GPS Bike Computers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

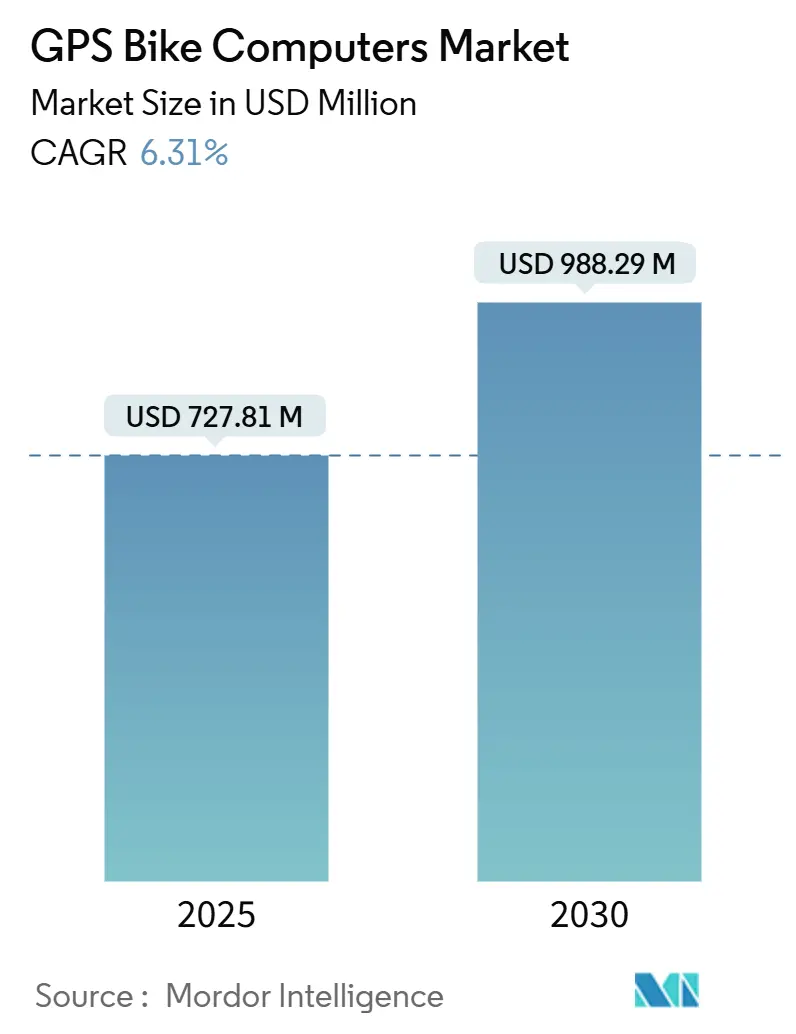

| Market Size (2025) | USD 727.81 Million |

| Market Size (2030) | USD 988.29 Million |

| Growth Rate (2025 - 2030) | 6.31% CAGR |

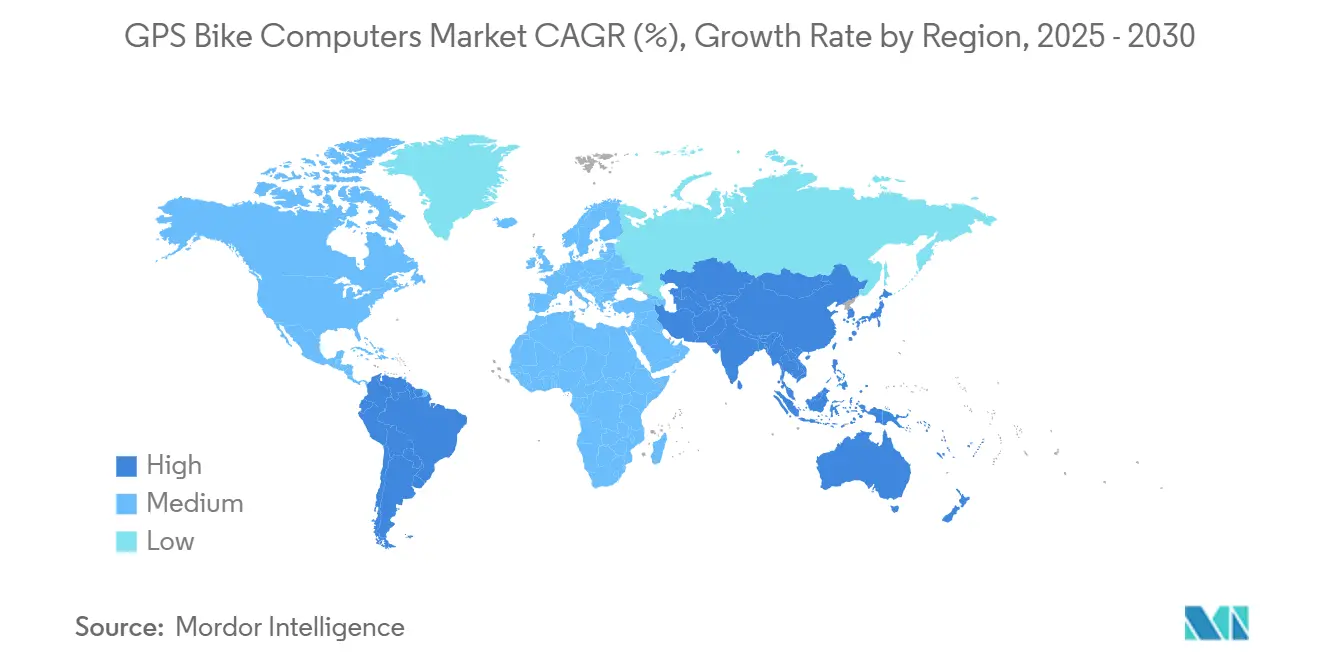

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

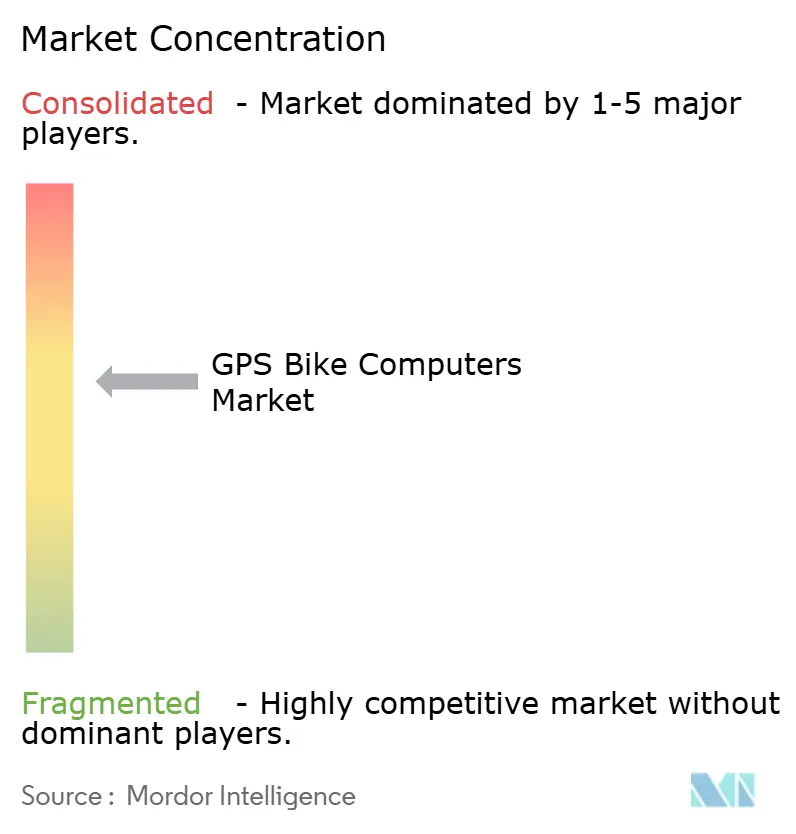

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPS Bike Computers Market Analysis by Mordor Intelligence

The GPS Bike Computers Market size is estimated at USD 727.81 million in 2025, and is expected to reach USD 988.29 million by 2030, at a CAGR of 6.31% during the forecast period (2025-2030). Robust e-bike adoption, the shift toward direct-to-consumer e-commerce, and the rollout of multi-band GNSS chips position the GPS bike computers market for steady expansion even as smartwatches and smartphones target casual cyclists. Solar charging and cellular eSIM modules are migrating quickly from flagship models to mid-range units, narrowing the feature gap across price tiers. In parallel, OEM bundling with e-bikes is accelerating product refresh cycles, while professional racing continues to showcase premium innovation that eventually diffuses into mainstream segments. Venture capital inflows into connected micromobility platforms add tailwinds, creating new data monetization opportunities for device makers.

Key Report Takeaways

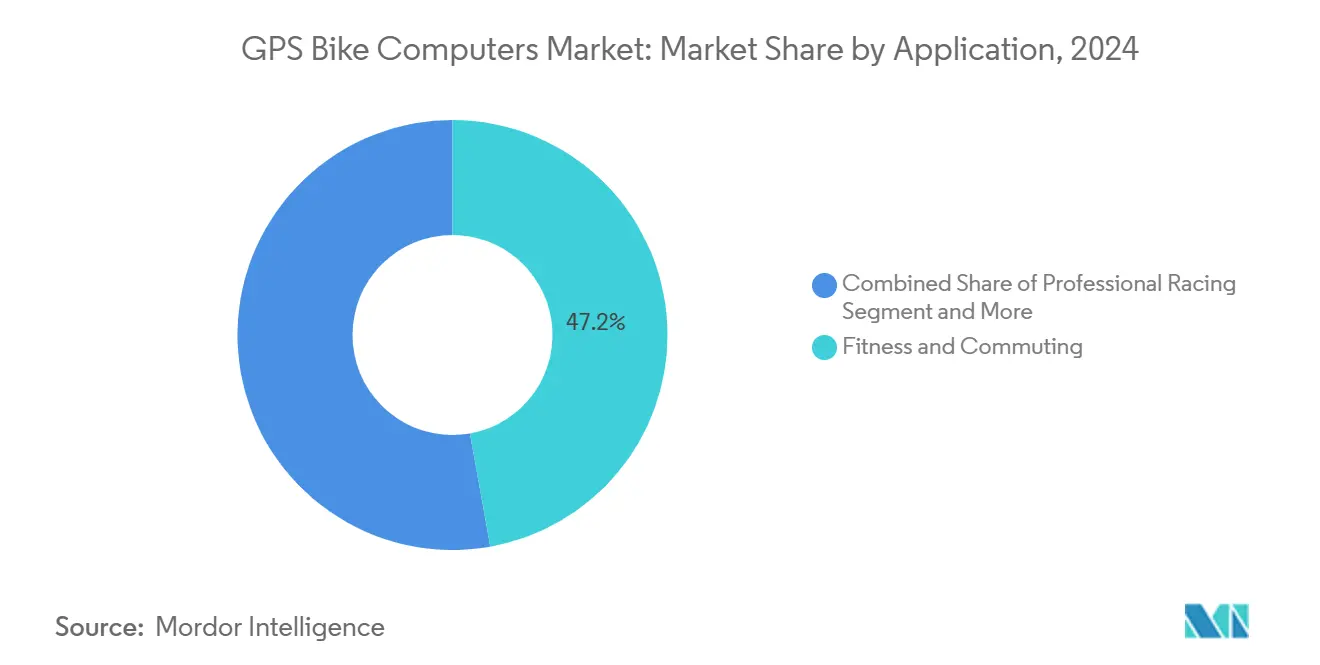

- By application, fitness and commuting commanded 47.18% of the GPS bike computers market share in 2024, and professional racing is forecast to post the highest 6.35% CAGR during the forecast period (2025-2030).

- By product type, mapping computers commanded a 63.46% share of the GPS bike computers market in 2024, whereas solar-powered mapping units are set to deliver a 6.47% CAGR during the forecast period (2025-2030).

- By bike type, e-bikes held 37.81% of the GPS bike computers market share in 2024 and are expanding at a 6.49% CAGR during the forecast period (2025-2030).

- By connectivity, ANT+ and Bluetooth captured 52.38% of revenue in 2024, while cellular eSIM devices led growth at a 6.38% CAGR during the forecast period (2025-2030).

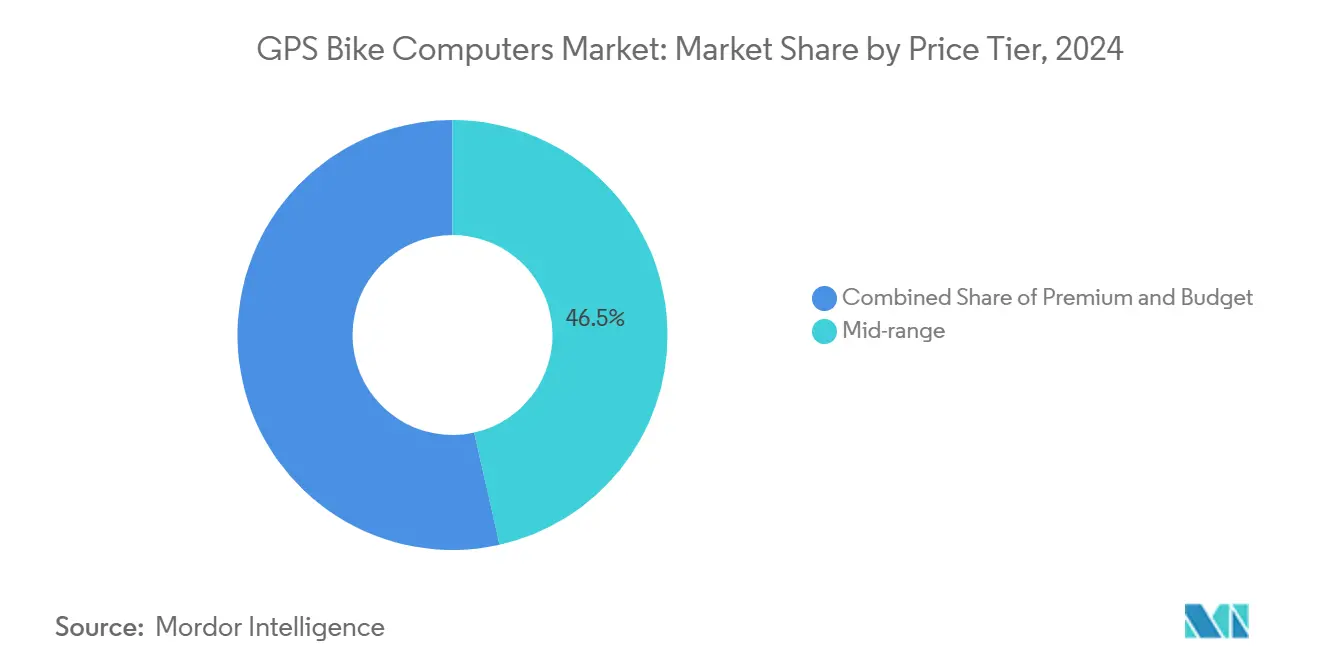

- By price tier, mid-range models contributed 46.51% of the market's value in 2024, but premium units are forecast to post a 6.39% CAGR during the forecast period (2025-2030).

- By distribution channel, online direct-to-consumer accounted for 41.26% of 2024 sales and shows the strongest 6.44% CAGR during the forecast period (2025-2030).

- By geography, Europe captured 38.44% of global revenue in 2024; Asia-Pacific is poised for the fastest 6.41% CAGR during the forecast period (2025-2030).

Global GPS Bike Computers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In E-Bike Sales Elevating Demand | +1.8% | Global, with early gains in Europe, China, North America | Medium term (2-4 years) |

| Rising Global Cycling Participation | +1.5% | Global, strongest in Europe, North America, emerging Asia Pacific | Long term (≥ 4 years) |

| Multi-Band GNSS And Solar-Charging Tech Improving Reliability | +1.2% | Global, premium segments first | Medium term (2-4 years) |

| Deep Integration With Smartphone/Cloud Fitness Ecosystems | +1.0% | Global, led by developed markets | Short term (≤ 2 years) |

| OEM Bundling Of Computers | +0.9% | Global, concentrated in premium bike segments | Medium term (2-4 years) |

| Insurer Telematics Incentives | +0.7% | Europe, North America, select Asia Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-Bike Sales Elevating Demand for GPS Head-Units

E-bike shipments are outpacing traditional bicycles, and every new e-bike platform introduces proprietary battery protocols and motor control signals that generic smartphones struggle to process. Dedicated GPS bike computers market vendors now ship CAN-bus-ready head-units that surface state-of-charge, torque levels, and range data on the same screen as navigation, giving riders a unified cockpit. Major e-bike OEMs such as Bosch add GPS modules that satisfy Europe’s EN 15194 electromagnetic compatibility rules, driving lock-in for compliant accessories [1]“eBike System 2 Technical Guidelines,” Bosch eBike Systems, bosch-ebike.com . Mid-tier Asian brands replicate this template, widening addressable volume. Given the typical three-year e-bike replacement cycle, attach rates for GPS head-units rise quickly, pushing incremental hardware revenue and recurring software fees for remote diagnostics.

Rising Global Cycling Participation & Data-Driven Training Culture

Recreational ridership surged during the lockdown easing, and that momentum persists as commuters seek active mobility. The GPS bike computers market benefits from athletes who look to translate professional telemetry into personal performance gains. Events like the Tour de France Femmes 2025 streamed live power, cadence, and aerodynamic drag data, cementing audience expectations for richer metrics. Platforms like Zwift and TrainerRoad create virtuous feedback loops: users record outdoor sessions on a GPS head-unit, sync data to the cloud, and receive structured intervals for the next ride, reinforcing device dependence. The expanding coaching economy, ranging from AI-driven training plans to human consultants, further boosts device penetration by mandating high-resolution ride files as proof of work.

Multi-Band GNSS & Solar-Charging Tech Improving Reliability

Dual-frequency reception mitigates multipath errors in dense urban grids, moving turn alerts earlier and shrinking wrong-turn penalties. Premium chipsets support RTK-like corrections, hinting at centimeter-level accuracy once mass-market subscription models mature. Solar cells built into bezels add 20-30% endurance under mid-latitude summer conditions, pushing runtime beyond traditional 20-hour ceilings. Brands such as COROS commercialized continuous-charge algorithms that prevent lithium-ion stress, bolstering warranty metrics [2]“Dura Solar Product Sheet,” COROS Wearables Inc., coros.com . Collectively, these advances enable multi-day bikepacking without spare batteries, amplifying the appeal of dedicated devices over power-hungry phones.

Deep Integration with Smartphone/Cloud Fitness Ecosystems

The GPS bike computers market is shifting from closed appliances to edge nodes in an always-on fitness mesh. Garmin’s Connect IQ storefront hosts third-party apps ranging from real-time wind scoring to insurance telematics, turning head-units into extensible platforms. eSIM variants deliver live tracking to family dashboards even when the rider’s phone dies, improving perceived safety. Automatic crash detection satisfies insurer mandates for ride-to-earn programs, creating new subsidy pathways that compress payback periods for consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of GPS Bike Computers | -0.8% | Global, particularly price-sensitive emerging markets | Medium term (2-4 years) |

| Competition from Smartwatches and Phones | -0.6% | Developed markets, urban centers | Long term (≥ 4 years) |

| Free Navigation Apps Reducing Value | -0.5% | Global, strongest in price-sensitive segments | Short term (≤ 2 years) |

| GNSS Chipset Shortage | -0.4% | Global, affecting all manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Dedicated GPS Bike Computers

Flagship devices retail between USD 400 and USD 600, a hurdle in regions where bicycles double as utilitarian transport. Entry-level models shave features—offline maps, solar panels—to hit USD 150 targets but still face competition from free phone apps. Certification fees for CE, FCC, and Bluetooth SIG add fixed overhead, eroding margin for low-volume SKUs. Currency fluctuations raise landed costs in Latin America and Southeast Asia, forcing distributors to trim inventory depth and lengthen lead times.

Cannibalization from Advanced Smartwatches & Phones

Wearables now offer dual-frequency GNSS and multi-day battery life, closing historical performance gaps. Apple and Samsung promote cycling-specific watch faces with power-meter pairing, siphoning novices who value all-in-one convenience. Smartphone mounts integrate vibration-dampening polymers to protect camera OIS systems, decreasing the breakage penalty that once favored dedicated units. While hardcore cyclists still demand handlebar-level glanceability, mainstream adoption may plateau in city commutes where smartwatch haptics suffice for navigation cues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Data-Intensive Racing Sparks Premium Pull-Through

Professional racing accounted for the smallest revenue slice in 2024 yet clocked a 6.35% CAGR outlook, underscoring how elite use cases steer product roadmaps. Teams run dual-computer setups—one head-unit for rider feedback, a second locked to telemetry for directors—multiplying per-bike ASPs. Conversely, fitness and commuting’s 47.18% share demonstrates mass-market volume, anchoring baseline demand through daily utility. The GPS bike computers market size is attributable to fitness commuters growing exponentially in 2025, and loyalty stems from safe-route suggestions and theft-alert integration.

The GPS bike computers industry also sees gravel and bikepacking riders demanding rugged casings and offline topo maps. Adventure enthusiasts accept a higher MSRP when solar panels cut power-bank weight, aligning with the segment’s self-supported ethos. Regulatory nuances, such as UCI display restrictions during racing sprints, shape UI decisions across all tiers.

By Product Type: Solar-Powered Mapping Units Gain Traction

Mapping models generated 63.46% of revenue in 2024 as turn-by-turn guidance morphed into a hygiene factor. The addition of on-device POI search and color touchscreens fuels uplift. Solar-powered mapping computers, while accounting for a minimal portion of the 2024 volume, are projected to grow considerably by 2030, reflecting a 6.47% CAGR that outstrips the broader GPS bike computers market. The underlying photovoltaic substrate adds a minimal material cost but extends battery longevity by double-digit percentages.

Non-mapping units remain relevant in time-trial disciplines where aero drag and weight trump navigational aids. However, firmware-defined upgrades allow certain mid-range SKUs to unlock maps post-purchase, creating deferred revenue streams. Component convergence—identical SoCs across mapping and non-mapping SKUs—enables cost efficiencies even as feature sets diverge.

By Bike Type: E-Bike Integration Rewrites Feature Priorities

E-bikes generated significant revenue in 2025, translating into the most important GPS bike computers market size slice for bike-type segmentation. Motor manufacturers expose CAN or UART data channels that head-units parse to forecast residual range in real time. Despite losing relative share, road bikes influence aerodynamics-led accessory design, such as flush mounts that maintain airflow. Mountain bike adoption benefits from depth maps that color-code trail gradients, a feature popularized by online platforms like Trailforks, now mirrored offline on-device to preserve phone batteries.

Cargo and utility bikes open enterprise prospects: fleet operators monitor delivery routes, driver behavior, and dwell times via cloud dashboards, monetizing data analytics rather than relying solely on hardware margin. Insurance underwriters pilot pay-as-you-ride schemes predicated on verified GPS logs, anchoring additional SaaS potential for vendors.

By Connectivity: eSIM Catapults Real-Time Services

While ANT+ and Bluetooth secured a 52.38% share in 2024, eSIM variants exhibit the steepest 6.38% CAGR as operators roll out machine-to-machine data bundles below USD 1 per month. Live weather alerts, group-ride geofencing, and in-ride Strava segment ranking hinge on uninterrupted uplinks that phone tethering cannot guarantee in low-coverage zones. Wi-Fi remains relegated to post-ride uploads but gains importance for over-the-air firmware pushed weekly to rectify GNSS ephemeris bugs.

Regulatory compliance around IMEI registration in India and Brazil complicates import timelines, pushing vendors toward regional SKUs. Nevertheless, cellular unlocks emergency-response value propositions attractive to parents and solo adventurers, helping justify premium pricing even in cost-conscious markets.

By Price Tier: Premium Innovation Filters Downward

Premium SKUs, priced above USD 450, are growing at a robust CAGR of 6.39% through 2030. They integrate contactless payments, on-device music storage, and multi-band GNSS antennas. Though only one-fifth of the 2024 volume, they drive a significant portion of gross profit, funding R&D migrating to mid-range lines, which accounted for 46.51% market share in 2024.

The GPS bike computers market benefits from trickle-down dynamics: multi-band GNSS costs fell robustly YoY, enabling 2025 mid-range launches with features previously exclusive to flagships. Budget SKUs risk obsolescence unless they bundle at least breadcrumb-style navigation and ANT+ sensor support, aspirational requirements.

By Distribution Channel: Direct-to-Consumer Reshapes Economics

Online brand stores captured 41.26% share as riders bypass traditional retailers for nationwide next-day shipping and firmware-update transparency, and are also growing at a robust CAGR of 6.44% through 2030. Brands such as Wahoo deploy virtual concierge chat to guide sensor pairing, mitigating the support void once filled by specialty bike shops.

Nevertheless, brick-and-mortar independents retain relevance for test rides and complex cockpit installations. OEM bundling is poised to swell as e-bike firms pre-install proprietary head-units, locking customers into aligned app ecosystems at the point of sale.

Geography Analysis

Europe contributed 38.44% of 2024 revenue, anchored by dense cycling lanes in the Netherlands, Germany, and Denmark that sustain daily utility riding. EU subsidies for e-cargo bikes catalyze commercial fleet uptake, broadening enterprise demand beyond enthusiast circles. The GPS bike computers market size tied to European subsidy programs is expected to increase significantly by 2030, contingent on continued municipal grants.

Asia-Pacific posts the fastest 6.41% CAGR, propelled by China’s e-bike volume and Japan’s silver-age fitness culture that values health analytics. Local brands leverage competitive manufacturing costs to release multiple mapping units, expanding addressable consumer segments. Australia’s gravel boom further drives premium adoption across the outback, where satellite coverage gaps favor dual-frequency receivers.

North America maintains robust replacement cycles driven by weekend endurance events and the rise of bikepacking tourism in U.S. national forests. However, urban cannibalization from smartwatches limits upside in metropolitan corridors. Latin America and the Middle East/Africa remain nascent, yet infrastructure investments paired with smartphone penetration position them as long-term upside once ASPs moderate.

Competitive Landscape

Garmin leads with an integrated stack—proprietary silicon, OS, and cloud services—yielding massive 2024 fitness revenue and a hardware gross margin above three-fifths. Wahoo Fitness, though smaller, commands loyalty via simplified UI and a trade-in program that reduces friction for annual upgrades. SRAM-backed Hammerhead leverages Android to accelerate feature cadence, recently releasing CLIMB+ that auto-detects gradient shifts.

Asian challengers Bryton, Magene, and Coospo compress development cycles to under nine months, responding swiftly to chipset price drops. Their aggressive MSRP strategy garners share in price-sensitive ASEAN and LATAM markets, where the GPS bike computers market still battles smartphone substitutes. Strategic partnerships define the next competitive frontier: Stromer’s pact with Spoke Safety embeds V2X chips, positioning future e-bikes as nodes in connected traffic ecosystems [3]“Spoke Safety Partnership Press Release,” Stromer AG, stromerbike.com .

Patent filings indicate rising R&D around optic flow sensors to augment GNSS in tree cover, reflecting a shift from pure satellite dependence to sensor fusion. M&A chatter centers on component suppliers specializing in flexible solar films, a chokepoint for scaling photovoltaic head-units. Overall, competitive intensity remains moderate; top five vendors held roughly three-fifth combined revenue in 2024, leaving room for specialist entrants targeting cargo fleets and gravel adventures.

GPS Bike Computers Industry Leaders

Garmin Ltd

Wahoo Fitness LLC

Hammerhead

Bryton Inc.

Giant Manufacturing Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Garmin introduced the Edge MTB, adding tactile side buttons and G-force-based crash alerts for alpine trail riders.

- August 2024: Stromer and Spoke Safety unveiled a V2X roadmap to broadcast cyclist position to connected cars, with pilot fleets slated for 2026.

- June 2024: Garmin released the Edge 1050, which features a 3.5-inch color touchscreen, integrated speaker, and Garmin Pay.

Global GPS Bike Computers Market Report Scope

GPS bike computers are specialized devices used by cyclists to track and monitor their rides. Equipped with global positioning system (GPS) technology, these devices provide real-time location data, navigation assistance, and performance metrics such as speed, distance, and elevation.

The scope of the report covers segmentation by type, application, and geography. By type, the market is segmented into mapping and non-mapping. By application, the market is segmented into athletics and sports, fitness and commuting, and recreational/leisure. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World.

For each segment, market sizing and forecasts have been done based on value (USD).

| Athletics & Sports |

| Fitness & Commuting |

| Recreational / Leisure |

| Professional Racing |

| Bikepacking / Adventure |

| Mapping GPS Bike Computers |

| Non-mapping GPS Computers |

| Solar-powered Mapping Units |

| Road Bicycles |

| Mountain Bikes |

| E-Bikes |

| Gravel / Cyclocross |

| Other Bikes |

| ANT+ Only |

| ANT+ & Bluetooth |

| Wi-Fi Enabled |

| Cellular eSIM |

| Premium |

| Mid-range |

| Budget |

| Online Direct-to-Consumer |

| Specialty Bike Stores |

| Mass Retail |

| OEM-Bundled Sales |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia & New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Athletics & Sports | |

| Fitness & Commuting | ||

| Recreational / Leisure | ||

| Professional Racing | ||

| Bikepacking / Adventure | ||

| By Product Type | Mapping GPS Bike Computers | |

| Non-mapping GPS Computers | ||

| Solar-powered Mapping Units | ||

| By Bike Type | Road Bicycles | |

| Mountain Bikes | ||

| E-Bikes | ||

| Gravel / Cyclocross | ||

| Other Bikes | ||

| By Connectivity | ANT+ Only | |

| ANT+ & Bluetooth | ||

| Wi-Fi Enabled | ||

| Cellular eSIM | ||

| By Price Tier | Premium | |

| Mid-range | ||

| Budget | ||

| By Distribution Channel | Online Direct-to-Consumer | |

| Specialty Bike Stores | ||

| Mass Retail | ||

| OEM-Bundled Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the GPS bike computers market by 2030?

The market is forecast to reach USD 988.29 million by 2030, growing at a 6.31% CAGR.

Which bike type is driving the fastest demand for dedicated head-units?

E-bikes lead both share (37.81% in 2024) and growth (6.49% CAGR), reflecting integration needs with motor systems.

How does cellular eSIM connectivity benefit cyclists?

ESIM enables live tracking, over-the-air updates, and emergency alerts without phone tethering, fueling a 6.38% CAGR for this segment.

Which region shows the highest growth outlook?

Asia-Pacific is projected to expand at a 6.41% CAGR thanks to rapid e-bike adoption and government micromobility incentives.

Who is the current market leader in premium GPS bike computers?

Garmin maintains the lead, supported by USD 1.8 billion in 2024 fitness revenue and a vertically integrated ecosystem.

Page last updated on: