Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Overhead Conveyor Market is Segmented by Type (Monorail, Power and Free, Others), Capacity (Light Duty, and More), Load Weight (< 50 Kg, 50-100 Kg, > 100 Kg), Speed (Fixed, Variable), Component (Track, Trolley, and More), Automation Level (Manual, Semi-Automated, and More), End-User Industry (Automotive and Auto Components, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

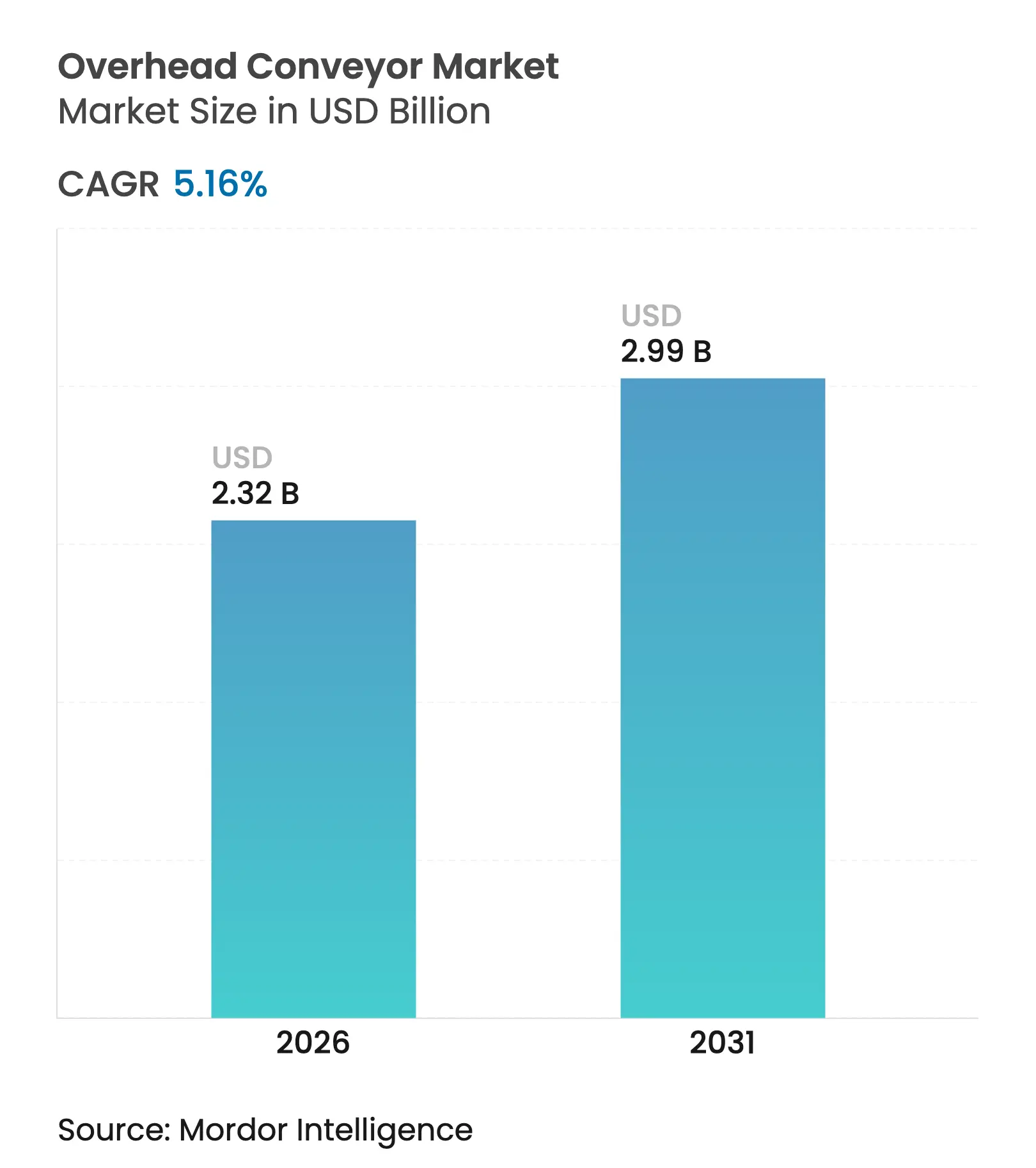

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 5.16 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players.webp&w=828&q=100) *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The overhead conveyor market size was valued at USD 2.21 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 5.16% during the forecast period (2026-2031). Healthy demand stems from manufacturers automating material flow to save floor space, trim labor exposure, and shorten takt times. Asia’s manufacturing resurgence, ongoing warehouse modernization in North America, and paint-shop retrofits in Europe continue to widen the addressable base for overhead conveyor solutions. Buyers increasingly favor modular, open-architecture platforms that combine mechanical reliability with advanced control software, while the e-commerce and food sectors provide new adjacency growth. Segment-level momentum is strongest in heavy-duty and fully automated configurations as factories consolidate process steps and bridge workforce gaps.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Industry 4.0-led demand for fully automated material-flow systems in automotive OEM plants Industry 4.0-led demand for fully automated material-flow systems in automotive OEM plants | +1.8% | Asia & Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Asia & Europe | Impact Timeline:Medium term (2-4 years) |

Rapid e-commerce fulfillment center build-outs in North America & Asia Rapid e-commerce fulfillment center build-outs in North America & Asia | +1.5% | North America & Asia | Short term (≤ 2 years) | |||

Food-grade overhead conveyors gaining traction to support stricter hygiene standards Food-grade overhead conveyors gaining traction to support stricter hygiene standards | +0.9% | US & EU | Medium term (2-4 years) | |||

Retrofit-driven replacement cycle in legacy paint-shop monorails Retrofit-driven replacement cycle in legacy paint-shop monorails | +0.7% | EU | Short term (≤ 2 years) | |||

Rising labor-scarcity premiums in GCC driving overhead automation projects Rising labor-scarcity premiums in GCC driving overhead automation projects | +0.4% | Middle East (GCC) | Medium term (2-4 years) | |||

Green-factory mandates spurring lightweight, energy-efficient track designs Green-factory mandates spurring lightweight, energy-efficient track designs | +0.3% | Global, with emphasis on Europe | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Industry 4.0-led demand for fully automated automotive plants

Automotive producers are re-engineering material flow around data-rich, sensor-driven overhead systems that synchronize with MES platforms and in-line quality stations. Siemens' EMS400S Box illustrates that standardized track hardware now ships with onboard PLCs capable of decentralized control, enabling plant managers to reroute carriers without shutting lines. German premium OEMs report 15% cycle-time cuts and ergonomic gains, demonstrating that automation returns extend beyond labor cost offsets. Asian assemblers deploy similar systems at greenfield sites to avoid retrofitting costs, accelerating the adoption curve. As lines converge on mixed-model production, adaptive overhead networks help manufacturers balance batch flexibility with continuous flow.

Rapid e-commerce fulfillment center build-outs

Surging online order volumes push distribution centers to exploit cubic footage rather than expand footprints. Ceiling-mounted conveyors operating 30-40 ft above floor level separate bulk carton movement from pick zones to ease congestion[1]Scott Stone, “Automation and Space: Conveyor Layouts,” Cisco-Eagle, cisco-eagle.com, and in North America operators budget an average of USD 1.5 million per site for conveyor and sortation upgrades, with 40% planning projects by 2027. Overhead paths marry efficiently with autonomous mobile robots on the floor, enabling multitier workflows that raise lines per hour without compromising pick accuracy. This design philosophy is being exported to Asia where land costs in megacities intensify the need for vertical material flow.

Food-grade overhead conveyors to meet stricter hygiene rules

Revisions to FDA and EU food directives now oblige processors to reduce harborage points that foster bacteria. Stainless-steel tracks, sealed carriers, and tool-less wash-down features yield premium prices but cut recall exposure. Ammeraal Beltech guidelines underscore EC 1935/2004-compliant materials, while Dorner’s 7350 Series targets wet-room sanitation protocols. The payoff appears in lower microbiological test failures and faster clean-in-place cycles, critical for multi-product plants. European meat and dairy facilities serve as early adopters; US produce packers and Asian seafood exporters are following suit.

Retrofit cycle in legacy paint-shop monorails

Europe’s auto painters are swapping 1990s-era monorails for energy-efficient, closed-loop conveyors that fine-tune dwell times for water-borne coatings. L.B. Foster’s radiator line retrofit retained mechanical beams yet embedded modern drives and feedback loops, slicing defect rates by 25%. Capital-light retrofits shorten payback to below four years, compared with a full rip-and-replace. EU climate directives and volatile power prices incentivize operators to cut oven idle times through smarter carrier pacing, elevating retrofit demand in Italy, France, and Spain.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex vs. floor-mounted belt systems for light loads High capex vs. floor-mounted belt systems for light loads | -0.8% | Global, with emphasis on price-sensitive markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.8% | Geographic Relevance:Global, with emphasis on price-sensitive markets | Impact Timeline:Medium term (2-4 years) |

Limited interoperability of proprietary control software across vendors Limited interoperability of proprietary control software across vendors | -0.6% | Global | Short term (≤ 2 years) | |||

Space-clearance constraints in low-ceiling brown-field sites Space-clearance constraints in low-ceiling brown-field sites | -0.4% | Global, with emphasis on older industrial facilities | Long term (≥ 4 years) | |||

Extended ROI horizon in price-sensitive South-Asian SMEs Extended ROI horizon in price-sensitive South-Asian SMEs | -0.3% | South Asia | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High capex vs. floor-mounted belt systems for light loads

Initial installs cost 40–60% more than floor belts, pressuring ROI for plants conveying components under 15 kg. SMEs in South and Southeast Asia often defer projects because credit terms remain costly. MasterMover estimates that overhead equipment penetrates mainly in operations where uptime, cleanliness, or multi-level flow provides disproportionate payback. Vendors now ship bolt-together track sections and pre-wired controls that cut installation downtime, yet capex parity with floor alternatives remains elusive for light duties.

Limited interoperability of proprietary control software

Plants running mixed equipment from different vendors face data silos that hamper line-wide optimization. Proprietary HMIs and closed communication stacks force integrators to install middleware or isolate sub-loops. SMAR’s ProcessView stresses OPC compliance as a route to open connectivity. Siemens is piloting AI agents that sit atop varied PLCs, offering a horizontal layer for predictive routing and maintenance. Progress is uneven; until cross-vendor standards mature, buyers hesitate to commit to single-supplier ecosystems.

By Type: Power & Free Systems Enable Complex Routing

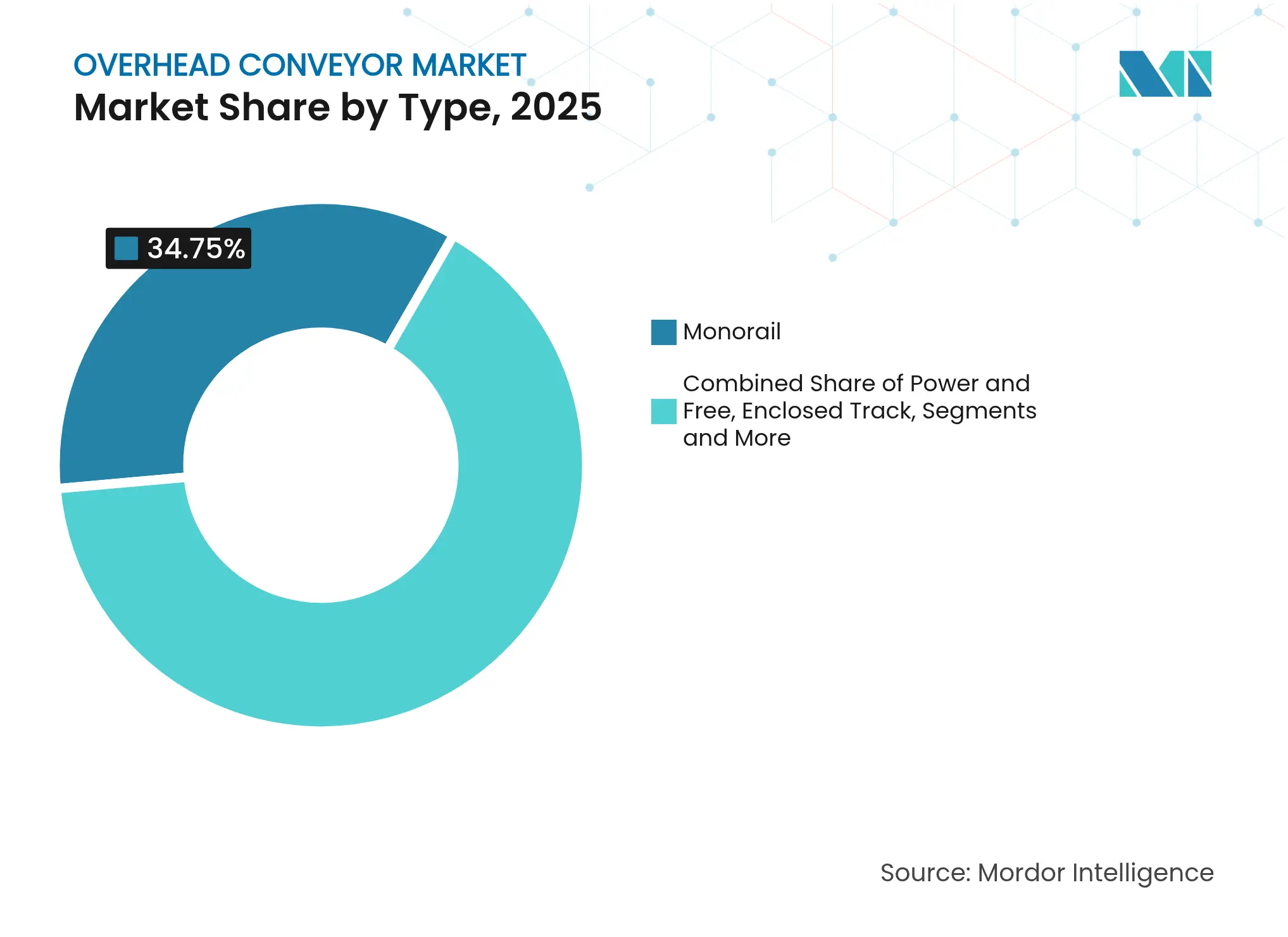

Overhead conveyor market size for type segmentation shows monorail systems capturing 34.75% revenue in 2025, but power & free designs are outpacing at a 6.32% CAGR. Power & free carriers disengage from the main chain, allowing buffering, sequencing, and overtaking functions critical in mixed-model assembly. Automotive body-in-white lines, appliance makers, and paint shops value this flexibility to synchronize divergent task times. Enclosed-track configurations mitigate particulate exposure in electronics and pharma plants, while inverted formats provide ergonomic load access. Suppliers such as Pacline and CALDAN push modular kits that clip onto legacy monorails, letting operators add free sections without scrap-and-build cycles. Overall, the overhead conveyor market continues to pivot toward hybrid architectures that blend monorail simplicity with power & free agility.

Second-generation systems integrate RFID tags, zone controllers, and decentralized drives to switch routes in milliseconds. This intelligence transforms previously linear tracks into network-like grids capable of alternative paths when workstations back up. Early adopters report 8–12% throughput gains during seasonal volume spikes. Cost remains above classic monorails, yet the payback emerges via lower change-over downtime and deferred capex on additional lines.

Note: Segment shares of all individual segments available upon report purchase

By Capacity: Heavy Duty Systems Support Manufacturing Complexity

Medium-duty equipment led with 41.35% of overhead conveyor market share in 2025, serving mainstream tasks from dashboard assembly to parcel sortation. Heavy-duty variants, however, show a 7.45% CAGR as factories merge machining, welding, and surface treatment on contiguous lines. Konecranes’ CXT overhead crane portfolio, rated up to 80 t, intersects with conveyor beams to hand off large modules without floor forklifts. In electric-vehicle platforms, battery packs and underbody frames weigh more than prior combustion components, raising load specifications. Vendors respond with dual-track carriers, stronger drop-forged chain links, and torque-dense drive units.

Modular engineering now lets OEMs mate identical trolleys to different track profiles, scaling payloads without redesigning control logic. Heavy-duty adoption also correlates with the trend toward fewer, longer takt lines; managers prefer one robust conveyor network instead of multiple parallel light-duty runs. As this paradigm gains traction, heavy-duty system share grows within overhead conveyor market size forecasts.

By Load Weight: Heavier Applications Drive Premium Growth

Lines moving sub-50 kg parts hold 46.70% revenue today, yet the >100 kg slice expands at 8.82% CAGR through 2031. Electric-vehicle battery modules, home-appliance shells, and industrial gearbox housings all trigger the shift. Columbus McKinnon’s acquisition of montratec broadens its portfolio into precision conveyance for heavier loads, underscoring how suppliers reposition toward high-value niches. Load growth drives investments in servo-driven carriers with positional repeatability that align to robotic stations without shuttles. Plants converting manual overhead hoists to automated trolleys cite safety gains and insurance premium reductions alongside productivity upside.

The load weight segmentation reveals important insights about the evolving nature of manufacturing automation, as heavier applications represent the new frontier for overhead conveyor implementation. Columbus McKinnon's acquisition of montratec GmbH enhances their precision conveyance capabilities for heavier applications, targeting markets such as electric vehicles and life sciences.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Speed: Variable Systems Enable Dynamic Production

Fixed-speed tracks account for 59.35% of the installed overhead conveyor market size, as they are favored for their simple mechanics and steady flow. Variable-speed models, expanding 8.02% CAGR, pair inverter drives with line sensors to modulate chain velocity. Russell Conveyor & Equipment reports 12-18% power savings when conveyors scale down during maintenance windows or low-volume shifts. Faster acceleration ramps also cut carrier queues between sequential stations, compressing buffer inventory. As dynamic scheduling, batch sizing, and late-stage customization advance, variable capability becomes table stakes for new RFQs.

The emergence of energy-efficient conveyor solutions represents a significant trend in the market, with variable speed drives (VSDs) playing a central role in optimizing power consumption based on operational demands. Russell Conveyor & Equipment highlights this trend, noting that automated conveyor systems with VSDs can adjust speed based on operational demands, leading to significant energy savings.

By Component: Software Controls Drive System Intelligence

Track frameworks still represent 29.55% of 2025 sales; yet control and software modules grow 10.32% annually. The overhead conveyor industry increasingly monetizes diagnostics, remote updates, and AI-guided routing rather than pure steel tonnage. Siemens AI agents are designed to provide unified dashboards spanning drives, PLCs, and MES, turning conveyors into data nodes. Vendors bundle subscription packages for predictive asset management, promoting recurring revenue streams. Buyers evaluate lifecycle costs beyond initial hardware, elevating the role of robust, cyber-secure control stacks.

The accelerating growth in control and software components signals a fundamental shift in how overhead conveyor systems create value for manufacturers. Siemens' introduction of AI agents for industrial automation at Automate 2025 exemplifies this trend, with these agents designed to operate autonomously across the industrial value chain while integrating with existing systems.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

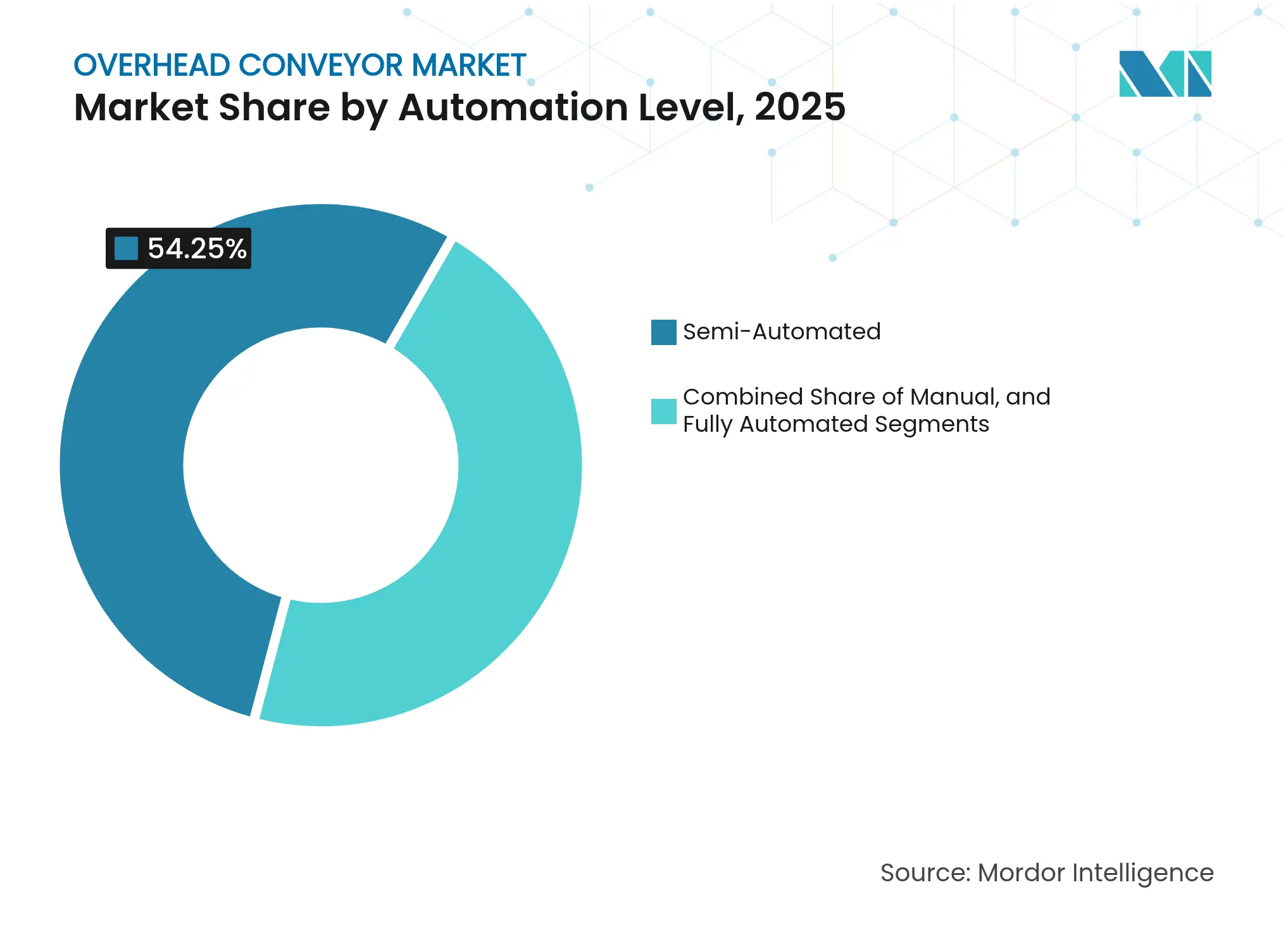

By Automation Level: Industry 4.0 Accelerates Full Automation

Semi-automated lines remain prevalent at 54.25% share, balancing capital with operator supervision. Fully automated systems, however, clock 11.3% CAGR as labor scarcity in OECD markets tightens. Rockwell Automation highlights data-ready smart machines as the next frontier, reinforcing conveyor integration with broader OT-IT convergence. Retrofit toolkits add sensors and edge controllers to legacy tracks, letting plants migrate gradually. In greenfield facilities, turnkey autonomous conveyor cells interface with robotic pick, vision, and AGV fleets, delivering lights-out logistics during third shifts.

The automation level segmentation reveals the market's evolutionary trajectory toward increasingly intelligent and autonomous systems. Rockwell Automation highlights key industrial automation trends for 2025, emphasizing the role of data-ready smart machines in enhancing efficiency and business value.

Note: Segment shares of all individual segments available upon report purchase

By End-use Industry: E-commerce Transforms Distribution Networks

Automotive keeps the lion’s share at 28.05%, yet e-commerce facilities expand fastest at 7.92% CAGR as retailers compress click-to-ship cycles. Premio’s ASRS case study shows overhead totes cutting floor congestion and tripling order throughput. Food and beverage processors adopt stainless, food-grade units to stay audit-ready, while aerospace and pharma segments require vibration-controlled carriers for delicate parts. The strategic value of overhead systems in these facilities extends beyond space efficiency to include sorting capabilities and workstation delivery functions that directly impact fulfillment speed and accuracy.

Also, the strategic implications for conveyor manufacturers are significant, as success increasingly depends on understanding industry-specific requirements and developing tailored solutions that address the unique challenges of each application environment.

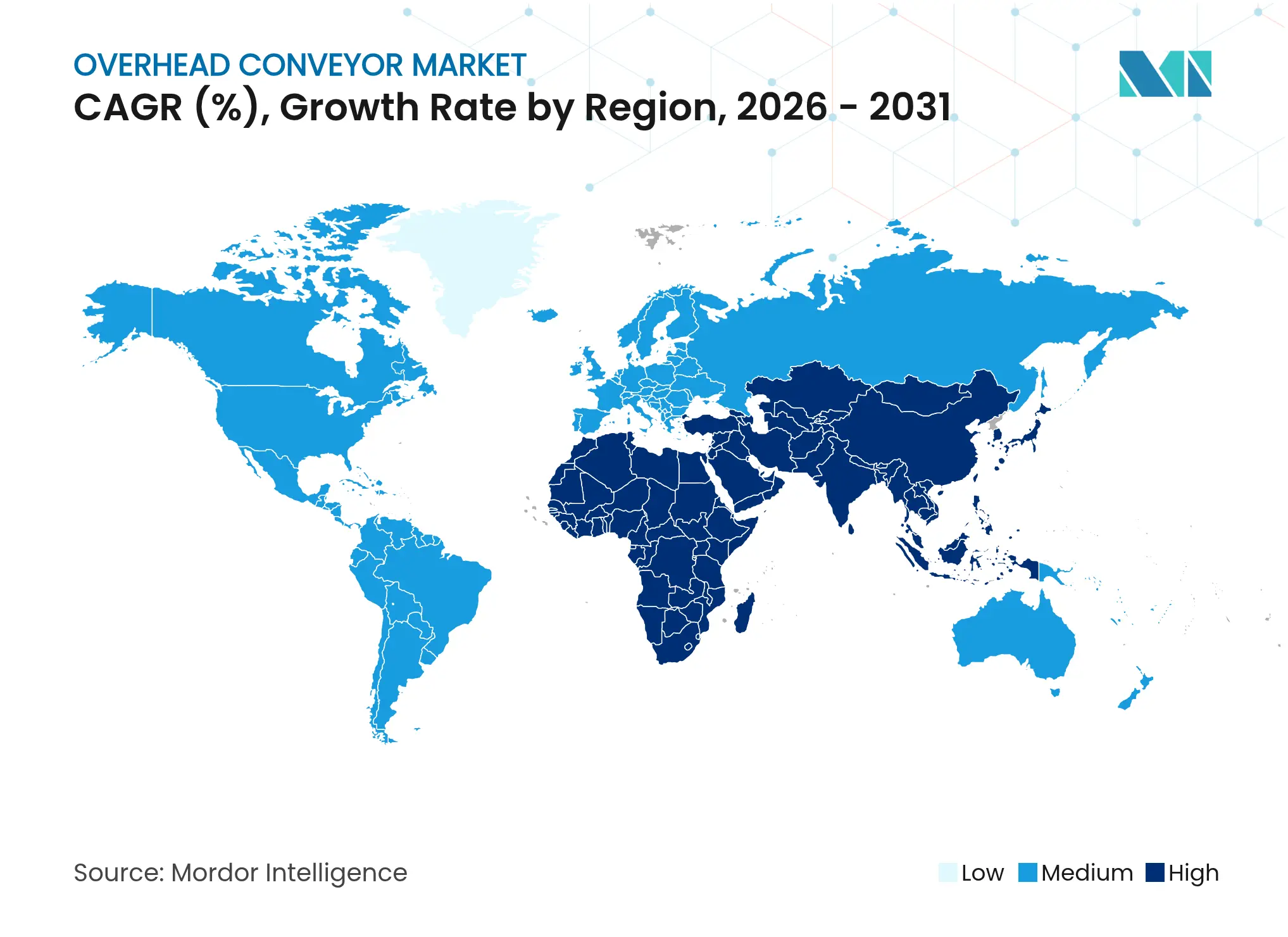

Asia commands 38.25% of revenue, propelled by large-scale greenfield factories in China, India, and ASEAN that leapfrog directly to Industry 4.0 layouts. Chinese automotive plants integrate overhead carriers with AGVs and digital twins to orchestrate mixed-model sequences.Indian appliance manufacturers bypass floor belts to preserve space in urban industrial parks. Southeast Asian e-commerce hubs retrofit mezzanines with overhead carton loops to accelerate last-mile dispatch. Regional 7.33% CAGR reflects both sheer industrial base expansion and rising automation intensity.

North America ranks second, fueled by warehouse automation and onshoring of strategic industries. US distribution centers invest in ceiling-level conveyor grids that pair with goods-to-person robotics, leveraging high ceilings typical of Class A facilities. Modern Materials Handling notes 40% of operators budgeting upgrades within two years, indicating a robust pipeline. Canadian metal fabricators adopt heavy-duty overhead beams to maneuver large weldments, offsetting domestic labor rates. The emphasis now lies on software-defined orchestration rather than mechanical differentiation.

Europe maintains a sophisticated installed base in automotive, aerospace, and food processing. German OEMs deploy AI-enabled controllers to schedule paint-shop carriers around energy-price signals, aligning green goals with cost. UK and Italian food processors invest in wash-down tracks to comply with post-Brexit divergence in hygiene audits. Retrofit programs dominate capital spending as mature factories update controls but reuse structurally sound steelwork. EU grants that support energy efficiency further incentivize conveyor upgrades over new floor space expansions.

Market Concentration

The market shows moderate concentration: the five largest vendors account for roughly 50% of global revenue, with Daifuku, Dematic, and SSI Schaefer heading integrated system supply, while Pacline, CALDAN, and Ultimation focus on niche engineering. Hardware leadership is no longer sufficient; differentiation pivots to interoperable controls and predictive analytics. Siemens’ AI agents underline this transition by embedding autonomy across heterogeneous equipment, offering operators a unified logic layer and challenging single-vendor lock-in. Traditional conveyor specialists respond by partnering with software firms or launching digital service arms.

Strategic moves favor modular product families that shorten lead times and simplify engineering. White-space expansion targets heavy-duty manufacturing, food-grade lines, and high-bay fulfillment centers in emerging markets. Columbus McKinnon’s montreac acquisition demonstrates a bolt-on approach to gain precision pallet conveyance. Regional integrators differentiate through rapid on-site support and customized line layouts, while global conglomerates leverage scale and project financing capabilities.

Competitive intensity is rising as robotic and AGV vendors encroach on conveyor territory, pitching flexible transport pods. Market incumbents counter with hybrid solutions that integrate robots atop conveyor carriers, offering blended attributes. Long-term success will hinge on ecosystem participation, cybersecurity readiness, and lifecycle service models rather than stainless-steel tonnage alone.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Overhead conveyors, once thought unsuitable for certain shapes, now adeptly transport these very loads. Historically, industrial facilities and paint systems have been the primary users of these conveyors, particularly in scenarios where human handling could jeopardize paint quality. These conveyors skillfully maneuver through challenging settings, from caustic washers and spray booths to high-temperature drying ovens, all while preserving their functionality. The study monitors global revenue generated from overhead conveyor systems by leading market players. Additionally, it evaluates various factors and growth drivers to refine market estimates.

The overhead conveyor market is segmented by type (monorail, power, and free, others), capacity (light duty, medium duty, heavy duty), end-user Vertical (Manufacturing, Warehousing and Logistics, Others), (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.