Dominican Republic Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

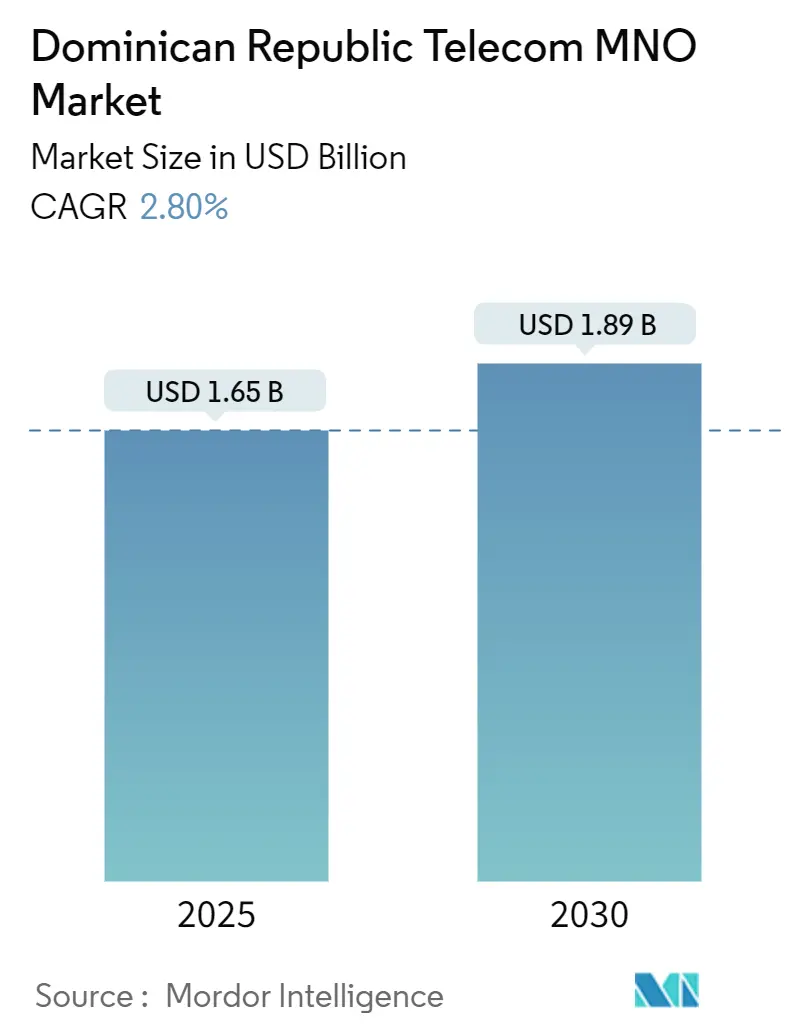

| Market Size (2025) | USD 1.65 Billion |

| Market Size (2030) | USD 1.89 Billion |

| Growth Rate (2025 - 2030) | 2.80% CAGR |

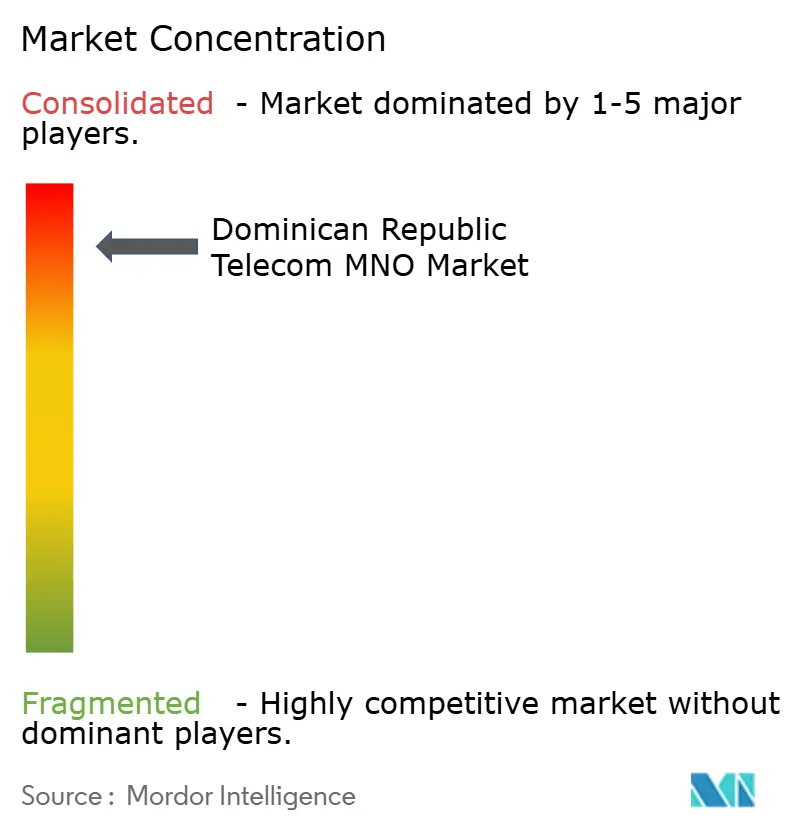

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dominican Republic Telecom MNO Market Analysis by Mordor Intelligence

The Dominican Republic Telecom MNO Market size is estimated at USD 1.65 billion in 2025, and is expected to reach USD 1.89 billion by 2030, at a CAGR of 2.80% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 12.40 million subscribers in 2025 to 13.76 million subscribers by 2030, at a CAGR of 2.10% during the forecast period (2025-2030). Growth is modest because mobile penetration is approaching 90% of the population, prompting operators to fine-tune pricing, upsell premium data plans, and bundle value-added services rather than chase new SIM activations. Heavy tourism inflows, surging remittance volumes, and the government-backed “RD Conectada” broadband program continue to unlock incremental revenue streams, especially for high-capacity data and roaming services. Regulatory clarity following the 2023-2025 spectrum reforms supports long-term network investment, while public-sector financing from the Inter-American Development Bank channels capital toward rural coverage upgrades. Operators simultaneously confront currency volatility, power-grid instability, and rural deployment economics that temper headline expansion, keeping the Dominican Republic Telecom MNO market firmly in a maturation phase.

Key Report Takeaways

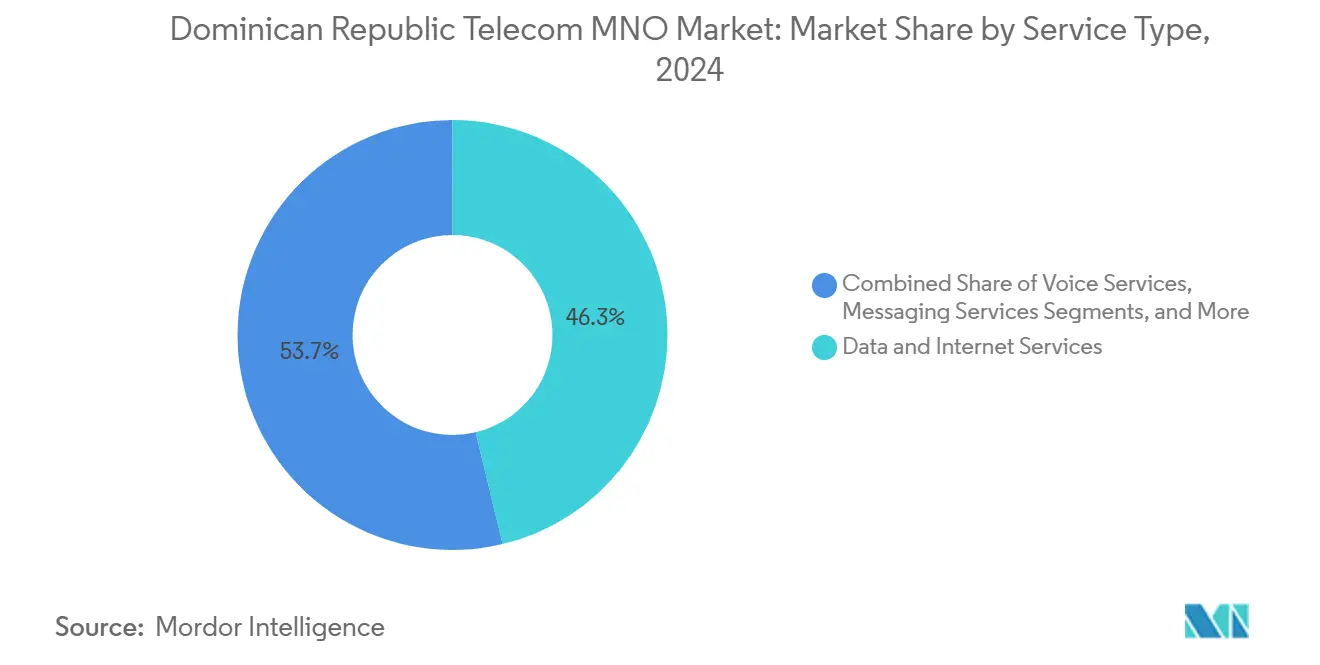

- By service type, data and internet services led with a 46.27% share of the Dominican Republic Telecom MNO market in 2024 and are expected to expand at a 2.95% CAGR through 2030, solidifying their role as the primary revenue engine.

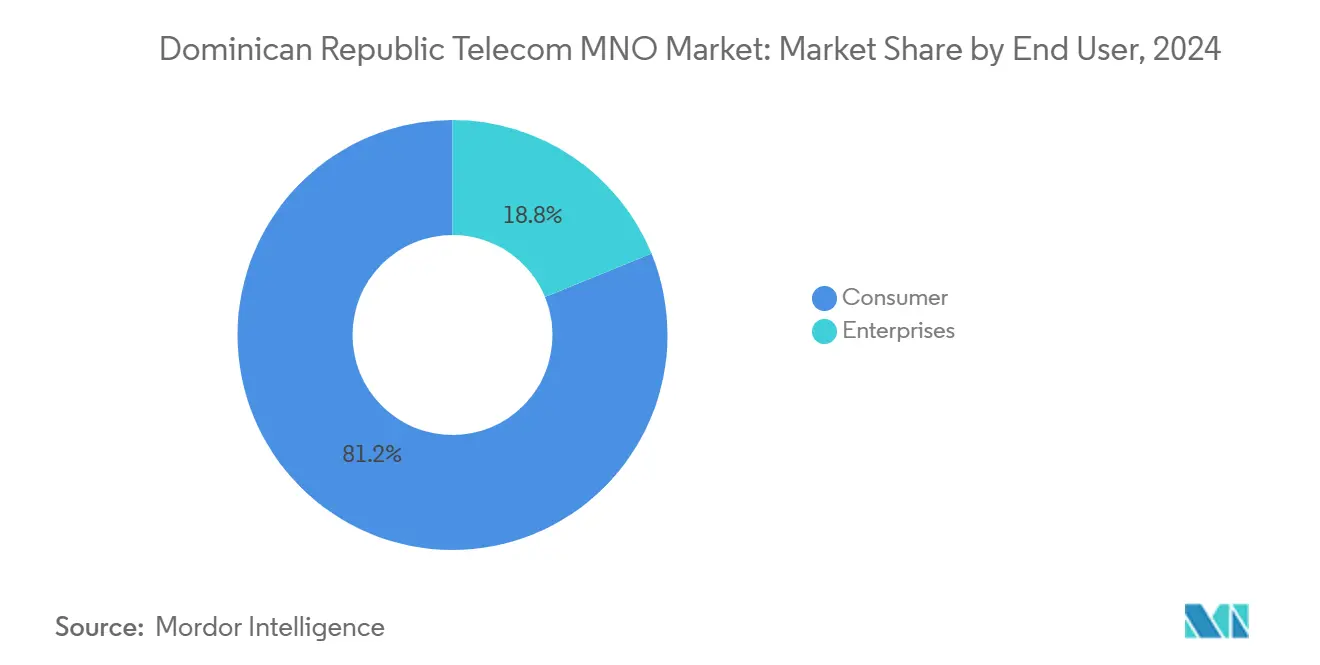

- By end user, the consumer segment accounted for 81.19% of the Dominican Republic Telecom MNO market size in 2024, whereas the Enterprise segment record the fastest 3.33% CAGR to 2030 as businesses digitize operations.

Dominican Republic Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Mobile-data Demand from 4G-to-5G Migration | +0.8% | Santo Domingo, Santiago and other urban corridors | Medium term (2-4 years) |

| National 5G Spectrum Auctions and Investment Incentives | +0.6% | Nationwide | Medium term (2-4 years) |

| Accelerated FTTH Rollouts under “RD Conectada” Broadband Plan | +0.5% | Rural and peri-urban | Long term (≥ 4 years) |

| Tourism-sector Need for Seamless Roaming and Wi-Fi Offload | +0.4% | Coastal resort clusters | Short term (≤ 2 years) |

| Fintech and E-commerce Boom Raising Mobile-payment Traffic | +0.3% | Urban hubs, extending to secondary towns | Medium term (2-4 years) |

| Smart-remittance IoT Kiosks in Rural Areas | +0.2% | Remittance-heavy rural provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Mobile-data Demand from 4G-to-5G Migration

Subscribers shifting from legacy 4G plans to 5G packages generate 40-50% higher ARPU as richer applications such as augmented-reality tours and real-time analytics go mainstream. Claro Dominicana targets 60% 5G population coverage by 2028, and infrastructure sharing agreements are trimming capex payback periods for rival networks. Affordable mid-tier 5G-enabled handsets from Chinese OEMs catalyze device upgrades, while government-mandated minimum speed increases raise baseline performance expectations. The resulting traffic surge compels operators to densify urban macro-sites and deploy small cells, materially lifting data monetization prospects within the Dominican Republic Telecom MNO market.

National 5G Spectrum Auctions and Investment Incentives

The 2021 and 2023 auctions raised a combined USD 74 million, assigning paired 700 MHz and 3.5 GHz bands to Claro and Altice under coverage-obligation clauses that extend advanced broadband to underserved districts. [1]CommsUpdate, “Dominican Republic 5G auction raises USD74m,” commsupdate.com Tax credits for projects exceeding USD 10 million further sweeten returns, nudging operators to front-load capex. Harmonization with 2023 World Radiocommunication Conference guidelines enables bulk procurement of global-band devices at lower unit cost, shortening rollout timelines and accelerating Dominican Republic Telecom MNO market penetration of premium data services.

Accelerated FTTH Rollouts under “RD Conectada” Broadband Plan

The state aims for 70% household broadband penetration by 2030, co-financing fiber trunk routes that double as 5G backhaul. [2]Listín Diario, “RD Conectada impulsa banda ancha,” listindiario.com Operators that already own fiber convert wholesale capacity into retail revenue by bundling gigabit FTTH with mobile-voice add-ons, reinforcing customer stickiness. Rural fiber spurs fixed wireless access propositions where terrain hinders trenching, giving carriers a low-latency alternative for households outside dense cores. Educational connectivity mandates attach enterprise-grade service level agreements, opening fresh B2B revenue streams inside the Dominican Republic Telecom MNO market.

Tourism-sector Need for Seamless Roaming and Wi-Fi Offload

Roughly 8 million international arrivals each year consume 3 to 5 times more mobile data than residents, generating lucrative roaming fees that cushion margin compression in mature urban zones. [3]Latinometrics, “The Dominican Investment Record,” latinometrics.com Resorts outsource managed Wi-Fi to carriers, creating annuity-like contracts and relieving cellular congestion during peak travel quarters. The tourism rebound post-pandemic sustains bandwidth upgrades along coastal belts, anchoring near-term revenue optimism for the Dominican Republic Telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Spectrum and Sector-specific Taxation Burden | -0.4% | Nationwide | Short term (≤ 2 years) |

| Rural Last-mile CAPEX vs Low ARPU Economics | -0.3% | Remote provinces | Long term (≥ 4 years) |

| Grid-power Instability Causing Network Outages | -0.2% | Nationwide, heavier in interior regions | Medium term (2-4 years) |

| FX-linked Equipment Costs Pressuring Margins | -0.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Spectrum and Sector-specific Taxation Burden

Regulatory levies swallow 15-20% of gross telecom revenue, squeezing free cash flow just as 5G requires elevated capital intensity. Smaller carriers with thinner balance sheets endure disproportionate strain, limiting competitive dynamism and slowing rural build-outs. Frequent policy revisions compound forecasting risk, encouraging defensive pricing that blunts growth momentum across the Dominican Republic Telecom MNO market.

Rural Last-mile CAPEX vs Low ARPU Economics

Deploying a single rural cell site can cost more than USD 50,000 yet serve fewer than 500 subscribers, pushing breakeven beyond seven years under current tariff ceilings. [4]OPEC Fund, “The 24-hour challenge: Can the Dominican Republic keep the lights on?,” opecfund.org Mountainous terrain inflates tower-erection and maintenance expenses, while diesel-backup generators raise opex when grid power falters. Operators therefore prioritize urban densification unless public subsidies offset poor economics, perpetuating the urban-rural digital divide inside the Dominican Republic Telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Revenue Transformation

Data and Internet Services captured 46.27% of the Dominican Republic Telecom MNO market share in 2024 and are growing at a 2.95% CAGR through 2030, reflecting explosive smartphone usage and video-heavy consumption habits. Operators monetize this appetite through tiered unlimited plans, sponsored-data partnerships, and zero-rating of strategic streaming platforms. The segment’s revenue resilience is reinforced by 97.4% broadband-capable connections, enabling smooth migration toward 5G-rich communication services. Voice remains relevant yet increasingly bundled into app-based VoLTE, lowering switching friction. Messaging struggles under OTT cannibalization, though enterprise-grade RCS sparks incremental traffic by integrating payment links and chatbots.

IoT and M2M applications, especially in smart agriculture and fleet telematics, remain nascent but promise outsized upside once nationwide narrow-band support materializes. Meanwhile, OTT and PayTV bundles ride the cord-cutting trend as operators reposition as content aggregators, shoring up ARPU against price wars. Roaming, cloud PBX, cybersecurity, and other value-added solutions round out a diversified portfolio that cushions volatility in any one revenue stream, keeping the Dominican Republic Telecom MNO market size on a controlled ascent.

By End User: Enterprise Digitalization Accelerates Growth

The Consumer base generated 81.19% of the Dominican Republic Telecom MNO market size in 2024, yet Enterprise revenues are rising faster at a 3.33% CAGR toward 2030. Manufacturing export zones, call-center clusters, and a burgeoning fintech scene rely on dedicated internet access, SD-WAN, and cloud on-ramp services. Operators upsell mobile workforce solutions, IoT dashboards, and cybersecurity add-ons, capturing higher-margin spend per account. Public-sector modernization under the Digital Agenda 2030 feeds demand for secure virtual private networks connecting ministries, schools, and e-government portals.

On the consumer side, unlimited family plans, handset financing, and loyalty apps help contain churn in a saturated SIM base. Cross-subsidy from enterprise cash flows funds 5G densification that also benefits households, creating virtuous infrastructure-sharing. As more SMEs formalize operations, dual-play bundles draw them into the enterprise bracket, enlarging addressable opportunity within the Dominican Republic Telecom MNO industry.

Geography Analysis

The Dominican Republic Telecom MNO market earns roughly 60% of its revenue from the Santo Domingo and Santiago metropolitan corridors, even though these regions house less than 40% of residents, a testament to higher ARPU and service adoption in urban pockets. Dense city grids justify deep fiber backhaul and small-cell overlays, enabling gigabit-class experiences that underpin premium pricing. Coastal tourism belts, from Punta Cana to Puerto Plata, post seasonal revenue spikes tied to roaming and hotel Wi-Fi offload, compelling operators to deploy portable capacity solutions during high season.

Rural provinces lag on coverage and quality because terrain and limited grid electricity hike deployment and operating costs; yet they represent a latent growth frontier as remittance-dependent households adopt mobile money and farmers explore IoT soil sensors. The Inter-American Development Bank’s USD 115 million loan earmarks rural towers and fiber spurs, sharing financial risk with private carriers. Border municipalities with Haiti exhibit unique cross-network calling patterns that inflate interconnect revenues but also demand heightened security protocols.

International capacity continues to strengthen: the Deep Blue One and SAm-1 submarine cable additions in 2024 increased inbound bandwidth diversity while trimming wholesale transit costs. Average national download speeds rose more than 25% between 2023 and 2025, enhancing the Dominican Republic Telecom MNO market’s regional competitiveness. Operators increasingly favor tower-sharing and public-private build-operate-transfer models to bridge the profitability gap between dense and sparse geographies, ensuring a more balanced spatial revenue mix by the decade’s close.

Competitive Landscape

Three companies dominate the Dominican Republic's telecom market. Claro Dominicana leverages América Móvil’s global scale to secure favorable equipment deals and expedite network upgrades. Altice Dominicana leverages European fixed-line expertise to manage fiber build-out costs and offer bundled mobile and gigabit services, thereby securing longer customer contracts. Viva (Trilogy Dominicana) competes on price, positions itself as a challenger brand, and leverages tower-sharing agreements to optimize capital budgets while meeting its spectrum license obligations.

These scale advantages drive distinct investment strategies. Claro has allocated USD 200 million for a fiber backbone that doubles as low-latency 5G transport and is testing AI-powered network optimization tools to maximize spectrum capacity. Altice focuses on fiber-to-the-home, aiming to cross-sell unlimited mobile data plans to gigabit fixed-service users. Viva minimizes costs by leasing neutral-host towers and outsourcing radio-access maintenance, enabling aggressive prepaid promotions despite limited spectrum depth. All three operators partner with resorts to provide managed Wi-Fi, capturing high-margin tourism traffic and easing macro-cell network congestion during peak seasons.

Network-sharing agreements are expanding as 5G raises capital intensity. Joint rural site builds reduce costs and fulfill universal-service obligations tied to recent spectrum auctions. Satellite broadband providers, such as Starlink, are entering remote areas, adding competition despite higher tariffs compared to mainstream mobile packages. For now, incumbent cellular operators retain an edge through control of retail distribution, national roaming, and robust billing systems. However, alternative access platforms are increasing competitive pressure as the decade progresses.

Dominican Republic Telecom MNO Industry Leaders

Viva (Trilogy Dominicana)

Altice Dominicana S.A.

Claro Dominicana

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: INDOTEL adopted Resolution 032-2025 to align the National Frequency Attribution Plan with WRC-23 outcomes, cementing long-term spectrum clarity.

- January 2025: Authorities mandated higher national minimum internet speeds, compelling operators to accelerate network upgrades.

- June 2024: Digicel activated the Deep Blue One subsea fiber system, diversifying regional backhaul options and improving international traffic resilience.

- May 2024: Telxius extended the SAm-1 cable to Puerto Rico, adding redundancy and lowering wholesale IP transit costs for Dominican carriers.

Dominican Republic Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the projected revenue for mobile-network operators in the Dominican Republic by 2030?

The Dominican Republic Telecom MNO market size is forecast to reach USD 1.89 billion by 2030.

How fast is the shift to 5G occurring nationwide?

Claro and Altice secured mid-band spectrum in recent auctions and must achieve nationwide 5G coverage targets within four years, driving medium-term network densification.

Which service line is growing fastest?

Data and Internet Services are expanding at a 2.95% CAGR to 2030 thanks to video-streaming demand and 5G premium tiers.

Why are enterprise revenues gaining share?

SMEs and the public sector are adopting cloud-based and mobile-first workflows, lifting Enterprise connectivity revenues at a 3.33% CAGR.

What challenges impede rural expansion?

High tower-build costs, grid instability and low ARPU extend payback periods, requiring universal-service funding and infrastructure sharing to close gaps.

How concentrated is market ownership?

The top two carriers hold more than 80% of industry revenue, resulting in an oligopolistic structure with a concentration score of 9.

Page last updated on: