Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

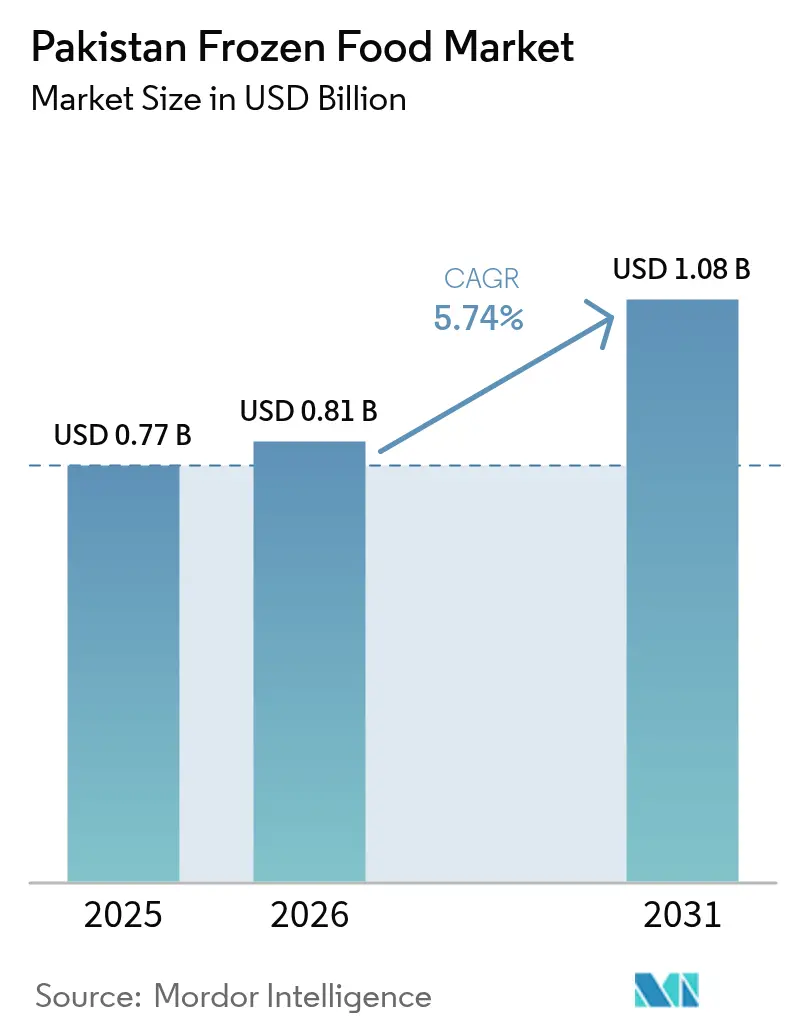

| Base Year Market Size (2025) | USD 0.77 Billion |

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

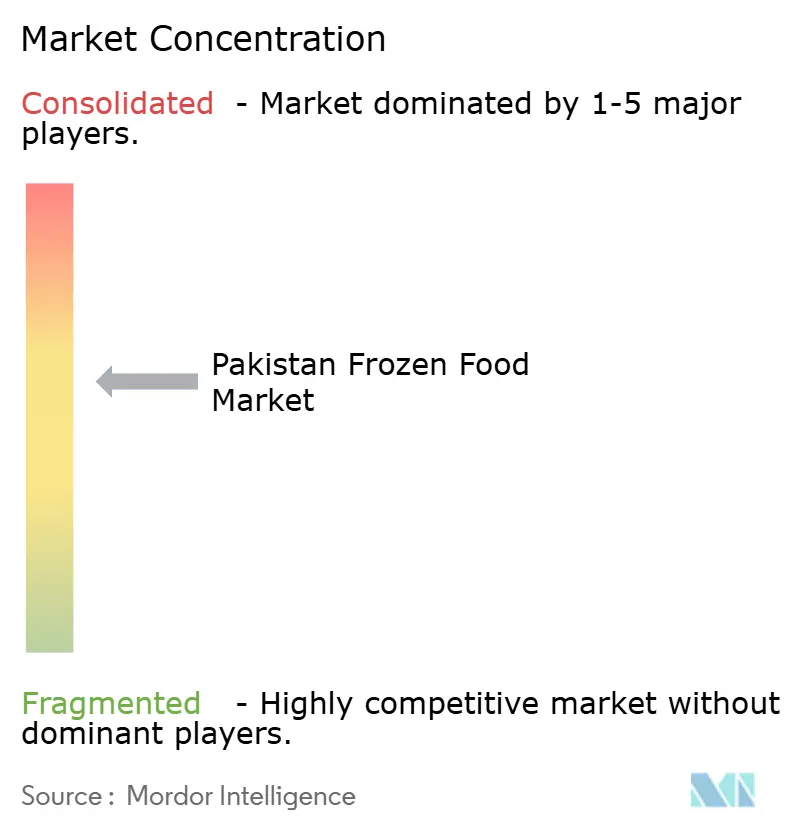

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Frozen Food Market Analysis by Mordor Intelligence

The Pakistan frozen food market size was valued at USD 0.77 billion in 2025 and estimated to grow from USD 0.81 billion in 2026 to reach USD 1.08 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031). Urban incomes are steadily increasing, more women are joining the workforce, and targeted industry incentives are strengthening demand for convenient, halal-certified meal options in major cities. In response, producers are expanding cold-chain infrastructure to reduce logistical losses and extend distribution into rural markets. The adoption of energy-efficient freezing technologies is enabling manufacturers to mitigate the impact of high power costs. At the same time, collaborations such as the partnership between Symrise and Shan Foods illustrate a broader movement toward greater localization of ingredients and packaging, a strategy designed to buffer the industry against currency fluctuations.

Key Report Takeaways

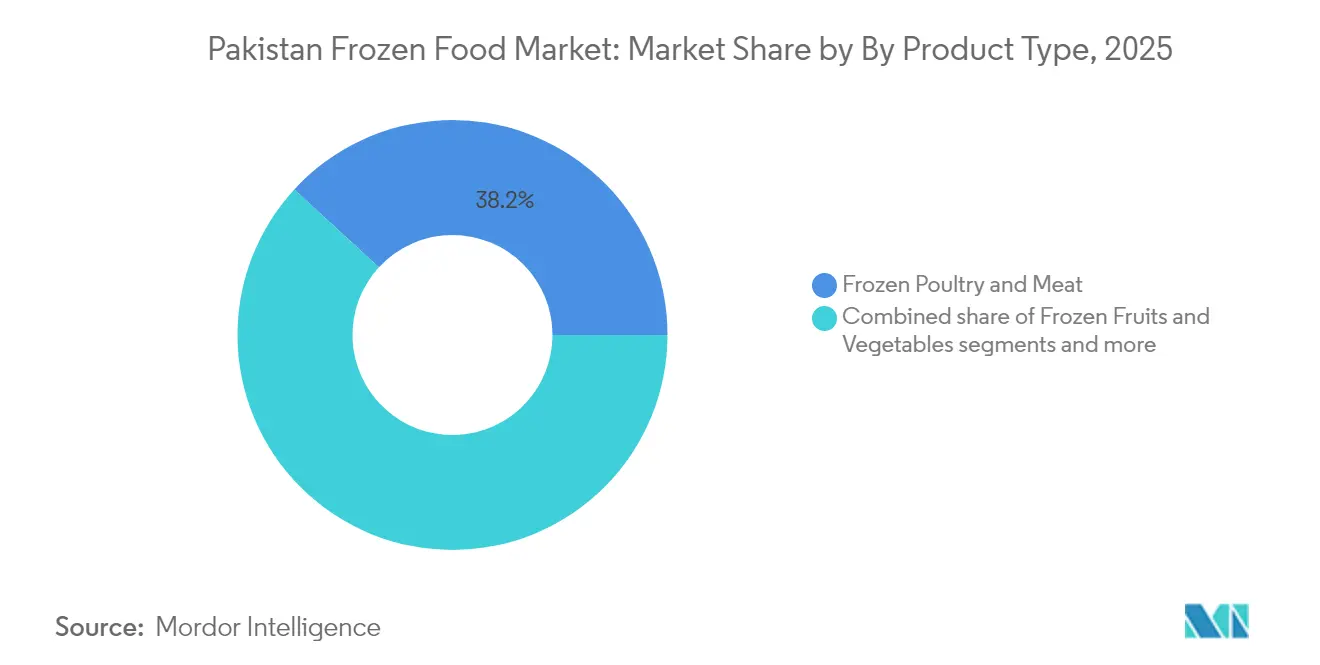

- By product type, frozen poultry and meat led the Pakistan frozen food market with a 38.16% share in 2025; frozen snacks and appetizers are projected to expand at a 7.38% CAGR between 2026 and 2031.

- By product category, ready-to-cook captured 42.63% revenue share in 2025; ready-to-eat is forecast to advance at a 7.72% CAGR through 2031.

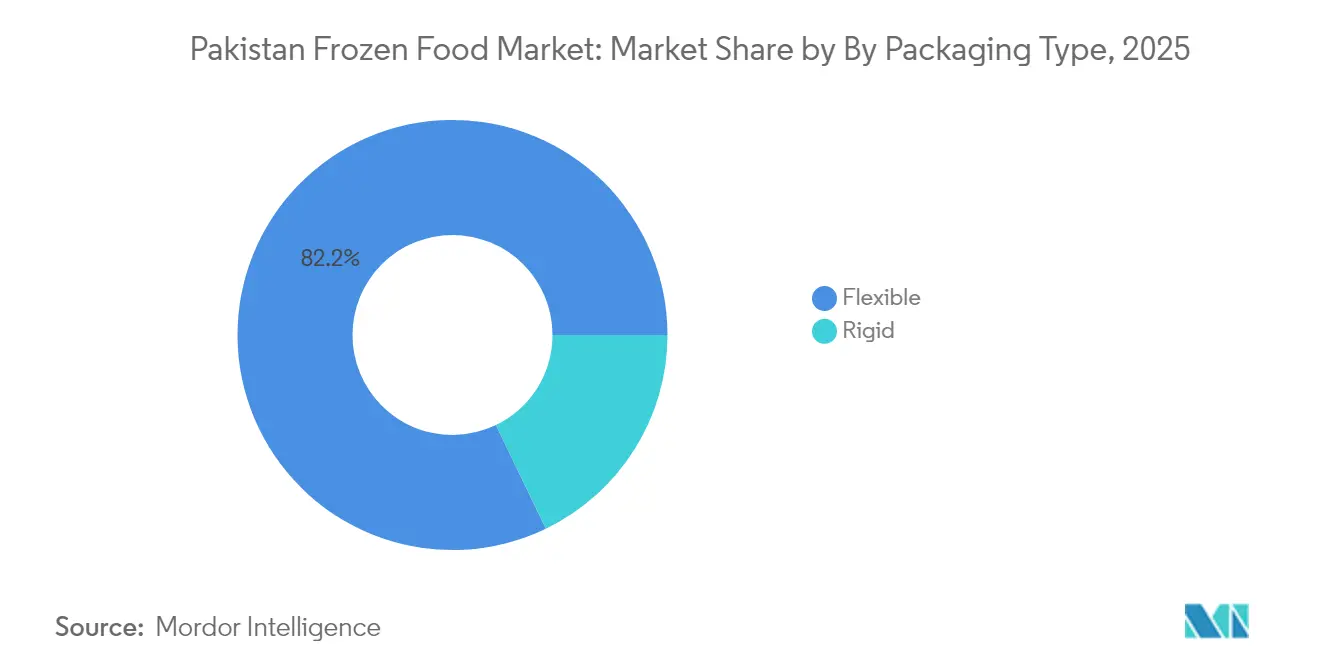

- By packaging type, flexible formats accounted for 82.15% of the revenue in 2025; rigid packaging is expected to rise at a 6.65% CAGR through 2031.

- By distribution channel, on-trade outlets accounted for a 71.78% share of the Pakistan frozen food market size in 2025, while off-trade is expected to grow at a 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation and growing working-women base | +1.2% | Punjab and Sindh cities | Medium term (2-4 years) |

| Cold chain and logistics investments | +0.9% | National industrial corridors | Long term (≥4 years) |

| Expansion of poultry and meat processing | +0.8% | Punjab and Khyber Pakhtunkhwa | Medium term (2-4 years) |

| Religious and halal positioning | +0.6% | Gulf export markets, nationwide Muslim consumers | Long term (≥4 years) |

| Adoption of advanced freezing technologies | +0.4% | Industrial hubs in Punjab and Sindh | Long term (≥4 years) |

| Zero-duty incentives on refrigeration | +0.3% | Manufacturing facilities country-wide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid urbanisation and growing working-women base

Pakistan’s shifting demographic landscape, shaped by rapid urbanization and a growing share of women in the workforce, is fueling a significant rise in demand for convenience foods. With 36.8% of the population residing in urban centers, purchasing power is increasingly concentrated in cities. Larger household sizes, averaging six members, also encourage bulk buying, particularly of frozen items. Moreover, with 57% of the population between the ages of 15 and 64, there is strong momentum toward time-saving food options, as noted by the Pakistan Bureau of Statistics. In major metropolitan areas such as Karachi and Lahore, the growing prevalence of dual-income families, driven in part by working women, has accelerated the shift toward ready-to-cook and ready-to-eat products. These developments are reinforced by a predominantly youthful population entering the labor force and falling fertility rates in rural regions, both of which contribute to changing consumption patterns. Consequently, frozen foods are transitioning from occasional purchases to everyday essentials, reshaping market dynamics across various income groups.

Cold chain and logistics investments

Strategic investments are driving the momentum of infrastructure modernization. Notably, CK Hutchison has unveiled a USD 1 billion port investment aimed at bolstering cold chain capabilities for temperature-sensitive products[1]Source: Reuters, “CK Hutchison plans USD 1 billion port investment in Pakistan,” reuters.com. This investment seeks to bridge significant gaps in Pakistan's cold storage network. The Pakistan Institute of Development Economics highlights a pressing issue: post-harvest losses for perishables in Pakistan hover between 30% and 40%, a consequence of insufficient refrigerated transport and storage facilities. In an effort to counter these challenges, international partnerships are promoting advanced freezing technologies. Companies such as Air Products and OctoFrost are at the forefront, rolling out Individual Quick Freezing (IQF) systems that not only maintain product quality but also prolong shelf life. Public-private partnerships play a pivotal role, harnessing both domestic investments and foreign expertise to drive growth. These infrastructural enhancements are not merely upgrades; they're vital for market expansion. A dependable cold chain network expands the geographic reach beyond urban locales, as outlined in the Strategic Trade Policy Framework.

Expansion of poultry and meat processing

Pakistan's livestock sector is experiencing a significant expansion of its capacity. In the Punjab and Khyber Pakhtunkhwa provinces, key players are investing in state-of-the-art slaughtering and processing facilities, aligning with international benchmarks. While Pakistan proudly stands as the world's fourth-largest milk producer, with only 3% of its production undergoing processing, there's a pronounced potential for value addition, especially in frozen dairy products, as highlighted by the Pakistan Institute of Development Economics. The push for Halal certification is not just a regulatory hurdle; it's catalyzing quality enhancements across the board. Companies are increasingly adopting HACCP-compliant systems, eyeing the Middle Eastern markets. Here, Pakistani food products have carved a niche, thanks to their familiar taste profiles. This surge in processing capacity not only ensures a steady supply of raw materials for frozen foods but also fosters economies of scale, driving down input costs for manufacturers.

Religious and halal positioning

Pakistan's Islamic identity offers a competitive edge in the global halal food market, especially in the Middle East. Here, brands like K&N's have carved out a significant niche[2]Source: FoodNavigator-Asia, “Why Pakistani food finds success in the Middle East,” foodnavigator-asia.com. Halal isn't just about religious adherence for these brands; it's also about ensuring quality and ethical sourcing, values that resonate deeply with Muslim consumers worldwide. Pakistani processors are increasingly adopting the Standards and Metrology Institute for Islamic Countries (SMIIC) certification. They're also investing in traceability systems and third-party audits to uphold halal integrity across the supply chain. This religious positioning not only segments the market but also allows Pakistani frozen food producers to set premium prices internationally. Domestically, they cultivate brand loyalty among consumers who prioritize halal authenticity. As global demand for halal food surges, Pakistani firms, with their genuine religious credentials and competitive manufacturing costs, are well-poised to seize a larger market share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy shortages and high power tariffs | -1.4% | National, acute in industrial zones | Short term (≤ 2 years) |

| Under-developed rural cold-chain infrastructure | -0.8% | Rural areas, particularly Balochistan and remote regions | Long term (≥ 4 years) |

| Fluctuating raw material and import costs | -0.6% | National, import-dependent processors | Medium term (2-4 years) |

| Limited consumer awareness beyond major cities | -0.4% | Secondary cities and rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy shortages and high power tariffs

Pakistan's energy crisis poses a major hurdle to the frozen food sector's growth. Industrial electricity costs hover between 13-15 cents per kilowatt-hour, putting Pakistan at a disadvantage compared to its regional peers. Even with sufficient generation capacity, industrial consumption dipped in fiscal year 2024. This decline is largely due to manufacturers turning to behind-the-meter solar setups and battery storage, aiming to lessen their reliance on the grid. Adding to the energy woes, circular debt issues lead to unreliable supply, pushing frozen food processors to invest in backup generation. Furthermore, power tariff hikes, a move to align with International Monetary Fund loan stipulations, have strained the economics for cold storage and freezing operations, which are notably energy-intensive. In response, the sector is rapidly embracing energy-efficient technologies and renewable systems. However, the substantial capital required for these investments poses a challenge, especially for smaller processors.

Under-developed rural cold-chain infrastructure

According to the Pakistan Bureau of Statistics, 63.2% of Pakistan's population lives outside urban centers, and these rural areas grapple with limited cold storage and refrigerated transport networks. This infrastructure shortfall is especially evident in Balochistan and the remote regions of Khyber Pakhtunkhwa. Here, challenges are exacerbated by restricted electricity access and subpar road connectivity. As a result, rural consumers, who primarily depend on traditional retail channels devoid of refrigeration, find their options limited. They can either choose shelf-stable alternatives or settle for products that have suffered quality degradation due to temperature fluctuations during distribution. The Food and Agriculture Organization (FAO) highlights this issue as a widespread constraint in the Asia-Pacific region. They note that micro, small, and medium food processing enterprises grapple with insufficient infrastructure, hampering their market reach. To bridge this rural infrastructure gap, there's a pressing need for synchronized public-private investments. This includes not just cold storage facilities and refrigerated vehicles, but also a dependable electricity supply. However, this endeavor is a multi-year challenge, limiting immediate market growth beyond urban locales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Meat Dominance Drives Market Structure

In 2025, Frozen Poultry and Meat products capture a 38.16% market share, underscoring the strength of Pakistan's livestock sector and the robust processing capabilities in its Punjab and Khyber Pakhtunkhwa provinces. This segment enjoys a boost, with meat and its preparations showcasing a competitive edge on the global stage. Meanwhile, Frozen Snacks and Appetisers are the standout performers, projected to grow at a 7.38% CAGR through 2031. This surge is largely attributed to urbanization and a shift in consumption habits, especially among the younger generation that values convenience and variety. Frozen Fruits and Vegetables, on the other hand, enjoy consistent demand.

Frozen Seafood grapples with supply chain hurdles, primarily due to a constrained coastal processing capacity. In contrast, Frozen-Cooked Ready Meals are carving out a niche as a premium offering, appealing to urban households with more disposable income. The sweltering climate and the rising penetration of modern retail in major cities have given Frozen Desserts and ice cream a significant boost. These segment dynamics not only highlight the evolving food landscape but also mirror broader economic shifts. While protein-based products continue to lead, categories centered around convenience are witnessing a rapid ascent. This trend aligns with the changing household structures, notably the rise of dual-income families seeking time-saving culinary solutions.

By Product Category: Ready-to-Cook Leads Market Evolution

In 2025, the Ready-to-Cook segment commands a 42.63% market share, resonating with the traditional Pakistani emphasis on ingredient control and authentic flavors. Decades of domestic food production have honed expertise in processing and established robust supply chains for raw materials. Meanwhile, Ready-to-Eat products are surging, boasting a 7.72% CAGR through 2031. This growth mirrors a shift in urban lifestyles, especially among professionals and working women, who now favor convenience over time-intensive cooking. Such a disparity in growth rates underscores a broader transformation in consumption habits, driven by rapid urbanization and tightening household schedules.

Highlighting this evolution, the Symrise-Shan Foods collaboration inaugurated a facility in September 2024, focusing on seasonings, bouillons, processed meats, and snacks. Their aim is to meld traditional flavors with contemporary convenience. Beyond these, other categories are emerging, featuring specialty items like ethnic frozen foods and products tailored for specific dietary needs, catering to niche markets. This segmentation underscores Pakistan's balancing act: honoring its rich culinary heritage while adapting to modern demands. Successful products are those that marry authentic taste with ease of preparation, appealing to a broad demographic spectrum.

By Packaging Type: Flexible Formats Optimize Cost and Convenience

In 2025, flexible packaging formats, including pouches and flow-wrap materials, account for a dominant 82.15% market share. This trend is largely driven by cost optimization and a focus on consumer convenience in a price-sensitive market. Households, especially those with an average of six members, are gravitating towards bulk purchases and easy storage solutions. Meanwhile, rigid packaging formats, such as trays and boxes, are experiencing a robust growth rate of 6.65% CAGR, driven by a push for premium product positioning and the evolving demands of modern retail for enhanced shelf presentation and product differentiation.

Technological advancements in barrier films and sealing technologies have revolutionized the packaging industry. These innovations not only extend shelf life but also reduce material costs, enabling competitive pricing that is crucial for market penetration. The rise of rigid packaging underscores a shift in the market towards premium categories. Here, urban consumers, often willing to pay a premium, prioritize presentation and perceived quality, seeking brand differentiation and convenience. Overall, the evolving packaging landscape signals a maturing market, with consumers diversifying their preferences across price and convenience.

By Distribution Channel: On-Trade Dominance Signals Market Maturity

In 2025, On-Trade channels dominate with a 71.78% market share, underscoring the sector's dependence on food service establishments, institutional buyers, and bulk purchasers who prioritize consistent supply and competitive pricing. This trend is influenced by Pakistan's average household size of 6 members, as highlighted by the Pakistan Bureau of Statistics. Such household dynamics make bulk purchasing through restaurants, catering services, and institutional channels a cost-effective strategy. Meanwhile, Off-Trade channels are on a growth trajectory, expanding at a 6.82% CAGR through 2031. This surge is fueled by the rise of modern retail and the increasing adoption of e-commerce in urban areas, where there's a notable uptick in consumers purchasing frozen foods for home use.

In the Off-Trade landscape, Supermarkets and Hypermarkets take the lead in retail penetration. However, Online Stores are emerging as the fastest-growing segment, buoyed by advancements in digital payment systems and enhanced cold chain delivery. While Convenience Stores are making headway in urban locales, their frozen food selections are hampered by refrigeration limitations. This shift in distribution channels mirrors the broader modernization of retail in Pakistan. Traditional wholesale markets are increasingly being supplemented by organized retail formats, which offer superior cold storage and added consumer convenience. Yet, this evolution is predominantly seen in major urban hubs.

Geography Analysis

Punjab province, home to major urban centers like Lahore and Faisalabad, leads Pakistan's frozen food market. Its dominance stems from a robust food processing infrastructure and higher per capita incomes. Sindh, bolstered by Karachi's population exceeding 15 million, stands as the second-largest market. Karachi, being Pakistan's primary port, enhances Sindh's strong import capabilities. Furthermore, with industrial growth and rising urbanization, Sindh witnesses a surge in convenience food adoption, especially among working professionals and dual-income households. Meanwhile, Khyber Pakhtunkhwa, with its agricultural prowess and proximity to Afghan trade routes, shows promise. However, its market development grapples with security issues and infrastructure challenges, particularly in ensuring cold chain reliability.

Balochistan faces hurdles in the frozen food market. Its sparse population density, limited electricity access, and underdeveloped transport networks hinder distribution beyond provincial capitals. While the coastal regions present seafood processing potential, these opportunities remain largely dormant due to infrastructural deficits and a lack of modern processing facility investments. Economic disparities are evident: urban hubs in Punjab and Sindh propel market growth, whereas rural areas across provinces lag in frozen food adoption, hindered by traditional preferences, purchasing power limitations, and insufficient cold chain infrastructure.

Geographic insights spotlight avenues for market growth, emphasizing the need for infrastructure enhancements and optimized distribution networks. A case in point is CK Hutchison's USD 1 billion port investment in Sindh, poised to bolster logistics and streamline frozen food trade. Regional strategies must be nuanced, considering cultural nuances, income disparities, and infrastructural strengths. A phased approach is vital: prioritize urban centers with high potential, then gradually expand to secondary cities and rural locales, tailoring product offerings and distribution methods accordingly.

Competitive Landscape

Established domestic players in Pakistan's frozen food market leverage local market insights, robust distribution networks, and cost-efficient operations, leading to a moderately concentrated landscape. K&N's stands out with a diverse portfolio that includes frozen meats, ready-to-eat meals, and snacks, bolstered by strong brand recognition and a wide retail footprint. Companies with integrated supply chains, overseeing everything from raw material sourcing to distribution, are better positioned to navigate challenges like rising energy tariffs and currency fluctuations.

Strategic alliances are redefining the competitive landscape. A prime example is the partnership between Symrise and Shan Foods, merging global technology with local insights to hasten product development and lessen reliance on imports. Companies are increasingly turning to technology for enhanced operational efficiency, evident in their investments in Individual Quick Freezing (IQF) systems and automated packaging lines, which boost product quality and trim labor costs.

There are untapped opportunities in premium frozen food segments, deeper penetration into rural markets. Pakistani firms can capitalize on halal certifications and genuine flavor profiles. The competitive scene mirrors broader industrial goals, emphasizing import substitution and export diversification. To thrive, companies must excel in quality management, adhere to regulatory standards, and optimize their supply chains, all while navigating energy challenges and seizing the rising domestic and global appetite for Pakistani frozen foods.

Pakistan Frozen Food Industry Leaders

PK Meat & Food Company

Dawn Frozen Foods

Sabroso

Al-Shaheer Corporation (Meat One)

K&N’s

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: CK Hutchison announced a USD 1 billion port investment in Pakistan that will significantly enhance cold chain infrastructure and logistics capabilities for frozen food imports and exports, addressing critical supply chain bottlenecks that have constrained market growth.

- September 2024: Symrise and Shan Foods inaugurated a state-of-the-art powder blending production facility in Pakistan, marking Symrise's first manufacturing presence in the country and targeting local production of seasonings, bouillons, processed meat, and snacks to reduce import dependence.

- April 2024: Saudi Arabia is committed to expediting USD 5 billion of initial investments in Pakistan under the Special Investment Facilitation Council framework, potentially including food processing and agricultural sectors that could benefit frozen food infrastructure development.

Pakistan Frozen Food Market Report Scope

Frozen food refers to any type of food that has been subjected to a freezing process to preserve it. Freezing food involves reducing its temperature to below its freezing point, which inhibits the growth of bacteria, yeasts, and molds that can cause food spoilage. Frozen food can include a wide variety of items, such as fruits, vegetables, meats, seafood, and prepared meals.

The frozen food market is segmented by category into ready-to-eat, ready-to-cook, ready-to-drink, and other frozen food types; by type into frozen fruits and vegetables, frozen meat and fish, frozen-cooked ready meals, frozen desserts, frozen snacks, and other applications; by freezing technique into individual quick freezing (IQF), blast freezing, belt freezing, and other freezing techniques; and by distribution channel into supermarkets and hypermarkets, convenience stores, online channels, and other distribution channels.

The report offers market size and forecasts in value (USD million) for all the above segments.

By Product Type

| Frozen Fruits and Vegetables |

| Frozen Meat and Poultry |

| Frozen Seafood |

| Frozen-Cooked Ready Meals |

| Frozen Snacks and Appetisers |

| Frozen Desserts and Ice-cream |

| Other Product Types |

By Product Category

| Ready-to-Eat |

| Ready-to-Cook |

| Other Categories |

By Packaging Type

| Flexible (Pouches, Flow-wrap) |

| Rigid (Trays, Boxes) |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Channels |

| By Product Type | Frozen Fruits and Vegetables | |

| Frozen Meat and Poultry | ||

| Frozen Seafood | ||

| Frozen-Cooked Ready Meals | ||

| Frozen Snacks and Appetisers | ||

| Frozen Desserts and Ice-cream | ||

| Other Product Types | ||

| By Product Category | Ready-to-Eat | |

| Ready-to-Cook | ||

| Other Categories | ||

| By Packaging Type | Flexible (Pouches, Flow-wrap) | |

| Rigid (Trays, Boxes) | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Channels | ||

Key Questions Answered in the Report

How large is the Pakistan frozen food market in 2026?

It is valued at USD 0.81 billion and is projected to grow at a 5.74% CAGR through 2031.

Which product type holds the largest share?

Frozen poultry and meat commands 38.16% of 2025 sales due to established livestock supply chains.

What is driving the fast growth of ready-to-eat meals?

Busier urban lifestyles and rising microwave ownership are fueling a 7.72% CAGR for ready-to-eat packs.

Which regions offer the best expansion prospects?

Punjab and Sindh remain priority hubs, but secondary cities in Khyber Pakhtunkhwa are emerging as new demand centers as cold-chain coverage improves.

Page last updated on: