Automotive Fascia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

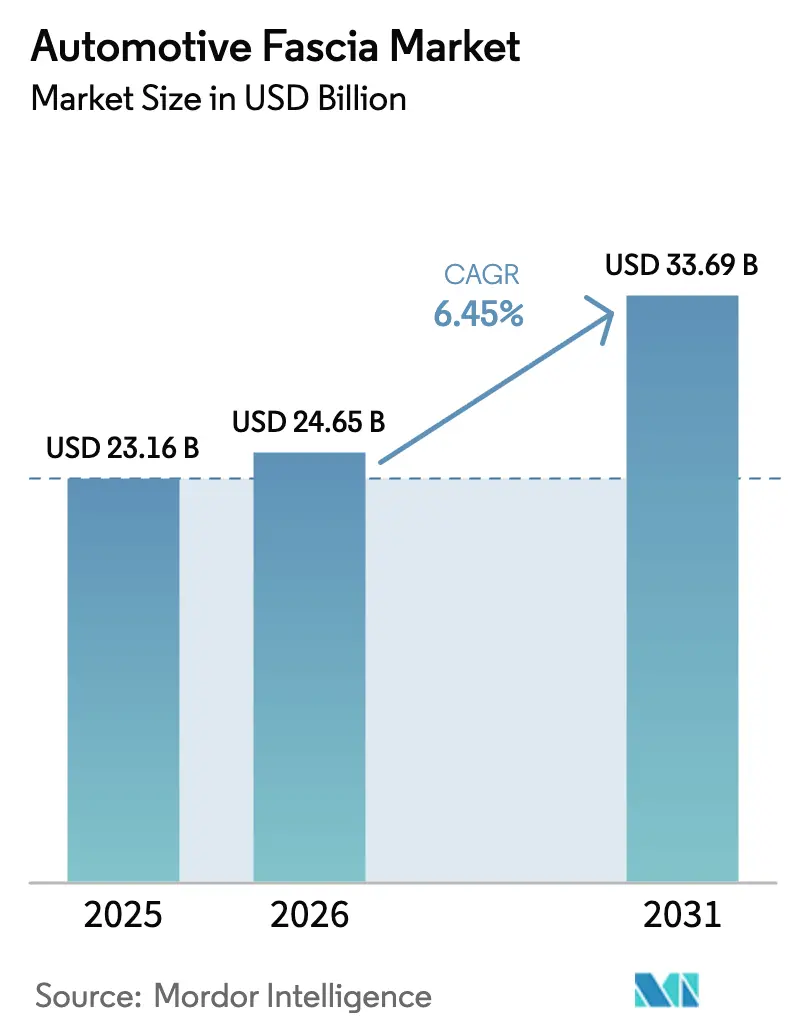

| Market Size (2026) | USD 24.65 Billion |

| Market Size (2031) | USD 33.69 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fascia Market Analysis by Mordor Intelligence

The Automotive Fascia Market size was valued at USD 23.16 billion in 2025 and estimated to grow from USD 24.65 billion in 2026 to reach USD 33.69 billion by 2031, at a CAGR of 6.45% during the forecast period (2026-2031). Continued electrification, tighter pedestrian-safety rules, and the push for lighter front-end modules redefine how bumpers, grilles, and lighting treatments come together. OEMs are shifting from stand-alone bumpers to fully integrated sensor platforms that house LiDAR, radar, and cameras while managing battery-cooling airflow. The European Union’s 2023 End-of-Life Vehicles update obliges automakers to raise recycled-plastic content, accelerating use of next-generation polyolefins and recycled aluminum skins[1]“End-of-Life Vehicles Directive Revision 2023,” European Commission, europa.eu .

Key Report Takeaways

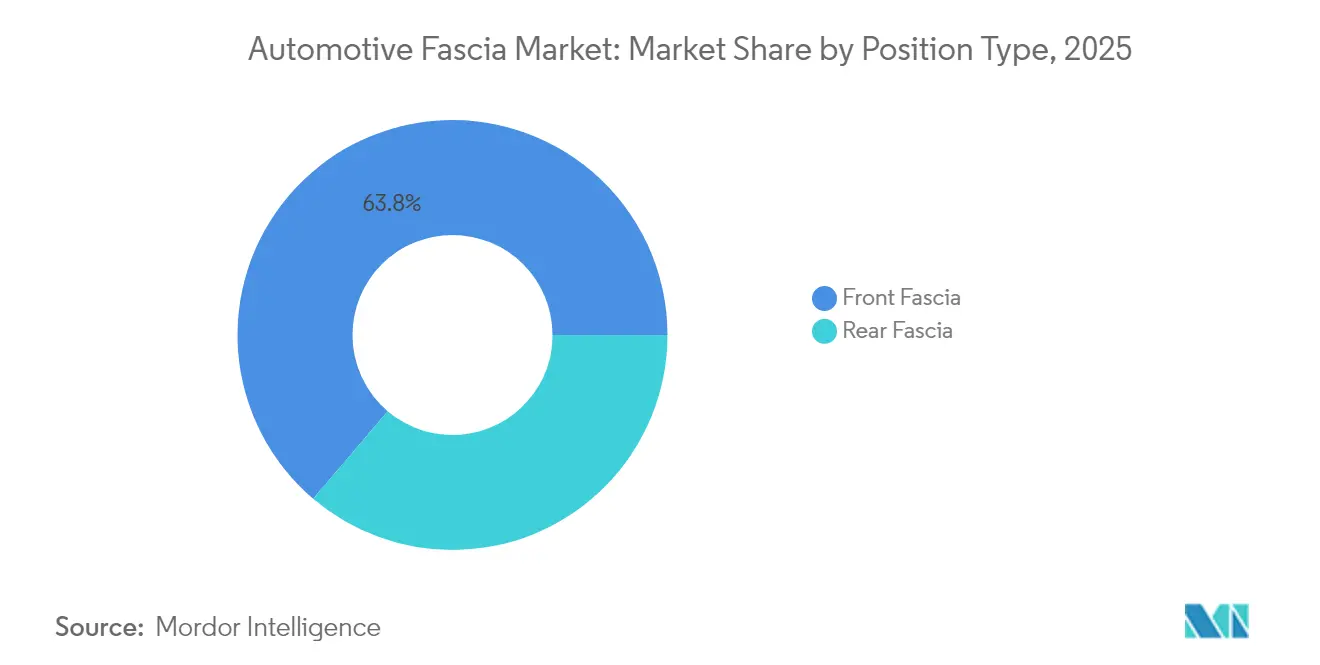

- By position type, front fascia commanded 63.78% of the automotive fascia market share in 2025 and is expanding at a 6.66% CAGR through 2031.

- By material, plastic-covered styrofoam held 46.10% of the automotive fascia market size in 2025, whereas plastic-covered aluminum is projected to grow at 5.96% CAGR to 2031.

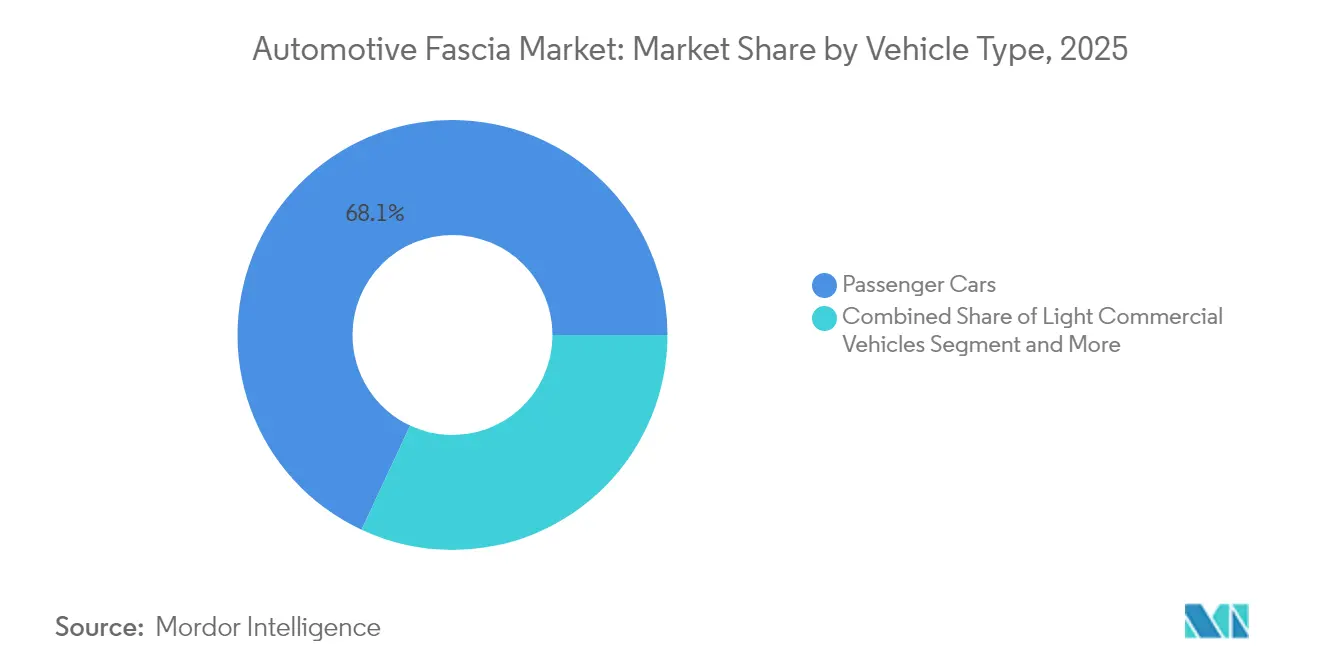

- By vehicle type, passenger cars accounted for 68.05% share of the automotive fascia market size in 2025 while electric passenger cars are advancing at a 7.01% CAGR through 2031.

- By sales channel, OEM supply held 85.88% share of the automotive fascia market size in 2025, yet the aftermarket is rising at 7.38% CAGR over the same period.

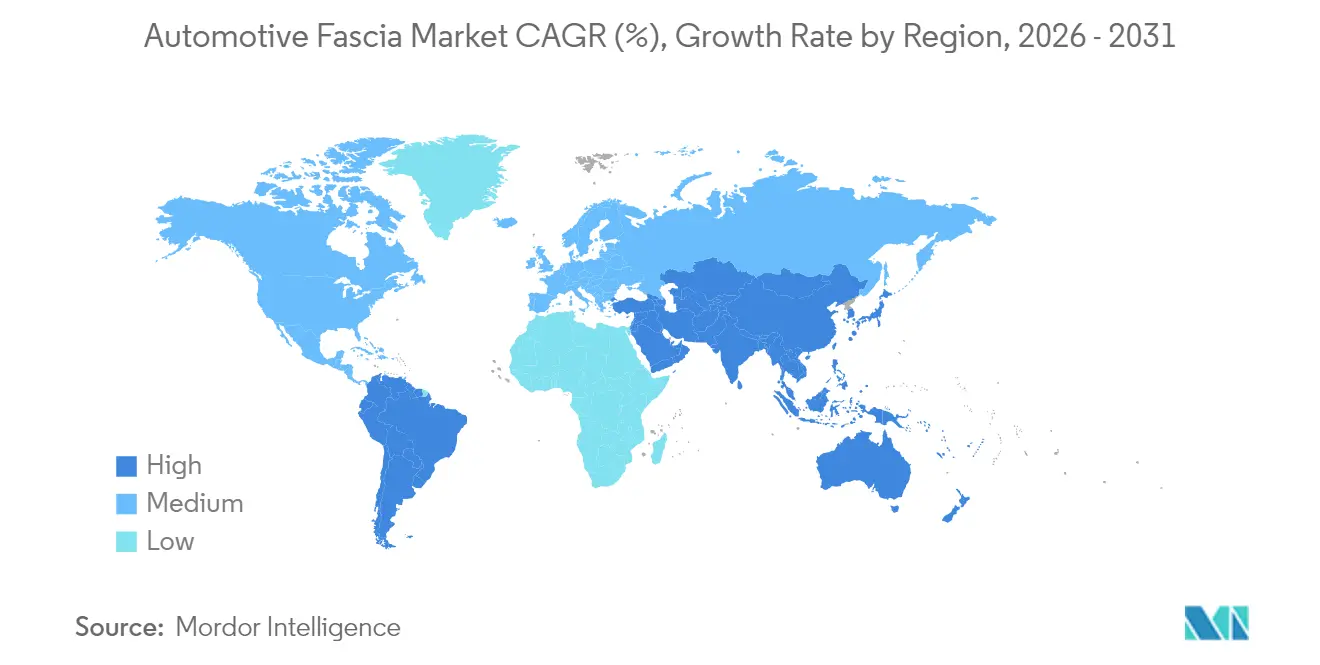

- By geography, Asia Pacific led with 47.96% revenue share in 2025, while South America is projected to record a 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Fascia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of EV & Autonomous Vehicle | +2.1% | Global, led by China and Europe | Long term (≥ 4 years) |

| Lightweighting & Emission-Regulation | +1.8% | North America and EU primarily, expanding to Asia | Long term (≥ 4 years) |

| Integration of Advanced Sensing | +1.3% | North America, Europe, China | Medium term (2-4 years) |

| Increasing Vehicle Production & Sales | +1.2% | Global, with concentration in Asia-Pacific | Medium term (2-4 years) |

| Modular Front-End Modules Adoption | +0.9% | Global, with early adoption in premium segments | Medium term (2-4 years) |

| Shift to Recycled & Bio-Based Polymers | +0.7% | EU and North America leading, global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of EV and Autonomous Vehicle Platforms

Electric vehicles change cooling loads and open grille-less design options, forcing suppliers to redesign fascia modules that can mount LiDAR, 4D radar, and high-resolution cameras without raising drag. Hyundai Mobis has introduced integrated front-face units for battery cars that package active shutters, millimeter-wave radar, and camera cleaning systems into a single sub-assembly. Additionally, Marelli announced a partnership with Hesai to embed LiDAR into headlamp housings, shifting sensing hardware from bumper skins to lighting clusters. Moreover, premium 800-volt EVs need electromagnetic shielding for high-frequency switching, so fascia panels blend aluminum films with plastic topcoats for EMI control.

Light-weighting and Emission-Regulation Compliance

Stricter CO2 caps in the EU and CAFE targets in North America push OEMs toward lighter structures that still pass FMVSS impact tests. Carbon-fiber reinforced plastics cut as much as 60% mass versus steel yet deliver the same crush-energy absorption. Constellium’s M-LightEn consortium commercializes ultra-high-strength aluminum grades with 80% recycled content, reducing component carbon intensity by half[2]“Project M-LightEn: Lightweight Solutions with 80% Recycled Aluminum,” Constellium SE, constellium.com . Toyoda Gosei is validating cellulose-nanofiber reinforced polypropylene to trim weight and cradle-to-grave emissions. Sensor additions add weight back in, so engineers juggle mass savings with LiDAR housings and radar radomes.

Integration of Advanced Sensing (LiDAR/Radar) into Fascia

ADAS adoption turns the fascia into an active sensing surface. Radar-transparent polycarbonate blends and thin paint formulas are now specified to ensure 77-81 GHz signals are not attenuated. Aeva and AGC’s Wideye division have demonstrated FMCW LiDAR units that mount behind glass, freeing bumper real estate for styling while preserving aerodynamic efficiency. Aptiv’s corner-radar strategy points to a distributed sensor layout that may reduce large central radar modules in the bumper but increases side-fender integration needs. Suppliers must balance structural stiffness, low dielectric loss, and paint durability within tight packaging envelopes.

Modular Front-End Modules Adoption by OEMs

Just-in-sequence delivery of complete front-end modules can cut line-side labor and capital outlay. LANXESS’s hollow-profile hybrid combines metal and plastic in a single shot to yield a torsionally stiff carrier that routes cooling fluid and cable harnesses. EV cooling loops are simpler, letting suppliers integrate radiator frames and pedestrian-impact beams into one unit. While modularization raises content per vehicle for Tier 1 firms, it also forces them to master logistics and thermal, lighting and sensor domains traditionally handled by different suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Same Raw-Material Price Volatility | -1.1% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| High Maintenance & Replacement Cost | -0.8% | Global, particularly in premium vehicle segments | Medium term (2-4 years) |

| ADAS-Led Fall in Collision Frequency | -0.6% | North America and Europe leading | Long term (≥ 4 years) |

| OEM Vertical Integration Curbing Aftermarket | -0.4% | Global, concentrated in EV platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Maintenance and Replacement Cost

Calibration of radar and camera modules after a minor parking scrape can lift repair bills by 37%, challenging insurer economics and consumer willingness to pay. OEM-approved bumper paints must remain radar-transparent, narrowing repair-paint options and steering work to certified centers with costly alignment rigs. Independent shops face five-figure investments in ADAS calibration bays, prompting market consolidation. The higher part complexity also boosts idle time, raising rental-car days and pushing insurers to negotiate deeper part discounts with Tier 1 vendors.

ADAS-Led Fall in Collision Frequency

Forward-collision warning and automatic emergency braking reduce front-end impacts, the very events that generate steady fascia-replacement revenue. A study suggests that up to 8,700 crashes and 70 fatalities could be prevented in the United States by 2040, trimming demand for front bumpers. Fewer accidents hurt volume, but deeper technology in each bumper raises the average selling price. European repair groups are pivoting to subscription-based service contracts, focusing on maintenance routines and software updates instead of collision repair.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Position Type: Front Fascia Drives Innovation

Front fascia assemblies represented 63.78% automotive fascia market share in 2025, underscoring their central role in aerodynamic drag reduction and pedestrian protection. This segment is forecast to progress at a 6.66% CAGR, fuelled by the need to mount high-definition cameras, long-range radar and cleaning nozzles without enlarging frontal area. Successive design cycles now route washer-fluid channels and heating elements directly into the bumper beam to guarantee sensor uptime in icy climates. Rear fascia systems trail in revenue but are also evolving to accommodate smart-lighting arrays and parking radars that help automated-parking software.

Valeo has begun validating fascia skins printed with embedded micro-LED matrices that deliver dynamic turn signals and cyclist alerts, a preview of communication-centric exteriors. The upcoming NHTSA FMVSS No. 228 rule changes amplify the need for compliant crush cans and deformable foams that maintain head-injury criteria below 1,000 HIC, driving deeper collaboration between polymer chemists and crash-simulation engineers. Bio-polypropylene foams with tuned cell geometry have emerged as candidates to balance energy absorption with recyclability.

By Material: Aluminum Gains Ground under Lightweight Mandate

Plastic-covered styrofoam retained a 46.10% slice of the automotive fascia market in 2025 due to mature molding economics and global tooling availability. Yet plastic-covered aluminum panels are on track for a 5.96% CAGR to 2031 as EV makers exploit aluminum’s thermal conductivity to dissipate inverter heat. Thin 1 mm aluminum substrates laminated with impact-modified PP outer skins weigh 15% less than comparable PP/EPP foams while passing pedestrian impact. Emerging composite skins blend bio-polyurethane back-foams with recycled aluminum films, allowing OEMs to advertise lower cradle-to-gate CO2.

MacDermid Enthone has released anodizing chemistries that accept low-temperature plastics over-molding without blistering, streamlining joins between metal and polymer skins. Recycled aluminum scrap flows from beverage cans into Constellium grades, proving automotive fascia industry progress toward circularity. Steel and rubber blends hold niche beachheads in heavy-duty trucks where stone-chip resistance outweighs weight concerns.

By Vehicle Type: Electric Passenger Cars Lead Growth Curve

Passenger cars delivered 68.05% of 2025 revenues in the automotive fascia market, reflecting global build volumes. Electric passenger cars are the fastest riser, with a 7.01% CAGR projected through 2031. Grille-less EV faces present smooth surfaces that can host brand-signature lighting strips and hidden sensors, motivating design studios to collaborate with Tier 1 fascia specialists early in program cycles. Light commercial vans need ruggedized bumpers that tolerate frequent curb contacts; however, last-mile delivery electrification is nudging this segment toward composite skins that resist low-speed knocks yet weigh less.

BMW’s Neue Klasse sedan, starting production in 2025, uses a flush fascia with active-air flaps that open only during battery fast-charge cooling cycles, demonstrating the intersection of thermal management and styling. Cellular PP foams infused with natural fibers damp inverter whine while shedding kilograms relative to glass-filled nylon. Medium and heavy trucks still specify high-durometer elastomer skins, but sensor fusion for highway-pilot systems will gradually raise content value even in this conservative space.

By Sales Channel: Aftermarket Finds Niche Growth

OEM installations dominated delivery lines with an 85.88% hold on the 2025 automotive fascia market share, supported by platform-wide standardization of sensor packages. Despite fewer collisions, the aftermarket is set for a 7.38% CAGR because calibration services, paint systems matched to radar transparency, and subscription-based software updates create new billable items. North American collision shops now advertise “ADAS-ready” bumper replacements that include calibration tokens coded to a specific VIN.

The European independent aftermarket keeps a 60% share of the spare-parts pool by adding remote-diagnosis and digital-inventory services. E-commerce pure-plays in the United States are forecast to lift online bumper sales between 2025 and 2029 by bundling paint-to-order services, compressing delivery lead times from weeks to days. OEM vertical integration on EV programs restricts third-party access to design blueprints, but right-to-repair legislation in several US states moderates that control.

Geography Analysis

In 2025, Asia Pacific secured 47.96% of the revenue share, solidifying its position as the manufacturing epicenter of the automotive fascia market. China is one of the largest producers of vehicles in 2024 and keeps scaling gigacasting pilots that could roll fascia, crash beam, and battery tray into one aluminum shot, reducing part counts. India’s auto-components roadmap targets a USD 200 billion turnover by FY26, supported by production-linked incentives that reimburse up to 13% of local value addition. Honda’s CAD 15 billion (USD 11 billion) commitment to develop a Canadian EV supply chain will open new North American export routes for Asian Tier 1 tooling firms.

South America is the fastest-growing region, with a 6.98% CAGR as Stellantis channels EUR 5.6 billion into Bio-Hybrid drivetrain platforms built in Brazil and Argentina. Bio-ethanol-compatible bumpers require coatings resistant to sugar-based fuel sprays, prompting local formulators to adapt resin chemistries. Colombia has become the region’s third-largest assembler, while Peru leverages free-trade agreements to ship plastic inserts and chrome trims into the United States duty-free. Exchange-rate volatility remains a cost-planning hurdle, so suppliers increasingly hedge resin contracts in USD.

North America and Europe retain strategic importance as regulation trend-setters. NHTSA’s pending pedestrian rule is already embedded in 2026 model-year North American fascia designs. The EU Circular Economy Action Plan pushes recyclates into trim components and incentivizes digital passports that log resin genealogy. War-risk premiums on Red Sea freight lanes have nudged OEMs toward near-shoring fascia tool builds in Mexico and Eastern Europe. Europe’s EV adoption pace demands fast cycles on grille-less styling; conversely, US demand is tied to charging-infrastructure roll-outs, leading to phased tooling plans that mix ICE and EV fascias on the same line for risk mitigation.

Competitive Landscape

Competitive intensity is moderate as the top five suppliers command roughly two-thirds of global fascia revenue, leaving room for niche specialists focused on sensor transparency and bio-materials. Plastic Omnium is channeling EUR 300 million toward hydrogen tank and fuel-cell integration that could place the firm at the center of zero-emission commercial-vehicle fascia assemblies. Magna is collaborating with NVIDIA on Level 2+ to Level 4 active-safety stacks, positioning its e-beam grille shutters and surround-view fascia trims as hardware anchors for over-the-air software features[3]“Magna and NVIDIA Expand ADAS Partnership,” Magna International Inc., magna.com. FORVIA leverages its seating and lighting portfolio to sell full-width lightbars behind color-matched polycarbonate bumper skins, bundling style and communication functions into one purchase order.

Gigacasting constitutes the most visible disruptive threat. Tesla’s 6,000-ton presses meld front structural rails with bumper attachments in a single aluminum melt, potentially shrinking the addressable market for bolt-on fascia carriers. Toyota, Ford, and Volvo are running feasibility prototypes, but pedestrian-impact zones and sensor replacements remain unresolved challenges that favor detachable bumper covers in the near term. Suppliers are hedging by developing quick-replace skin panels that fasten to gigacast structures without adhesive, preserving aftermarket revenue streams.

White-space growth areas range from LiDAR integration brackets to bio-based polyurethane foams that match petroleum counterparts on impact strength. LANXESS markets flax-fiber reinforced thermoplastics that cut CO2 by 50% compared with glass-fiber staples while passing Euro NCAP pedestrian tests. LyondellBasell has introduced polypropylene compounds using mechanically recycled feedstock paired with mass-balance certified bio-naptha, appealing to OEM recyclability scorecards. The march toward software-defined vehicles is blurring lines between electronics and exterior trim, evident in the GM-Magna-Wipro SDVerse marketplace that lets automakers purchase software modules decoupled from hardware.

Automotive Fascia Industry Leaders

Magna International

Flex-N-Gate Corporation

Plastic Omnium

Faurecia SE

Samvardhana Motherson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BMW commenced production of the iX LCI at its Dingolfing plant, featuring up to 701 km WLTP range and 25% higher drive power, prompting new fascia-cooling layouts for higher current loads.

- February 2025: Polyplastics introduced PLASTRON LFT RA627P, a long cellulose-fiber reinforced polypropylene offering a lower carbon footprint than glass-fiber grades, targeting EV motor housings and fascia carriers.

Global Automotive Fascia Market Report Scope

Automotive fascia refers to a decorative panel that is mounted on top of the bumper at the front and rear end of the vehicle. A bumper valance panel, a piece that is mounted on top or under the bumper is also considered a part of the automotive fascia. Further, automotive fascia comprises space for grilles, headlamps, bumpers, and vehicle emblems, among others, and is designed to provide a unified appearance to a vehicle.

The automotive fascia market is segmented into position type, material, vehicle type, sales channel, and geography. Based on the position type, the market is segmented into front fascia and rear fascia. Based on the material, the market is segmented into plastic-covered styrofoam, plastic-covered aluminum, and other materials (steel, rubber, etc.). Based on vehicle type, the market is segmented into passenger cars and commercial vehicles. Based on sales channel, the market is segmented into original equipment manufacturer (OEM) and aftermarket. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

For each segment, the market sizing and forecast have been mentioned based on value (USD).

| Front Fascia |

| Rear Fascia |

| Plastic-covered Styrofoam |

| Plastic-covered Aluminum |

| Other Materials (Steel, Rubber, etc.) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Position Type | Front Fascia | |

| Rear Fascia | ||

| By Material | Plastic-covered Styrofoam | |

| Plastic-covered Aluminum | ||

| Other Materials (Steel, Rubber, etc.) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive fascia market and how fast is it growing?

The market is valued at USD 24.65 billion in 2026 and is forecast to reach USD 33.69 billion by 2031, growing at a 6.45% CAGR during the forecast period (2026-2031).

Which region holds the largest share of revenue?

Asia-Pacific leads with 47.96% of global revenue due to its dominant vehicle‐production base and mature supply chains.

What is the fastest-growing regional market through 2031?

South America is projected to expand at a 6.98% CAGR through 2031, supported by Stellantis’s EUR 5.6 billion investment in Bio-Hybrid vehicle programs.

Which product segment generates the most revenue?

Front fascia assemblies account for 63.78% of 2025 sales because they integrate aerodynamics, pedestrian-impact structures and ADAS sensors.

What main trends are propelling demand for new fascia designs?

Electrification, lightweighting mandates, and the need to embed LiDAR and radar in grille-less vehicle fronts are driving rapid product redesign cycles.

How concentrated is supplier competition in this industry?

The top five Tier 1 suppliers control considerable share of the automotive fascia market revenue, reflecting moderate concentration and ongoing opportunities for niche materials and sensor specialists.

Page last updated on: