Baked Goods Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

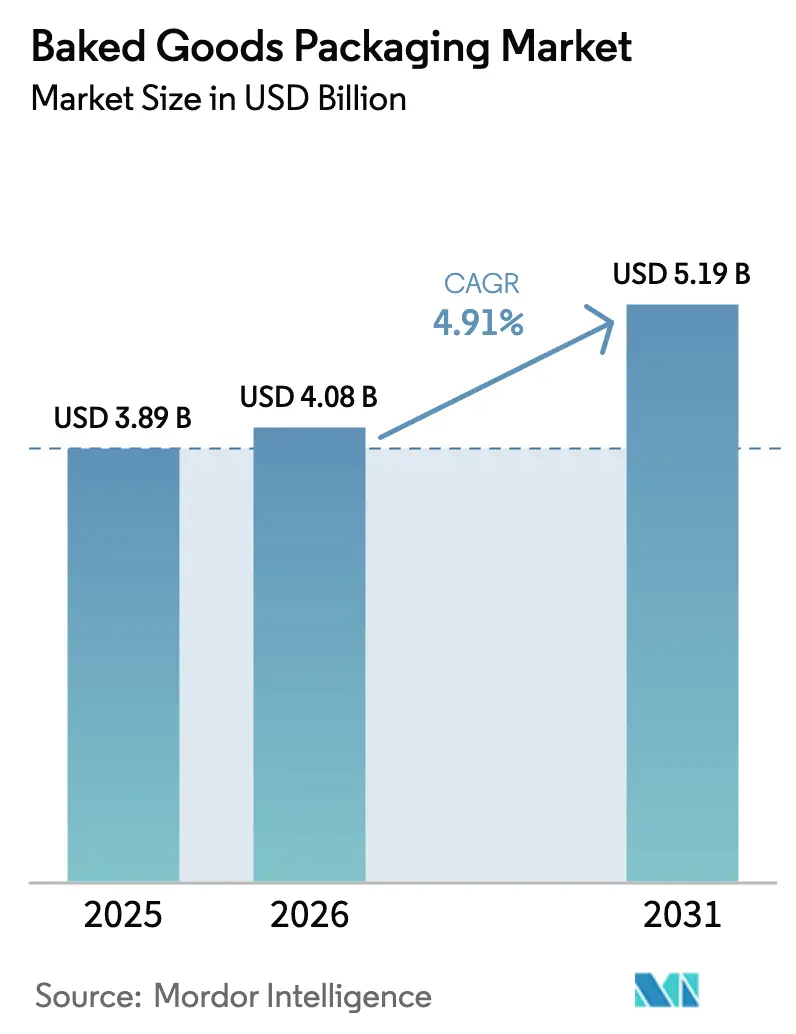

| Market Size (2026) | USD 4.08 Billion |

| Market Size (2031) | USD 5.19 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

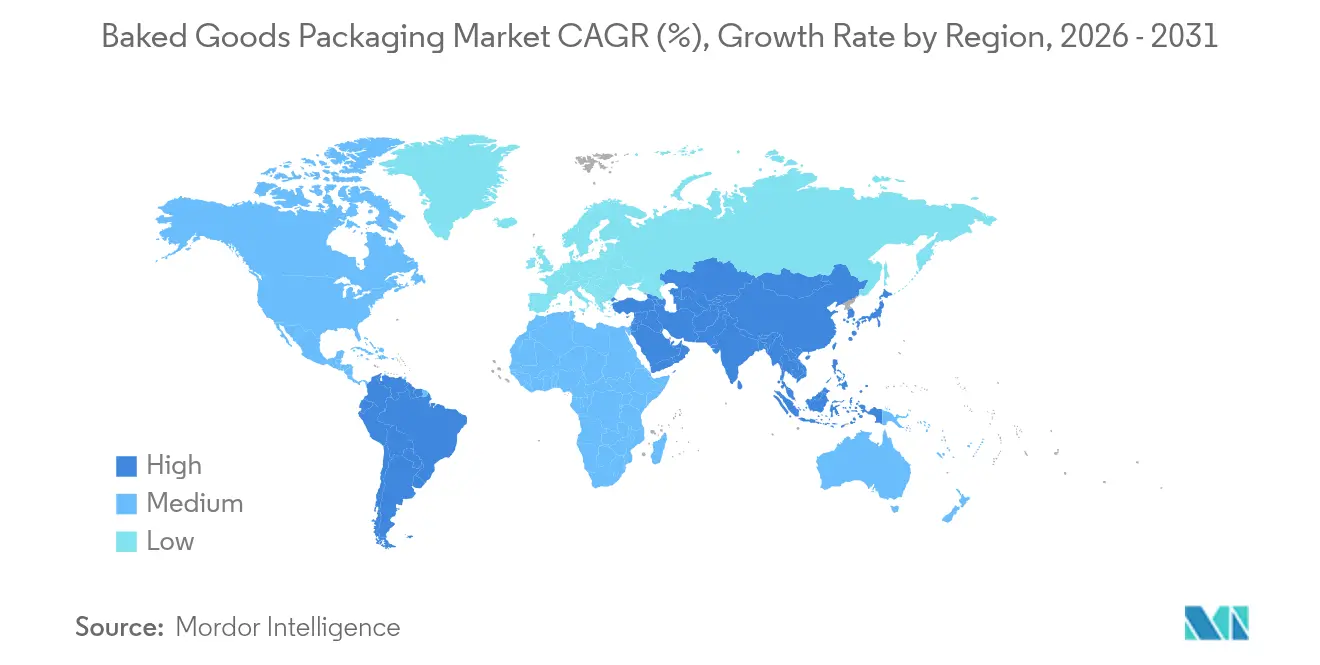

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baked Goods Packaging Market Analysis by Mordor Intelligence

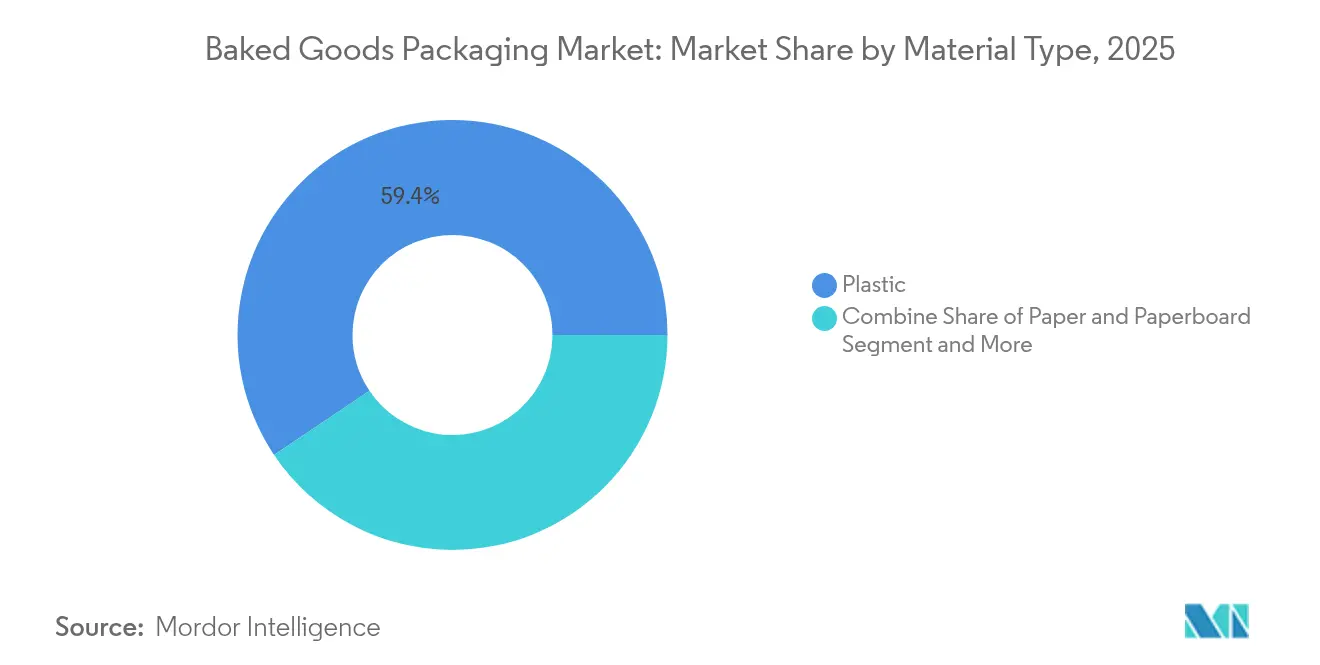

The baked goods packaging market size was valued at USD 3.89 billion in 2025 and estimated to grow from USD 4.08 billion in 2026 to reach USD 5.19 billion by 2031, at a CAGR of 4.91% during the forecast period (2026-2031). Rising e-commerce volumes, stringent sustainability mandates and innovations in shelf-life-extending technologies are together sustaining robust demand for packaging that protects product quality, reduces waste and complies with tightening regulations. North America leads with 32.53% revenue share in 2024, supported by mature retail logistics and early adoption of intelligent packaging, while Asia-Pacific records the fastest trajectory at 6.56% CAGR through 2030 as urban consumers adopt packaged bakery products. Plastic remains the dominant substrate with 60.12% share, yet paper and paperboard post the strongest 6.74% CAGR as brand owners migrate to recyclable formats under Extended Producer Responsibility rules. Flexible formats account for 54.35% of volumes, reflecting cost-efficient barrier properties that meet the freshness requirements of bread, cookies and pastries. Competitive intensity is moderate: Amcor, Mondi and Huhtamaki combine vertical integration with R&D scale, but mid-tier players are gaining share through niche sustainable materials and smart-label solutions aimed at direct-to-consumer bakery shipping.

Key Report Takeaways

- By material type, plastic retained 59.42% of baked goods packaging market share in 2025, while paper and paperboard are forecast to expand at a 6.65% CAGR through 2031.

- By packaging type, flexible formats contributed 53.78% revenue in 2025; rigid formats exhibit a slower 3.15% CAGR outlook to 2031.

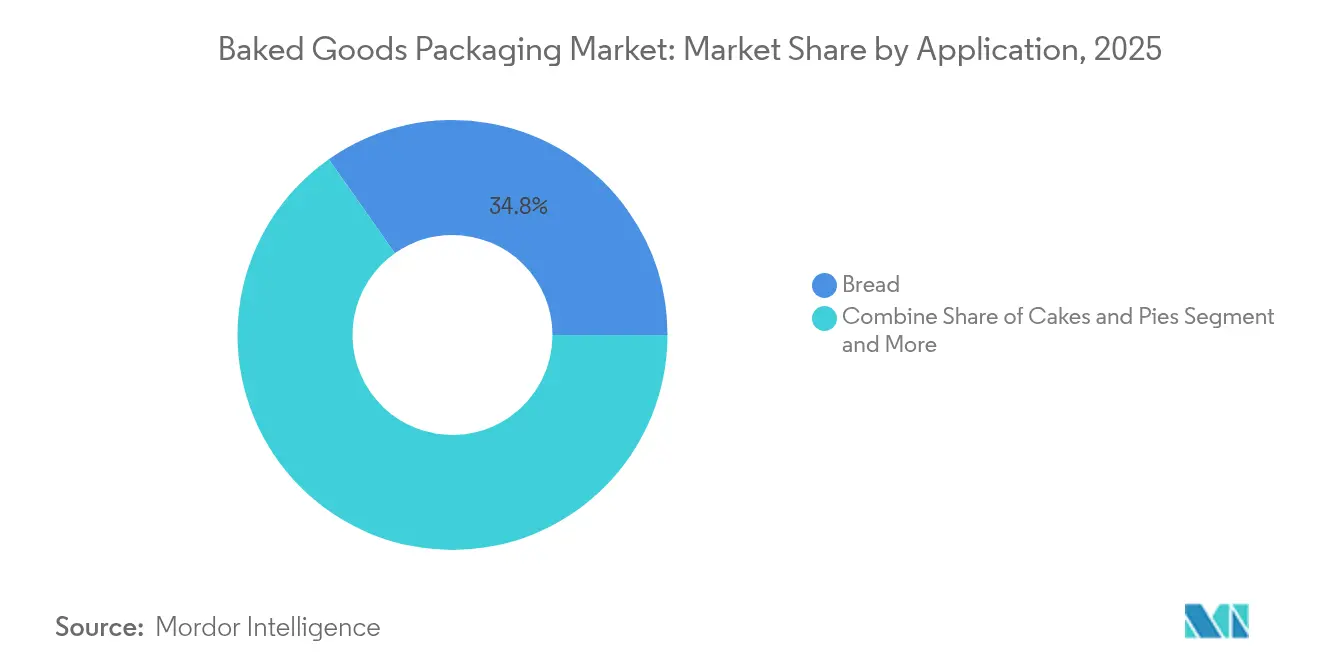

- By application, bread commanded 34.76% of the baked goods packaging market size in 2025; cookies and crackers are projected to grow at 7.21% CAGR during 2026-2031.

- By packaging technology, modified-atmosphere packaging held 29.66% share in 2025, whereas active and oxygen-scavenger systems are predicted to rise at 7.89% CAGR to 2031.

- By geography, North America led with 32.11% revenue share in 2025, and Asia-Pacific is poised for the fastest 6.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baked Goods Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global consumption of bakery products | +1.2% | Global, with strongest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Convenience-food demand spurring packaged formats | +0.8% | North America & Europe, expanding to urban APAC | Short term (≤ 2 years) |

| Shift toward sustainable and recyclable materials | +0.6% | Europe leading, North America following, APAC emerging | Long term (≥ 4 years) |

| Growth of e-commerce and D2C bakery shipping | +0.5% | Global, with early gains in North America, Europe, urban Asia | Medium term (2-4 years) |

| Active and MAP technologies extending shelf-life | +0.4% | North America & Europe core, spill-over to APAC | Medium term (2-4 years) |

| Adoption of digital printing for SKU proliferation | +0.3% | Global, with fastest adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Consumption of Bakery Products

Urbanization and income gains are elevating daily bread and pastry intake, particularly in Asia-Pacific where bakery product consumption climbed 12% between 2022 and 2024. [1] AIPIA, “News on Smart, Active & Intelligent Packaging,” aipia.info Individual packs with high-barrier films are now essential for tropical climates lacking robust cold chains. Portion-controlled pouches tailored for single breakfasts and school snacks also enable wider retail reach, amplifying volumes for local converters. Multinational bakers are standardizing pack designs across regions to simplify sourcing and contain costs while meeting divergent shelf-life needs.

Convenience-Food Demand Spurring Packaged Formats

On-the-go lifestyles have accelerated demand for resealable, easy-open bakery packs that preserve freshness after first use. Hybrid laminates incorporating peelable seals and micro-perforations help maintain crisp texture in croissants and baguettes kept on office desks. Digital printing supports short runs and rapid SKU rotation, allowing brands to launch limited-edition flavors without large inventory risk. Direct-to-consumer models rely on robust secondary cartons and insulated liners, enabling frozen sourdough delivery nationwide without compromising crust or crumb integrity.

Shift Toward Sustainable and Recyclable Materials

European Union rules mandating recyclability by 2030 are pushing rapid migration from multilayer plastics toward barrier papers coated with bio-based polymers. Companies are re-engineering pack formats to eliminate hard-to-separate layers, adopting mono-material polyethylene films compatible with existing recycling streams. Early movers are capturing shelf space by displaying eco-labels that resonate with shoppers seeking low-impact snacks. Brands piloting fiber-based trays for mini-cakes report 15% material savings and reduced landfill fees.

Growth of E-commerce and D2C Bakery Shipping

Online grocery and bakery websites require packaging that withstands vibration, stacking and temperature swings. Multi-layer pouches with ethylene scavengers keep artisanal rolls fresh for 72 hours transit. Several US bakeries now employ cobot-enabled lines that auto-bag and case-pack 300 loaves per minute, offsetting labor gaps and ensuring shipment accuracy. Unboxing experiences that reveal premium foil-embossed liners help justify subscription pricing and build repeat orders, reinforcing the baked goods packaging market’s omnichannel momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polymer and paper pulp prices | -0.7% | Global, with strongest impact in price-sensitive markets | Short term (≤ 2 years) |

| Stringent PFAS and plastic taxation policies | -0.5% | Europe & North America leading, global expansion expected | Medium term (2-4 years) |

| Labor shortages driving packaging-line capex | -0.4% | North America & Europe core, emerging in developed APAC | Medium term (2-4 years) |

| Rising counterfeit flexible pouches harming brand equity | -0.3% | Global, with concentration in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polymer and Paper Pulp Prices

Oil-linked resin costs and weather-driven pulp shortages tighten converter margins. Contract lags hinder immediate price pass-through, prompting producers to lightweight structures or down-spec closures to stay competitive. Capacity closures totaling 500,000 tons of paper in North America illustrate the shift toward profit-focused production.[2]Smurfit Westrock, “Smurfit Westrock Reports First Quarter 2025 Results,” smurfitwestrock.com Buyers with long-term agreements and dual-sourcing strategies mitigate supply risk but face higher inventory financing.

Stringent PFAS and Plastic Taxation Policies

US and EU moves to phase out PFAS coatings by 2025 force rapid R&D into alternative barriers such as aqueous dispersions. The transition raises unit costs 6-10% yet opens branding opportunities around clean labels. Parallel plastic taxes of up to EUR 800 per ton on non-recycled content accelerate interest in compostable films, though home-compost certification remains limited. Pack converters that qualify early for food-contact safety retain key accounts while late adopters risk delistings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Gains Ground Despite Plastic Dominance

Plastic retained 59.42% revenue in 2025 owing to proven moisture and oxygen barriers essential for high-volume bread lines. However, paper and paperboard grew fastest at 6.65% CAGR as retailers expanded recyclable private-label SKUs. The baked goods packaging market size for paper solutions is expected to top USD 1.32 billion by 2031, aided by barrier-paper sandwiches that meet grease-resistance demands without fluorochemicals. Europe’s exemption of paper from recycled-content quotas gives it a regulatory edge. Producers are investing in extrusion-coated kraft grades that run on existing form-fill-seal lines, minimizing capital outlays for bakers. Bio-based plastics hold niche appeal for premium cookies but face scale and cost barriers. Metal tins persist in holiday gift assortments, offering 18-month shelf-life and collectible value.

Sustainability scorecards at global retailers now attach monetary bonuses for suppliers shifting volume from multilayer PE/PA to mono-PP or paper wraps. Nordic producers reported 9% sales uplift after swapping to windowed kraft bags that showcase crust color. Investors anticipate that baked goods packaging market share for fiber-based options will expand further once aqueous coatings achieve parity with EVOH in oxygen transmission. Converters are therefore partnering with chemical firms to commercialize cellulose-based barriers that enable full curb-side recyclability.

By Packaging Type: Flexible Solutions Maintain Leadership

Flexible pouches and bags accounted for 53.78% of 2025 shipments, a lead driven by lower material per gram of bread versus clamshells. Lightweighting strategies removed 3,200 tons of resin from North American supply chains last year, saving USD 6 million in freight. The baked goods packaging market size for flexible formats is predicted to reach USD 3.06 billion by 2031. Polyester-based laminates dominate high-speed pillow packs, while mono-polyethylene structures gain share in rollstock for automatic slicing lines. Reclosable zippers and laser perforation improve consumer convenience, extending product life by two days on average.

Rigid options such as PET domes cater to decorated cakes where visual presentation commands price premiums. Corrugated sleeves with die-cut windows now surround premium panettone, merging structural strength and shelf appeal. Glass jars have re-emerged for artisanal biscotti in gift channels, but their weight limits e-commerce adoption. RFID-enabled labels compatible with PET recycling streams demonstrate how smart features can dovetail with circularity goals. Such advances reinforce flexible packaging’s supremacy while keeping an eye on traceability.

By Application: Cookies and Crackers Drive Growth

Bread applications delivered 34.76% revenue in 2025, reflecting daily household consumption and supermarket dominance. Mass bakers standardize PE/PP coextrusions that seal below 140 °C to accelerate line speeds. Cookies and crackers are projected to lead incremental growth at 7.21% CAGR as consumers snack between meals and seek resealable trays preventing moisture pick-up. Unit packs of 100 kcal crackers support calorie-control programs, and kraft/carton hybrids help premium brands justify shelf premiums. This dynamic pushes converters to design high-opacity gusseted bags that protect chocolate-coated biscuits from light-induced bloom.

Cakes and pies exhibit steady seasonal demand linked to celebrations, relying on windowed folding cartons with internal PET barriers. Pastries such as croissants and Danish rolls see urban-café demand, adopting metallized OPP to arrest rancidity in butter-rich fillings. Specialty baked goods, including gluten-free brioche and ethnic sweet buns, create micro-niches requiring custom barrier profiles and multilingual graphics. The baked goods packaging market share of cookies and crackers is expected to surpass 18.35% by 2031 as new flavor launches proliferate.

By Packaging Technology: Active Solutions Accelerate

Modified-atmosphere packs held 29.66% share in 2025, favored for pan bread and tortilla lines where nitrogen flush extends mold-free life to 14 days. Yet active oxygen-scavenging sachets are forecast to grow 7.89% CAGR, appealing to clean-label bakers avoiding calcium propionate. The baked goods packaging market size attributable to active solutions could exceed USD 972 million by 2031. Integration of ethanol emitters in crusty rolls maintains organoleptic quality without altering moisture content. IoT-enabled biosensors now detect real-time CO₂ rise signaling spoilage, a breakthrough discussed in recent food-safety research.

Vacuum technology continues in par-baked baguettes for foodservice, where 25-day chilled life offsets daily labor. Edible films from potato starch remain pilot scale but promise zero-waste propositions for bite-sized muffins. Converter alliances with biotech firms are accelerating enzyme-embedded coatings that neutralize mold spores, fitting premium organic positions. Equipment OEMs are bundling gas-mix analyzers with form-fill-seal lines to guarantee package integrity, reinforcing technology adoption.

Geography Analysis

North America generated 32.11% of 2025 revenue, underpinned by high per-capita bread intake and entrenched mass-production infrastructure. Supermarket private brands account for increasing shelf presence, demanding cost-effective yet visually differentiated packs that meet evolving PFAS restrictions. Regional converters invest in robotics to counter labor shortages, achieving 20% throughput gains and enabling same-day fulfillment for online grocers. Smart-label pilots tracking temperature excursions from bakery to doorstep further strengthen demand for intelligent solutions.

Europe follows closely, distinguished by pioneering circular-economy regulations that drive rapid transition to mono-material laminates and fiber-based trays. Retailers impose strict recyclability scorecards, prompting suppliers to certify packs under local collection schemes. Governments incentivize research into compostable coatings, accelerating commercialization of bio-attributed PE that carries lower carbon intensity. German bakeries lead in laser-perforated bread bags allowing controlled moisture release, cutting food waste by 8% in trials.

Asia-Pacific posts the fastest 6.47% CAGR, fueled by urban population growth and westernized breakfast habits. Multinational bakers erect greenfield plants with high-speed sliced-bread lines, importing shelf-life know-how to manage humid climates. Domestic converters transition from generic OPP bags to high-clarity laminates featuring QR codes that authenticate product origin and build trust amid food-safety concerns. Governments in Japan and South Korea fund R&D into cellulose-nanofiber barriers, positioning local firms at the forefront of bio-material innovation. Southeast Asian e-commerce penetration expands regional parcel volumes, forcing packs to balance barrier needs with transport durability.

Latin America records steady mid-single-digit expansion. Economic recovery supports premium cookie imports packaged in BNOPP-metallized films resistant to tropical humidity. Regional SMEs adopt low-cost MAP sachets to extend shelf life from 5 to 12 days, unlocking interstate distribution. Meanwhile, Middle East and Africa remain nascent, with growth tempered by cold-chain gaps and fluctuating disposable income. Nevertheless, investment in industrial bakeries across the Gulf Cooperation Council is spawning demand for multilayer pillow packs able to endure high ambient temperatures.

Competitive Landscape

The baked goods packaging market is fragmented. Top players—Amcor, Mondi and Huhtamaki—hold 18.7% combined revenue, leveraging integrated resin procurement, proprietary coating chemistries and geographically dispersed plants. Strategic focus centers on developing recyclable mono-materials and aligning with global retailers’ plastic reduction targets. Recent patent filings reveal heat-resistant paper laminates that withstand 180 °C bakery tunnel ovens, offering seamless pack-and-bake functionality.

Consolidation among paper majors is reshaping scale economics. International Paper closed a USD 7.2 billion takeover of DS Smith, creating a heavyweight in corrugated solutions suitable for secondary shipping cartons. Simultaneously, Smurfit WestRock’s combination valued at USD 11.2 billion yields global fiber-based capacity, enabling synchronized roll-outs of barrier-coated boards across continents. These mergers enhance bargaining power with grocery chains seeking simplified, region-wide sourcing.

Mid-tier innovators are capturing growth niches. Graphic Packaging is scaling renewable-content cartons for cakes, reporting record USD 2.1 billion Q1 2025 revenue. [3]Graphic Packaging, “Graphic Packaging Holding Company to Host First Quarter 2025 Earnings Conference Call,” investors.graphicpkg.comAvery Dennison introduced an RFID label compatible with PET recycling, easing track-and-trace for snack packs. Technology vendors such as Oxipital supply AI-vision systems that detect seal faults at 800 ppm, slashing waste and reinforcing brand integrity. Private equity interest is growing in specialty coating firms developing PFAS-free water barriers, underscoring the premium commanded by ESG-compliant capabilities.

Competitive tactics revolve around automation, sustainability commitments and customer co-creation. Amcor’s lifecycle-analysis service quantifies carbon savings for clients switching to ultra-thin BOPE film, deepening strategic partnerships. Mondi pilots blockchain-verified paper sources, satisfying provenance audits for European retailers. Huhtamaki invests in long-term power-purchase agreements that deliver 100% renewable electricity to its North American sites, lowering Scope 2 emissions and aligning with bakery customers’ targets. These moves reinforce differentiation beyond price, anchoring long-term contracts in the baked goods packaging market.

Baked Goods Packaging Industry Leaders

Huhtamaki Oyj

Mondi Plc

Smurfit Westrock

Amcor Plc

International Paper Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Smurfit Westrock closed 500,000 tons of paper capacity and unveiled investments in high-efficiency converting plants in Washington and Wisconsin.

- January 2025: International Paper completed its acquisition of DS Smith, creating a global leader in sustainable packaging solutions with projected USD 514 million annual synergies.

- May 2024: Aspire Bakeries outlined Science-Based Targets for carbon reduction and higher recycled content in packaging.

- April 2024: Lotus Bakeries pledged 100% recyclable packaging by end-2025, eliminating 555 tons of material in 2023.

Global Baked Goods Packaging Market Report Scope

Baked goods packaging serves two primary purposes: preserving product freshness and facilitating easy transportation. Given bread's relatively short consumption timeframe, various materials, including paper, bags, cloth wraps, and boxes, are suitable for these purposes. This study analyzes market demand by tracking revenue generated from packaging designed for baked goods.

The Baked Goods Packaging Market is Segmented by Material Type (Plastic, Paper), Packaging Type (Flexible, Rigid), Application (Cakes, Pies, Pastries, Bread, Cookies and Crackers, Other Applications), Geography (North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

| Plastic |

| Paper and Paperboard |

| Metal |

| Other Material Types |

| Flexible |

| Rigid |

| Bread |

| Cakes and Pies |

| Pastries |

| Cookies and Crackers |

| Other Applications |

| Modified-Atmosphere (MAP) |

| Active/Oxygen-scavenger |

| Vacuum |

| Edible and Dissolvable Films |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Plastic | ||

| Paper and Paperboard | |||

| Metal | |||

| Other Material Types | |||

| By Packaging Type | Flexible | ||

| Rigid | |||

| By Application | Bread | ||

| Cakes and Pies | |||

| Pastries | |||

| Cookies and Crackers | |||

| Other Applications | |||

| By Packaging Technology | Modified-Atmosphere (MAP) | ||

| Active/Oxygen-scavenger | |||

| Vacuum | |||

| Edible and Dissolvable Films | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the baked goods packaging market?

The baked goods packaging market is worth USD 4.08 billion in 2026 and is projected to reach USD 5.19 billion by 2031.

Which region is growing fastest for baked goods packaging?

Asia-Pacific is forecast to rise at a 6.47% CAGR through 2031 due to urbanization and rising disposable incomes.

Why are flexible packages preferred in bakery applications?

Flexible films offer lower material usage, strong barrier properties and cost-efficient transport, giving them 53.78% market share in 2025.

How are sustainability regulations shaping material choices?

EU and US rules phasing out PFAS and taxing virgin plastic are steering converters toward paper, mono-material PE and bio-based coatings.

What technology is gaining traction beyond modified-atmosphere packaging?

Active oxygen-scavenger systems are expanding at 7.89% CAGR as brands pursue preservative-free shelf-life extension.

Who are the leading companies in baked goods packaging?

Amcor, Mondi and Huhtamaki lead the field, followed by consolidating paper giants such as Smurfit WestRock and International Paper.

Page last updated on: