Semaglutide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

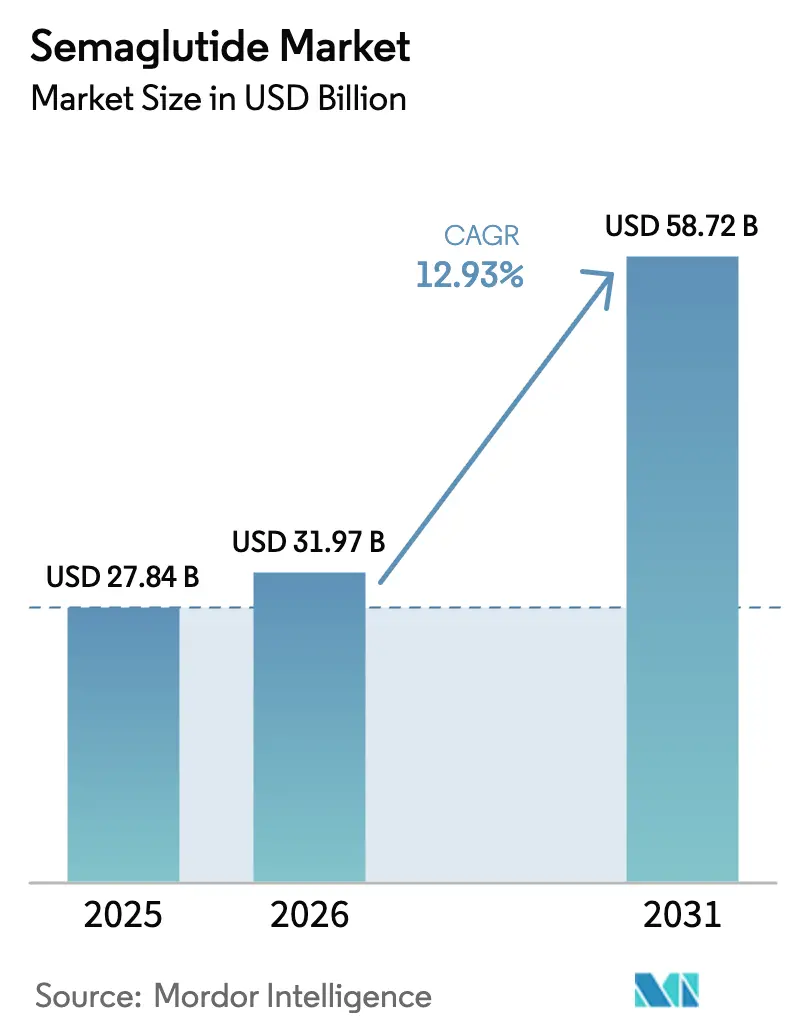

| Market Size (2026) | USD 31.97 Billion |

| Market Size (2031) | USD 58.72 Billion |

| Growth Rate (2026 - 2031) | 12.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Semaglutide Market Analysis by Mordor Intelligence

The Semaglutide Market size was valued at USD 27.84 billion in 2025 and is estimated to grow from USD 31.97 billion in 2026 to reach USD 58.72 billion by 2031, at a CAGR of 12.93% during the forecast period (2026-2031).

This growth reflects a strategic shift from single-disease glucose control to integrated cardiometabolic management, anchored by broader payer coverage for cardiovascular risk reduction, employer-sponsored weight management programs, and real-world adherence data that favor once-weekly dosing. North America remains the revenue anchor, yet accelerated approvals in Europe and Asia-Pacific are widening geographic demand. Clinician adoption is rising as cardiology and endocrinology societies embed GLP-1 receptor agonists into secondary-prevention algorithms, while contract manufacturers race to alleviate pen-fill bottlenecks. Competitive intensity is intensifying as Eli Lilly’s tirzepatide prompts Novo Nordisk to expand its oral formulations and dose strengths, thereby heightening the focus on manufacturing scale, supply security, and patient-centric delivery formats.

Key Report Takeaways

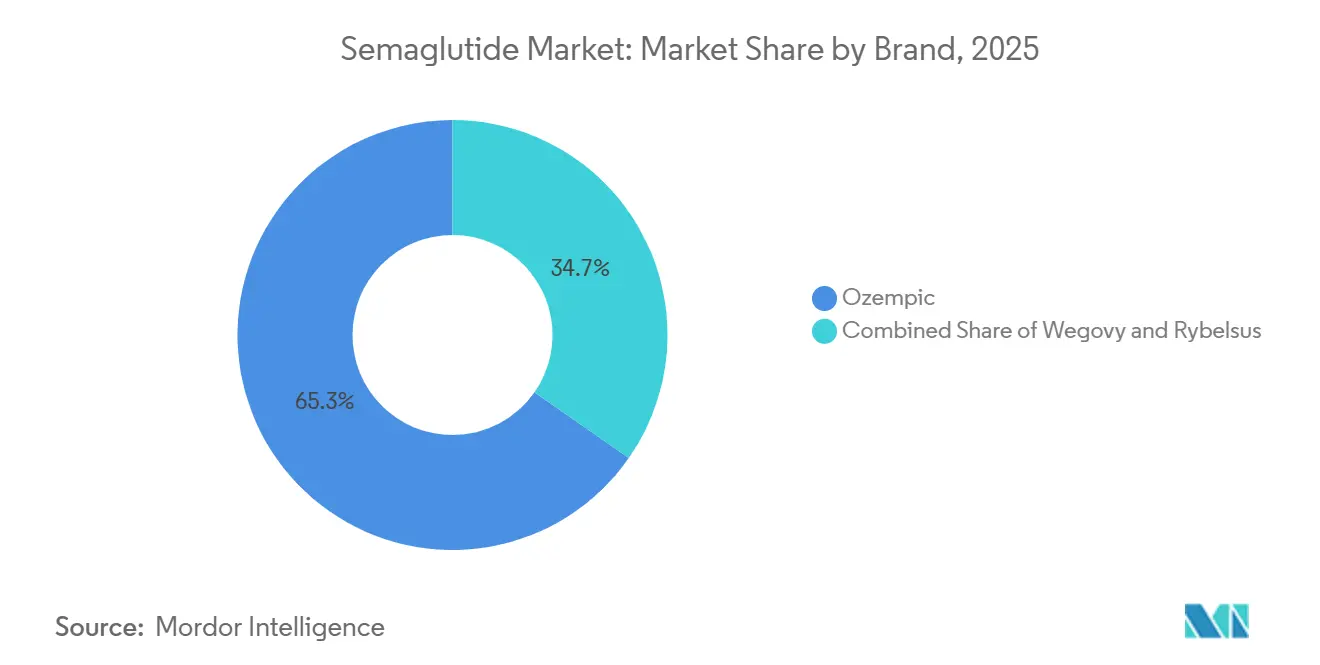

- By brand, the Ozempic segment led with a 65.31% share of the semaglutide market in 2025; Wegovy is forecast to expand at a 15.13% CAGR through 2031.

- By formulation, the injectable segment led with a 59.73% share of the semaglutide market in 2025; oral is forecast to expand at a 16.87% CAGR through 2031.

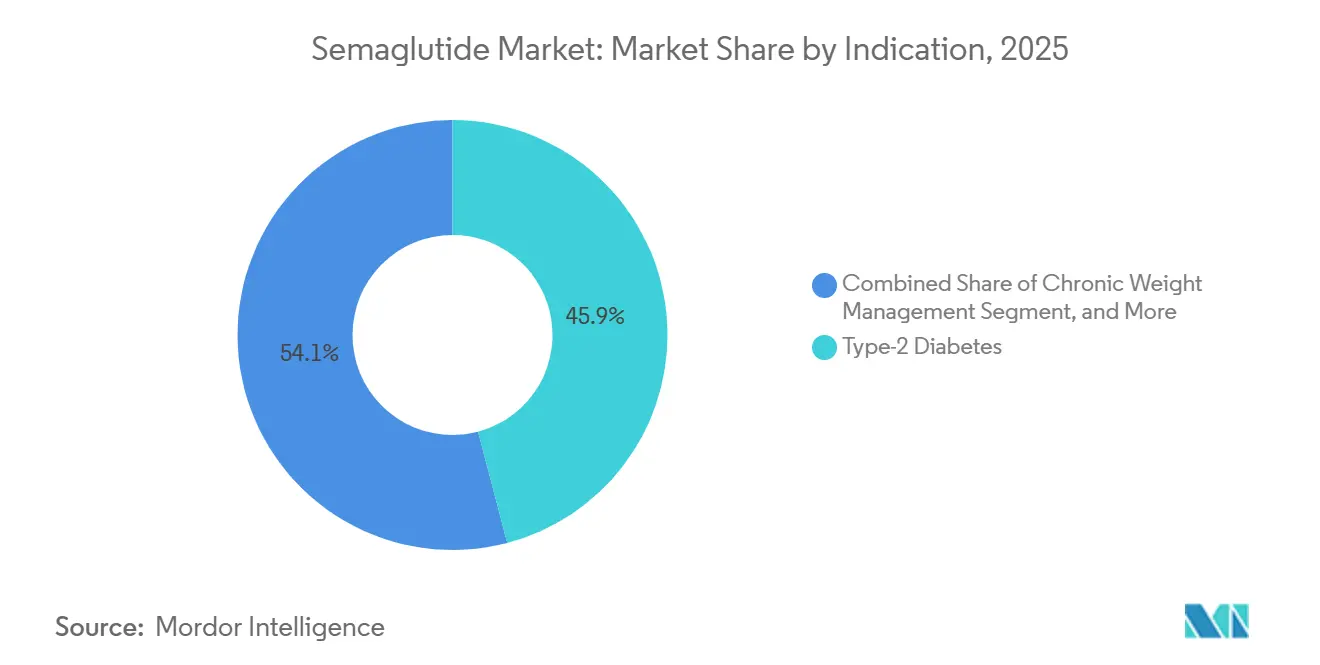

- By indication, type 2 diabetes accounted for 45.88% of the semaglutide market size in 2025, while cardiovascular risk reduction is projected to advance at a 13.23% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 65.36% of 2025 revenue; online pharmacies are projected to record the highest CAGR of 14.35% from 2026 to 2031.

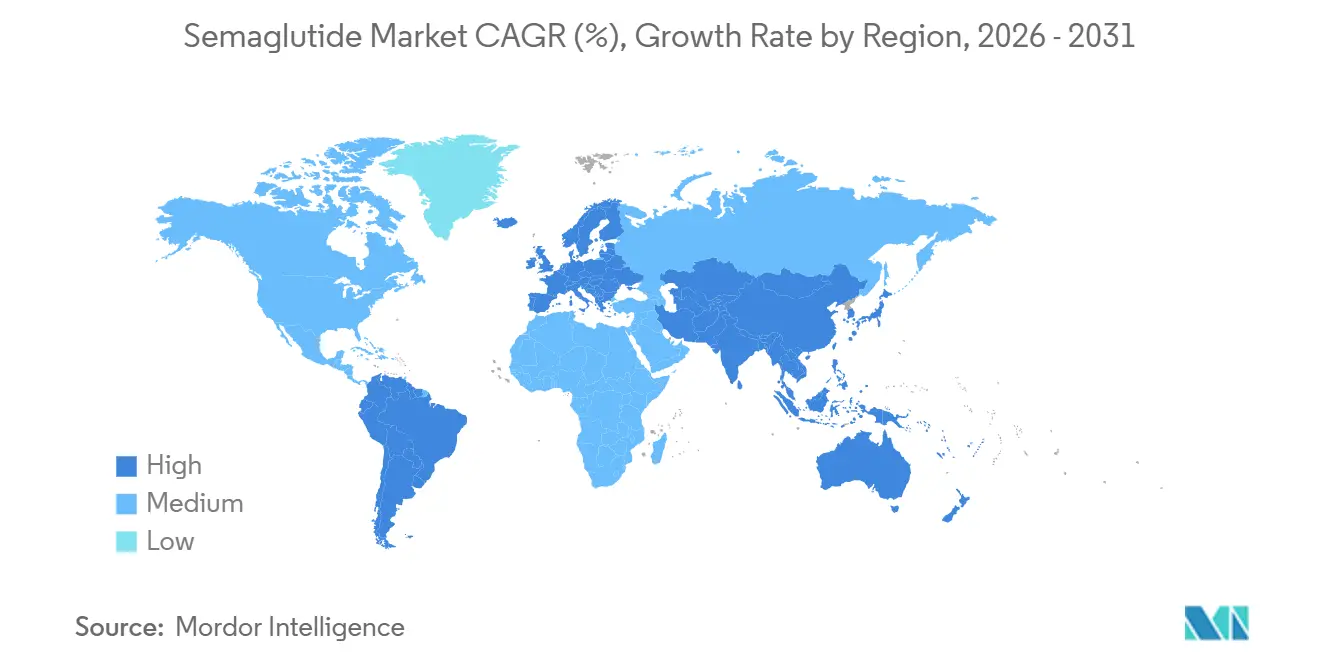

- By geography, North America accounted for 46.38% of the 2025 revenue, while the Asia-Pacific region is the fastest-growing, with a 17.12% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Semaglutide Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity & type-2 diabetes | +2.8% | Global, highest in North America, Middle East, Pacific Islands | Long term (≥ 4 years) |

| Superior weight-loss efficacy versus other GLP-1 RAs | +2.1% | North America and Europe | Medium term (2–4 years) |

| Expanded regulatory approvals for CVD risk reduction | +3.2% | North America and Europe, spillover to Asia-Pacific | Medium term (2–4 years) |

| Growing adoption of self-injectable pens & oral tablets | +1.5% | Global, faster uptake in high-income markets | Short term (≤ 2 years) |

| Employer-sponsored obesity-management programs | +1.9% | North America, select European markets | Short term (≤ 2 years) |

| API supply-chain localization incentives in Asia | +1.4% | China, India, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity & Type-2 Diabetes

Global obesity surpassed 1 billion adults in 2024, while 537 million people lived with diabetes, creating fundamental demand for therapies that address both conditions.[1]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” diabetesatlas.org Middle Eastern ministries included GLP-1 agonists on essential medicines lists in 2025, signaling a policy-level acceleration of demand. Asia-Pacific health agencies report earlier onset of diabetes, with China noting that 35% of new diagnoses now occur in adults under 45 years. Working-age populations favor once-weekly injections over daily pills, reinforcing uptake. The interplay between rising disease burden and patient convenience is thus central to the expansion of the semaglutide market.

Superior Weight-Loss Efficacy Versus Other GLP-1 RAs

Wegovy achieved a 15.8% mean weight loss in the STEP 1 trial, whereas tirzepatide posted a 22.5% mean weight loss, prompting U.S. payers to tier formularies by patient profile. European cost-effectiveness bodies updated modeling frameworks in 2025 to credit cardiovascular benefit, tilting decisions toward semaglutide for secondary prevention.[2]National Institute for Health and Care Excellence, “Semaglutide for Managing Overweight and Obesity,” nice.org.uk Novo Nordisk is currently testing 25 mg and 50 mg oral doses to close the efficacy gap without injections, with Phase III readouts expected in late 2026.

Expanded Regulatory Approvals for CVD Risk Reduction

The FDA cleared Wegovy’s cardiovascular label in March 2024, following the publication of the SELECT trial results, which showed a 20% relative risk reduction in major adverse cardiovascular events.[3]Food and Drug Administration, “FDA Approves First Treatment to Reduce Risk of Serious Heart Problems,” fda.gov The EMA followed in June 2024, Canada in September 2024, and South Korea in December 2025, creating synchronized access in high-income markets. Japan’s priority review is slated to conclude by mid-2026, extending the semaglutide market into national insurance coverage.

Growing Adoption of Self-Injectable Pens & Oral Tablets

Pre-filled FlexTouch pens achieve 12-month adherence rates of above 70%, compared to 50–60% for daily oral medications. Oral semaglutide holds an 8% prescription share yet covers needle-averse cohorts. Surveys show that 42% of patients would switch to oral therapy if its efficacy matched that of injectables, underscoring the need for trials of higher-dose tablets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & limited reimbursement | –1.8% | Middle-income markets, pressure also in high-income formularies | Medium term (2–4 years) |

| Supply shortages of pen-fill & cartridge capacity | –1.2% | North America and Europe | Short term (≤ 2 years) |

| GI side effects driving real-world discontinuations | –0.9% | Global, higher where dietitian support is sparse | Short term (≤ 2 years) |

| Regulatory scrutiny of off-label cosmetic use | –0.6% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Limited Reimbursement

Semaglutide ranked among the costliest chronic therapies in obesity care, at USD 1,300 per month in 2025. Brazil, Mexico, South Africa, and Turkey declined reimbursement, citing budget-impact models showing 5-8% of drug spending would shift to a single product. Even in high-income markets, prior-authorization delays average six weeks, which can dampen initiation. Tiered pricing and patient-assistance programs have yet to impact uptake in price-sensitive geographies significantly.

Supply Shortages of Pen-Fill & Cartridge Capacity

Novo Nordisk flagged pen-fill lines as the bottleneck in 2024, despite a USD 2 billion capacity expansion; validation of aseptic filling lines extends 18–24 months. Spot shortages fostered gray-market imports, prompting FDA import alerts in 2025. Supply normalization is expected by late 2026 as new lines and vertically integrated assets come online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Brand: Ozempic’s Diabetes Franchise Anchors Revenue While Wegovy Captures Obesity Growth

Ozempic held a 65.31% brand share in 2025, underpinned by its 2017 launch and subsequent inclusion in cardiometabolic guidelines following the SUSTAIN-6 study, which showed a 26% reduction in cardiovascular events. Wegovy is advancing at a 15.13% CAGR through 2031 as expanded labels unlock broader payer coverage. The semaglutide market size for cardiovascular risk reduction is therefore scaling rapidly, enabling Novo Nordisk to segment indications and optimize lifecycle revenue. Rybelsus, the oral variant, serves injection-averse patients and is positioned to gain share pending higher-dose approvals.

Competitive pressure from tirzepatide is prompting Novo Nordisk to accelerate oral dose escalation and explore combination regimens with amylin analogs. Brand-level negotiations vary by budget silo, with Ozempic reimbursed under diabetes spend and Wegovy under obesity or preventive care, granting the innovator flexibility to shift promotional focus. This multi-brand strategy stabilizes revenue even as individual formularies shift volume between indications.

By Formulation: Injectable Pens Dominate While Oral Tablets Target Injection-Averse Cohorts

Injectable pens accounted for 59.73% of 2025 revenue and are forecast to grow at a 16.87% CAGR, as once-weekly dosing sustains 72% 12-month adherence. Oral tablets currently hold the balance; they exploit SNAC technology protected by patents through 2032, temporarily insulating against generic erosion. If ongoing Phase III trials validate the 25 mg and 50 mg doses, the oral segment’s semaglutide market share is likely to increase, particularly in primary care channels.

Manufacturing economics differ: oral bioavailability below 1% drives up API usage and cost, whereas injectables concentrate demand on pen-fill capacity. Innovation across delivery devices, including auto-injectors with integrated sharps disposal, is expected to sustain injectable preference despite gains in oral administration. The semaglutide industry is therefore investing on both fronts to meet heterogeneous patient preferences.

By Indication: Cardiovascular Risk Reduction Emerges as Fastest-Growing Segment

Type 2 diabetes retained a 45.88% revenue share in 2025; however, cardiovascular risk reduction is expanding at a 13.23% CAGR, the fastest among all indications. The incorporation of GLP-1 therapy into cardiology guidelines encourages the initiation of GLP-1 therapy in secondary prevention regimens, thereby boosting the semaglutide market. Chronic weight management remains sizable, supported by employer programs and increasing social acceptance that obesity is a chronic disease requiring pharmacotherapy.

“Other” investigational uses, such as non-alcoholic steatohepatitis, offer pipeline upside but currently contribute marginal revenue. Payers are tightening prior-authorization criteria to curb off-label prescribing, helping preserve budget predictability. Over the forecast period, cardiovascular indications are expected to significantly expand the semaglutide market size by capturing high-risk patients with elevated baseline costs.

By Distribution Channel: Hospital Pharmacies Retain Majority Share as Online Platforms Scale

Hospital pharmacies dispensed 65.36% of 2025 volumes due to initiation during inpatient cardiometabolic events. Retail chains handle routine refills but face prior-authorization hurdles that extend dispensing timelines. Online pharmacies are advancing at a 14.35% CAGR, driven by telehealth integration, discreet home delivery, and bundled coaching programs. New FDA guidance now requires synchronous video consultation before prescribing, raising compliance costs yet not halting digital uptake.

For manufacturers, online channels present higher gross-to-net spreads due to direct contracting, creating incremental margin opportunity. The semaglutide industry is thus partnering with telehealth platforms to secure future share and patient engagement data.

Geography Analysis

North America generated 46.38% of global revenue in 2025, driven by extensive employer coverage and the inclusion of Medicare Part D for diabetes, as well as the growth of cardiovascular indications. U.S. adult obesity prevalence reached 41.9% in 2024, sustaining high demand. Canada added the cardiovascular label in 2024, and provincial formularies followed by mid-2025, expanding patient eligibility. Mexico remains largely private pay due to limited public reimbursement, moderating uptake.

Europe exhibits broad albeit patchy reimbursement. Germany’s IQWiG recognized considerable additional benefit for cardiovascular prevention in 2025, enabling premium pricing. The UK’s NICE recommended semaglutide for adults with established CVD and BMI ≥ 27 kg/m² in March 2025, opening NHS access to more than 1 million patients. France and Italy await real-world evidence before finalizing budgets, while Spain completed formulary inclusion in late 2025. Aging demographics and high cardiovascular burden underpin continued growth.

The Asia-Pacific region posts the strongest growth at a 17.12% CAGR. China approved the obesity indication in late 2024 and targets essential-medicine reimbursement in 2026, amplified by domestic API production scaling. Japan’s anticipated mid-2026 cardiovascular approval will unlock national insurance coverage, while South Korea’s December 2025 label extension makes it the regional trailblazer. India’s market is currently cash-based, yet biosimilar initiatives by Dr. Reddy’s and Gland Pharma aim to widen affordability post-2031 patent expiries. Australia reimburses Wegovy under the Pharmaceutical Benefits Scheme but enforces strict prior-authorization criteria.

The Middle East & Africa and South America together hold smaller shares but exhibit double-digit growth. Gulf Cooperation Council states added semaglutide to formularies in 2024-2025, although high list prices restrict access to insured populations. Brazil rejected public reimbursement in 2024, yet private demand persists in major urban centers. Over time, the expansion of middle classes and evolving reimbursement policies are expected to unlock incremental volume.

Competitive Landscape

Novo Nordisk maintains its leading position through Ozempic, Wegovy, and Rybelsus; however, Eli Lilly’s tirzepatide products are shifting the semaglutide market toward a duopoly. Both firms are investing billions in manufacturing capacity; Novo Nordisk’s USD 11 billion purchase of Catalent facilities in 2024 signals vertical integration aimed at securing pen-fill output. Contract manufacturers such as Bachem, PolyPeptide Group, and WuXi AppTec are scaling peptide output, fragmenting supply lines, and introducing more geographic resilience.

Emergent players include Hybio and Zhejiang Jiuzhou in China and SG Biopharm in South Korea, each leveraging localization incentives to sign offtake contracts with Western brand owners. Indian companies, including Dr. Reddy’s, Sun Pharma, Gland Pharma, and Torrent, are developing biosimilar pipelines timed to coincide with post-2031 patent cliffs. Regulatory uncertainty persists, as the FDA has yet to finalize its guidance on GLP-1 biosimilars, creating a timing risk for follow-on entrants. Innovation opportunities span oral bioavailability enhancers, ultra-long-acting injectables that may halve injection frequency, and fixed-dose combinations pairing semaglutide with SGLT-2 inhibitors or amylin analogs.

Semaglutide Industry Leaders

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Canada authorized a generic version of Ozempic, marking the first regulatory approval for a semaglutide follow-on in a significant market. Pharmacies await supply, yet the approval signals future price competition and broader access.

- December 2025: Ajanta Pharma inked a supply and marketing deal with Biocon, granting exclusive rights across 23 emerging markets and semi-exclusive rights in three more, strengthening Ajanta’s footprint in metabolic care.

- December 2025: Emcure Pharmaceuticals launched Poviztra, a semaglutide-based weight-loss therapy, at USD 106 (INR 8,790) per month, becoming the first Indian company to commercialize Novo Nordisk’s molecule for obesity.

- November 2025: Novo Nordisk partnered with Emcure to expand GLP-1 distribution across India, leveraging Emcure’s national network for increased penetration of obesity care.

Global Semaglutide Market Report Scope

Semaglutide is an antidiabetic medication used for the treatment of type 2 diabetes and an anti-obesity medication used for long-term weight management. The semaglutide market is segmented by brands and geography. By brands, the market is segmented into Ozempic, Wegovy, and Rybelsus. The report also covers the market sizes and forecast for the semaglutide market in major countries across different regions. For each segment, the market size is provided in terms of value (USD) and volume (units).

| Wegovy |

| Ozempic |

| Rybelsus |

| Injectable |

| Oral |

| Type-2 Diabetes |

| Chronic Weight Management |

| Cardiovascular Risk Reduction |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Brand | Wegovy | |

| Ozempic | ||

| Rybelsus | ||

| By Formulation | Injectable | |

| Oral | ||

| By Indication | Type-2 Diabetes | |

| Chronic Weight Management | ||

| Cardiovascular Risk Reduction | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size of the semaglutide market by 2031?

The semaglutide market size is projected to reach USD 58.72 billion by 2031, reflecting a 12.93% CAGR from 2026.

Which indication is growing fastest for semaglutide products?

Cardiovascular risk reduction drives growth at a 13.23% CAGR as payers recognize its role in secondary prevention.

Why are injectable formulations still dominant despite oral options?

Once-weekly injectable pens deliver higher adherence and steady pharmacokinetics, sustaining 59.73% revenue share in 2025.

What regions present the highest growth potential?

The Asia-Pacific region shows the fastest trajectory, with a 17.12% CAGR, driven by regulatory acceleration and local API production.

How are employers influencing demand in the United States?

Employer-sponsored plans covered weight-management drugs for 44% of insured lives by mid-2025, expanding access and volume.

Page last updated on: