Passive Fire Protection Coating Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

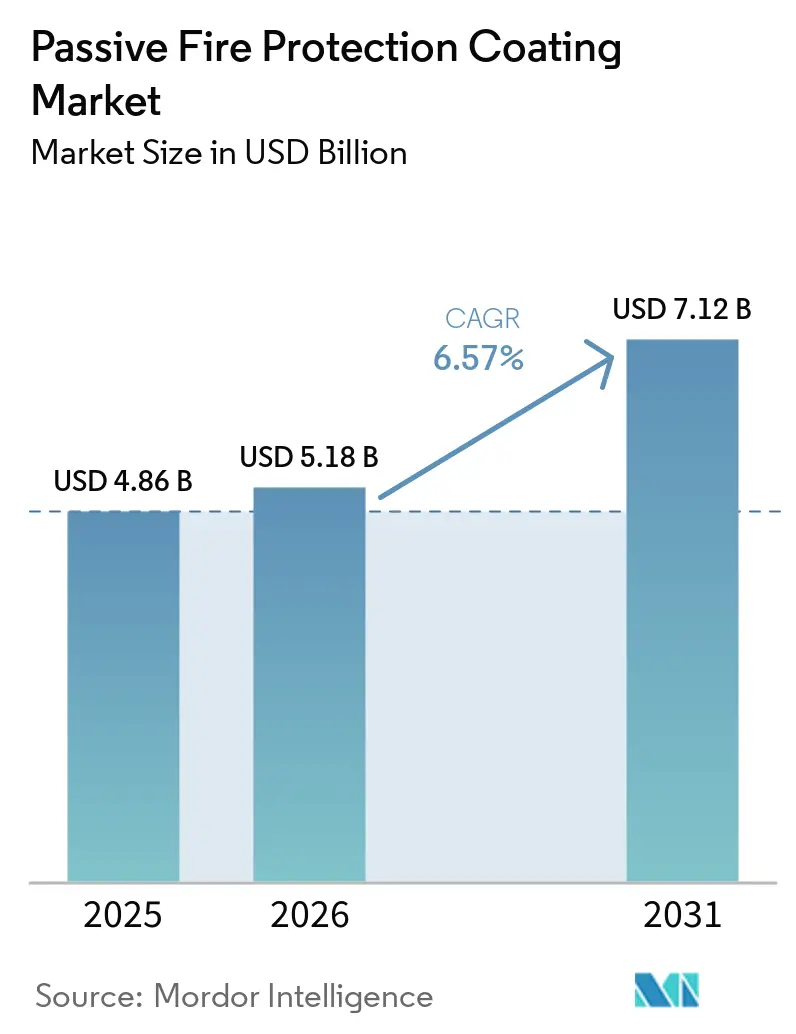

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 7.12 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passive Fire Protection Coating Market Analysis by Mordor Intelligence

The Passive Fire Protection Coating Market size is expected to grow from USD 4.86 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 7.12 billion by 2031 at 6.57% CAGR over 2026-2031. Owners of high-rise towers, LNG (Liquefied Natural Gas) terminals, and grid-scale battery sites are prioritizing coatings that reduce fire-related downtimes. This shift in focus is driving demand toward ultra-thin intumescents, which add minimal dead load. In response to stricter VOC (Volatile Organic Compound) caps in the European Union and California, there is a transition from solvent-borne films to 100%-solids epoxies. These epoxies cure faster and emit no regulated emissions. Energy-transition investments in hydrogen pipelines, battery energy-storage systems (BESS), and offshore wind substations are expanding the application base. Additionally, with the global phase-out of fluorinated firefighting foams scheduled for July 2026, capital is being redirected from active suppression methods to durable passive barriers. Competitive intensity remains moderate, as the top five suppliers account for only 40% of global revenue. However, suppliers with ISO (International Organization for Standardization) 17025-accredited labs are gaining an advantage as regulators move toward mandatory third-party verification of fire-performance claims.

Key Report Takeaways

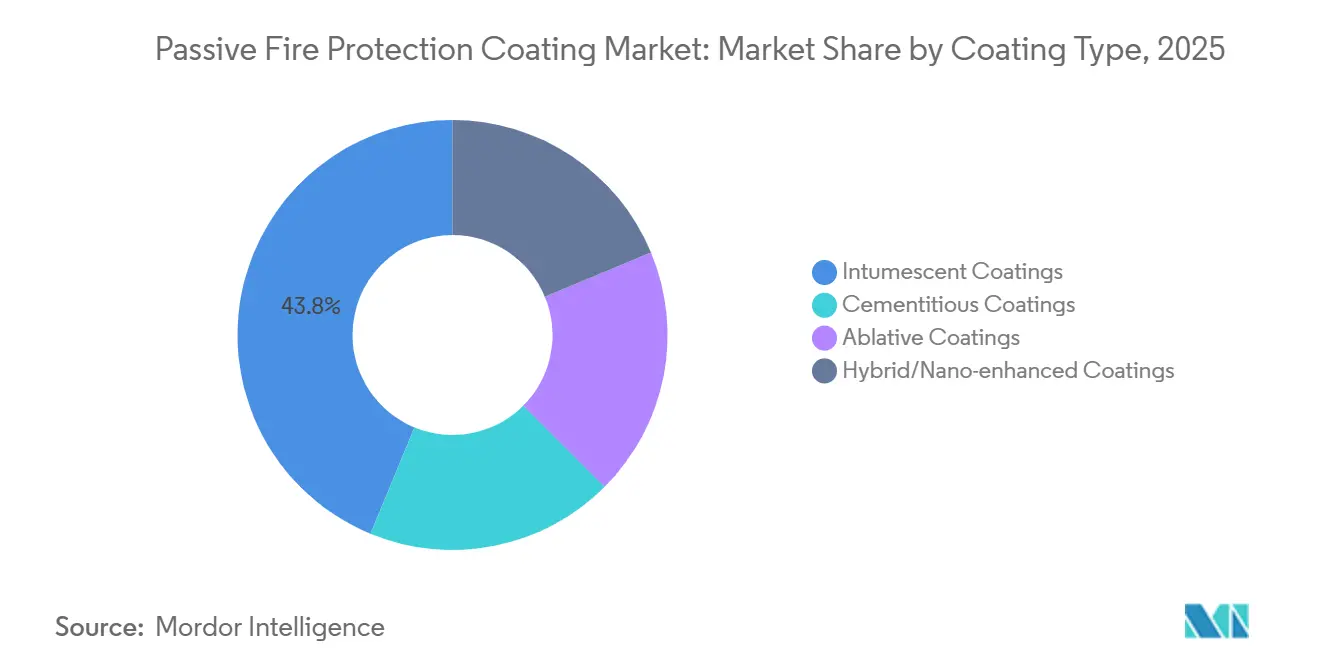

- By coating type, intumescents coatings led with 43.78% of the passive fire protection coating market share in 2025; hybrid and nano-enhanced products are forecast to post the fastest 6.87% CAGR through 2031.

- By technology, solvent-based chemistries captured 34.88% of revenue in 2025, whereas 100%-solids epoxies are projected to expand at a 7.22% CAGR to 2031.

- By substrate, structural steel accounted for 56.11% of demand in 2025, while coatings for wood elements are on track for a 7.43% CAGR to 2031.

- By fire scenario, cellulosic fire protection held 50.73% of spending in 2025, but cryogenic-spill applications will rise fastest at 7.32% CAGR through 2031.

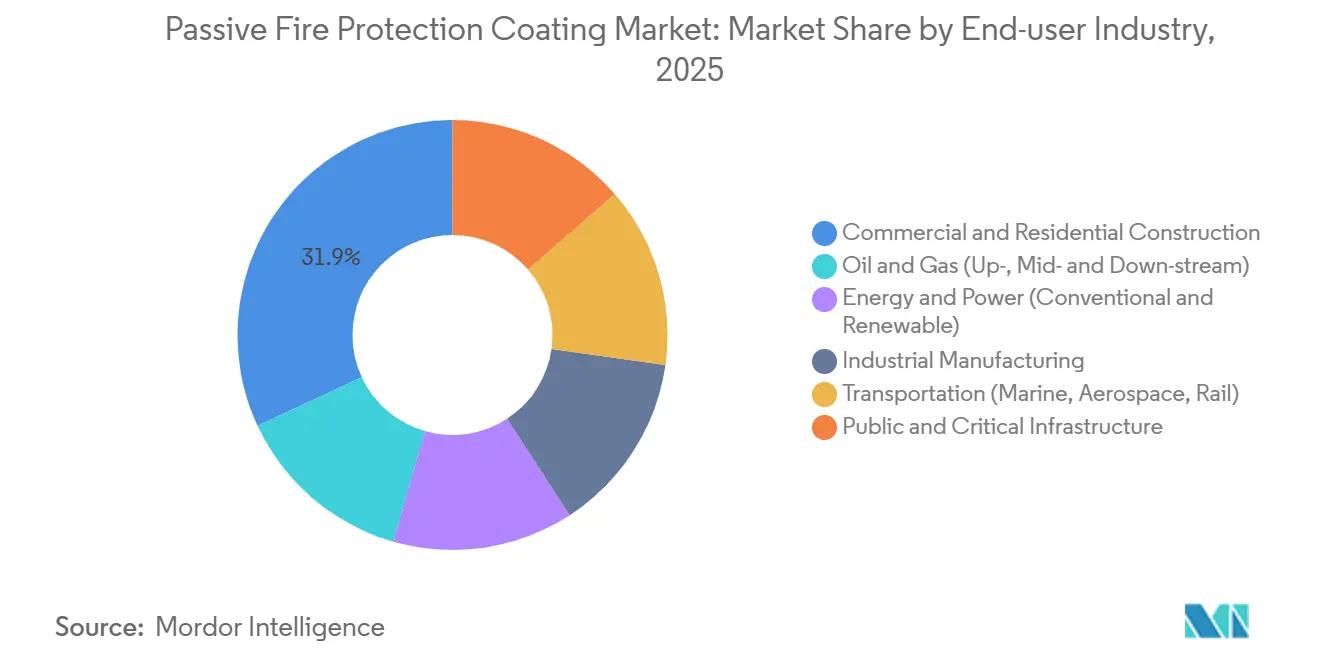

- By end-user industry, commercial and residential construction represented 31.93% of 2025 revenue; public and critical-infrastructure projects form the quickest-growing segment at 7.52% CAGR to 2031.

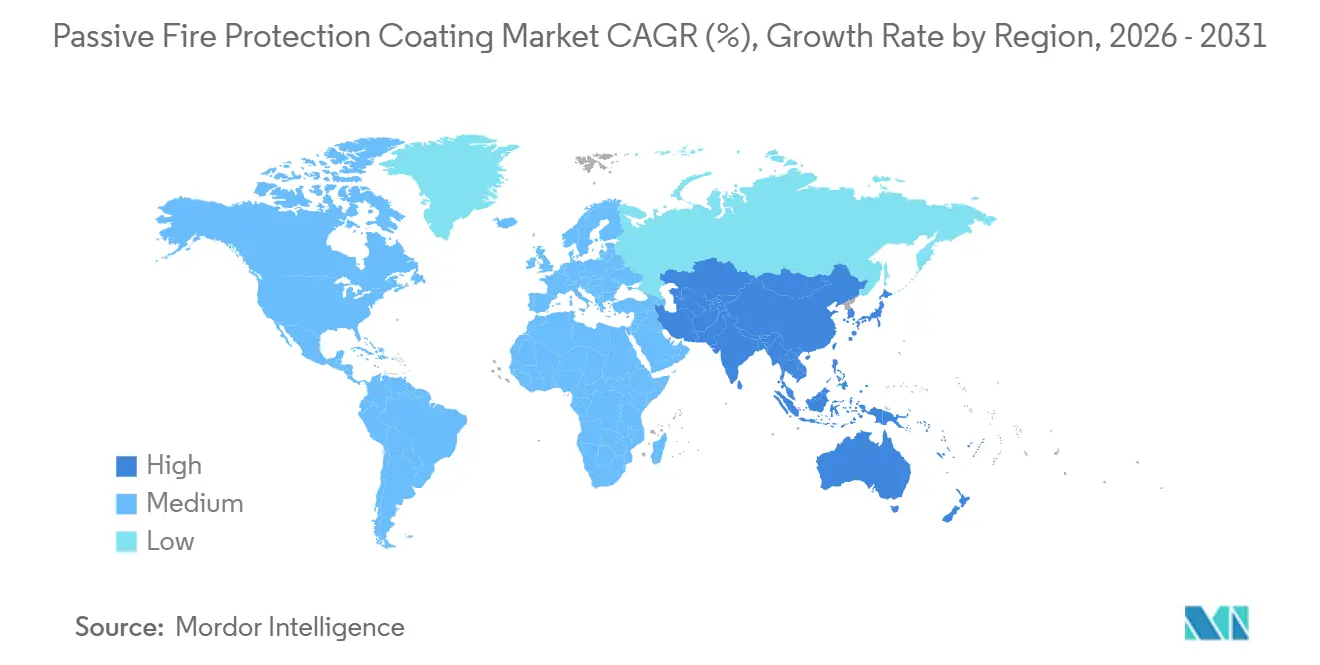

- By geography, Asia-Pacific commanded 37.43% of global value in 2025 and is projected to advance at a 7.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Passive Fire Protection Coating Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent fire-safety regulations in commercial & industrial real-estate | +1.2% | Global, with early enforcement in the EU, North America, and Gulf Cooperation Council states | Short term (≤ 2 years) |

| Rapid build-out of high-rise & public infrastructure worldwide | +1.5% | APAC core (China, India, ASEAN-6), spill-over to the Middle East & Africa | Medium term (2–4 years) |

| Expansion of oil, gas & power assets (including LNG) | +0.9% | North America (Gulf Coast, Permian Basin), the Middle East, and Australia | Medium term (2–4 years) |

| Advances in ultra-thin epoxy-intumescent formulations | +0.7% | Global, led by Western Europe and Japan | Long term (≥ 4 years) |

| Digital-twin & sensor-embedded PFP systems enabling predictive maintenance | +0.4% | North America, Western Europe, with pilot deployments in Singapore and the UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Fire-Safety Regulations In Commercial & Industrial Real Estate

Governments are increasingly adopting performance-based codes, mandating third-party certification of coatings and shortening compliance timelines for asset owners. In December 2025, the United Kingdom transitioned from BS 476 to BS EN 13501-1, effectively prohibiting combustible cladding on structures exceeding 18 meters and driving demand for Euroclass-rated intumescents. India's National Building Code 2024 mandates IS 3809-tested coatings for commercial buildings over 15 meters, leading to retrofits across 1.2 million square meters of office space in Mumbai and Bengaluru. The European Union's updated Construction Products Regulation, effective Q3 2027, requires International Organization for Standardization (ISO) 17025-verified performance declarations, imposing significant non-compliance penalties on smaller suppliers[1]European Commission, “Construction Products Regulation Revision,” ec.europa.eu. In California, early adopters are addressing 2025 amendments to Rule 1113, capping volatile organic compound (VOC) content at 50 grams per liter for architectural coatings. As these regulations gain traction, ultra-thin, zero-VOC epoxies are becoming standard in passive fire protection coating bids.

Rapid Build-Out Of High-Rise & Public Infrastructure Worldwide

Urbanization in emerging markets is driving the construction of record numbers of super-tall structures exceeding 300 meters, necessitating coatings with three-hour hydrocarbon exposure ratings. In 2025, China completed 87 buildings, surpassing 200 meters, each utilizing approximately 12,000 square meters of intumescent film on steel columns. India's metro-rail expansion mandates Underwriters Laboratories (UL) 263-compliant coatings for underground platforms to curb smoke spread. The Gulf Cooperation Council, with a USD 1.3 trillion infrastructure agenda spanning airports, seaports, and six new cities, adheres to the United Arab Emirates Fire and Life Safety Code, which demands two-hour resistance for primary members. Such projects are bolstering the passive fire protection coating market, with stringent fire-rating clauses now common in turnkey Engineering, Procurement, and Construction (EPC) contracts. Contractors are increasingly integrating coatings into lump-sum bids, streamlining procurement but raising quality-assurance expenses.

Expansion Of Oil, Gas & Power Assets Including LNG

Between 2026 and 2031, global LNG capacity is poised to expand by 140 million tons per annum (Mtpa), with major projects in Qatar, the United States, and Mozambique opting for ISO 22899-1-rated coatings to ensure jet-fire protection. Coatings must withstand cryogenic spills at -162°C, remaining ductile under thermal shock; suppliers are now embedding ceramic microspheres in epoxy matrices to address this. The International Energy Agency forecasts a USD 2.8 trillion investment in upstream and midstream capital expenditure by 2030, suggesting a coating market potential of USD 33-50 billion, given that passive systems typically account for 1.2-1.8% of project costs[2]International Energy Agency, “World Energy Outlook 2025,” iea.org. Additionally, as grid-scale Battery Energy Storage System (BESS) installations aim for 500 gigawatt-hours (GWh) by 2030, there's a growing demand for intumescents to mitigate thermal-runaway events. Collectively, these ventures are pushing the ceiling of the passive fire protection coating market size.

Advances In Ultra-Thin Epoxy-Intumescent Formulations

As labor and space costs increase, asset owners are opting for films that achieve the 120-minute rating with a dry-film thickness (DFT) below 1,500 micrometers (µm). Sherwin-Williams' FIRETEX M90/03 complies with Underwriters Laboratories (UL) 263 standards at 1,200 µm, reducing labor hours compared to cementitious sprays requiring a 25-millimeter build. Research indicates that organic intumescents retain 92% char strength after 5,000 hours of weathering, exceeding the 78% retention of spray-applied fireproofing. Formulators are utilizing expandable graphite, ammonium polyphosphate, and nano-silica to enhance expansion ratios and slow char erosion during hydrocarbon fires. These advancements support the adoption of higher-priced epoxies, particularly in regions with high humidity and ultraviolet (UV) exposure, where traditional gypsum-based materials degrade in less than ten years.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High installed cost versus conventional cladding | -0.8% | Global, most acute in price-sensitive markets (South Asia, Sub-Saharan Africa, Latin America) | Short term (≤ 2 years) |

| Performance degradation in humid, UV-rich or cryogenic settings | -0.5% | Tropical zones (Southeast Asia, Caribbean, coastal Africa), Arctic installations (Northern Canada, Russia, Norway) | Medium term (2–4 years) |

| Supply-chain volatility for phosphorus-based flame-retardant feedstocks | -0.4% | Global, with acute shortages in North America and Europe due to China's export restrictions | Short term (≤ 2 years) |

| Regulatory uncertainty around nano-additive ecotoxicity | -0.3% | European Union (REACH restrictions), with spillover to the UK, Switzerland, and California | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Installed Cost Versus Conventional Cladding

Fully installed intumescent systems cost USD 35-85/m² compared to USD 15-30/m² for unrated plaster, representing a cost difference that impacts purchasing decisions in regions where fire insurance penetration is below 15% of asset value. In developed markets, labor accounts for up to 65% of the total cost. Additionally, a shortage of National Association of Corrosion Engineers (NACE) or Society for Protective Coatings (SSPC)-certified applicators has extended project handover timelines by four to six weeks in the United States and Western Europe. In South Asia, annual wage inflation exceeding 8% between 2023 and 2025 has prompted many developers to choose sprinklers over coatings, despite the 40% higher lifetime maintenance costs associated with sprinklers.

Performance Degradation In Humid, UV-Rich Or Cryogenic Settings

Field audits on North Sea platforms indicated that 18% of coatings applied between 2018 and 2022 exhibited cracking within three years due to salt spray and freeze-thaw cycling. In coastal Africa, coatings exposed to over 1,200 kilowatt-hours per square meter per year (kWh/m²/year) of UV radiation showed a 15% reduction in char-expansion capacity within 24 months, necessitating costly reapplications. Arctic LNG terminals face challenges from cryogenic shocks, as many epoxy coatings fail at temperatures below -40°C. This has delayed permit approvals in northern Canada and Russia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coating Type: Intumescents Retain Leadership As Hybrids Accelerate

In 2025, Intumescents accounted for 43.78% of the revenue, achieving 60-180 minute ratings with just a tenth of the weight of cementitious products. This advantage is significant for seismic retrofits, which aim to limit added dead load. While starting from a smaller base, hybrids and nano-enhanced films are set to grow at a projected 6.87% compound annual growth rate (CAGR), due to their dual-mechanism protection that combines intumescence with ablative heat absorption. Cementitious layers, previously preferred for their low price, are losing ground due to their 25 mm thickness, which reduces usable floor space and complicates HVAC (heating, ventilation, and air conditioning) routing. Ablatives remain niche, catering to aerospace and naval compartments where peak heat flux surpasses 200 kilowatts per square meter (kW/m²).

Water-based intumescents gained traction following California’s 2025 volatile organic compound (VOC) cap of 50 grams per liter (g/L). They are now standard in high-rise specifications, allowing application without respirators. Jotun’s Steelmaster 1200WF, achieving ICC-ES AC23 compliance at 1,350 micrometers (µm) dry film thickness (DFT), demonstrates that eco-friendly chemistry can meet stringent performance standards. Such advancements improve profit margins and reduce installation time, positively influencing the market outlook for passive fire protection coatings.

By Technology: Solvent-Based Dominates But 100 %-Solids Epoxy Surges

In 2025, solvent-borne systems captured 34.88% of the market, especially in refurbishment jobs where near-white-metal blasting isn't feasible. However, 100% solids epoxies are on track for a 7.22% CAGR through 2031, driven by their zero-VOC credentials and the ability to return to service on the same day in occupied buildings. Water-based films face challenges in humid areas, where 80% relative humidity (RH) can extend curing beyond 72 hours, risking rain washout. Meanwhile, powder and ultraviolet (UV)-cured variants are limited to factory lines, used for automotive subframes and prefabricated steel modules, justifying their capital expenditure with electrostatic booths and UV lamps.

Starting January 2026, the European Union (EU) Industrial Emissions Directive will ban operations emitting over 50 milligrams per normal cubic meter (mg/N m³) VOC without thermal oxidizers, which come with a price tag of EUR 0.2-0.5 million (USD 0.23-0.58 million). This regulation is pushing the industry towards greater than or equal to 80% volume-solids chemistry. PPG forecasts that by 2029, these high-solids grades will make up 55% of European demand, solidifying their position in the passive fire protection coating market.

By Substrate: Steel Dominates, Wood Gains Traction

In 2025, structural steel accounted for 56.11% of coating volumes, underscoring its widespread use in skyscrapers, petrochemical plants, and rail stations. However, engineered wood, specifically cross-laminated timber and glulam, is on the rise, expanding at a 7.43% CAGR. This growth is supported by 2024 amendments to the International Building Code, which now allow 18-story mass-timber towers if they use two-hour-rated coatings for protection. Concrete needs additional films in tunnels and garages to combat hydrocarbon spill fires exceeding 1,200°C. Other substrates, like cable insulation, are carving out a niche in data centers.

Wood has distinct penetration needs; for effective anchoring as char forms, low-viscosity primers must penetrate 2-3 millimeters (mm) into the fibers. Tremco’s WB Firefilm, a hybrid acrylic-epoxy primer, achieves a commendable 15% penetration while maintaining a VOC level under 100 g/L. This positions it favorably for the growing mass-timber markets in Canada and Scandinavia. Such innovations are driving incremental growth in the passive fire protection coating market.

By Fire Scenario: Cellulosic Still Leads, Cryogenic Protection Accelerates

In 2025, standard cellulosic curves made up 50.73% of expenditures, catering to office and residential needs, where fires can reach 925°C in 60 minutes. However, cryogenic-spill coatings are set to grow at a 7.32% CAGR. With 140 liquefied natural gas (LNG) terminals under construction, there's a demand for epoxies that remain ductile at -162°C and can withstand International Organization for Standardization (ISO) 22899-1 jet-fire tests. Offshore rigs and refineries, facing hydrocarbon pool and jet fires, require coatings with faster expansion kinetics to handle temperatures that can hit 1,100°C in just five minutes.

As of 2026, fluorinated firefighting foams will be phased out globally under the Stockholm Convention. This shift is prompting aviation hangars and marine engine rooms to seek passive solutions with a three-hour rating, reallocating budgets that were previously dedicated to active suppression systems. Consequently, the passive fire protection coating market is witnessing a boost from this substitution effect, a trend not fully anticipated by traditional forecasts.

By End User Industry: Construction Dominates, Critical Infrastructure Surges

In 2025, commercial and residential projects accounted for 31.93% of expenditures, driven by high-rise offices, mixed-use towers, and multifamily blocks, contributing an annual 2.1 billion square meters (m²). However, the fastest growth, at a 7.52% CAGR, is seen in public and critical-infrastructure sectors, spanning data centers, hospitals, and transit hubs, as governments bolster defenses against potential cascading failures. The oil and gas sector remains steady, with coatings constituting 1.2-1.8% of total capital expenditure (capex) in midstream and upstream projects. Energy utilities are now specifying films to protect transformers from arc-flash temperatures reaching 10,000°C. At the same time, semiconductor fabs are on the lookout for low-outgassing coatings to prevent contamination of wafer tools.

Hyperscale data centers, especially those exceeding a 100 megawatt (MW) information technology (IT) load, are now mandated to use Underwriters Laboratories (UL) 2196-compliant coatings on cable trays, as per Google's guidelines set for Q1 2025. This requirement is driving retrofits across a significant 1.8 million m² in North America and Europe, further expanding the passive fire protection coating market's footprint in the digital-infrastructure sector.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 37.43% of the revenue and is set to grow at a 7.21% Compound Annual Growth Rate (CAGR) through 2031. Under its 14th Five-Year Plan, China allocated CNY 2.7 trillion (USD 380 billion) for urban renewal. Meanwhile, India's Smart Cities Mission is enhancing fire codes in 100 municipalities. Starting April 2025, Japan will require intumescent coatings on buildings taller than 31 meters. In January 2026, South Korea's Green Building Certification introduced bonus points for three-hour passive protection, encouraging private developers to opt for premium epoxies. These initiatives position the Asia-Pacific region as a leader in the passive fire protection coating market.

North America's growth faces challenges due to a skilled labor shortage, leading to a 15-22% increase in installation costs and extending project timelines by up to six weeks. Nevertheless, the USD 110 billion Infrastructure Investment and Jobs Act allocates funds for coatings on 18,000 bridges and 12,000 transit stations, ensuring a consistent demand valued between USD 1.8-2.4 billion. In Canada, a 2025 code update mandates two-hour ratings for timber buildings exceeding six stories, resulting in a sales surge in British Columbia and Ontario. Additionally, Mexico's maquiladora corridors now require Underwriters Laboratories (UL) 263 coatings for warehouses handling flammable goods, broadening the regional adoption.

Europe, the Middle East, and Africa are witnessing varied developments. The European Union's (EU) Q3 2027 Construction Products Regulation (CPR) revision is set to elevate compliance costs per product, favoring firms equipped with International Organization for Standardization (ISO) 17025 laboratories. In the Gulf Cooperation Council (GCC), a USD 1.3 trillion pipeline mandates two-hour ratings for all new terminals, leading to a 23% spike in coating imports in Dubai and Abu Dhabi. Conversely, Sub-Saharan Africa's adoption is limited; with fire insurance covering under 10% of building values and weak codes outside major capitals, the market for passive fire protection coatings is largely confined to government-funded hospitals and telecom hubs.

South America sees a mix of developments. Brazil's code, effective March 2025, mandates passive barriers on residential towers exceeding 23 meters, impacting 18,000 buildings. In Argentina, Buenos Aires petrochemical sites are being retrofitted to meet Instituto Argentino de Normalización y Certificación (IRAM) 11910 hydrocarbon standards. Chile's seismic resilience initiative is directing USD 2.1 billion towards intumescent upgrades until 2030.

Competitive Landscape

The passive fire protection coating market is moderately fragmented. Top companies include PPG Industries, Inc., The Sherwin-Williams Company, Akzo Nobel N.V., Jotun, and Hempel A/S. The primary competitive strategies include formulation innovation, geographic expansion, and vertical integration into application services. In Q2 2025, PPG acquired a 65% stake in a Mumbai-based applicator network for USD 18 million, securing downstream labor income and optimizing customer onboarding. In March 2026, Sherwin-Williams expanded its Coffeyville plant to increase its 100%-solids epoxy capacity, aligning with the European Union’s (EU) 2026 Volatile Organic Compounds (VOC) cap.

Regional companies such as No-Burn and Firefree Coatings secure contracts in data centers and semiconductor facilities by offering bundled ten-year adhesion warranties and rapid-cure chemistries. Digital-twin integration is emerging as a significant differentiator; PPG’s PITT-CHAR NX Internet of Things (IoT) system integrates char-thickness data into Structural-Health dashboards, enabling operators to adjust inspection schedules and reduce total ownership costs. The EU’s upcoming Construction Products Regulation (CPR) validation and the International Organization for Standardization (ISO) 17025 lab requirement may exclude formulators unwilling to invest EUR 1.5-3 million (USD 1.75-3.50 million) in accredited fire-test facilities, potentially driving consolidation and increasing barriers to entry.

Passive Fire Protection Coating Industry Leaders

The Sherwin-Williams Company

Jotun

Akzo Nobel N.V.

PPG Industries, Inc.

Hempel A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: At ADIPEC, Akzo Nobel N.V.'s International brand introduced Chartek 2218E, a low-density epoxy coating designed for offshore platforms. This product is part of the passive fire protection coating solutions, offering enhanced safety by providing thermal insulation and fire resistance.

- March 2025: Hempel A/S introduced Hempafire Extreme 550, a solvent-free passive fire protection coating certified for four-hour cellulosic fire resistance. The product is designed to be compatible with waterborne primers, offering enhanced safety and compliance for construction and industrial applications.

Global Passive Fire Protection Coating Market Report Scope

Passive fire protection coatings are materials applied to structural elements, such as steel, to insulate and delay fire spread without human intervention. These coatings form a protective char barrier, maintaining structural integrity during a fire and allowing time for evacuation.

The passive fire protection coating market is segmented by coating type, technology, substrate, fire scenario, end-user industry, and geography. By coating type, the market is segmented into intumescent coatings, cementitious coatings, ablative coatings, and hybrid/nano-enhanced coatings. By technology, the market is segmented into solvent-based, water-based, 100%-solids epoxy, and powder & UV-cured. By substrate, the market is segmented into structural steel, concrete, wood, and other substrates (plastics, cables, composites). By fire scenario, the market is segmented into cellulosic fire protection, hydrocarbon pool & jet-fire protection, and cryogenic spill protection. By end-user industry, the market is segmented into commercial & residential construction, oil & gas (up-, mid- & down-stream), energy & power (conventional & renewable), industrial manufacturing, transportation (marine, aerospace, rail), and public & critical infrastructure. The report also covers the market size and forecasts for passive fire protection coating in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Intumescent Coatings |

| Cementitious Coatings |

| Ablative Coatings |

| Hybrid/Nano-enhanced Coatings |

| Solvent-based |

| Water-based |

| 100%-Solids Epoxy |

| Powder & UV-cured |

| Structural Steel |

| Concrete |

| Wood |

| Other Substrates (Plastics, Cables, Composites) |

| Cellulosic Fire Protection |

| Hydrocarbon Pool & Jet-Fire Protection |

| Cryogenic Spill Protection |

| Commercial & Residential Construction |

| Oil & Gas (Up-, Mid- & Down-stream) |

| Energy & Power (Conventional & Renewable) |

| Industrial Manufacturing |

| Transportation (Marine, Aerospace, Rail) |

| Public & Critical Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of APAC | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East & Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East & Africa |

| By Coating Type | Intumescent Coatings | |

| Cementitious Coatings | ||

| Ablative Coatings | ||

| Hybrid/Nano-enhanced Coatings | ||

| By Technology | Solvent-based | |

| Water-based | ||

| 100%-Solids Epoxy | ||

| Powder & UV-cured | ||

| By Substrate | Structural Steel | |

| Concrete | ||

| Wood | ||

| Other Substrates (Plastics, Cables, Composites) | ||

| By Fire Scenario | Cellulosic Fire Protection | |

| Hydrocarbon Pool & Jet-Fire Protection | ||

| Cryogenic Spill Protection | ||

| By End-user Industry | Commercial & Residential Construction | |

| Oil & Gas (Up-, Mid- & Down-stream) | ||

| Energy & Power (Conventional & Renewable) | ||

| Industrial Manufacturing | ||

| Transportation (Marine, Aerospace, Rail) | ||

| Public & Critical Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of APAC | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East & Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How large will the passive fire protection coating market be by 2031?

The Passive Fire Protection Coating Market size is expected to grow from USD 4.86 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 7.12 billion by 2031 at 6.57% CAGR over 2026-2031.

Which coating type holds the largest share?

Intumescent coating led with 43.78% of the passive fire protection coating market share in 2025.

What technology segment is growing fastest?

100%-Solids epoxy systems are forecast to post the highest 7.22% CAGR through 2031.

Which region will expand most quickly?

Asia-Pacific is expected to rise at a 7.21% CAGR on sustained urban-infrastructure spending.

Page last updated on: