Ecuador Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

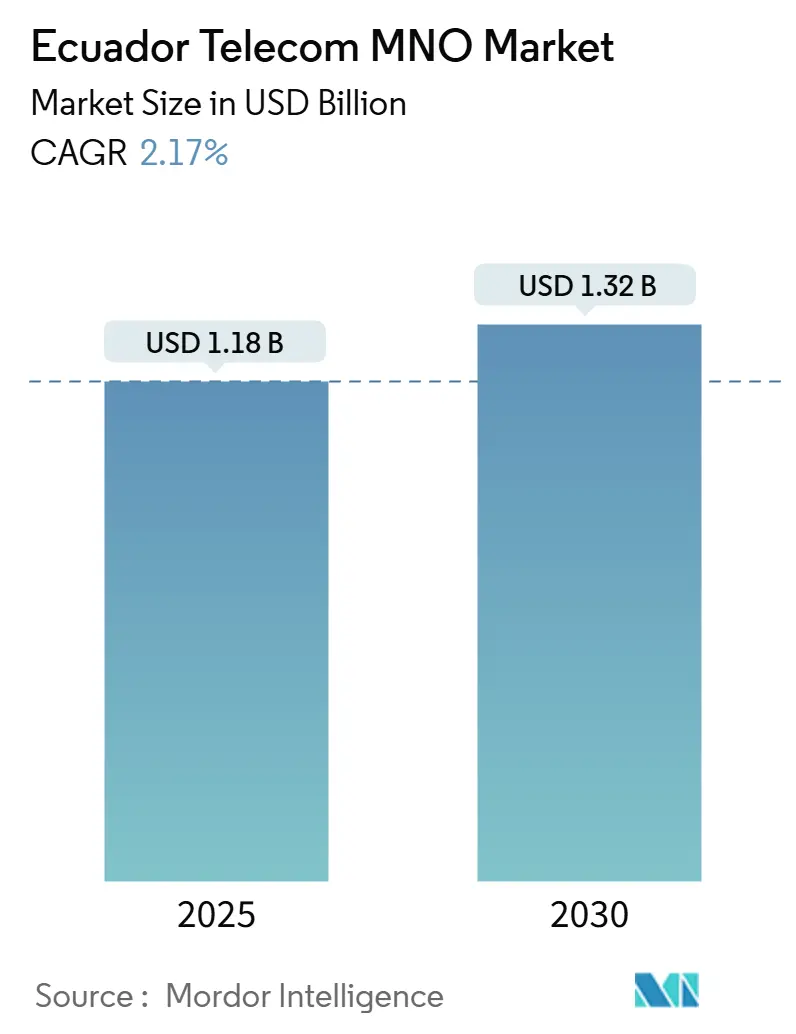

| Market Size (2025) | USD 1.18 Billion |

| Market Size (2030) | USD 1.32 Billion |

| Growth Rate (2025 - 2030) | 2.17% CAGR |

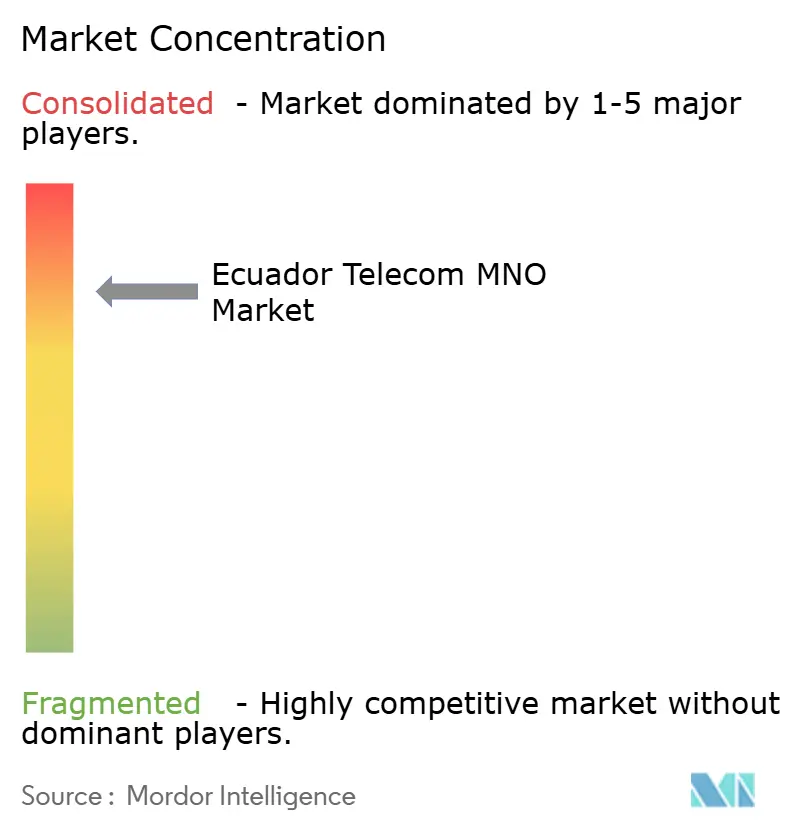

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ecuador Telecom MNO Market Analysis by Mordor Intelligence

The Ecuador Telecom MNO Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.32 billion by 2030, at a CAGR of 2.17% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 18.80 subscribers in 2025 to 21.5 subscribers by 2030, at a CAGR of 2.78% during the forecast period (2025-2030).

This moderate expansion underscores the sector’s ability to protect margins by modernizing networks rather than pursuing aggressive geographic build-outs. Demand continues to migrate from voice to data, propelled by faster smartphone uptake, price-stable post-paid plans enabled by dollarization, and coverage obligations that push 4G to 92% of the population by 2025. Operators are also honing spectrum and tower-sharing efficiencies to counter rising energy costs, while private-LTE pilots in the Amazon Basin reveal a nascent but promising industrial-IoT revenue stream. Although an energy crunch and macro headwinds weigh on consumer wallets, service resilience has kept churn low and ARPU steady in urban strongholds.

Key Report Takeaways

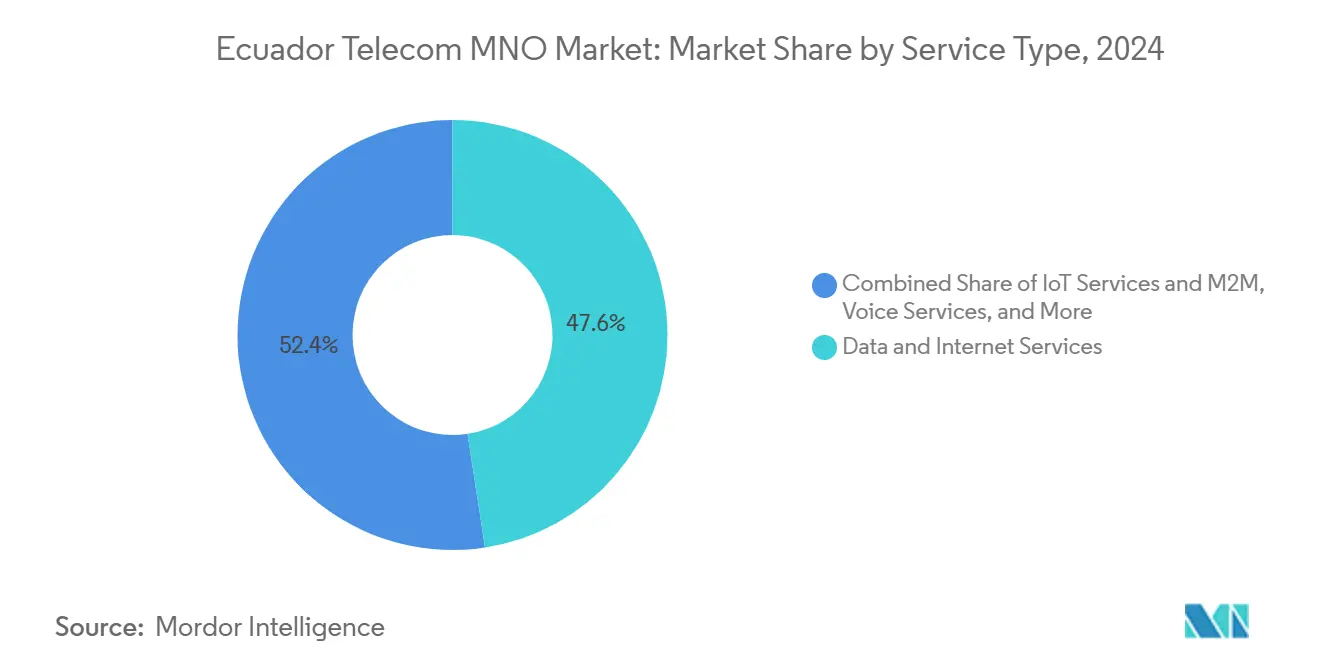

- By service type, data and internet captured 47.59% of the Ecuador telecom MNO market share in 2024; IoT and M2M revenues are forecast to accelerate at a 2.20% CAGR through 2030.

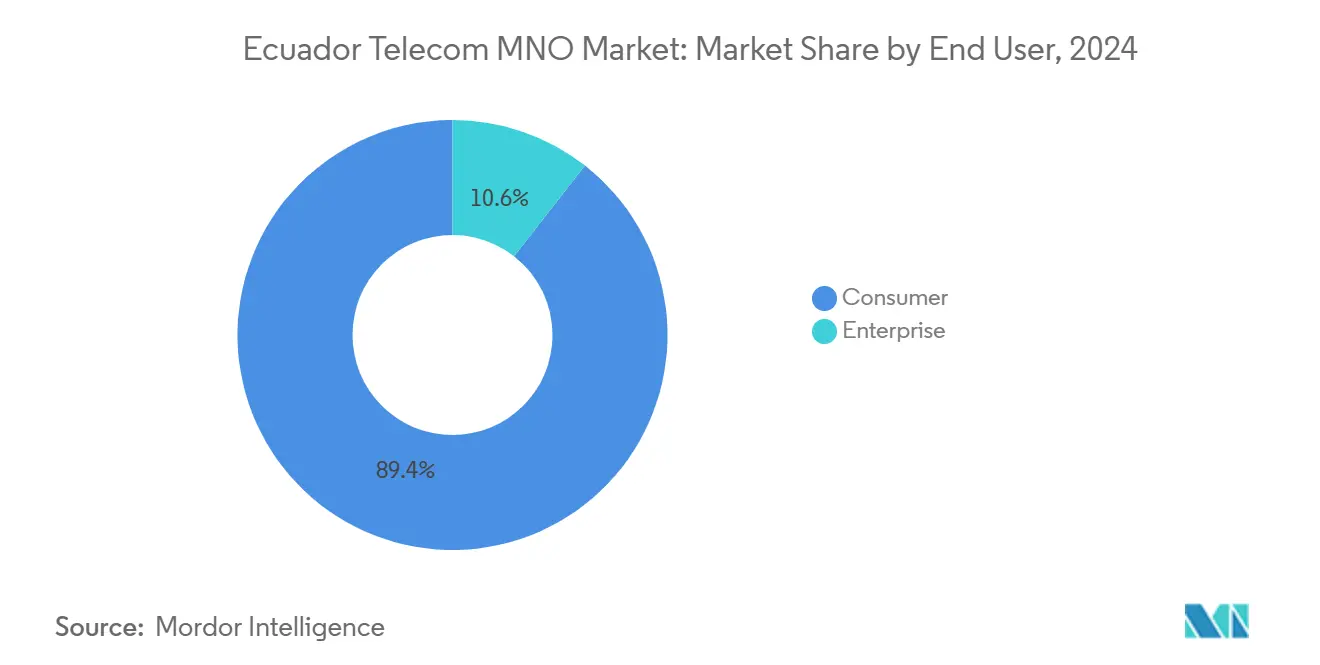

- By end user, consumer subscriptions held 89.44% of the Ecuador telecom MNO market size in 2024, while enterprise lines are set to post a 3.10% CAGR between 2025 and 2030.

Ecuador Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government 4G-coverage obligation and rural connectivity fund | +0.8% | National; rural provinces | Medium term (2-4 years) |

| Accelerated smartphone adoption and data-centric usage | +0.5% | Urban hubs; rural spill-over | Short term (≤ 2 years) |

| National FTTH roll-outs by CNT, Netlife and Claro Hogar | +0.4% | Quito, Guayaquil, Cuenca | Medium term (2-4 years) |

| Cloud and edge demand from new hyperscaler entrants | +0.3% | Business districts | Long term (≥ 4 years) |

| Private-LTE / 5G for mining and oilfield IoT in Amazon Basin | +0.2% | Amazon Basin sites | Long term (≥ 4 years) |

| Tower-sharing regulation cutting CAPEX by up to 35% | +0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government 4G-Coverage Obligation and Rural Connectivity Fund

Mandated expansion from 60.74% to 92% population coverage by 2025 compels every mobile operator to extend networks into 392 uncovered parishes. Spectrum access is now tied to meeting rollout milestones, and a dedicated rural fund partly offsets capital risk. Operators view these targets less as compliance costs and more as low-competition subscriber pools that can lift market penetration toward 100% over time. [1]Revista Latinoamericana de Economía y Sociedad Digital, “Digital Gap in Ecuador’s Rural Provinces,” rlesd.org

Accelerated Smartphone Adoption and Data-Centric Usage

Median mobile download speeds of 18.73 Mbps already support video streaming and e-commerce apps. Coupled with “roam-like-at-home” tariff elimination inside the Andean bloc, data volumes jumped 19% year-on-year, translating into steadier ARPU even as voice minutes slide.

National FTTH Roll-outs by CNT, Netlife and Claro Hogar

Claro’s Light ODN deployment and CNT’s FTTx upgrades supply backhaul capacity to dense cell sites and open fixed-mobile bundling opportunities. Average fixed speeds now top 98.68 Mbps, letting operators cross-sell cloud gaming and home-office packages amid work-from-anywhere trends. [2]Developing Telecoms, “Claro Ecuador Deploys ZTE Light ODN,” developingtelecoms.com

Cloud and Edge Demand from New Hyperscaler Entrants

Google’s 30-project alliance with CNT and Telconet’s all-flash storage refresh prime the country for low-latency applications. Banks and retailers are testing edge nodes in Guayaquil to keep transaction data onshore, aligning with data-sovereignty rules while reducing response times under 15 milliseconds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High spectrum reserve prices and absent 5G road-map | -0.7% | National | Long term (≥ 4 years) |

| Persistent rural-urban affordability divide | -0.4% | Rural and low-income zones | Medium term (2-4 years) |

| Macroeconomic volatility pressuring consumer ARPU | -0.3% | Nationwide | Short term (≤ 2 years) |

| Surge in copper-cable theft and vandalism | -0.2% | Infrastructure corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Spectrum Reserve Prices and Absent 5G Road-map

ARCOTEL’s reserve levels remain steep relative to peers, delaying fresh auctions and stalling nationwide 5G deployment beyond CNT’s pilots in Guayaquil and Manta. The cost hurdle diverts funds from rural LTE expansion and slows device ecosystem development. [3]Budde Comm, “Ecuador Telecoms and Spectrum Pricing Snapshot,” budde.com.au

Persistent Rural-Urban Affordability Divide

Only 46% of rural households own a mobile phone, versus 65.2% in cities, largely due to income disparities and higher service-cost ratios. Even discounted ETAPA EP fibre plans start at USD 8.00 monthly—still material for subsistence farmers—so operators continue to test community micro-franchises and data sachets to reach these segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data and Internet Services Drive Revenue Transformation

Data and internet traffic accounted for 47.59% of the Ecuador telecom MNO market size in 2024 on the back of increasing video consumption and social commerce activity. That share is projected to edge higher as operators bundle zero-rated education platforms to comply with school connectivity mandates, solidifying data as the single largest revenue pillar. Voice still captures meaningful volumes in peri-urban zones, but minutes dropped 12% in 2024, confirming a secular shift to over-the-top calling applications. Messaging revenues are pivoting to enterprise authentication and A2P services where SMS remains indispensable for banking and e-government notifications.

IoT and M2M subscriptions, although small at present, show the fastest lane with a 2.20% CAGR through 2030, underpinned by private LTE links inside gold and copper mines in Zamora-Chinchipe and Orellana. Operators position managed-IoT as an annuity that blends connectivity with analytics dashboards and device financing. Pay-TV over mobile reached 9.3% of smartphone users after Claro integrated its OTT video catalog into post-paid tiers, signaling upside in bundled entertainment. Wholesale transit, roaming inside the Andean Community, and SMS firewall services round out non-traditional revenue that mutes top-line volatility during economic shocks.

By End User: Enterprise Growth Accelerates Digital Transformation

Consumer contracts still represented 89.44% of the Ecuador telecom MNO market share in 2024, but enterprise spending is expanding more quickly as businesses digitize procurement, logistics, and customer interfaces. The Ecuador telecom MNO market size for enterprise lines is growing at a 3.10% CAGR; this acceleration stems from hyperscaler entry that lowers cloud prices and raises the connectivity requirements of small manufacturers and agribusiness exporters. Banks now insist on redundant fiber plus LTE fail-over at every branch, while oil producers backhaul seismic data over secured microwave rings into Quito data centers for AI processing.

Google’s public-sector alliance with CNT injects cloud workflows into hospitals and schools, spurring additional MPLS and SD-WAN contracts. Telconet’s two tier-IV data centers host more than 300 corporate tenants that increasingly purchase cross-connects to all three mobile networks, reflecting demand for carrier diversity. Although household wallets tighten during rolling blackouts, enterprises justify telecom upgrades by offsetting productivity losses, making this segment a stabilizing force in otherwise cyclical revenues for operators.

Geography Analysis

Ecuador’s coastal province of Guayas remains the largest revenue engine, buoyed by Guayaquil’s 88.59 Mbps median download speed and dense base-station grid that supports higher data-bundle monetization. Retail, logistics, and port activities produce sustained demand for IoT asset tracking and edge analytics, translating into thicker margins for operators with fiber-backed microwave rings around the city. Pichincha, anchored by Quito, hosts the public-sector cloud initiative led by CNT and Google, creating a pool of government contracts that require secure multiline connectivity across ministries and hospitals.

The Galapagos archipelago, although small in population, enjoys outsized strategic visibility. SES’s satellite upgrade to 2.5 Gbps and the pending 20 Tbps Galapagos Cable System allow operators to craft premium eco-tourism bundles that include unlimited roaming data and virtual-reality wildlife experiences. These high-ARPU tourist products diversify revenue away from Ecuador’s mainland consumer base and mitigate seasonality. Coastal Esmeraldas and Manabí provinces benefit from submarine cable landings that shave latency for fintech users, a differentiator for digital banks underwriting micro-loans to artisanal fishing communities.

Inland Sierra regions face rugged topography that complicates tower placement, but mandatory infrastructure sharing has opened multi-operator clusters on existing ridges, slashing build costs by up to 35%. Mobile network operators are also piloting solar-powered micro-sites in Cotopaxi to address energy-supply volatility. In the Amazon Basin, Zamora-Chinchipe and Orellana attract bespoke private-LTE grids serving copper and petroleum extraction; although subscriber densities are thin, average revenue per industrial connection exceeds USD 28 monthly, well above the consumer average of USD 7.20. Cross-border corridors near Colombia and Peru leverage “roam-like-at-home” pricing to spur informal trade, making seamless handoffs a customer-experience imperative for long-haul truckers and agro-exporters.

Competitive Landscape

The Ecuador telecom MNO market is moderately concentrated around Claro, Millicom-backed Tigo, and state-owned CNT. Claro defends its 54% share by coupling nationwide LTE-Advanced coverage with aggressive FTTH-to-mobile bundles; its ZTE Light ODN roll-out cut fiber installation time by 30%, accelerating penetration in gated communities. Tigo has begun re-branding Movistar stores and migrating 3.7 million subscribers to its Panama billing stack, aiming to unlock cross-border roaming synergies and launch pan-regional content partnerships. CNT, leveraging sovereign-backed financing, fulfills regulatory coverage mandates first, then parlay those assets into enterprise projects such as secure VPNs for ministries.

Technology partnerships create additional differentiation. Nokia’s 5G pilot with CNT in Guayaquil and Manta delivers fixed-wireless speeds near 850 Mbps, showcasing a future upgrade path once auctions resolve. Telconet, though not an MNO, exerts influence by selling wholesale fiber and co-location services to all three players, a gatekeeper role bolstered by Huawei’s all-flash arrays that quadruple IOPS efficiency. Tower companies SBAC and Phoenix Tower International own over 60% of shared sites, allowing operators to shift from capex-heavy builds to opex-based leases and keep balance-sheet leverage in check.

Strategically, operators eye adjacent verticals. Claro bundles cloud storage and cybersecurity add-ons for SMEs. Tigo explores embedded-finance products leveraging Millicom’s fintech know-how, while CNT positions itself as the government’s digital-services arm, potentially securing long-term annuity contracts. Competitive intensity therefore moves from price warfare to solution depth, with customer-experience KPIs such as net-promoter score rising in board-level priority. Given these dynamics, future consolidation appears unlikely under current antitrust thresholds, but spectrum-sharing alliances for 5G rural deployments are plausible should auction prices remain elevated.

Ecuador Telecom MNO Industry Leaders

Claro

Movistar

CNT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CNT and Google announced a strategic cooperation agreement covering 30 initiatives spanning healthcare, education, transparency, state modernization, and security.

- October 2024: SBA Communications acquired 7,000 towers from Millicom for USD 975 million under a 15-year master leaseback, with 2,500 new towers planned

- September 2024: Telconet finalized branching units and landing points for the CSN-1 submarine cable, increasing international bandwidth resilience.

- June 2024: The ICT Ministry granted radio-spectrum permits to seven firms, broadening competitive opportunities across mobile and fixed wireless domains.

Ecuador Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the forecast revenue for Ecuador’s mobile-network-operator segment by 2030?

The Ecuador telecom MNO market size is projected to reach USD 1.32 billion by 2030.

Which carrier currently leads subscriber share in Ecuador?

Claro holds around 50% Ecuador telecom MNO market share, maintaining clear leadership.

How fast is the enterprise segment growing relative to consumer lines?

Enterprise subscriptions are set to grow at a 3.10% CAGR between 2025 and 2030, outpacing the flat consumer segment.

What impact do high spectrum reserve prices have on 5G rollout?

Elevated reserve prices delay nationwide 5G deployment and subtract an estimated 0.7 percentage points from forecast CAGR.

Why are operators focusing on private LTE in the Amazon Basin?

Mining and oilfield sites demand reliable, low-latency connectivity, allowing operators to secure high-ARPU industrial IoT contracts.

How does dollarization influence mobile-service pricing?

Dollarized pricing shields consumers from currency devaluation, enabling predictable monthly plans that support smartphone upgrades.

Page last updated on: