Size and Share of Advanced Authentication Market In Healthcare Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

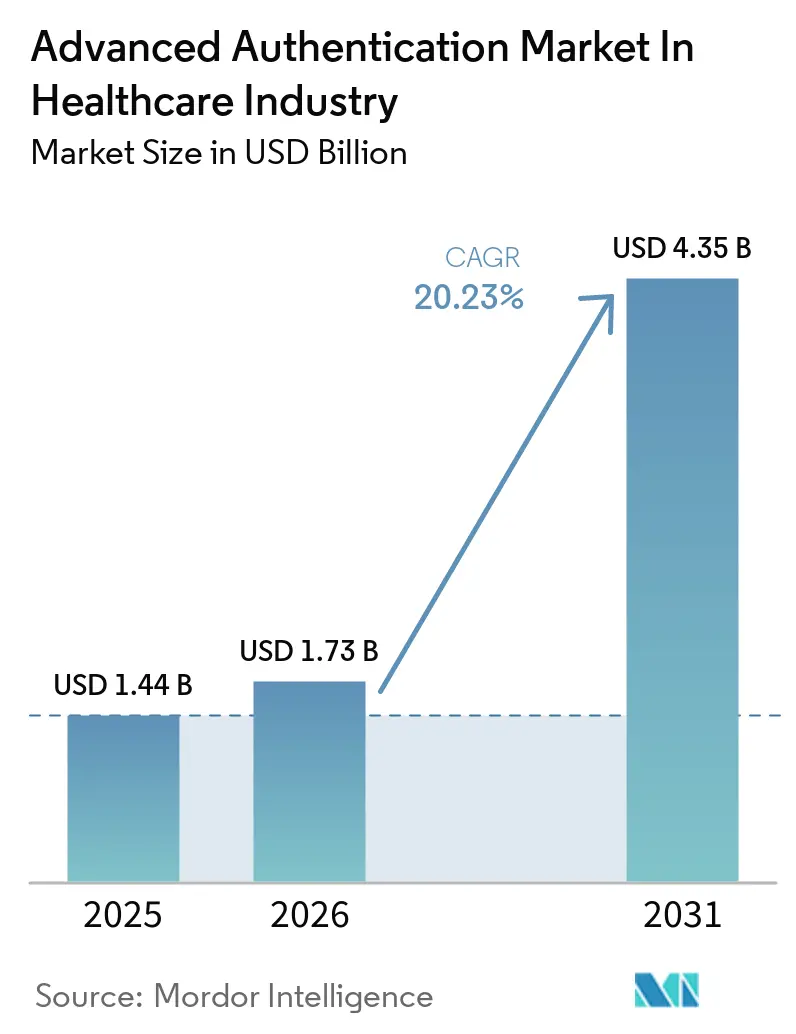

| Market Size (2026) | USD 1.73 Billion |

| Market Size (2031) | USD 4.35 Billion |

| Growth Rate (2026 - 2031) | 20.23% CAGR |

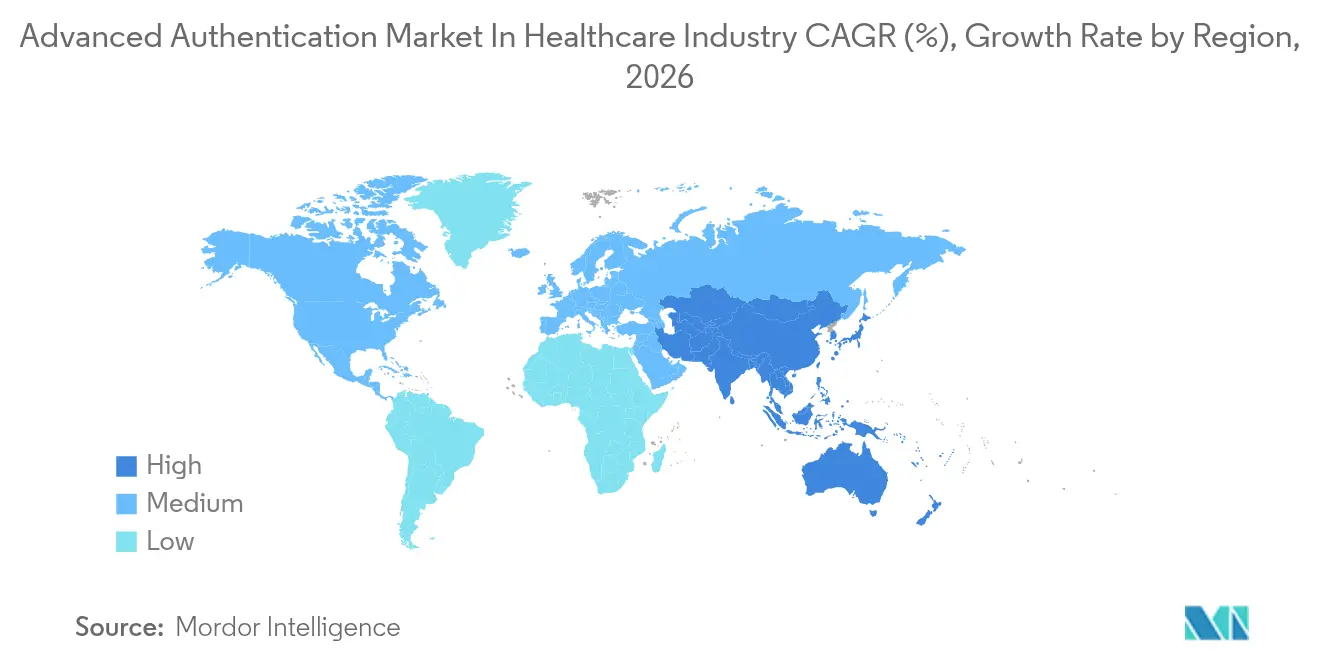

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

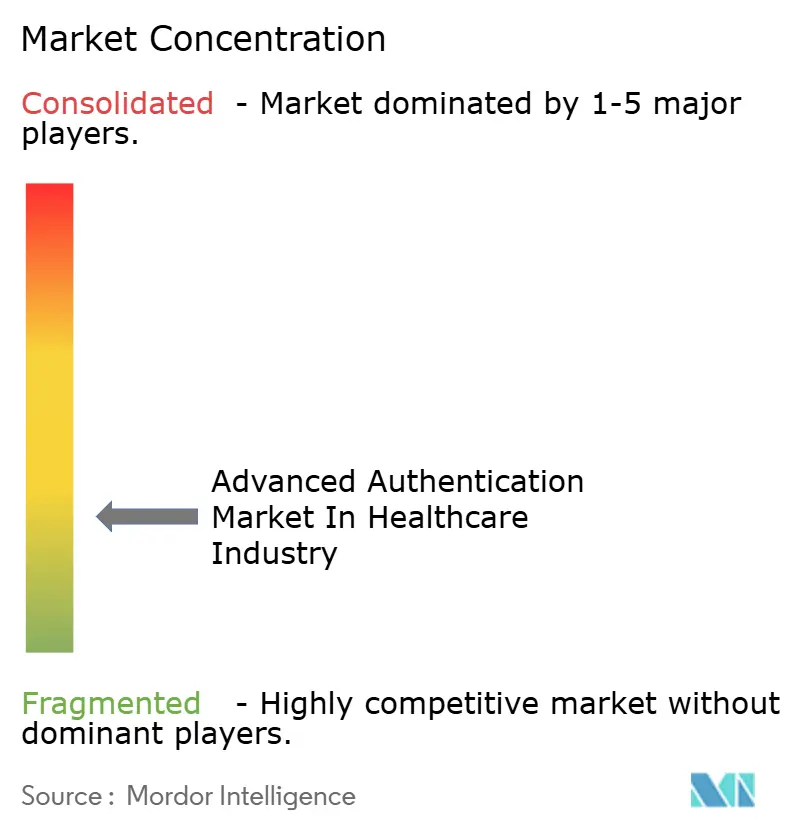

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Advanced Authentication Market In Healthcare Industry by Mordor Intelligence

The advanced authentication market size in healthcare industry was valued at USD 1.44 billion in 2025 and estimated to grow from USD 1.73 billion in 2026 to reach USD 4.35 billion by 2031, at a CAGR of 20.23% during the forecast period (2026-2031). Rapid budget reallocation after the February 2024 Change Healthcare breach, stricter global data-protection mandates, and the rise of connected medical devices are accelerating the adoption of phishing-resistant identity controls. Hospitals now spend up to 12% of their IT budgets on cybersecurity, with authentication singled out as a key area of focus because credential theft triggered 74% of 2024 breaches. Cloud-delivered identity platforms lead deployment because they spread compliance workloads across shared responsibility models, while biometric log-ons reduce workflow friction when seconds matter at the bedside. Vendors that combine sub-second clinician access, FHIR-aligned single sign-on, and zero-trust-ready continuous verification are well-positioned to win as healthcare boards treat identity assurance as a patient-safety infrastructure rather than an optional overhead.

Key Report Takeaways

- By authentication method, biometrics led with 47.85% revenue share in 2025; mobile smart credentials are advancing at a 22.05% CAGR to 2031.

- By authentication factor, multi-factor controls accounted for 63.10% of the advanced authentication market share in 2025 and are growing at a 21.10% CAGR through 2031.

- By component, solutions captured 67.05% of 2025 revenue, while services are projected to expand at 20.90% CAGR.

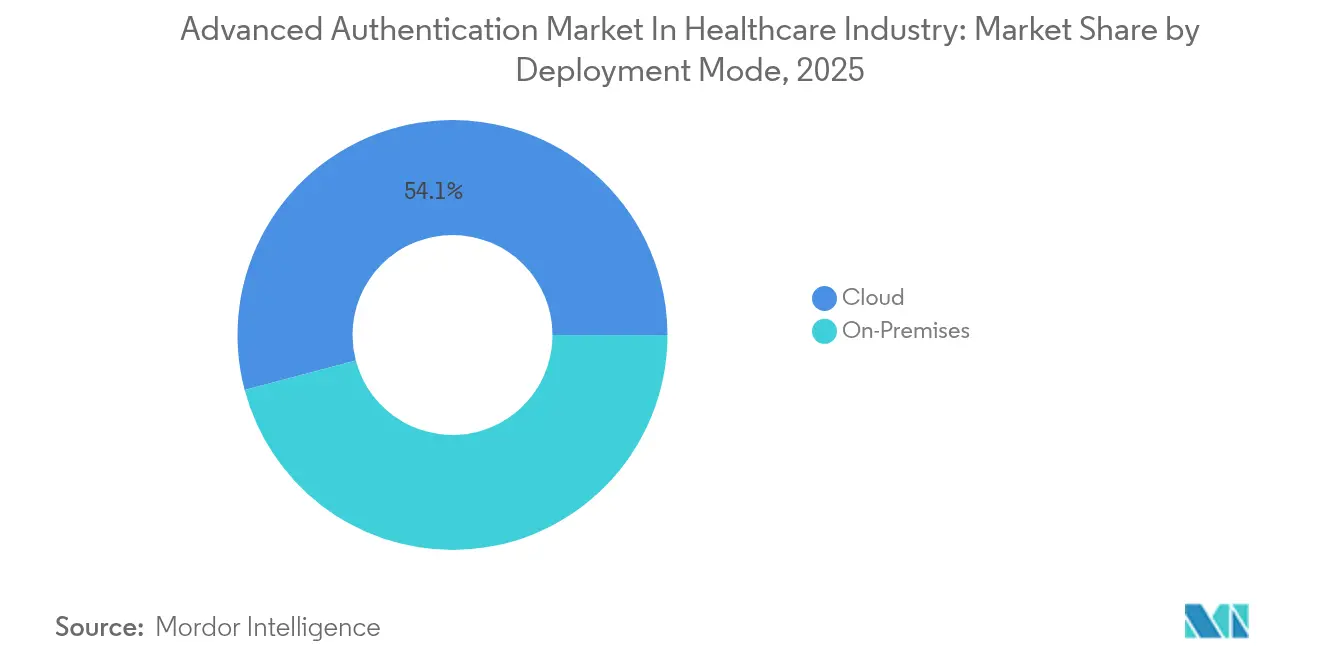

- By deployment mode, cloud platforms held 54.12% share of the advanced authentication market size in 2025 and are set to rise at 21.20% CAGR.

- By end user, hospitals and clinics commanded 46.10% revenue in 2025; medical device manufacturers post the fastest growth at 22.10% CAGR.

- By geography, North America dominated with 39.95% share in 2025, whereas Asia-Pacific is forecast to record a 22.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Advanced Authentication Market In Healthcare Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Connected Medical Devices Expanding Attack Surface | +4.2% | Global, concentration in North America and Europe | Medium term (2-4 years) |

| Regulatory Mandates for Patient Data Protection | +5.1% | Global, led by North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift to Remote Telehealth Requiring Secure Identity Verification | +3.8% | North America and Europe core, Asia-Pacific emerging | Short term (≤ 2 years) |

| Rising Healthcare Ransomware Attacks Driving Security Budgets | +4.6% | Global, highest impact in North America | Short term (≤ 2 years) |

| Integration of Biometric Authentication in EHR Systems | +3.3% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Rapid Adoption of Zero Trust Architecture in Hospital IT Networks | +3.9% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Healthcare Ransomware Attacks Driving Security Budgets

Ransomware caused 238 of 444 healthcare cyber events in 2024 and accounted for 69% of compromised records, underscoring the lethality of credential theft pipelines. The USD 2.4 billion fallout from the Change Healthcare outage revealed the monetary weight of weak authentication in the healthcare cybersecurity space. Average security budgets rose from 5% to 12% of IT spending, and board directives now frame password retirement as a measurable patient safety objective. FinCEN tracked USD 305.4 million in ransomware payouts tied to 389 healthcare incidents between 2022 and 2024, which hardened the business case for password-less strategies.[1]Financial Crimes Enforcement Network, “FinCEN Analysis Reveals Ransomware Trends in Bank Secrecy Act Data,” fincen.gov Providers that rolled out phishing-resistant factors recorded measurable drops in privileged-account compromise, validating the link between strong identity proofing and ransomware resilience.

Regulatory Mandates for Patient Data Protection

FDA Section 524B, operational since March 2023, requires device manufacturers to embed authentication and publish software bills of materials in every pre-market submission.[2]U.S. Food and Drug Administration, “Cybersecurity in Medical Devices: Quality System Considerations and Content of Premarket Submissions,” fda.gov NIST SP 800-63A-4, issued in July 2025, upgrades biometric standards to include presentation-attack detection at false-match rates below 1 in 10,000.[3]National Institute of Standards and Technology, “Digital Identity Guidelines SP 800-63A-4,” nist.gov HIPAA enforcement accelerated, with USD 142 million in 2024 penalties tied to access-control lapses. The European GDPR mirrors these fines, with penalties of up to 4% of global revenue, prompting multinationals to unify their identity policies across continents. Cyber-insurance renewals now mandate multi-factor deployment, making regulatory and market forces converge on the same authentication baseline.

Proliferation of Connected Medical Devices Expanding Attack Surface

As of 2022, over half of connected medical devices shipped with a critical, unpatched vulnerability, providing low-skill pivot points into hospital networks. Joint FDA–CISA advisories in January 2025 exposed hard-coded backdoors in Contec CMS8000 monitors, forcing emergency segmentation and device-level credential controls. Modern infusion pumps support certificate-based mutual authentication, whereas legacy equipment relies on MAC address whitelists, creating a two-tier identity stack. Real-time device attestation and signed firmware updates are becoming procurement check boxes, and suppliers that cannot furnish them risk losing tenders.

Shift to Remote Telehealth Requiring Secure Identity Verification

CMS telehealth flexibilities now extend through January 2026, which sustains a spike in remote visits but also widens identity gaps. Two-thirds of FCC telehealth grants financed remote-monitoring gear that lacked robust identity proofing. HHS accreditation now checks for multi-factor gatekeeping before data transit, so platform owners retrofit FIDO2 keys or biometric liveness checks into patient apps. NIST SP 1800-30 provides technical guidelines for such ecosystems, and early adopters report smoother reimbursement audits once secure identity verification is demonstrated.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Costs for Legacy Hospital IT Systems | -2.8% | Global, acute in North America and Europe with aging infrastructure | Medium term (2-4 years) |

| Interoperability Challenges Among Disparate Healthcare Applications | -2.1% | Global, most severe in North America due to fragmented EHR landscape | Long term (≥ 4 years) |

| User Resistance from Clinical Staff Due to Workflow Friction | -1.6% | Global, acute in emergency and surgical units | Short term (≤ 2 years) |

| Limited Broadband Connectivity in Rural Healthcare Facilities | -1.3% | Rural zones in North America, Asia-Pacific, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs for Legacy Hospital IT Systems

Many hospitals juggle more than 150 applications that run on unsupported operating systems. Custom integration for each legacy platform pushes project bills into the multi-million-dollar range, a challenge for providers running on 2-3% margins. Identity gateways translate old LDAP or proprietary log-ons into modern SAML or OAuth, but add complexity. Capital committees often choose diagnostic equipment over invisible security, leading to deferred upgrades until after a breach or consent decree.

Interoperability Challenges Among Disparate Healthcare Applications

FHIR and HL7 govern data structure rather than identity federation, so clinicians still manage up to a dozen passwords. The Cures Act information-blocking rule demands open data exchange, yet external partners often lack compatible credentials, spawning manual workarounds. SMART on FHIR brings OAuth alignment but coverage remains patchy, forcing parallel identity silos that inflate support costs and increase reuse of weak passwords.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Authentication Method: Biometrics Speed Clinical Touchpoints

Biometrics accounted for 47.85% of advanced authentication market in healthcare industry revenue in 2025, giving this segment nearly half of the advanced authentication market share. The modality excels because surgical teams can unlock records with gloved fingerprints or palm-vein scans in under one second. The advanced authentication market size for biometrics is projected to rise at 19.60% CAGR through 2031 as liveness detection standards mature. Vendors embed multispectral sensors into mobile carts, securing both device and session in one gesture. Implementation success hinges on hygiene protocols that disinfect scanners without degrading accuracy.

Mobile smart credentials record the fastest growth, in advanced authentication market in healthcare industry, at a 22.05% CAGR to 2031, driven by the convergence of physical door access and logical log-on inside one smartphone wallet. Hospitals can revoke these digital badges instantly, trimming risk when staff depart. Smart cards persist under Defense Health Agency mandates but face plateauing demand because reader fleets are expensive to maintain. Hardware tokens secure sterile zones where phones are barred; however, market share is eroding as FIDO2 on-device keys become the standard. One-time passwords are falling out of favor after documented SIM-swap exploits.

By Authentication Factor: Multi-Factor Becomes the Default

Multi-factor solutions, in advanced authentication market in healthcare industry, held 63.10% share in 2025 and expand at 21.10% CAGR as cyber-insurance carriers refuse coverage without them. Risk-based engines now elevate factor count only when anomalous behavior is detected, blending security with clinician usability. Push-fatigue attacks documented in late 2024 accelerated migration to FIDO2 hardware keys that block replay. The advanced authentication market in healthcare industry size tied to multi-factor deployments is forecast at USD 2.86 billion by 2031.

Single-factor still protects 36.90% of endpoints, largely patient portals where convenience outweighs risk. Governance committees segment applications by data-classification level, deploying biometric-plus-token gates on e-prescribing while keeping username-password pairs on cafeteria systems. This tiered model aligns with NIST guidance and avoids blanket friction that could undercut adoption.

By Component: Services Close the Skills Gap

Solutions accounted for 67.05% of 2025 revenue of advanced authentication market in healthcare industry, encompassing identity platforms, sensors, and tokens. Yet services log a faster 20.90% CAGR because few hospitals can staff 24/7 identity operations. Managed security service providers now bundle identity governance, privileged-access audits, and zero-trust policy tuning under monthly retainers. That shift converts capex to opex and injects specialist talent that community hospitals cannot recruit.

Large medical centers, in advanced authentication market in healthcare industry, are embracing hybrid models, keeping strategic governance on-site while offloading biometric enrollment drives and real-time anomaly detection. Vendors that offer both software and white-glove services tend to gain retention, as clients prefer to have a single point of contact.

By Deployment Mode: Cloud Scales with Telehealth

Cloud deployments held 54.12% revenue in 2025 and grow at 21.20% CAGR, reflecting the need to support surging telehealth log-ons without adding data-center racks. Microsoft Entra and similar SaaS identity layers apply conditional access based on risk scores, geolocation, and device health. Providers appreciate auto-patching and built-in compliance attestations.

On-premises directories remain in 45.88% of environments due to data-sovereignty clauses and sunk hardware costs. Many CIOs pursue hybrid models in which authoritative directories remain on-site, while cloud brokers handle session tokens for SaaS applications. The advanced authentication industry increasingly regards hybrid as a transition state rather than an end goal.

By End User: Manufacturers Face New Design Mandates

Hospitals and clinics delivered 46.10% of 2025 spend, but medical device manufacturers are the fastest risers at 22.10% CAGR. FDA Section 524B forces authentication into design documentation, so vendors scramble to retrofit certificate stores and secure boot in upcoming product lines. The advanced authentication market in healthcare industry size for device makers will nearly triple by 2031 as every infusion pump and monitor must prove provenance.

Insurers, labs, and pharma firms also expand budgets. CMS interoperability rules push OAuth-secured APIs, demanding identity brokers in payer stacks. Clinical trial data sets require tamper-proof log-ons to satisfy FDA 21 CFR Part 11 audit trails. Authentication is now a common thread across the healthcare continuum, knitting together patient, provider, and supply-chain roles.

Geography Analysis

North America dominated with 39.95% of 2025 revenue of advanced authentication market in healthcare industry, helped by high breach costs, aggressive regulators, and strong IT budgets. OCR issued USD 142 million in penalties during 2024, and 68% cited authentication gaps. The Change Healthcare outage demonstrated ecosystem-wide ripple effects, which moved identity to the board agenda. Canada follows similar paths through provincial e-healthcards, while Mexico is earlier in its journey but is adding identity controls as private providers adopt electronic records.

The Asia-Pacific region posts the fastest regional growth at a 22.60% CAGR through 2031. Japan modernizes hospital identity under government digitization schemes that embed face recognition in EHR kiosks. India links Aadhaar biometrics to the Ayushman Bharat Digital Mission, creating a massive new user base secured by fingerprints and iris scans. China mandates multi-factor authentication controls within smart hospital rollouts that utilize national health clouds. Australia and South Korea ride mature broadband and smartphone penetration to push mobile authentication in remote care. Despite momentum, data-protection laws vary widely, so vendors must tailor cloud hosting and key escrow models by advanced authentication market in healthcare industry.

Europe sits between these poles. GDPR fines up to 4% of global turnover motivate early compliance, and Germany’s e-healthcard program embeds X.509 certificates by default. The United Kingdom’s NHS is rolling identity across integrated care systems, yet complexity slows timelines. France, Italy, and Spain invest through national digital-health funds, but procurement cycles remain lengthy. Advanced authentication market adoption is slower in Eastern Europe, and older infrastructure restrains cloud shifts, yet pan-EU standards exert steady pressure for convergence. South America, the Middle East, and Africa trail in penetration but benefit from new hospital builds that can leapfrog straight to cloud-native identity.

Competitive Landscape

The advanced authentication market in healthcare industry is moderately fragmented. Imprivata partners with Epic and Oracle Health to supply tap-and-go single sign-on that preserves audit trails while cutting chart access to under one second. Microsoft relies on its Entra stack to upsell identity services into Azure-hosted clinical applications, bundling conditional access with Office 365 deployments. Okta, boosted by its Auth0 acquisition, courts developer teams building patient portals with custom flows.

Competition revolves around three axes, including login latency, cross-app interoperability, and phishing resistance. Vendors that score under 500 milliseconds on workstation unlocks win clinician support. Cross-platform federation remains a moat; proprietary connectors into Cerner, Meditech, or Allscripts keep rivals out. FIDO2 keys and public-key credentials mark the new security bar, and suppliers lagging on hardware-backed factors risk contract churn.

White space opens in embedded medical devices, where Section 524B pulls authentication left into R&D lifecycles. Start-ups tout behavioral biometrics that monitor typing cadence and cursor flow to re-score sessions in real time, aligning with zero-trust models. Incumbents retrofit risk engines but struggle with legacy code bases. M&A is likely as platform players buy specialist sensor firms to own the full stack from fingerprint pads to analytics.

Leaders of Advanced Authentication Market In Healthcare Industry

NetMotion Software, Inc

CJIS Solutions LLC

Micro Focus International PLC

NEC Corporation

Thales Group (Gemalto NV)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NIST published SP 800-63A-4, raising biometric liveness detection standards.

- January 2025: FDA and CISA disclosed hard-coded backdoors in Contec CMS8000 monitors, forcing device-level authentication retrofits.

- October 2024: CISA alert detailed push-fatigue attacks that bypass weak multi-factor deployments

- September 2024: FDA issued draft guidance that turns authentication into a design checkpoint for all future medical devices.

Scope of Report on Advanced Authentication Market In Healthcare Industry

Every organization needs a reliable security system to confirm the truth of something or the identity of a person. The primary or traditional password method is too often breached or copied or share, thereby exposing data to theft or malicious intrusions. Thus there is a need for two factors or multi-factor authentication. It dramatically reduces the risk of threats.

The Advanced Authentication Market in Healthcare Industry Report is Segmented by Authentication Method (Biometric, Smart Card, Mobile Smart Credentials, Hardware Token, Other Authentication Methods), Authentication Factor (Single Factor, Multi-Factor), Component (Solutions, Services), Deployment Mode (On-Premises, Cloud), End User (Hospitals and Clinics, Health Insurance Providers, Pharma and Biotech Companies, Medical Device Manufacturers, Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Biometric |

| Smart Card |

| Mobile Smart Credentials |

| Hardware Token |

| Other Authentication Methods |

| Single Factor |

| Multi-Factor |

| Solutions |

| Services |

| On-Premises |

| Cloud |

| Hospitals and Clinics |

| Health Insurance Providers |

| Pharma and Biotech Companies |

| Medical Device Manufacturers |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| By Authentication Method | Biometric | ||

| Smart Card | |||

| Mobile Smart Credentials | |||

| Hardware Token | |||

| Other Authentication Methods | |||

| By Authentication Factor | Single Factor | ||

| Multi-Factor | |||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | On-Premises | ||

| Cloud | |||

| By End User | Hospitals and Clinics | ||

| Health Insurance Providers | |||

| Pharma and Biotech Companies | |||

| Medical Device Manufacturers | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the advanced authentication market in healthcare?

It stands at USD 1.73 billion and is projected to reach USD 4.35 billion by 2031.

Which authentication method leads hospital deployments?

Biometrics led with 47.85% revenue share in 2025 and continues to grow thanks to sub-second clinician access.

Why are medical device makers investing in authentication?

FDA Section 524B now requires proof of embedded cyber controls, driving a 22.10% CAGR in spend by manufacturers.

Which region is growing the fastest?

Asia-Pacific posts a 22.60% CAGR through 2031 as Japan, India, and China roll out biometric and mobile identity programs.

How are ransomware trends influencing purchasing?

USD 305.4 million in ransomware payments between 2022 and 2024 pushed boards to double cybersecurity budgets, with authentication the first spend line.

What role does cloud deployment play?

Cloud platforms held 54.12% share in 2025 because they provide elastic scale for telehealth log-ons and shift audit burdens to certified providers.

Page last updated on: