Password Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

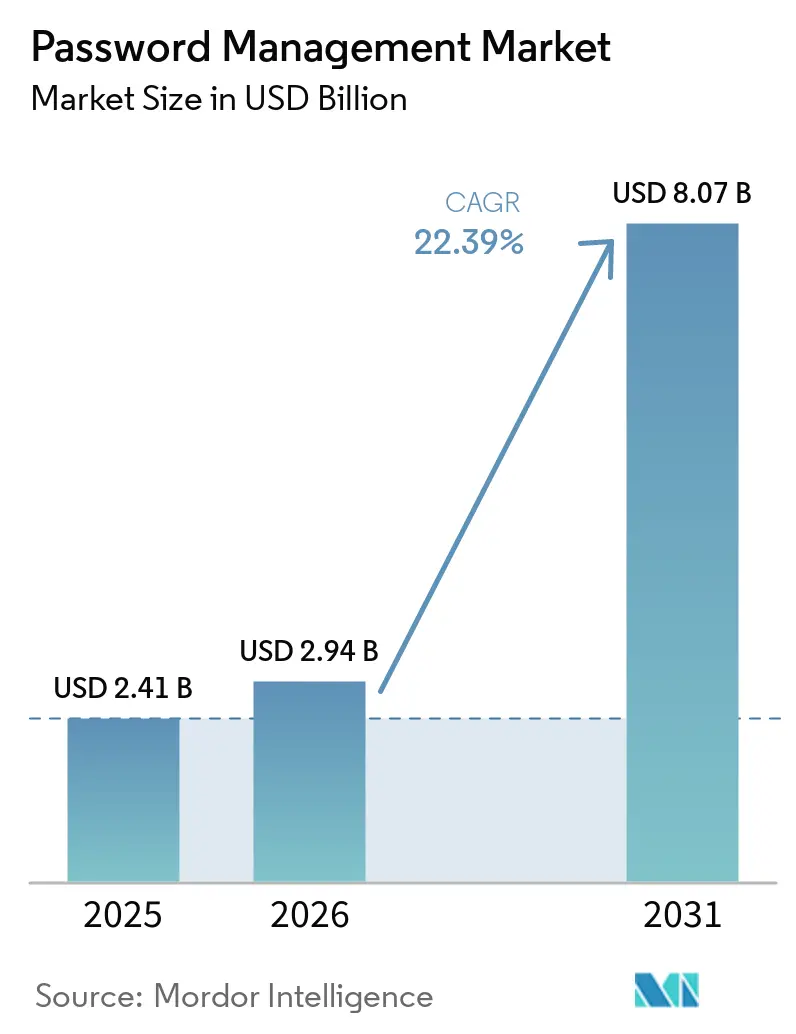

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 8.07 Billion |

| Growth Rate (2026 - 2031) | 22.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Password Management Market Analysis by Mordor Intelligence

The Password Management Market size is projected to expand from USD 2.41 billion in 2025 and USD 2.94 billion in 2026 to USD 8.07 billion by 2031, registering a CAGR of 22.39% between 2026 to 2031. Heightened regulatory scrutiny of privileged access, tighter cyber-insurance underwriting, and the need to tame credential sprawl across thousands of cloud applications are pushing organizations to adopt enterprise-grade password vaults at an accelerated pace. Cloud delivery remains dominant, yet hybrid deployment models are steadily gaining favor as data-residency laws in Europe and the Middle East require sensitive secrets to stay on-premises. Mobile-first authentication, led by biometric-enabled vaults, is growing fastest as bring-your-own-device programs expand. Meanwhile, the rise of API-driven development is blurring the boundary between password managers and full-featured secrets-management platforms.

Key Report Takeaways

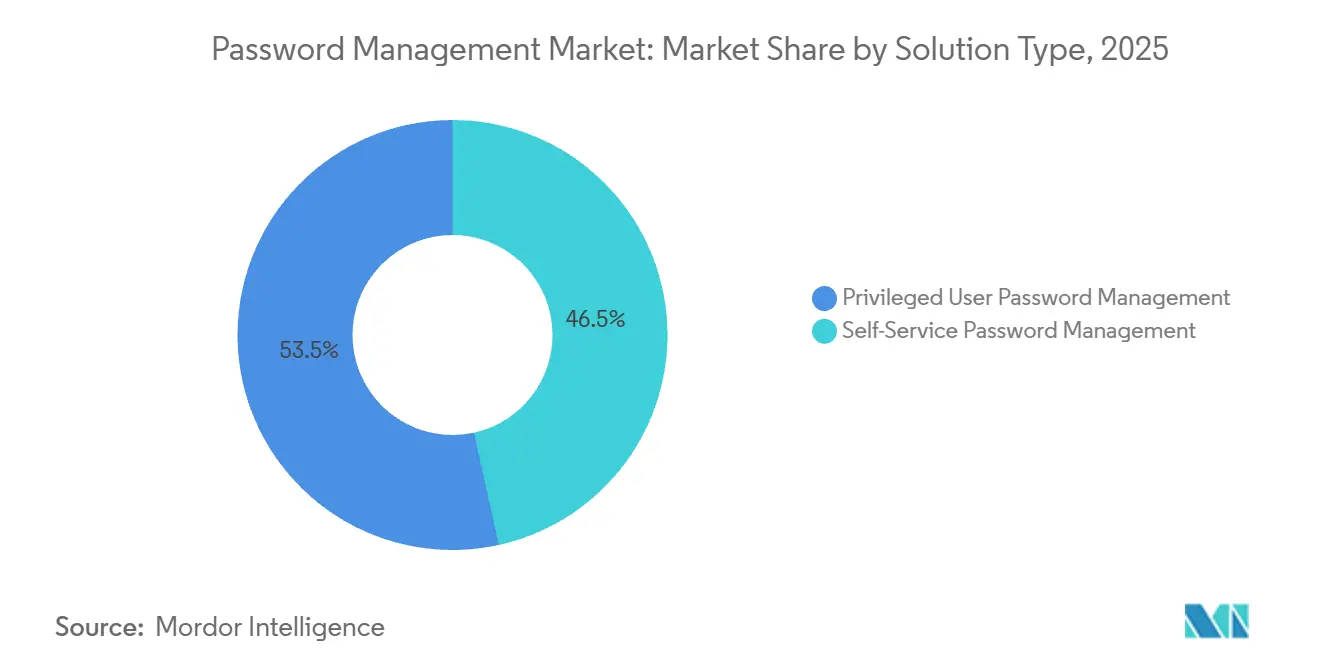

- By solution type, self-service tools held 46.5% of the password management market share in 2025, while privileged vaults are forecast to advance at a 23.8% CAGR through 2031.

- By access technology, desktops and laptops accounted for 38.1% of the password management market size in 2025; however, mobile solutions are predicted to expand at a 24.1% CAGR through 2031.

- By deployment mode, cloud-hosted offerings secured a 64.4% share in 2025, whereas hybrid models are poised for a 23.9% CAGR growth out to 2031.

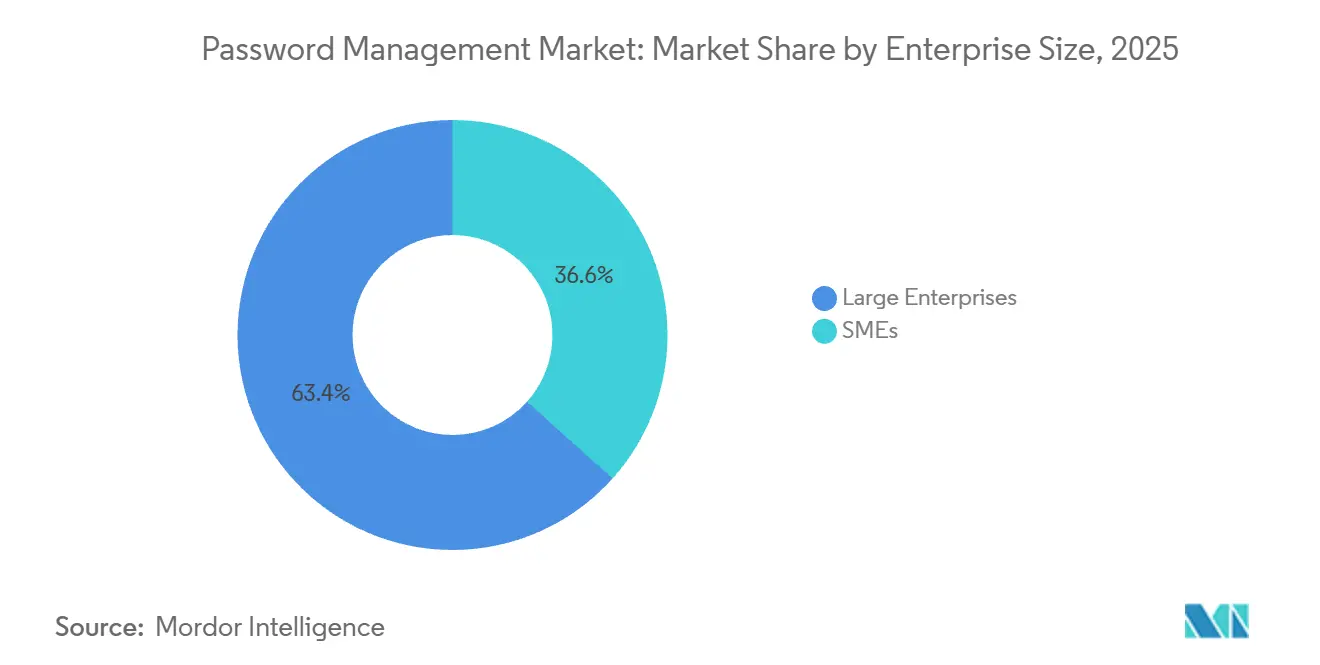

- By enterprise size, large organizations commanded 63.4% of 2025 spending; however, small and medium enterprises are set to grow the quickest at a 24.3% CAGR through 2031.

- By end-user vertical, banking, financial services, and insurance accounted for 29.1% of 2025 revenue, while healthcare and life sciences are projected to achieve a 25.9% CAGR through 2031.

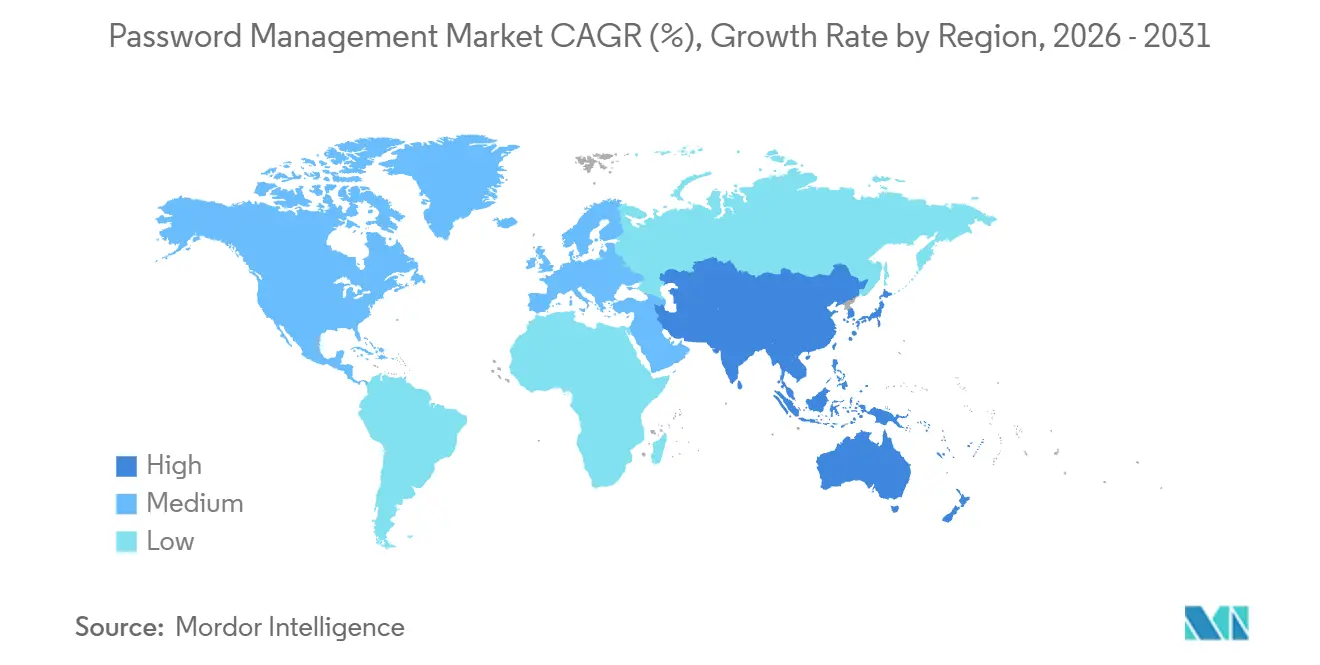

- By geography, North America held 38.93% of global revenues in 2025; the Asia Pacific is the fastest riser, with a 24.13% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Password Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-trust programs accelerating privileged password vault deployments in North American BFSI | +4.2% | North America, spillover to Europe and Asia Pacific hubs | Medium term (2-4 years) |

| EU GDPR and NIS-2 mandates triggering enterprise-wide password audits and upgrades | +3.8% | Europe, global subsidiaries | Short term (≤ 2 years) |

| Surge in SaaS identity sprawl creating demand for cross-platform vaults in Asia Pacific mid-market | +3.5% | Asia Pacific core, emerging Latin America and Middle East | Medium term (2-4 years) |

| Workforce mobility and BYOD driving mobile-first password managers in Nordics | +2.9% | Nordic countries, spreading to Western Europe and North America | Short term (≤ 2 years) |

| Cyber-insurance underwriting requiring automated credential hygiene proof in United States | +3.1% | United States, early Canada and United Kingdom | Short term (≤ 2 years) |

| API-first integration needs for RPA and DevOps pipelines fueling secrets-management adoption | +4.4% | Global technology hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Zero-Trust Programs Accelerating Privileged Password Vault Deployments in North American BFSI

Regulators linked credential misuse to unauthorized trading and loan-fraud incidents in 2024 and 2025, prompting United States and Canadian banks to embed privileged vaults into zero-trust architectures. The Office of the Comptroller of the Currency required institutions with assets above USD 10 billion to provide just-in-time access and session recording for every administrative account.[1]Office of Public Affairs, “OCC Bulletin 2025-15,” U.S. Department of the Treasury, treasury.gov CyberArk noted that 68% of its first-half 2025 bookings came from financial-services upgrades to dynamic privileged access management vaults that rotate passwords every 90 minutes. Mid-tier banks lacking appliance budgets turned to cloud-delivered privileged access, a capability rapidly expanded by Delinea in 2025. Similar mandates are emerging in Europe and the Asia Pacific, indicating global spillover.

EU GDPR and NIS-2 Mandates Triggering Enterprise-Wide Password Audits and Upgrades

The Network and Information Security Directive 2 entered full force in October 2024 and, together with GDPR, compelled European firms to inventory every credential across subsidiaries and supply-chain partners. Fines linked to weak password hygiene totaled EUR 1.2 billion (USD 1.3 billion) over 2024-2025 and elevated password vault roll-outs above other security projects. Germany, France and the Netherlands spearheaded hybrid architectures that keep privileged passwords on-premises while routing employee credentials to managed cloud vaults. Non-EU corporations serving European customers must also comply, broadening global demand.

Surge in SaaS Identity Sprawl Creating Demand for Cross-Platform Vaults in Asia Pacific Mid-Market

Mid-market enterprises in India, Southeast Asia and Australia averaged 47 SaaS applications each in 2025, up from 32 in 2023. API keys, shared logins and service accounts proliferated outside single sign-on coverage, leaving fertile ground for phishing and credential-stuffing attacks. Vendors such as 1Password and Dashlane expanded regional teams to deliver vaults that synchronize across Windows, macOS, iOS, Android and Linux without privileged-access-management complexity. Remote work further catalyzed adoption as personal devices joined corporate networks.

API-First Integration Needs for RPA and DevOps Pipelines Fueling Secrets-Management Adoption

Robotic process automation and DevOps pipelines multiplied machine identities that traditional password stores cannot govern. Platforms such as HashiCorp Vault and CyberArk Conjur stepped in with dynamic credential generation and time-scoped tokens. GitHub revealed that 23% of public repositories still contained hard-coded secrets in 2025, underscoring exposure. Okta’s 2024 purchase of a secrets-management startup highlighted convergence between identity and DevOps workflows. As microservices multiply, secrets-management capabilities have become essential to zero-trust strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Profile Breaches (e.g., LastPass 2022) Undermining User Trust, Especially in DACH Region | -2.1% | Germany, Austria, Switzerland, with reputational spillover to broader European market | Short term (≤ 2 years) |

| Rising Adoption of Passkeys / FIDO2 Reducing Future TAM in Consumer Segment | -1.8% | Global, with early adoption in North America and Western Europe | Long term (≥ 4 years) |

| Regulatory Data-Residency Rules Complicating Cloud Vault Roll-Outs in Middle East | -1.3% | Middle East core, with similar constraints emerging in Russia, China and select African markets | Medium term (2-4 years) |

| Persistent Shadow-IT Password Stores Inflating Migration Costs for Large Enterprises | -1.5% | Global, with concentration in large enterprises across North America, Europe and Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High-Profile Breaches Undermining User Trust, Especially in DACH Region

The 2022 LastPass breach revealed encrypted vault data and unencrypted metadata, triggering a lingering trust deficit across Germany, Austria and Switzerland. Many organizations pivoted to on-premises or open-source options such as Bitwarden, citing transparency advantages over proprietary encryption. Germany’s Federal Office for Information Security urged independent vendor assessments in 2024. Until vendors embrace standardized encryption and continuous third-party audits, caution in the DACH region will restrain cloud adoption.

Rising Adoption of Passkeys and FIDO2 Reducing Future TAM in Consumer Segment

Google, Apple, and Microsoft enabled passkeys across their ecosystems in 2025, placing public-key cryptography and biometrics at the center of consumer authentication. The FIDO Alliance expects to have 1.2 billion passkey-ready devices by mid-2025.[2]Research Team, “2025 Device Landscape,” FIDO Alliance, fidoalliance.org As consumers shift to passwordless login, demand for self-service password tools could taper. Enterprises, however, still rely on legacy applications that cannot consume FIDO2 standards, ensuring the relevance of password vaults through at least 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Privileged Vaults Outpace Self-Service Growth

Privileged password tools represented the fastest-growing solution, advancing at a 23.8% CAGR through 2031, while self-service applications, although larger today, face growth deceleration. Banking, healthcare, and public-sector mandates now require credential rotation, access logging, and separation of duties, capabilities embedded only in privileged platforms. Cyber-insurance clauses reinforce the shift by denying favorable premiums to firms that rely on static spreadsheets.

Self-service tools held a 46.5% market share in 2025. Self-service vendors continue to enhance enterprise features, yet remain susceptible to the consumer shift toward passkeys. Hybrid work introduces new endpoints and expands the password management market, but the security premium associated with administrative accounts ensures that privileged vaults continue to drive growth.

By Access Technology: Mobile Devices Lead Growth

Mobile solutions hold the strongest tailwind, forecast to rise at 24.1% to 2031, whereas desk-based clients maintain 38.1% of 2025 spending. The Nordic model has demonstrated that biometric-enabled vaults on smartphones can improve both user experience and compliance simultaneously. iCloud Keychain and Windows Hello now incorporate passkey storage, intensifying competitive pressure on independent vendors and making differentiated cross-platform support mandatory.

Growth in the password management market stems from remote work and 5G connectivity that allow real-time credential sync without latency. Desktops and laptops remain indispensable for developers and analysts, ensuring multipronged access strategies prevail.

By Deployment Mode: Hybrid Architectures Gain Momentum

Cloud offerings held a 64.4% share in 2025, thanks to lower maintenance costs; however, hybrid models are on track for a 23.9% CAGR amid European and Middle Eastern data-sovereignty mandates. Enterprises increasingly store privileged passwords locally while directing workforce credentials to managed SaaS vaults. Leading vendors now package split-custody architectures that lower operational friction without breaching national regulations.

Small firms with lean IT teams still favor pure SaaS delivery, but stringent sectoral rules in banking, defense, and government signal durable demand for hybrid variants, keeping the password management market diversified.

By Enterprise Size: SMEs Drive Fastest Expansion

Large organizations remain the spending anchor, owning 63.4% of 2025 revenue; however, small and medium enterprises are expected to grow at a 24.3% CAGR through 2031, as subscription pricing, self-service onboarding, and cloud hosting lower barriers to entry. Cyber-insurance clauses now extend to smaller policyholders, pushing even 100-employee firms to adopt automated credential hygiene.

Simplified licensing from 1Password and Bitwarden aligns with toolchains popular in smaller businesses, adding momentum to the password management market size at the lower end of the spectrum.

By End-User Vertical: Healthcare Leads Growth Amid EHR Integration

Banking, financial services, and insurance retained their first position in 2025 with a 29.1% share, but healthcare and life sciences are the fastest-growing sectors at a 25.9% CAGR through 2031. Electronic health record ecosystems have created sprawling API keys, medical device credentials, and service accounts that legacy password policies cannot monitor. In 2024, federal guidance required providers to extend privileged access controls to any system processing patient data.

The retail, government, manufacturing, and education sectors have also adopted password vaults to combat ransomware and supply-chain intrusions, underscoring the breadth of the password management market.

Geography Analysis

North America contributed 38.9% of 2025 revenue, propelled by zero-trust mandates, cyber-insurance terms, and a mature cloud landscape. United States banks responded swiftly to the new OCC guidance, while Canadian institutions followed a similar pattern of integration. Growth will gradually moderate as enterprise penetration peaks, and attention shifts to small and medium-sized organizations.

The Asia Pacific is projected to post the fastest regional CAGR of 24.13% through 2031. Cloud-first government projects, a vibrant startup ecosystem, and widespread mobile internet drive demand for cross-platform vaults. India and Southeast Asia exhibit the sharpest adoption curves, while Japan and South Korea focus on regulatory compliance and workforce mobility.

Europe demonstrates robust hybrid deployments under the pressures of GDPR and NIS-2. DACH markets remain cautious, favoring open-source or self-hosted solutions in the wake of the LastPass incident. Elsewhere, regulations on data localization in Russia and parts of the Middle East and Africa are fostering local vendor ecosystems, ensuring the password management market retains regional nuances.

Competitive Landscape

The competitive field remains moderately fragmented as privileged-access specialists, consumer-oriented vault providers and open-source projects address overlapping use cases in the password management market. CyberArk and Delinea retain leadership of the high-governance segment through longstanding compliance deployments. 1Password, Dashlane and Keeper Security focus on employee self-service scenarios, while Bitwarden attracts developer communities with transparent source code and self-hosting flexibility. Meanwhile, Microsoft, Apple and Google embed credential storage directly into their operating systems, steadily encroaching on entry-level demand for standalone vaults.

API-first integration has become a decisive battleground because robotic process automation and DevOps pipelines need reliable secrets rotation across thousands of service accounts. HashiCorp Vault and CyberArk Conjur satisfy this requirement with dynamic, time-scoped tokens that blur the line between password managers and full privileged-access suites. Okta signaled similar ambitions by purchasing a secrets-management startup in 2024, bringing machine credential governance into its identity platform. Microsoft’s patent for distributed vault synchronization shows that hyperscalers are investing in edge-centric architectures to cut latency and satisfy data-sovereignty rules.[3]Media Relations, “Distributed Credential Vault Patent,” United States Patent and Trademark Office, uspto.gov Google extended passkey application programming interfaces to Chrome and Android in 2025, underlining a push to make passwordless authentication ubiquitous.

Recent strategic moves underscore the market’s competitive tempo. CyberArk allocated USD 150 million to launch data centers in Singapore, Sydney and Mumbai, meeting in-country hosting mandates for regulated customers. Microsoft activated native passkey support in Windows 11 and Azure Active Directory, compelling rivals to differentiate beyond baseline password storage. 1Password’s USD 75 million secrets-management acquisition and Bitwarden’s partnership with Amazon Web Services both aim to capture cloud-native workloads that merge human and machine identity governance. Dashlane’s ISO 27001 certification and Keeper Security’s insurance-readiness dashboard highlight growing buyer emphasis on third-party audits and risk reporting during large-scale procurements.

Password Management Industry Leaders

LastPass (GoTo)

1Password (AgileBits)

Dashlane Inc.

Keeper Security, Inc.

Bitwarden, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Bitwarden partnered with Amazon Web Services to embed vault functions inside AWS Identity and Access Management, expediting secure cloud workload deployment.

- October 2025: CyberArk invested USD 150 million to add data centers in Singapore, Sydney and Mumbai for low-latency privileged access management.

- September 2025: Microsoft enabled native passkey authentication in Windows 11 and Azure Active Directory, aiming to eliminate enterprise passwords without disrupting legacy apps.

- August 2025: 1Password acquired a secrets-management company for USD 75 million, integrating API key governance into its product line.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the password management market as all software and cloud services that create, store, synchronize, and audit human-generated credentials across consumer and enterprise endpoints. The scope tracks revenues from subscription, license, and maintenance fees for self-service vaults and privileged credential vaults that integrate with directory, single-sign-on, and MFA tools.

Scope exclusion: one-time professional services and standalone biometric/passkey platforms are kept out to avoid double counting.

Segmentation Overview

- By Solution Type

- Self-Service Password Management

- Privileged User Password Management

- By Access/Technology Type

- Desktop and Laptop

- Mobile Devices

- Voice-Enabled Password Reset

- Browser Extensions and Web Vaults

- By Deployment Mode

- Cloud-Hosted

- On-Premises

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Vertical

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecommunications

- Government and Public Sector

- Retail and E-Commerce

- Manufacturing

- Education

- Other End-User Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed CISOs, IAM architects, MSP channel partners, and regional cybersecurity regulators across North America, Europe, and Asia. Insights on average seat pricing, renewal churn, and mobile vault uptake helped us adjust secondary indicators and close information gaps before final triangulation.

Desk Research

We began with open data from authorities such as the U.S. National Institute of Standards and Technology, the Cybersecurity & Infrastructure Security Agency, the European Union Agency for Cybersecurity, and the FIDO Alliance, which quantify breach vectors and credential hygiene mandates. Trade statistics on global SaaS exports, SEC 10-Ks outlining identity-security revenue lines, and patent filings accessed through Questel informed baseline technology adoption curves. Further context came from Verizon's Data Breach Investigations Report, industry association white papers, and news archives gathered via Dow Jones Factiva. These examples illustrate the tier-1, non-paywalled sources we tapped; numerous additional outlets buttressed data validation.

Market-Sizing & Forecasting

A top-down model starts with the global population of paid digital identities, layers credential proliferation per user, applies password-manager penetration rates, and multiplies by blended annual seat prices. Select bottom-up checks, supplier revenue roll-ups and channel ASP multiplied by volume samples, reconcile totals. Key variables include the number of internet users, average accounts per employee, cyber-insurance premium trends, zero-trust program adoption, privileged access spend, and regional FX shifts. Multivariate regression combined with scenario analysis generates the 2025-2030 outlook while gap handling rules flag regions lacking transparent financials for iterative adjustment.

Data Validation & Update Cycle

Outputs pass variance tests against breach incident frequencies and listed-vendor earnings, then undergo a two-step analyst peer review. Reports refresh yearly, with mid-cycle updates when material events, such as major hacks or regulatory changes, trigger a re-contact of sources, ensuring clients receive the latest synced view.

Why Our Password Management Baseline Commands Reliability

Published estimates rarely align because firms pick different solution baskets, pricing bases, and refresh rhythms. We confront those divergences up front.

Key gap drivers include: some publishers omit consumer freemium seats, others fold biometric passkey platforms into the same pool, and several freeze exchange rates for the entire forecast window, while Mordor rolls quarterly FX and inflation updates into its model.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.40 B (2025) | Mordor Intelligence | - |

| USD 3.22 B (2025) | Regional Consultancy A | Leaves out consumer freemium usage and applies static ASP uplift |

| USD 3.64 B (2024) | Trade Journal B | Bundles biometric/passkey revenues and discloses no refresh cadence |

The comparison shows that when scope breadth, price realism, and update cadence are harmonized, Mordor's figures offer a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the password management market in 2026?

The password management market size stands at USD 2.94 billion in 2026.

What is the expected growth rate for password management solutions to 2031?

Market revenue is projected to advance at a 22.39% CAGR between 2026 and 2031.

Which deployment model is growing fastest?

Hybrid architectures are set to expand at a 23.9% CAGR through 2031 due to data-residency mandates.

Why are privileged password vaults gaining traction?

Regulatory audits and cyber-insurance clauses favor tools that rotate credentials and record privileged sessions.

Which region will see the quickest expansion?

Asia Pacific is forecast to record the highest regional CAGR at 24.13% through 2031.

How are passkeys affecting demand for password managers?

Rising consumer adoption of passkeys reduces future demand for self-service managers, though enterprise needs persist.

Page last updated on: