Micro-Perforated Food Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

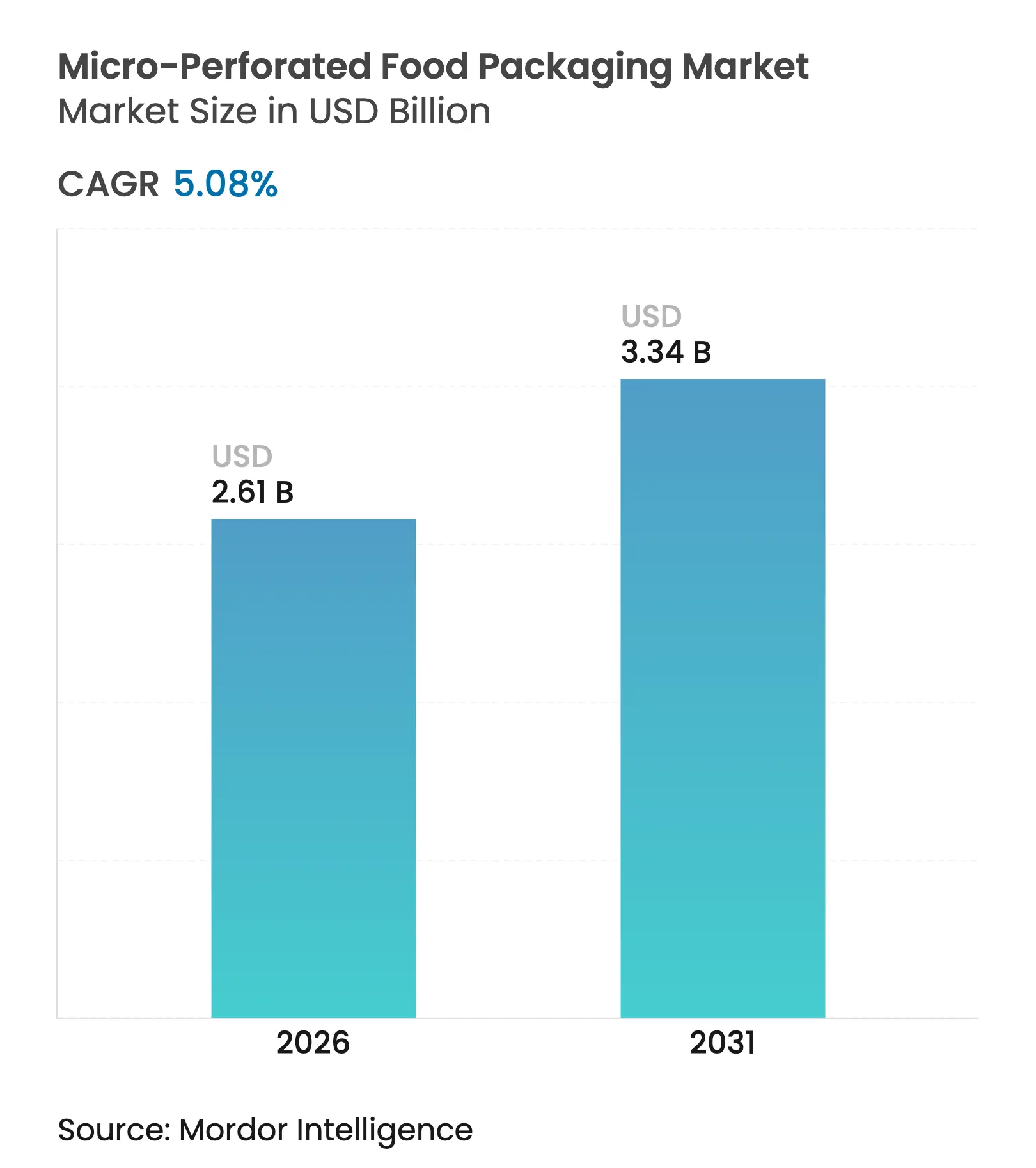

| Market Size (2026) | USD 2.61 Billion |

| Market Size (2031) | USD 3.34 Billion |

| Growth Rate (2026 - 2031) | 5.08 % CAGR |

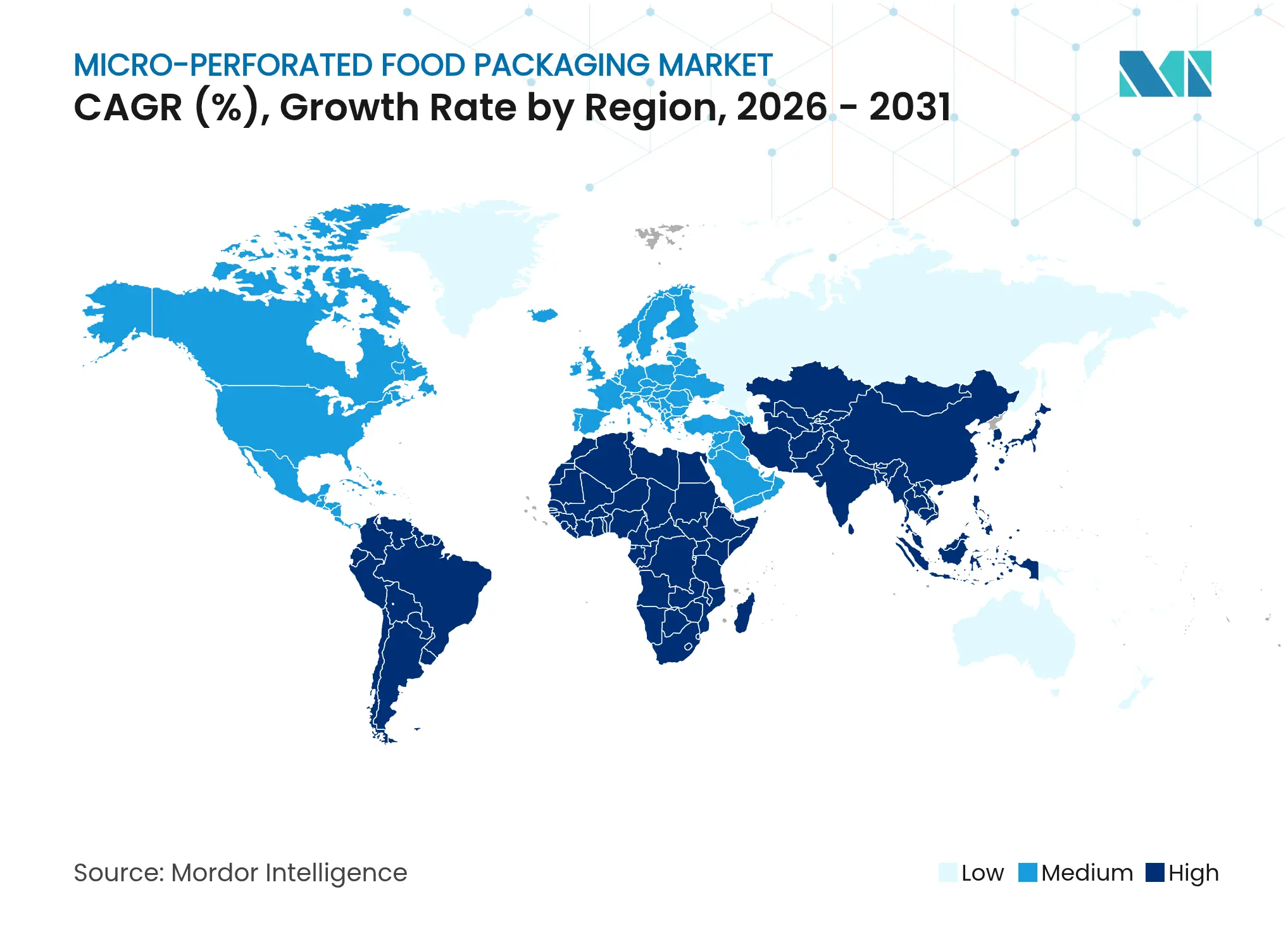

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

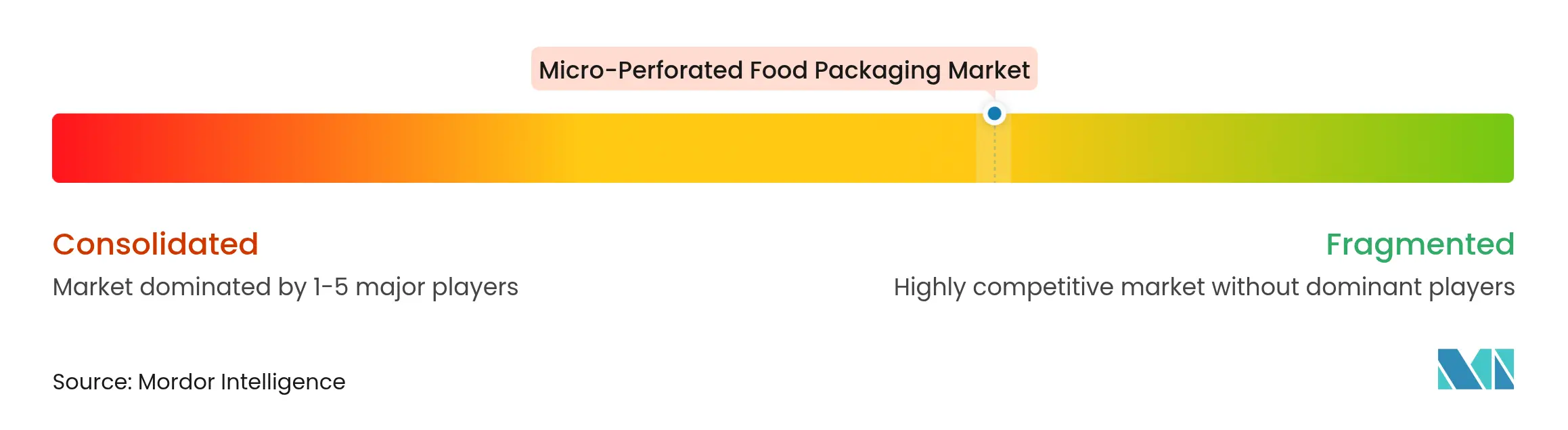

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Micro-Perforated Food Packaging Market Analysis by Mordor Intelligence

The micro-perforated food packaging market size is expected to grow from USD 2.48 billion in 2025 to USD 2.61 billion in 2026 and is forecast to reach USD 3.34 billion by 2031 at 5.08% CAGR over 2026-2031. Rising sustainability mandates, AI-enabled laser perforation, and consumer demand for longer shelf life fresh produce are the primary growth engines. Polyethylene remains the go-to substrate thanks to its proven performance and established conversion infrastructure, yet biodegradable films are gaining ground as brands prepare for recycled-content targets. E-commerce grocery expansion fuels interest in rugged flow-wraps and pouches, while AI-controlled oxygen-transmission-rate (OTR) systems fine-tune perforation patterns in real time and reduce shrink. Regionally, North America leads on account of stringent food safety rules and mature cold chains, whereas Asia-Pacific emerges as the fastest-growing arena, propelled by rising middle-class incomes and food-waste-reduction policies. Competitive intensity is rising after Amcor’s USD 8.43 billion merger with Berry Global, which consolidated R&D firepower and widened the technology moat.

Key Report Takeaways

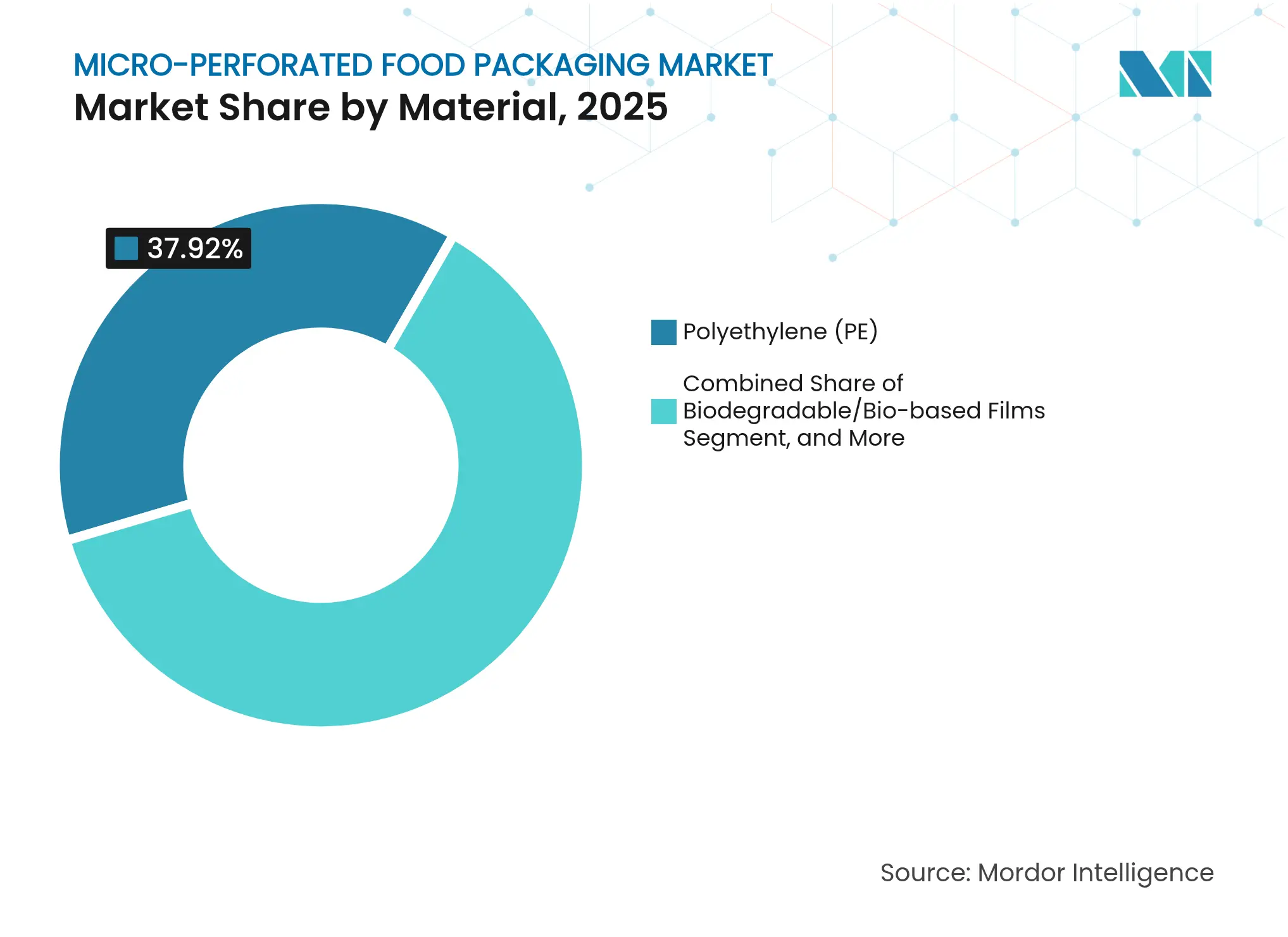

- By material, polyethylene held 37.92% of micro-perforated food packaging market share in 2025, while biodegradable films are projected to expand at an 8.05% CAGR to 2031.

- By packaging type, bags and wickets led with 44.73% revenue share in 2025; flow-wraps and pouches are forecast to post the fastest 7.23% CAGR through 2031.

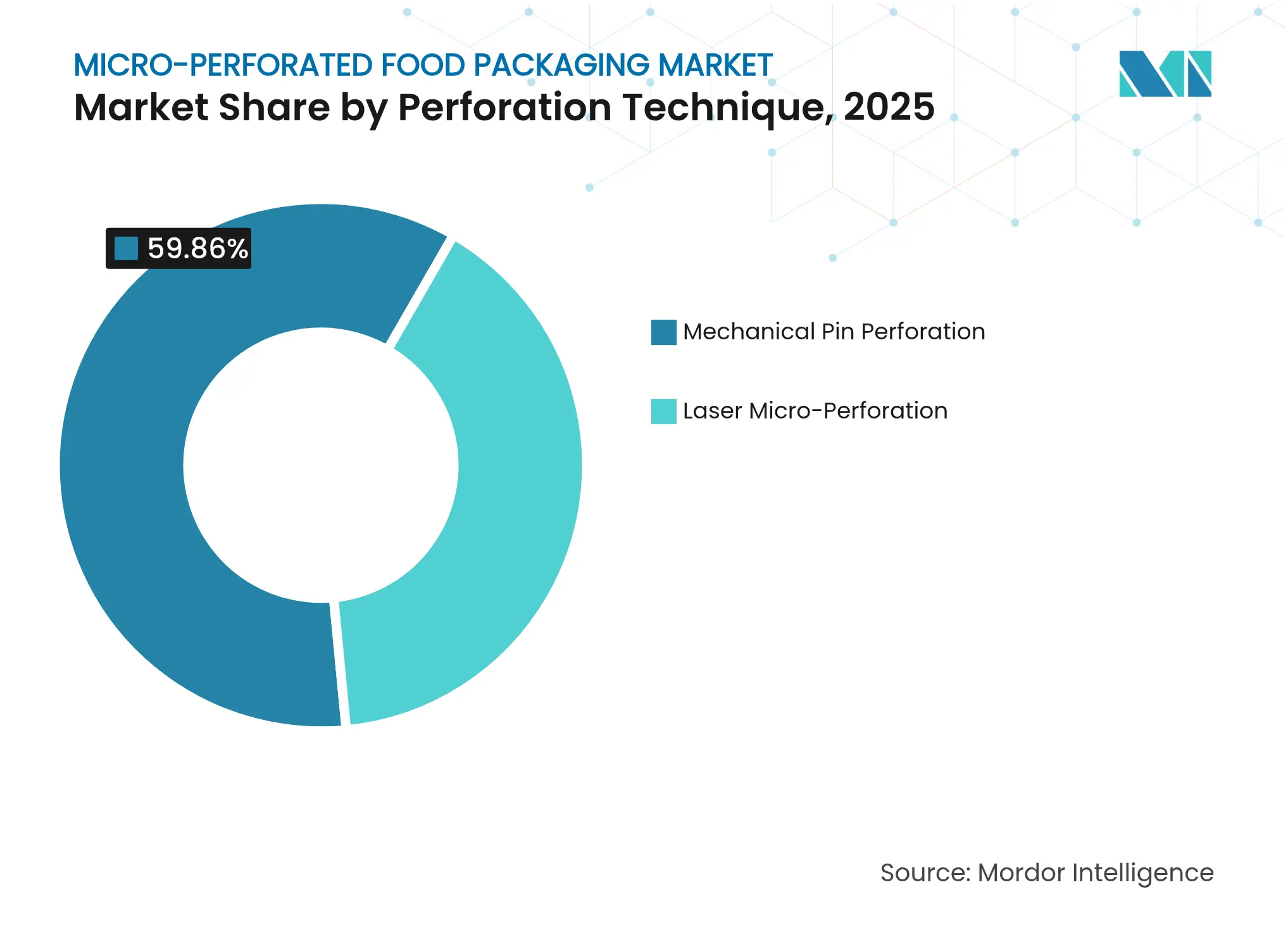

- By perforation technique, mechanical pin systems retained 59.86% share of the micro-perforated food packaging market size in 2025, whereas laser micro-perforation is set to grow at a 7.01% CAGR.

- By application, fresh fruits and vegetables accounted for 39.67% share of the micro-perforated food packaging market size in 2025, while ready-to-eat meals will log a 8.61% CAGR to 2031.

- By geography, North America commanded 35.12% of 2025 revenue; Asia-Pacific registers the fastest 6.92% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Micro-Perforated Food Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging consumption of fresh-cut produce via modern retail Surging consumption of fresh-cut produce via modern retail | +1.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:+1.2% |

Geographic Relevance

:Global, with concentration in North America & EU |

Impact Timeline

:Medium term (2-4 years) |

Demand for extended-shelf-life bakery and confectionery packs Demand for extended-shelf-life bakery and confectionery packs | +0.8% | Global, particularly strong in APAC emerging markets | Short term (≤ 2 years) | |||

Sustainability push for lightweight polyolefin films Sustainability push for lightweight polyolefin films | +0.6% | EU & North America leading, APAC following | Long term (≥ 4 years) | |||

Growth of e-commerce grocery delivery Growth of e-commerce grocery delivery | +0.5% | Global, with early gains in urban centers | Medium term (2-4 years) | |||

AI-driven laser perforation enabling dynamic OTR control AI-driven laser perforation enabling dynamic OTR control | +0.4% | North America & EU innovation hubs | Long term (≥ 4 years) | |||

Vertical-farm micro-portion produce packaging Vertical-farm micro-portion produce packaging | +0.3% | Regional, concentrated in Japan, Singapore, Netherlands | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Consumption of Fresh-Cut Produce via Modern Retail

Retail chains demand packaging that holds optimal gas composition for 7-14 days versus the prior 3-5 day benchmark, driving wider adoption of the micro-perforated food packaging market. Studies show micro-perforated PLA film can extend cherry tomato shelf life by 40% while preserving nutrients. The trend dovetails with urban consumers’ preference for convenience and supports vertically integrated retailers that set in-house packaging specs.

Demand for Extended-Shelf-Life Bakery and Confectionery Packs

Moisture management is critical to prevent staleness or mold. Laser systems produce 30-100 µm holes, enabling precise water-vapor control and helping brands expand into humid export markets. Private-label lines leverage the performance boost to position products as “long-lasting fresh,” sustaining the micro-perforated food packaging market’s momentum.

Sustainability Push for Lightweight Polyolefin Films

EU Regulation 2025/40 compels 30% recycled content in plastic food packs by 2030, accelerating thinner-gauge films that use 15-20% less resin while keeping the same OTR. Producers cut raw-material cost—roughly 60-70% of total film expenses—while meeting compliance needs.[1]European Union, “Regulation 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu

Growth of E-Commerce Grocery Delivery

Transit times stretch to 24-48 hours in online grocery channels, compared with 6-12 hours in physical retail. Optimized micro-perforated packs paired with ice packs reduced litchi quality losses by 35% in one study, underscoring their fit for e-commerce. Rising online penetration boosts demand for protective, breathable formats that safeguard produce during the last mile.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of laser-perforated film production High cost of laser-perforated film production | -0.7% | Global, particularly impacting price-sensitive markets | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:-0.7% |

Geographic Relevance

:Global, particularly impacting price-sensitive markets |

Impact Timeline

:Short term (≤ 2 years) |

Plastic-waste legislation and recyclability mandates Plastic-waste legislation and recyclability mandates | -0.4% | EU & North America leading, expanding globally | Medium term (2-4 years) | |||

Crop-specific respiration variability causing shrink losses Crop-specific respiration variability causing shrink losses | -0.3% | Global, with higher impact in tropical and subtropical regions | Medium term (2-4 years) | |||

Emergence of cellulose-based breathable films Emergence of cellulose-based breathable films | -0.2% | EU & North America innovation hubs, spreading to APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Laser-Perforated Film Production

Laser units cost USD 200,000-500,000 per line and consume 30-50% more energy than mechanical systems, inflating operating costs and limiting uptake among small converters. The premium narrows as volumes rise but remains a near-term hurdle for the micro-perforated food packaging market.

Plastic-Waste Legislation and Recyclability Mandates

The EU’s ban on PFAS in food packaging and the call for full recyclability by 2030 force redesigns and raise compliance costs. Divergent national rules in Asia add complexity for exporters, elevating risk and slowing investment decisions.

Segment Analysis

By Material: Biodegradable Films Challenge PE Dominance

Polyethylene retained 37.92% micro-perforated food packaging market share in 2025 owing to cost efficiency and broad converter familiarity. Biodegradable films chart an 8.05% CAGR, propelled by retailer pledges to switch to compostable solutions. Research confirms that perforated PLA matches PE’s shelf-life gains while composting within six months. The micro-perforated food packaging market size for biodegradable materials is projected to climb steadily as regulations tighten.

Technical hurdles remain: PLA’s moisture sensitivity and lower heat resistance require formulation tweaks and chilled-storage logistics. Suppliers now add nucleating agents and specialty coatings that deliver comparable OTR without undermining clarity. Such upgrades help the micro-perforated food packaging industry meet recycled-content targets without sacrificing performance.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Flow-Wraps Gain E-Commerce Traction

Bags and wickets commanded 44.73% revenue in 2025, reflecting entrenched retail practices and low unit cost. Flow-wraps and pouches are on track for a 7.23% CAGR, buoyed by online grocery’s need for puncture-resistant formats. Inline perforation during flow-wrap sealing trims a processing step and curbs waste, boosting throughput. When tied to advanced pattern control, flow-wraps can hold specific OTR profiles for delicate berries during two-day shipping, reinforcing their appeal within the micro-perforated food packaging market.

Lidding films and trays service premium meal-kit providers that seek window clarity and rigid protection. Suppliers integrate peel-reseal features that allow consumers to portion fresh produce, extending usability and reducing waste—another tailwind for the micro-perforated food packaging industry.

By Perforation Technique: Laser Technology Drives Precision Revolution

Mechanical pin systems still account for 59.86% of the micro-perforated food packaging market size due to low capex and ease of maintenance. Laser micro-perforation grows 7.01% yearly, providing 30 µm hole diameters and tighter tolerances. AI-linked lasers monitor product respiration rates and auto-correct patterns, reducing rejects and supporting premium SKUs. Acoustic sensors verify hole integrity in real time, shortening setup cycles.

High equipment cost slows adoption in emerging markets, yet co-packers servicing multinational brands increasingly specify laser quality for export compliance. Mechanical lines remain relevant for bulk produce where exact OTR is less critical, confirming a dual-technology landscape within the micro-perforated food packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Ready-to-Eat Meals Drive Innovation

Produce retained 39.67% share in 2025, underscoring the category’s reliance on respirable packaging. Ready-to-eat meals lead growth at 8.61% as urban dwellers embrace convenience. Multi-component trays demand zone-specific perforation to balance proteins, vegetables, and sauces. Some converters embed QR-enabled freshness sensors that track internal CO₂ build-up, cutting waste and differentiating premium SKUs. Bakery segments exploit micro-perforation mainly for moisture venting rather than oxygen ingress, confirming diverse functional needs across the micro-perforated food packaging market.

Meat, fish, and cheese require low-oxygen atmospheres to avert spoilage. Perforation counts are minimal yet critical; too many holes trigger oxidation, too few foster anaerobic conditions that breed pathogens. Precision tuning, therefore, positions laser systems as the preferred option in chilled protein case-ready packs.

Geography Analysis

North America’s dominance stems from harmonized FDA guidelines and retailer demand for 7-14 day shelf life. Supermarket chains enforce stringent vendor scorecards that reward reduced shrink, resulting in broad acceptance of micro-perforated solutions. The region also leads in e-commerce grocery orders exceeding 15% penetration, amplifying the value of robust breathable packs that endure parcel networks.

Europe aligns growth with sustainability imperatives. Regulation 2025/40 mandates full recyclability, compelling converters to redesign film structures around monomaterial PE or paper composites. Germany and the Netherlands pilot vertical farming tie-ups where Grower-Packer-Retailer collaborations specify delivered OTR at pack hand-over. The United Kingdom balances EU divergence with its Plastics Packaging Tax, nudging adoption of recycled-content micro-perforated films.

Asia-Pacific’s rapid urbanization and rising disposable incomes underpin surging demand. Chinese e-commerce giants set strict delivery freshness KPIs, spurring investment in AI-driven laser perforation lines. Japan focuses on micro-portion packs for single-person households; precision breathable pouches ensure that leafy greens stay crisp for a week. Southeast Asian regulators, led by Thailand’s heavy-metal limits for food-contact films, compel converters to upgrade to compliant, micro-perforated designs, fueling regional market growth.

Competitive Landscape

Market Concentration

The micro-perforated food packaging market remains moderately fragmented, though the Amcor-Berry Global combination elevates scale-driven R&D. The merged entity’s USD 180 million annual innovation budget accelerates new resin chemistries and AI-laser platforms.[3]Amcor, “Amcor Completes Combination with Berry Global,” amcor.com Sealed Air intensifies focus on food e-commerce partnerships, rolling out perforated Cryovac lines optimized for cold-chain parcels. Mondi invests in paper-based micro-perforated wraps aimed at confectionery, coupling barrier coatings with curbside recyclability.

Specialists like Elen Laser and Ultraperf differentiate through modular laser heads that retrofit onto existing flow-wrappers, lowering adoption barriers. Regional converters in Asia license patented acoustic monitoring to guarantee hole consistency at high line speeds, catering to multinational brand owners’ quality audits. Private-equity interest rises as smaller converters install first-generation lasers to serve vertical-farm suppliers, signaling continued consolidation potential inside the micro-perforated food packaging industry.

Micro-Perforated Food Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its all-stock combination with Berry Global, creating a larger packaging group targeting USD 3 billion annual cash flow.

- April 2025: Hotpack invested USD 100 million in a 70,000 sq ft New Jersey plant to manufacture customizable food packs for US clients.

- March 2025: Amcor priced USD 2.2 billion in senior notes to refinance merger debt and fund sustainable-packaging R&D.

- February 2025: The European Union enacted Regulation 2025/40 on Packaging and Packaging Waste, mandating 30% recycled content in PET food packs by 2030.

Table of Contents for Micro-Perforated Food Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surging consumption of fresh-cut produce via modern retail

- 4.2.2Demand for extended-shelf-life bakery and confectionery packs

- 4.2.3Sustainability push for lightweight polyolefin films

- 4.2.4Growth of e-commerce grocery delivery

- 4.2.5AI-driven laser perforation enabling dynamic OTR control

- 4.2.6Vertical-farm micro-portion produce packaging

- 4.3Market Restraints

- 4.3.1High cost of laser-perforated film production

- 4.3.2Plastic-waste legislation and recyclability mandates

- 4.3.3Crop-specific respiration variability causing shrink losses

- 4.3.4Emergence of cellulose-based breathable films

- 4.4Supply-Chain Analysis

- 4.5Regulatory Landscape, Policy and Standards

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

- 4.8Recycling and Sustainability Landscape

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material

- 5.1.1Polypropylene (PP)

- 5.1.2Polyethylene (PE)

- 5.1.3Polyethylene Terephthalate (PET)

- 5.1.4Biodegradable/Bio-based Films

- 5.1.5Other Material

- 5.2By Packaging Type

- 5.2.1Bags and Wickets

- 5.2.2Lidding Films and Trays

- 5.2.3Flow-wraps and Pouches

- 5.2.4Other Packaging Types

- 5.3By Perforation Technique

- 5.3.1Laser Micro-Perforation

- 5.3.2Mechanical Pin Perforation

- 5.4By Application

- 5.4.1Fruits and Vegetables

- 5.4.2Bakery and Confectionery

- 5.4.3Ready-to-Eat and Prepared Meals

- 5.4.4Meat, Fish and Cheese

- 5.4.5Other Applications

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Russia

- 5.5.2.7Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2India

- 5.5.3.3Japan

- 5.5.3.4South Korea

- 5.5.3.5Australia and New Zealand

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1Middle East

- 5.5.4.1.1United Arab Emirates

- 5.5.4.1.2Saudi Arabia

- 5.5.4.1.3Turkey

- 5.5.4.1.4Rest of Middle East

- 5.5.4.2Africa

- 5.5.4.2.1South Africa

- 5.5.4.2.2Nigeria

- 5.5.4.2.3Egypt

- 5.5.4.2.4Rest of Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves (MandA, JV, Capacity Adds)

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1Amcor Plc

- 6.4.2Sealed Air Corporation

- 6.4.3Mondi Plc

- 6.4.4Coveris Management GmbH

- 6.4.5KM Packaging Services Ltd

- 6.4.6Bolloré Group

- 6.4.7Uflex Ltd

- 6.4.8Specialty Polyfilms Pvt Ltd

- 6.4.9Greendot Biopak Pvt Ltd

- 6.4.10Ultraperf Technologies

- 6.4.11Nordfolien GmbH

- 6.4.12TCL Packaging Ltd

- 6.4.13Berry Global Inc

- 6.4.14Graphic Packaging International

- 6.4.15Preco LLC

- 6.4.16LasX Industries Inc

- 6.4.17ID Technology LLC

- 6.4.18Fresh Produce Technologies Inc

- 6.4.19ClearBags

- 6.4.20Elen Laser Systems

- 6.5Heat-Map Analysis

- 6.6Competitor Analysis – Emerging vs Established Players

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

Global Micro-Perforated Food Packaging Market Report Scope

Micro-perforated food packaging is a type of packaging that has tiny holes in it to allow for controlled airflow. This helps to regulate the levels of carbon dioxide and oxygen within the package, which can extend the shelf life of perishable food items like fruits, vegetables, and baked goods. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The micro-perforated food packaging market is segmented by material (Polypropylene (PP), Polyethylene (PE), Polyethylene Terephthalate (PET), and Other Materials), by application (Fruits & Vegetables, Bakery & Confectionary, Ready-to-Eat Products and Other Applications) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.