Particle Counters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

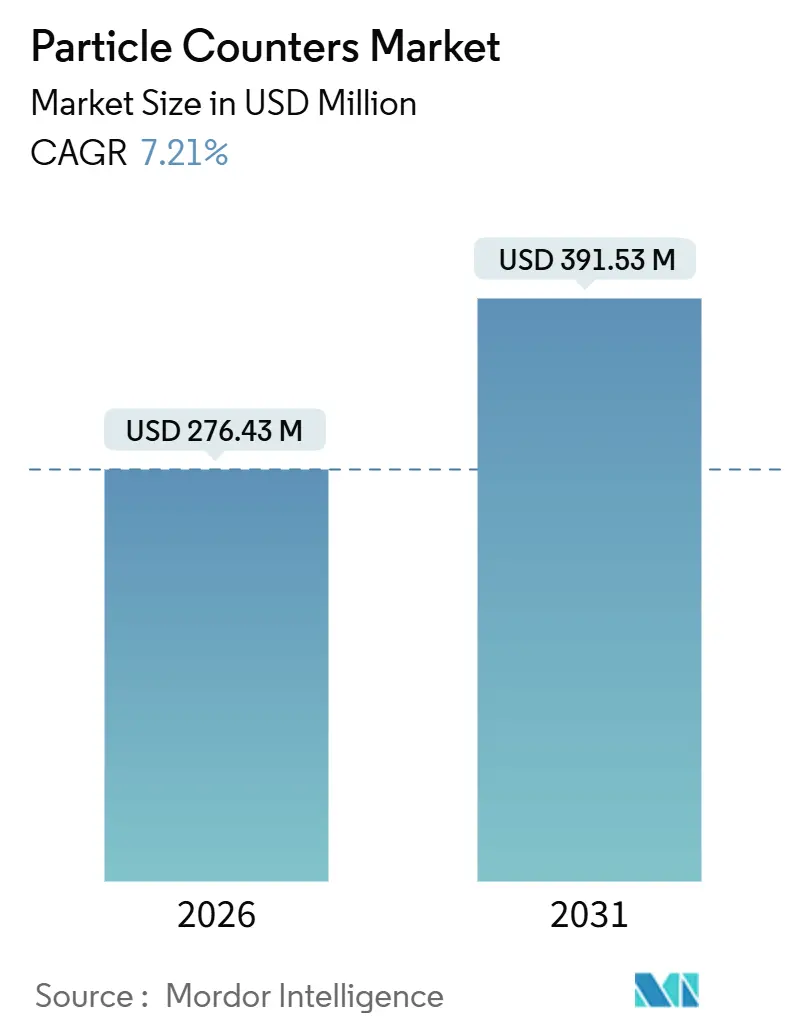

| Market Size (2026) | USD 276.43 Million |

| Market Size (2031) | USD 391.53 Million |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

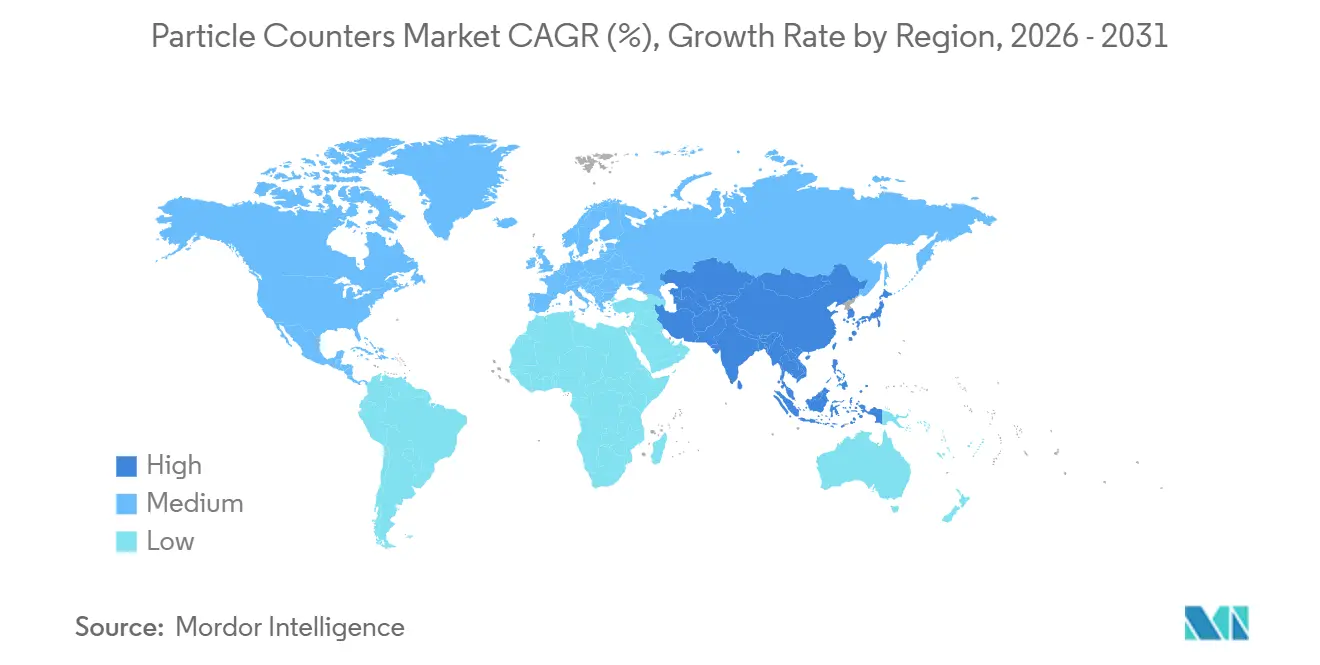

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Particle Counters Market Analysis by Mordor Intelligence

The Particle Counters Market size is estimated at USD 276.43 million in 2026, and is expected to reach USD 391.53 million by 2031, at a CAGR of 7.21% during the forecast period (2026-2031).

This growth trajectory stems from revised GMP Annex 1 rules mandating continuous viable and non-viable monitoring, semiconductor fabs moving to 2-nanometer logic nodes that require sub-10 nanometer detection, and large-scale ambient air-quality programs across Asia that are expanding monitoring density by an order of magnitude. Demand is further reinforced by cell-therapy cleanrooms, EV battery gigafactories with ultra-dry rooms, and AI-enabled predictive maintenance platforms that cut calibration costs. As a result, buyers are migrating from standalone handheld units to networked remote counters that integrate audit-trail automation, edge analytics, and cloud-based data integrity.

Competition pivots on three levers: sensitivity, connectivity, and service. Incumbents led by Danaher, TSI, and Spectris are bundling water-based condensation technology, 21 CFR Part 11 software, and ISO/IEC 17025 onsite calibration to preserve recurring revenue. Niche firms target price-sensitive segments with simplified optics and subscription-free firmware, while integrators introduce digital twins that predict sensor drift. Regional dynamics amplify these strategies. North America favors high-value pharmaceutical and advanced logic fabs; Asia-Pacific scales massive ambient networks and gigafactories; Europe lags as fab postponements delay new orders. Collectively, these trends underpin an enduring replacement cycle, sustaining the particle counters market as a critical instrumentation niche across health, electronics, energy, and climate research.

Key Report Takeaways

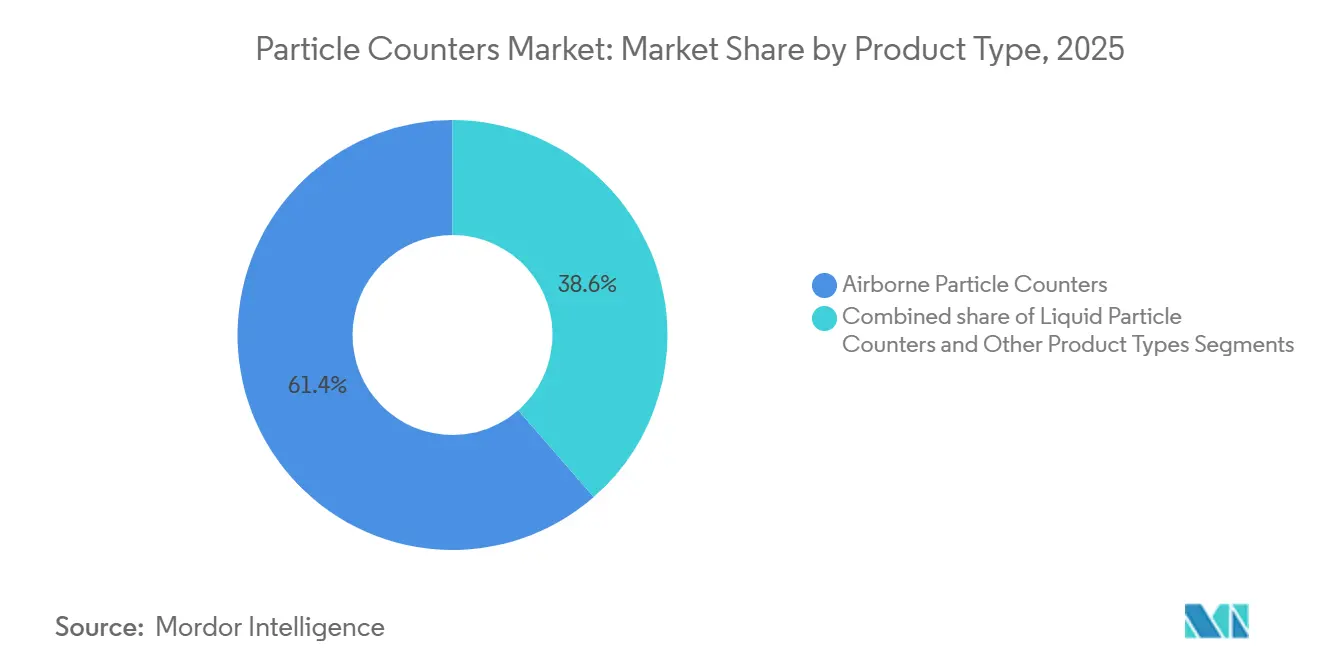

- By product type, airborne counters led with a 61.42% market share of particle counters in 2025, while liquid counters are projected to expand at a 9.32% CAGR through 2031.

- By application, cleanroom monitoring accounted for 64.09% of the particle counter market size in 2025; aerosol monitoring and research are forecasted to advance at an 8.97% CAGR through 2031.

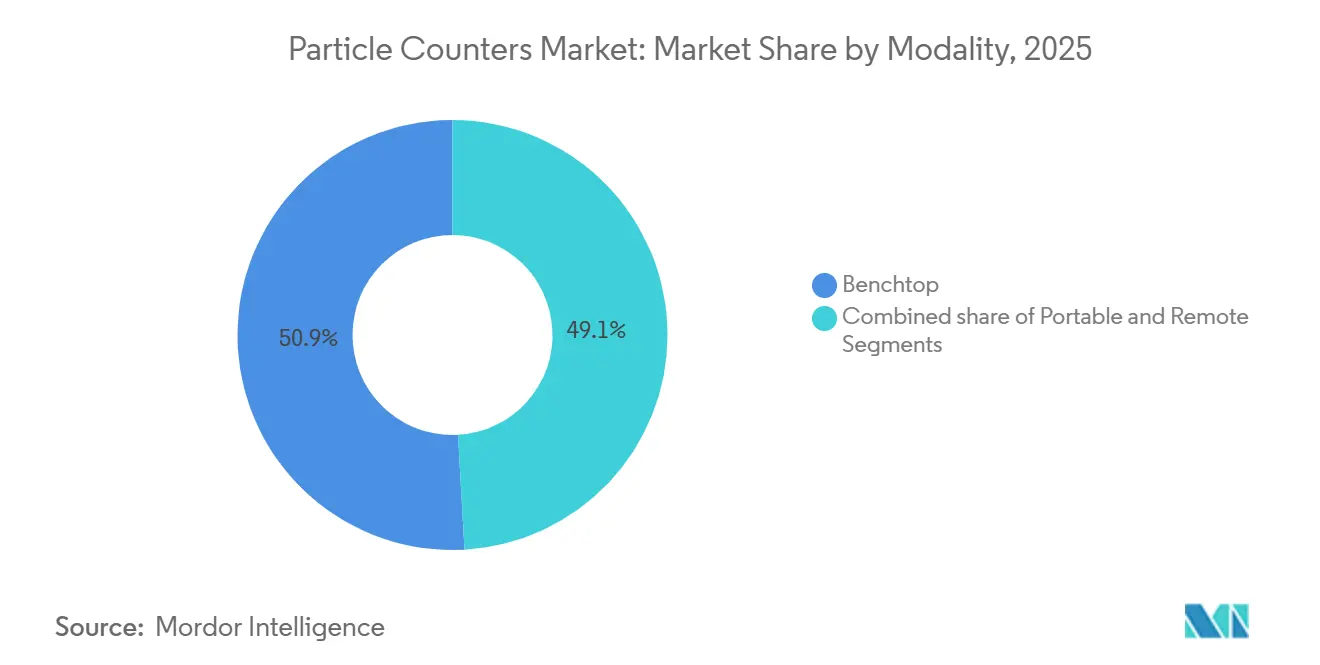

- By modality, benchtop instruments held 50.89% share of the particle counters market in 2025, whereas remote instruments are poised for an 8.68% CAGR between 2026 and 2031.

- By end user, pharmaceutical and biotechnology companies captured 38.20% of the particle counters market in 2025; academic and research institutes are projected to grow at a 9.67% CAGR through 2031.

- By geography, North America accounted for 41.65% of the particle counters market in 2025, but the Asia-Pacific region is expected to grow at an 8.18% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Particle Counters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Cleanroom Standards | +1.8% | North America, Europe | Medium term (2-4 years) |

| Rapid Growth in Biologics & Cell-Therapy | +1.5% | North America, Asia-Pacific | Medium term (2-4 years) |

| Sub-Micron Monitoring for 2 nm Semiconductors | +1.3% | Taiwan, South Korea, Japan, United States | Long term (≥ 4 years) |

| EV Battery Gigafactories & Ultra-Dry Rooms | +1.0% | Germany, China, South Korea | Medium term (2-4 years) |

| Government-Funded Ambient Networks | +0.9% | India, China, Southeast Asia | Short term (≤ 2 years) |

| AI-Enabled Predictive Maintenance | +0.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Global Cleanroom Standards (ISO 14644 & GMP Annex 1)

As of August 2023, Annex 1 requires sterile drug manufacturers to maintain continuous particle logs in Grade A and B zones, replacing periodic spot checks. ISO 14644-5:2025 further allows operators to extend requalification intervals from six to 24 months when online data demonstrates compliance, thereby reducing downtime and validation costs. Instruments such as Beckman Coulter’s MET ONE 3400+ automate SOPs and audit trails, ensuring one-click compliance for FDA inspectors[1]. Companies that have delayed upgrades now face heightened regulatory scrutiny, accelerating a replacement wave across legacy handheld fleets.

Rapid Growth in Biologics and Cell-Therapy Manufacturing

Single-use bioreactors pose unseen breach risks, prompting CDMOs to install real-time particle counters in filling suites that can flag bag failures before USD 5 million batches are lost. The FDA’s 2024 guidance on advanced therapies treats environmental monitoring as a critical quality attribute, cementing continuous particle trending as standard practice. TSI’s BioTrak counter differentiates viable microbes from inert particles, closing a long-standing data gap that once forced operators to cross-reference separate air samplers. More than 1,200 active cell-therapy trials concentrate demand in the United States and China, fuelling strong unit sales to facilities that reconfigure cleanrooms between campaigns.

Accelerating Semiconductor Node Shrink Demanding Sub-Micron Monitoring

At the 2-nanometer node, a stray 20 nm contaminant can short adjacent transistors and crater yield. Traditional optical counters typically stop at roughly 100 nm, so fabs often adopt condensation particle counters that generate aerosols for optical detection. TSI’s Nano LPM, launched in November 2025, delivers accurate 10 nm liquid detection by aerosolizing UPW and counting residuals with water-based condensation optics, eliminating microbubble artifacts that plagued earlier systems. Capital intensity reinforces the value proposition: a 0.1% yield gain at a USD 40 billion fab offsets millions of dollars in sensor spending.

Surge in EV Battery Gigafactories and Ultra-Dry Room Adoption

Lithium-ion cathode coating runs below 1% RH to curb lithium oxidation, necessitating ISO Class 6-8 rooms with continuous particle tracking. Volkswagen’s 40 GWh Salzgitter plant already fields more than 200 remote counters networked via industrial Ethernet. Yet, low humidity shifts the refractive indices of laser beams, so algorithms now auto-correct for moisture to contain sizing errors within 15%. Tesla’s Nevada facility couples predictive maintenance software to these sensors, cutting unplanned downtime by roughly 20% and underscoring how digital twins amplify instrument ROI.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx for HEPA-Grade Environments | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Scarcity of Certified Calibration Capacity | -0.6% | Asia-Pacific, Middle East & Africa, Latin America | Long term (≥ 4 years) |

| Sensor Drift in High-Humidity Lines | -0.4% | Southeast Asia, India, Brazil | Short term (≤ 2 years) |

| European Fab Consolidation | -0.3% | Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for HEPA-Grade Controlled Environments

Constructing an ISO Class 7 cleanroom averages USD 1,500-3,000 per ft², while a 20-counter network can add USD 200,000 in hardware alone. Recurring services—such as filters, calibration, and licenses—absorb 20-30% of that outlay each year, posing a challenge to smaller CDMOs and academic labs. Many generic producers in Southeast Asia, therefore, rely on handheld validation instead of continuous monitoring, accepting higher regulatory risk to conserve cash. Leasing and calibration-as-a-service models have emerged, yet uptake is slow because asset-heavy firms prefer ownership for depreciation benefits.

Scarcity of Certified Calibration Technicians and Laboratories

Fully traceable calibration hinges on ISO/IEC 17025 labs that reference national metrology institutes. Fewer than 200 such labs worldwide offer aerosol calibration, and fewer than 30 serve the entire Indian subcontinent and Southeast Asia[2]National Institute of Standards and Technology, “Accredited Calibration Laboratories List,” nist.gov. Instruments shipped abroad face 4-week turnarounds and freight risks, so many owners run with expired certificates. Field-service teams from TSI and Beckman Coulter do bring portable transfer standards on-site, but the daily rates of USD 2,000-5,000 price out small facilities, reinforcing a two-tier compliance landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Counters Gain on Semiconductor Wet-Process Needs

Airborne particle counters retained 61.42% of the particle counters market share in 2025, cementing their role in pharmaceutical cleanrooms, wafer fabs, and national monitoring grids. Liquid particle counters, however, will register a 9.32% CAGR through 2031 as fabs push UPW purity into the single-digit parts-per-trillion range and gigafactories police deionized rinse water for metallic seeds that trigger dendrites. The particle counters market size for liquid applications is thus poised to narrow the volume gap with airborne units, while commanding higher margins due to sub-10 nm detection requirements.

Vendors now integrate aerosolization stages and water-based condensation optics to bypass Mie-scattering limits, enabling actual resolutions of 10 nm. Instruments such as the Nano LPM carry a 20-30% price premium but justify the cost by preventing scrap on USD 5 billion lithography lines. In contrast, aerodynamic and condensation sizers are used in inhaler validation, atmospheric science, and diesel filter testing. Although collectively accounting for less than 10% of shipment volume, these niche devices sustain steady demand from academic labs and regulatory agencies that require ultrafine resolution beyond standard optical microscopes.

By Application: Aerosol Research Rides Academic Funding Wave

Cleanroom Monitoring generated 64.09% of 2025 revenue as Annex 1 and ISO 14644 automation turned real-time logging from best practice into baseline expectation[3]. Yet Aerosol Monitoring and Research will post the quickest growth at 8.97% CAGR to 2031, propelled by the NSF’s ASCENT network and DOE aerosols-cloud programs that flood universities with grant funds for SMPS and condensation counters. The particle counters market size for research is therefore expanding faster than legacy pharma demand, a signal that public health and climate science are shifting industry frontiers.

Projects exploring ultrafine links to Alzheimer’s, cardiovascular disease, and atmospheric radiative forcing require instruments down to 10 nm. Manufacturers respond with dual-mode units that toggle between airborne and liquid channels, letting investigators capture both particle size and chemical fingerprint in a single run. Pharmaceutical and semiconductor labs also leverage these research-grade features to map root-cause mechanisms behind micro-contamination, blurring historical lines between production QA and academic discovery.

By Modality: Remote Units Capture Continuous-Monitoring Mandate

Benchtop units accounted for 50.89% of shipments in 2025 due to their high flow rates and established role in quarterly room certification. However, remote instruments are expected to grow at an 8.68% CAGR as operators retrofit Power-over-Ethernet nodes across ceiling grids and connect them to MES or BMS software for instant deviation alerts. The particle counters market embraces this shift because continuous data closes gaps left by episodic audits, thereby reducing batch-failure risk.

AeroTrak+ remote models include five-year laser warranties and onboard storage for six months, addressing lifetime cost anxieties that once deterred adoption. Portable counters remain vital for troubleshooting and field surveys, particularly in areas where calibration labs are scarce. They now pair dual channels and battery packs to fit personal exposure studies, expanding use cases beyond factory walls. Though average sale prices are lower, portability opens new buyer pools in hospitals, data centers, and food-processing plants that historically could not justify fixed installations.

By End User: Academic Institutes Accelerate on Aerosol-Health Research

Pharmaceutical and biotechnology companies held 38.20% of demand in 2025, anchored by sterile injectables and cell-therapy suites that cannot risk microbial ingress. Academic and Research Institutes, however, are slated to advance at a 9.67% CAGR as federal and foundation grants bankroll ultrafine-particle studies across epidemiology, climate, and materials science. The particle counters market size for universities is thus rising, both in terms of instrument count and technical sophistication, especially as on-campus nanofabs require ISO Class 5-7 containment.

Clinical labs utilize counters to validate the sterility of blood products and compounded medications, while aerospace and food processors adopt them for component cleanliness and HACCP programs. This spectrum underscores a bifurcated customer base: high-reliability buyers prioritize full life-cycle service, whereas grant-funded labs accept manual data pulls to stretch scarce budgets. Vendors are responding with tiered portfolios and subscription-based analytics, allowing users to upgrade capabilities without replacing hardware.

Geography Analysis

North America accounted for 41.65% of 2025 revenue, supported by FDA Annex 1-equivalent oversight and CHIPS Act incentives that underwrite the construction of new fabs in Arizona and Ohio. The particle counters market size in the region expands steadily because pharma and logic-node leaders treat continuous monitoring as non-negotiable for compliance and yield. ISO/IEC 17025 coverage exceeds 50 accredited labs, trimming calibration downtime to under one week. Local incumbents leverage this service network to lock in annuity contracts and defend share against price-focused imports.

The Asia-Pacific region will record the fastest growth at an 8.18% CAGR through 2031, as India and China invest billions in ambient networks, and as Taiwan, Japan, and South Korea ramp up 2-nm production lines. Government allocations—Rs. 19,614 crore in India and CNY 30 billion in China—fortify public tenders that often bundle calibration services to overcome technician scarcity. Meanwhile, over 80 EV battery plants across China, Korea, and Japan embed hundreds of remote counters per site, rapidly expanding the installed base. Vendors offering turnkey calibration-as-a-service gain traction because only 30 accredited aerosol labs serve the entire sub-continent, making on-site verification far more practical.

Europe claims roughly 23% share but faces headwinds. Intel has postponed its EUR 30 billion Magdeburg fab, and ASML shipped only 60 EUV tools in 2025, down from earlier projections, which has muted fresh equipment orders. Growth instead rests on Annex 1 replacement cycles and on battery-cell lines such as Volkswagen’s Salzgitter and Northvolt’s Ett, which still trail Asia in capacity. The region benefits from a dense calibration infrastructure at PTB and NPL, ensuring compliance speed; however, suppliers are increasingly pivoting toward software upgrades and sensor retrofits to offset lulls in new installations.

The Middle East & Africa, as well as South America, jointly contribute under 10% but hold latent upside. Brazil’s adoption of Annex 1-style monitoring in 2024 forces local drug makers to modernize, yet the absence of domestic calibration labs slows rollouts. Gulf states exploring local semiconductor fabs could unlock demand for instruments, but projects remain at the feasibility stage. In both regions, portable counters validated against transfer standards offer a stopgap until home-grown metrology capacity matures.

Competitive Landscape

The particle counters market is moderately concentrated. Danaher, TSI Incorporated, and Spectris collectively control roughly 50-55% of the global revenue, anchored by deep service staff rosters, proprietary optics, and FDA-validated software. Nonetheless, fragmentation is accelerating as challengers introduce AI modules that predict sensor drift and condensation designs that replace butanol with water, easing maintenance. Particle Measuring Systems’ 2024 acquisition of its long-time Irish distributor illustrates a broader trend toward direct sales, which strengthens post-sale engagement and secures data-service revenues.

Patents tell a defensive story. RION filed multiple Brownian-motion sizing and microbial counting patents between 2020 and 2025, while TSI expanded claims around water-based condensation growth. These moves protect incumbents’ ultrafine niches but stop short of disruptive platform shifts, leaving room for startups that mesh particle, gas, and acoustic sensing into unified edge devices. Calibration capacity remains a strategic chokepoint: fewer than 50 accredited labs serve emerging Asia, so vendors bundling onsite calibration gain negotiating leverage. Kanomax, Climet, and Suzhou Honri exploit this by offering counters 30-40% cheaper than premium brands, trading margin for quick share in price-sensitive markets.

White-space opportunities cluster around services. Mobile reference labs that co-calibrate low-cost sensor grids can trim field expenses by 40-50%, a compelling pitch for governments scaling ambient networks. Digital twins that model sensor aging permit just-in-time calibration, cutting downtime and consumables. Vendors able to wrap these analytics into annual contracts stand to elevate lifetime value per instrument even as hardware ASPs compress under competitive pressure.

Particle Counters Industry Leaders

TSI Inc.

Lighthouse Worldwide Solutions

RION Co., Ltd.

Spectris

Danaher

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Spectris recorded a 4 % increase in its order backlog despite a 2 % year-on-year revenue dip in Q1 2025, indicating continued appetite for advanced particle-counting solutions amid broader market headwinds.

- March 2025: TSI launched the Nano LPM System, delivering 10 nm liquid detection for UPW and securing preorder commitments from three Taiwan logic fabs valued at USD 15 million

- October 2024: Sonicu launched its new particle counter monitoring solution on April 27, 2024. The system is specifically designed for manufacturing cleanrooms. It aims to enhance yield rates and reduce scrap by providing precise environmental monitoring.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the particle counters market as the revenue generated from portable, benchtop, remote, and inline instruments that detect and count airborne or liquid particles for contamination monitoring across pharmaceutical, semiconductor, life-science, and critical-process environments. Coverage spans sales of new devices only, reported in USD, for 2019-2030, with mid-year 2025 as the current baseline.

Scope Exclusions: Used or rental equipment, aftermarket spares, and calibration services sit outside this valuation.

Segmentation Overview

- By Product Type

- Airborne Particle Counters

- Liquid Particle Counters

- Other Product Types

- By Application

- Cleanroom Monitoring

- Contamination Monitoring of Liquids

- Aerosol Monitoring and Research

- By Modality

- Benchtop

- Portable

- Remote

- By End User

- Pharmaceutical and Biotechnology Companies

- Clinical and Diagnostic Laboratories

- Academic and Research Institutes

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cleanroom certification experts, plant engineers at biotech firms, and regional distributors across North America, Europe, and Asia Pacific. These discussions tested adoption thresholds, typical average selling prices, and shipment trends that were difficult to observe in documents alone, letting us validate secondary findings and adjust assumptions where gaps emerged.

Desk Research

We first map the addressable demand using freely available benchmarks such as United States Pharmacopeia cleanroom classifications, European Medicines Agency GMP directives, US EPA Safe Drinking Water data, and semiconductor fab capacity statistics from SEMI. Trade flow records from UN Comtrade help us gauge liquid counter penetration in water utilities. In addition, World Bank industrial value added series and peer-reviewed journals on aerosol metrology round out macro indicators. Select proprietary feeds, including D&B Hoovers for company revenues and Dow Jones Factiva for deal tracking, refine market share splits. The sources cited are illustrative only, with many additional public and paid datasets consulted in the full build.

Market-Sizing & Forecasting

The core model applies a top-down rebuild that starts with installed ISO-classified cleanroom area, regulated potable-water treatment volume, and semiconductor wafer starts. Each demand pool is multiplied by verified device density ratios, then converted to value through regionally blended ASPs. Bottom-up tests, such as supplier roll-ups and sampled channel checks, act as guardrails that keep totals realistic. Key variables include GMP cleanroom expansions, fab capacity additions, regulatory inspection frequency, and price erosion linked to optical sensor cost curves. A multivariate regression framework projects these drivers forward and feeds an ARIMA overlay to smooth short-run volatility before 2030.

Data Validation & Update Cycle

Outputs pass three-layer checks that flag variance against historical import volumes and listed financials. Senior reviewers challenge anomalies, and we reconnect with select respondents when swings exceed preset bands. We refresh every twelve months, with interim flashes after material policy or supply-chain shocks, so clients receive the latest calibrated view.

Why Mordor's Particle Counters Baseline Earns Dependability

Published estimates often differ because publishers pick dissimilar device mixes, geographic splits, and forecast cadences. Clients therefore encounter values that rarely line up.

Key gap drivers in this space include whether handheld dust counters are bundled, if projected ASP declines are linear or stepwise, and the point in the fiscal year when foreign-currency conversions are locked. Mordor fixes its scope on contamination-grade airborne and liquid instruments only, reports blended transactional ASPs, and refreshes models annually, which collectively narrows error bands.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 257.81 million (2025) | Mordor Intelligence | - |

| USD 625.3 million (2024) | Global Consultancy A | Includes dust and industrial air samplers, applies list prices, last update 2024 |

| USD 619.87 million (2024) | Research House B | Combines aftermarket services, uses five-year-old currency rates, limited primary validation |

The comparison shows that wider scopes and older cost assumptions inflate peer figures, whereas our disciplined variable selection and yearly refresh keep Mordor's baseline balanced and traceable for confident decision making.

Key Questions Answered in the Report

What is the current valuation of the particle counters market?

The particle counters market size was USD 276.43 million in 2026 and is projected to reach USD 391.53 million by 2031.

Which segment is expanding the fastest?

Liquid particle counters are forecast to grow at 9.32% CAGR, outpacing all other product categories.

Why are remote particle counters gaining traction?

Annex 1 and ISO 14644 revisions mandate continuous monitoring, prompting facilities to adopt networked remote units that log data 24/7 and issue real-time alerts.

Which region offers the highest growth potential?

Asia-Pacific is projected to advance at an 8.18% CAGR, buoyed by semiconductor fabs, battery gigafactories, and expanding ambient air-quality networks.

How are vendors adding value beyond hardware sales?

Leaders now package calibration-as-a-service, AI-driven predictive maintenance, and cloud analytics to lock in recurring revenue and improve instrument uptime.

Page last updated on: