Insulated Parcel Mailers And Small-Format Cold-Chain Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.61 Billion |

| Market Size (2030) | USD 5.23 Billion |

| Growth Rate (2025 - 2030) | 7.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Insulated Parcel Mailers And Small-Format Cold-Chain Packaging Market Analysis by Mordor Intelligence

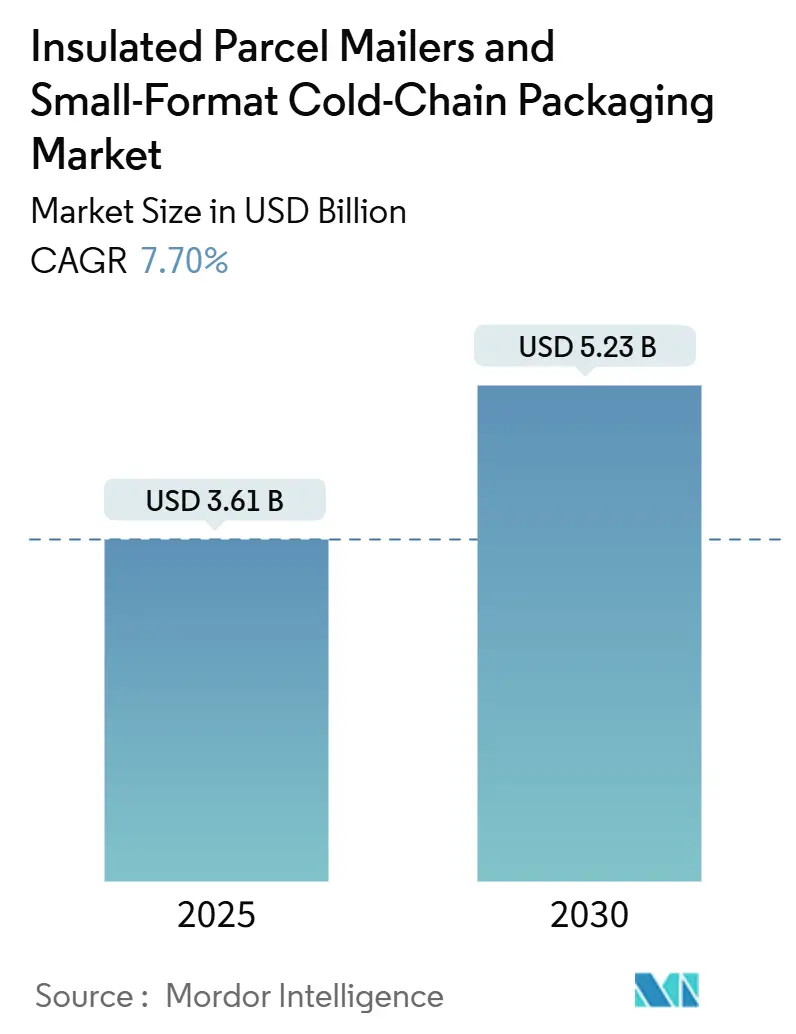

The insulated parcel mailers and small-format cold-chain packaging market size reached USD 3.61 billion in 2025 and is projected to increase to USD 5.23 billion by 2030, growing at a 7.70% CAGR. Strong uptake for temperature-sensitive biologics, the meal-kit e-commerce boom, and stricter global distribution practice enforcement are collectively driving demand for lightweight formats that maintain contents between 2 °C and 8 °C during last-mile transit. Pharmaceutical distributors continue to specify validated, sensor-enabled shippers, while meal-kit brands favor fiber-based mailers that meet municipal curbside recycling rules. Competitive rivalry is intensifying as suppliers race to scale vacuum-insulated panel (VIP) pouches that provide -80°C protection without the need for dry ice. At the same time, the volatility of recycled paper pulp and PET resin pricing complicates cost management, prompting converters to enter into long-term supply agreements and implement hedging strategies. Across regions, North America maintains the largest installed base of qualified shippers, but the Asia-Pacific region is translating rapid direct-to-patient drug adoption into the fastest regional growth pace.

Key Report Takeaways

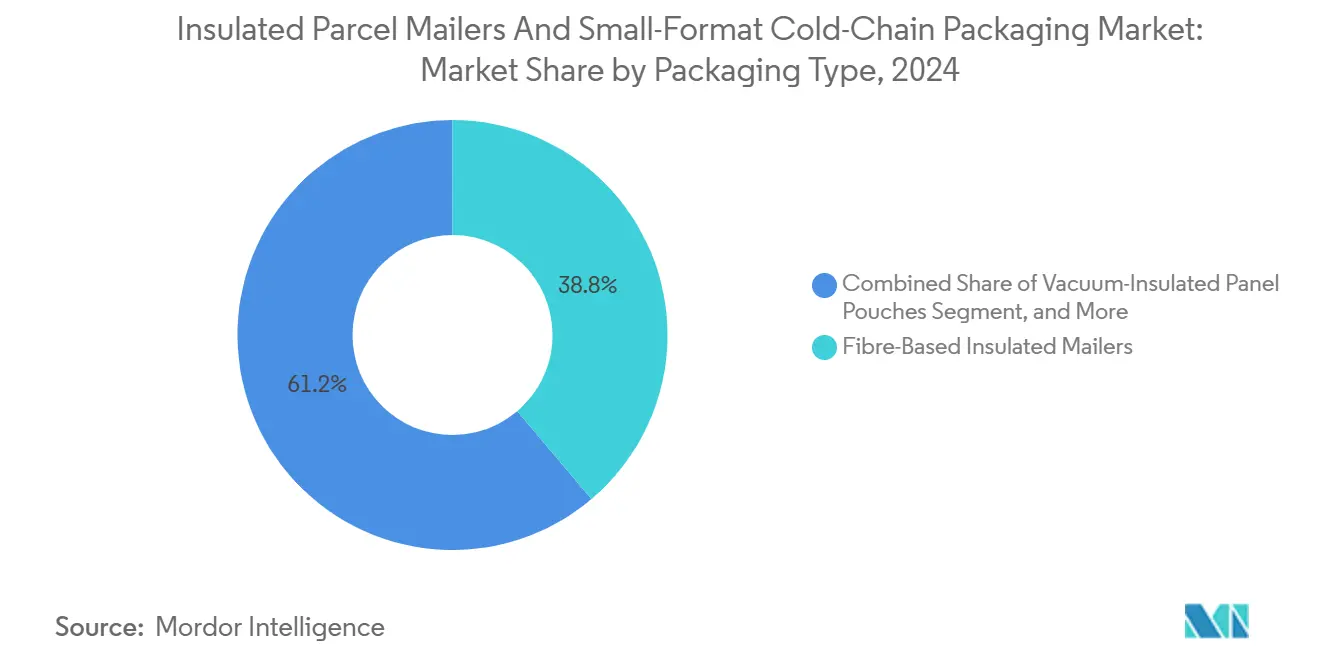

- By packaging type, fiber-based insulated mailers captured 38.81% of the insulated parcel mailers and small-format cold-chain packaging market share in 2024.

- By temperature range, the insulated parcel mailers and small-format cold-chain packaging market size for deep-frozen solutions (-80 °C) is projected to grow at a 9.17% CAGR through 2030.

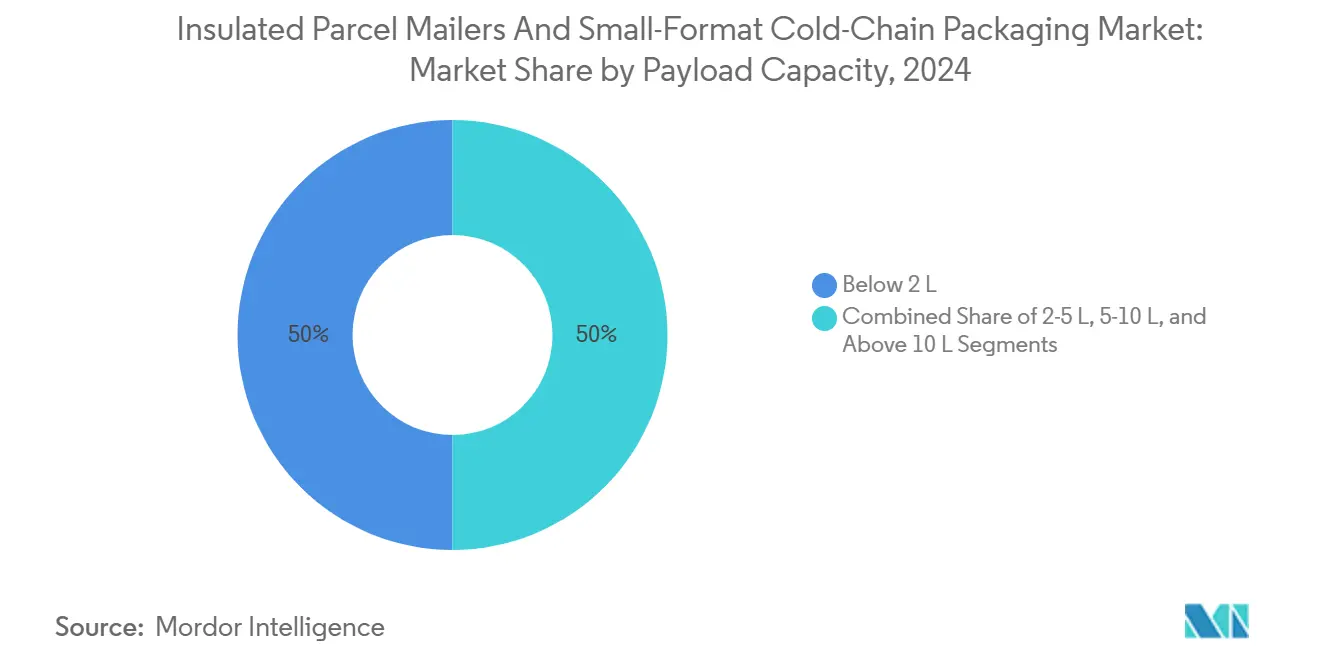

- By payload capacity, the below 2-liter class held 41.26% of the insulated parcel mailers and small-format cold-chain packaging market size in 2024.

- By end-user industry, the insulated parcel mailers and small-format cold-chain packaging market size for direct-to-patient pharmacy services is projected to grow at an 8.51% CAGR through 2030.

- By geography, North America led the insulated parcel mailers and small-format cold-chain packaging market with a 43.71% share in 2024.

Global Insulated Parcel Mailers And Small-Format Cold-Chain Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Temperature-Sensitive Biologics Pipeline Expansion | +2.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| E-Commerce Meal-Kit Boom in Last-Mile Delivery | +1.8% | North America, Europe, APAC urban centers | Short term (≤ 2 years) |

| Stricter GDP and USP <1079> Compliance Enforcement | +1.5% | Global, led by FDA and EMA jurisdictions | Long term (≥ 4 years) |

| Corporate ESG Mandates Favoring Curb-Side-Recyclable Liners | +1.2% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Surge in Decentralized Clinical Trials (DCTs) Post-Covid-19 | +0.9% | Global, accelerated in North America and Europe | Short term (≤ 2 years) |

| Growth of Direct-to-Patient Pharmacy Services in APAC | +0.8% | APAC core, spill-over to emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Temperature-Sensitive Biologics Pipeline Expansion

Cell and gene therapy approvals rose to 15 in 2024, each requiring -80 °C logistics validated for excursions and duration.[1]Food and Drug Administration, “Approved Cellular and Gene Therapy Products,” fda.gov Manufacturers have increased global cell-therapy capacity by 40%, and shipping specifications now routinely require VIP liners to minimize dry-ice sublimation and maintain the viability of payloads for over 96 hours. Updated FDA guidance demands real-time temperature telemetry, turning IoT-ready mailers into a de facto compliance tool. Large contract logistics providers have begun housing -80 °C buffer storage at regional cross-docks, shrinking lane risk. As a result, the insulated parcel mailers and small-format cold-chain packaging market faces a sustained pull from clinical to commercial biotech pipelines.

E-Commerce Meal-Kit Boom in Last-Mile Delivery

Meal-kit deliveries increased 28% in 2024, shifting cold-chain volume toward small, consumer-address shipments. Thermal packaging now accounts for 35% of total kit logistics costs, sparking interest in curbside-recyclable fiber liners, such as Aptar’s FiberCool, which maintains a temperature range of 2 °C-8 °C for 48 hours. Urban density favors payloads of less than 5 liters, allowing couriers to meet elevator space limits and consumer demand for smaller, more frequent orders. Meal-kit brands test reusable totes but struggle with reverse logistics compliance, keeping single-trip recyclable mailers in pole position. This dynamic underpins short-term growth but also accelerates the quest for lighter, mono-material substrates.

Stricter GDP and USP 1079 Compliance Enforcement

The FDA issued 47 warning letters in 2024 over temperature excursions during pharma distribution. New USP chapters require mapping every shipper configuration, pushing suppliers to maintain ISO 13485 documentation for each temperature band. The European Medicines Agency mirrored these rules, stretching compliance pressure across multinational drug lanes. Sponsors now score bidders partly on the depth of their validation files, nudging smaller vendors without quality systems out of tender lists. Consequently, premium pricing for fully qualified mailers holds firm, reinforcing revenue quality within the insulated parcel mailers and small-format cold-chain packaging market.

Corporate ESG Mandates Favoring Curb-Side-Recyclable Liners

Eighty-nine percent of Fortune 500 pharmaceutical firms published 2030 recyclable packaging targets in 2024. Pfizer is committed to 100% recyclable secondary packaging, and ProAmpac answered with commercial FiberCool mailers that meet ASTM curbside guidelines.[2]Packaging World Staff, “Aptar Launches FiberCool Recyclable Insulated Packaging,” packagingworld.com City-level recycling programs now accept fiber-based insulation, removing prior landfill roadblocks. Brands also use life-cycle data to quantify greenhouse-gas savings when switching from metalized bubble to fiber. Sustainability scorecards in RFPs, therefore, tilt awards toward mono-material, recyclable designs, intensifying the competitive race for patent-protected paper-based barrier technologies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled Paper Pulp and PET Resin Prices | -1.4% | Global, particularly impacting North America and Europe | Short term (≤ 2 years) |

| Limited Payload Flexibility vs Active Packaging | -0.9% | Global, concentrated in pharmaceutical applications | Medium term (2-4 years) |

| Inefficient Reverse-Logistics in Emerging Markets | -0.7% | APAC emerging markets, Latin America, Africa | Long term (≥ 4 years) |

| Uncertain Regulatory Stance on PFAS-Based Barrier Films | -0.6% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Recycled Paper Pulp and PET Resin Prices

Recycled PET spot prices swung 34% in 2024, trading between USD 1,200 and USD 1,610 per metric ton, while paper pulp climbed 18% on supply disruptions.[3]Plastics News Staff, “Recycled PET Prices 2024,” plasticsnews.com Converter margins compressed as recycled-content mandates locked them into pricier input mixes. Quarterly index-linked contracts replaced annual fixed-price agreements, but smaller converters lack scale to hedge. Elevated resin costs ripple quickly into meal-kit channels, which are highly price sensitive. Short-term margin pressure, therefore, slows reinvestment in new curbside-recyclable designs, moderating upside for the insulated parcel mailers and small-format cold-chain packaging market.

Limited Payload Flexibility vs Active Packaging

Passive mailers struggle with payload variability compared with compressor-based active containers. Pharmaceutical lanes shifting from bulk pallet shipments to mixed-dose parcel flows require flexible cube designs. VIP pouches partly address the gap but remain constrained by preset phase-change brick positions. Sponsors shipping seasonal volume spikes face inventory complexity when stockpiling multiple SKUs. Consequently, some biologics shippers allocate critical risk-share lanes back to active systems, dampening full adoption of passive insulated parcel formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Fiber Mailers Anchor Mass Adoption

Fiber-based insulated mailers accounted for 38.81% of the insulated parcel mailers and small-format cold-chain packaging market in 2024, reflecting corporate sustainability mandates and the increasing availability of municipal recycling capacity. VIP pouches, although still emerging, are forecast to grow at a 9.87% CAGR, driven by pharma qualification programs for -80 °C shipments. Metalized bubble designs maintain a niche hold in cost-constrained lanes, whereas phase-change sleeves meet the demanding requirements of chemical shipments that require tight temperature windows of 15 °C-25 °C.

ProAmpac’s FiberCool launch in June 2024 highlights how paper-backed barriers can achieve hold times of 2 °C-8 °C while enabling curbside recycling. Pelican BioThermal lifted VIP output by 45% in 2024 to target gene-therapy sponsors requiring longer routes without dry ice. ISO 13485 documentation remains easier for entrenched formats, giving incumbents time to optimize their cost curves before new entrants scale in. As these innovations gain share, the insulated parcel mailers and small-format cold-chain packaging market sees a dual path: high-volume fiber solutions for meal kits and high-value VIP pouches for biologics.

By Temperature Range: Deep-Frozen Demand Accelerates

Refrigerated mailers dominated the market with a 46.54% share in 2024, driven by the high volume of insulin, vaccine, and monoclonal antibody shipments. Deep-frozen -80 °C formats are projected to post a 9.17% CAGR to 2030, as gene-therapy and cell-therapy volumes expand and regulatory bodies tighten excursion tolerances. The ambient and −20 °C categories maintain steady roles in specialty food and legacy pharmaceutical distribution.

VIP technology eliminates dry-ice sublimation, extending hold times past 120 hours and lowering hazardous-goods surcharges. IoT sensors embedded in VIP walls feed continuous lane data to quality teams, supporting new USP evidence requirements. As airlines limit dry-ice quotas for safety, shippers pivot to phase-change bricks that charge at -80 °C freezers. These factors will keep deep-frozen formats a high-margin niche within the insulated parcel mailers and small-format cold-chain packaging market.

By Payload Capacity: Small Cubes Mirror Precision Medicine

Mailers under 2 liters captured 41.26% share of the insulated parcel mailers and small-format cold-chain packaging market size in 2024 as precision-medicine therapies and single-dose biologics shifted cargo from pallets to parcels. The 2-5 liter class, favored by meal-kit proteins and clinical trial kits, is set to register a 9.89% CAGR through 2030.

Decentralized trials multiplied in 2024, pushing sponsors to ship investigational products direct to patients, with average kit sizes of 3 liters. Smaller cubes reduce freight costs and fit into apartment lobbies, yet still maintain 48-hour temperature windows. Technology providers now offer modular brick layouts that allow clients to toggle between 1-liter and 2-liter payloads without requalifying the entire system. Such configurability further widens adoption across healthcare and food channels.

By End-User Industry: Pharma Remains the Center of Gravity

Pharmaceutical firms generated 52.49% of 2024 revenue, reflecting the high value per shipment and uncompromising quality expectations. Direct-to-patient pharmacy services are projected to have the fastest trajectory, with an 8.51% CAGR, driven by the shift of specialty drugs from hospital to home care.

Regulators approved 47 novel specialty therapies in 2024, and 73% required refrigerated or frozen storage and distribution. Patient-centric models rely on secure parcel mailers that maintain temperature throughout the doorstep dwell time. Clinical research organizations, another growing buyer group, demand fully documented mailers to support regulatory dossiers. Together, these factors lock pharma and its adjacent services into the growth engine of the insulated parcel mailers and small-format cold-chain packaging market.

Geography Analysis

North America accounted for 43.71% of 2024 revenue, thanks to the United States’ vast biologics pipeline, a mature 3PL network, and stringent GDP auditing. Large parcel integrators offer region-wide cold-chain nodes, enabling same-day recovery in the event of lane deviations. Shipper hesitancy regarding single-use plastics is accelerating the adoption of fiber-based replacements in Canada and the United States.

The Asia-Pacific region is the fastest-growing region, with a 9.29% CAGR through 2030, driven by China’s 32% expansion of cold-chain infrastructure to meet the drug needs of an aging population. India’s CRO sector added dozens of hybrid trial hubs that rely on 2-8 °C mailers. Regional governments are aligning GDP rules with ICH guidelines, encouraging multinational sponsors to standardize parcel packaging across borders.

Europe shows steady gains as the EMA and national agencies harmonize GDP audits and support curbside recycling goals. The Middle East and Africa, as well as Latin America, lag behind due to infrastructure gaps, but airline partnerships, such as those between Sonoco ThermoSafe and Saudia Cargo, aim to improve reliable lane access.

Competitive Landscape

Market concentration is moderate, with the top five suppliers accounting for approximately 35% of global revenue. Sonoco ThermoSafe, Pelican BioThermal, CSafe Global, TemperPack, and ProAmpac all maintain ISO-certified validation labs that attract pharma RFPs. Arsenal Capital Partners’ USD 725 million buyout of Sonoco ThermoSafe in September 2025 underscores private-equity confidence in segment cash flows.

Technology leadership is split: TemperPack bets on recyclable fiber mailers, ProAmpac scales mono-material liners, while Pelican BioThermal expands VIP reuse pools. CSafe’s Silverpod MAX RE showcases pallet-size solutions made with recycled materials that still meet stringent -20 °C lanes. Start-ups such as Ecovative Design pilot mycelium insulation, targeting zero-waste credentials.

Regional expansion strategies dominate 2025 playbooks. Nordic Cold Chain Solutions added EU distribution partners, and UPS Healthcare invested in ultra-low nodes in the Netherlands. Suppliers with in-house molding plus logistics ties win because they can guarantee lane integrity and sustainability reporting in a single bundle.

Insulated Parcel Mailers And Small-Format Cold-Chain Packaging Industry Leaders

-

Sonoco ThermoSafe

-

Cold Chain Technologies Inc.

-

Pelican BioThermal LLC

-

TemperPack Technologies Inc.

-

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Arsenal Capital Partners closed the USD 725 million acquisition of Sonoco ThermoSafe to accelerate product innovation and global reach.

- October 2024: Pelican BioThermal introduced the Crēdo Vault reusable shipper with advanced phase-change bricks and IoT tracking.

- October 2024: Sonoco ThermoSafe signed a master lease pact with Saudia Cargo to expand shipper pools across the Middle East and Africa.

- August 2024: CSafe Global debuted the Silverpod MAX RE pallet shipper built with recycled materials for large-volume pharma lanes.

Global Insulated Parcel Mailers And Small-Format Cold-Chain Packaging Market Report Scope

| Fibre-Based Insulated Mailers |

| Metalized Bubble Mailers |

| Phase-Change Material (PCM) Sleeves |

| Vacuum-Insulated Panel Pouches |

| Ambient 15-25 degree Celsius |

| Refrigerated 2-8 degree Celsius |

| Frozen -20 degree Celsius |

| Deep-frozen -80 degree Celsius |

| Below 2 L |

| 2-5 L |

| 5-10 L |

| Above 10 L |

| Pharmaceuticals |

| Clinical Research Organisations |

| Food and Meal-Kit Providers |

| Specialty Chemicals |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Type | Fibre-Based Insulated Mailers | ||

| Metalized Bubble Mailers | |||

| Phase-Change Material (PCM) Sleeves | |||

| Vacuum-Insulated Panel Pouches | |||

| By Temperature Range | Ambient 15-25 degree Celsius | ||

| Refrigerated 2-8 degree Celsius | |||

| Frozen -20 degree Celsius | |||

| Deep-frozen -80 degree Celsius | |||

| By Payload Capacity | Below 2 L | ||

| 2-5 L | |||

| 5-10 L | |||

| Above 10 L | |||

| By End-User Industry | Pharmaceuticals | ||

| Clinical Research Organisations | |||

| Food and Meal-Kit Providers | |||

| Specialty Chemicals | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the insulated parcel mailers and small-format cold-chain packaging market?

It is valued at USD 3.61 billion in 2025 and is projected to reach USD 5.23 billion by 2030.

Which region shows the fastest growth in cold-chain parcel mailers?

Asia-Pacific leads growth with a forecast 9.29% CAGR through 2030 on the back of expanding direct-to-patient services.

Which packaging type is gaining share the quickest?

Vacuum-insulated panel pouches are growing at 9.87% CAGR thanks to gene-therapy and cell-therapy shipping needs.

Why are fiber-based mailers popular with meal-kit brands?

They comply with curbside recycling programs and maintain 2 °C-8 °C for up to two days, cutting landfill waste.

How do new GDP regulations influence shipper selection?

Tighter FDA and EMA rules demand fully validated mailers with real-time temperature data, favoring ISO-certified suppliers.

What is the main cost pressure facing packaging converters?

Volatile pricing for recycled paper pulp and PET resin squeezes margins and complicates long-term contract pricing.

Page last updated on: