Mice Model Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

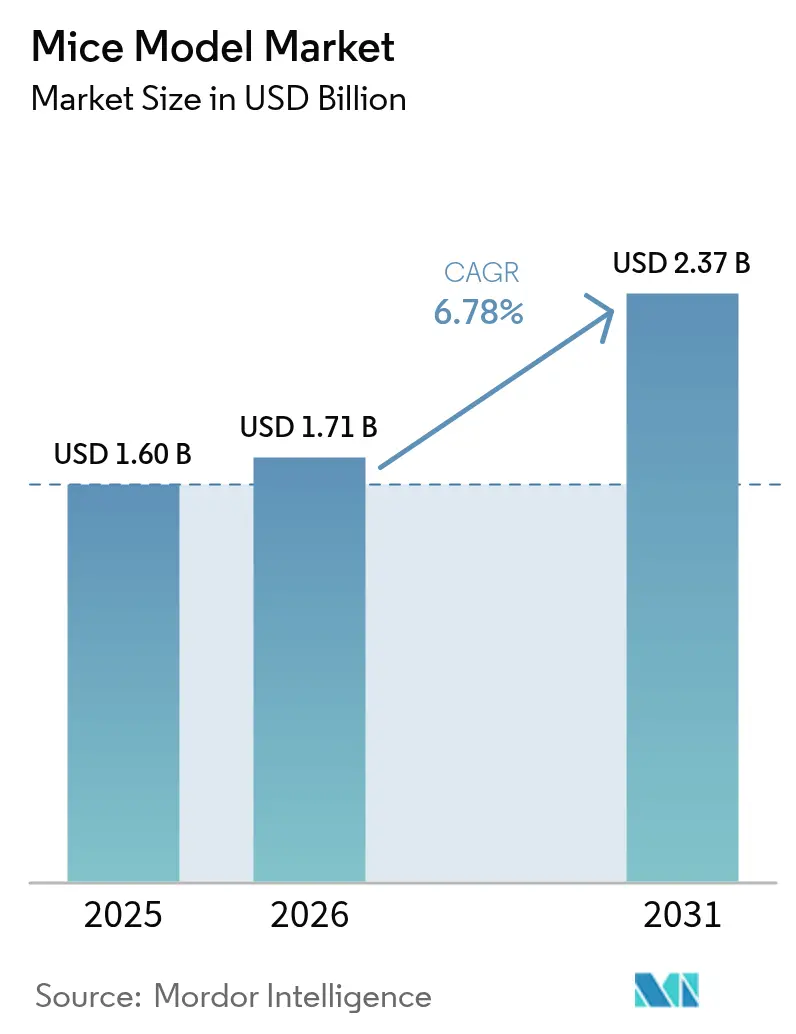

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.37 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

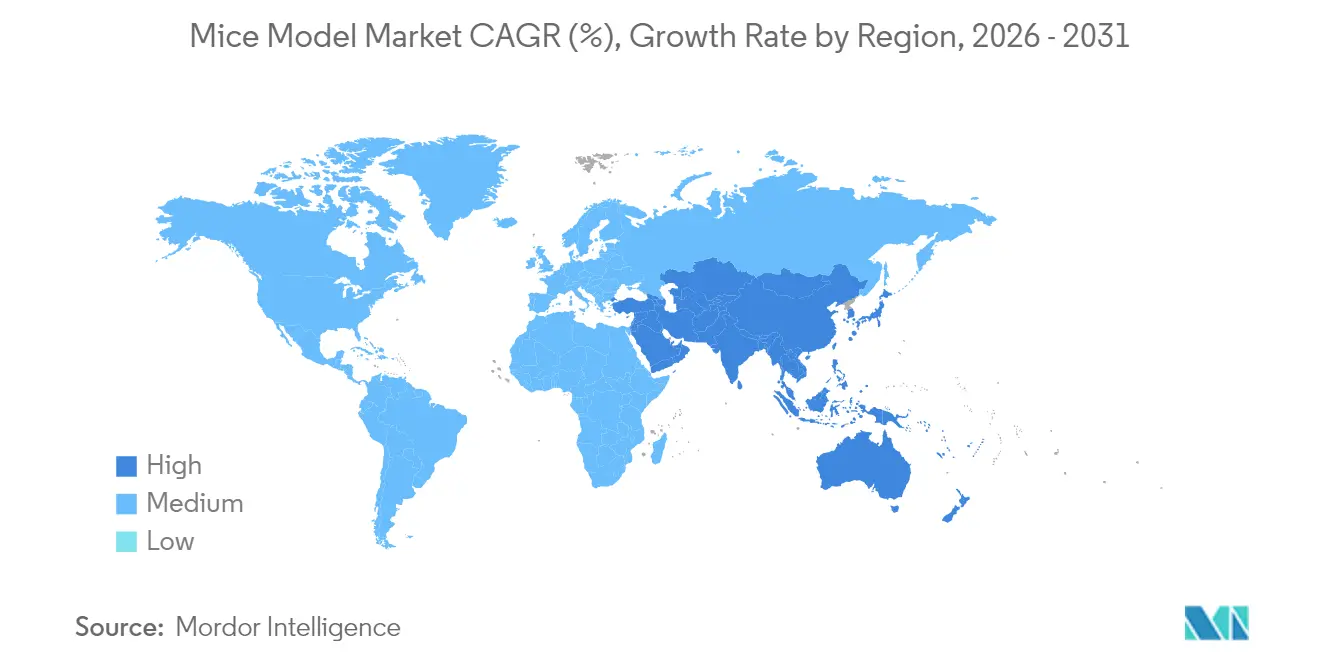

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mice Model Market Analysis by Mordor Intelligence

Mice model market size in 2026 is estimated at USD 1.71 billion, growing from 2025 value of USD 1.60 billion with 2031 projections showing USD 2.37 billion, growing at 6.78% CAGR over 2026-2031. Steady demand stems from oncology, immunology, and rare-disease pipelines that depend on genetically engineered strains with greater translational validity. CRISPR/Cas9 maintains the largest technology footprint and is simultaneously the fastest-growing method, compressing model-generation timelines and lowering costs. North America retains leadership thanks to concentrated R&D funding and deep pharmaceutical activity, yet Asia-Pacific is closing the gap as China, Japan, and South Korea pour capital into local breeding infrastructure. Contract research organizations (CROs) are capturing an expanding share of outsourced studies, while humanized immune system and patient-derived xenograft (PDX) libraries rise in importance for immuno-oncology validation. Regulatory momentum toward alternative methods introduces headwinds but also pushes model developers to deliver higher-fidelity, ethically refined lines.

Key Report Takeaways

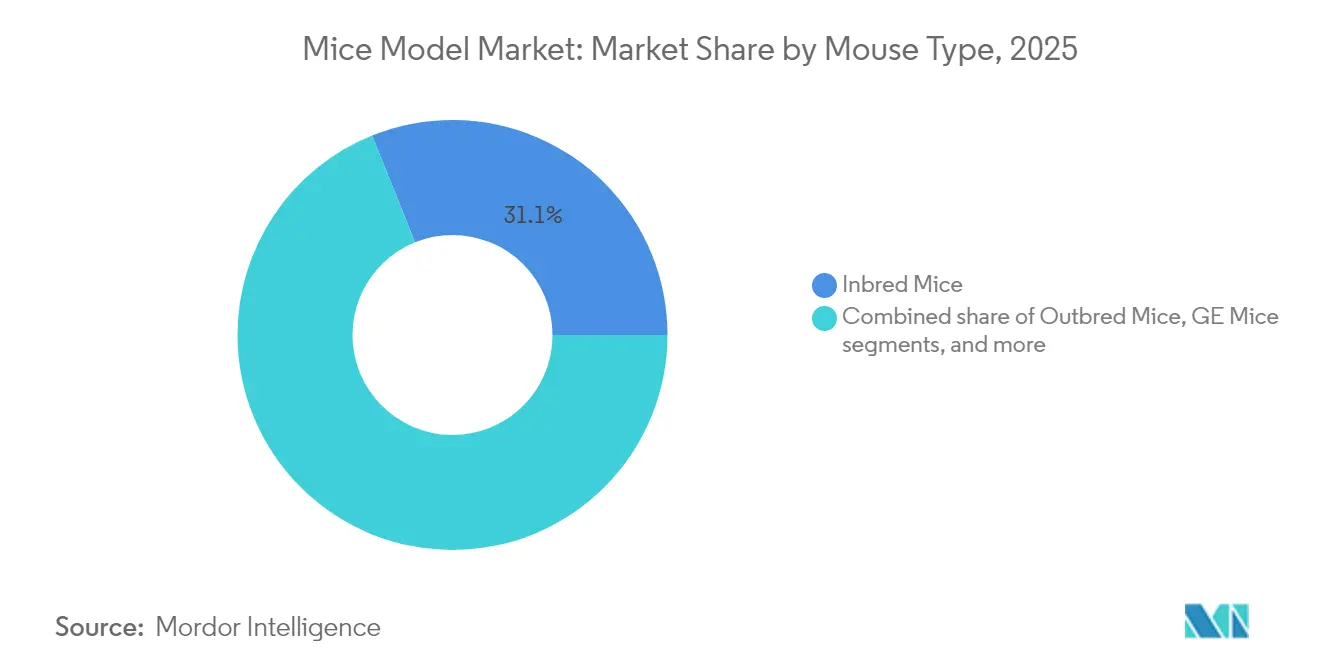

- By mouse type, inbred mice led with 31.10% of the mice model market share in 2025; genetically engineered mice are projected to expand at a 9.84% CAGR through 2031.

- By service, breeding services commanded 44.10% of the mice model market in 2025, whereas genetic testing is set to grow the fastest at 9.05% CAGR to 2031.

- By technology, CRISPR/Cas9 held 37.80% of the mice model market size in 2025 and will advance at a 13.60% CAGR over the forecast period.

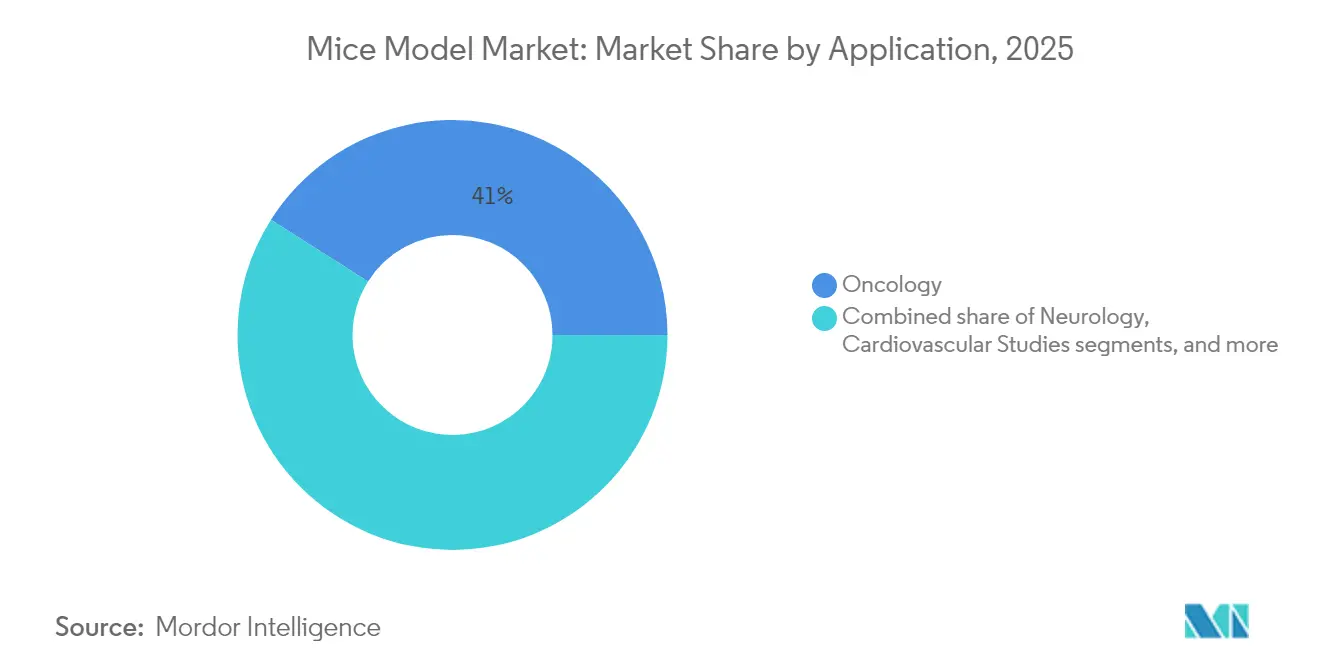

- By application, oncology accounted for 41.00% of the mice model market in 2025, while infectious-disease studies are poised for an 10.88% CAGR between 2026-2031.

- By end-user, pharmaceutical and biopharmaceutical firms controlled 48.00% of the mice model market in 2025; CROs post the highest growth outlook at 8.90% CAGR.

- Geographically, North America retained 41.50% of the global mice model market in 2025; Asia-Pacific logs the fastest regional CAGR at 8.12% toward 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Mice Model Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Humanized Mice for Immuno-Oncology Drug Validation | +1.7% | North America, Europe, China | Medium term (2-4 years) |

| Rapid Adoption of CRISPR-Edited Knock-In Models for Target Gene Function Studies | +1.4% | Global, with concentration in US, Europe, Japan | Short term (≤ 2 years) |

| Expansion of Contract Breeding Services Supporting Big-Pharma Pipeline Surge | +1.2% | North America, Europe, emerging in APAC | Medium term (2-4 years) |

| Accelerating Demand for Patient-Derived Xenograft (PDX) Libraries among CROs | +1.0% | North America, Europe, China, Japan | Medium term (2-4 years) |

| High-Throughput In-Vivo Screening Preference in Pre-Clinical Toxicology | +0.8% | Global, with early adoption in US and Europe | Short term (≤ 2 years) |

| Government-Funded Consortia Promoting Rare-Disease Mouse Model Repositories | +0.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Humanized mice revolutionizing immuno-oncology validation

Humanized models, generated by engrafting human immune components into immunodeficient strains, are rapidly displacing traditional xenografts. These mice replicate checkpoint-inhibitor and CAR-T responses more faithfully, trimming late-stage attrition. BioDuro reports a 70% uplift in predictive accuracy for immunotherapies, broadening use beyond efficacy studies to safety and biomarker discovery. Harvard scientists recently identified novel PD-1 resistance mechanisms in such models, highlighting their analytical depth. Pharmaceutical sponsors therefore allocate larger budgets to humanized cohorts, boosting recurring demand across North America, Europe, and China.

CRISPR technology accelerating genetic model development

CRISPR/Cas9 has moved mouse-line creation from multiyear projects to multi-month undertakings. Yale’s 2025 Cas12a platform[1]Yale News, “New CRISPR Tool Enables More Seamless Gene Editing,” news.yale.edu enables multiplexed edits in one generation, while Taconic shows 40% lower production costs relative to embryonic stem-cell methods. More than 60% of custom orders now specify CRISPR designs, pushing suppliers to scale automated microinjection and electroporation. As complexity rises, multiplexed edits become essential for polygenic disorders, reinforcing the technology’s growth path.

Contract breeding services supporting big-pharma pipeline surge

Pharma sponsors are increasingly trimming fixed infrastructure costs and outsourcing colony expansion and quality control. Boston Children’s Mouse Gene Manipulation Core illustrates integrated offerings spanning CRISPR knock-ins, embryo microinjection, quarantine, and cryopreservation.[2]Boston Children’s Hospital, “Research Cores,” Boston Children’s Hospital, research.childrenshospital.org Outsourcing delivers 30-40% operational savings and accelerates study starts by avoiding facility build-outs. Vendors invest in high-throughput genetic monitoring to curb drift, aligning with reproducibility mandates. As drug pipelines swell, mid-tier CROs in North America and Europe are re-tooling to match demand, while APAC entrants add price flexibility.

Patient-derived xenograft libraries becoming essential for oncology drug development

PDX models retain patient tumor heterogeneity, enabling more accurate efficacy screens. Crown Bioscience’s collection now tops 3,000 models, and the XENTURION biobank[3]Franco Bertotti, “XENTURION: Matched PDX and Tumoroid Resource for Metastatic Colorectal Cancer,” Nature Communications, nature.com integrates 128 colorectal PDXs with omics annotations, sharpening patient-stratification insights. Sponsors attribute 15-20% fewer Phase II/III failures to PDX-guided selection, translating into multi-billion-dollar R&D savings. CROs thus scale dedicated PDX facilities and combine them with tumoroid screening, especially for immuno-oncology combinations.

Restraints Impact Analysis of Mice Model Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in In-Silico Organ-on-Chip Alternatives Reducing Animal Use | -1.0% | North America, Europe, emerging in APAC | Medium term (2-4 years) |

| Stringent 3Rs Compliance and Ethics Review Delays | -0.8% | Global, with strongest impact in Europe | Short term (≤ 2 years) |

| Supply Disruptions from Pathogen-Free Colony Maintenance Costs | -0.7% | Global | Short term (≤ 2 years) |

| Rising Public Pressure Fueling Investor ESG Restrictions | -0.5% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advances in in-silico and organ-on-chip alternatives reducing animal use

Artificial intelligence modeling and microfluidic organ chips are winning regulatory encouragement, with the FDA outlining a roadmap to phase out certain monoclonal antibody assays.[4]U.S. Food and Drug Administration, “Roadmap to Reducing Animal Testing in Preclinical Safety Studies,” fda.gov These platforms offer rapid toxicity data and ethical advantages, drawing venture backing across North America and Europe. Yet whole-organism complexity remains hard to mimic, leading investigators to note that systemic immune and metabolic interactions still require murine confirmation. Consequently, alternative tools are viewed as complementary rather than outright replacements in the medium term.

Stringent 3Rs compliance creating regulatory hurdles

Global ethics committees now enforce tighter Replacement, Reduction, and Refinement standards. Europe has added additional documentary layers under the updated Directive 2010/63/EU, while FDA Modernization Act 2.0 permits non-animal data packages in some instances. Reviews prolong study timelines and raise administrative costs, especially for smaller labs with limited regulatory staff. Major academic centers respond with training programs and digital tracking tools, yet delays continue to weigh on project starts and may temper short-term growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Mice Model Market Segment Analysis

By Mouse Type:

Genetically engineered mice drive precision medicineGenetically uniform inbred strains captured 31.10% of the mice model market share in 2025, reinforcing their role in assay reproducibility. Nevertheless, genetically engineered mice are advancing at a 9.84% CAGR as CRISPR multiplexing simplifies complex allele combinations. The mice model market size tied to these engineered lines is forecast to add roughly USD 440 million between 2026 and 2031, propelled by oncology and neurodegenerative studies demanding polygenic constructs. Researchers value rapid knockout, knock-in, and conditional systems that clarify gene function in real time. Outbred stocks remain relevant for population-diversity modeling, while hybrid/congenic lines serve immunology niches where MHC compatibility is paramount. Vendors increasingly bundle genotyping, phenotyping, and colony management to ensure scientific rigor and to protect intellectual property tied to bespoke strains. Collaborative consortia expand global repositories, democratizing access and reducing duplication of effort across laboratories.

In the long term, multigenic humanized platforms are expected to overtake single-gene mutants as sponsors demand closer human translatability. Partnerships between academic genome centers and commercial breeders have accelerated line validation, helping dodge earlier bottlenecks in embryo availability. Advanced cryopreservation reduces drift, enabling labs to store critical alleles without active breeding. Against this backdrop, engineered murine models become indispensable for mechanism-focused precision-medicine pipelines, supporting therapeutic modalities from gene editing to antibody-drug conjugates.

By Service:

Genetic testing emerges as growth engineBreeding services held 44.10% of the mice model market in 2025, underscoring the foundational need for reliable colony expansion. Yet genetic testing rises fastest, growing at 9.05% CAGR as sponsors require molecular confirmation of each edit before committing to GLP toxicology studies. The mice model market size associated with testing should approach USD 232 million by 2031, benefiting specialized laboratories with next-generation sequencing platforms. Cryopreservation services add resilience, preserving high-value germplasm and offsetting pathogen risks. Rederivation and quarantine remain compliance staples, especially after high-profile contamination events prompted stricter vivarium audits.

Service providers differentiate by offering integrated dashboards that track breeding metrics, genotype results, and health status in real time. Leading companies deploy barcoding and AI-assisted image recognition to flag phenotypic drift early. Pharmaceutical clients value this transparency, often embedding quality clauses into master service agreements. Consequently, the service ecosystem migrates from transactional tasks toward data-rich, consultative engagements that weave genetic insight into every stage of model utilization.

By Technology:

CRISPR/Cas9 revolutionizes model generationCRISPR/Cas9 commanded 37.80% of the mice model market in 2025 and is expected to accelerate at 13.60% CAGR. Its dominance stems from unmatched editing efficiency, validated by Yale’s Cas12a system that executes multiplex edits in a single generation. Embryonic stem-cell injection continues to serve large-fragment integrations critical for reporter constructs, while nuclear transfer offers niche cloning capabilities despite technical overhead. Automated microinjection systems now achieve 94% pipette insertion accuracy, trimming variability and labor costs.

Looking ahead, CRISPR-VIM—virus-like particle delivery—reduces embryo handling and could broaden access for labs lacking advanced micromanipulation gear. Vendors leverage cloud-based design pipelines that calculate guide-RNA off-target scores, shortening quote-to-construct cycles. As intellectual-property disputes settle, cross-licensing paves the way for standardized protocols, ensuring reproducibility across continents and scaling the overall mice model market.

By Application:

Infectious-disease research accelerates post-pandemicOncology retained 41.00% revenue in 2025, reflecting the sector’s dependence on PDX and humanized models to forecast checkpoint-inhibitor efficacy. Yet infectious-disease research posts the fastest 10.88% CAGR, fueled by pandemic preparedness funding and antimicrobial-resistance programs. The mice model market size for infectious uses is projected to surpass USD 418 million by 2031 as sponsors evaluate next-generation antivirals and pathogen-specific vaccines.

Immunology studies rely on refined models that replicate cytokine networks, while neuroscience investigators integrate longitudinal imaging to map degeneration pathways. Cardiovascular and metabolic fields benefit from telemetry implants and diet-induced disease settings that approximate clinical heterogeneity. This widening application spectrum underscores the mice model market’s adaptability and importance to diverse therapeutic portfolios.

By End-User:

CROs gain ground through specialized expertisePharmaceutical and biopharmaceutical companies owned 48.00% of the mice model market in 2025, channeling models into target validation and IND-enabling studies. CROs, however, deliver the fastest growth at 8.90% CAGR, riding demand for turnkey efficacy and safety packages. Some CROs now operate colony capacities exceeding midsize pharma firms, offering economies of scale that anchor multi-year framework deals. Academic institutes remain key innovators, housing transgenic core facilities that pilot novel constructs before commercial scale-out occurs.

Government programs, such as the NIH PAR-25-327 grant, funnel resources into ultra-rare disease line development, often transferring validated strains to public repositories for broader access. Non-profits like the Michael J. Fox Foundation underwrite Parkinson’s disease lines, ensuring rapid dissemination to investigators. Collectively, these user segments reinforce a collaborative ecosystem that propels the mice model market forward.

Geography Analysis

North America Mice Model Market

North America held 41.50% of the mice model market in 2025, buoyed by National Institutes of Health grants that prioritize gene-based therapies and translational models. The NIH PAR-25-327 mechanism specifically funds ultra-rare neurologic disorder research using sophisticated murine systems. Regional suppliers deploy CRISPR high-throughput cores and pathogen-free facilities, cementing first-to-market advantages. Regulatory shifts, such as the FDA plan to phase out certain animal tests, pressure legacy models yet simultaneously spur demand for advanced lines with heightened predictive power.

EMEA and South America Mice Model Market

Asia-Pacific registers the highest 8.12% CAGR, thanks to aggressive national investments. China’s National Resource Center for Mutant Mice produced knockouts for 10,881 genes by mid-2024, creating a domestic pipeline that feeds CRO expansion. Japan refines quality protocols for PDX adoption, and South Korea channels Smart Farm funding into germ-free barrier facilities. Multinational sponsors partner with local breeders like GemPharmatech, which opened a San Diego node to bridge US-APAC demand.

Europe sustains a 5.73% CAGR underpinned by collaborative funding and strong ethics governance. The European Medicines Agency’s Regulatory Science to 2025 agenda encourages innovative non-clinical models while upholding the 3Rs principle. Middle East and Africa and South America together represent emerging corridors with CAGRs of 7.46% and 6.95% respectively. Gulf nations fund translational centers focused on metabolic disorders prevalent in local populations, while Brazilian institutes advance tropical-disease models that align with regional epidemiology. Global pharma’s clinical footprint in these areas boosts demand for standardized murine assays, ensuring harmonized data across multicenter trials.

Competitive Landscape

The mice model market shows moderate concentration: the top five vendors—Charles River Laboratories, Taconic Biosciences, The Jackson Laboratory, GenOway, and Inotiv, Inc.—control a significant portion of the market size. These leaders integrate breeding, genetic engineering, health monitoring, and global logistics. Charles River enhances differentiation through in-house CRISPR services and immuno-oncology study suites. Taconic leverages license-free strains and rapid-access CRISPR editing to appeal to fast-moving biotech clients, while The Jackson Laboratory partners with disease foundations to distribute novel lines efficiently.

Strategic alliances intensify. Biocytogen’s RenLite antibody platform secured a licensing agreement with Janssen, pairing proprietary humanized mice with downstream therapeutic discovery. Meanwhile, academic pipelines feed commercial catalogs; Yale transfers Cas12a-engineered strains under non-exclusive terms, broadening market access.

Niche specialists grow around PDX and organ-specific humanized models, often capturing business from small biotech firms seeking tailored translational readouts. Competitive tension also arises from alternative-method developers in the organ-on-chip space; however, most sponsors still couple these platforms with murine validation, sustaining core demand. Pricing remains stable for standard lines, yet premium humanized strains command mark-ups exceeding 150% due to complex licensing and breeding costs.

Mice Model Industry Leaders

Charles River Laboratories International Inc.

GenOway

Inotiv, Inc.

Taconic Biosciences, Inc.

The Jackson Laboratory

- *Disclaimer: Major Players sorted in no particular order

Mice Model Market Companies Covered in this Report

- Aragen Bioscience

- Biocytogen Pharma

- Biomere

- Charles River

- CLEA Japan

- Crown BioScience Intl.

- Cyagen Biosciences.

- GemPharmatech

- GenOway

- Harbour BioMed

- Ingenious Targeting Laboratory

- Innovative Research

- Inotiv, Inc.

- Janvier Labs

- Melior Inc.

- Ozgene

- PolyGene AG

- Taconic Biosciences

- The Jackson Laboratory

- Trans Genic

Recent Industry Developments in Mice Model Market

- April 2025: GemPharmatech expanded its U.S. operations with a new San Diego facility offering lab rental, breeding, and in vivo preclinical studies, giving clients access to an extensive library of genetically engineered lines.

- March 2025: Yale University researchers developed new CRISPR-Cas12a mouse lines enabling simultaneous assessment of multiple genetic changes related to various diseases, significantly enhancing research capabilities in immunological responses and genetic disorders.

- March 2025: A Nature Communications paper introduced CRISPR-VLP-induced targeted mutagenesis, a virus-like particle method that simplifies generation of engineered mouse models.

- February 2025: The Chan Zuckerberg Initiative released the Rare As One Network Cycle 1 Impact Report, highlighting patient-led efforts to build animal-model infrastructure for rare-disease research.

Mice Model Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the mice model market as global revenue from the sale or licensed use of live, laboratory-bred mice together with custom genetic-engineering services that create disease, transgenic, knock-in, knock-out, and humanized strains for pre-clinical discovery, safety, and validation work across pharmaceutical, biotechnology, CRO, and academic settings. Because mice share more than ninety-nine percent of their genome with humans, Mordor Intelligence treats them as the principal small-animal proxy for human pathophysiology in drug development.

Scope Exclusions: Rat or other rodent models, in-vitro organoids, in-silico simulations, and fee-for-service testing that does not bundle mice procurement are deliberately excluded.

Segments Covered in This Report

- By Mouse Type

- Inbred Mice

- Outbred Mice

- Genetically Engineered Mice

- Hybrid/Congenic Mice

- By Service

- Breeding

- Cryopreservation

- Rederivation & Quarantine

- Genetic Testing

- Other Services

- By Technology

- CRISPR/Cas9

- Embryonic Stem Cell Injection

- Nuclear Transfer

- Microinjection

- Other Technologies

- By Application

- Oncology

- Immunology & Inflammation

- Neurology

- Cardiovascular Studies

- Metabolic Diseases

- Infectious Diseases

- Other Applications

- By End-User

- Pharmaceutical & Biopharmaceutical Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Dozens of semi-structured interviews with vivarium managers, transgenic-core directors, CRO procurement heads, and university researchers across North America, Europe, and Asia helped us validate demand drivers, average selling prices, breeding-cycle yields, and expected CRISPR adoption shifts.

Desk Research

We first compile open data from tier-one sources such as NIH RePORTER grant files, FDA IND statistics, European Commission laboratory-animal-use reports, OECD trade codes for live laboratory animals, and peer-reviewed PubMed trend analyses. Annual reports and 10-Ks of major breeders, cost curves captured through D&B Hoovers, news flows screened on Dow Jones Factiva, and portals like the American Association for Laboratory Animal Science further anchor supply, price, and regulatory signals. This list is illustrative; many additional references inform data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down production and trade reconstruction estimates the annual pool of research mice, which is then corroborated with selective bottom-up supplier revenue roll-ups and sampled ASP × volume checks. Variables such as active pre-clinical candidate counts, R&D expenditure, share of genetically engineered strains, average litter size, and outsourcing penetration feed the model. Forecasts employ multivariate regression enhanced with exponential smoothing, and scenario ranges are refined through expert consensus before lock-in.

Data Validation & Update Cycle

Outputs undergo variance checks against historical delivery records, currency normalization, and inter-analyst peer review. Reports refresh yearly, with interim updates triggered by regulatory changes or material breeder acquisitions. Before publication, one analyst repeats the validation loop so clients receive the latest view.

How Mordor Intelligence's Mice Model Market Size Compares to Other Published Estimates

Published estimates often diverge because firms choose different scopes, variables, and refresh cadences, which can meaningfully shift totals. Mordor analysts apply a disciplined scope, transparent variable selection, and an annual refresh, giving decision-makers a dependable reference point.

Key gap drivers include competitor inclusion of rat sales, reliance on unvalidated price escalators, and three-year data refresh cycles that inflate or deflate totals relative to our 2025 baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.60 B (2025) | Mordor Intelligence | |

| USD 1.70 B (2025) | Regional Consultancy A | Bundles custom lab service contracts and partial rat models; ASPs held constant since 2019 |

| USD 1.78 B (2025) | Trade Journal B | Applies uniform 10 % price growth and omits in-house colony consumption data |

The comparison shows that when our clearly defined scope and annually refreshed variables are applied, Mordor's figure sits at the balanced center of the available spectrum, giving stakeholders a transparent, repeatable baseline they can confidently build upon.

Key Questions Answered in the Report

Why is CRISPR/Cas9 viewed as a game-changer for mouse model development?

It enables rapid, highly precise gene edits, letting researchers create complex multigene models in months instead of years, which accelerates target-validation cycles in drug discovery.

What makes humanized mice increasingly important for immuno-oncology studies?

These models incorporate human immune components, allowing checkpoint-inhibitor and CAR-T therapies to be tested in a living system that mimics patient immune responses more accurately than traditional xenografts.

How are contract research organizations (CROs) reshaping the mice model landscape?

CROs now bundle breeding, genetic testing, and phenotyping into turnkey packages, giving pharma companies faster project starts and eliminating the need for costly in-house vivarium expansion.

In what way do patient-derived xenograft (PDX) libraries improve oncology drug screening?

PDX models preserve the genetic heterogeneity of original tumors, helping researchers pinpoint biomarker-driven subgroups and reduce late-stage clinical failures tied to poor translational relevance.

What role do rare-disease consortia play in advancing new mouse models?

Government-funded initiatives pool resources to create and share knockout strains for understudied disorders, filling gaps that lack commercial incentives and enabling preclinical testing for ultra-rare conditions.

Why are organ-on-chip and in-silico tools considered both a threat and an opportunity for the mice model market?

They promise ethical, high-throughput alternatives for certain assays, encouraging refinement of animal studies; yet they currently complement rather than fully replace whole-organism models needed for systemic safety and efficacy evaluation.

Page last updated on: