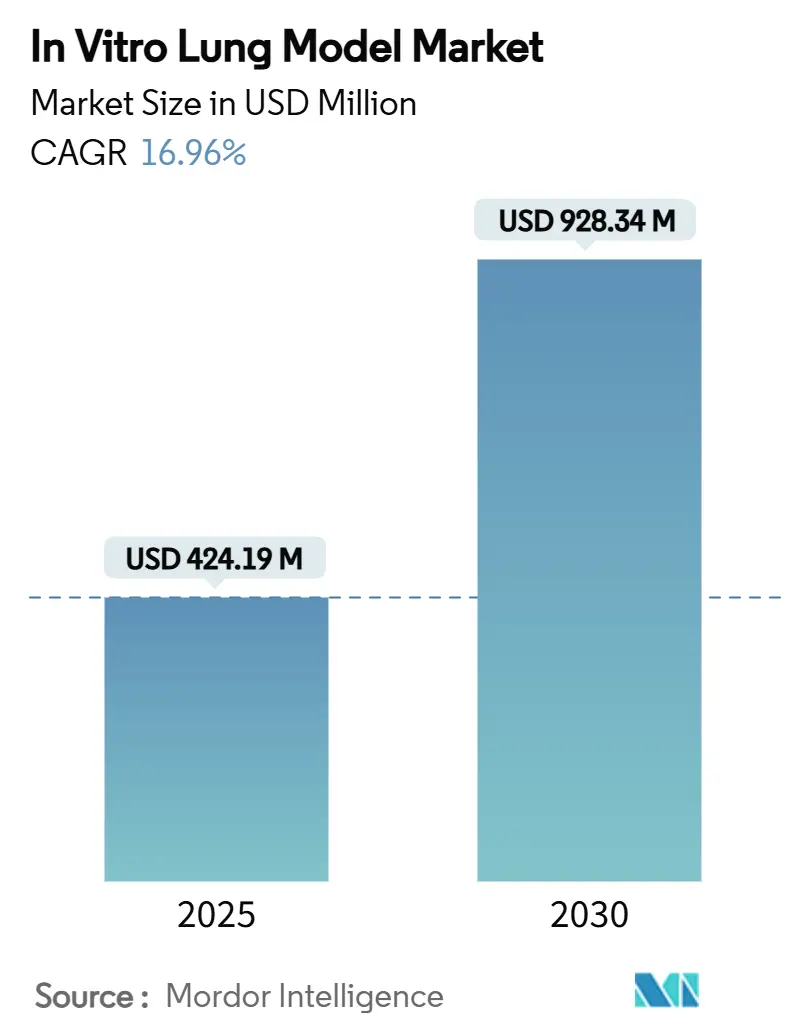

| Market Size (2025) | USD 424.19 Million |

| Market Size (2030) | USD 928.34 Million |

| Growth Rate (2025 - 2030) | 16.96% CAGR |

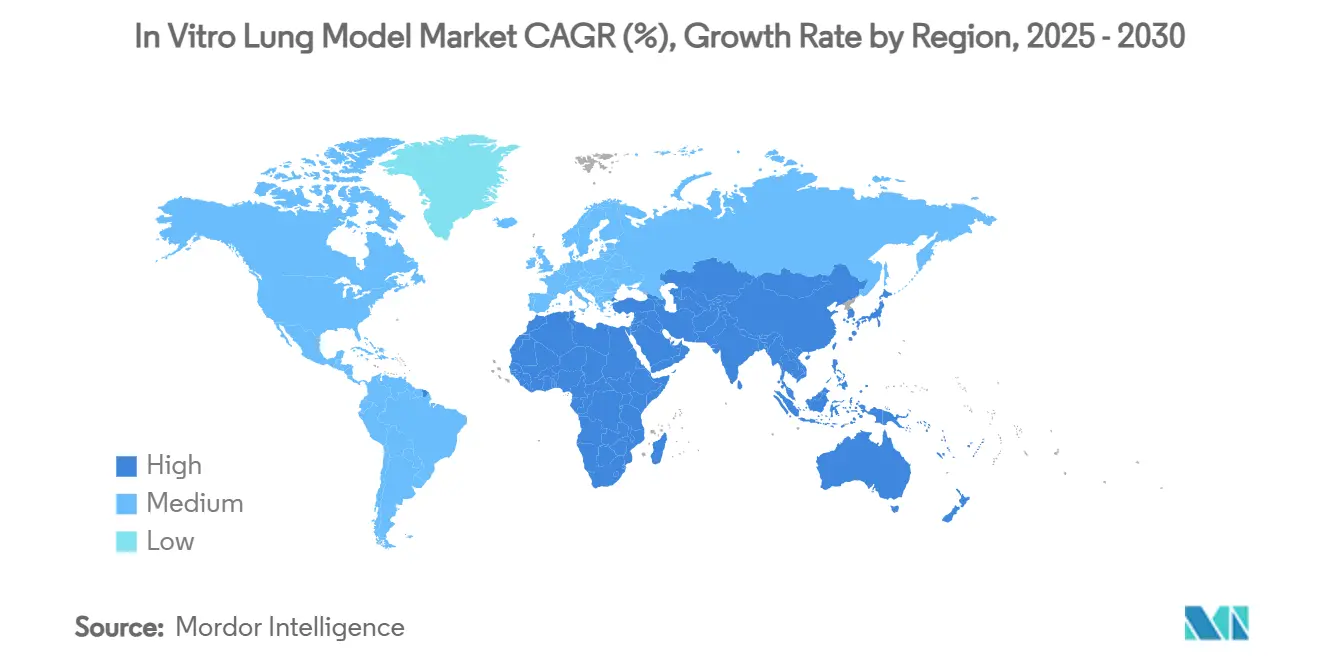

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In Vitro Lung Model Market Analysis by Mordor Intelligence

The In Vitro Lung Model Market size is estimated at USD 424.19 million in 2025, and is expected to reach USD 928.34 million by 2030, at a CAGR of 16.96% during the forecast period (2025-2030).

Regulatory agencies are openly endorsing in-vitro alternatives most notably the FDA’s 2024 guidance on New Alternative Methods thereby accelerating corporate investment in organ-on-chip and organoid platforms. Rapid post-pandemic growth in inhaled therapeutics, sustained Horizon Europe grants, and continuing advances in stretchable microfluidic systems are reinforcing demand from both drug developers and academic laboratories. At the same time, validation bottlenecks and capital-intensive hardware temper adoption rates, obliging suppliers to pair technical innovation with rigorous regulatory engagement.

Key Report Takeaways

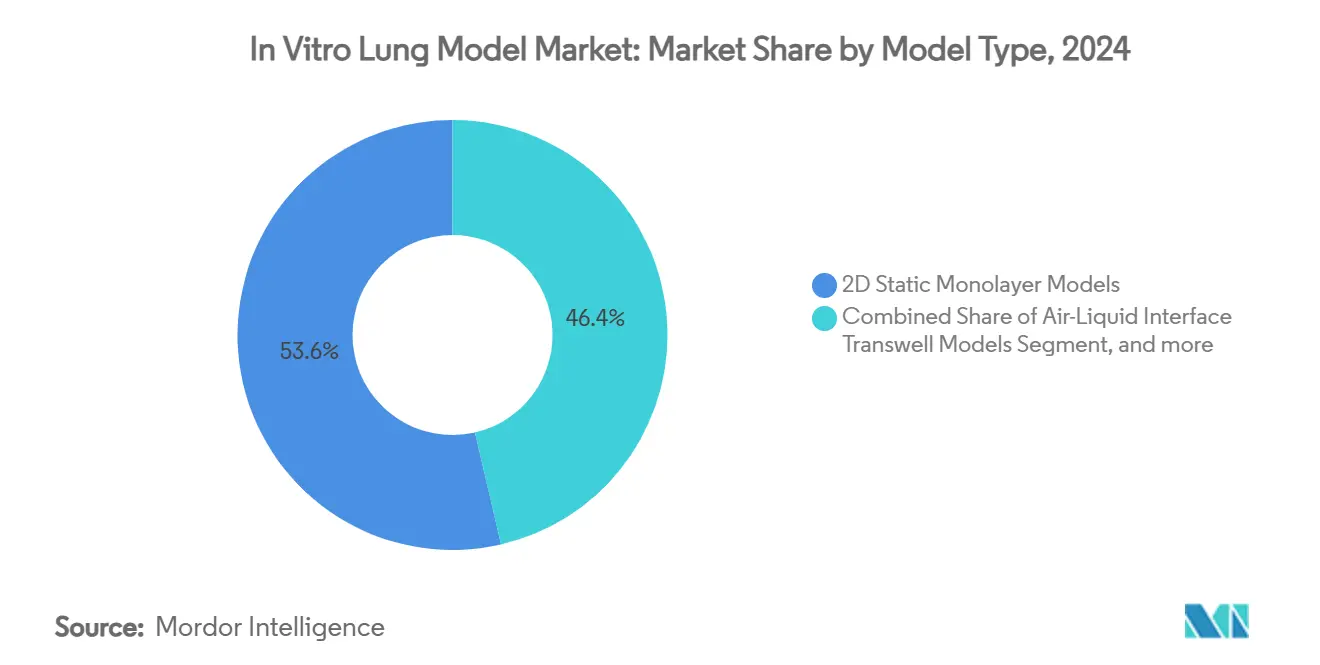

- By model type, 2D static monolayer models led with 53.63% of the in vitro lung model market share in 2024, while organ-on-chip microfluidic models are advancing at an 18.05% CAGR through 2030.

- By application, drug discovery & lead optimisation accounted for 44.87% of the in vitro lung model market size in 2024; Disease Modelling is expanding at 19.40% CAGR to 2030.

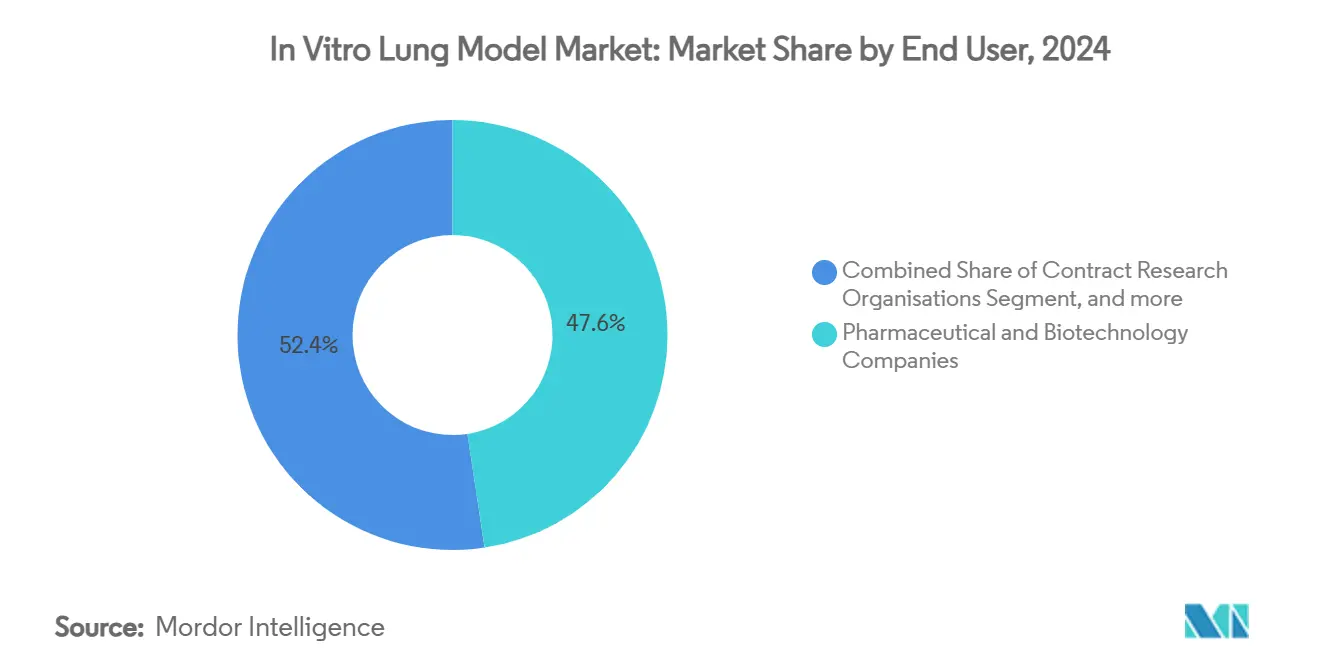

- By end user, pharmaceutical & biotechnology companies held 47.62% of the in vitro lung model market share in 2024, whereas academic & research institutes record the fastest 21.85% CAGR through 2030.

- By geography, North America maintained 42.05% revenue in 2024; Asia-Pacific is set to expand at a 26.32% CAGR over the forecast horizon.

Global In Vitro Lung Model Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global phase-out of animal testing | +4.2% | North America & EU lead, global follow-on | Medium term (2-4 years) |

| Surge in inhaled therapeutics post-pandemic | +3.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| EU-funded Horizon projects on scalable lung micro-physiology | +2.1% | Europe with spillover to North America | Long term (≥ 4 years) |

| Commercialisation of stretchable microfluidic lung systems | +2.9% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shift to iPSC-derived patient-specific lung models | +2.6% | Global, strongest in North America | Long term (≥ 4 years) |

| Rising respiratory disease burden | +1.8% | Global, ageing regions pronounced | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global phase-out of animal testing enhancing demand for lung alternatives

Legislatures on three continents are mandating systematic reductions in vertebrate testing, prompting drug developers to align pipeline workflows with validated in-vitro lung constructs.[1]U.S. Food and Drug Administration, “Modernization Act Guidance on New Alternative Methods,” fda.gov FDA guidance now lists organ-on-chip data among acceptable toxicity endpoints, a position echoed by the European Parliament’s roadmap, creating a policy-driven tailwind that reclassifies lung models as compliance necessities rather than exploratory tools.[2]European Commission, “EU Roadmap for Animal-Testing Phase-out,” europa.eu Pharmaceutical firms are reallocating preclinical budgets toward microfluidic chips that better anticipate human pharmacokinetics, thereby boosting order volumes for full-integrated breathing systems. Vendors capable of generating Good Laboratory Practice data packages see an immediate competitive lift as regulatory filings increasingly reference chip-based toxicity read-outs. Over the medium term, multi-agency alignment is expected to cut validation cycles, widening the customer base to cost-sensitive generics manufacturers.

Surge in inhaled therapeutics post-pandemic boosting respiratory R&D

The COVID-19 crisis reframed respiratory drug delivery as a universal strategic priority, expanding inhaled modality pipelines across antivirals, fibrosis agents, and COPD biologics. Sophisticated 3D airway constructs now enable granular tracking of aerosol deposition profiles under variable breathing regimes, giving formulation scientists actionable metrics before animal or clinical stages. This real-time insight shortens lead optimisation loops and lowers attrition linked to poor pulmonary targeting. The clear linkage between airway-specific pharmacology and pandemic resilience continues to attract venture capital, keeping start-up suppliers well-funded for translational improvements. Short-term gains materialise mainly in North America and Europe; Asia-Pacific uptake accelerates as local pharma pivots toward respiratory franchises.

EU-funded Horizon projects advancing scalable lung micro-physiology

Horizon Europe’s multi-year grants are underwriting consortia that merge bioprinting, sensor integration, and AI analytics to produce standardised lung chips ready for industrial volume.[3]Horizon Europe, “Scalable Organ-on-Chip Consortia,” cordis.europa.eu Deliverables include harmonised manufacturing protocols, quality-control algorithms, and cross-border validation datasets. Such standard-setting lowers technical risk for mid-sized biotech buyers that previously avoided bespoke microfluidic solutions. European suppliers benefit from preferential adoption in domestic regulatory filings, yet open-access project outputs also lift North American licensees. Over the long term, these frameworks can compress cost curves and extend chip utility beyond discovery into post-approval safety monitoring.

Commercialisation of stretchable microfluidic lung systems

Next-generation lung chips now incorporate elastomeric membranes actuated at physiologic frequencies, faithfully simulating breathing mechanics and surfactant dynamics. Drug permeation and inflammatory signalling differ markedly under cyclic stretch, compelling toxicologists to switch from static cultures to dynamic chips for decisive go/no-go calls. Integrated smoke-inhalation channels further widen use-cases to environmental toxicology and tobacco-harm reduction. Platform vendors partner with imaging-software firms to automate read-outs, lowering the expertise hurdle for first-time users. The resulting mid-term CAGR uplift is strongest in North America, where regulatory submissions already cite stretch data to explain mode-of-action nuances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardised OECD validation for lung constructs | -3.1% | Global, high in regulated markets | Medium term (2-4 years) |

| Capital intensity of dynamic lung-on-chip platforms | -2.4% | Global, cost-sensitive regions | Short term (≤ 2 years) |

| Supply-chain variability of primary human airway cells | -1.8% | Global, supplier cluster-dependent | Short term (≤ 2 years) |

| Interoperability gaps with legacy high-throughput systems | -1.5% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of standardised OECD validation for lung constructs

OECD guidelines covering skin, eye, and hepatic in-vitro assays are yet to be matched by a lung-specific test battery, leaving sponsors to negotiate bespoke validation packages for every assay run. The absence heightens regulatory risk and forces duplicative inter-lab ring trials that slow commercial roll-outs. Meanwhile, divergent national acceptance criteria create patchwork compliance hurdles, particularly for global multi-centre studies. Ongoing cross-agency working groups promise harmonised protocols, but consensus timelines still run multiple years, leading many mid-tier CROs to defer investment in complex chips.

Capital intensity of dynamic lung-on-chip platforms for CROs

Micro-machined silicone membranes, precision pumps, and high-resolution live-cell imaging suites push per-station hardware costs to six-figure USD sums, a threshold too steep for many fee-for-service CROs operating on slim utilisation margins. Even when capital is found, specialist operator training adds further overhead, elongating ROI. This economic burden confines adoption to big pharma and flagship academic institutes, curbing broader market expansion in the short term. Vendors are responding with subscription-based leasing models, yet depreciation and servicing facts still deter lower-volume users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Model Type: Organ-on-Chip Platforms Drive Innovation

The in vitro lung model market size for 2D Static Monolayer systems remains the largest market share of 53.63% in 2024, yet the category’s CAGR lags markedly behind dynamic microfluidic platforms. organ-on-chip systems integrate breathing motions and fluid shear, yielding data that more accurately forecasts human exposure outcomes, a feature driving their 18.05% growth trajectory. ALI Transwell inserts function as a pragmatic bridge for high-throughput toxicology screens, sustaining volume demand from consumer-product safety labs. Meanwhile, 3D cell aggregates fill a crucial niche in oncology research where spheroid geometry better reflects tumour oxygen gradients.

Automated 3D printing has begun to erode historical cost barriers: BMF Biotechnology’s nano-resolution printers fabricate chip housings within hours, cutting per-unit expenditure by double-digit percentages. Research institutions exploit mucus-enriched bioinks to recreate airway viscosity, enhancing cilia beat synchrony and pathogen entry modelling. The iterative feedback between biomedical engineers and toxicologists is set to accelerate innovation, positioning organ-on-chip suppliers for above-trend revenue realisation.

By Application: Disease Modelling Emerges as Growth Driver

Disease Modelling now contributes an outsized share of incremental in vitro lung model market revenue, riding a 19.40% CAGR wave as pharma recognises that earlier disease-biology fidelity reduces late-stage attrition risks. Legacy dominance of drug discovery & lead optimisation endures due to entrenched plate-based workflows with 44.87% in 2024, yet its share gradually dilutes as precision-medicine consortia direct grants to rare-disease organoid projects. Inhalation Toxicology maintains resilient demand thanks to regulatory compulsion to replace animal studies, particularly in chemicals and consumer-goods testing.

Personalised Medicine & Biomarker Discovery sits at the frontier, leveraging iPSC lung organoids from genetically profiled donors to stratify trial cohorts and pinpoint predictive signatures. Integrating machine-vision analytics with phenotypic screens enables millisecond-scale detection of subtle endpoint shifts, unlocking high-content biomarkers that feed AI-driven target discovery pipelines. Consequently, industry partnerships with data-science vendors have multiplied, embedding computational discovery deep into chip-based assays.

By End User: Academic Institutions Lead Adoption

Academic & Research Institutes are the fastest-rising customer group, adding 21.85% CAGR as public funding prioritises non-animal research infrastructures. Their openness to exploratory protocols means new chip formats secure reference publications that later sway regulatory dossiers. Pharmaceutical & Biotechnology Companies still dominate revenue due to scale with 47.62% market share in 2024, yet procurement policies increasingly stipulate demonstrable regulatory precedents before large-volume roll-outs.

Contract Research Organisations position themselves as translators, purchasing a modest chip fleet to offer fee-based assays that shield smaller pharma from capital expenditures. Government awards such as BARDA’s USD 7.1 million tissue-chip grant to the University of Rochester illustrate how policy nudges accelerate academic-to-industry knowledge transfer. Emerging diagnostic ventures also tap lung organoids to validate companion tests, broadening the In Vitro Lung Model industry customer spectrum.

Geography Analysis

North America leads the in vitro lung model market with 42.05% revenue in 2024, anchored by FDA regulatory clarity and a dense cluster of biotech start-ups that have normalised chip-based assays in IND submissions. Federal grants and venture capital co-fund translational projects, ensuring steady product upgrades and robust domestic demand.

Asia-Pacific, however, posts the steepest 26.32% CAGR, propelled by Chinese and South Korean funding schemes that subsidise academic-corporate consortia building local chip manufacturing lines. CN Bio’s new Seoul-based distribution pact exemplifies how foreign suppliers leverage regional enthusiasm for human-relevant testing to secure first-mover gains.

Europe maintains mid-teens growth underwritten by Horizon grants and a region-wide roadmap to retire animal studies, stimulating recurring orders for OECD-aligned validation studies. The presence of precision-engineering firms in Germany and the Netherlands supports the localisation of microfluidic component supply, reducing lead times for European buyers.

Latin America and the Middle East & Africa remain nascent but opportunity-rich. Local CROs predominantly deploy monolayer or ALI inserts, yet pilot Horizon-linked training programs aim to seed organ-on-chip know-how. Policy convergence around chemical-safety reform could fast-track uptake once infrastructure grants are unlocked.

Competitive Landscape

The in vitro lung model market hosts a diverse mix of pure-play organ-chip developers, legacy cell-culture suppliers, and integrated hardware-consumable platforms. Emulate, CN Bio, and Mimetas headline the dynamic-chip niche, each bundling stretch mechanics, perfusion control, and assay-specific consumables into turnkey packages. Traditional incumbents such as ATCC and Lonza capitalise on proprietary primary-cell lines and GMP-grade media, reinforcing high recurring-revenue streams.

Consolidation trends have started: Merck KGaA purchased HUB Organoids to fold 3D airway constructs into its portfolio, signalling that large life-science conglomerates view organ-on-chip as a strategic adjacency. Suppliers differentiate through data services; CN Bio’s PhysioMimix bioavailability kits integrate PK-PD modelling modules, locking clients into extended subscription renewals.

Competitive intensity is set to climb as Asian manufacturers upscale cost-efficient alternatives, compelling Western leaders to prioritise automation and regulatory data packs over price competition. Firms investing early in GMP-compliant production will likely achieve accelerated market penetration once clinical researchers demand chips for post-approval safety monitoring.

In Vitro Lung Model Industry Leaders

AlveoliX AG

ATCC Global

Epithelix Sàrl

MatTek Corporation

TissUse GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Nagoya University researchers developed a breakthrough method to generate alveolar epithelial type 2 cells from mouse fibroblasts in 7-10 days without stem cell technology, potentially revolutionizing lung cell production for research applications and reducing dependence on primary cell sources.

- June 2025: CN Bio introduced cross-species DILI services to enhance in vitro to in vivo extrapolation during preclinical drug development, expanding their PhysioMimix platform capabilities to include comparative toxicity studies between human and animal models.

- May 2025: CN Bio expanded access to organ-on-chip solutions for Asia-Pacific customers through a distributor agreement with SCINCO in South Korea, capitalizing on the region's biotechnology sector growth and regulatory shifts toward human-relevant testing methods.

- April 2025: Emulate applauded the FDA's roadmap to reduce animal testing and embrace organ-chip technologies, positioning the company to benefit from regulatory shifts toward alternative testing methods in pharmaceutical development.

Global In Vitro Lung Model Market Report Scope

As per the scope of the report, in vitro lung models are defined as cell models that represent normal or diseased lung physiology. These cells when constructed in a monolayer on a Petri plate are called 2D in vitro models. 3D models have a 3-dimensional architecture and use supports and scaffolds to maintain their structure. The in vitro lung model market is segmented by Type (2D Cell Models, 3D Cell Models), Application (Drug Screening, Toxicology, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| 2D Static Monolayer Models |

| Air-Liquid Interface (ALI) Transwell Models |

| 3D Cell Aggregates & Spheroids |

| Organ-on-Chip Microfluidic Models |

| 3D Bioprinted Lung Tissues |

| Drug Discovery & Lead Optimisation |

| Inhalation Toxicology & Safety Assessment |

| Disease Modelling |

| Personalised Medicine & Biomarker Discovery |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organisations |

| Academic & Research Institutes |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Model Type | 2D Static Monolayer Models | |

| Air-Liquid Interface (ALI) Transwell Models | ||

| 3D Cell Aggregates & Spheroids | ||

| Organ-on-Chip Microfluidic Models | ||

| 3D Bioprinted Lung Tissues | ||

| By Application | Drug Discovery & Lead Optimisation | |

| Inhalation Toxicology & Safety Assessment | ||

| Disease Modelling | ||

| Personalised Medicine & Biomarker Discovery | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Research Organisations | ||

| Academic & Research Institutes | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the in vitro lung model market in 2025?

It is valued at USD 424.19 million and is projected to grow to USD 928.34 million by 2030 at a 16.96% CAGR.

Which model type is growing fastest?

Organ-on-Chip microfluidic models are advancing at an 18.05% CAGR due to their ability to replicate breathing mechanics and fluid shear.

Why is Asia-Pacific the most attractive growth region?

Government-funded biotechnology programs, regulatory openness to human-relevant assays, and local manufacturing capacity underpin a 26.32% regional CAGR.

How are academic institutes influencing market adoption?

Universities secure public grants, publish validation data, and train the next generation of researchers, resulting in a 21.85% CAGR for the academic end-user segment.

What remains the key barrier to broader commercial uptake?

The absence of OECD-standardized lung-specific validation protocols increases regulatory uncertainty, slowing large-scale pharmaceutical adoption.

Which companies currently lead the competitive landscape?

Emulate, CN Bio, and Mimetas dominate the organ-on-chip niche, while ATCC and Lonza remain strong in primary-cell supply and basic culture systems.

Page last updated on: