Thermal Insulation Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 83.3 Billion |

| Market Size (2031) | USD 107.93 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

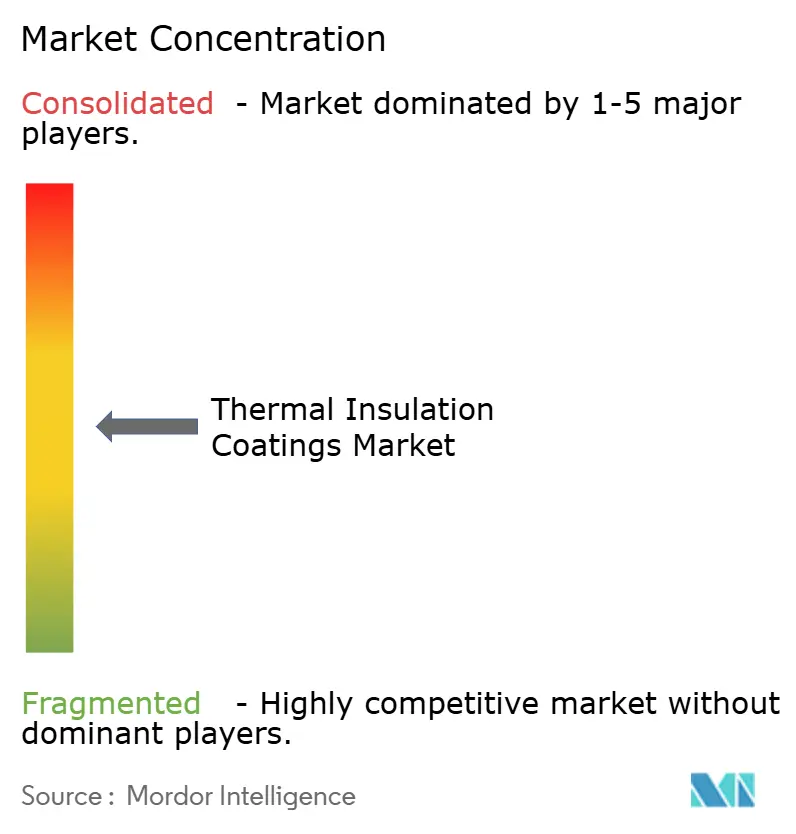

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermal Insulation Coatings Market Analysis by Mordor Intelligence

The Thermal Insulation Coatings Market size was valued at USD 79.09 billion in 2025 and estimated to grow from USD 83.3 billion in 2026 to reach USD 107.93 billion by 2031, at a CAGR of 5.32% during the forecast period (2026-2031). This performance signals sustained demand that now stretches far beyond conventional construction use cases and into electrified process-heat systems, LNG infrastructure, and battery thermal management. Enforceable energy-efficiency codes, mounting decarbonization mandates, and the build-out of fourth-generation district-heating grids across Europe are accelerating the adoption of advanced thermal barriers capable of service temperatures above 1,200 °C. In parallel, Asia-Pacific’s industrial expansion is widening the customer base for high-performance coatings in refineries, petrochemicals, and automotive components, while North American aerospace programs are stimulating uptake of ultra-high-temperature yttria-stabilized zirconia (YSZ) systems. The resulting competitive environment rewards suppliers that combine vertical integration with materials science advances, such as hybrid aerogel-epoxy formulations that deliver sub-0.020 W m-¹ K-¹ thermal conductivity.

Key Report Takeaways

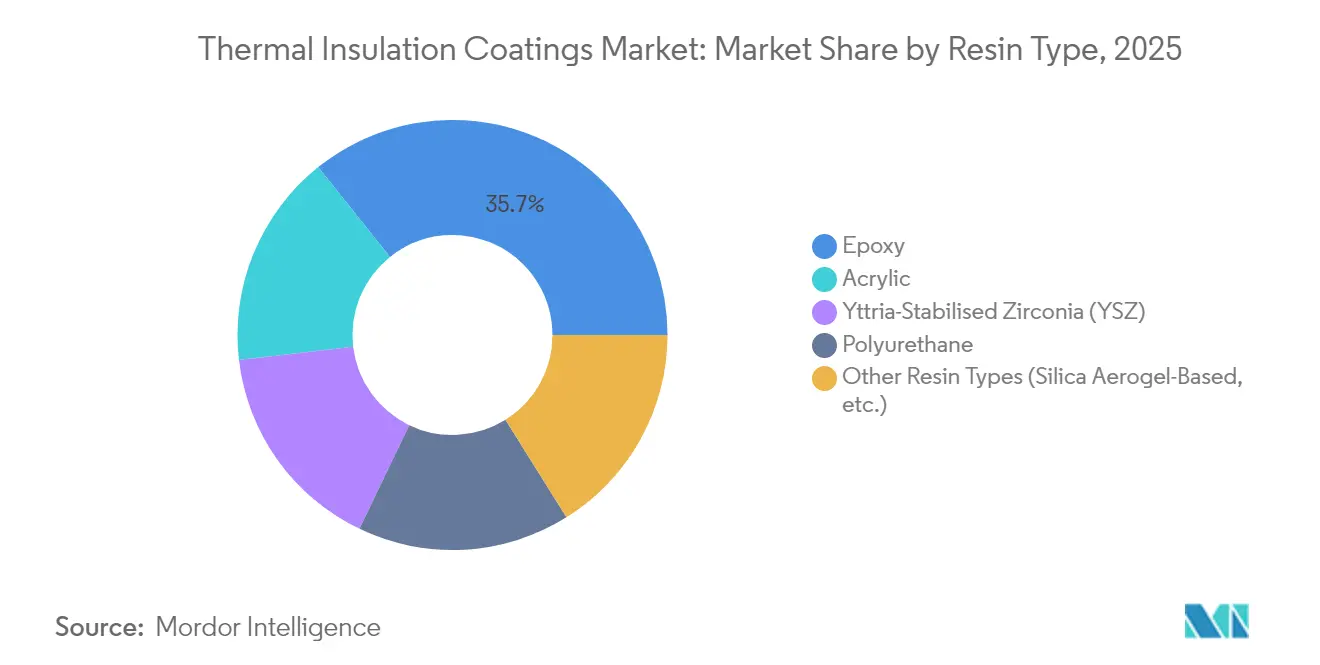

- By resin type, epoxy formulations led with 35.74% of thermal insulation coatings market share in 2025; silica-aerogel coatings are projected to expand at a 5.74% CAGR through 2031.

- By coating form, liquid spray systems accounted for 44.72% share of the thermal insulation coatings market size in 2025 and are growing at a 6.21% CAGR to 2031.

- By application, building envelope solutions held 42.05% of the thermal insulation coatings market share in 2025, whereas automotive components will record the fastest 6.68% CAGR through 2031.

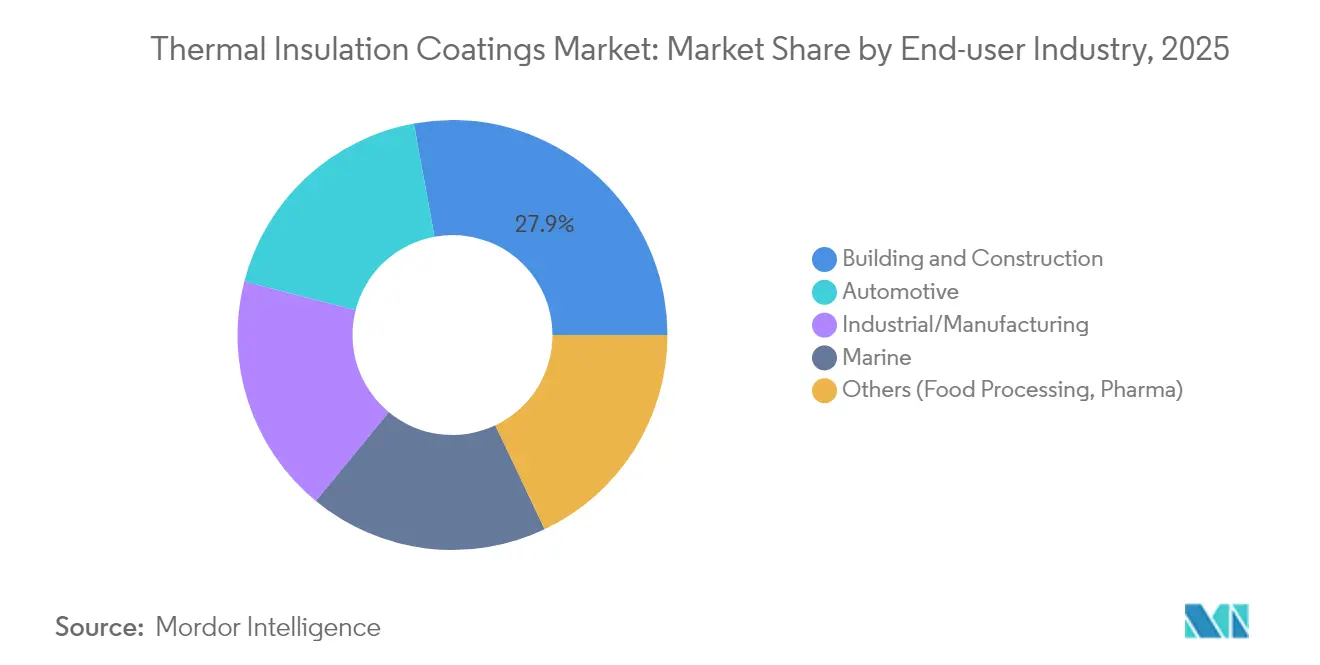

- By end-user industry, building and construction represented 27.88% of the thermal insulation coatings market size in 2025, while other end-user industries are growing fastest at a CAGR of 5.83%.

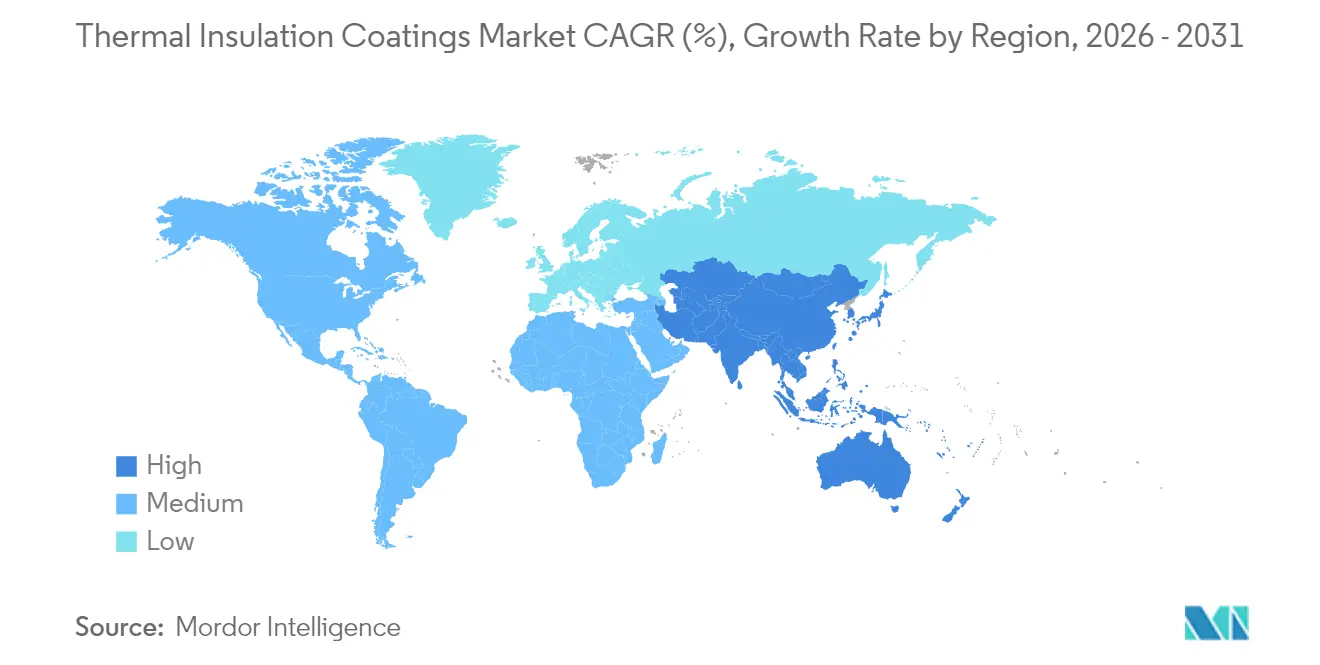

- By geography, Asia-Pacific commanded 39.62% revenue share in 2025, while also registering the highest regional CAGR of 5.96% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermal Insulation Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction of new refineries | +1.2% | Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Expansion of district heating and cooling networks | +0.8% | Europe, North America | Long term (≥ 4 years) |

| Increasing demand for construction industry | +1.5% | Global | Short term (≤ 2 years) |

| Electrification of process heat in heavy industry | +0.9% | Europe, North America | Long term (≥ 4 years) |

| Surge in LNG cold-chain logistics | +0.6% | Asia-Pacific, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction of New Refineries

Global refinery buildouts continue to anchor the thermal insulation coatings market. New complexes in India, China, and the Arabian Gulf specify multilayer epoxy barriers for distillation towers and heat-exchanger shells that run between 200 °C and 800 °C. Project owners increasingly bundle corrosion resistance and digital thickness monitoring into the same coating package to curb unplanned outages and extend asset life. Suppliers that can certify systems for both normal and cyclic temperature environments gain access to the largest capital projects pipeline.

Expansion of District Heating and Cooling Networks

Fourth-generation district-heating grids operate at lower supply temperatures, demanding coatings capable of reducing distribution losses while surviving repetitive thermal cycling. Denmark’s municipal energy cooperatives demonstrate that advanced insulation can shave multiple percentage points from annual heat losses, thereby improving heat-pump efficiency. Similar retrofits across Germany and Sweden specify aerogel-infused primers to meet the stricter heat-retention targets.

Increasing Demand for Construction Industry

Stringent 2024 building-energy codes tighten R-value thresholds for wall assemblies and roofing systems. Spray-applied ceramic microsphere coatings meet new prescriptive paths without increasing wall thickness, making them popular in dense urban retrofits. Building-information-modeling workflows now embed coating-layer data to predict summer peak-load reductions and optimize HVAC sizing. Turkey’s two-year payback studies on climate-adaptive envelope strategies further validate commercial viability.

Electrification of Process-Heat in Heavy Industry

High-temperature heat pumps and resistance-heated furnaces alter thermal-cycling profiles, prompting demand for coatings that tolerate rapid ramp-ups to 250 °C. Demonstration plants in the Netherlands apply multilayer alumina-bond-coat systems topped with YSZ to maximize refractory life. Pilot projects use phase-change-material backfills to capture off-cycle heat, positioning coatings as integral to storage performance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital requirement | –0.7% | Global | Short term (≤ 2 years) |

| Volatile raw-material (epoxy and PU) prices | –0.5% | Global | Medium term (2-4 years) |

| Limited applicability in ultra-high-temperature assets | –0.3% | Industrial regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Requirement

Plasma-spray booths, automated gantries, and controlled-atmosphere curing ovens can cost several million USD, limiting new-entrant capacity. Large integrated producers therefore dominate long-run supply contracts, while smaller applicators face financing hurdles. Portfolio restructuring, as seen in recent divestiture discussions inside diversified chemistry groups, underscores capital intensity pressures.

Volatile Raw-Material (Epoxy and PU) Prices

Epoxy and polyurethane feedstocks track crude-oil price movements, exposing coaters to margin swings. Supply disruptions amplify risks because specialty resins rely on a handful of global producers. Some formulators lock in multi-year supply contracts or pursue backward integration, but such hedging demands sizeable balance-sheet flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Epoxy Dominance Faces Aerogel Challenge

Epoxy systems retained a 35.74% share of the thermal insulation coatings market in 2025, buoyed by strong adhesion and chemical resistance that suit refinery piping, marine deck plates, and offshore platforms. They underpin a significant portion of the thermal insulation coatings market size for protective-lining projects scheduled across APAC and the Middle East. Enhanced formulations embed hollow-glass microspheres to bring thermal conductivity below 0.180 W m-¹ K-¹ without sacrificing film toughness.

Silica-aerogel coatings, while holding only single-digit revenue today, record a 5.74% CAGR to 2031. Ultra-low conductivity readings of 0.015 W m-¹ K-¹ unlock ambient-pressure applications that once demanded vacuum-insulated panels. Manufacturers co-disperse aerogel powder into epoxy matrices to combine mechanical strength with near-super-insulating performance, giving the segment outsized influence on future specifications. At the aerospace frontier, entropy-stabilized oxide and YSZ platforms target turbine-blade skins running above 1,200 °C, suggesting further technology crossover opportunities.

By Coating Form: Liquid Spray Technology Leads Innovation

Liquid spray lines captured 44.72% of thermal insulation coatings market share in 2025 and continue to outpace other forms at a 6.21% CAGR. Their chief advantages include seamless coverage on weld seams and radius bends, plus production-rate gains from robot-integrated spray heads. Process yards now deploy vision analytics to gauge wet-film thickness and self-correct gun speed, minimizing overspray and improving yield. Powder lines remain relevant in gridshell architecture and certain pipeline externals where electrostatic attraction ensures uniform film builds.

By Application: Building Envelope Leadership Amid Automotive Surge

The building segment controlled 42.05% of the thermal insulation coatings market in 2025 as architects adopt coatings that deliver double-digit surface-temperature drops and contribute toward net-zero-energy targets. High-reflectance ceramic products achieve 10 °C roof surface reductions in peak summer, lowering cooling loads in Mediterranean and Gulf climates.

Automotive systems present the fastest growth path at 6.68% CAGR. Electric-vehicle pack designs favor thin dielectric layers offering both thermal isolation and puncture resistance. Functions extend beyond batteries to motor housings and inverter casings, where low-density ceramic fillers improve acoustic damping. Industrial equipment, storage tanks, and marine shells continue to command staple demand. Advanced deck-coating lines claim measurable fuel savings by pairing drag-reduction topcoats with thermally insulating under-layers.

By End-user Industry: Oil and Gas Leads Amid Diversification

Building and construction accounted for 27.88% of the thermal insulation coatings market size in 2025, supported by sustained refinery maintenance cycles and new LNG export terminals. Mandates to cut fugitive methane emissions elevate pipeline insulation specifications, as cooler external pipe walls reduce soil heating and associated microbial corrosion. Building and construction follow closely, fuelled by stricter code enforcement and green-building certification schemes.

The thermal insulation coatings industry increasingly caters to diversified sectors: advanced manufacturing embraces heat-pump and thermal-storage packages, food processors insulate aseptic tanks to stabilize fermentation profiles, and pharmaceutical freeze-dryers turn to cryogenic-rated layers for sub-zero reliability. Such breadth buffers the market against single-sector downturns and fertilizes cross-disciplinary innovation.

Geography Analysis

Asia-Pacific holds 39.62% of 2025 revenue, reflecting megaproject pipelines in China, India, and South Korea. Regional governments prioritize refinery self-sufficiency, which directly inflates the thermal insulation coatings market. Added momentum comes from LNG cold-chain terminals in Japan and floating storage regasification units serving Southeast Asian islands.

North America is assisted by aerospace propulsion programs and process-heat electrification pilots in heavy industry alleys. Federal stimulus packages encourage district-energy retrofits, steering municipal utilities toward advanced coating overlays that lower distribution losses. Regulations like Canada’s National Energy Code for Buildings 2020, which lifts thermal-resistance requirements for wall assemblies, anchor recurrent demand for spray-applied ceramic microsphere products.

Europe maintains leadership in policy-driven decarbonization and commands the densest district-heating market, fostering continuous specification upgrades for coatings with validated ex-situ thermal-cycling endurance. Scarcity of new-build heavy industry shifts focus to retrofitting aging industrial parks with high-temperature heat-pump systems, where coatings moderate conductive losses on hot-oil loops. Meanwhile, the Middle-East and Africa leverages oil-capex programs to expand adoption in petrochemical parks, whereas South America’s mining belts employ coatings to buffer process vessels against aggressive acids and wide daily temperature swings.

Competitive Landscape

The thermal insulation coatings market is characterized by moderate fragmentation: global multinationals such as AkzoNobel, PPG Industries, and Sherwin-Williams coexist with highly specialized mid-tier firms. Global players leverage branded distribution, integrated raw-material backbones, and digital color-matching suites to command prime positioning on multi-site contracts.

Thermal Insulation Coatings Industry Leaders

Jotun

AkzoNobel N.V.

BASF

PPG Industries, Inc.

The Sherwin-Williams Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Oerlikon and MTU Aero Engines advanced their collaboration to establish a state-of-the-art thermal-spray factory aimed at lifting productivity and embedding digital quality controls in aerospace component production.

- March 2024: Hempel A/S introduced Hempatherm IC, a two-part thermal insulation coatings system designed to replace conventional insulation in the corrosion-under-insulation temperature range, extending equipment service life.

Global Thermal Insulation Coatings Market Report Scope

Thermal insulation coatings have a broad range of use. They can actually reduce temperatures across the medium in either direction. That is, they can actually keep heat in like insulation. The thermal insulation coatings market is segmented by resin and end-user industry. By resin market is segmented by acrylic, epoxy, polyurethane, yttria-stabilized zirconia, and other resins, and in terms of end-user industry segmentation is done in terms of building and construction, industrial/manufacturing, automotive, marine, and other end-user industries. The report also covers the market size and forecasts for the thermal insulation coatings market in 15 countries across major regions. The report offers market size and forecasts for thermal insulation coatings in terms of revenue (USD million) for all the above segments.

| Acrylic |

| Epoxy |

| Polyurethane |

| Yttria-Stabilised Zirconia (YSZ) |

| Other Resin Types (Silica Aerogel-Based, etc.) |

| Liquid Spray |

| Powder |

| Vacuum-Deposited |

| Building Envelope (Walls, Roofs) |

| Industrial Equipment and Pipelines |

| Storage Tanks and Vessels |

| Automotive Components |

| Marine Hull and Deck Structures |

| Aerospace and Turbine Parts |

| Building and Construction |

| Industrial/Manufacturing |

| Automotive |

| Marine |

| Others (Food Processing, Pharma) |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Acrylic | |

| Epoxy | ||

| Polyurethane | ||

| Yttria-Stabilised Zirconia (YSZ) | ||

| Other Resin Types (Silica Aerogel-Based, etc.) | ||

| By Coating Form | Liquid Spray | |

| Powder | ||

| Vacuum-Deposited | ||

| By Application | Building Envelope (Walls, Roofs) | |

| Industrial Equipment and Pipelines | ||

| Storage Tanks and Vessels | ||

| Automotive Components | ||

| Marine Hull and Deck Structures | ||

| Aerospace and Turbine Parts | ||

| By End-user Industry | Building and Construction | |

| Industrial/Manufacturing | ||

| Automotive | ||

| Marine | ||

| Others (Food Processing, Pharma) | ||

| By Geography | Asia Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the present valuation of the thermal insulation coatings market?

The thermal insulation coatings market is valued at USD 83.3 billion in 2026.

Which resin category commands the largest share?

Epoxy-based coatings lead with 35.74% share in 2025, owing to their robustness in harsh industrial settings.

Which geographic region is expanding fastest?

Asia-Pacific grows at a 5.96% CAGR through 2031, supported by refinery buildouts and LNG infrastructure investments.

What application area is recording the highest growth?

Automotive components exhibit a 6.68% CAGR as electric-vehicle battery packs demand advanced thermal management.

How are district-heating upgrades influencing demand?

Fourth-generation grids require coatings that curb distribution losses, thereby lifting demand for aerogel-enhanced insulation.

Page last updated on: