Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

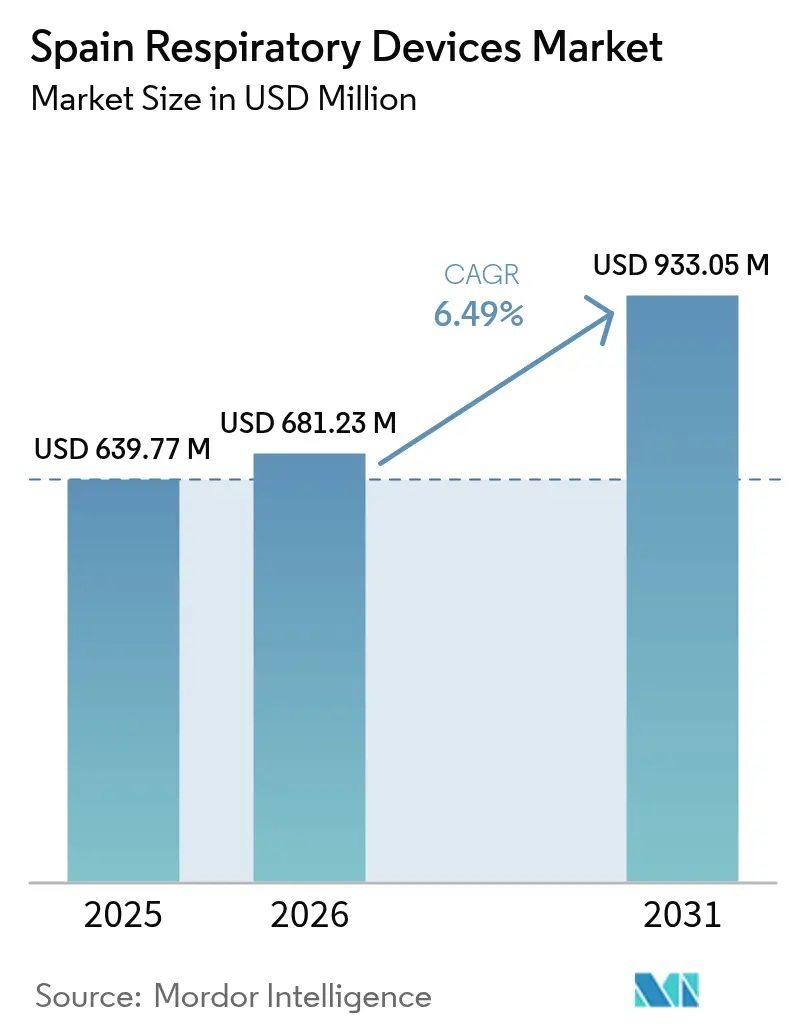

| Base Year Market Size (2025) | USD 639.77 Million |

| Market Size (2026) | USD 681.23 Million |

| Market Size (2031) | USD 933.05 Million |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

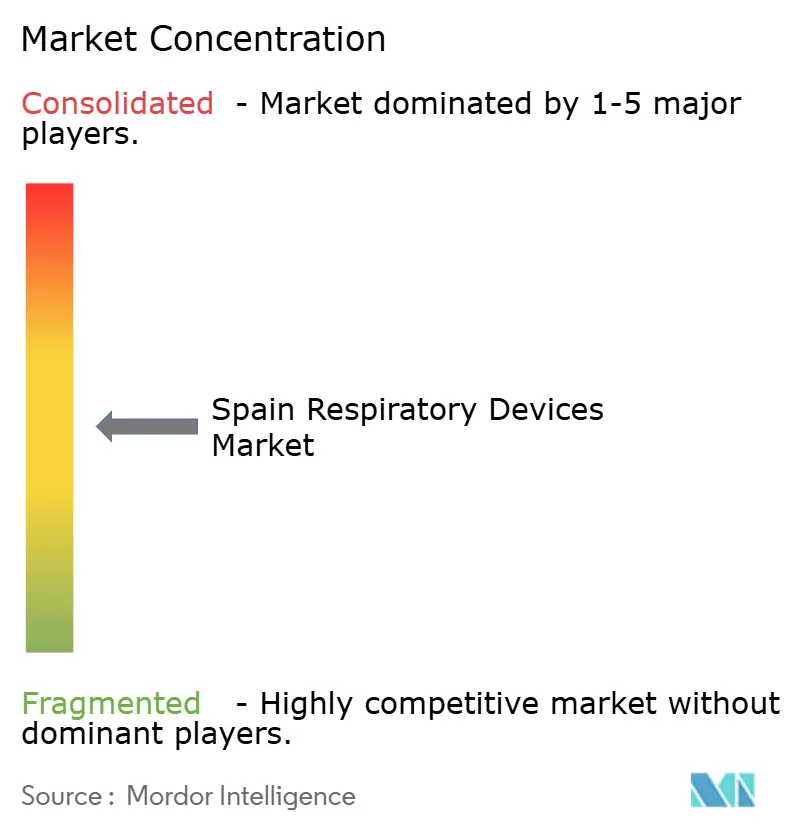

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Respiratory Devices Market Analysis by Mordor Intelligence

The Spain Respiratory Devices Market size was valued at USD 639.77 million in 2025 and estimated to grow from USD 681.23 million in 2026 to reach USD 933.05 million by 2031, at a CAGR of 6.49% during the forecast period (2026-2031). Robust public health coverage, the rapid expansion of home-based care, and continuous innovation in therapeutic equipment underpin this trajectory. Accelerated population ageing intensifies demand for ventilators and oxygen systems, while a growing burden of chronic obstructive pulmonary disease (COPD) and sleep apnea broadens the addressable patient pool. Government incentives that promote local manufacturing and digital health adoption further support revenue growth. At the same time, heightened regulatory costs, workforce shortages, and stricter environmental rules temper short-term momentum yet encourage scale advantages for established suppliers.

Key Report Takeaways

- By product type, therapeutic devices led with 56.14% revenue share in 2025; diagnostic and monitoring devices are forecast to expand at a 7.54% CAGR through 2031.

- By indication, COPD captured 41.25% of Spain respiratory devices market share in 2025, while sleep apnea is projected to grow at a 7.79% CAGR to 2031.

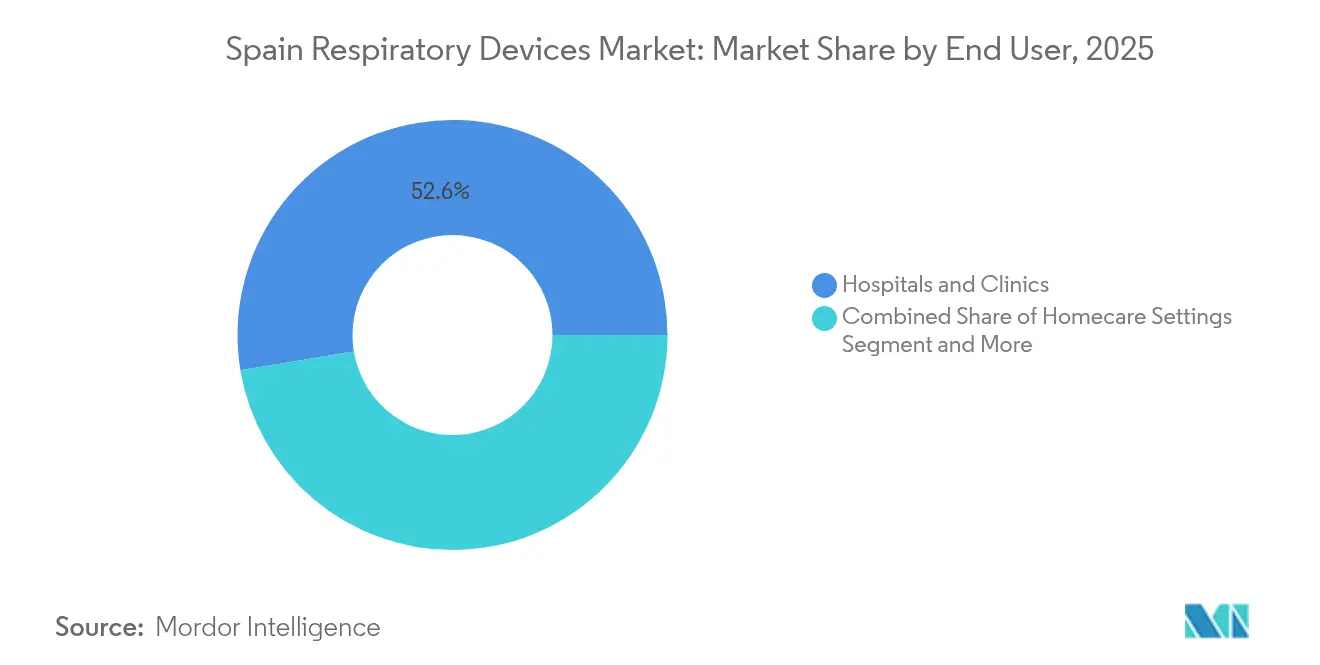

- By end user, hospitals and clinics accounted for 52.62% of the Spain respiratory devices market size in 2025; homecare settings are advancing at an 8.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Respiratory Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of COPD, Asthma, TB & Sleep-Apnea | +1.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Rapid Ageing of Spain's Population | +1.5% | National, pronounced in rural regions | Long term (≥ 4 years) |

| Expansion of Home-Based Respiratory Care & Tele-Monitoring | +1.2% | National, early adoption in Madrid, Barcelona | Medium term (2-4 years) |

| Surge In E-Cigarette–Related Lung Injuries | +0.8% | National, higher impact in metropolitan areas | Short term (≤ 2 years) |

| Post-COVID Government Incentives for Local Ventilator Output | +0.6% | Regional, focused on Andalusia, Catalonia | Medium term (2-4 years) |

| Adoption of AI-Enabled Predictive Maintenance for Ventilators | +0.4% | National, hospital-centric deployment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of COPD, Asthma, Tuberculosis, and Sleep Apnea

COPD affects 11.8% of Spanish adults and drove a 35.9% rise in hospital discharges for respiratory diseases, a pattern that strengthens long-term sales of ventilators, nebulizers, and spirometers. Sleep apnea remains widely underdiagnosed despite affecting nearly half of older adults at elevated dementia risk, creating fresh headroom for positive airway pressure devices and home sleep testing kits. Advances in tuberculosis PCR kits with 100% sensitivity expand demand for portable diagnostic systems in public health laboratories. Together, these epidemiological shifts lengthen device replacement cycles and enlarge the Spain respiratory devices market far beyond acute care settings.

Rapid Ageing of Spain’s Population

The cohort aged 90 years or older swelled 58.29% from 2013 to 2023, reaching 608,321 citizens. An ageing index of 142.35% highlights growing demand for non-invasive ventilation, oxygen concentrators, and airway clearance devices tailored to home use. With single-person households forecast to account for 33.5% of all households by 2039, manufacturers prioritise intuitive interfaces and remote monitoring features that let older adults remain independent. Hospitals already maintain dedicated non-invasive ventilation units in 83% of facilities, signalling sustained procurement for ageing-related disorders.[1]Source: Antonio Antón et al., “Home Mechanical Ventilation Practices in Spain and Portugal,” PubMed, pubmed.ncbi.nlm.nih.gov These demographic realities embed structural growth in the Spain respiratory devices market.

Expansion of Home-based Respiratory Care and Tele-monitoring

Universal Health Care legislation approved in 2024 extends device reimbursement to previously ineligible populations, unlocking fresh demand for home ventilation, oxygen therapy, and sleep solutions. Telerehabilitation pilots report high satisfaction among elderly COPD patients, citing enhanced communication and lower travel burden. The European Health Data Space regulation, effective 2027, will standardise data flows and thereby strengthen remote monitoring capabilities nationwide. Subscription-based software services surrounding connected devices create recurring revenue streams and reinforce vendor lock-in across the Spain respiratory devices market.

Surge in e-cigarette-related Lung Injuries

Clinical imaging uncovers significant pulmonary damage from vaping, driving acute need for high-resolution CT scanners, mechanical ventilators, and oxygen therapy systems in emergency departments. The government’s precautionary mask-wearing policy inside hospitals during respiratory illness peaks underscores heightened vigilance over airborne pathogens. The trend enlarges short-cycle sales to acute care units within the Spain respiratory devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Advanced Devices | -1.2% | National, acute in public hospitals | Long term (≥ 4 years) |

| EU MDR Compliance Delaying Product Launches | -0.9% | National, affecting all manufacturers | Medium term (2-4 years) |

| Shortage of Respiratory Therapists | -0.7% | National, severe in rural areas | Long term (≥ 4 years) |

| Environmental Curbs on Single-Use Plastics In Disposables | -0.5% | EU-wide, implementation by 2026 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Advanced Devices

Hospitals operate under strict budget ceilings even after recent public-health outlays, causing extended procurement cycles for premium ventilators and AI-enabled monitors. Regional authorities lean on cost-per-quality-adjusted-life-year thresholds that favour proven mid-range products. The Canary Islands’ decision to reduce its IGIC tax on medical devices to zero illustrates how targeted fiscal levers can mitigate affordability constraints. In the absence of nationwide VAT relief, price sensitivity will continue to cap immediate growth in the Spain respiratory devices market.

EU MDR Compliance Delaying Product Launches

Manufacturers must secure extensive clinical evidence and enhance post-market surveillance to satisfy the Medical Device Regulation, extending approval timelines and raising costs. Notified-body bottlenecks create scheduling delays, forcing smaller entities to reprioritise pipelines.[2]Source: European Commission, “Guidance – MDR documents,” health.ec.europa.eu Although legacy devices can remain on the market until 2028, new entrants confront heavier administrative burdens, slowing innovation refresh rates across the Spain respiratory devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Devices Anchor Current Leadership

Therapeutic devices accounted for 56.14% of 2025 revenue, reflecting a clinical preference for continuous airway pressure systems, ventilators, and oxygen concentrators. Positive airway pressure innovations such as KPAP enhance comfort and adherence among sleep apnea patients, locking in recurring mask and tubing sales. Ventilator development programs funded under national recovery schemes lower price barriers, further widening penetration. Nebulizers remain critical for COPD management, while portable oxygen systems support growing homecare demand. The Spain respiratory devices market size for therapeutic equipment is projected to rise in tandem with ageing-linked comorbidities.

Diagnostic and monitoring devices hold a smaller base but record the fastest 7.54% CAGR. Connected spirometers, wearable capnographs, and home sleep tests gain popularity amid wider telehealth rollouts. Early diagnosis of respiratory disease lowers hospital admissions, strengthening policy support for screening tools. As a result, diagnostic platforms capture a rising share of the Spain respiratory devices market.

By Indication: COPD Remains Largest; Sleep Apnea Fastest

COPD represented 41.25% of 2025 revenue due to widespread prevalence and chronic management needs. Long-term oxygen therapy, high-frequency chest wall oscillation, and nebulised bronchodilators anchor demand. Spain respiratory devices market share for COPD solutions stays robust as smoking-related morbidity persists.

Sleep apnea is poised for the quickest 7.79% CAGR. Expanded diagnostic capacity using peripheral arterial tonometry and rising public awareness shorten treatment gaps. Positive airway pressure usage gains further momentum following evidence of cognitive benefits in at-risk seniors. Together, these dynamics elevate the Spain respiratory devices market size attached to sleep apnea care.

By End User: Hospitals Dominate Yet Homecare Surges

Hospitals and clinics held 52.62% revenue share in 2025, reflecting Spain’s centralised model and the presence of non-invasive ventilation units in 83% of facilities. Capital budgets prioritise ventilators, anaesthesia circuits, and monitoring platforms that support acute interventions. Homecare settings record the strongest 8.03% CAGR. Universal Health Care implementation extends coverage to migrants and underserved citizens, stimulating prescriptions for portable oxygen concentrators and sleep therapy devices. The Spain respiratory devices market size for domestic use expands as tele-monitoring lowers readmission rates and strengthens adherence.

Long-term care facilities and ambulatory surgical centres round out demand. The rise in minimally invasive procedures boosts single-day throughput and creates incremental needs for short-term ventilation and airway management kits. Simultaneously, long-term institutions equip wards with mobile suction and humidification units to cater to frail elders.

Geography Analysis

Regional disparities shape adoption trends within the unified health-service framework. Madrid and Barcelona lead digital-health usage owing to stronger fibre networks and specialist density. These provinces also pilot early home-ventilation reimbursement schemes, accelerating uptake of connected concentrators and smart inhalers. Andalusia positions itself as a manufacturing hub, evidenced by the locally engineered ResUHUrge ventilator and AI-assisted ECMO projects.

Catalonia showcased adaptability during COVID-19 by re-purposing veterinary ventilators, underscoring regional ingenuity in crisis response. The Canary Islands introduced zero IGIC tax on medical devices to promote affordability, a policy that could gain traction in other autonomous communities.

Rural provinces face sharper therapist shortages and heavier ageing burdens, encouraging uptake of user-friendly home units. Upcoming European Health Data Space rules will harmonise data exchange, smoothing nationwide deployment of tele-respiratory platforms. Overall, the Spain respiratory devices market maintains cohesive growth, yet suppliers benefit from tailoring go-to-market strategies to each region’s demographic and policy landscape.

Competitive Landscape

The Spain respiratory devices market remains moderately fragmented. ResMed is posting 10% year-on-year sales growth to USD 1.3 billion in its fiscal Q2 2025, a performance linked to expanding sleep-health portfolios. Philips has produced 95% of replacement units tied to its earlier recall, restoring brand credibility ahead of renewed competition in the sleep device niche. Fisher & Paykel Healthcare, Medtronic, and Hamilton Medical drive innovation in humidification, invasive ventilation, and high-flow nasal therapy.

Domestic innovators gain visibility through targeted grants. Corify Care develops advanced cardiac and respiratory monitoring solutions in Madrid, while Andalusian start-ups leverage regional R&D funding to add AI overlays to ECMO platforms. EU MDR compliance costs and documentation hurdles limit smaller peers, yet those possessing niche expertise in low-cost ventilation or disposable redesign carve out defensible positions.

Strategic moves include ResMed’s allocation of 6-7% revenue to R&D for machine-learning models that predict therapy effectiveness. Fisher & Paykel Healthcare invests in humidification systems optimised for post-operative care, targeting ambulatory centres. Philips pilots remote firmware updates that keep ventilator fleets cyber-secure, reinforcing its value proposition to public hospitals. These initiatives magnify digital ecosystems and foster aftermarket income, safeguarding market leadership.

Spain Respiratory Devices Industry Leaders

GE HealthCare

Koninklijke Philips N.V.

Fisher & Paykel Healthcare Ltd

Medtronic plc

ResMed

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Spain reintroduced mandatory face masks in hospitals amid a rise in respiratory illnesses, underscoring persistent infection-control priorities.

- March 2023: Conus Airway, a new startup launched by BHV Partners, is set to revolutionize medical devices for anesthesia and respiratory tract surgeries. The innovative devices will be crafted using technology pioneered by the esteemed head of pediatric thoracic surgery at Valencia's University and Polytechnic La Fe Hospital.

Spain Respiratory Devices Market Report Scope

As per the scope of the report, respiratory devices are respiratory diagnostic devices, therapeutic devices, and breathing devices for administering long-term artificial respiration. It may also include a breathing apparatus used for resuscitation, by forcing oxygen into the lungs of a person who has undergone asphyxia. Spain's Respiratory Devices Market is Segmented by Type (Diagnostic and Monitoring Devices (Spirometers, Sleep Test Devices, and Other Diagnostic and Monitoring Devices), Therapeutic Devices (Positive Airway Pressure (PAP) Devices, Humidifiers, Nebulizers, Ventilators, Inhalers, and Other Therapeutic Devices) and Disposables). The report offers the value (in USD million) for the above segments.

By Product Type

| Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | |

| Peak Flow Meters | |

| Other Diagnostic & Monitoring Devices | |

| Therapeutic Devices | Positive Airway Pressure (PAP) Devices |

| Humidifiers | |

| Nebulizers | |

| Ventilators | |

| Inhalers | |

| Oxygen Concentrators | |

| Other Therapeutic Devices | |

| Disposables | Breathing Circuits |

| Masks | |

| Filters | |

| Other Disposables |

By Indication

| COPD |

| Asthma |

| Sleep Apnea |

| Cystic Fibrosis |

| Tuberculosis |

| Other Respiratory Disorders |

By End User

| Hospitals and Clinics |

| Homecare Settings |

| Ambulatory Surgical Centers |

| Long-term Care Facilities |

| By Product Type | Diagnostic & Monitoring Devices | Spirometers |

| Sleep Test Devices | ||

| Peak Flow Meters | ||

| Other Diagnostic & Monitoring Devices | ||

| Therapeutic Devices | Positive Airway Pressure (PAP) Devices | |

| Humidifiers | ||

| Nebulizers | ||

| Ventilators | ||

| Inhalers | ||

| Oxygen Concentrators | ||

| Other Therapeutic Devices | ||

| Disposables | Breathing Circuits | |

| Masks | ||

| Filters | ||

| Other Disposables | ||

| By Indication | COPD | |

| Asthma | ||

| Sleep Apnea | ||

| Cystic Fibrosis | ||

| Tuberculosis | ||

| Other Respiratory Disorders | ||

| By End User | Hospitals and Clinics | |

| Homecare Settings | ||

| Ambulatory Surgical Centers | ||

| Long-term Care Facilities | ||

Key Questions Answered in the Report

What is the current value of the Spain respiratory devices market?

Spain respiratory devices market size is USD 681.23 million in 2026.

How fast will the market grow through 2031?

The market is forecast to post a 6.49% CAGR between 2026 and 2031.

Which product category leads revenue?

Therapeutic devices hold 56.14% of 2025 revenue owing to high adoption of ventilators and positive airway pressure systems.

Why is homecare the fastest-growing end-user segment?

Universal Health Care coverage, tele-monitoring advances, and an ageing population fuel an 8.03% CAGR for homecare demand.

What regulatory shifts most affect suppliers?

EU MDR compliance prolongs product launches and raises documentation costs, while EU packaging rules force redesign of single-use disposables.

Page last updated on: