Cell Counting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

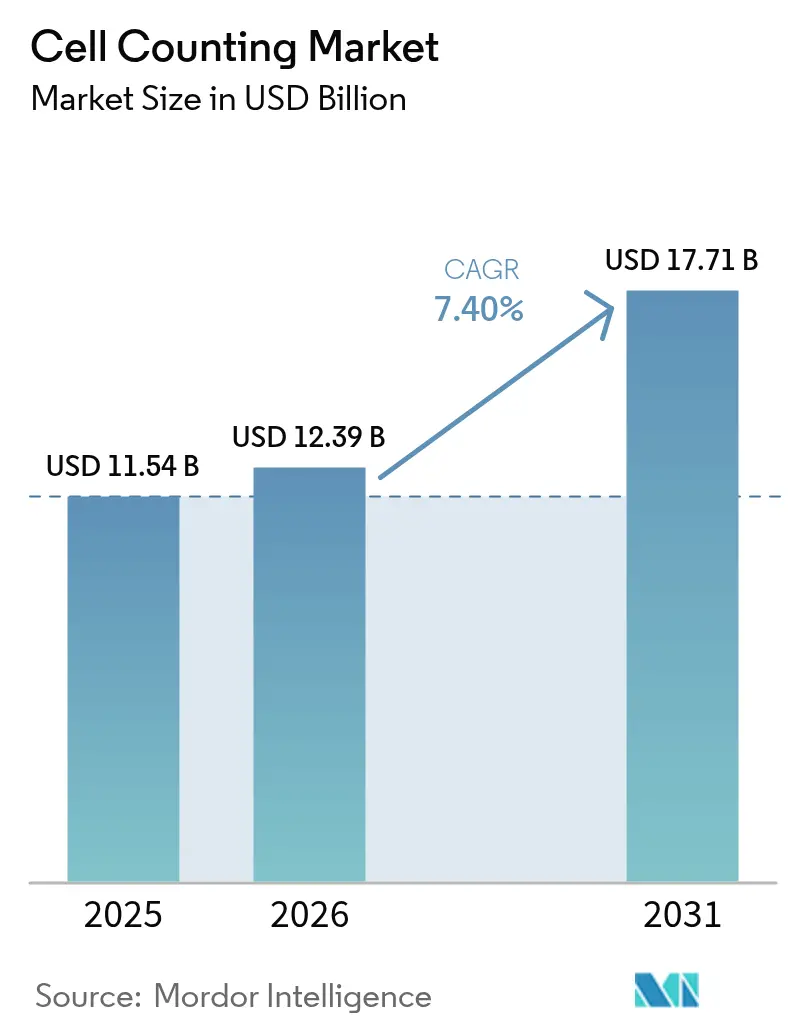

| Market Size (2026) | USD 12.39 Billion |

| Market Size (2031) | USD 17.71 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cell Counting Market Analysis by Mordor Intelligence

The cell counting market size was valued at USD 11.54 billion in 2025 and estimated to grow from USD 12.39 billion in 2026 to reach USD 17.71 billion by 2031, at a CAGR of 7.40% during the forecast period (2026-2031). Continued demand for precision diagnostics, tighter process control in cell-therapy manufacturing, and the routine use of real-time viable cell density monitoring in single-use bioprocessing sustain this robust expansion. Consumables remain the economic engine, as laboratories purchase reagents, assay kits, and media every day to keep culture workflows running. Image-based and microfluidic platforms equipped with machine learning are widening access to high-quality counts, reducing operator subjectivity, and cutting turnaround times. Capital investment decisions are guided by the need to integrate automation and AI so that one platform can handle routine hematology, multiparametric flow cytometry, and advanced regenerative-medicine assays within the same ecosystem. North America’s early adoption of spectral cytometry and Asia-Pacific’s race to build local cell therapy capacity jointly anchor near-term revenue visibility, while supply-chain resilience strategies are tempering risk.

Key Report Takeaways

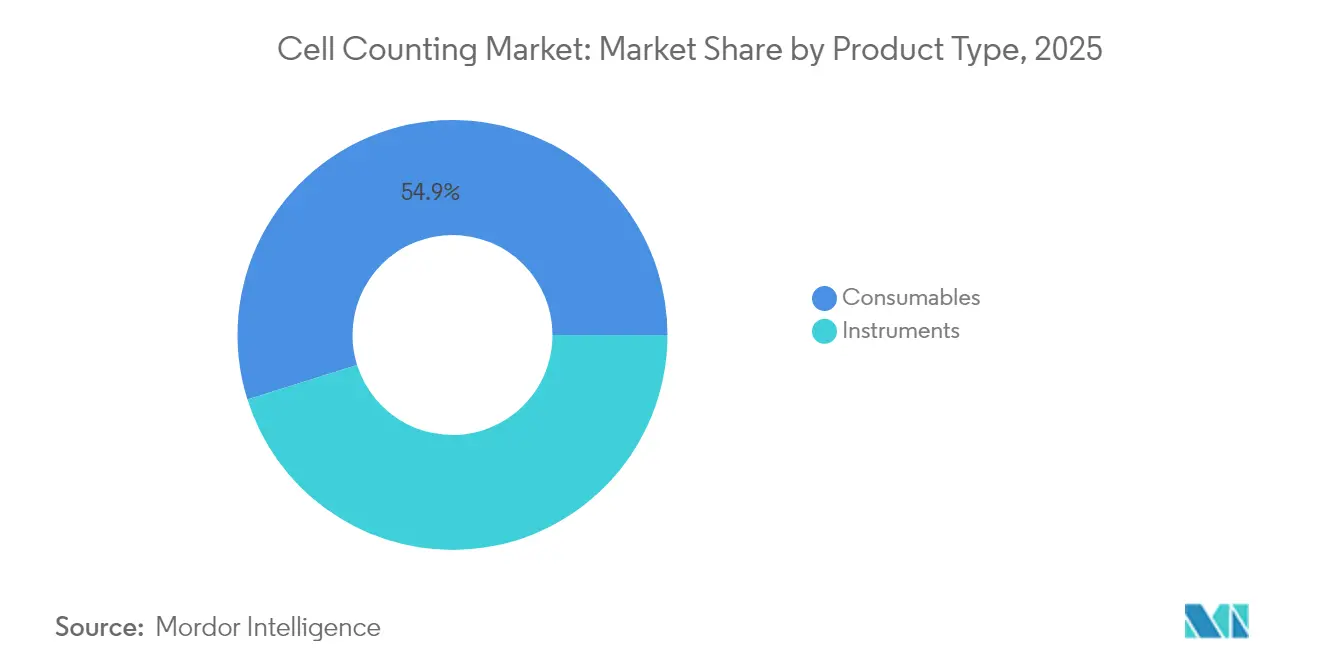

- By product type, consumables commanded 54.85% of 2025 revenue; instruments will expand at a 7.60% CAGR to 2031.

- By application, research led with 40.10% of 2025 revenue, while clinical diagnostics is advancing at a 7.55% CAGR.

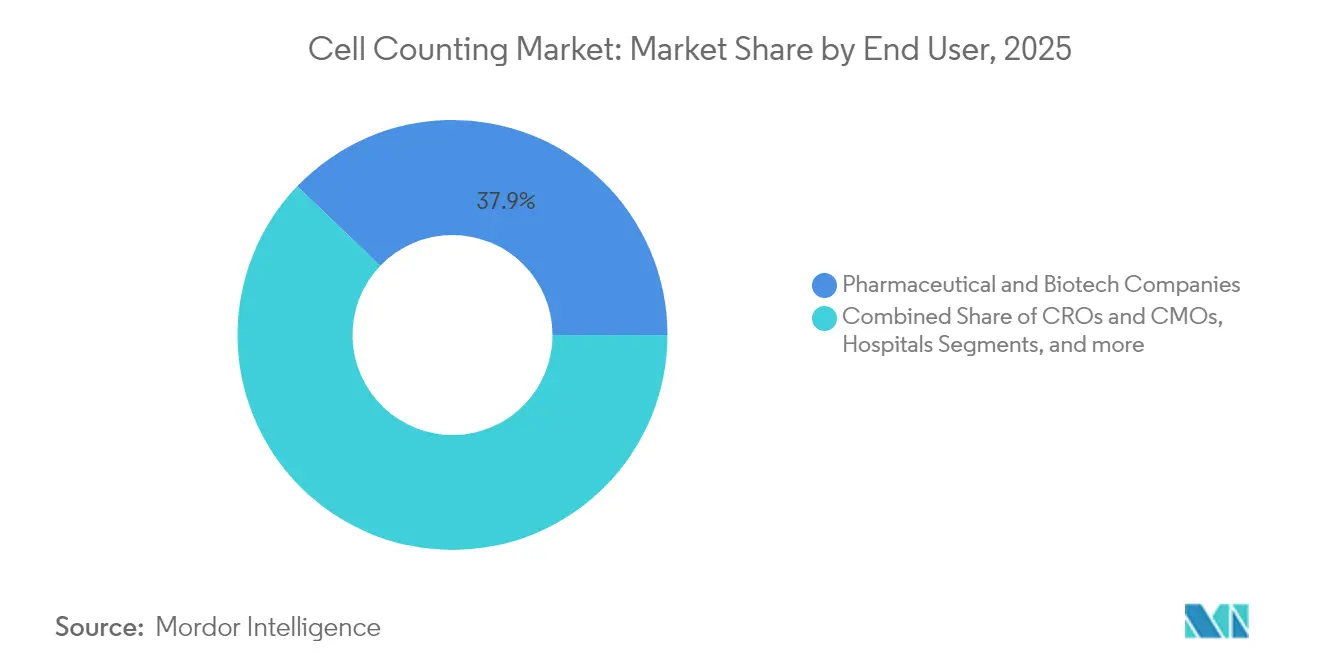

- By end-user, pharmaceutical and biotech companies controlled 37.85% of demand in 2025; hospitals and clinical labs are growing fastest at 7.88% CAGR.

- By technology, flow cytometry held 44.10% revenue share in 2025, whereas image-based cytometry is projected to grow at an 8.02% CAGR.

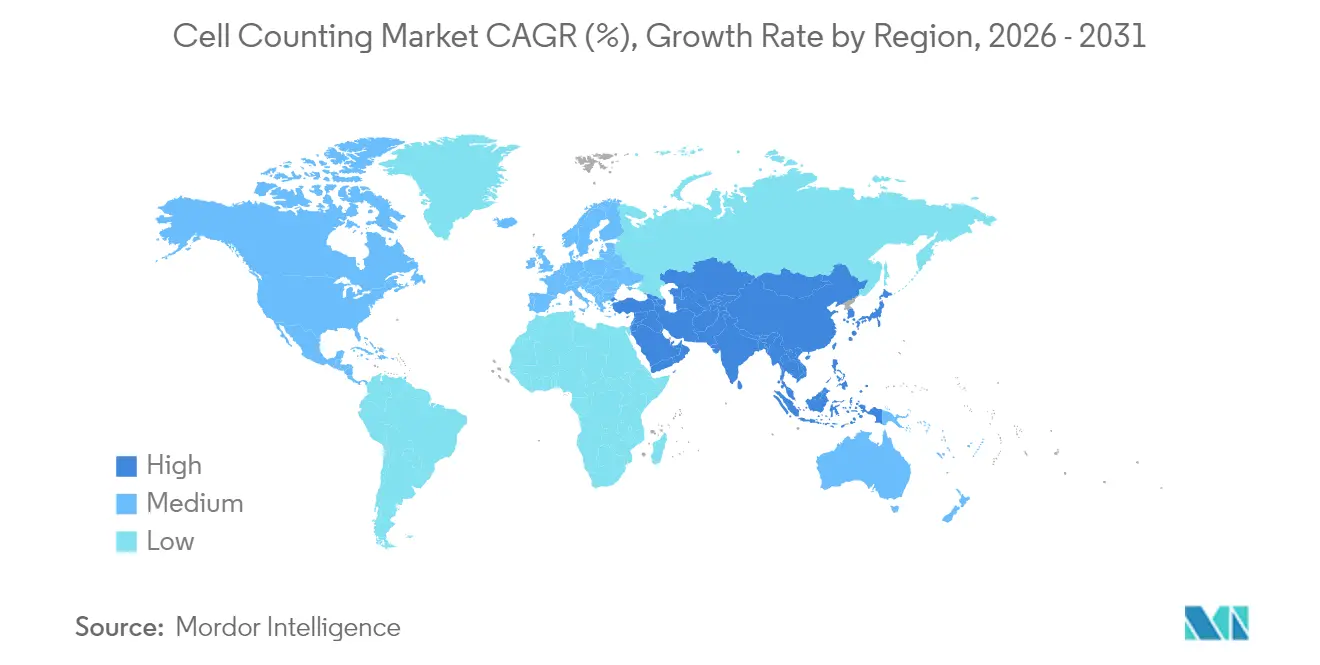

- By region, North America captured 39.20% of 2025 revenue; Asia-Pacific is forecast to show the strongest 7.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cell Counting Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing incidence of target diseases & blood disorders | +1.2% | North America, Europe | Medium term (2-4 years) |

| High-throughput flow cytometry & automated hematology analyzers | +1.8% | North America, Europe, APAC | Short term (≤ 2 years) |

| AI-powered image-based cell counters for regenerative medicine | +1.5% | US, Japan, Germany | Medium term (2-4 years) |

| Microfluidic lab-on-chip cell counting in point-of-care testing | +1.0% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Single-use bioprocessing boosting real-time monitoring | +0.8% | North America, Europe, China, India | Medium term (2-4 years) |

| Label-free impedance-based cytometry for rapid QC | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Use of High-throughput Flow Cytometry & Automated Hematology Analyzers

New spectral flow cytometers such as Beckman Coulter’s CytoFLEX mosaic offer 88 detection channels and nanoparticle sensitivity down to 80 nm, enabling deep immunophenotyping that exceeds the limits of traditional 10-color panels. Spectral unmixing algorithms remove complex compensation steps and shrink operator training requirements, while automated hematology systems from Sysmex and Siemens Healthineers integrate coagulation and immunology modules to streamline consolidated testing workflows. Combined, these platforms reduce sample hand-offs, lower error rates, and allow labs to scale routine counts and specialized assays on a single software spine.

Rising Adoption of AI-powered Image-based Cell Counters for Regenerative Medicine

Machine learning-enabled image analysis drives consistent enumeration even when operators vary in skill. The Singapore-MIT Alliance for Research and Technology showed that UV absorbance spectroscopy paired with AI detects microbial contamination in 30 minutes versus 14 days for sterility culture tests. NanoEntek’s fluorescence-based counters differentiate live and dead CAR T cells from tiny sample volumes, trimming reagent costs and supporting precise dosing. Deep learning libraries built on diverse donor samples adapt to different culture conditions, solving historical challenges caused by clumping and debris.

Integration of Microfluidic Lab-on-a-chip Cell Counting in Point-of-care Testing

Smartphone-linked chips count 10^5–10^7 cells/mL with accuracy comparable to benchtop flow cytometers while fitting in a clinician’s pocket. BD’s MiniDraw fingertip sampling kit pairs seamlessly with such platforms, widening access to near-patient complete blood counts. By coupling bright-field imaging with automated recognition algorithms, these devices produce live-dead discrimination without staining, bringing CD4+/CD8+ enumeration and fetal cell analysis to remote clinics.

Expansion of Single-use Bioprocessing Driving Demand for Real-time Viable Cell Density Monitoring

Sartorius Stedim’s ambr miniature bioreactors yielded 125 × 10^6 cells/mL and cut media consumption by 87%, yet such intensification requires in-situ monitoring so that sterile bags remain closed. Raman probes mounted through disposable ports now predict metabolite trends and viable density in perfusion systems, eliminating contamination risk. Corning’s cloud-connected confluence sensors let operators adjust feed profiles remotely, improving batch consistency.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced cell counting systems & maintenance | -1.8% | Global, higher in developing markets | Short term (≤ 2 years) |

| Shortage of skilled technicians in low-income regions | -1.2% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Standardization gaps in digital cell-imaging analytics hindering cross-lab reproducibility | -0.9% | Global | Medium term (2-4 years) |

| Data-integrity compliance burdens slowing cloud-connected device rollout | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Cell Counting Systems & Maintenance

Spectral flow cytometers can exceed USD 500,000, and annual service contracts often add 10–15% of purchase price. Core facility surveys confirm that upkeep competes with funding for new assays, pressing labs to stagger upgrades or share instruments. Smaller clinics in emerging economies face steeper barriers because manufacturer service hubs cluster around major urban centers.

Shortage of Skilled Technicians in Low-income Regions

Flow cytometry demands mastery of optics, compensation theory, and large-file data analytics, whereas advanced image-based instruments require familiarity with AI model validation. Many training programs lag behind commercial innovation, and skilled operators migrate to wealthier regions, leaving rural and peripheral labs under-utilizing expensive assets. Remote-learning modules and simplified end-user interfaces help, yet sustainable competence still hinges on long-term investment in local education programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Drive Recurring Revenue Growth

Consumables captured 54.85% of cell counting market share in 2025 and are tracking a 7.14% CAGR toward 2031. Reagents, assay kits, sera, and single-use sensors are reordered continuously, unlike instruments whose purchases are episodic. The shift to disposable bioreactors reinforces this dynamic because every new batch requires a fresh set of sterile bags, tubing, and media supplements. Within consumables, specialized growth media tailored for stem-cell expansion command premium pricing due to stringent purity requirements, while viability assay kits that combine fluorometric stains with apoptotic markers are displacing trypan-blue methods. Instruments, although a smaller revenue pool, set the installed-base foundation that fuels downstream consumables. Spectrophotometers remain ubiquitous in academia for quick density checks, yet multiparametric flow cytometers and image-based counters are becoming indispensable in therapy production suites where morphology, viability, and phenotype must be tracked in parallel.

The installed fleet of automated cell counters is splitting along two innovation tracks. Image-based models leverage high-resolution CMOS sensors and cloud analytics to return confluence, viability, and morphology readouts in under 30 seconds, while impedance-based devices offer label-free counts ideal for hematopoietic stem cell transplants where minimal manipulation is vital. Microfluidic chip counters further promise to reduce reagent volumes by orders of magnitude, making them attractive for high-cost cell therapy batches that cannot spare large sample volumes. As instrument vendors adopt pay-per-use cloud licenses, laboratories in budget-constrained settings gain entry without large capital outlays, yet long-term cost of ownership remains tied to consumables subscription models embedded in reagent cartridges.

By Application: Clinical Diagnostics Accelerate Automation Adoption

Research activities maintained 40.10% of 2025 revenue as oncology, immunology, and vaccine programs continue to absorb high-throughput platforms. Tumor organoid screening requires precise seeding densities and viability confirmation before drug dosing, while CRISPR screens depend on accurate counts to normalize editing efficiencies. Clinical diagnostics, though smaller in absolute terms, will outpace research by growing at 7.55% CAGR as hospitals automate hematology lines and deploy point-of-care analyzers capable of providing differential counts within five minutes of finger-stick collection. Digital smear analysis cuts pathologist review time, enhancing diagnostic throughput during seasonal surges of hematologic testing.

Industrial and bioprocess segments are advancing as real-time viable cell density becomes mandatory for both fed-batch and continuous perfusion modes. Raman and capacitance sensors feed closed-loop controllers that adjust glucose or lactate feeds to stabilize metabolic profiles, mitigating batch-to-batch variability. Environmental testing has emerged as a niche, with breweries and water-treatment plants adopting rapid microfluidic counters to detect microbial contamination faster than plate counts. Combined, these trends ensure diversified demand so that no single application dominates the cell counting market.

By End-User: Hospitals Embrace Automation for Efficiency Gains

Pharmaceutical and biotech companies consumed 37.85% of 2025 outlays, leveraging automated capacity for screening, process development, and release testing. Continuous manufacturing pilots in gene therapy rely on in-line counters synchronized with process analytical technology frameworks to maintain evidence trails for regulators. CROs and CMOs adopt flexible counters that can toggle between research-grade and GMP-compliant modes, catering to variable client requirements. Hospitals and clinical labs, growing at 7.88% CAGR, push suppliers to integrate robotics so one technician can supervise multiple instruments. BD and Biosero’s robotic link reduces human touchpoints, raising daily throughput without adding headcount bd.com. Academic centers remain vital early-adopter hubs; they test prototype features such as unsupervised gating algorithms before these trickle into mainstream clinical versions.

In low-resource settings, NGOs finance the deployment of portable analyzers for HIV monitoring and maternal health programs. These devices combine microfluidic chips, solar-charged batteries, and smartphone interfaces, reflecting an inclusive design philosophy that widens the cell counting market. Public-private partnerships explore lease-to-own models so district hospitals can shift capital expenditure into manageable operating payments, sustaining instrument fleets and driving recurring reagent demand.

By Technology: Image-Based Systems Gain AI-Powered Advantages

Flow cytometry retained 44.10% revenue share in 2025 thanks to regulatory familiarity and unmatched multiplex throughput. Spectral flow advances collapse fluorescence overlap issues, enabling 40+ color panels in routine labs and pushing experimental design toward systems-level immunoprofiling. Yet image-based cytometry is set to expand at 8.02% CAGR to 2031 because AI eliminates subjective gating and extracts morphological context absent from light-scatter data. Vendors embed convolutional neural networks validated on open datasets to meet reproducibility expectations of peer-review journals and regulators, accelerating trust in automated output cellandgene.com.

Spectrophotometry retains a foothold when cost and simplicity trump granularity; yeast-based fermentation labs appreciate the absence of staining and low calibration overhead. Impedance counters offer reagent-free operation ideal for stem-cell harvesting stations concerned about functional residue contamination. Microfluidic chips consolidate hydrodynamic focusing, staining, and imaging on a credit-card-sized substrate, opening doors for rugged field units used in disaster-relief clinics or animal health campaigns. Collectively, these technology options ensure end-users can match analytical depth to budget and workflow needs, preserving the diversified appeal of the cell counting market.

Geography Analysis

North America led the cell counting market with 39.20% revenue share in 2025 on the back of a mature biopharmaceutical manufacturing base, heavy federal research funding, and quick integration of next-generation cytometry in clinical pathways. The United States benefits from FDA device-clearance momentum for automated hematology and home-use differential counters, encouraging hospitals and at-home care providers to adopt advanced platforms. Canada’s public health labs deploy image-based systems for hematologic malignancy surveillance, while Mexico’s growing medical-device import incentives widen access to mid-range analyzers. Across the region, integrated service networks ensure downtime is minimal, strengthening customer loyalty to incumbent vendors.

Asia-Pacific is the fastest-growing territory, projected at 7.66% CAGR, underpinned by China’s push to localize cell therapy supply chains and Japan’s expedited regulatory routes for regenerative-medicine products. Government grants fund the build-out of GMP suites, each anchored by high-throughput counters that guarantee process consistency. South Korea, leveraging its biosimilar leadership, invests in continuous perfusion plants where real-time capacitance probes guard against culture crashes. India’s vaccine hubs adopt low-cost microfluidic instruments, pairing them with digital dashboards to satisfy stringent batch-release documentation. Australia’s translational institutes emphasize point-of-care deployment in remote communities, fostering demand for rugged field analyzers.

Competitive Landscape

The cell counting market remains moderately fragmented, with the top five suppliers well short of an 80% aggregate share. Danaher (Beckman Coulter), Thermo Fisher Scientific, and BD dominate multiparametric flow cytometry, leveraging global service networks and broad reagent catalogs. Sartorius Stedim and Corning focus on single-use bioprocess monitoring, while NanoEntek and Logos Biosystems carve niches in compact, image-based counters. Competitive differentiation centers on workflow integration; suppliers pair hardware with informatics platforms so users can archive raw FCS files, AI-generated morphometric features, and batch metadata in a single cloud environment.

Strategic collaboration intensity is rising. BD’s link with Biosero embeds robotic arms that load tubes, run washes, and start acquisitions without human intervention, shrinking shift-labor costs[1]BD, “Robotic Integration of Flow Cytometers,” bd.com. Siemens Healthineers and Scopio Labs deliver digital morphology modules that cut smear-review times by 60%, proving the value of high-resolution, full-field imaging[2]Siemens Healthineers, “Integrated Hemostasis Testing Expansion,” siemens-healthineers.com. Meanwhile, start-ups commercialize smartphone-based microfluidic chips that fit humanitarian budgets, nudging incumbents toward tiered pricing strategies.

Regulatory harmonization exerts further pressure. The FDA and NIST jointly drafted standards for cell therapy counting, covering linearity, precision, and reference materials[3]National Institute of Standards and Technology, “Standards for Cell Counting in Cell Therapy,” nist.gov. Vendors able to validate against these benchmarks win early adopter confidence. M&A activity is therefore likely as established firms acquire agile AI or microfluidic innovators to fast-track compliance. Overall, the cell counting market rewards those combining instrument breadth, reagent continuity, and software orchestration into cohesive, scalable solutions.

Cell Counting Industry Leaders

Thermo Fisher Scientific

Becton, Dickinson and Company

Bio-Rad Laboratories

Merck KGaA

Danaher Corporation (Beckman Coulter, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Beckman Coulter Life Sciences launched the CytoFLEX mosaic Spectral Detection Module, delivering up to 88 detection channels and nanoparticle detection down to 80 nm.

- February 2025: Beckman Coulter Life Sciences and Indiana University School of Medicine received a USD 2.5 million National Cancer Institute grant to enhance leukemia and lymphoma diagnostics in Western Kenya.

- July 2024: BD and Quest Diagnostics formed a partnership to co-develop flow cytometry-based companion diagnostics for oncology and immunology applications.

- May 2023: Siemens Healthineers signed a distribution agreement with Scopio Labs to offer full-field digital cell morphology platforms capable of 40-sample-per-hour throughput.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cell counting market as all instruments, spectrophotometers, flow cytometers, hematology analyzers, image-based and impedance counters, and their associated consumables, reagents, sera, assay kits, and microplates that are purchased to obtain quantitative counts of live, dead, or specific sub-sets of cells across clinical, research, and industrial settings. According to Mordor Intelligence, the market stood at USD 11.54 billion in 2025 and is forecast to reach USD 16.55 billion by 2030.

Scope exclusion: We do not track metabolic viability readers that rely solely on ATP or resazurin chemistry.

Segmentation Overview

- By Product Type

- Instruments

- Spectrophotometers

- Flow Cytometers

- Hematology Analyzers

- Automated Cell Counters

- Image-based Cell Counters

- Impedance Cell Counters

- Microfluidic Chip Counters

- Consumables

- Media, Sera & Reagents

- Assay Kits

- Others

- Instruments

- By Application

- Research

- Cancer Research

- Stem-Cell & Regenerative Medicine

- Immunology & Infectious-Disease

- Drug Discovery & Toxicology

- Clinical & Diagnostic

- Hematology Diagnostics

- Point-of-Care Testing

- Industrial & Bioprocess

- Biopharmaceutical Manufacturing

- Food & Beverage Quality-Control

- Environmental Monitoring

- Research

- By End User

- Hospitals & Clinical Labs

- Research & Academic Institutes

- Pharmaceutical & Biotech Companies

- CROs & CMOs

- Other Industrial Labs

- By Technology

- Flow Cytometry

- Image-Based Cytometry

- Spectrophotometry

- Impedance (Coulter Principle)

- Microfluidics & Lab-on-Chip

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed laboratory managers in North America, Europe, and Asia-Pacific, product managers from leading instrument OEMs, and distributors serving midsize clinical labs. These conversations clarified typical replacement cycles, reagent pull-through ratios, and country-level reimbursement shifts that desk sources only hinted at, letting us refine assumptions and stress-test early model outputs.

Desk Research

We began with structured searches through open-access portals such as the US Food & Drug Administration 510(k) database, PubMed, and Eurostat trade files to size the installed base and shipment flows of primary instruments. Scientific society dashboards, for example, the International Society for Advancement of Cytometry and the American Association for Clinical Chemistry, offered usage benchmarks and conference abstracts that signal emerging demand pockets. Company 10-Ks, investor decks, and hospital procurement tenders were screened in D&B Hoovers, while Dow Jones Factiva supplied deal flow and pricing moves. Customs manifests accessed via Volza complemented our view on cross-border flows of consumables. This list is illustrative; many additional public and subscription sources informed data checks.

Market-Sizing & Forecasting

A top-down reconstruction was run first. Production and trade statistics were aligned with average selling prices to yield a value pool by region, which was then corroborated with selective bottom-up roll-ups of flagship supplier revenues and sampled ASP × volume checks. Key variables like installed analyzer base, average tests per day, reagent consumption per test, oncology and hematology test volumes, and capital budget growth in biopharma drive the model. Multivariate regression with GDP per capita, oncology incidence, and R&D spend predicts growth, while scenario analysis cushions policy or pricing shocks. Where bottom-up estimates fell short, we imputed volumes using validated utilization ratios from peer labs of similar size.

Data Validation & Update Cycle

Outputs pass three analyst reviews that flag anomalies against historical trends and external yardsticks. We reconvene respondents if variances exceed agreed thresholds. The study refreshes annually; interim updates trigger after material events such as major regulatory approvals or recalls. A final pre-publication sweep ensures clients receive the latest reconciled numbers.

Why Mordor's Cell Counting Baseline Commands Reliability

Published figures often diverge because firms slice the market differently, apply distinct ASP progressions, or freeze their models for longer intervals. We recognize these levers upfront and align scope, data year, and refresh cadence before sizing.

Key gap drivers include inclusion of only consumables by some publishers, early base years that miss recent price inflation, or exclusion of emerging markets where low-cost automated counters are penetrating fast. Our disciplined segmentation and annual refresh narrow these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.54 B (2025) | Mordor Intelligence | - |

| USD 11.12 B (2024) | Global Consultancy A | base year one year earlier; excludes veterinary and food-testing labs |

| USD 10.24 B (2024) | Trade Journal B | bundles reagents for cell culture, inflating consumables share |

| USD 7.70 B (2022) | Research Publisher C | conservative ASPs and limited geographic coverage beyond G7 |

Taken together, the comparison shows how scope breadth, pricing inputs, and update rhythm shift totals. By tracing every variable back to verifiable series and refreshing yearly, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the cell counting market?

The cell counting market size reached USD 12.39 billion in 2026 and is projected to hit USD 17.71 billion by 2031.

Which product segment generates the most revenue?

Consumables lead the market with 54.85% revenue share in 2025, thanks to the constant need for reagents, media, and assay kits.

Which geographic region is growing the fastest?

Asia-Pacific is the fastest-growing region, forecast to expand at a 7.66% CAGR through 2031, driven by large-scale investments in cell and gene therapy manufacturing.

Why are image-based cytometers gaining popularity?

Image-based cytometers combine AI-driven analysis and label-free imaging to reduce operator subjectivity, cut reagent costs, and support real-time monitoring in regenerative-medicine workflows.

What is the main restraint hindering wider adoption of advanced cell counters?

High capital and maintenance costs—spectral flow cytometers can exceed USD 500,000—limit uptake, especially in budget-constrained laboratories and developing markets.

Which end-user group is growing the fastest?

Hospitals and clinical laboratories are the fastest-growing end-user segment, advancing at an 7.88% CAGR as automation initiatives shorten turnaround times and cut labor costs.

Page last updated on: