Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

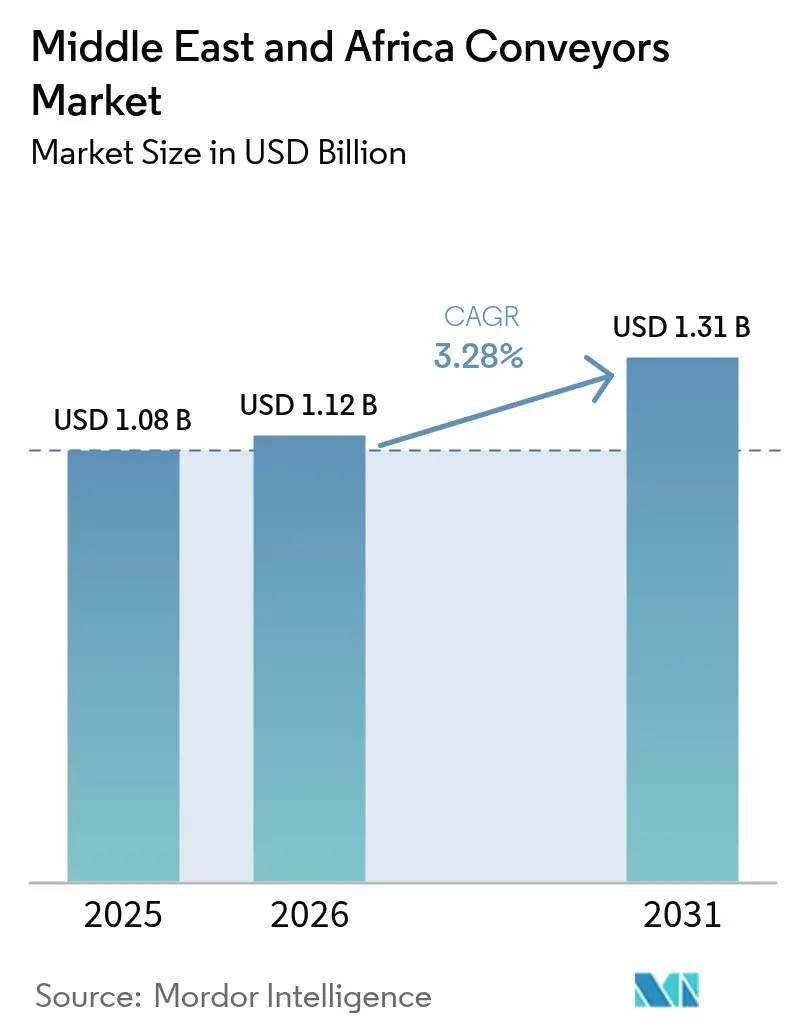

| Base Year Market Size (2025) | USD 1.08 Billion |

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

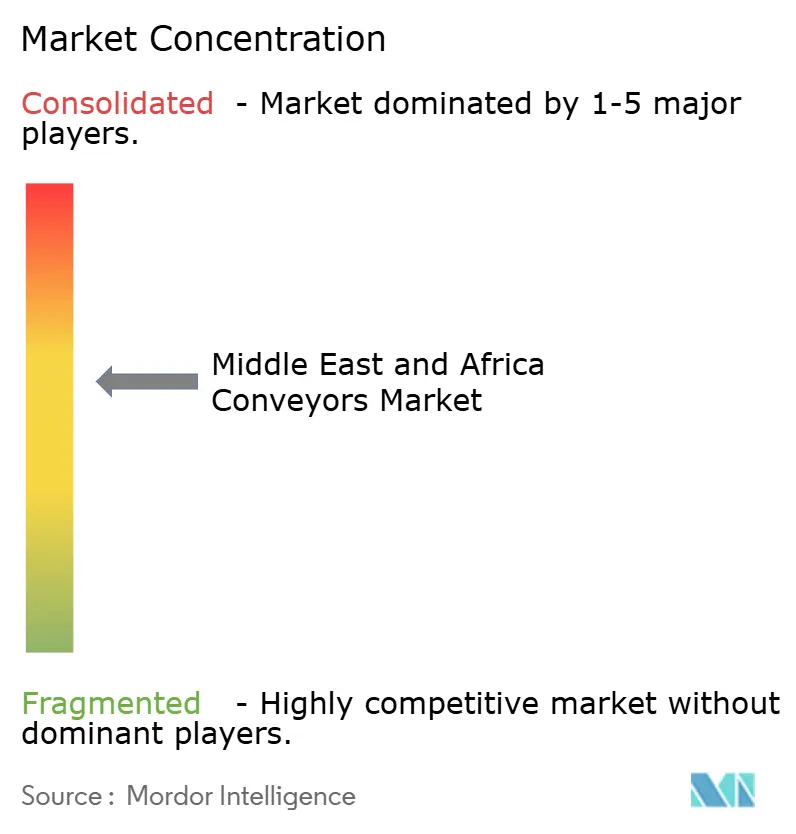

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Conveyors Market Analysis by Mordor Intelligence

The Middle East and Africa conveyors market size is expected to grow from USD 1.08 billion in 2025 to USD 1.12 billion in 2026 and is forecast to reach USD 1.31 billion by 2031 at 3.28% CAGR over 2026-2031. Expansion is aligned with sovereign infrastructure agendas, airport capacity additions, and e-commerce fulfillment build-outs, catalyzing steady equipment demand even as input-cost volatility and technician shortages temper the overall uptake. Robust pipeline activity across Saudi Arabia’s megaprojects and the United Arab Emirates’ logistics-hub strategy is driving equipment standardization toward energy-efficient, sensor-rich conveyor platforms that integrate easily with warehouse management software. At the same time, mining modernization in South Africa and Morocco is propelling large-scale belt installations, while quick-commerce players are embracing vertical conveyor solutions to maximize cubic space in urban settings. Global integrators are responding with modular designs and predictive-maintenance suites that cut unplanned downtime and sharpen the total cost-of-ownership value proposition.

Key Report Takeaways

- By product type, belt conveyors led with 48.12% of the Middle East and Africa conveyors market share in 2025, whereas overhead conveyors are forecast to advance at a 5.18% CAGR through 2031.

- By end-user, airport applications accounted for 34.85% of the Middle East and Africa conveyors market size in 2025, while retail and e-commerce segments are poised for the fastest 6.33% CAGR to 2031.

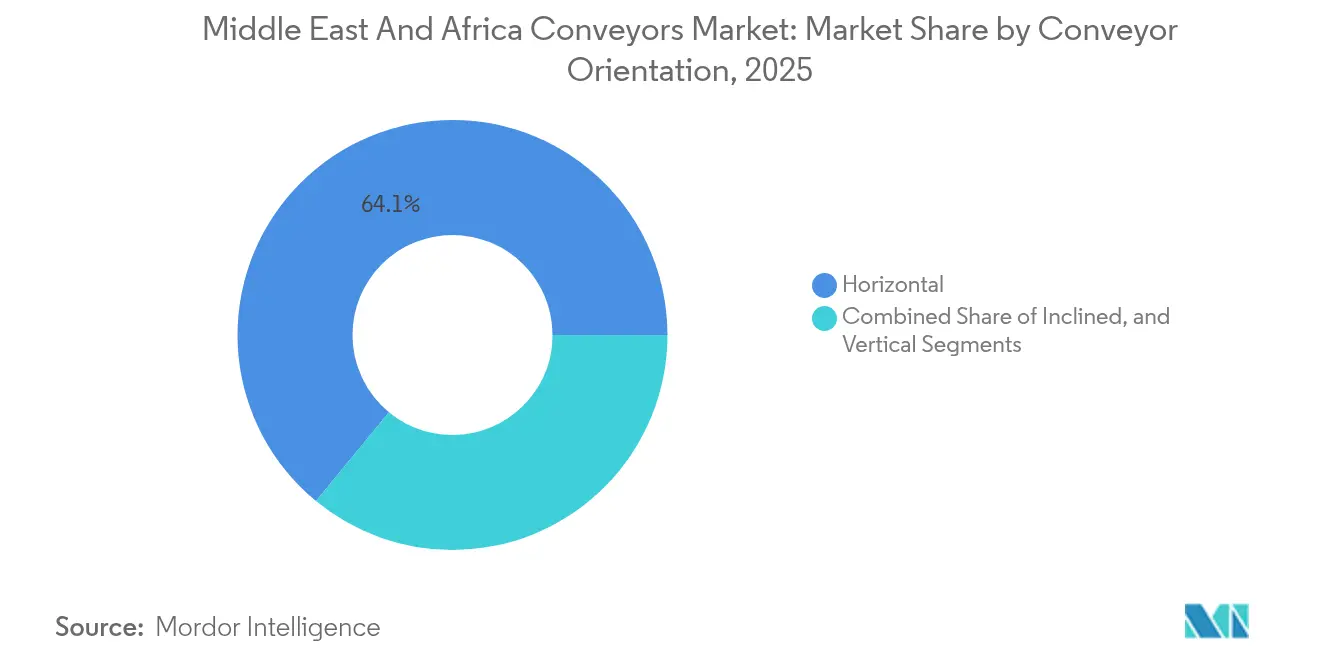

- By conveyor orientation, horizontal systems captured 64.05% share of the Middle East and Africa conveyors market size in 2025, and vertical conveyors will expand at a 6.52% CAGR through 2031.

- By conveyor location, floor-mounted captured 78.65% share of the Middle East and Africa conveyors market size in 2025, and vertical conveyors will expand at a 5.71% CAGR through 2031.

- By country, Saudi Arabia held 25.05% of the Middle East and Africa conveyors market share in 2025; the United Arab Emirates is set to record the highest 5.29% CAGR during 2026-2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Conveyors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of E-Commerce | +1.2% | UAE, Saudi Arabia, Egypt; spillover to Qatar and Kuwait | Medium term (2-4 years) |

| Rise of Infrastructure Megaprojects Across GCC | +1.0% | Saudi Arabia (NEOM, Qiddiya), UAE (Dubai South), Qatar | Long term (≥ 4 years) |

| Accelerating Warehouse Automation Investments by 3PLs | +0.8% | UAE, Saudi Arabia, South Africa; emerging in Egypt and Kenya | Short term (≤ 2 years) |

| Surge in Airport Baggage Handling System Upgrades | +0.7% | UAE (Dubai, Abu Dhabi), Saudi Arabia (Riyadh, Jeddah), Qatar (Doha), Egypt (Cairo) | Medium term (2-4 years) |

| Mining Sector Modernization in Africa | +0.5% | South Africa, Egypt, Morocco; nascent in Nigeria and Kenya | Long term (≥ 4 years) |

| Greenfield Electric-Vehicle Assembly Plants | +0.4% | Saudi Arabia, UAE, Egypt, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth Of E-Commerce

Online retail penetration in the UAE and Saudi Arabia rose to 15% of total sales in 2024, magnifying the gap between consumer demand and fulfillment capacity.[1]Swisslog, “Automation Solutions at Gulfood Manufacturing 2024,” swisslog.com Amazon’s 100,000-square-meter Riyadh facility and Noon’s 200,000-square-meter Dubai expansion both rely on modular belt, roller, and goods-to-person conveyors capable of processing more than 5,000 orders per hour in peak periods. Cross-border parcel inflows via Jebel Ali climbed 40% year over year, forcing 3PLs to deploy high-speed merge conveyors and automated customs sortation. Conveyors equipped with RFID readers and vision-guided diverters deliver 99.9% sort accuracy, ensuring compliance with same-day delivery promises. As fulfillment operators adopt multi-level mezzanines, conveyor intensity per square meter is rising, further amplifying demand for sensor-rich modular platforms that can be re-scaled quarterly rather than annually.

Rise Of Infrastructure Megaprojects Across GCC

Saudi Arabia’s USD 500 billion NEOM and USD 35 billion King Salman International Airport projects require more than 50 kilometers of aggregate, baggage, and construction conveyors engineered for 50 °C ambient temperatures and desert sandstorms. Similar large-scale developments in Dubai South and Qatar’s tourism corridors specify ISO 50001 energy management, catalyzing uptake of variable-frequency drives and regenerative braking. OEMs are building solar-ready power trains and offering hybrid electric-pneumatic drives to meet embodied-carbon reduction targets of up to 40%. Tender cycles that run through 2030 necessitate flexible local assembly capacity so suppliers avoid foreign-exchange swings and import-duty spikes. These projects cement long-term conveyor demand yet create lumpy order patterns that favor vendors with robust regional partnerships.

Accelerating Warehouse Automation Investments By 3PLs

Third-party logistics providers invested more than USD 1 billion in conveyor-centric warehouse automation between 2024 and 2025, a 60% jump from the previous biennium. CEVA Almajdouie Logistics plans to retrofit five Saudi distribution centers with conveyor-fed automated storage and retrieval systems by 2026, while Asyad’s acquisition of Skybridge Freight Solutions embeds conveyor platforms in a new Duqm Port distribution hub. Operators now view conveyors as data-generating assets that feed WMS dashboards with throughput metrics and predictive-maintenance alerts, slicing order cycle times by up to 30%. Demand is shifting toward Ethernet/IP-ready conveyors equipped with embedded sensors and OPC-UA gateways, a capability present in less than half of the installed base, signaling a sizable retrofit opportunity.

Surge In Airport Baggage-Handling System Upgrades

Dubai International, Al Maktoum International, and King Salman International airports collectively allocate USD 10 billion for next-generation baggage systems through 2030, each targeting 15,000 bags per hour per terminal. Specifications include RFID-enabled tracking, redundant loops for transfer passengers, and dynamic re-sort capabilities that inflate installed cost per linear meter by 40% compared with origin-destination layouts. Cairo International’s 8-kilometer belt upgrade cut mishandling by 35% within six months, demonstrating the operational payoff of standardized, sensor-rich conveyors. Integrators with proven hub-airport credentials remain well-positioned owing to complex routing algorithms and stringent IATA traceability standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure | -0.6% | Africa (South Africa, Egypt, Nigeria, Kenya); secondary impact in GCC for SME adopters | Short term (≤ 2 years) |

| Limited Skilled Maintenance Workforce | -0.4% | Sub-Saharan Africa (Nigeria, Kenya, Morocco); isolated GCC sites (Oman, Bahrain) | Medium term (2-4 years) |

| Volatile Raw Material Prices | -0.3% | Global, with acute impact on Africa due to currency depreciation and import dependency | Short term (≤ 2 years) |

| Fragmented OEM and After-Sales Network in Africa | -0.2% | Sub-Saharan Africa (Nigeria, Kenya, Rest of Africa); minimal impact in North Africa and GCC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure

Typical conveyor installations cost USD 800–2,500 per linear meter for standard belt and roller systems, escalating to USD 8,000 per meter for overhead power-and-free lines. African operators incur an extra 15–25% because of import duties and currency depreciation, stretching payback periods beyond five years for companies running on sub-10% EBITDA margins. Financing gaps persist as local banks offer limited equipment-leasing products, nudging SMEs toward low-cost gravity rollers or manual handling. OEMs that provide vendor financing and pay-per-use models are beginning to unlock the “missing-middle” segment representing nearly one-third of untapped demand.

Limited Skilled Maintenance Workforce

Vacancy rates for industrial maintenance roles exceed 20% in Nigeria, Kenya, and Morocco, forcing operators to fly in expatriate technicians at daily rates approaching USD 1,200 plus travel. Downtime penalties rise accordingly, eroding ROI for capital-intensive conveyor lines. In response, equipment makers are embedding remote diagnostics and augmented-reality troubleshooting that lowers mean-time-to-repair from eight hours to two. Kanoo Machinery’s partnership with Combilift incorporates a training academy targeting 500 certified technicians by 2026, illustrating how service contracts bundled with skills development can command premiums and reinforce brand loyalty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Overhead Conveyors Gain Traction In Space-Constrained Facilities

Belt conveyors represented 48.12% of the Middle East and Africa conveyors market in 2025, entrenched in mining, airport baggage, and food processing applications where load limits reach 500 kg per meter. Roller conveyors dominate carton and pallet flows in general manufacturing, while pallet conveyors serve heavy automotive sub-assemblies exceeding 1,000 kg. Overhead systems, although smaller in absolute terms, will post a 5.18% CAGR through 2031 as pharmaceutical clean rooms and multi-level automotive plants target contamination-free routing and floor-space optimization.

Interroll’s modular conveyor platform, installed across multiple UAE and Saudi fulfillment hubs in 2024, underscores the pivot toward plug-and-play sections that maintenance teams can reconfigure within four-hour windows, cutting total lifecycle costs by up to 25% . Overhead power-and-free lines are slated for Lucid Motors’ EV plant and Ceer’s Saudi assembly campus, where body panels must traverse painting, welding, and final-assembly zones without obstructing floor traffic. The embedded trend is a migration to sensor-enabled, IoT-ready platforms that allow predictive health monitoring and software-driven throughput optimization, aligning with regional mandates for ISO 50001 compliance.

By End-User Industry: Retail And E-Commerce Overtake Traditional Segments

Airport operators accounted for 34.85% of 2025 demand in the Middle East and Africa conveyors market, reflecting historic investment in hub-airport baggage infrastructure. Yet retail and e-commerce fulfillment centers will record the fastest 6.33% CAGR through 2031 as online penetration climbs and same-day delivery expectations spread from the GCC to Egypt and Kenya.

Food and beverage producers led by Almarai and Nestlé are retrofitting stainless-steel hygienic conveyors to satisfy HACCP protocols, raising average spend per facility by 40%. Meanwhile, pharmaceutical clean rooms demand overhead power-and-free systems engineered for FDA 21 CFR Part 11 traceability, driving per-meter costs to USD 10,000 but radically reducing contamination risk. The blurring of segment boundaries is evident as e-commerce operators adopt pharmaceutical-grade vision inspection for shrinkage control, while beverage plants install e-commerce-style tote conveyors for mixed-SKU kitting. Suppliers with cross-sector case studies hold a competitive edge as convergence accelerates.

By Conveyor Orientation: Vertical Systems Enable Cubic Utilization

Horizontal conveyors held 64.05% of 2025 installations, reflecting simple, single-level warehouse design norms relevance in the Middle East and Africa conveyors market. Inclined belts account for another 15-20% in truck-loading docks and multi-level plants. Vertical spiral and reciprocating lifts will grow at a 6.52% CAGR through 2031 as land prices in Jebel Ali and Riyadh industrial zones climbed 30% from 2022 to 2024.

Spiral conveyors occupy up to 30% less floor area than inclined belts for the same elevation change, making them attractive in clean rooms where square-meter construction costs surpass USD 5,000. They also serve as key interchange nodes for autonomous mobile robots, allowing three-dimensional goods flow that slashes horizontal travel distances by 50%. Integrated control architectures ensure seamless hand-offs between AMRs and vertical lifts, supporting lights-out fulfillment operations that raise picks per hour while curbing labor overhead.

By Conveyor Location: Overhead-Mounted Systems Capture Automotive And Pharma Growth

Floor-mounted conveyors made up 78.65% of 2025 deployments, favored for easy maintenance access in airports, mining, and general distribution. Overhead installations will expand at a 5.71% CAGR through 2031, driven by automotive paint shops, pharmaceutical packaging, and apparel fulfillment hubs demanding gravity-assisted accumulation and uncluttered aisles in the Middle East and Africa conveyors market.

Power-and-free variants facilitate buffer management, enabling carriers to pause at workstations without stalling the loop, thereby lifting overall equipment effectiveness by around 15 percentage points. Nestlé’s forthcoming 117,000-square-meter Jeddah facility will deploy overhead conveyors integrated with robotic palletizers and stretch wrappers, proof that overhead layouts now anchor Industry 4.0 factory floor design. As wage inflation averages 8–10% annually, fulfillment centers are also adopting overhead garment-on-hanger systems for apparel and overhead tote routes for small-parts picking to offset labor costs, giving OEMs further runway for technological differentiation.

Geography Analysis

Saudi Arabia contributed 25.05% of 2025 revenue, propelled by the conveyor-intensive NEOM and King Salman International Airport projects, both scheduled for major equipment awards between 2025 and 2027. Public Investment Fund backing assures financing resilience, although order flow will remain cyclical as mega-projects move from civil works to fit-out phases.

The United Arab Emirates, while starting from a smaller base, is forecast to have the highest 5.29% CAGR, underpinned by Dubai South’s airport expansion and the widening of Khalifa Port, which collectively double fulfillment square footage and stimulates conveyor demand in ground-handling and cross-docking facilities. AD Ports Group’s crane investments in Congo and Angola signal an outward push that will export UAE conveyor demand into Africa via EPC contracts overseen from Abu Dhabi.

South Africa anchors African bulk-material conveyor activity with multi-kilometer belt lines in gold and platinum operations. Egypt and Morocco add phosphate and cement flows, while Nigeria and Kenya show early signs of conveyor adoption in port and general manufacturing upgrades. Import duties and currency swings inflate landed costs by up to 30%, but local assembly partnerships and aftermarket hubs are emerging to counteract pricing pressure, setting the stage for gradual Middle East and Africa conveyors market formalization.

Competitive Landscape

Global integrators Daifuku, Swisslog, Siemens Logistics, and Vanderlande account for roughly half of large turnkey awards, leveraging sensor-rich platforms and multiyear service agreements that lock in software revenues. Regional distributors such as Melco Conveyor Equipment, CITCOnveyors, and Kanoo Machinery fill retrofit and mining niches through spare-parts proximity and customization for harsh environments. This dual-track ecosystem offers OEMs the opportunity to marry modular hardware with open-architecture analytics, building hybrid packages that resonate with both global 3PLs and mid-market manufacturers.

Autonomous mobile robot vendors like AutoStore and Geek+ are eroding pure-play conveyor footprints in 20-30% of new fulfillment centers, prompting conveyor makers to add AMR interfaces and develop mixed-mobility workflows that preserve share of wallet. Siemens’s decision to divest its airport logistics unit in early 2025 highlights ongoing portfolio realignment as integrators navigate margin compression and lengthening project cycles in the Middle East and Africa conveyors market.

Local content is emerging as a decisive edge in Africa: distributors who can stock critical spares and provide 24-hour on-site support capture premium contracts even when competing against bigger brands. Kanoo Machinery’s 2024 partnership with Combilift, encompassing a technician academy, typifies the blend of product, service, and training that fortifies customer stickiness in skill-scarce environments

Middle East And Africa Conveyors Industry Leaders

Daifuku Co. Ltd

SSI Schaefer AG

Mecalux SA

BEUMER Group GmbH and Co. KG

Swisslog Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CIMC TIANDA has officially launched in the Middle East market by appointing a regional Sales Director. Worldwide Supply Chain ME, Indicates an increasing requirement for intralogistics and automated conveyor systems in warehouses/distribution centers across the Middle East

- March 2025: Messe Frankfurt’s Materials Handling Saudi Arabia showcased next-generation belt, overhead, and vertical conveyors engineered for 50 °C ambient temperatures, underscoring strong order pipelines tied to GCC megaproject build-outs.

- March 2025: Swisslog debuted an upgraded AutoStore-plus-conveyor solution at Saudi Food Manufacturing Expo 2025, positioning the platform for three-level mezzanine fulfillment centers that demand 5,000-order-per-hour peak throughput.

- January 2025: Siemens AG reached an agreement to sell its airport logistics business for EUR 300 million (USD 320 million), reallocating capital toward sensor-rich digital conveyor platforms and altering the competitive field for baggage-handling projects.

Middle East And Africa Conveyors Market Report Scope

Conveyor systems are mechanical devices or assemblies that are used to transport various materials with little effort. There are different kinds of conveyor systems, usually consisting of a frame that supports either wheels, rollers, or a belt, upon which the materials move from one place to another. The scope of the study is currently focused exclusively on the Middle East and African region.

The Middle East and Africa Conveyors Market Report is Segmented by Product Type (Belt Conveyors, Roller Conveyors, Pallet Conveyors, Overhead Conveyors, Screw Conveyors, Chain Conveyors), End-User Industry (Airport, Retail and E-Commerce, Automotive, General Manufacturing, Food and Beverage, Pharmaceuticals, Mining and Minerals), Conveyor Orientation (Horizontal, Inclined, Vertical), Conveyor Location (Floor-Mounted, Overhead-Mounted), and Geography (UAE, Saudi Arabia, Qatar, Oman, Kuwait, Bahrain, Turkey, Israel, South Africa, Egypt, Nigeria, Kenya, Morocco). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Belt Conveyors |

| Roller Conveyors |

| Pallet Conveyors |

| Overhead Conveyors |

| Screw Conveyors |

| Chain Conveyors |

By End-User Industry

| Airport |

| Retail and E-Commerce |

| Automotive |

| General Manufacturing |

| Food and Beverage |

| Pharmaceuticals |

| Mining and Minerals |

By Conveyor Orientation

| Horizontal |

| Inclined |

| Vertical |

By Conveyor Location

| Floor-Mounted |

| Overhead-Mounted |

By Country

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Morocco | |

| Rest of Africa |

| By Product Type | Belt Conveyors | |

| Roller Conveyors | ||

| Pallet Conveyors | ||

| Overhead Conveyors | ||

| Screw Conveyors | ||

| Chain Conveyors | ||

| By End-User Industry | Airport | |

| Retail and E-Commerce | ||

| Automotive | ||

| General Manufacturing | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Mining and Minerals | ||

| By Conveyor Orientation | Horizontal | |

| Inclined | ||

| Vertical | ||

| By Conveyor Location | Floor-Mounted | |

| Overhead-Mounted | ||

| By Country | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Qatar | ||

| Oman | ||

| Kuwait | ||

| Bahrain | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Middle East and Africa conveyors market in 2026?

The market is valued at USD 1.12 billion in 2026, with steady growth forecast through 2031.

What CAGR is expected through 2031 for conveyor sales in the region?

The market is projected to expand at 3.28% per year from 2026 to 2031.

Which country will grow fastest in conveyor demand?

The United Arab Emirates is anticipated to post the highest 5.29% CAGR, propelled by logistics-hub investments.

Which segment is expanding most rapidly?

Retail and e-commerce fulfillment centers are set for a 6.33% CAGR as online shopping penetration accelerates.

Why are vertical conveyors becoming more popular?

Rising urban land prices make multi-level warehouses economical, and vertical lifts enable cubic storage without enlarging footprints.

What is the main challenge for conveyor operators in Africa?

A shortage of skilled maintenance technicians increases downtime and service costs, prompting OEMs to embed remote diagnostics and local training programs.

Page last updated on: