Heat-Resistant Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

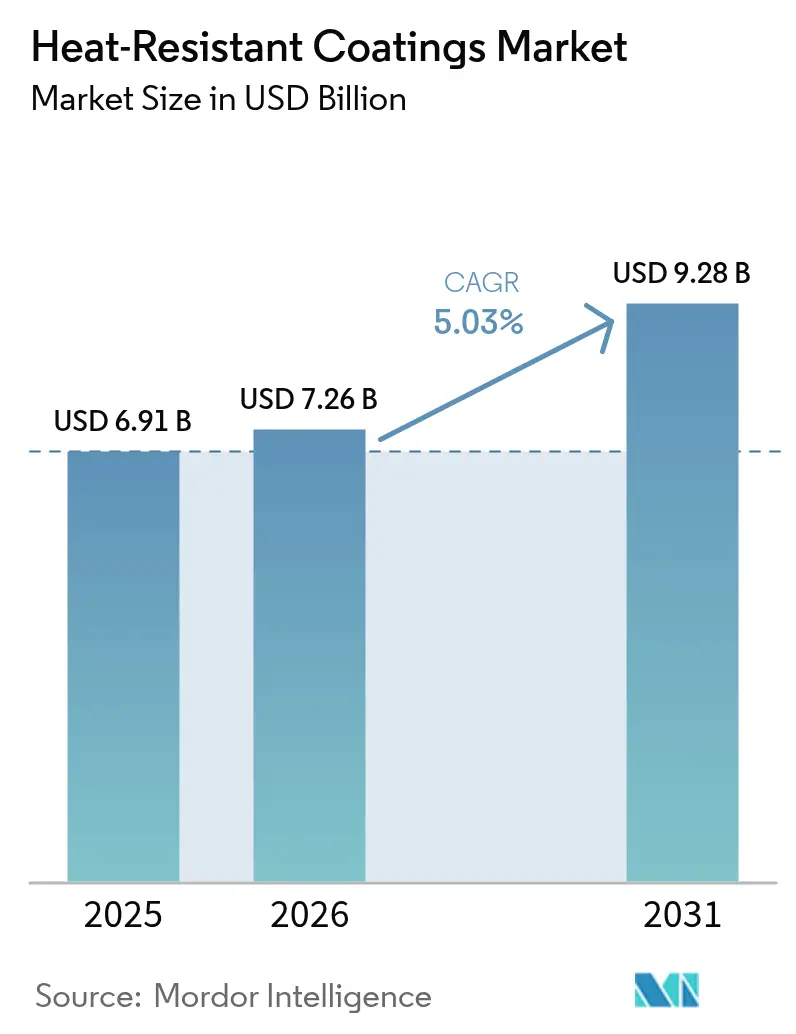

| Market Size (2026) | USD 7.26 Billion |

| Market Size (2031) | USD 9.28 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Heat-Resistant Coatings Market Analysis by Mordor Intelligence

The Heat-Resistant Coatings market size is expected to grow from USD 6.91 billion in 2025 to USD 7.26 billion in 2026 and is forecast to reach USD 9.28 billion by 2031 at 5.03% CAGR over 2026-2031. Rising global infrastructure investments, tighter fire-safety rules and the aerospace sector’s push for reusable spacecraft continue to widen demand. Asia-Pacific retains scale advantages through government-led building programs and manufacturing expansion, while North America and Europe emphasize high-performance solutions that meet stricter environmental rules. Technology adoption shows two clear tracks: water-borne systems hold volume leadership owing to lower VOC emissions, and UV/EB-curable chemistries post the fastest gains by combining rapid cure with minimal environmental impact. Silicone-based resins dominate both scale and growth because of unmatched stability above 600 °C, and emerging power-generation projects are shifting volume toward energy infrastructure where thermal management is critical. Raw-material price swings and a shortage of certified applicators remain counterweights, yet sustained innovation in sustainable formulations and automated spray systems keeps the long-term outlook positive.

Key Report Takeaways

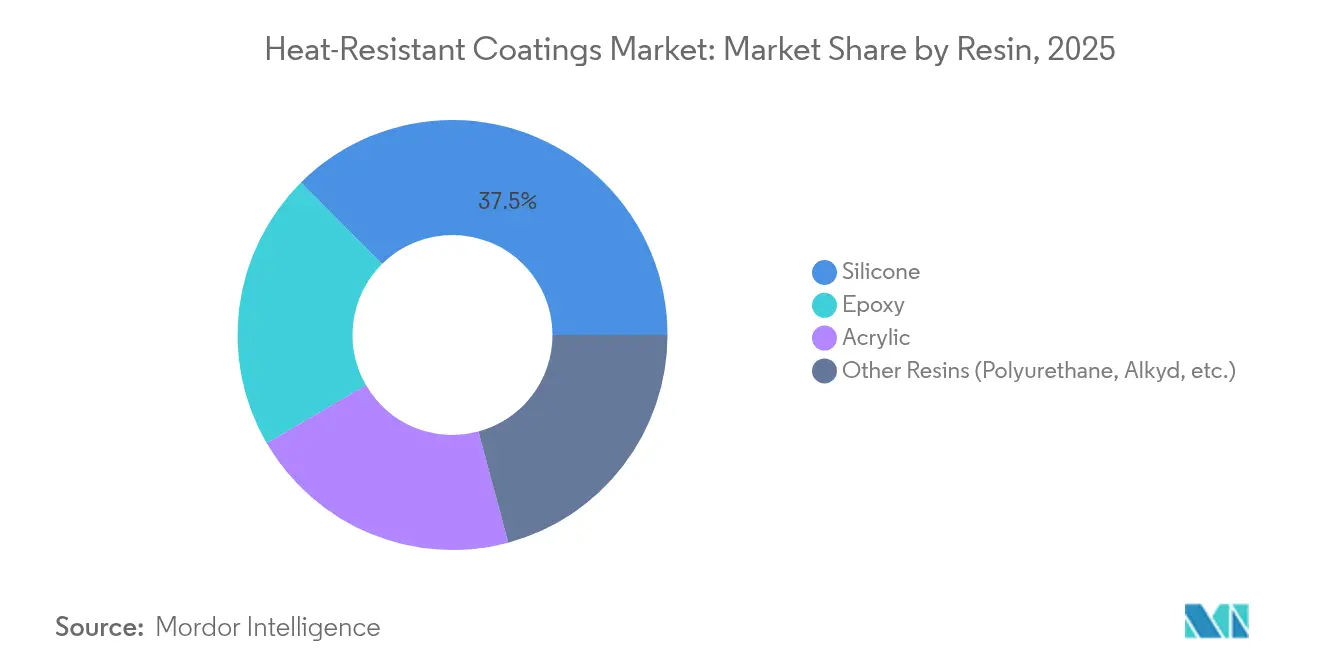

- By resin, silicone commanded 37.45% heat-resistant coatings market share in 2025 and is growing at 8.78% CAGR, the fastest among all chemistries.

- By technology, waterborne systems captured 38.74% of the 2025 heat-resistant coatings market share, while UV/EB-curable systems are advancing at 7.08% CAGR.

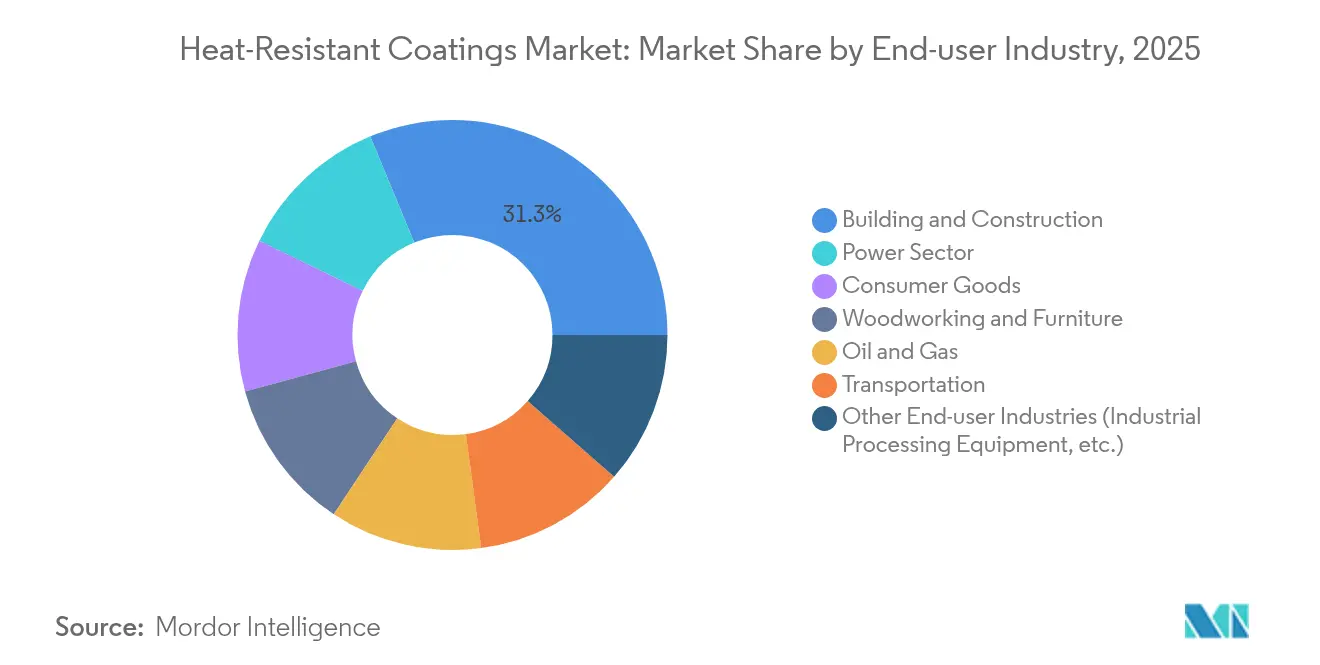

- By end-user industry, building and construction accounted for 31.25% of 2025 revenue; the power sector is the fastest-growing end-use at 9.55% CAGR.

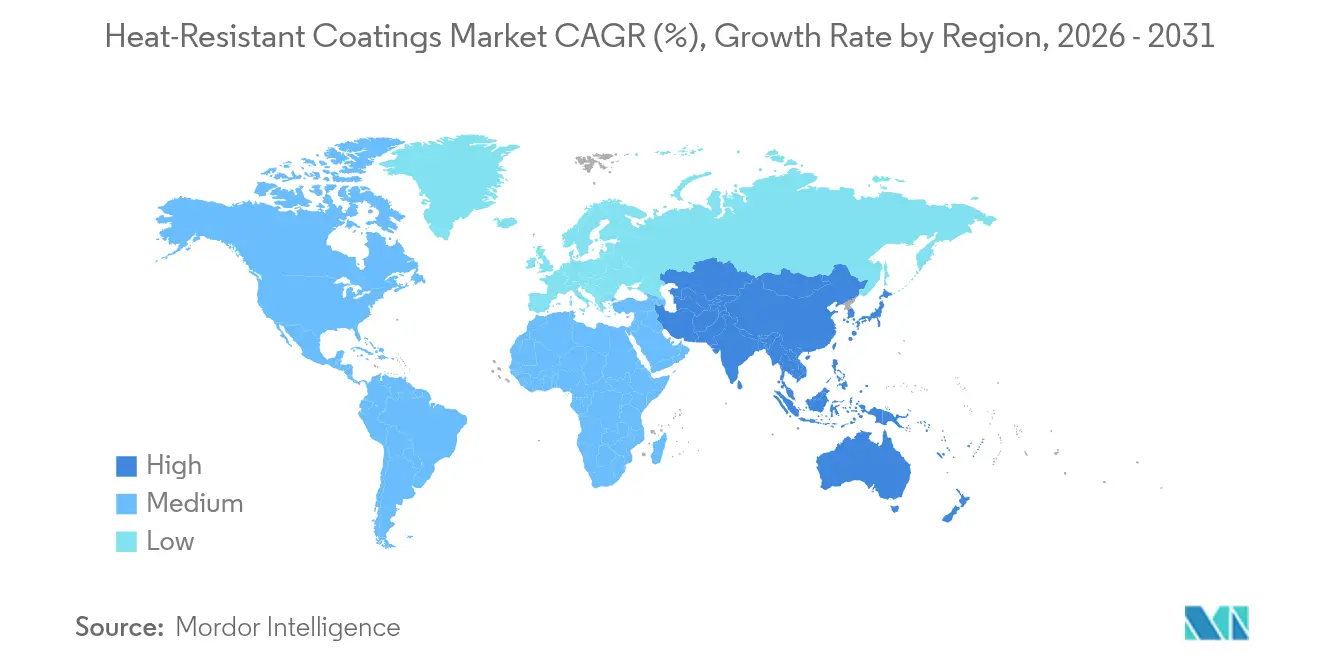

- By geography, Asia-Pacific led with 47.12% of 2025 revenue and is expanding at a 7.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Heat-Resistant Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in global infrastructure spending | 1.5% | Global, with APAC leading | Medium term (2-4 years) |

| Stricter global fire-safety regulations | 0.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Growing demand from the aerospace industry | 1.2% | North America, Europe, and emerging in APAC | Long term (≥ 4 years) |

| Rising awareness toward fire protection equipment | 0.6% | Global, with faster adoption in developed markets | Medium term (2-4 years) |

| Reusable spacecraft and space-tourism vehicles | 0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Global Infrastructure Spending

Governments are funding record levels of infrastructure aimed at climate resilience and urban growth. The United States Infrastructure Investment and Jobs Act earmarked USD 225 million for updated energy codes that influence coating specifications[1]U.S. International Trade Commission, “Certain Epoxy Resins From South Korea, Taiwan and Thailand,” usitc.gov. Emerging Asia-Pacific economies add momentum as Indonesia, India, and China accelerate airport, bridge, and smart-city projects that specify high-temperature barrier films. Public-private partnerships in transport tunnels and district-heating lines further widen demand for long-cycle thermal coatings.

Stricter Global Fire-Safety Regulations

Fire-code revisions raise minimum performance thresholds for ignition resistance, smoke toxicity, and end-use surface temperature. The International Fire Code 2024 introduces updated flame-spread benchmarks that immediately affect coating formulations. California’s Fire Code Chapter 24 mandates automatic extinguishing systems and specialized ventilation for coating booths handling heat-resistant products. EU directives continue to shrink allowed solvent content, pushing builders toward low-VOC silicone-acrylic hybrids. Retrofits of high-rise facades and transportation hubs create demand spikes as owners bring assets into compliance. Manufacturers that certify products above the new baseline win specification priority and reduce the need for costly rework.

Growing Demand from the Aerospace Industry

Gas-turbine and spacecraft programs rely on coatings able to tolerate extreme thermal cycling without spallation. Honeywell expanded its thermal-barrier coating line in South Carolina to support next-generation engines that operate above 1,300 °C. Ytterbium-silicide research from the Tokyo University of Science targets higher oxidation resistance for jet engines, signaling future commercial adoption. Qualification cycles are long, but once approved, suppliers secure premium, multi-year contracts. European airframers aim to cut fuel burn by 15% through hotter core temperatures, further enlarging the addressable heat-resistant coatings market. Asia-Pacific suppliers are entering joint ventures to localize production as regional aircraft projects mature.

Rising Awareness Toward Fire Protection Equipment

Corporate risk programs now bundle passive and active fire-safety measures, elevating the role of intumescent and ceramic-filled coatings. AI-enabled monitoring systems require coatings that remain stable at sensor interface points and can self-report degradation. Insurance carriers in North America and Europe offer premium discounts when structures apply listed passive fire-protection films, strengthening the value proposition. Museums and heritage trusts deploy low-gloss, non-yellowing silicone topcoats on artifacts, widening the industry’s cultural-asset segment. The combination of regulatory pressure and financial incentives sustains expansion even in lower-growth construction markets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicone and epoxy prices | -0.7% | Global, with Asia-Pacific supply concentration | Short term (≤ 2 years) |

| VOC limits on solvent-borne systems | -0.5% | North America and the EU, expanding globally | Medium term (2-4 years) |

| Applicator skill shortage for multi-layer systems | -0.3% | Global, acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicone and Epoxy Prices

A United States International Trade Commission ruling found certain epoxy imports were sold below fair value, tightening domestic supply and raising costs. Simultaneous outages in key Asian silicone plants amplified volatility. Smaller formulators lacking long-term contracts faced double-digit cost spikes that eroded margins and triggered product repricing. Producers hedge by dual-sourcing precursors and expanding in-house monomer capacity, but capital outlays delay immediate relief. Although raw-material swings are cyclical, they compress cash flow and hinder research and development spending in the short term.

VOC Limits on Solvent-Borne Systems

Revisions to NSF/ANSI/CAN 600 sliced allowable xylene, ethylbenzene, and toluene levels in potable-water coatings to near-trace amounts. South Coast AQMD Rule 1151 in California imposes lower-toxicity targets that paradoxically raise VOC if manufacturers swap exempt solvents, complicating compliance. Global majors accelerate water-reducible and powder development, but line-conversion costs and certification hurdles weigh on profitability. Regional patchworks of VOC caps obligate suppliers to maintain multiple formulations, swelling inventory complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin: Silicone Dominance Drives Innovation

Silicone resins accounted for 37.45% of the 2025 heat-resistant coatings market share, reflecting the chemistry’s ability to tolerate temperatures above 600 °C without losing adhesion. That leadership is matched by the fastest segment CAGR of 8.78% through 2031, making silicone the pivotal growth engine of the heat-resistant coatings market. Demand spans exhaust stacks, flare stacks, bake ovens, and aerospace parts where failure is unacceptable. Epoxies retain relevance in mid-temperature zones but face cost headwinds and regulatory scrutiny on bisphenol-A derivatives. Acrylics fill price-sensitive applications in consumer goods where surface temperature peaks are lower.

By Technology: Water-Borne Leadership Amid UV Innovation

Water-borne systems secured 38.74% of 2025 revenue, underscoring wide acceptance in OEM and maintenance cycles. Formulators have solved early issues around humidity sensitivity, producing films that equal or exceed solvent-borne corrosion resistance. UV/EB-curable chemistries clock a 7.08% CAGR, fueled by near-instant curing and elimination of bake ovens. Powder coatings continue stable uptake in pipelines and appliance parts owing to 100% solids content and minimal waste, while solvent-borne technologies lose share under tightening VOC laws.

By End-User Industry: Construction Stability Versus Power Growth

Building and construction generated 31.25% of the 2025 demand, providing the largest volume base for the heat-resistant coatings market. Continuous retrofits of curtain walls, fire doors, and structural steel keep orders steady. At the other end, the power sector posts a 9.55% CAGR through 2031, driven by higher-temperature turbines and peak-load balancing plants that run hotter for efficiency gains. Oil and gas remains another core user segment, applying ceramic-filled films to process pipes and flare stacks that see thermal shock.

The U.S. Department of Energy’s ultra-high-temperature TBC program for gas turbines targets operation above 1,300 °C, directly raising coating performance bars. Transportation applications, especially electric vehicles, demand lightweight coatings that dissipate battery heat while surviving possible thermal runaway events. Specialty applications in consumer goods, such as high-end cookware, extend the market’s breadth without materially shifting volume totals.

Geography Analysis

Asia-Pacific led with 47.12% of 2025 revenue and advances at 7.35% CAGR, powered by megaprojects in transport, housing, and energy. China’s Belt and Road corridors require heat-resistant primers for bridges and tunnels exposed to wildfire and chemical spill risks. India, under its Make in India vision, expands domestic manufacturing of cookstoves, boilers, and industrial ovens that all specify heat-stable films.

North America remains an innovation center. Aerospace primes in the United States and Canada specify metallic and ceramic barrier coats qualified to MIL standards. Federal infrastructure outlays replace aging bridges and improve energy grids, each project mandating low-VOC, high-temperature finishes.

Europe emphasizes sustainability. EU VOC ceilings tighten yearly, pushing builders to waterborne silicones and powder options. Automotive platforms in Germany, France, and Italy integrate lightweight metal components coated with nano-structured ceramic films for thermal regulation. Markets in South America, the Middle East and Africa grow from a smaller base yet benefit from technology transfer and the adoption of international safety codes, widening the total addressable heat-resistant coatings market.

Competitive Landscape

The sector remains highly consolidated. PPG Industries leverages global resin synthesis and local blending sites to shorten lead times. Sherwin-Williams balances a broad architectural footprint with specialized industrial coatings such as the Heat-Flex range, giving it scale plus niche depth. Technology investments center on robotic applications, digital inspection, and green chemistry. Suppliers embed sensors in film builds to track in-service temperature and signal maintenance needs.

Heat-Resistant Coatings Industry Leaders

Jotun

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Kansai Paint Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: PPG Industries launched PPG PITT-THERM 909 spray-on insulation, a silicone-based coating aimed at high-heat environments in oil, gas and petrochemical facilities.

- June 2023: Sherwin-Williams introduced Heat-Flex CUI-mitigation coatings, a four-product ultra-high-solids epoxy line designed to combat corrosion under insulation.

Global Heat-Resistant Coatings Market Report Scope

The heat-resistant coatings market report includes:

| Silicone |

| Epoxy |

| Acrylic |

| Other Resins (Polyurethane, Alkyd, etc.) |

| Solvent-borne |

| Water-borne |

| Powder |

| UV/EB-curable |

| Building and Construction |

| Oil and Gas |

| Power Sector |

| Transportation |

| Woodworking and Furniture |

| Consumer Goods |

| Other End-user Industries (Industrial Processing Equipment, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin | Silicone | |

| Epoxy | ||

| Acrylic | ||

| Other Resins (Polyurethane, Alkyd, etc.) | ||

| By Technology | Solvent-borne | |

| Water-borne | ||

| Powder | ||

| UV/EB-curable | ||

| By End-user Industry | Building and Construction | |

| Oil and Gas | ||

| Power Sector | ||

| Transportation | ||

| Woodworking and Furniture | ||

| Consumer Goods | ||

| Other End-user Industries (Industrial Processing Equipment, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the heat-resistant coatings market?

The market stands at USD 7.26 billion in 2026 and is projected to hit USD 9.28 billion by 2031 on a 5.03% CAGR.

Which region leads the heat-resistant coatings market?

Asia-Pacific holds 47.12% of 2025 revenue and is also the fastest-growing region at 7.35% CAGR through 2031.

Why are silicone-based coatings growing so fast?

Silicone commands 37.45% market share and grows at 8.78% CAGR because it withstands temperatures above 600 °C without losing adhesion, making it ideal for high-heat industrial and aerospace uses.

How are VOC regulations affecting technology choices?

Tighter VOC caps in North America and Europe shift buyers toward water-borne and UV-curable systems, reducing reliance on solvent-borne coatings and driving innovation in low-emission chemistries.

Which end-user industry will grow the quickest?

The power sector shows the fastest expansion at 9.55% CAGR as utilities upgrade turbines and adopt higher operating temperatures to improve efficiency.

Page last updated on: