Fireproofing Coatings For Wood Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

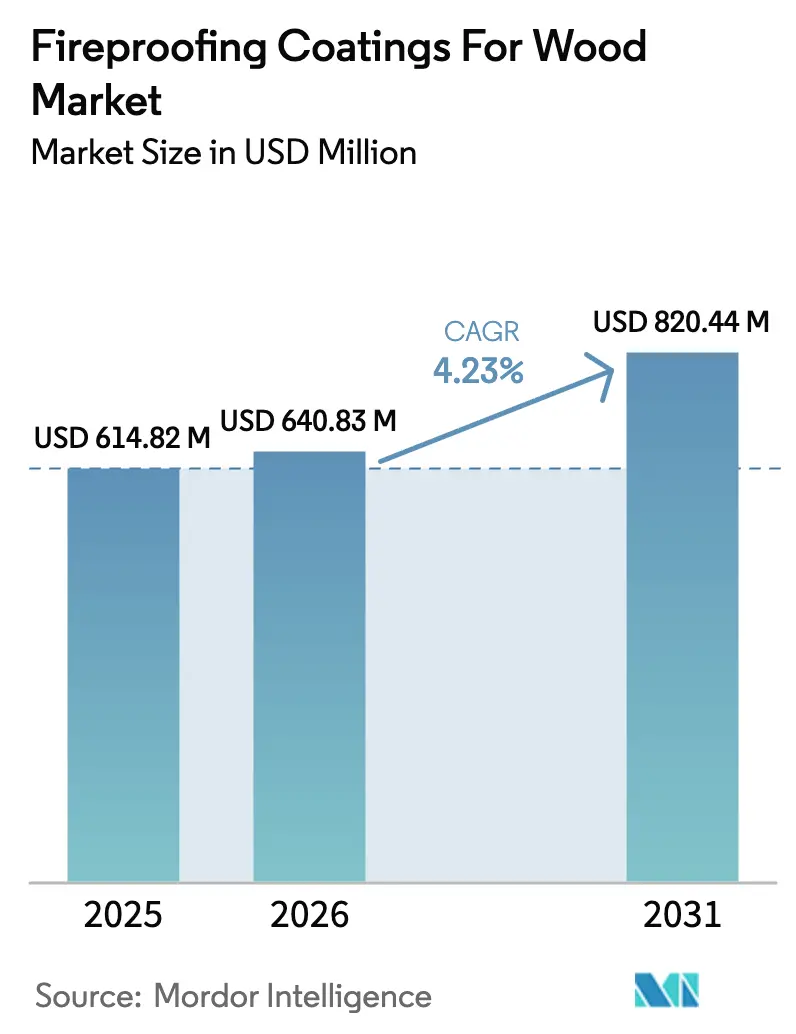

| Market Size (2026) | USD 640.83 Million |

| Market Size (2031) | USD 820.44 Million |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fireproofing Coatings For Wood Market Analysis by Mordor Intelligence

The Fireproofing Coatings For Wood Market size is projected to be USD 614.82 million in 2025, USD 640.83 million in 2026, and reach USD 820.44 million by 2031, growing at a CAGR of 4.23% from 2026 to 2031. Heightened fire-safety codes, insurance incentives, and the expansion of mass-timber construction elevate demand even as volume growth stays modest. Water-borne, halogen-free acrylic systems are replacing solvent formulations in response to VOC caps in California and the European Union. North America led with a 39.98% share in 2025, yet Asia-Pacific is on course for the fastest 4.87% annual growth on the back of Japan’s CLT boom and Australia’s carbon-neutral building mandates. Acrylic resins commanded 74.69% of demand in 2025 because their char chemistry tolerates moisture found in kiln-dried lumber. Insurance discounts for ASTM E84 Class A-rated timber further strengthen the pull for certified intumescent systems.

Key Report Takeaways

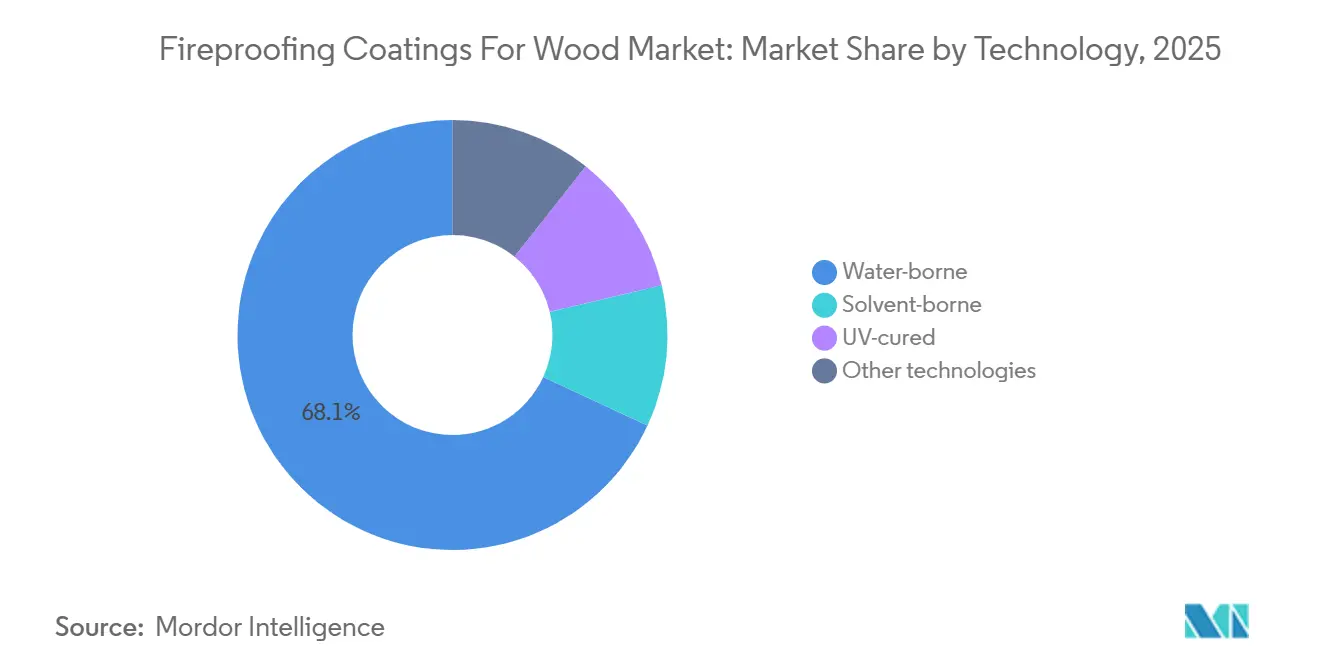

- By technology, water-borne technology secured 68.09% of 2025 revenue and is forecast to expand at a 4.47% CAGR to 2031.

- By resin type, acrylic resins captured 74.69% of demand in 2025 and are projected to grow at a 4.37% CAGR through 2031.

- By coating type, halogen-free coatings held 78.87% share in 2025 and represent the fastest 4.57% CAGR segment to 2031.

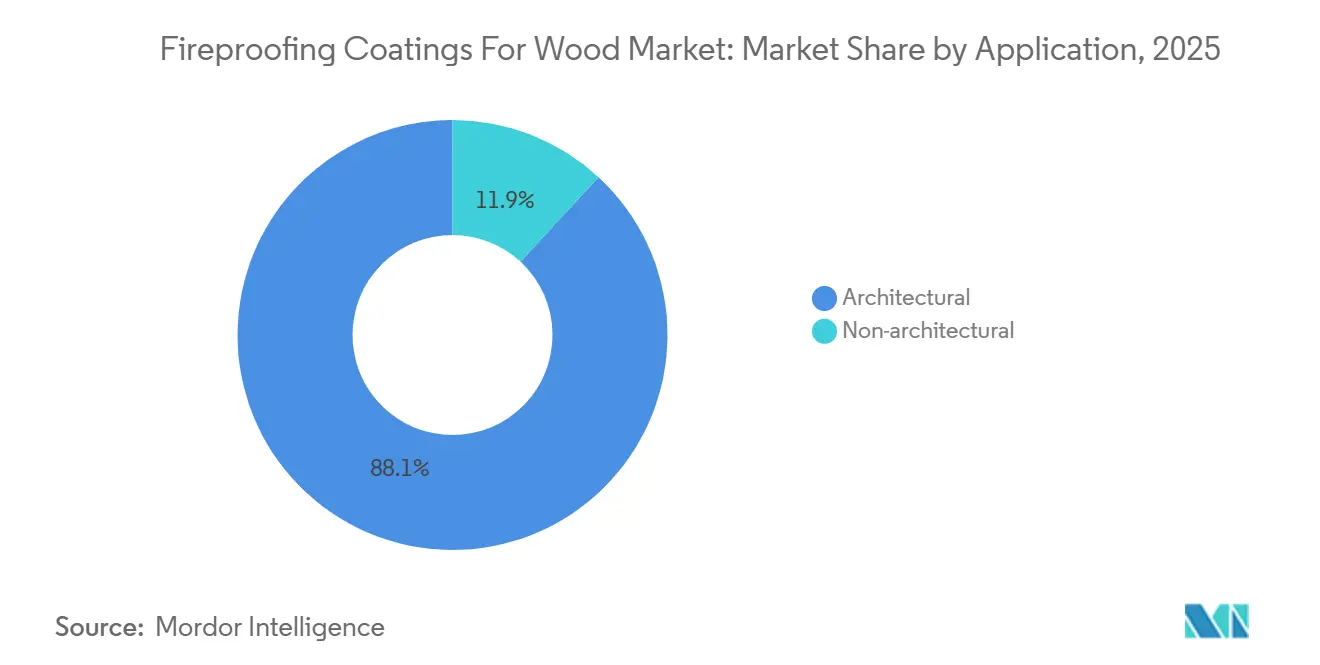

- By application, architectural applications commanded 88.12% of 2025 revenue; they are projected to expand at a 4.43% CAGR through 2031.

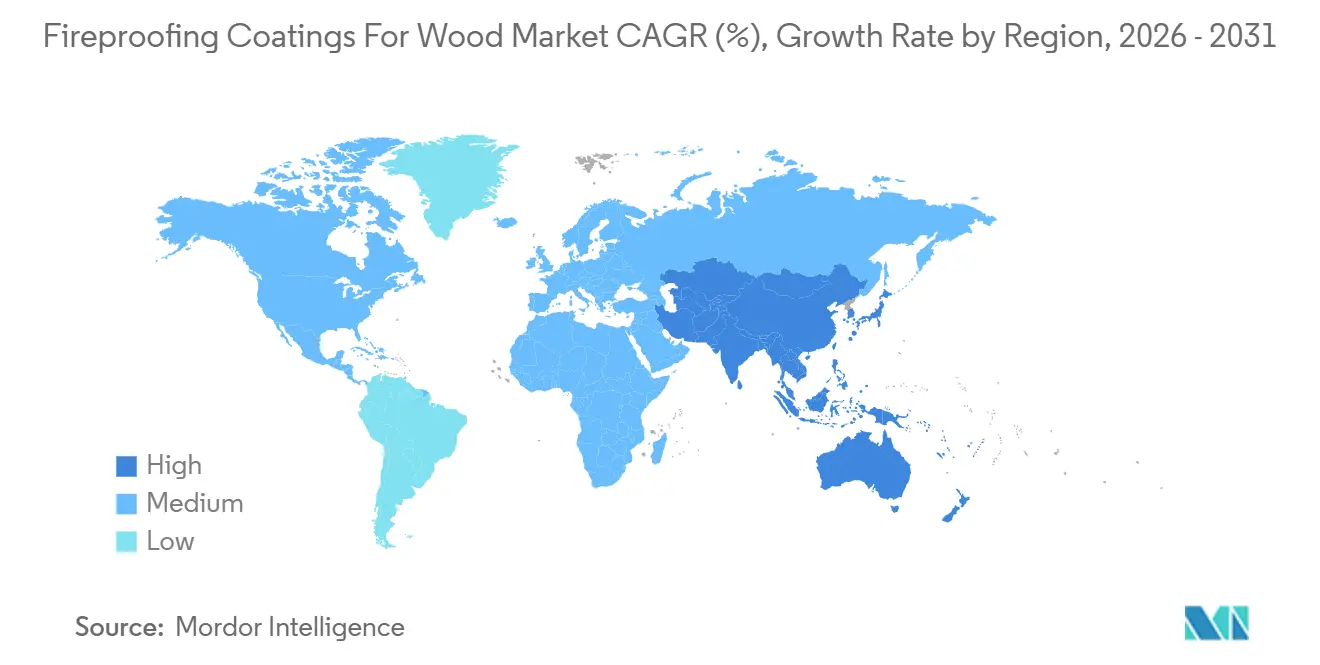

- By geography, North America led with a 39.98% share in 2025, whereas Asia-Pacific is forecast to post a 4.87% CAGR, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fireproofing Coatings For Wood Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent fire-safety codes and certification mandates | +1.2% | Global, with strongest enforcement in North America, Europe, and Japan | Long term (≥ 4 years) |

| Expansion of mass-timber construction in Asia-Pacific | +1.0% | APAC core (Japan, Australia, China), spill-over to South Korea and New Zealand | Medium term (2-4 years) |

| Shift toward halogen-free, low-VOC formulations | +0.8% | North America and EU leading, APAC adoption accelerating | Medium term (2-4 years) |

| Insurance discounts for coated structural wood | +0.5% | North America (California, Louisiana), Australia | Short term (≤ 2 years) |

| BIM-integrated digital fire-rating specifications | +0.3% | North America and Europe, early adoption in Singapore and UAE | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Fire-Safety Codes and Certification Mandates

Under the 2024 International Building Code, mass-timber structures can rise to mid- and high-rise levels, provided the exposed wood achieves a flame-spread index within acceptable standards. This benchmark is only attainable through the application of intumescent coatings. Meanwhile, Eurocode 5's 2025 update offers designers a financial edge: by recognizing the protective char from these coatings, they can reduce timber dimensions. In Japan, similar provisions apply to mid-rise CLT residences in seismic zones. Here, the stipulation is that certified coatings must achieve a rating on the ASTM E119 scale. Furthermore, NFPA 703 has introduced a mandate for third-party certification, a move that has bolstered market share for suppliers with accredited laboratories[1]National Fire Protection Association, “NFPA 703 Standard for Fire Retardant-Treated Wood,” nfpa.org. Together, these regulations firmly integrate intumescent coatings into the design framework for mid- and high-rise timber structures.

Expansion of Mass-Timber Construction in Asia-Pacific

Between 2024 and 2025, Japan saw a significant increase in the construction of CLT buildings, adding several structures taller than 10 stories[2]Japan CLT Association, “Mass Timber Construction Statistics Japan,” clta.jp. Under its 2025 National Construction Code, Australia now permits the use of CLT in bushfire-prone areas, provided the coated surfaces adhere to BAL 40 flow conditions. By 2027, China greenlit new CLT production lines, targeting a supply for timber housing; each square meter will require fire-rated coating. In 2025, South Korea allocated funding to subsidize CLT schools, ensuring they meet the KS F 3111 standards. Collectively, these initiatives are significantly boosting the demand for Fireproofing Coatings for Wood.

Shift Toward Halogen-Free, Low-VOC Formulations

Halogen-free coatings held 78.87% of 2025 demand and will grow at 4.57% through 2031 as specifiers avoid hydrogen-halide off-gassing that corrodes steel connectors. Water-borne acrylics already comply with regulatory standards that set a cap on emissions, effective in 2027. New product launches now prominently feature ammonium polyphosphate and melamine, stepping in for antimony trioxide, which has been banned under updated guidelines. The U.S. HAP standard for 2024 has cut the permissible level of methyl ethyl ketone, pushing manufacturers to pivot towards acetone. While acetone evaporates more rapidly, this characteristic narrows application windows, especially in humid conditions. Such regulatory shifts are steering the Fireproofing Coatings For Wood market towards the adoption of acrylic water-borne technology.

Insurance Discounts for Coated Structural Wood

California's FAIR Plan slashed premiums for CLT buildings showcasing ASTM E84 Class A coatings. This move rendered the upgrade cost-neutral within the inaugural policy year for numerous projects. In Louisiana, a discount was rolled out for hurricane-rated timber, treated with mold-resistant fire retardants. This initiative aims to reduce lifecycle costs, especially in the Gulf Coast's humid climate. Meanwhile, insurers in Australia have begun equating BAL 40-certified intumescent coatings with fiber-cement cladding. This shift translates to annual premium reductions. Such incentives bolster payback periods, encouraging developers to opt for certified products, even if they come with a heftier initial price tag.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost differential vs. conventional finishes | -0.7% | Global, most acute in price-sensitive APAC and South American markets | Medium term (2-4 years) |

| VOC/HAP limits on solvent technologies | -0.5% | North America and EU primary impact, ripple effect in APAC export-oriented manufacturers | Long term (≥ 4 years) |

| Premature weathering in tropical humidity | -0.3% | Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia), coastal India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

VOC/HAP Limits on Solvent Technologies

California's Rule 1113 effectively sidelines traditional xylene-rich epoxies. Meanwhile, the EU is set to tighten its caps by 2027. In the U.S., a 2024 HAP rule drastically reduced permissible levels of methyl ethyl ketone. This change has led to extended cure times in humid areas, throwing contractor schedules into disarray. Over in China, the introduction of GB 38507-2020 set limits. However, with weak enforcement outside of tier-1 cities, a solvent-heavy gray market continues to thrive. As the industry rapidly shifts towards water-borne chemistries, smaller formulators, lacking expertise in dispersion, find themselves increasingly burdened.

Premature Weathering in Tropical Humidity

After months at high humidity, acrylic binders lose tensile strength. This degradation allows char salts to leach, reducing fire resistance from a standard duration to just around an hour. Field audits conducted revealed that a significant percentage of coated CLT façades experienced chalking within a relatively short period. While siloxane coupling agents can extend the service life, they come with an increase in formulation costs and necessitate pH adjustments, posing challenges for smaller regional producers. In Malaysia, government projects now mandate a rigorous QUV test, a benchmark that only a portion of products currently meet. These durability challenges not only hinder adoption in equatorial regions but also underscore a significant research and development focus for the Fireproofing Coatings for Wood industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Systems Dominate Amid VOC Crackdowns

Water-borne systems accounted for 68.09% of the Fireproofing Coatings For Wood market share in 2025 and are projected to grow at a 4.47% CAGR through 2031. These systems not only adhere to compliance standards but also manage timber moisture without blistering. The adoption of single-component packaging mitigates pot-life risks and simplifies contractor tooling, further solidifying this technology's lead. While solvent-borne products, preferred for rail interiors and marine bulkheads, commanded a significant portion of the demand, they grapple with tightening regulations, constraining their growth. UV-cured coatings, though enticing Scandinavian panel makers with rapid factory cures, remain a niche due to thick intumescent films limiting light penetration.

Transitioning to water-borne systems alters logistics dynamics: denser formulations elevate freight costs per liter, yet reduce onsite ventilation needs, streamlining permitting processes. Major producers, equipped with dispersion lines, can absorb these added costs, posing challenges for smaller firms and shifting the competitive balance. As regulations extend into emerging regions, the dominance of water-borne systems is poised to bolster the market size advantage for integrated multinationals in the Fireproofing Coatings for Wood sector.

By Resin Type: Acrylic Dominance Rooted in Char Chemistry

Acrylic resins captured 74.69% of consumption in 2025 and will maintain a 4.37% CAGR to 2031. Their phosphorus-rich char foams, which activate at specific temperatures and resist moisture in kiln-dried lumber, have made them the preferred choice for architects. Polyurethane boasts abrasion strength that is particularly valued in schools and hospitals. However, its two-component mixing process strains labor budgets. Silicone's hydrophobic network performs exceptionally in coastal and tropical climates. Still, its pricing limits its adoption to premium bushfire zones. Epoxy and vinyl ester are favored on offshore platforms, where chemical resistance is prioritized over VOC limits, and they are witnessing modest growth.

Acrylic's dominance is stabilizing the supply of raw materials, particularly ammonium polyphosphate and expandable graphite. This trend is also streamlining the learning curves for regional blenders. Furthermore, acrylics are bolstering long-term forecasts for the Fireproofing Coatings For Wood market, especially as upcoming code changes seem to favor increasingly stringent VOC thresholds, a challenge best addressed by acrylic solutions.

By Coating Type: Halogen-Free Formulations Reshape Supply Chains

Halogen-free lines held 78.87% share in 2025 and will expand fastest at 4.57% CAGR through 2031. This growth is driven by rising concerns over corrosion from hydrogen halides and exclusions from LEED credits. Ammonium polyphosphate continues to be the preferred char former. However, a price surge followed a 2024 plant fire, highlighting the risks of supply concentration in Shandong. While graphite flakes offer significant expansion advantages, they come at a tripled cost, leading to loadings stabilizing. Halogenated systems, holding a smaller market share, are limited to regions with lenient regulations and older plant assets, resulting in subdued growth.

Transitioning to halogen-free compounds compels formulators to reevaluate their pigment stabilization and anti-settling strategies, elevating technical challenges. This shift benefits established players with substantial research and development investments, leading to a transformation in the supplier landscape of the Fireproofing Coatings for Wood market.

By Application: Architectural Segment Captures Mass-Timber Boom

Architectural uses represented 88.12% of 2025 revenue and will advance at a 4.43% CAGR to 2031, buoyed by the CLT high-rise pipeline authorized under IBC 2024. An 18-story tower alone could utilize significant volumes of coating, overshadowing the modest needs of rail or yacht interiors. Meanwhile, non-architectural applications, making up a smaller share of demand, are inching ahead, adapting to evolving marine and rolling-stock standards.

With architecture leading the way, research and development are pivoting towards quicker application methods and lighter hues to align with design aesthetics. Given the segment's prominence, water-borne acrylic formulations are becoming the industry standard, bolstered by regulatory preferences, thus ensuring steady growth for the Fireproofing Coatings For Wood market.

Geography Analysis

North America led the Fireproofing Coatings for Wood market with a 39.98% share in 2025. This was bolstered by numerous mass-timber projects initiated under the USDA grant program. California's premium discount for ASTM E84 Class A timber invigorated momentum in areas prone to wildfires. Canada's updated 2025 code permits 12-story structures across the nation, while British Columbia mandates a significant timber usage in new public buildings, ensuring a robust stream for retrofitting. Collectively, these factors contribute to steady growth projected until 2031.

Asia-Pacific is the fastest-growing region at a 4.87% CAGR. Between 2024 and 2025, Japan constructed several CLT towers exceeding 10 stories. Australia's approvals in bushfire zones further amplify regional demand, China's commitment to timber housing, and South Korea's substantial subsidy. While Indonesia and Vietnam grapple with humidity-related weathering issues, technological solutions like siloxane couplers are bridging the gap.

Europe commanded a significant share in 2025. Leading the charge in mass-timber adoption are Germany, the UK, and Nordic countries, utilizing Eurocode 5’s reduced cross-section method. The UK’s Fire Safety Act has spurred a wave of retrofits, and France’s RE2020 carbon regulations are nudging residential builders towards timber. While Southern Europe hesitates due to seismic worries, it's experimenting with hybrid designs, favoring coated timber for its aesthetic appeal. The region is projected to grow steadily.

South America, alongside the Middle-East and Africa, collectively holds a notable share. In 2024, Brazil greenlit multi-story timber structures, igniting demand in São Paulo. Meanwhile, Dubai and Riyadh, under broader sustainability agendas, have established timber content targets, introducing the Fireproofing Coatings For Wood market to regions traditionally dominated by steel. Challenges like limited local CLT production and import tariffs moderate growth.

Competitive Landscape

The fireproofing coatings for wood market is moderately fragmented. Mid-tier specialists address regional needs with brush-applied, single-component products that bypass spray-booth capital, a boon in Southeast Asia’s fragmented contractor base. Niche innovators are piloting lignin-based binders that trim lifecycle carbon, although pricing remains above acrylics. Competitive intensity now hinges on humidity, durability, and digital specification libraries. Companies that verify 2,000-hour QUV performance and host full BIM datasets stand to capture a disproportionate share as mass-timber codes ripple worldwide.

Fireproofing Coatings For Wood Industry Leaders

Akzo Nobel N.V.

Teknos Group

The Sherwin-Williams Company

Sika AG

Rudolf Hensel GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Remmers Gruppe SE agreed to acquire 50.01% of India’s Teknovace for INR 3 billion (USD 36 million), establishing an APAC hub for intumescent research and development and production, including fireproofing coatings for wood.

- October 2025: Remmers and Burnblock launched a Euroclass B fire-retardant system that blends Burnblock’s non-toxic treatment with Remmers' topcoats, broadening sustainable options for interior and exterior timber.

Global Fireproofing Coatings For Wood Market Report Scope

Fireproofing coatings for wood are specialized fire-retardant paints or varnishes applied to timber surfaces to enhance resistance to ignition, slow flame spread, and reduce toxic smoke emissions. These coatings, often intumescent, swell under heat to form a protective char barrier that insulates the wood, delays structural failure, and improves safety and property protection.

The market is segmented by technology, resin type, coating type, application, and geography. By technology, the market is segmented into water-borne, solvent-borne, UV-cured, and other technologies. By resin type, the market is segmented into acrylic, polyurethane/urethane, silicone, alkyd, and other resin types. By coating type, the market is segmented into halogen-free and halogenated. By application, the market is segmented into architectural and non-architectural. By geography, the market is segmented regionally. The report also covers the market size and forecasts in 25 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Water-borne |

| Solvent-borne |

| UV-cured |

| Other technologies |

| Acrylic |

| Polyurethane/Urethane |

| Silicone |

| Alkyd |

| Other Resin Types |

| Halogen-free |

| Halogenated |

| Architectural |

| Non-architectural |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Indonesia | |

| Vietnam | |

| Thailand | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Egypt | |

| Iran | |

| Turkey | |

| Morocco | |

| Rest of Middle-East and Africa |

| By Technology | Water-borne | |

| Solvent-borne | ||

| UV-cured | ||

| Other technologies | ||

| By Resin Type | Acrylic | |

| Polyurethane/Urethane | ||

| Silicone | ||

| Alkyd | ||

| Other Resin Types | ||

| By Coating Type | Halogen-free | |

| Halogenated | ||

| By Application | Architectural | |

| Non-architectural | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Indonesia | ||

| Vietnam | ||

| Thailand | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Egypt | ||

| Iran | ||

| Turkey | ||

| Morocco | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Fireproofing Coatings for Wood market in 2026?

The Fireproofing Coatings for Wood market size is estimated at USD 640.83 million in 2026.

What is the expected growth rate for Fireproofing coatings through 2031?

Industry value is forecast to rise to USD 820.44 million by 2031, registering a 4.23% CAGR between 2026 and 2031.

Which technology leads current demand?

Water-borne systems captured 68.09% of 2025 revenue and remain the leading choice due to global VOC regulations.

Why are halogen-free coatings gaining share?

Halogen-free chemistries avoid corrosive hydrogen halides, qualify for LEED credits, and meet new regulations, driving a 4.57% CAGR.

Which region will grow fastest?

Asia-Pacific is set to post a 4.87% CAGR through 2031 as Japan, Australia, and China scale mass-timber projects.

Page last updated on: