Bolivia Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.42 Billion |

| Market Size (2030) | USD 1.77 Billion |

| Growth Rate (2025 - 2030) | 4.46% CAGR |

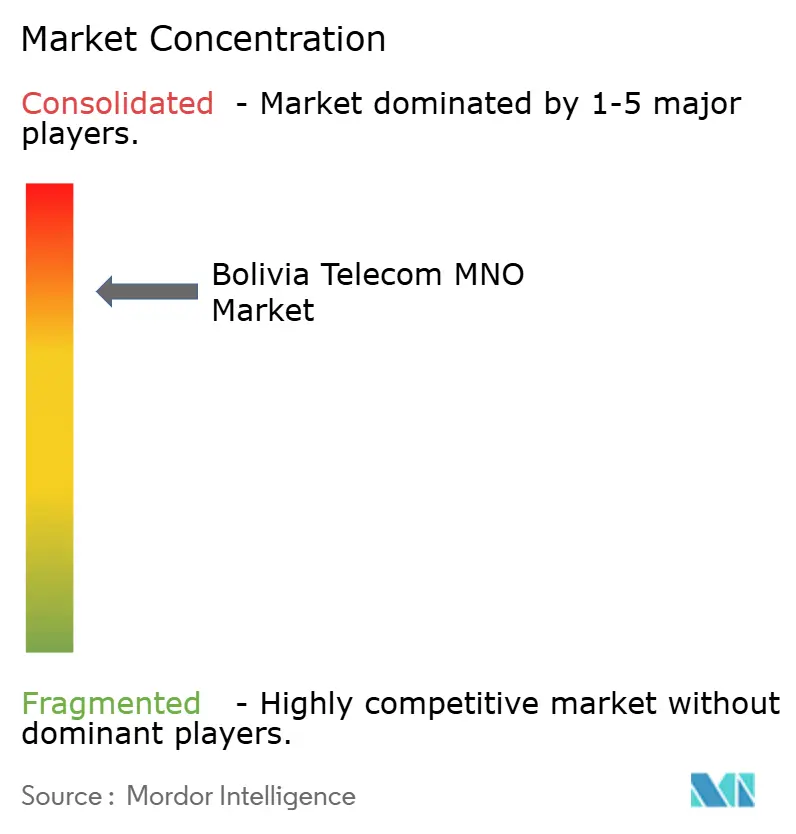

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bolivia Telecom MNO Market Analysis by Mordor Intelligence

The Bolivia Telecom MNO Market size is estimated at USD 1.42 billion in 2025, and is expected to reach USD 1.77 billion by 2030, at a CAGR of 4.46% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 12.10 million subscribers in 2025 to 14.40 million subscribers by 2030, at a CAGR of 3.56% during the forecast period (2025-2030).

Mounting demand for mobile broadband, state-funded backbone fiber, and forthcoming Pacific-route subsea cable capacity are steering the Bolivia Telecom MNO market toward higher-value digital services. Operators are shifting capital toward 4G densification, early 5G spectrum preparation, and enterprise connectivity bundles as mobile internet penetration has already climbed to 91%. The government’s view of connectivity as a basic right codified in General Law No. 164 underpins investment incentives, while the cooperative overlay in 15 provinces tempers aggressive price hikes yet expands rural reach. Currency-peg pressures, low ARPU, and spectrum cost uncertainty restrain margins, but enterprise IoT demand, cloud off-takes from mining and agritech, and regional transit cost reductions sustain a medium-term growth runway.

Key Report Takeaways

- By service type, data services led with 47.11% revenue share in 2024; IoT and M2M is forecast to expand at a 4.81% CAGR through 2030.

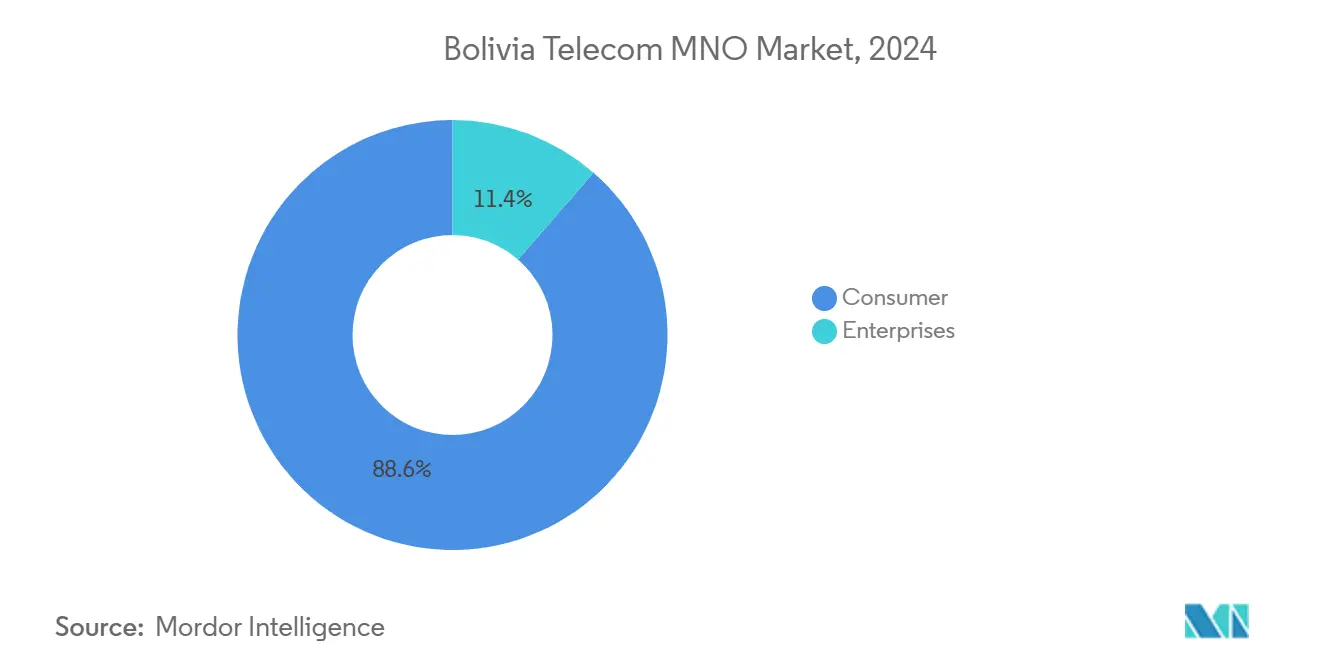

- By end user, consumer lines held 89.50% of the Bolivia Telecom MNO market share in 2024, while enterprise services are advancing at a 7.40% CAGR to 2030.

Bolivia Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile-data traffic from 4G uptake | +1.2% | La Paz, Santa Cruz, Cochabamba | Short term (≤ 2 years) |

| State-funded national fiber backbone | +0.8% | Municipal capitals and rural areas | Medium term (2-4 years) |

| Enterprise digitization for B2B IoT and cloud | +0.6% | Urban, mining belts, agri-zones | Medium term (2-4 years) |

| Regulatory rural-coverage mandates | +0.4% | Remote regions nationwide | Long term (≥ 4 years) |

| Cooperative-led FTTH in secondary cities | +0.3% | Tarija, Sucre, Potosí | Medium term (2-4 years) |

| Pacific-route subsea cable access | +0.2% | National – international gateways | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding Mobile-Data Traffic from 4G-Smartphone Uptake

Bolivia recorded a leap in mobile internet penetration from 23% in 2013 to 91% in 2024, and 4G now covers 87% of the population. Traffic growth stresses networks yet catalyzes ARPU-mix improvements for operators owning richer spectrum portfolios. Entel delivers average download speeds of 11.55 Mbps, while Tigo optimizes latency for mobile gaming audiences.[1]Ookla, “Speedtest Global Index Bolivia 2024,” ookla.com The surge encourages densification projects in La Paz’s highlands and Santa Cruz’s lowlands and widens the Bolivia Telecom MNO market for digital content partners.

State-Funded National Fiber Backbone Expansion

Entel’s program to blanket 100% of municipal capitals with FTTH by 2025 is the country’s largest telecom build. Combined with its Starlink lease for remote villages, the fiber spine reduces backhaul costs and frees mobile capacity for video and fintech apps.[2]BNamericas, “Entel to Cover All Municipal Seats with Fiber by 2025,” The build supports e-government services and underpins enterprise SLA commitments, reinforcing the Bolivia Telecom MNO market as a gateway for landlocked neighbors to Pacific bandwidth.

Enterprise Digitisation Driving B2B Cloud and IoT Connectivity

Mining automation, smart irrigation, and municipal sensor grids fuel an enterprise connectivity CAGR of 7.40%. The AGRIdigitalización program already links 10,000 smallholders to market and finance platforms. Corporate clients accept premium tariffs, enabling operators to diversify away from low-margin consumer bundles and lift the Bolivia Telecom MNO market toward SaaS-linked revenue streams.

Regulatory Push for Rural Coverage and Universal-Service Obligations

Bolivia’s telecom law obliges licensees to extend service into low-income districts, enforced by the ATT regulator. The PRONTIS scheme has installed sites in nearly 9,000 locations. Mandatory reach creates barriers for newcomers yet grants incumbents protected volumes and voice/data cross-subsidy leeway, stabilizing the Bolivia Telecom MNO market’s long-term subscriber base.[3]Digital Watch, “Bolivia PRONTIS Programme Update 2024,” digitalwatch.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low ARPU and price-sensitive consumers | -0.9% | Rural and peri-urban zones nationwide | Short term (≤ 2 years) |

| High spectrum fees and limited 5G availability | -0.6% | Nationwide | Medium term (2-4 years) |

| Lengthy municipal tower permitting | -0.4% | Dense urban boroughs | Short term (≤ 2 years) |

| Backhaul bottlenecks in Amazon and Andean areas | -0.3% | Beni, Pando, mountainous western corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low ARPU and Price-Sensitive Consumer Base

Average revenue per user slumped from USD 40.3 in 2013 to USD 11.1 by 2023 even as connections multiplied. A persistent dollar peg amplifies handset import costs, but operators cannot push tariffs without inviting churn. Cooperative members also veto steep rises, forcing carriers to chase volumes rather than premium upsells across the Bolivia Telecom MNO market.

High Spectrum Fees and Limited 5G Allocations

June 2024 licensing extended access to only seven firms, and upcoming 5G auctions may impose even higher reserve prices. Capital diverted to spectrum weakens rollout budgets, delaying nationwide standalone 5G and testing the Bolivia Telecom MNO market’s readiness for ultralow-latency verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Sustain Revenue Dominance

Data services generated 47.11% of 2024 revenue, anchoring the Bolivia Telecom MNO market size for operator cash flows. Voice continues its secular retreat as over-the-top applications cannibalize minutes. IoT and M2M lines, though still niche, are booked to post a 4.81% CAGR to 2030, the fastest clip within the Bolivia Telecom MNO market, as miners fit autonomous haulage fleets and municipalities instrument waste and water grids. SMS persists for enterprise notifications, but Pay-TV and OTT face margin squeeze from international streamers demanding costly licenses. Bundled 4G+fixed fiber plans allow carriers to upsell content at thin incremental cost, stabilizing ARPU drift.

The Bolivia Telecom MNO market size for IoT is projected to accelerate when the Humboldt and SAC-2 cables push transit prices down, making cloud endpoints more affordable. Operators that pair NB-IoT overlays with edge data centers near Cochabamba are positioned to capture device activation surges once Bolivia’s 5G spectrum is unlocked.

By End User: Consumers Still Rule but Enterprises Accelerate

Residential subscribers contributed 89.50% of 2024 lines, a legacy of Bolivia’s mobile-first adoption path. Price ceilings and cooperative influence anchor consumer tariffs, so carriers differentiate with loyalty wallets, zero-rating social apps, and handset financing. Even with low yields, the segment guarantees base load for spectrum monetisation across the Bolivia Telecom MNO market.

Enterprises, while smaller in volume, are pacing a 7.40% CAGR to 2030. Government smart-city pilots, mining telemetry feeds, and agritech sensor networks require fixed-mobile converged SLAs that command double-digit ARPU premiums. The ATT-UNDP SIMAT collaboration illustrates official intent to funnel public-sector workloads to domestic carrier clouds. The Bolivia Telecom MNO market share for enterprise lines is therefore set to widen as macro-industries digitize.

Geography Analysis

Government “Digital Nation” Program Accelerating National Fibre Backbone Roll-out

Regionally, bandwidth concentration favors the western highlands around La Paz and Cochabamba, but Tarija logged Bolivia’s quickest cellular downloads at 19.32 Mbps in 2024, and Santa Cruz topped fixed speeds at 34.72 Mbps. The Pacific-crossing Humboldt system, the SAC-2 upgrade, and a Peru-Chile terrestrial interconnect will trim wholesale IP prices, lifting the Bolivia Telecom MNO market size for transit-intensive OTT and gaming segments.

Rugged Amazon basin and Andean slopes still pose capex hurdles. PRONTIS installations in 9,000 remote nodes partially bridge gaps, yet tower access often hinges on municipal sign-offs that stretch beyond 12 months. Entel’s FTTH campaign to hit every municipal capital by 2025 should even out speed inequities and enable small ISPs to piggy-back backhaul at lower lease rates.

A hybrid competitive map emerges: 15 not-for-profit cooperatives dominate pockets such as Santa Cruz cooperativa COTAS, while national carriers cross-subsidize rural sites from urban profits. Border-gateway diversity elevates Bolivia’s status as a landing backup for Paraguay and northern Argentina, deepening the Bolivia Telecom MNO market’s strategic relevance in the Andean corridor.

Competitive Landscape

5G Spectrum Awards to All Three Tier-1 MNOs Enabling Premium ARPU Uplift

The market revolves around Entel, Tigo, and Viva, with Entel controlling about 50% of SIMs. Opensignal metrics show Entel winning coverage at 8.6 points, Tigo ranking first on consistent-quality at 51.8%, and Viva leading uploads at 7.7 Mbps. Entel deploys state capital to blanket fiber and has leased Starlink capacity for jungle areas, locking early-mover rights for 5G carrier aggregation trials.

Tigo rides operational efficiency, posting USD 1.37 billion revenue in Q1 2025 and targeting 60% mobile 5G coverage by 2028. Viva capitalizes on nimble upgrades and niche SME bundles. Each player eyes enterprise IoT as the next battleground, exploiting differential latency and security tiers to outmaneuver rivals within the Bolivia Telecom MNO market.

Cooperatives, while marginal in national share, control critical local loops in 15 provinces. Their community mandate curbs price hikes but grants grassroots loyalty. As 5G approaches, carriers may seek leasing or joint-build pacts with cooperatives to accelerate rural rollout without duplicating steel in inhospitable terrains, preserving cash for spectrum fees and edge computing nodes.

Bolivia Telecom MNO Industry Leaders

Entel Bolivia

Tigo Bolivia

Viva Bolivia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Entel confirmed plans to extend FTTH to 100% of municipal capitals, marking Bolivia’s largest fiber program.

- November 2024: Cirion Technologies unveiled the SAC-2 subsea route to improve LatAm-North America latency.

- June 2024: ICT Ministry awarded radio spectrum licences to seven companies, shaping 5G auction dynamics.

Bolivia Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Bolivia Telecom MNO market in 2025?

The Bolivia Telecom MNO market size is USD 1.42 billion in 2025 and is projected to grow to USD 1.77 billion by 2030 at a 4.46% CAGR.

Which service segment generates most revenue for carriers?

Data services generate 47.11% of 2024 revenue, reflecting the shift from voice to mobile broadband usage.

What is the fastest-growing segment through 2030?

IoT and M2M lines are forecast to register a 4.81% CAGR, propelled by mining automation, agritech sensors, and smart-city projects.

How concentrated is operator ownership?

Three nationwide operators—Entel, Tigo, and Viva—hold nearly all subscriptions, with Entel alone at roughly 50%, resulting in a market concentration score of 9.

What geographic zones show the highest mobile speeds?

Tarija leads cellular downloads at 19.32 Mbps, while Santa Cruz tops fixed broadband speeds at 34.72 Mbps, due to heavier infrastructure investment in those economic centers.

Which factor most limits near-term revenue growth?

Low ARPU, currently around USD 11.1, constrains margin expansion because Bolivia’s consumer base remains highly price sensitive.

Page last updated on: