Paraguay Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

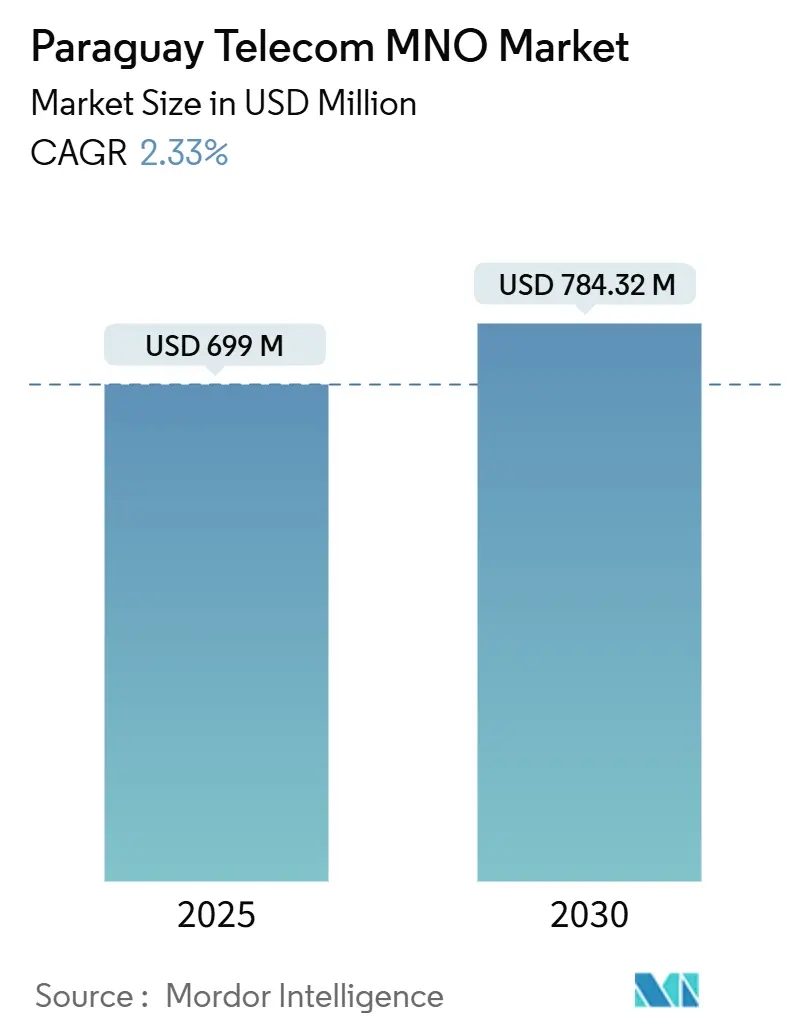

| Market Size (2025) | USD 699 Million |

| Market Size (2030) | USD 784.32 Million |

| Growth Rate (2025 - 2030) | 2.33% CAGR |

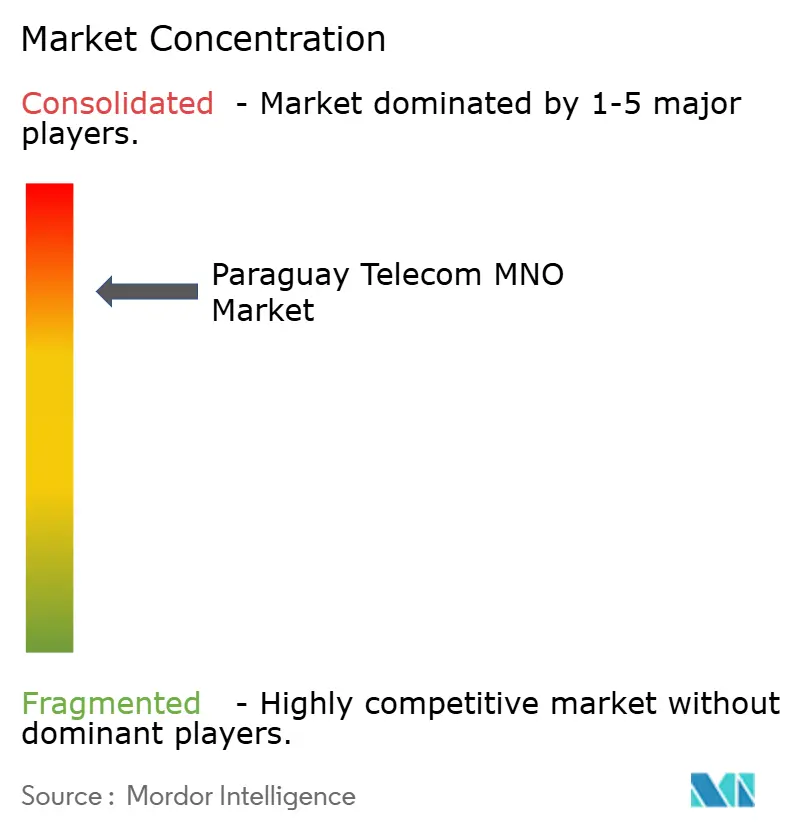

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paraguay Telecom MNO Market Analysis by Mordor Intelligence

The Paraguay Telecom MNO Market size is estimated at USD 699 million in 2025, and is expected to reach USD 784.32 million by 2030, at a CAGR of 2.33% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 8.90 million Subscribers in 2025 to 9.83 million Subscribers by 2030, at a CAGR of 2.02% during the forecast period (2025-2030).

This measured growth reflects the country’s land-locked cost structure, cautious spectrum policy, and operator discipline focused on infrastructure sharing rather than price wars. Data-centric revenue, digital-government projects, and wholesale transit links with Brazil and Argentina sustain momentum, while moderate competitive intensity protects EBITDA margins and preserves cash for targeted 5G and fiber investments. Regulatory clarity under CONATEL and the central bank’s instant-payments ecosystem further encourages demand for high-availability mobile broadband.

Key Report Takeaways

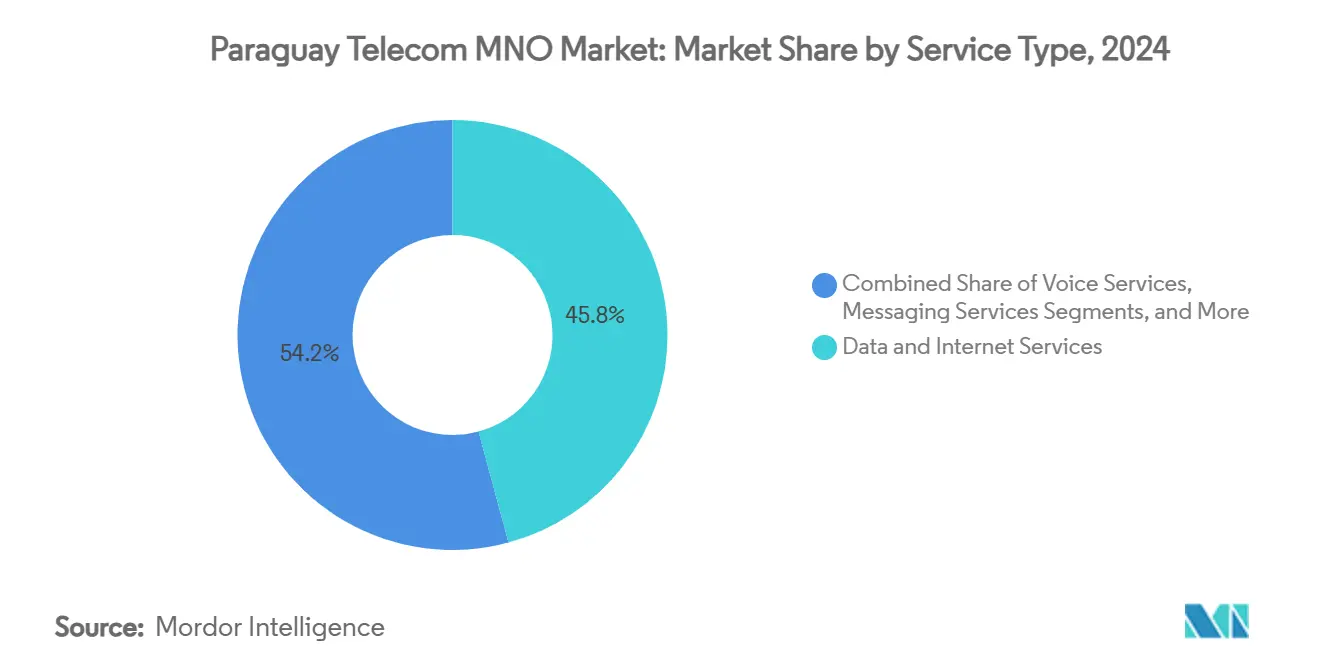

- By service type, data and Internet services led with 45.80% of Paraguay telecom MNO market share in 2024 and are projected to grow at a 2.88% CAGR through 2030.

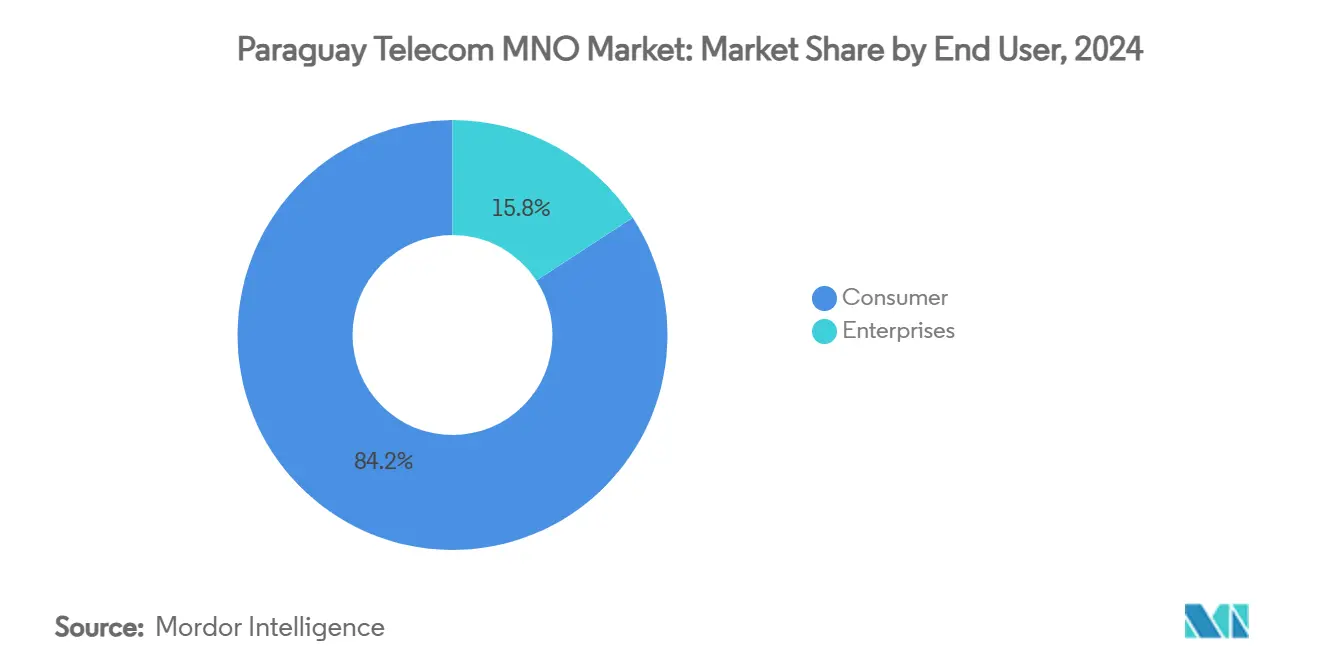

- By end user, the consumer segment accounted for 84.19% of Paraguay telecom MNO market size in 2024, while enterprise revenue is set to advance at a 2.96% CAGR between 2025-2030.

Paraguay Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging mobile-data consumption | +0.8% | Urban nodes in Asunción and Ciudad del Este | Medium term (2-4 years) |

| Accelerated fiber roll-outs via PPPs | +0.6% | Rural corridors and secondary towns | Long term (≥ 4 years) |

| 4G-to-5G spectrum re-farming | +0.4% | High-traffic urban centers | Medium term (2-4 years) |

| Digital-government transformation programs | +0.3% | Nationwide, pilot cities first | Short term (≤ 2 years) |

| Cloud/edge demand from agritech and fintech SMEs | +0.2% | Soybean belt and financial hubs | Medium term (2-4 years) |

| Cross-border wholesale transit links | +0.1% | Borders with Brazil, Argentina, Bolivia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Mobile-Data Consumption

Daily transactions through the central bank’s SPI instant-payments rail quadrupled to 560,000 by August 2024, embedding smartphones at the center of everyday commerce and fueling data-heavy app use. [1]Central Banking staff, “Payment and Market Infrastructure Development: Central Bank of Paraguay,” CentralBanking.com Operators convert this demand into higher ARPU through tiered bundles and zero-rated financial apps, while rural uptake rises as mobile money substitutes for sparse branch networks. Tigo’s nationwide Tigo Money wallet exemplifies how the Paraguay telecom MNO market unlocks incremental revenue from financial inclusion without deep handset subsidies.

Accelerated Fiber Roll-outs via PPPs

Public-private partnerships allow operators to co-fund long-haul fiber, spreading the capex burden that Paraguay’s geography imposes. The World Bank frames telecom PPPs as catalytic infrastructure, and local projects mirror this logic by tying universal-service funds to private trenching in low-density corridors. [2]World Bank, “Public-Private-Partnership Legal Resource Center,” PPP.WorldBank.orgShared middle-mile lines reduce backhaul bottlenecks, enabling 4G densification and supporting eventual 5G microwave offload in secondary towns.

4G-to-5G Spectrum Re-farming

CONATEL’s 2025 consultation to release 400 MHz in the 3.5 GHz band signals a deliberate path: operators squeeze more LTE capacity while selectively lighting 5G in premium zones. The tactic eases cash-flow strain and lets demand for enhanced mobile broadband mature before large outlays. Claro’s regional fiber and radio investments position it to pivot quickly once rules are finalized. [3]BNamericas, “By 2028, 60% of Claro's Mobile Coverage Will Be 5G,” BNamericas.com

Digital-Government Transformation Programs

Paraguay’s National Development Plan 2030 embeds e-procurement, e-health, and digital-ID modules that require carrier-grade networks. Government contracts give operators predictable traffic and showcase reliability to enterprise prospects, while recent data-protection legislation codifies security standards that telecoms can monetize as managed services. [4]PPC Land, “Paraguay Passes Comprehensive Data Protection Law,” PPC.land

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-locked backhaul cost premium | −0.4% | National | Long term (≥ 4 years) |

| Low banked-population limits post-paid upsell | −0.3% | Rural and lower-income urban sectors | Medium term (2-4 years) |

| Delayed number-portability implementation | −0.2% | Nationwide | Short term (≤ 2 years) |

| Illicit grey-route voice traffic | −0.1% | Border gateways | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land-locked Backhaul Cost Premium

Reliance on Brazilian and Argentine landing stations inflates IP transit prices, compressing margins on international bandwidth and inhibiting aggressive data pricing. Although new fiber PPPs alleviate domestic middle-mile constraints, cross-border fees remain structural. Operators pursue transit deals that reposition Paraguay as a regional traffic bridge, but pay-back periods extend beyond the forecast window, tempering near-term profitability.

Low Banked-Population Limits Post-paid Upsell

Only a minority of adults hold formal bank accounts, restricting credit-based billing. Pre-paid dominates, capping ARPU and complicating bundling of handset financing or OTT subscriptions. Mobile wallets provide a workaround, yet regulatory ceilings on transaction volumes keep them shy of full post-paid substitutes. Telecom-microfinance alliances are emerging but require risk-scoring innovations to scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Mix Evolution

Data and Internet captured 45.80% Paraguay telecom MNO market share in 2024, rising to half of revenue on a 2.88% CAGR through 2030. Strong smartphone adoption, propelled by zero-rating of instant payments, increases average monthly data traffic and raises operator appetite for spectrum re-farming. Voice revenue erodes as OTT calling proliferates, even as CONATEL enforces net-neutrality to curb selective blocking. Messaging experiences similar cannibalization from social platforms, whereas IoT and M2M subscriptions start to scale in livestock monitoring and logistics. Content deals, such as Tigo’s exclusive national league rights until 2027, sustain pay-TV viability and fortify churn defense. Other value-added services, roaming packs, device insurance, and cloud backup offer incremental margins that smooth the transition from simple connectivity to lifestyle ecosystems.

The segment’s expansion underscores the Paraguay telecom MNO market size shift toward digital applications. Operators leverage carrier billing for app stores, and partnerships with streaming providers bundle data allowances with localized content. Cloud gaming pilots, contingent on low-latency 5G slices, are staged for launch in densely populated districts. Wholesale transit of over-the-top traffic across Paraguayan fiber corridors signals another monetization path once cross-border fees normalize.

By End User: Enterprise Growth Accelerates Digital Transformation

The consumer segment generated 84.19% of Paraguay telecom MNO market size in 2024, reflecting a prepaid orientation and rising data bundles. Yet enterprise revenue, expanding at a 2.96% CAGR, becomes the fastest-growing slice as SMEs digitize supply chains. Agritech solutions demand resilient IoT links for soil analytics, while fintech platforms require redundant connectivity to support the SPI instant-payments backbone. Government e-procurement portals and municipal smart-city pilots anchor bandwidth commitments that stretch beyond best-effort mobile. Operators craft managed security and hybrid-cloud offers, carving new revenue lines without heavy spectrum dependence.

Enterprise penetration also diversifies churn risk in the Paraguay telecom MNO market. Long-term contracts stabilize cash flows, enabling capex planning for edge nodes that cache content closer to rural cooperatives. Competitive differentiation shifts from coverage maps to service-level agreements, prompting carriers to certify Tier III data-center resilience and recruit specialized solutions architects. These capabilities set the stage for future monetization of network APIs under 5G standalone architecture.

Geography Analysis

Urban clusters capture the bulk of traffic and investment, with Asunción and Ciudad del Este housing the highest-density cell sites and first 3.5 GHz trials. The Paraguay telecom MNO market size in these corridors is projected to climb on a mid-single-digit CAGR as 5G adoption begins. Suburban rings witness spillover capacity upgrades, whereas secondary cities such as Encarnación await cost-efficient backhaul before meaningful 5G deployment. Rural coverage remains 4G-oriented, but PPP fiber projects encourage small-cell overlays to serve agro-export zones.

Paraguay’s borders simultaneously inflate and mitigate cost pressures. Higher transit tariffs suppress retail pricing flexibility, yet wholesale opportunities emerge as Bolivia and landlocked Brazilian states seek diverse routes. Regulatory cooperation agreements between CONACOM and Brazil’s antitrust agency smooth the groundwork for shared ducts and reciprocal interconnect discounts. Operators could turn geographic disadvantage into regional hub status once bilateral peering norms mature.

The national instant-payments boom illustrates how digital ecosystems shift geographic bandwidth patterns. Transaction peaks coincide with crop-harvest payouts, spiking demand in soy-belt provinces. Telecoms respond by provisioning temporary bandwidth boosts and leveraging mobile edge computing to cache fintech workloads closer to farming cooperatives. Over the forecast horizon, rural data corridors transform from cost centers into incremental profit pools as agritech adoption deepens.

Competitive Landscape

Telecel (Tigo) is the reference operator, commanding a significant share in Paraguay's telecom MNO market in 2024 on the strength of nationwide LTE, exclusive football content, and entrenched Tigo Money wallets. Personal Paraguay leverages its global Telefónica lineage to compete on network quality, while Claro lifts group-wide capex USD 7.7 billion earmarked for 2024-2029 regional fiber to accelerate 5G nodes and AI-enabled capacity planning.

Infrastructure sharing is the dominant efficiency lever. Millicom transferred more than 9,000 towers into carve-out entities, unlocking capital and lowering tenancy costs for all tenants. Future sharing agreements are expected around dark fiber and RAN-sharing in low-ARPU districts, supported by CONATEL’s draft open-access guidelines. MVNO entry remains muted because wholesale fees align with cost-plus formulas that limit margin room; none hold more than 0.5% subscriber share.

Strategic focus shifts to enterprise ICT stacks. Tigo bundles SD-WAN and cloud gateways, Claro tests satellite-to-cell services for remote agribusiness, and Personal courts fintechs with carrier billing APIs. Competitive intensity is therefore less about headline tariffs and more about service-portfolio breadth and vertical expertise. Operators that translate regional group synergies into localized solutions retain an edge.

Paraguay Telecom MNO Industry Leaders

Tigo (Telecel Paraguay S.A.)

Telecom Personal Paraguay (Núcleo S.A.)

Claro Paraguay (AMX Paraguay S.A.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Paraguay enacted a comprehensive data-protection law, setting compliance requirements for telecom customer information.

- March 2025: Claro tested direct satellite-to-cell connectivity in pilots with Anatel, exploring rural coverage alternatives.

- February 2025: CONATEL opened consultation on 400 MHz in the 3.5 GHz band for 5G allocations, marking a milestone toward next-gen spectrum release.

Paraguay Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumers |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumers |

Key Questions Answered in the Report

What is the current size of the Paraguay telecom MNO market?

The Paraguay telecom MNO market size stood at USD 699 million in 2025 and is projected to reach USD 784.32 million by 2030.

Which operator leads the market?

Telecel (Tigo) leads with 55% Paraguay telecom MNO market share, bolstered by 37% EBITDA margins and exclusive sports content.

How fast is the enterprise segment growing?

Enterprise revenue is forecast to expand at a 2.96% CAGR through 2030, driven by agritech and fintech digitalization.

When will 5G become mainstream in Paraguay?

Operators target selective 5G launches in major cities from 2025, with Claro aiming for 60% population coverage by 2028.

What are the main restraints on market growth?

Paraguay’s land-locked backhaul premium and low banking penetration, which limits post-paid adoption, shave a combined 0.7 percentage points off forecast CAGR.

How are operators addressing rural coverage gaps?

Carriers pursue PPP fiber projects and pilot satellite-to-cell technology to broaden coverage without incurring prohibitive terrestrial build costs.

Page last updated on: