Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.33 Billion |

| Market Size (2026) | USD 3.53 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

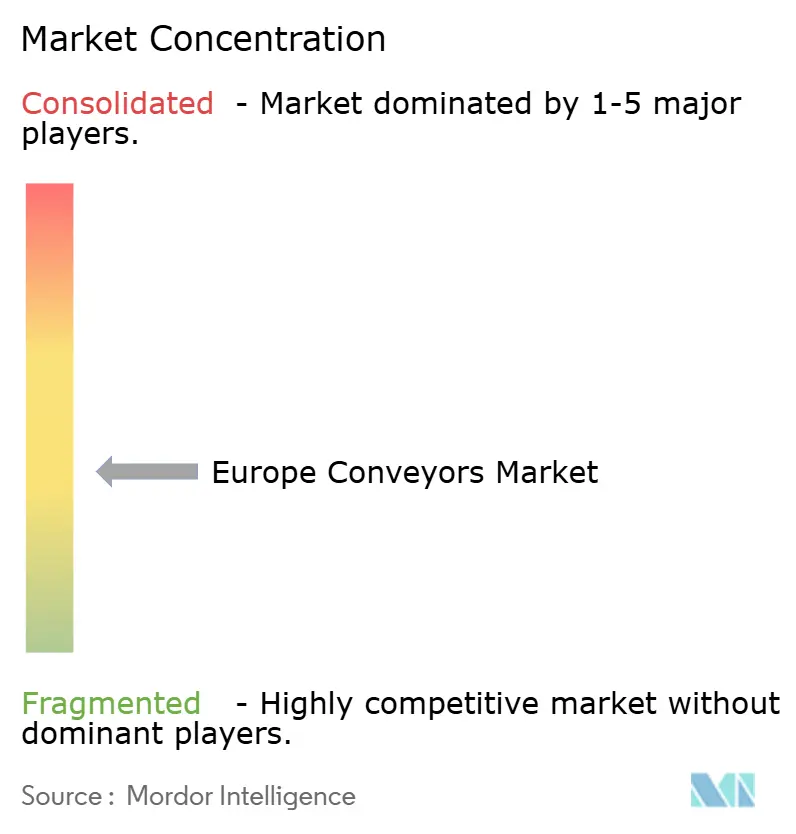

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Conveyors Market Analysis by Mordor Intelligence

The Europe Conveyors Market size is expected to grow from USD 3.33 billion in 2025 to USD 3.53 billion in 2026 and is forecast to reach USD 4.71 billion by 2031 at 5.98% CAGR over 2026-2031. Wage inflation above 5% in Germany and France during 2024, rising vacancy rates in the Nordics, and tight delivery windows in e-commerce are turning boardroom focus from low-cost labor toward predictive-uptime economics. Subsidies of up to 40% on automation capital expenditure under the European Union’s Recovery and Resilience Facility have compressed conveyor payback horizons from four years to under 2.5 years for mid-sized manufacturers. Same-day e-commerce fulfillment is the fastest-growing end-use as micro-fulfillment centers deploy 800-1,200 meters of conveyors within 15 kilometers of urban cores. Variable-frequency drives and regenerative braking retrofits aimed at cutting industrial energy use by 11.7% before 2030 are beginning to reshape upgrade priorities under Directive 2023/1791. Autonomous mobile robots are encroaching on short-distance transfers, yet high-throughput sortation lines moving more than 10,000 parcels per hour remain firmly in conveyor territory due to AMR congestion, battery-swap logistics, and collision-avoidance latency

Key Report Takeaways

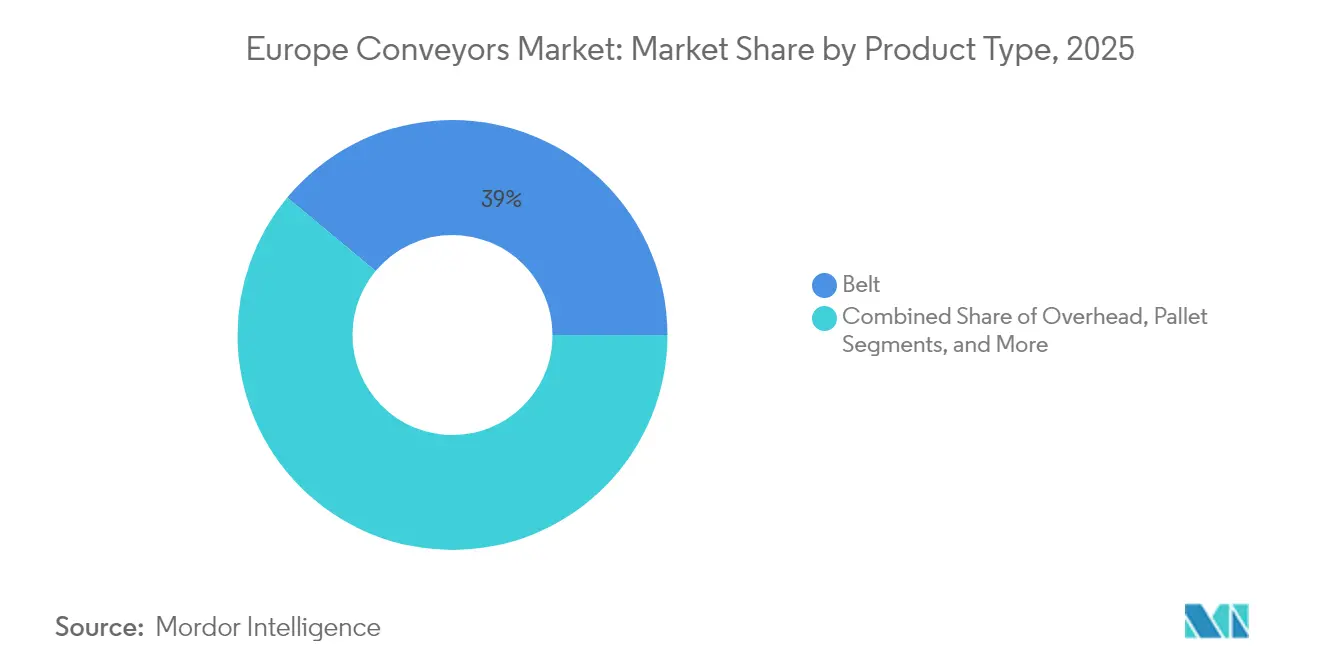

- By product type, belt conveyors led with 38.96% revenue share in 2025, while overhead conveyors are projected to expand at 8.17% CAGR through 2031.

- By end-user industry, airport baggage handling accounted for 28.41% of demand in 2025; e-commerce and retail installations are forecast to rise at 8.95% CAGR to 2031.

- By load type, unit-load configurations held 68.12% of the Europe conveyors market share in 2025 and are set to grow at 7.86% CAGR through 2031.

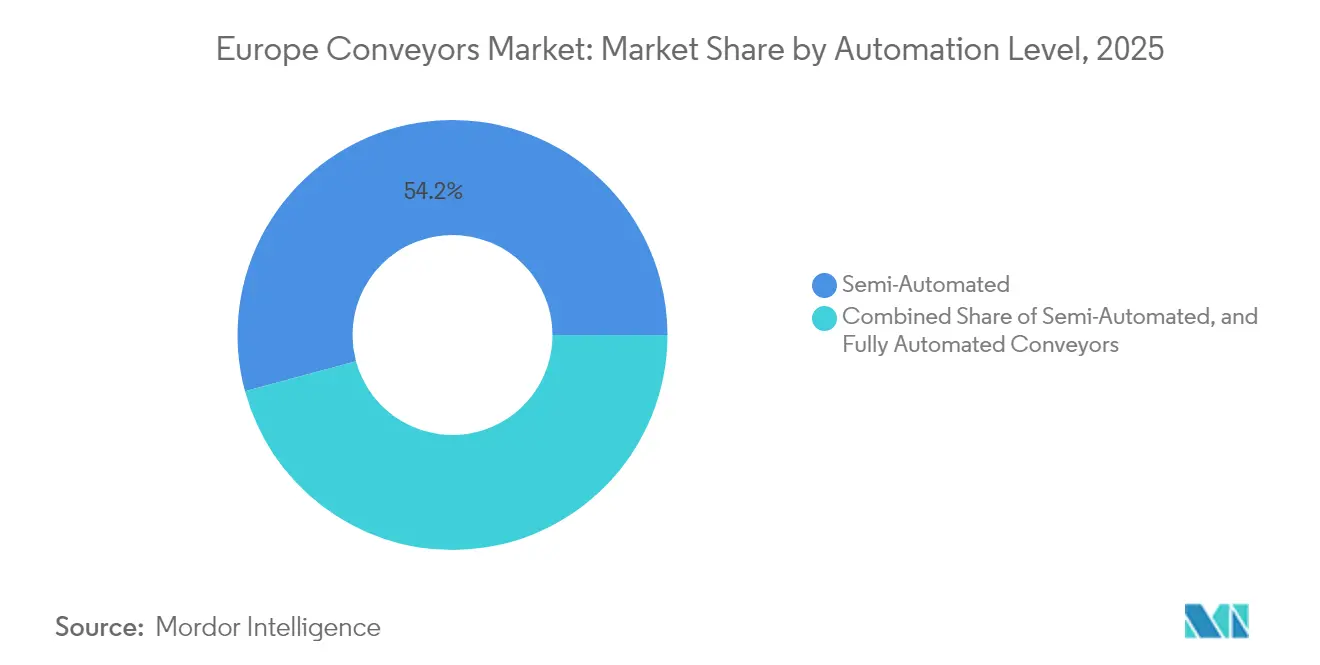

- By automation level, semi-automated systems represented 54.22% of installations in 2025, whereas fully automated smart platforms are advancing at a 7.62% CAGR forecast to 2031.

- By service,unit-load configurations held 28.85% of the Europe conveyors market share in 2025 predictive, IIoT-enabled service agreements moved from 10.04% of CAGR forecast to 2031.

- By country, Western Europe generated 55.18% of 2025 revenue; Eastern Europe is the fastest-growing region, posting an 8.64% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Conveyors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labor Costs Across Western Europe | +1.5% | Western Europe (Germany, France, UK, Benelux), spillover to Nordics | Medium term (2-4 years) |

| Explosive Growth of Same-Day E-Commerce Fulfilment | +1.8% | Pan-European, concentrated in urban hubs (Paris, Berlin, Amsterdam, Madrid) | Short term (≤ 2 years) |

| Tightening EU Food-Safety Regulations Prompting Hygienic Conveyor Adoption | +0.7% | Pan-European, strongest in Germany, France, Italy (dairy and bakery clusters) | Medium term (2-4 years) |

| Automation Subsidies Under EU Recovery and Resilience Facility | +1.2% | France, Italy, Spain, Poland (RRF beneficiary states) | Short term (≤ 2 years) |

| Shift Toward Predictive-Maintenance Contracts Powered by IIoT | +0.9% | Western Europe and Nordics (early adopters), expanding to Eastern Europe | Long term (≥ 4 years) |

| Sustainability Mandates Driving Energy-Efficient Conveyor Retrofits | +0.8% | Pan-European, compliance-driven in Germany, Netherlands, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Same-Day E-Commerce Fulfillment

Parcel volumes in the European Union increased 18% during 2024, pushing same-day delivery penetration in urban e-commerce to 22%. Retailers responded by opening micro-fulfillment centers within 15 kilometers of city centers, each fitted with high-speed sortation conveyors that handle 5,000-8,000 parcels per hour. Ocado’s Smart Platform at Auchan’s Polish facility routes totes via a grid of overhead conveyors to robotic pick stations, enabling 40,000 stock-keeping units to flow through a single site. Amazon’s EUR 700 million (815.5 USD million) network expansion added more than 1,000 mobile robots and complementary conveyor lines across Germany, France, and Spain. The spread of decentralized fulfillment nodes is boosting conveyor density per square meter, favoring modular layouts that bolt onto automated storage and retrieval systems. Cross-border e-commerce grew 12% in 2024 after simplified VAT rules streamlined customs clearance, elevating throughput demands at EU sortation hubs.[1]European Commission, “Recovery and Resilience Facility,” commission.europa.eu

Rising Labor Costs Across Western Europe

Manufacturing wages rose 5.2% in Germany, 5.1% in France, and 4.8% in the United Kingdom during 2024, compressing margins in labor-intensive warehousing. The EU minimum-wage directive set a floor at 60% of median pay, eliminating cheap-labor advantages for manual palletizing. SSI Schaefer installations demonstrate 30-50% headcount cuts after conveyor automation, improving return-on-investment timelines. Automotive producers retrofit overhead conveyors to move parts just-in-sequence, trimming assembly cycle times 15% and reducing repetitive-strain injuries. Labor shortages are acute in the Nordics, where Sweden’s manufacturing vacancy rate reached 6.8% in 2024, driving demand for conveyors integrated with collaborative robots that one operator can oversee from a single console

Automation Subsidies Under EU Recovery and Resilience Facility

The Recovery and Resilience Facility committed EUR 345 million (USD 402.01million) to France’s Industrie du Futur program and EUR 25 million (USD 29.13 million) to Italy’s CIM 4.0 initiative in 2024, underwriting up to 40% of qualified automation investments such as conveyor lines. Poland’s Smart Industry program co-financed EUR 18 million (USD 20.97 million) in logistics automation, and Spain’s Perte Agroalimentario earmarked EUR 12 million (USD 13.98 million) for hygienic conveyor upgrades. Subsidies shorten payback periods to under 2.5 years for companies with less than EUR 50 million (USD 58.26 million) in annual revenue, accelerating order cycles for European conveyor suppliers. Because most grants sunset by 2027, integrators are experiencing a near-term surge in bid activity, especially among smaller manufacturers that historically deferred automation for cost reasons. Suppliers able to package equipment, software, and grant-application support are converting tenders at higher win rates than hardware-only competitors.

Shift Toward Predictive-Maintenance Contracts Powered by IIoT

Sensor penetration on Western European conveyor lines hit 38% in 2024, enabling condition-based servicing that slices unplanned downtime 25-35% compared with fixed-interval programs. Interroll’s RollerDrive streams vibration and temperature data to cloud analytics, flagging bearing wear up to 72 hours before failure. Dematic’s iQ suite uses machine learning to predict component degradation and trim spare-parts inventories 20%. Siemens Logistics applied a digital twin at Munich Airport’s baggage-handling system to optimize diverter sequencing, removing peak-hour bottlenecks and sustaining throughput above 97% of rated capacity. Predictive-maintenance contracts generated 28% of leading suppliers’ aftermarket revenue in 2024, up from 19% in 2023, reflecting end-users’ willingness to pay for guaranteed uptime over transactional parts sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Capital Expenditure for Advanced Systems | -1.3% | Pan-European, most acute in Southern and Eastern Europe (budget-constrained SMEs) | Short term (≤ 2 years) |

| Shortage of Skilled Conveyor-Maintenance Technicians | -0.9% | Western Europe and Nordics (aging workforce), emerging in Eastern Europe | Medium term (2-4 years) |

| Fragmented EU Regulations Hindering Cross-Border Standardisation | -0.5% | Pan-European, compliance overhead highest in multi-country operations | Long term (≥ 4 years) |

| Rising Competition From Autonomous Mobile Robots | -0.6% | Western Europe (early AMR adoption), expanding to Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Expenditure for Advanced Systems

Fully automated conveyors with vision-guided sortation cost USD 500-800 per linear meter, versus USD 150-250 for semi-automated belts, deterring small and medium-sized enterprises in Southern and Eastern Europe. A 2,000 m² fulfillment center needs roughly 1,200 meters of conveyor, translating to USD 600,000-960,000 upfront for smart platforms. Leasing models remain nascent; only 12% of 2024 projects were financed as operating expenses, so most buyers still fund through capital budgets. European Central Bank deposit rates at 3.25% in mid-2024 lifted financing costs, lengthening payback periods especially in Poland and the Czech Republic where wages hover at USD 12-15 per hour. Energy-efficiency retrofits mandated under Directive 2023/1791 add USD 50-100 per meter, further inflating project totals.

Rising Competition From Autonomous Mobile Robots

European AMR shipments expanded 42% in 2024 to about 18,000 units, offering reconfigurable material flows without fixed tracks.[2]Amazon, “European Logistics Network Investment Announcement 2024,” reuters.comYet conveyors dominate in high-throughput lines exceeding 10,000 parcels per hour, where AMR fleets struggle with congestion and battery-swap downtime. Overhead conveyors, forecast to grow 8.54% CAGR, are unaffected because they occupy vertical airspace. Hybrid sites combining AMRs for inbound receiving and conveyors for outbound sortation represent 16% of 2024 warehouse projects in Western Europe, signaling coexistence rather than substitution. Total cost of ownership for AMRs, including software licenses and battery replacements every 3-4 years, often surpasses conveyor maintenance over a decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Overhead Systems Gain Altitude in Space-Constrained Facilities

Overhead conveyors are projected to expand at 8.17% CAGR between 2026 and 2031, outpacing all other variants as paint shops and cleanrooms fight for floor space. Belt units commanded 38.96% of 2025 revenue, underpinned by food processing and parcel sortation, where flat surfaces handle irregular packages gently. Roller lines support automotive final assembly with zero-pressure accumulation that prevents part damage during stoppages. Pallet conveyors move loads exceeding one ton in bulk warehouses, while specialty spiral or climbing designs elevate products between mezzanine levels. Interroll’s plug-and-play modules cut installation time 30%, appealing to operators who must minimize downtime during changeovers.

Europe conveyors market demand for overhead designs is rising because they integrate easily with robotic paint-cells, maintaining ±2 mm positioning for uniform coats and less overspray. Pharmaceuticals favor ceiling-mounted tracks that eliminate floor supports harboring microbes, easing cleanroom validation. Specialty spiral units, climbing several floors, consume a third of the footprint required by inclined belts, freeing warehouse aisles for AGV traffic. Compliance with Regulation 2023/1230 obliges overhead makers to add redundant safety relays and cloud-accessible documentation, adding USD 8,000-15,000 per install but ensuring future cybersecurity readiness

By End-User Industry: E-Commerce Installations Surge Past Airport Modernization

E-commerce and retail lines will post a 8.95% CAGR through 2031 as two-hour delivery targets spur dense urban micro-fulfillment centers. Airports retained 28.41% share in 2025, underpinned by Brussels and Zurich baggage-system overhauls processing up to 50,000 bags daily. Automotive EV plants rely on synchronised conveyors to deliver battery packs and power electronics just-in-sequence, trimming line-side inventory. Food manufacturers invest in stainless-steel modular belts complying with EHEDG to cut wash-down time.

Europe conveyors market solutions for e-commerce couple vision-guided diverters achieving 99.8% sort accuracy at 2.5 m/s with tote-based loops tied to shuttle storage. KNAPP’s German facility merges 210 shuttles and 1,800 meters of conveyors to fill 12,000 order lines per hour. Pharmaceutical plants integrate conveyors with automated inspection, verifying vial fill, cap torque, and label placement at 600 units per minute. Mining sites in Poland and Spain still favor heavy-duty belts moving over 1,000 t/h of aggregates along multi-kilometer routes.

By Load Type: Unit-Load Dominance Reflects Omnichannel Distribution Shift

Unit-load systems accounted for 68.12% of the Europe conveyors market share in 2025 and should advance 7.86% CAGR to 2031 as omnichannel distribution requires carton-level traceability. Parcels pass barcode and RFID checkpoints at every junction, feeding real-time inventory data to WMS dashboards. Bulk-load conveyors remain vital in cement and grain, where capacities exceed 1,000 t/h, but new retail and 3PL warehouses seldom specify troughed belts.

Europe conveyors market installations at DHL’s Warsaw hub span 2,400 meters, process 25,000 parcels per hour, and reach 99.7% sort accuracy. Modular designs let operators re-route flows by swapping 1-meter sections without civil works, a flexibility that bulk systems cannot match. EU packaging rules requiring 65% cardboard recycling by 2030 are pushing retailers to standardize carton sizes, further aligning with unit-load conveyor dimensions.

By Automation Level: Fully Automated Platforms Close Gap on Semi-Automated Incumbents

Semi-automated lines captured 54.22% revenue in 2025 thanks to lower costs, yet fully automated platforms are rising 7.62% CAGR on the back of labor scarcity in Nordics and Benelux. Smart conveyors monitor weight, dimensions, and barcodes in real time then tweak speed and diverter timing automatically to maximize flow. Siemens Logistics’ Parcel Sorter 3000 moves 12,000 parcels per hour with automated induction that erases manual singulation labor, trimming operating costs 40% .

Europe conveyors market buyers weighing semi- versus fully automated solutions balance upfront USD 200-350 per meter against USD 500-800 for advanced versions. Edge-computing gateways deliver sub-50 ms control loops, avoiding latency issues in cloud-based decision logic. Regulation 2023/1230 will require encrypted data links and audit logs, nudging even cost-sensitive operators toward smarter platforms that already embed cybersecurity.

By Service: Predictive Maintenance Contracts Reshape Aftermarket Economics

By service,unit-load configurations held 28.85% of the Europe conveyors market share in 2025 predictive, IIoT-enabled service agreements moved from 10.04% of CAGR forecast to 2031.Signaling a pivot from spare-parts sales to uptime guarantees. Installation wor civil engineering, cabling, commissioning still represents 15-20% of project value for multi-story sortation centers. Preventive maintenance based on fixed-hour intervals is giving way to sensor-driven programs that extend component life 20-30%.

Europe conveyors market suppliers like Dematic commit to 99.5% availability, accepting penalties if downtime exceeds thresholds. IIoT retrofits cost USD 3,000-8,000 per zone but pay back inside two years via lower overtime, reduced emergency call-outs, and optimized energy profiles. Directive 2023/1791 mandates energy audits every four years for large firms, putting additional momentum behind service contracts that couple performance monitoring with efficiency upgrades.

Geography Analysis

Western Europe generated 55.18% of 2025 revenue on the strength of Germany’s EV investments, UK parcel-hub upgrades, and France’s food-processing automation, yet growth trails emerging areas because most factories already run conveyors. German automakers poured EUR 4.2 billion into EV capacity in 2024, wiring overhead tracks that cut assembly cycles up to 18%. UK parcel carriers expanded hubs after cross-border e-commerce volumes rose 14% under simplified VAT rules. France’s Industrie du Futur grants covered 40% of qualified automation spend, compressing conveyor ROI below 2.5 years. Italy and Spain leveraged CIM 4.0 and Perte Agroalimentario subsidies to retrofit hygienic belts in dairy and bakery plants, slashing wash-down downtime by a quarter.

Northern Europe faces acute labor gaps; Sweden’s vacancy rate hit 6.8% in 2024. The Netherlands invested EUR 280 million (USD 326.27 million) in warehouse automation, dedicating up to 40% of capex to conveyors that link goods-to-person shuttles with sortation exits. Brussels Airport laid 20 kilometers of belts to lift on-time baggage delivery to 97.5% . Denmark’s meat exporters adopted stainless-steel modular lines that cut cleaning cycles from 90 to 35 minutes. Finland’s Digirail project piloted conveyor-based intermodal transfers, trimming container handling by 30%.

Eastern Europe is the growth engine, forecast at 8.64% CAGR through 2031 as nearshoring drives automotive and electronics inflows. Volkswagen committed USD 2.8 billion to Poland while LG Energy Solution added USD 1.7 billion (USD 139.82 million) in battery capacity, both requiring synchronized conveyors for JIS component feeds. The Czech Republic secured USD 2.2 billion for EV plants and USD 1.3 billion for tire lines, fueling heavy-duty roller demand. Poland’s Smart Industry grants cut fulfillment lead times from 48 hours to 24 hours in new 3PL warehouses. Hungary deployed EUR 120 million in tax incentives to lure tier-1 suppliers that installed overhead conveyors for EV components. Romania and Bulgaria attract light-manufacturing projects favoring semi-automated belts as a hedge against labor cost swings.

Competitive Landscape

The top five suppliers, Daifuku, SSI Schaefer, Dematic, Vanderlande, and KNAPP, held roughly 38-42% of 2024 revenue, indicating a moderately concentrated structure that still leaves room for mid-tier specialists. Turnkey integrators secure multi-year service contracts bundling hardware, warehouse software, and predictive analytics, locking clients into proprietary ecosystems that generate recurring revenue. Daifuku’s 2024 purchase of Contec added ISO Class 5-ready cleanroom conveyors for pharma and semiconductors. SSI Schaefer’s link-up with AutoStore embeds cube storage into high-speed sorters tailored for micro-fulfillment.

Europe conveyors market challengers such as Interroll and FlexLink differentiate on modularity, pre-assembled drives, and tool-free belt tensioning that slash installation hours 30% . Technology races center on IIoT sensors, edge-compute diverter control, and vision-guided sortation. Regulation 2023/1230 requires encrypted data streams and access logs, raising compliance overhead that favors large vendors with cybersecurity budgets.

Autonomous mobile robots threaten short-haul movements, but conveyors keep dominance above 10,000 items per hour. Hybrid projects that harness AMRs for inbound pallets and conveyors for outbound parcels are growing, yet throughput economics still steer high-volume flows toward belts. Finally, retrofit opportunities climb as 2010-vintage lines need energy-efficiency updates to meet Directive 2023/1791, a segment where smaller integrators can thrive by offering cost-effective upgrade kits.

Europe Conveyors Industry Leaders

SSI Schaefer AG

Mecalux S.A.

Beumer Group GmbH and Co. KG

KNAPP AG

Swisslog AG (KUKA AG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Vanderlande Industries secured a contract to upgrade baggage handling infrastructure at Frankfurt Airport, deploying advanced conveyor systems with AI-powered sortation algorithms designed to process increased passenger volumes following the airport's Terminal 3 expansion plans, though specific contract values remain undisclosed pending final regulatory approvals.

- September 2025: Dematic announced the expansion of its European service network with new maintenance hubs in Poland and the Czech Republic, targeting the growing installed base of automated conveyor systems in Eastern European manufacturing and logistics facilities, with investments focused on IIoT-enabled predictive maintenance capabilities to support the region's 8.98% CAGR growth trajectory through 2030.

- August 2025: Interroll launched its next-generation modular platform conveyor (MPC) series at LogiMAT 2025, featuring enhanced energy efficiency that reduces power consumption by 35% compared to previous models through optimized motor control and regenerative braking, addressing the European Union's Energy Efficiency Directive 2023/1791 mandates for 11.7% industrial energy reduction by 2030.

- July 2025: SSI Schaefer commissioned an automated distribution center for a major European pharmaceutical distributor in the Netherlands, integrating 2,200 meters of conveyor infrastructure with robotic picking systems to handle temperature-controlled medications, achieving throughput of 15,000 order lines per hour while maintaining GDP compliance for pharmaceutical logistics.

Europe Conveyors Market Report Scope

Conveyor systems are mechanical devices or assemblies that are used to transport various materials with little effort. There are different kinds of conveyor systems, usually consisting of a frame that supports either wheels, rollers, or a belt, upon which the materials move from one place to another. The scope of the study is currently focused exclusively on the European region.

The Europe Conveyors Market Report is Segmented by Product Type (Belt, Roller, Pallet, Overhead, Specialty), End-User Industry (Airport, E-Commerce and Retail, Automotive Manufacturing, General Manufacturing, Food and Beverage, Pharmaceuticals, Mining and Bulk-Handling), Load Type (Unit Load, Bulk Load), Automation Level (Manual, Semi-Automated, Fully Automated), Service (Installation, Preventive Maintenance, Predictive Maintenance), and Country (Western Europe, Northern Europe, Eastern Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Belt |

| Roller |

| Pallet |

| Overhead |

| Specialty (Spiral, Climbing, Sorting) |

By End-User Industry

| Airport |

| E-Commerce and Retail |

| Automotive Manufacturing |

| General Manufacturing |

| Food and Beverage |

| Pharmaceuticals |

| Mining and Bulk-Handling |

By Load Type

| Unit Load |

| Bulk Load |

By Automation Level

| Manual |

| Semi-Automated |

| Fully Automated / Smart Conveyors |

By Service

| Installation |

| Preventive Maintenance |

| Predictive / IIoT-Enabled Maintenance |

By Country

| Western Europe | United Kingdom |

| France | |

| Germany | |

| Italy | |

| Spain | |

| Northern Europe | Nordics |

| Benelux | |

| Eastern Europe | Poland |

| Czech Republic | |

| Rest of Eastern Europe |

| By Product Type | Belt | |

| Roller | ||

| Pallet | ||

| Overhead | ||

| Specialty (Spiral, Climbing, Sorting) | ||

| By End-User Industry | Airport | |

| E-Commerce and Retail | ||

| Automotive Manufacturing | ||

| General Manufacturing | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Mining and Bulk-Handling | ||

| By Load Type | Unit Load | |

| Bulk Load | ||

| By Automation Level | Manual | |

| Semi-Automated | ||

| Fully Automated / Smart Conveyors | ||

| By Service | Installation | |

| Preventive Maintenance | ||

| Predictive / IIoT-Enabled Maintenance | ||

| By Country | Western Europe | United Kingdom |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Northern Europe | Nordics | |

| Benelux | ||

| Eastern Europe | Poland | |

| Czech Republic | ||

| Rest of Eastern Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe conveyors market?

The market stands at USD 3.53 billion in 2026 and is expected to rise to USD 4.71 billion by 2031.

Which product category holds the largest share today?

Belt conveyors lead with 38.96% of 2025 revenue thanks to broad use in parcel and food applications.

Which end-user segment is growing the fastest?

E-commerce and retail installations are forecast to expand at 8.95% CAGR through 2031, outpacing airports and automotive plants.

Why are overhead conveyors gaining popularity?

They free floor space in paint shops and cleanrooms, support heavier loads, and meet contamination-control standards.

How are EU subsidies affecting investment decisions?

Grants covering up to 40% of automation capex under the Recovery and Resilience Facility shorten conveyor payback periods to under 2.5 years, accelerating procurement.

What role do predictive-maintenance contracts play?

IIoT-enabled service agreements now account for 28% of supplier aftermarket revenue, reducing unplanned downtime by up to 35%.

Page last updated on: