Corrosion Protection Polymer Coating Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

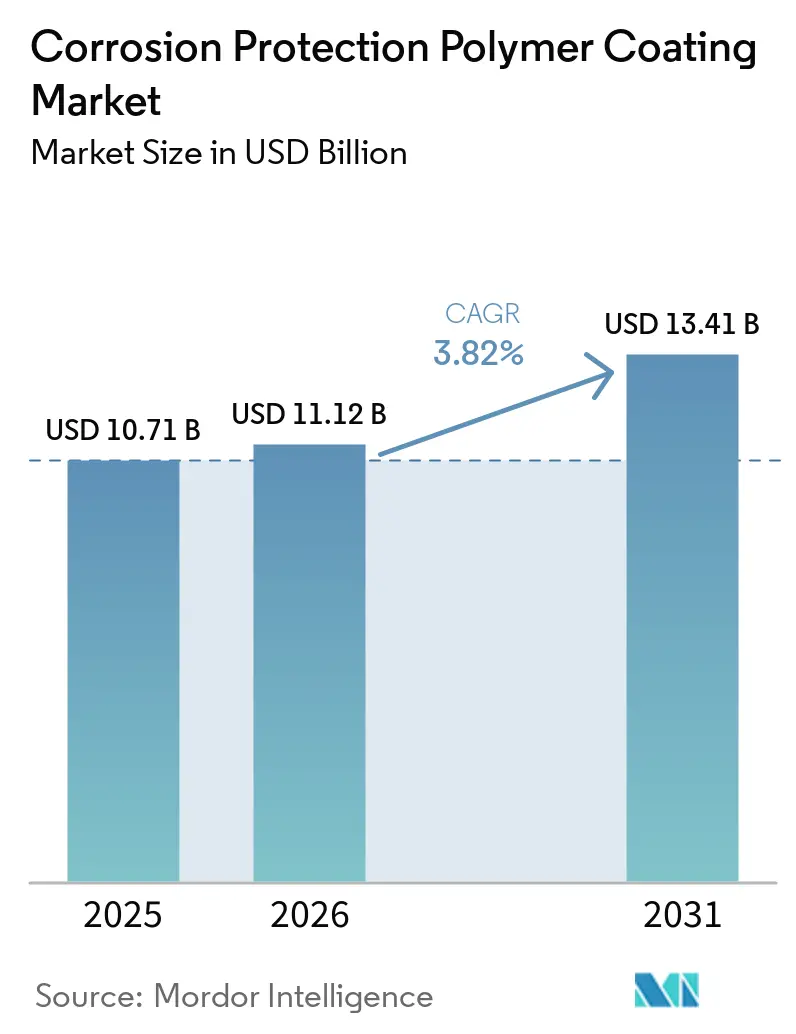

| Market Size (2026) | USD 11.12 Billion |

| Market Size (2031) | USD 13.41 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrosion Protection Polymer Coating Market Analysis by Mordor Intelligence

The Corrosion Protection Polymer Coating Market size is expected to grow from USD 10.71 billion in 2025 to USD 11.12 billion in 2026 and is forecast to reach USD 13.41 billion by 2031 at 3.82% CAGR over 2026-2031. As the focus shifts from merely replacing corroded assets to extending their service life, advanced coating systems are becoming increasingly prominent. These systems offer remarkable durability, particularly in challenging environments such as splash zones and deep-water settings. The urgency for this durability is heightened by a looming labor shortage in the United States, where a significant shortfall of infrastructure workers has made qualified re-application crews a rare find. Investments are increasingly flowing into fluoropolymer chemistries, celebrated for their resilience against chloride attacks and adherence to hydrogen purity standards, especially in offshore power-to-X plants. In this competitive arena, suppliers who blend low-VOC platforms with digital twin maintenance tools are reaping the rewards, as asset owners gravitate toward predictive models over traditional calendar-based inspections.

Key Report Takeaways

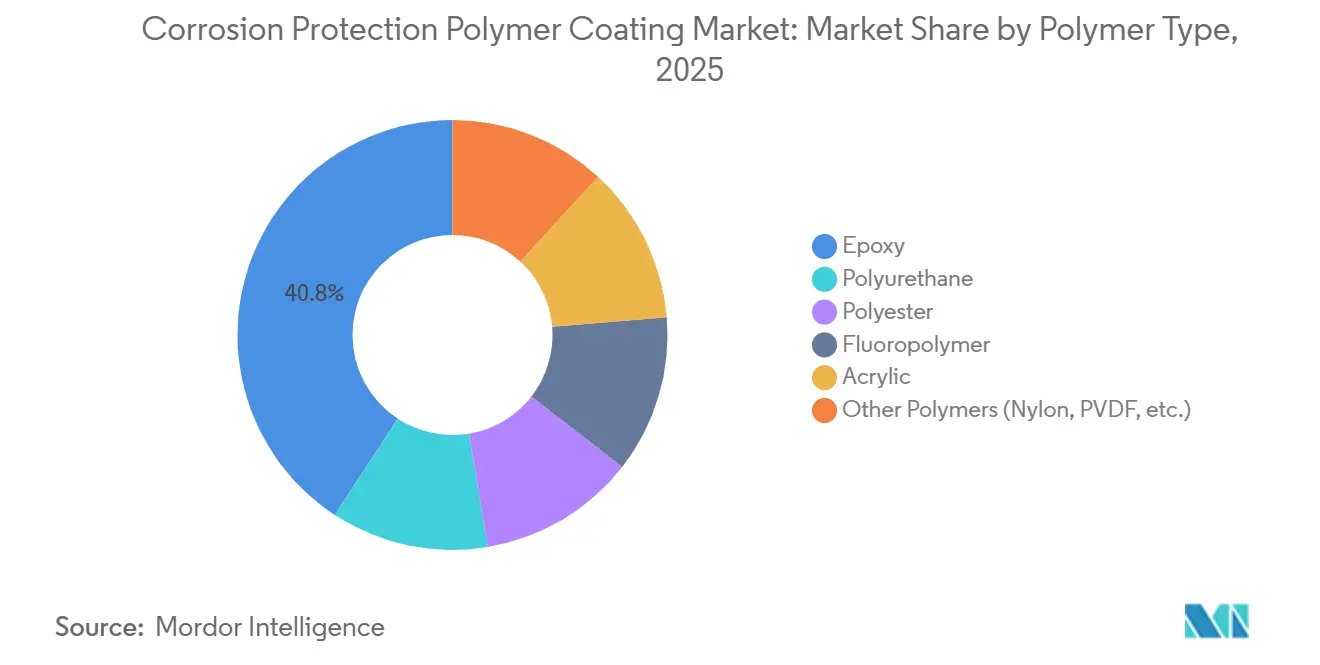

- By polymer type, epoxy systems led with 40.78% revenue share in 2025, while fluoropolymer coatings are projected to expand at a 4.57% CAGR through 2031.

- By formulation, solvent-borne products accounted for 44.68% of 2025 revenue, while powder coatings are advancing at a 4.68% CAGR over 2026-2031.

- By technology, thermosetting chemistries represented 61.19% of 2025 revenue; thermoplastic systems are set to grow at a 4.83% CAGR to 2031.

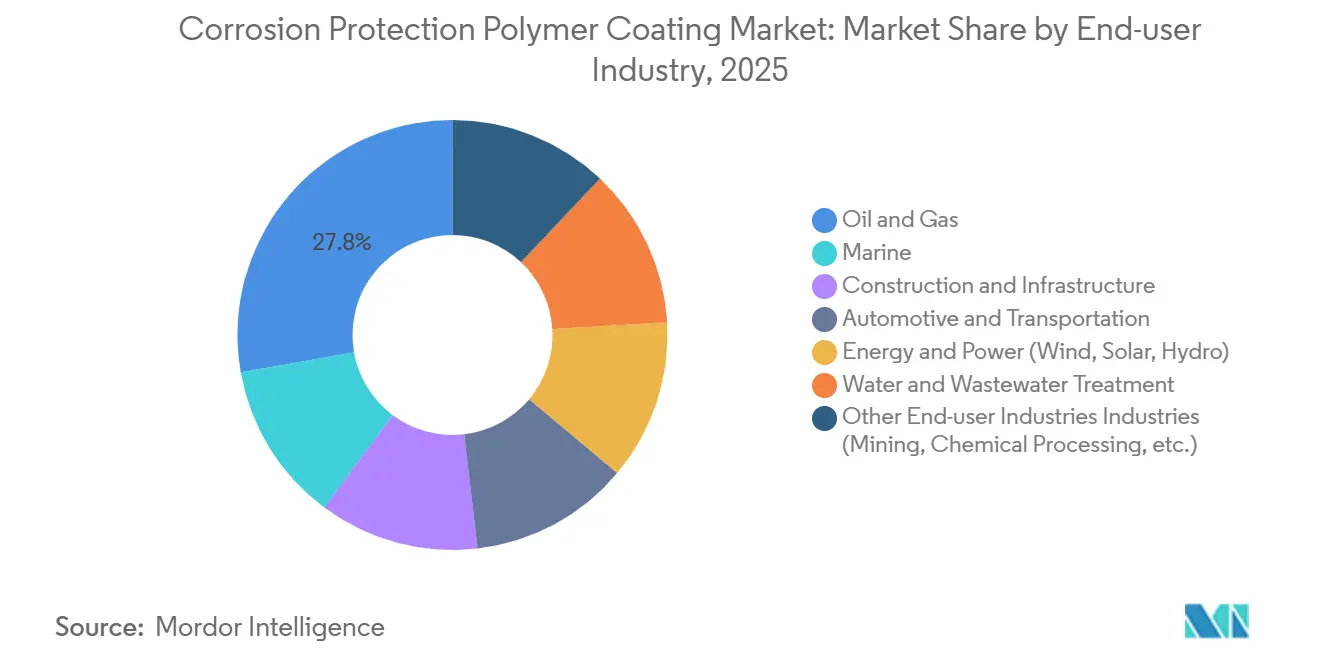

- By end-user, oil and gas installations captured 27.78% demand in 2025, yet energy and power assets register the fastest 5.03% CAGR during 2026-2031.

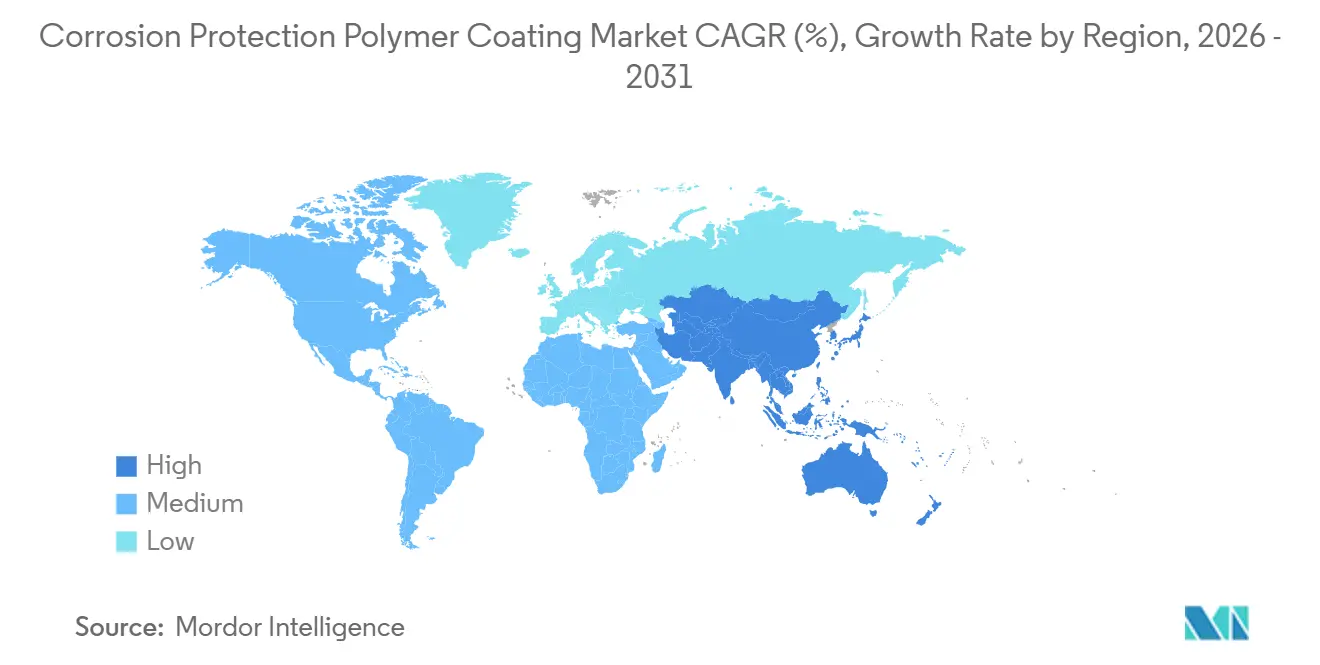

- By geography, Asia-Pacific generated 44.78% revenue in 2025 and is forecast to expand at a 4.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corrosion Protection Polymer Coating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure boom in emerging economies | +1.20% | Asia-Pacific core, spill-over to Middle-East and South America | Medium term (2-4 years) |

| Shift toward asset-life extension and lifecycle-cost reduction | +0.90% | Global, early uptake in North America and Europe | Long term (≥ 4 years) |

| Offshore renewable H₂/NH₃ projects in corrosive sites | +0.60% | North Sea, Middle-East, Australia, pilot activity in Asia-Pacific | Long term (≥ 4 years) |

| Digital-twin-driven predictive maintenance uptake | +0.40% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Naval modernization need for low-magnetic coatings | +0.30% | United States, China, India, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Boom in Emerging Economies

In 2026, China approved projects encompassing airports, cross-sea ferries, UHV grids, and hydropower, all of which necessitate long-term corrosion protection. Meanwhile, India’s National Infrastructure Pipeline has allocated a substantial budget for energy and roads, bolstering the demand for epoxy and polyurethane systems that comply with ISO 12944 C5-M standards[1]NITI Aayog, “National Infrastructure Pipeline,” niti.gov.in . Multilateral lending has increased private infrastructure investments in emerging markets. In Latin America and Sub-Saharan Africa, deferred-maintenance backlogs often exceed significant portions of asset values, prompting owners to adopt high-build coatings to delay replacements. Growth in greenfield FDI into infrastructure highlights the rising influence of private capital in shaping regional specifications, often aligning with public budgets. The shift towards international standards benefits global suppliers with certified laboratories, while disadvantaging local players lacking third-party data.

Shift Toward Asset-Life Extension and Lifecycle-Cost Reduction

Sherwin-Williams demonstrated that a slightly higher upfront cost for a long-term system can result in substantial savings in total ownership costs, particularly when labor and downtime are considered. BioBond emphasized that preventive maintenance can lead to significant savings compared to reactive repairs and emergency replacements, reinforcing the importance of long-life coatings. Offshore hydrogen and ammonia projects, such as SwitcH2’s Atlantico, have moved away from lower-grade epoxies, opting instead for PVDF and PTFE topcoats. Wärtsilä’s floating ammonia cracker integrates corrosion-resistant alloys with polymer linings designed to withstand both cryogenic ammonia and seawater. Procurement trends now prioritize “best value over asset life,” encouraging suppliers to provide electrochemical impedance data rather than relying solely on film-thickness metrics.

Offshore Renewable H₂/NH₃ Projects in Corrosive Sites

SwitcH2’s FPSOs, located in high-salinity splash zones, integrate seawater electrolysis, Haber-Bosch synthesis, and cryogenic storage. These zones present challenges for conventional marine epoxies, which are prone to amine sensitivity and hydrogen permeation. Wärtsilä’s offshore cracker requires fluoropolymer linings capable of resisting both liquid ammonia and the risks of hydrogen embrittlement. The Global Wind Energy Council forecasts significant growth in offshore wind capacity during the 2026-2031 period. Standards such as ISO 24656:2022 mandate specific dry film thicknesses in splash zones, a niche where thermoplastic powders and high-build epoxies excel. Regions such as the North Sea, Middle-East, and Australia, with their power-to-x ambitions, are driving demand for suppliers with fluoropolymer expertise.

Digital-Twin-Driven Predictive Maintenance Uptake

An SAE paper successfully modeled an automotive e-coat line, predicting thin zones before inspection and thereby reducing scrap. This digital twin approach, when combined with embedded electrochemical impedance sensors, enables asset owners to transition from fixed cycles to condition-based recoats, thereby extending service life. The U.S. Navy is testing fleet-wide digital twins that integrate hull-coating conditions with cathodic-protection currents to reduce corrosion costs. Companies such as Nordson and Gema are utilizing closed-loop powder lines that document film build and cure temperatures, generating auditable data for warranty claims. Although only a small percentage of coating projects currently deploy such sensors, early adopters have reported significantly fewer unplanned outages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC/HAP emission regulations | -0.50% | North America and Europe, rising in Asia-Pacific | Short term (≤ 2 years) |

| Global shortage of certified applicators | -0.30% | Global, acute in North America, Europe, Middle-East | Medium term (2-4 years) |

| Lengthy qualification cycles for novel systems | -0.20% | Global, especially the oil and gas and nuclear sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC/HAP Emission Regulations

In January 2025, the U.S. EPA capped VOCs in aerosol coatings, granting an extension for compliance until January 2027[2]U.S. Environmental Protection Agency, “National Emission Standards for Aerosol Coatings,” epa.gov . This move required swift reformulations in the industry. Meanwhile, in February 2026, the EU tightened Ecolabel rules, introducing a lifecycle carbon footprint threshold that favors water-borne and powder products. North Carolina demonstrates how state regulations can exceed federal limits, leading to the need for multiple SKU variants across jurisdictions. The financial burden of reformulation is significant, accompanied by a lengthy testing period, which poses challenges, particularly for smaller players. As a result, coal-tar enamels and high-solvent epoxy mastics are losing market share to high-solids polyurethanes and powder systems, which meet both emissions and performance standards.

Global Shortage of Certified Applicators

Launched in March 2026, AMPP’s TalentForce aims to address the skills gap through apprenticeships and stackable credentials. The industry is experiencing labor attrition in blasting, spraying, and inspection trades, alongside growing certification demand. In the Middle-East, project delays have increased due to a shortage of AMPP-qualified crews. In response, owners are selecting long-lasting coatings to reduce lifecycle touchpoints. Suppliers, recognizing the challenge, have started operating training academies in collaboration with AMPP to ensure a steady labor pipeline.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Polymer Type: Fluoropolymers Capture High-Value Offshore Projects

In 2025, epoxy systems dominated the corrosion protection polymer coating market, capturing 40.78% of sales, thanks to their long-proven track record in pipelines and ballast tanks. While fluoropolymer volumes remain modest, they are projected to achieve a 4.57% CAGR during the forecast period of 2026-2031. This growth is driven by the demand for PVDF and PTFE in offshore hydrogen and ammonia platforms, where tolerance to chloride spray and process purity is paramount. Between 2026 and 2031, fluoropolymers are set to surpass other polymer groups in the corrosion protection market, bolstered by their premium pricing and compliance with stringent standards. Polyurethanes, prized for their UV resilience, are the preferred choice for façade metals and automotive topcoats. However, their sensitivity to moisture in humid conditions limits their use in marine applications. On the other hand, polyester leads in household appliances and HVAC systems, with bio-attributed resins playing a pivotal role in significantly reducing embodied carbon.

Field data underscores a rising interest in thermoplastic liners. United Pipeline Systems has rolled out extensive miles of HDPE Tite Liner, a move that avoids the weld-zone holidays common with fusion-bonded epoxy. Research into PU/PTFE/cellulose nanofiber composites indicates a trend toward single-coat solutions, departing from the conventional multi-layer stacks. This evolution aligns with the owner's goals of minimizing field operations. Today's supply chain focus has shifted to lifecycle data, moving beyond just initial adhesion tests. As a result, suppliers are now tasked with monitoring installed coatings via EIS sensors and supplying third-party salt-spray performance data for tender bids.

By Formulation: Powder Coatings Strengthen on VOC and Carbon Rules

In 2025, solvent-borne systems commanded a 44.68% share of the revenue in the corrosion protection polymer coating market, valued for their thick single-coat application and ease of field repairs. However, tightening regulations from the EPA and EU have stymied their expansion, steering buyers toward high-solids and exempt-solvent blends. Powder coatings, enjoying a 4.68% CAGR during the forecast period of 2026-2031, benefit from dust-on-dust technology that reduces curing steps and bio-attributed polyesters, which are gaining traction due to green building credits. Significantly, powder coatings are increasingly favored in the appliance and construction sectors, where attributes such as low odor and overspray reclamation are in high demand.

Water-borne epoxies are the preferred choice for potable water applications and interiors requiring low odor. However, their slow curing times in chilly marine yards present challenges. High-solids novolacs strike a commendable balance between performance and regulatory compliance, but they come with the caveat of requiring heated plural pumps and a proficient workforce. A 2026 study unveils self-healing powders laced with PDMS microcapsules, boasting the potential to double service life and penetrate infrastructure markets, traditionally the realm of solvent-based epoxies. Furthermore, factory automation systems are now adeptly tracking cure temperatures and film builds, generating data for ESG audits that highlight commendable reductions in waste and energy use.

By Technology: Thermoplastics Advance in Seamless Pipeline Barriers

In 2025, thermosetting chemistries accounted for 61.19% of the revenue in the corrosion protection polymer coating market. Networks such as epoxy, polyurethane, and polyester, known for their resistance to solvents and heat, play a pivotal role in applications ranging from refineries to ballast tanks. The demand for thermoplastics is increasing, growing at a rate of 4.83% annually. This growth is primarily driven by HDPE and PP liners, which create joint-free barriers within pipelines, effectively eliminating corrosion hotspots at girth welds. The thermoplastic systems market for pipeline coatings is expected to grow steadily during the forecast period of 2026-2031, supported by the adoption of standards such as ISO 21809 and CAN/CSA Z245.21.

Hybrid stacks, which combine epoxy primers with thermoplastic topcoats, are setting new benchmarks in impact resistance and flexibility. Deep-water projects now specify syntactic polypropylene layers, engineered to withstand temperatures of up to 140 degrees Celsius and depths of up to 3,000 meters. A key feature of these coatings is their reparability; technicians can seamlessly heat-fuse damaged sections, avoiding the need for blasting. This capability is especially critical in scenarios where certified applicators are in limited supply.

By End-User Industry: Energy and Power Emerges as Fastest Riser

Oil and gas accounted for 27.78% of the 2025 demand, underscoring the sector's entrenched legacy. However, the energy and power sector is outpacing with a growth rate of 5.03% CAGR during the forecast period of 2026-2031. This surge is driven by the offshore wind and solar industries' requirement for 1,000-micron systems to comply with ISO 12944-9 and ISO 24656 duty cycles. As a result, the corrosion protection polymer coating market for energy and power is expanding at a faster pace than its oil and gas counterpart, fueled by a projected boost in offshore wind capacity by 2030. Simultaneously, marine fleets are adopting foul-release silicone hull coatings to minimize drag and counteract corrosion.

In the construction sector, users are gravitating towards durable rebar and bridge steels, meticulously considering lifecycle costs. In the automotive sector, there is a push towards lightweighting to curtail coating areas. This shift has tempered volume growth, even as powder clearcoats gain traction. While niche, the water treatment and mining sectors maintain a steady reliance on chemical-resistant linings and abrasion shields.

Geography Analysis

In 2025, the Asia-Pacific dominated the corrosion protection polymer coating market, accounting for 44.78% of the revenue and projecting a 4.55% CAGR during the forecast period of 2026-2031. China's public works and India's infrastructure initiatives are driving up the demand for epoxy and polyurethane, even as the region tightens its VOC regulations. To cater to the growing demand in appliances and two-wheelers, local giants like Berger Paints and Kansai Nerolac are broadening their plant operations. As companies diversify their supply chains, ASEAN hubs are emerging as prime locations for factory investments. A notable example is PPG's expansion of its industrial coatings site in Vietnam, highlighting its confidence in the region.

North America is capitalizing on federal funding for bridges, water projects, and Atlantic offshore wind initiatives. While the EPA's VOC caps challenge formulators, PPG's major investments in a Carolina aerospace site and an Ohio automotive expansion signal their trust in the region's potential. Canada's oil-sands pipelines, favoring fusion-bonded epoxy, face approval hurdles, prompting a shift in focus towards maintenance recoats. Simultaneously, Mexican automotive hubs are seeing a rise in powder and e-coat volumes, largely due to near-shoring trends.

Europe's tightening Ecolabel is pushing solvent lines towards specialized applications. The North Sea and Baltic regions' expanding offshore wind projects are boosting the demand for thick-build epoxies and thermoplastic powders, especially with the ISO 24656 mandate. The potential merger of AkzoNobel and Axalta could alter market dynamics, but it also offers a chance to pool research and development resources, especially for low-carbon formulations. Eastern Europe's macroeconomic challenges are slowing growth, yet increased defense spending is spurring demand for naval coatings in Poland and Norway. In the Middle-East, ambitious projects like NEOM are necessitating systems resilient to the desert's UV rays and thermal shocks. Meanwhile, Africa's port and mining sectors are experiencing demand fluctuations, closely linked to global commodity trends.

Competitive Landscape

The corrosion protection polymer coatings market is moderately fragmented. Major players like PPG, Sherwin-Williams, AkzoNobel, Jotun, and Hempel dominate the corrosion protection polymer coatings market. The AkzoNobel-Axalta partnership, with its considerable revenue, is poised to challenge PPG's stronghold in the marine sector, eyeing a swift closure. The industry's competitive landscape is increasingly centered on sustainability, digital services, and broadening geographic reach. BASF, AkzoNobel, and Arkema are at the forefront, supplying bio-attributed polyester resins that significantly cut carbon emissions, giving them a competitive edge in LEED projects. In a strategic move, Sherwin-Williams rolled out OneCure powder, enabling a dual application of primer and topcoat, thereby drastically reducing line downtime.

Digital integration stands out as a key differentiator in the market. SAE's virtual paint-shop models not only minimize scrap but also hasten validation. Nukote, leveraging predictive analytics, boasts a marked decrease in outages. AMPP’s Coatings Inspector Program enhances application quality and indirectly benefits co-sponsoring suppliers through elevated training standards. While regional specialists enjoy advantages with quick turnarounds and services in local languages, they face consolidation challenges as global players advocate for uniform, low-VOC, ISO-certified products across the globe.

Corrosion Protection Polymer Coating Industry Leaders

Akzo Nobel N.V.

Jotun

PPG Industries, Inc.

The Sherwin-Williams Company

Hempel A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Akzo Nobel N.V. and Axalta Coating Systems Ltd. have signed a definitive all-stock merger agreement, forming a global coatings company with an enterprise value of approximately USD 25 billion. This merger will redefine competition in the corrosion protection polymer coatings market.

- July 2024: Akzo Nobel N.V. has launched an upgraded and automated production line at its Suzhou site in China, as part of a EUR 14 million investment to double the plant's capacity for marine and protective coatings. This expansion is expected to enhance its corrosion protection polymer coatings under the protective coatings segment.

Global Corrosion Protection Polymer Coating Market Report Scope

Corrosion Protection Polymer Coatings are thin-layered coatings or paints made from polymers that provide superior adhesion and protection against corrosion. During the production and usage of various metal products, factors such as oxidation and corrosion, often triggered by high temperatures and humidity, can degrade material performance or cause failure. Polymer coatings create a protective barrier that prevents metal materials from interacting with the external environment, thereby effectively extending their service life.

The Corrosion Protection Polymer Coating Market is segmented by polymer type, formulation, technology, end-user industry, and geography. By polymer type, the market is segmented into epoxy, polyurethane, polyester, fluoropolymer, acrylic, and other polymers. By formulation, the market is segmented into solvent-borne, water-borne, powder coating, and high-solids coating. By technology, the market is segmented into thermosetting coatings and thermoplastic coatings. By end-user industry, the market is segmented into oil and gas, marine, construction and infrastructure, automotive and transportation, energy and power, water and wastewater treatment, and other end-user industries. The report also covers the market size and forecasts for corrosion protection polymer coating in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Epoxy |

| Polyurethane |

| Polyester |

| Fluoropolymer |

| Acrylic |

| Other Polymers (Nylon, PVDF, etc.) |

| Solvent-borne |

| Water-borne |

| Powder Coating |

| High-solids Coating |

| Thermosetting Coatings |

| Thermoplastic Coatings |

| Oil and Gas |

| Marine |

| Construction and Infrastructure |

| Automotive and Transportation |

| Energy and Power (Wind, Solar, Hydro) |

| Water and Wastewater Treatment |

| Other End-user Industries Industries (Mining, Chemical Processing, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | South Africa |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

| By Polymer Type | Epoxy | |

| Polyurethane | ||

| Polyester | ||

| Fluoropolymer | ||

| Acrylic | ||

| Other Polymers (Nylon, PVDF, etc.) | ||

| By Formulation | Solvent-borne | |

| Water-borne | ||

| Powder Coating | ||

| High-solids Coating | ||

| By Technology | Thermosetting Coatings | |

| Thermoplastic Coatings | ||

| By End-user Industry | Oil and Gas | |

| Marine | ||

| Construction and Infrastructure | ||

| Automotive and Transportation | ||

| Energy and Power (Wind, Solar, Hydro) | ||

| Water and Wastewater Treatment | ||

| Other End-user Industries Industries (Mining, Chemical Processing, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | South Africa | |

| Saudi Arabia | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the corrosion protection polymer coating market?

The corrosion protection polymer coating market stands at USD 11.12 billion in 2026 and is forecast to reach USD 13.41 billion by 2031 at a 3.82% CAGR from 2026 to 2031.

Which polymer type is expected to grow the fastest over 2026-2031?

Fluoropolymer coatings, driven by offshore hydrogen and ammonia projects, are set to post a 4.57% CAGR, the highest among polymer groups.

How are tightening VOC rules influencing formulation choices?

Stricter EPA and EU limits are steering buyers away from solvent-borne blends and toward powder, water-borne, and high-solids systems that meet low-VOC and carbon-footprint thresholds.

Why are asset owners prioritizing 25-30 year coating systems?

Labor shortages for certified applicators and the superior total-cost-of-ownership profile of long-life coatings make fewer re-application cycles economically attractive.

Which end-user segment is forecast to register the fastest growth?

Energy and power installations, especially offshore wind infrastructure, are expected to expand at a 5.03% CAGR through 2031.

Page last updated on: