Security Paper Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.92 Billion |

| Market Size (2031) | USD 8.73 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

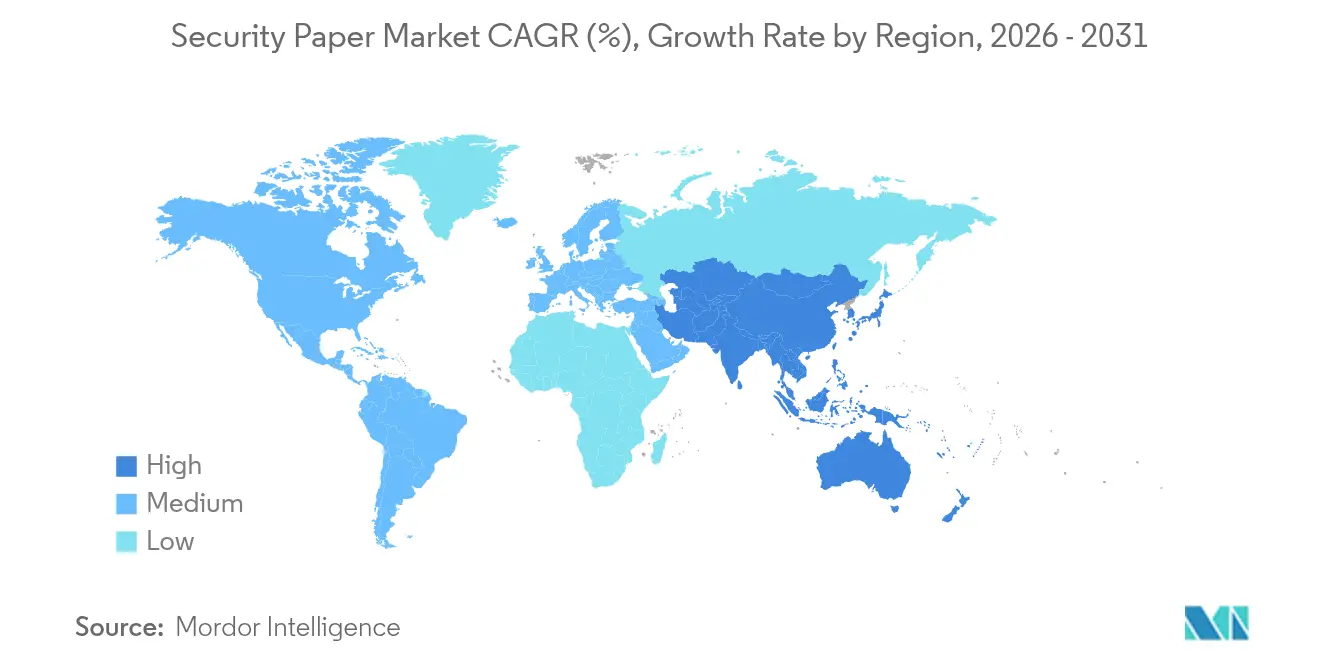

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

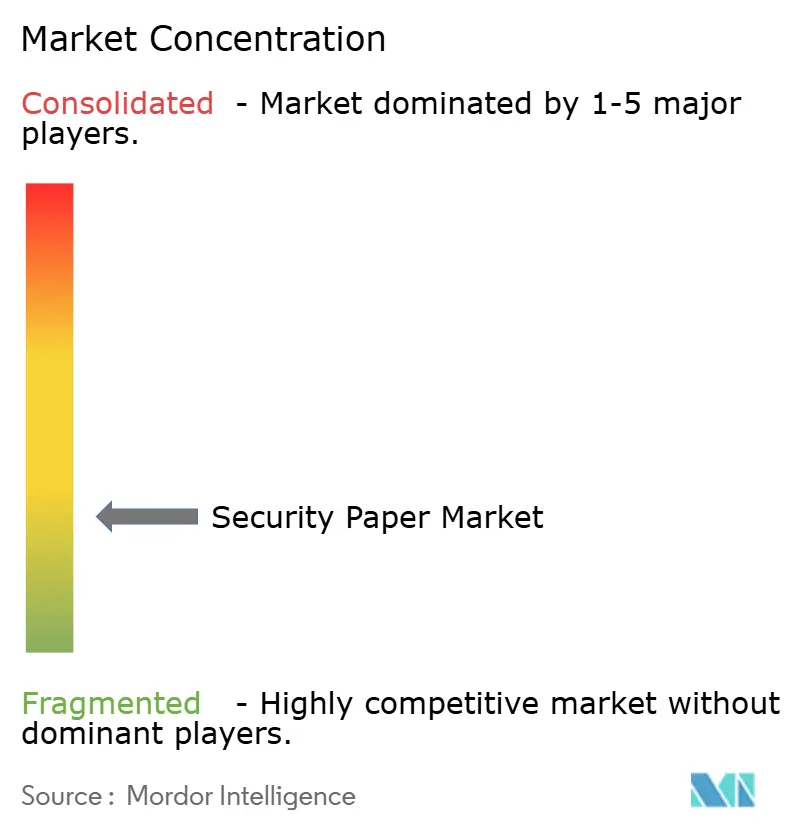

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Security Paper Market Analysis by Mordor Intelligence

The security paper market size is expected to grow from USD 6.60 billion in 2025 to USD 6.92 billion in 2026 and is forecast to reach USD 8.73 billion by 2031 at 4.78% CAGR over 2026-2031. The momentum comes from a steady rise in sophisticated counterfeiting attempts, renewed banknote redesign programmes, and growing demand for tamper-evident packaging in pharmaceutical and luxury value chains. India’s April 2025 alert on high-quality counterfeit ₹500 notes highlights the advanced techniques now confronting central banks. Simultaneously, polymer and hybrid substrates are gaining favour because they enable complex optical features and extend note life, giving issuers a lower total cost of ownership. Supply-chain resilience is emerging as a strategic theme, with manufacturers exploring recycled and region-specific fibres to offset cotton volatility and align with sustainability mandates.

Key Report Takeaways

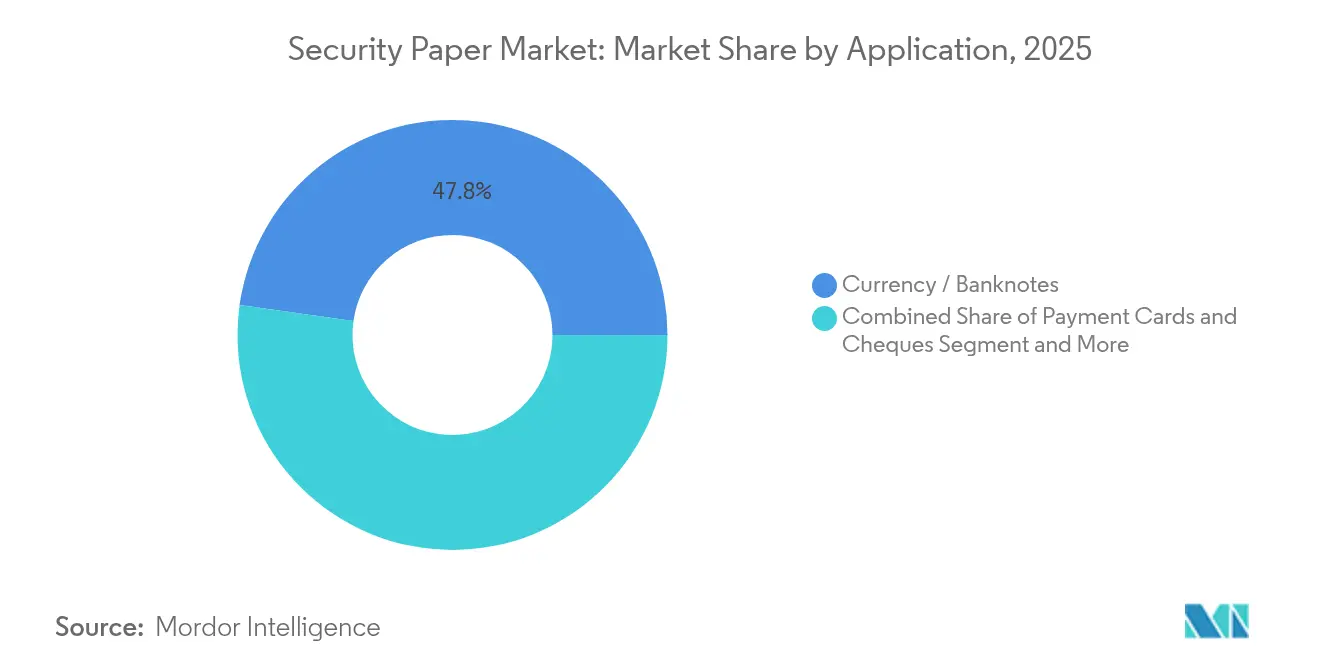

- By application, currency and banknotes led with 47.78% of security paper market share in 2025, while secure packaging and labels are projected to expand at an 8.22% CAGR to 2031.

- By substrate type, cotton-fibre paper accounted for 56.10% of the security paper market size in 2025; recycled-fibre papers hold the fastest outlook at a 9.05% CAGR through 2031.

- By security feature, security threads captured 33.21% of security paper market share in 2025, whereas RFID/NFC-embedded formats are advancing at a 6.29% CAGR.

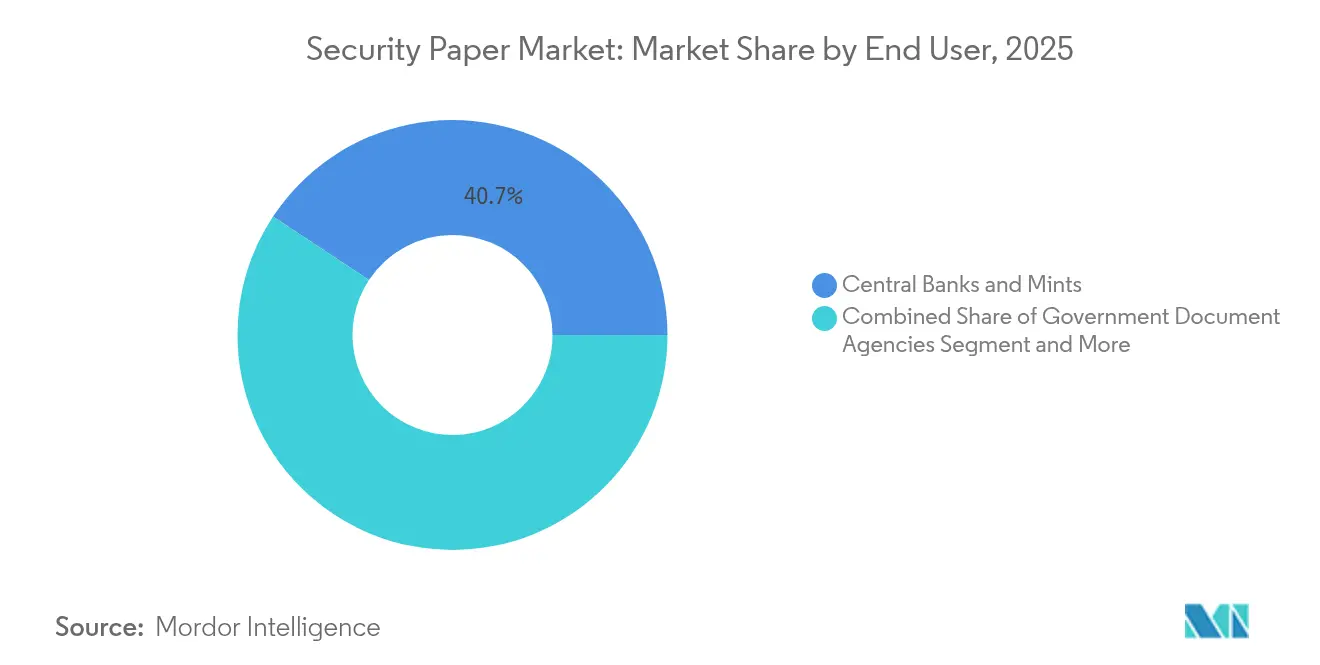

- By end user, central banks and mints held 40.72% revenue share in 2025; secure printing houses post the highest projected CAGR at 6.88% to 2031.

- By geography, Asia-Pacific contributed 32.10% of 2025 revenue and is forecast to grow at 6.74% CAGR, maintaining regional primacy.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Security Paper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising fraud and counterfeiting incidents | +1.2% | Global, with acute impact in APAC and emerging markets | Short term (≤ 2 years) |

| Expansion of secure-document programmes (e-passports, ID) | +0.8% | Global, led by North America & EU regulatory frameworks | Medium term (2-4 years) |

| Polymer and hybrid substrate migration | +0.6% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Excise-stamp mandates for sin-tax goods | +0.4% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| RFID/NFC-integrated "smart paper" adoption | +0.3% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Tamper-evident packaging for high-value goods | +0.2% | Global, concentrated in pharmaceutical and luxury sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Fraud and Counterfeiting Incidents

Escalating fraud has become a structural growth pillar for the security paper market. India’s 2025 seizure of near-perfect counterfeit INR 500(USD 5.58) notes illustrates how spelling micro-errors are now among the few visible detection clues. The U.S. Department of Homeland Security warns that generative AI will heighten document forgery sophistication, forcing issuers to adopt multi-layer substrates that combine tactile, optical and digital elements.[1]U.S. Department of Homeland Security, “Impacts of Adversarial Use of Generative AI on Homeland Security,” dhs.gov Central banks respond by shortening redesign cycles, which keeps the security paper market in a perpetual upgrade mode. Across Asia-Pacific, polymer trials show counterfeit rejection rates improving by double digits once transparent windows and micro-perforations are introduced, reinforcing confidence in substrate migration. For producers, the arms race translates into steady R&D spend and a premium pricing corridor that buffers margins even when commodity fibres face inflationary spikes.

Expansion of Secure-Document Programmes

Governments are modernising identity infrastructures, intertwining physical credentials with digital verification rails. TOPPAN’s 2024 acquisition of HID Citizen Identity Solutions fused traditional security printing with biometric enrolment platforms, offering agencies a single procurement lane. Patent filings exceed 6,000 for blockchain-anchored identity solutions, signalling industry commitment to privacy-preserving, user-centric ID architectures.[2]Matthew Comb & Andrew Martin, “Mining Digital Identity Insights: Patent Analysis Using NLP,” SpringerOpen, eurasip.org National projects such as the Philippines’ abaca-infused polymer passports demonstrate localisation strategies that embed regional fibres into global-grade substrates. Demand therefore tilts toward hybrid papers that can store encrypted chips while still displaying visible watermarks, cementing a multi-dimensional revenue stream for the security paper market.

Polymer and Hybrid Substrate Migration

Durability, lifecycle economics and feature density are propelling polymer adoption. Romania’s 100-leu commemorative polymer note showcased transparent windows and laser micro-perforations, elevating counterfeit deterrence without compromising throughput on high-speed sorters. Libya joined the cohort in 2025, switching to De La Rue’s SAFEGUARD substrate that integrates SPARK Live optical ink. Field data from the Philippines indicate polymer notes last up to 7.5 years—roughly 2.5 times longer than cotton—delivering lifecycle savings that outweigh higher initial procurement costs. Hybrid compositions that sandwich cotton layers between polymer film are gaining traction, easing transition pains by retaining tactile familiarity while boosting strength. Such shifts sustain premium substrate volumes, helping the security paper market offset incremental digital-payment erosion.

Excise-Stamp Mandates for Sin-Tax Goods

Governments are tightening excise controls on tobacco, alcohol and other high-levy items, with U.S. Code Title 26 prescribing explicit stamp standards that only specialised security papers can meet. European Union directives similarly require holographic or UV-tagged stamps, generating niche but recurring orders for security printers. Mandates serve dual objectives—securing tax receipts and curbing illicit trade—which together ensure that stamp volumes remain resilient even when broader print markets decline. Suppliers that can blend overt holograms with covert RFID chips gain competitive advantage, positioning the security paper market for adjacent growth in track-and-trace solutions for pharmaceuticals and beverages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-payment substitution | -0.8% | Global, accelerated in developed markets | Medium term (2-4 years) |

| High cost of advanced security features | -0.4% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Sustainability pressure on cotton fibre sourcing | -0.3% | Global, with acute impact in North America and EU | Long term (≥ 4 years) |

| Climate-driven fibre supply disruptions | -0.2% | Regional, concentrated in major cotton-producing areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-Payment Substitution

Central-bank research shows consumer preference shifting toward digital wallets, casting a structural shadow on cash volumes.[3]European Central Bank, “Consumer Demand for Central Bank Digital Currency as a Means of Payment,” ecb.europa.eu Trials of a digital pound with offline functionality by the Bank of England illustrate that central-bank digital currencies could replicate many cash roles without physical notes. While migration will be gradual—Japan still issued 280 million high-tech notes in 2024—the trajectory is downward in mature economies. For the security paper market, that means defensive strategies of portfolio diversification toward passports, tax stamps and smart packaging.

High Cost of Advanced Security Features

Cutting-edge inks infused with TiO₂ and ZnO nanoparticles or AI-driven watermark algorithms raise unit costs, especially for budget-constrained issuers. Patent applications covering diffractive pigments and composite label films underscore the R&D intensity required to stay ahead of counterfeiters. Emerging markets often opt for stripped-down features, exposing them to higher fraud risk and slowing premium adoption within the security paper industry. Suppliers must therefore balance feature depth with cost efficiency, offering tiered solutions that keep the security paper market accessible across income brackets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Currency Dominance Amid Packaging Growth

Currency and banknotes retained a commanding 47.78% slice of the security paper market in 2025, underpinned by Japan’s roll-out of 3D-hologram notes and frequent redesigns across Asia-Pacific. Despite an uptick in digital wallets, cash remains crucial for unbanked populations, giving the security paper market resilient base volumes. Cheques and payment cards hang on as secondary use cases, especially in regions where bank penetration is climbing. Identity and travel documents occupy a growing middle ground because e-passport issuance cycles are accelerating in Europe and North America. Secure packaging and labels, although only a mid-single-digit share today, are projected to rise at an 8.22% CAGR to 2031 as pharmaceutical serialisation laws widen coverage. That trajectory signals a gradual re-balancing of the security paper market away from pure currency dependency.

The segment mix also reflects risk-management strategies. Central banks favour polymer for high-denomination notes yet still specify cotton for lower tiers, spreading sourcing risk. Packaging converters, by contrast, gravitate towards synthetic and recycled fibres that pair security with sustainability. Ticketing and certificate applications retain niche demand in academic and events sectors, providing long-tail revenue. Collectively, these dynamics underline why application diversification is the foremost hedge against structural cash decline for companies active in the security paper market.

By Substrate Type: Cotton Leadership Faces Sustainability Pressure

Cotton-fibre sheets secured 56.10% of the security paper market share in 2025, a position earned through centuries-old manufacturing ecosystems and user familiarity. Yet consecutive droughts in Texas and a 10% output dip in India forced imports to double, inflating input costs and exposing supply vulnerability. Polymer substrates now enjoy clear durability and cost-in-use advantages, encouraging central banks in Libya, Romania and the Philippines to transition core denominations. Hybrid papers marry cotton’s tactile feel with polymer film strength, easing psychological barriers among cash users and enabling gradual equipment retrofits.

Recycled-fibre variants register a 9.05% CAGR, the fastest pace in the segment, driven by environmental scorecard pressures from both regulators and corporate sustainability officers. Abaca and linen offer region-specific opportunities, giving issuers a chance to localise supply and cut transport emissions. Looking ahead, lifecycle assessments will dictate substrate selection as much as counterfeit resistance, elevating the strategic value of in-house fibre R&D within the security paper industry.

By Security Feature Integration: Traditional Features Evolve

Security threads dominated 2025 with 33.21% use across issued papers, thanks to their proven track record and compatibility with existing printing lines. Watermarks continue as a foundational layer, but the rise of optically variable devices makes each new series visibly distinct, complicating counterfeiter learning curves. UV and IR fibres add covert layers that require specialist scanners, a popular choice for passports and excise stamps. Holographic imagery has moved from flat foils to dynamic portrait elements, as showcased in Japan’s 2024 notes. The fusion of multiple features is standard practice, with seven or more separate elements common on high-value denominations, reinforcing the multi-pronged defence strategy that sustains premium ASPs in the security paper market.

Second-generation innovations integrate machine-readable pixels within threads, letting bank-sorting machines authenticate notes at 40 notes per second. Colour-shifting inks provide a quick public check, while micro-text adds forensic back-office verification. The arms race creates a virtuous cycle of vendor-issuer collaboration, with each redesign feeding back into R&D pipelines for subsequent improvement. As a result, the security paper industry enjoys a built-in cadence of feature refreshes that cushions revenue against macro-economic swings.

By End User: Central Banks Lead Diversification

Central banks and mints consumed 40.72% of global volume in 2025, leveraging long-term supply contracts that grant them pricing power yet provide suppliers with predictable cash flows. Government document agencies form the next tier, hungry for chip-enabled passports that dovetail with e-gate infrastructure upgrades at borders. Commercial banks still commission cheques, bank drafts and high-value certificates, but their share is plateauing as online channels gain traction. Secure printing houses emerge as the fastest-expanding end user, clocking a 6.88% CAGR, since outsourcing allows smaller governments to bypass capital-intensive internal print works.

Brand-protection specialists and packaging converters round out the user matrix, positioning the security paper market to capture demand from industries outside its traditional lane. This widening spectrum compels suppliers to develop modular platforms that can serve both currency and consumer-goods clients without compromising risk segregation or regulatory compliance.

By Smart Paper Integration: RFID/NFC Adoption Accelerates

RFID-enabled formats are projected to outpace all conventional feature sets at a 6.29% CAGR, propelled by falling chip costs and rising demand for interactive authentication. Early pilots in luxury handbags allow customers to tap labels with smartphones for provenance checks, an experience that is migrating to high-value drugs and electronics. On the governmental side, e-passports already pair RFID with laser-engraved portraits, and next-generation ID cards are expected to embed multi-frequency antennas compatible with national database readers. These capabilities transform security paper from a static barrier to a dynamic data conduit, creating ancillary revenue in software analytics and lifecycle services. Suppliers capable of horizontal integration across paper, chip and middleware layers hold a strategic edge as the security paper market pivots toward cyber-physical convergence.

Geography Analysis

Asia-Pacific held 32.10% of 2025 revenue, and the region’s security paper market size is forecast to expand at 6.74% CAGR as polymer adoption widens and national ID projects scale. Japan’s July 2024 banknote launch proved the commercial viability of 3D hologram portraits, likely setting a new benchmark for neighbours planning redesigns. The Philippines rolled out its first polymer series in January 2025, anchoring its monetary modernisation programme. India’s twin dynamics of counterfeit threats and cotton-supply worries are spurring interest in blended substrates that reduce dependence on imported lint.

North America and Europe sit in maturity phase yet still command premium ASPs because issuers demand layered security that meets ISO and ICAO passport stipulations. The European Central Bank’s exploration of a digital euro introduces strategic uncertainty, but Romania’s 2024 polymer commemorative note confirms that Euro-linked markets remain committed to high-security physical cash for the foreseeable future.

The Middle East and Africa show leap-frog potential; Libya’s 2025 polymer switch is a bellwether for neighbouring states. Gulf issuers such as the UAE embrace durable polymer substrates to cope with harsh climates. South America, led by Brazil and Argentina, is expected to prioritise tax-stamp revamps to stem illicit alcohol flows, giving the security paper market a fresh revenue pipeline in excise applications.

Competitive Landscape

Sector consolidation is reshaping market structure as players chase scale and technology breadth. TOPPAN Security’s June 2025 purchase of dzcard Group doubled its banking-card capacity and extended its personalisation network across Thailand, the Philippines and India. Crane NXT followed by acquiring De La Rue’s Authentication arm for GBP 300 million, signalling investor appetite for high-margin ID and brand-protection assets.

Patent analytics show Chinese firms leading RFID and smart-paper filings, challenging Western incumbents on innovation turf. Incumbents maintain advantage through entrenched central-bank relationships that create switching costs. Yet greenfield opportunities exist in recycled fibres and AI-enhanced watermarks, fields where newcomers can differentiate. While price competition remains limited due to strict qualification cycles, technological race intensity is high, compelling top players to earmark 6-8% of revenue for R&D. Overall, the competitive equilibrium implies mid-level consolidation but ample room for specialist disruptors that focus on adjacent verticals, thereby sustaining a vibrant security paper market.

Security Paper Industry Leaders

Giesecke+Devrient Currency Technology GmbH

Fedrigoni Group

Infinity Security Papers Limited

Ceprohart SA

Drewsen Specialty Papers GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: DREWSEN SPEZIALPAPIERE finalised its acquisition of PORTALS PAPER LTD, expanding its passport-grade product slate.

- February 2025: Crane NXT signed a GBP 300 million deal to purchase De La Rue Authentication Solutions

- June 2025: TOPPAN Security acquired dzcard Group, doubling card capacity across Asia

- January 2025: The Central Bank of Libya issued new polymer notes featuring SPARK Live® ink

Global Security Paper Market Report Scope

Security paper is used in security printing that incorporates features that can be used to identify or authenticate a document as the original. Its various applications include currency, payment cards, and stamps.

| Currency / Banknotes |

| Payment Cards and Cheques |

| ID and Travel Documents |

| Certificates and Ticketing |

| Secure Packaging and Labels |

| Other Application |

| Cotton-fibre Paper |

| Polymer Substrate |

| Hybrid Cotton-Polymer |

| Synthetic Fibres (Abaca, Linen) |

| Recycled-fibre Paper |

| Watermarks |

| Security Threads |

| Holograms and OVD |

| UV/IR Fibres and Dyes |

| RFID/NFC Embedded |

| Micro-printing and Nanotext |

| Colour-shifting Inks |

| Central Banks and Mints |

| Government Document Agencies |

| Secure Printing Houses |

| Commercial Banks |

| Brand-Protection and Packaging Firms |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Application | Currency / Banknotes | ||

| Payment Cards and Cheques | |||

| ID and Travel Documents | |||

| Certificates and Ticketing | |||

| Secure Packaging and Labels | |||

| Other Application | |||

| By Substrate Type | Cotton-fibre Paper | ||

| Polymer Substrate | |||

| Hybrid Cotton-Polymer | |||

| Synthetic Fibres (Abaca, Linen) | |||

| Recycled-fibre Paper | |||

| By Security Feature Integration | Watermarks | ||

| Security Threads | |||

| Holograms and OVD | |||

| UV/IR Fibres and Dyes | |||

| RFID/NFC Embedded | |||

| Micro-printing and Nanotext | |||

| Colour-shifting Inks | |||

| By End User | Central Banks and Mints | ||

| Government Document Agencies | |||

| Secure Printing Houses | |||

| Commercial Banks | |||

| Brand-Protection and Packaging Firms | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the security paper market?

The security paper market size is USD 6.92 billion in 2026, with a forecast to reach USD 8.73 billion by 2031.

Which application segment leads global demand?

Currency and banknotes remain dominant, accounting for 47.78% of 2025 revenue.

Why are polymer substrates gaining ground?

Polymer notes last up to 7.5 years and support advanced security features like transparent windows, reducing lifecycle costs.

How fast is the recycled-fibre segment growing?

Recycled-fibre papers exhibit a 9.05% CAGR through 2031, the fastest rate among substrates.

Page last updated on: