Organ-on-chip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

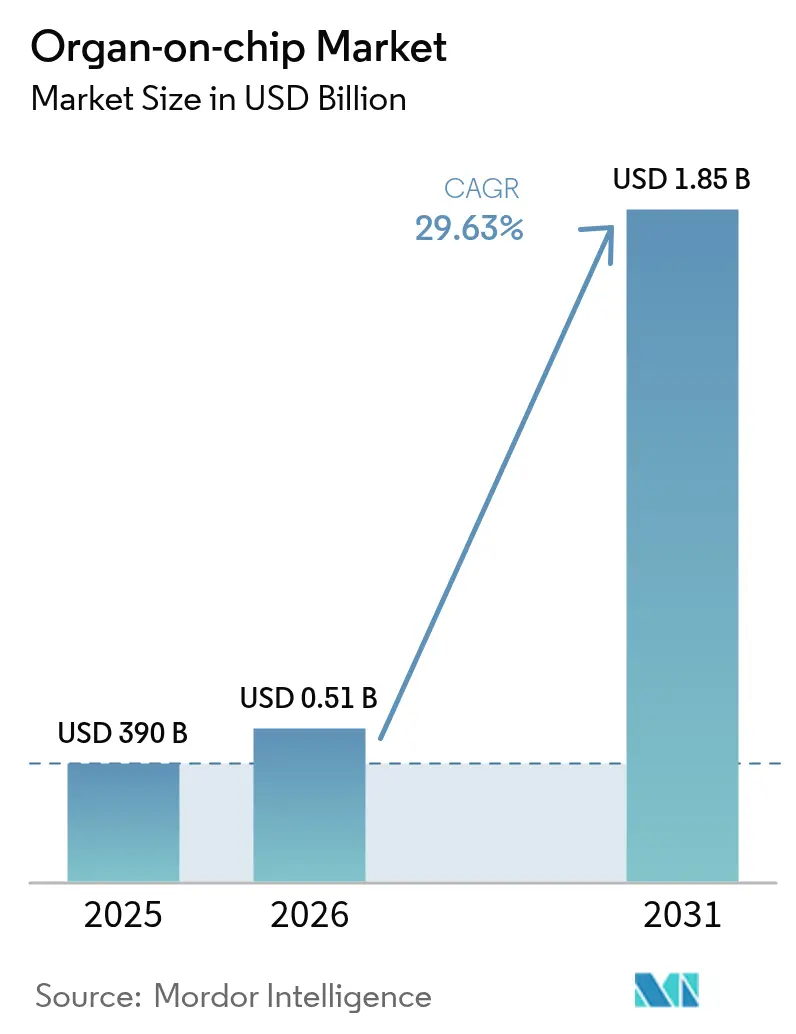

| Market Size (2026) | USD 0.51 Billion |

| Market Size (2031) | USD 1.85 Billion |

| Growth Rate (2026 - 2031) | 29.63% CAGR |

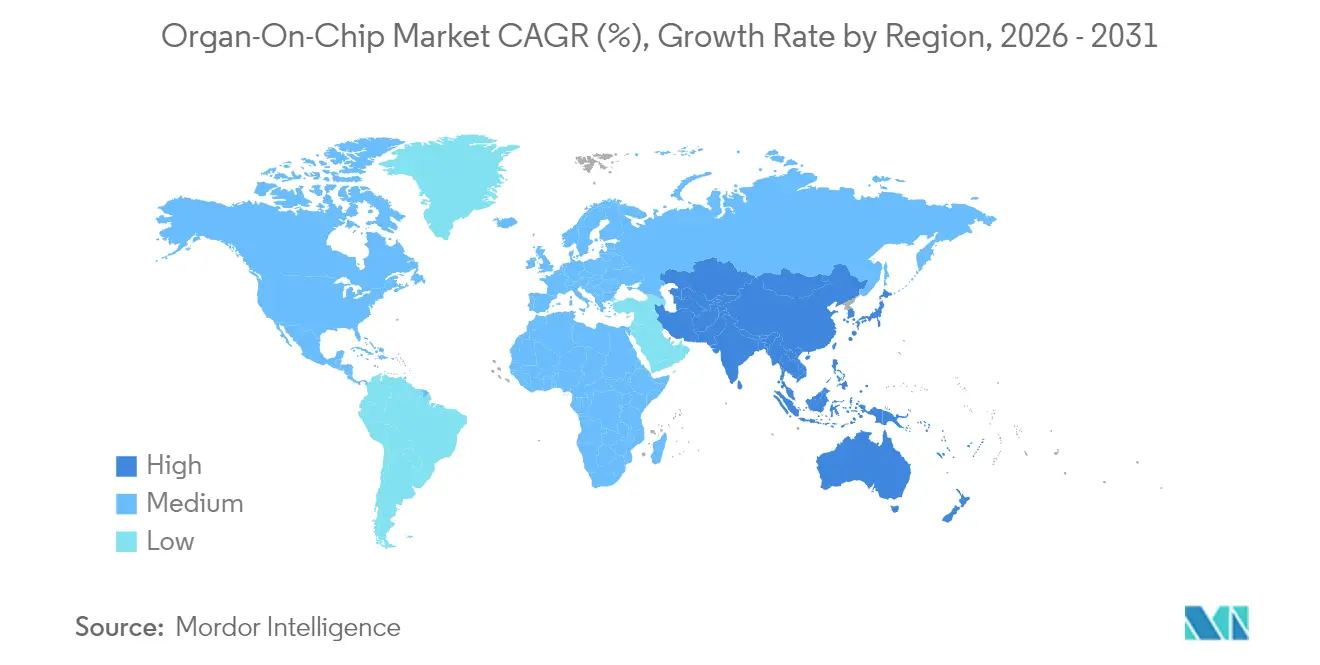

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organ-on-chip Market Analysis by Mordor Intelligence

The Organ-on-chip Market size is expected to grow from USD 390 million in 2025 to USD 510 million in 2026 and is forecast to reach USD 1.85 billion by 2031 at 29.63% CAGR over 2026-2031.

Demand is rising as regulators validate microphysiological systems, pharmaceutical firms redirect R&D funds toward animal-free testing, and 3D printing lowers device fabrication costs. Early commercial traction is strongest in North America, where the FDA Modernization Act 2.0 and the ISTAND Pilot Program have shortened approval timelines. Asia-Pacific is set for the fastest expansion on the back of heavy public spending, while Europe benefits from standardization roadmaps that ease cross-border adoption. Competitive intensity is growing as companies integrate artificial intelligence, strike co-development deals, and scale automated production lines.

Key Report Takeaways

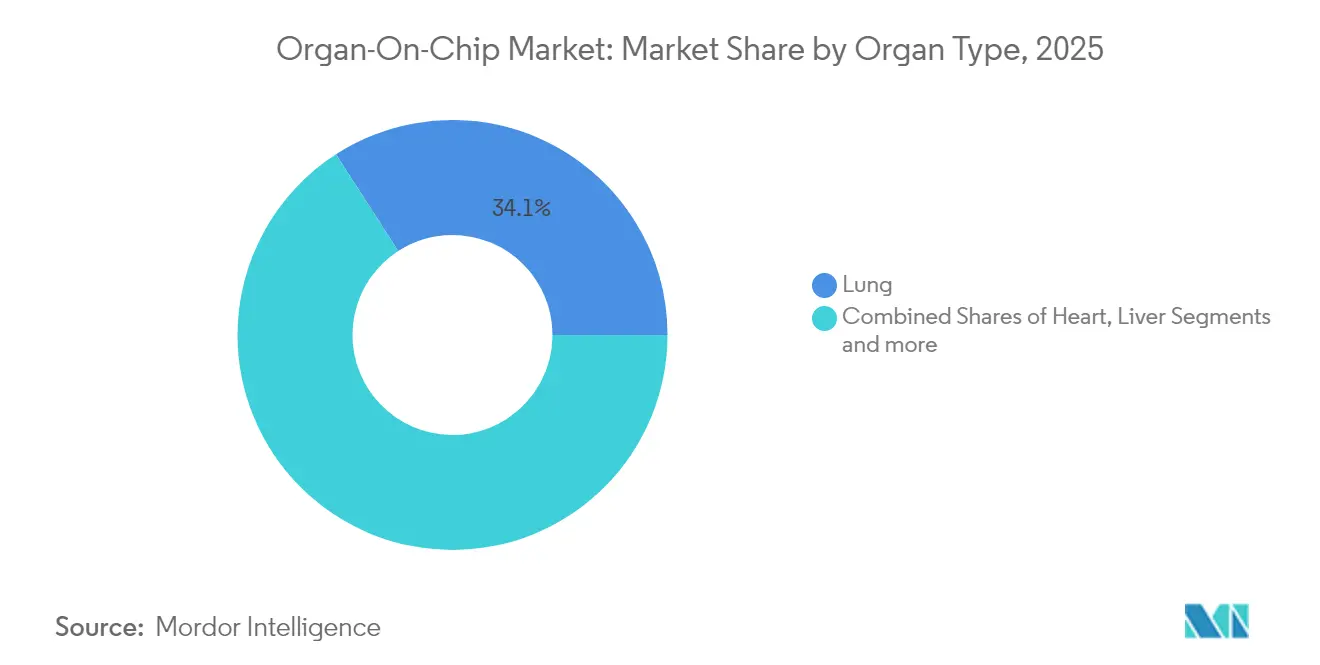

- By organ type, lung models led with 34.12% of organ-on-chip market share in 2025; heart chips are projected to grow at a 32.11% CAGR through 2031.

- By application, drug discovery platforms accounted for 57.45% of the organ-on-chip market size in 2025, while disease modeling is set to expand at a 33.18% CAGR to 2031.

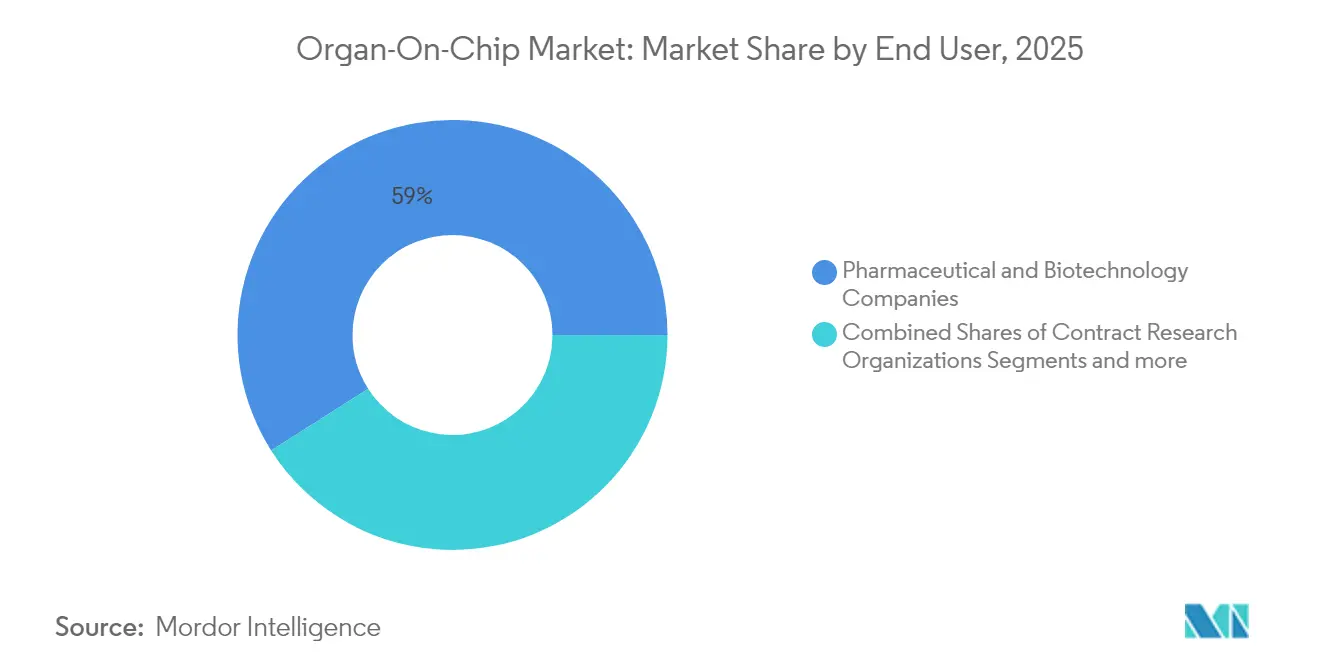

- By end user, pharmaceutical and biotechnology companies held 59.02% of the organ-on-chip market share in 2025; contract research organizations are positioned for the highest 35.07% CAGR between 2026-2031.

- By geography, North America dominated with 42.15% revenue share in 2025, whereas Asia-Pacific is forecast to register a 34.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Organ-on-chip Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Animal-free preclinical testing mandates | +7.5% | North America, Europe | Medium term (2-4 years) |

| Burden of chronic and complex diseases | +6.2% | Developed healthcare markets | Long term (≥ 4 years) |

| Precision medicine & patient-derived chips | +5.8% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Early detection of drug toxicity | +4.3% | Regions with strong pharmaceutical R&D | Short term (≤ 2 years) |

| Strategic investments & partnerships | +3.9% | North America, Europe, China | Short term (≤ 2 years) |

| Microfabrication & 3D bioprinting advances | +3.2% | Global innovation hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Shift Toward Animal-Free Preclinical Testing Mandates

The FDA’s decision in October 2025 to phase out compulsory animal studies for monoclonal antibodies, coupled with the FDA Modernization Act 2.0, is accelerating uptake of human-relevant test beds.[1]U.S. Congress, “FDA Modernization Act 2.0,” congress.gov The agency’s pilot program that lets developers submit non-animal data has prompted pharmaceutical groups to revise internal protocols and divert screening budgets to organ chips. Europe is moving in parallel as regulators tighten restrictions on animal research. These policy moves create a stable demand floor, drive procurement frameworks among contract research organizations, and shorten sales cycles for platform vendors. Firms that combine chips with AI-enabled analytics stand to benefit most because they offer a turnkey path that aligns with post-2025 compliance deadlines. The animal-free mandate therefore anchors medium-term revenue visibility in the organ-on-chip market.

High Burden of Chronic & Complex Diseases Requiring Better Models

Chronic disorders such as metabolic syndrome, non-alcoholic fatty liver disease, and neurodegenerative conditions account for an expanding share of global morbidity. A 2024 study using Hesperos’ multi-organ chip replicated NAFLD progression and highlighted therapeutic windows that animal models miss.[2]Hesperos Inc., “Human-on-a-Chip NAFLD Study,” nature.com This ability to mimic human pathophysiology supports go-no-go R&D decisions and lowers clinical attrition costs. Demand is especially pronounced in markets with aging populations and sizable public insurance schemes, which now prioritize translational research that directly benefits patient outcomes. As these health systems push for higher predictive validity, organ chips emerge as indispensable tools, sustaining long-term momentum in the organ-on-chip market.

Rising Demand for Precision Medicine & Patient-Derived Chips

Personalized oncology and rare-disease programs rely on test systems that capture individual heterogeneity. Researchers at Columbia University have built customizable multi-organ constructs linking heart, bone, liver, and skin tissues through vascular flow. By loading patient-specific cells, clinicians can benchmark therapeutic regimens before first-in-human dosing. Uptake is most evident at comprehensive cancer centers in the United States, Japan, and Germany, where reimbursement agencies are piloting outcome-based contracts that reward tailored interventions. This clinical pull continues to widen addressable use cases and cements organ-on-chip technology as a core pillar of precision medicine.

Need for Early Detection of Drug Toxicity and New Product Launches

Drug-induced liver injury accounts for nearly 40% of late-stage failures. The FDA’s acceptance of a human Liver-Chip into the ISTAND Pilot Program in September 2024 provides a validated route for toxicity claims.[3]U.S. Food and Drug Administration, “ISTAND Pilot Program Acceptance of Human Liver-Chip,” fda.gov CN Bio’s PhysioMimix Bioavailability assay kit, launched in November 2024, complements these efforts by assessing oral absorption under dynamic flow conditions. Together, regulatory endorsement and novel assays incentivize sponsors to integrate chips earlier in discovery. The resulting shift in workflow keeps short-term growth in the organ-on-chip market on track.

Restraints Impact Analysis of Organ-on-chip Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technical complexity & skill gap | −5.4% | Emerging markets | Medium term (2-4 years) |

| High capital & operating costs | −4.8% | Resource-limited regions | Short term (≤ 2 years) |

| Limited regulatory validation & guidelines | −3.6% | Regions with evolving frameworks | Medium term (2-4 years) |

| High CapEx for automated tool-chains | −3.2% | Emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technical Complexity & Skill Gap Hindering Broad Adoption

Operating microfluidic platforms demands cross-disciplinary expertise in cell biology, engineering, and sensor integration. A May 2024 review in Frontiers in Lab-on-a-Chip Technology surveyed smaller laboratories and found limited access to trained personnel and standardized protocols. Multi-organ systems exacerbate the burden because each module requires tight flow control and synchronized data capture. To bridge the gap, industry groups advocate modular devices, automated media exchange, and cloud-based analytics. Yet, until these tools become mainstream, complexity will temper uptake, particularly outside tier-one research hubs.

High Capital & Operating Costs of Microfluidic Infrastructure

Precision pumps, gas-controlled incubators, and high-content imaging add significant overhead. Consumables, frequent sterilization, and the need for skilled technicians inflate per-assay expenses. While LCD 3D printing has trimmed unit costs, many institutions still face budget constraints. Venture-backed startups can amortize equipment, but publicly funded labs often struggle to justify the initial outlay. As price compression proceeds, the organ-on-chip market will broaden, yet short-term adoption remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Organ-on-chip Market Segment Analysis

By organ type:

Lung dominance and cardiac accelerationLung chips commanded 34.12% of the organ-on-chip market share in 2025 due to their utility in respiratory toxicity, infectious-disease research, and aerosol delivery studies. The launch of high-fidelity 3D-bioprinted alveolar constructs by POSTECH researchers has strengthened model relevance and drawn funding from vaccine makers. These platforms mimic airway biomechanics, enable endpoints such as ciliary beat frequency, and integrate immune cell layers. With regulatory agencies prioritizing respiratory-drug safety following COVID-19, procurement remains steady. In parallel, heart-on-chip devices are on track for the fastest 32.11% CAGR through 2031, driven by arrhythmia screening and cardiotoxicity testing for oncology compounds. Automated fabrication that embeds force-sensing microwires reduces hands-on time and encourages broader deployment across academic core facilities.

The brain and central-nervous-system subsegment is gaining momentum as researchers seek alternatives to rodent models in neurodegenerative research. Kidney- and liver-based chips hold strong positions; the latter benefits from the ISTAND-validated human Liver-Chip, which anchors safety packages for metabolic candidates. Multi-organ arrays linking vascular, epithelial, and immune components represent the next frontier. Vendors that offer ready-to-use, modular plates stand to capture incremental orders as sponsors move toward systemic pharmacology studies.

By application:

Drug discovery leadership and disease modeling momentumDrug discovery remained the largest use case, representing 57.45% of organ-on-chip market size in 2025. Sponsors employ chip-based phenotypic screens to filter chemical libraries before investing in animal studies. The resulting hit-to-lead refinement lowers expenditure on low-probability compounds and shortens go-to-clinic timelines. Disease modeling, although smaller, is expanding at a 33.18% CAGR through 2031 as advanced chips recreate complex pathologies such as non-alcoholic steatohepatitis and inflammatory bowel disease. These systems support mechanism-of-action research and biomarker validation, activities that traditional cultures cannot replicate under dynamic perfusion.

ADME and toxicology workflows use liver, kidney, and gut constructs to estimate bioavailability, metabolic clearance, and off-target liabilities. The FDA’s focus on drug-induced liver injury metrics, combined with CN Bio’s newly launched bioavailability kit, signals official acceptance of chip-derived PK data. Precision-medicine deployments remain niche but are gaining clinical traction, especially in oncology where ex vivo tumor chips inform personalized regimens for refractory patients. Infectious-disease models that simulate pathogen entry across mucosal barriers round out the application portfolio.

By end user:

Pharma strength and CRO dynamismPharmaceutical and biotechnology companies accounted for 59.02% organ-on-chip market size in 2025 as they integrate microphysiological data into regulatory dossiers for new chemical entities. Internal labs run comparative studies that position chip read-outs alongside historical animal results, gradually phasing out legacy assays. Budgets earmarked for predictive toxicology and first-in-class modalities sustain recurring demand for consumables and software analytics.

Contract research organizations are forecast to outpace all other groups with a 35.07% CAGR to 2031. These service providers act as force multipliers for small and mid-cap sponsors that lack in-house microfluidic capacity. Several CROs have installed turnkey systems from Emulate and MIMETAS to expand fee-for-service menus covering cardiotoxicity, permeability, and disease modeling. Academic institutes continue to pioneer novel chip architectures, often spinning out venture-backed firms. Cosmetics and personal-care brands are piloting skin-on-chip assays to meet regulations that restrict animal testing, adding diversification to the demand base.

Geography Analysis

North America Organ-on-chip Market

North America generated 42.15% of 2025 revenue for the organ-on-chip market, buoyed by the FDA’s ISTAND framework, deep venture pools, and collaborations between Ivy League universities and big pharma. The United States hosts most early-stage chip trials, while Canada supplies polymer microfabrication expertise that feeds contract manufacturers. Reimbursement pilots under Medicare’s coverage-with-evidence paradigm further encourage hospital-based translational studies.

APAC Organ-on-chip Market

Asia-Pacific is on course for the swiftest 34.21% CAGR through 2031. China leverages state grants that subsidize microfluidic tooling, and its contract research ecosystem scales at speed to handle multinational outsourcing. Japan’s Pharmaceuticals and Medical Devices Agency has issued guidance on microphysiological data submissions, giving local developers a route to domestic approval. South Korean consortia align chip production with national initiatives in cell and gene therapy, creating synergistic demand.

Europe Organ-on-chip Market

Europe maintains a robust share powered by Horizon Europe grants and a consolidated academic network. The CEN/CENELEC roadmap published in July 2024 maps pathways for material qualification, sterilization, and cell integrity that foster cross-lab comparability. France and Germany finance industry clusters that pair nanoscale engineering with primary human-cell banks. The region’s stringent animal-welfare rules accelerate substitution of in vivo assays with chip models, especially in safety pharmacology and cosmetics.

Regulatory Landscape

Regulatory acceptance is shifting from broad support for New Approach Methodologies toward defined qualification and consensus-standard pathways for microphysiological systems (MPS), including organ-on-chip. In the United States, the FDA continues to use its Drug Development Tool (DDT) qualification programs and the ISTAND Pilot Program to let sponsors include non-animal, chip-derived evidence in submissions for specific contexts of use; this is reinforced by the FDA Modernization Act 2.0 and agency actions to reduce animal testing requirements for certain drug classes.

In Europe, standardization and regulatory-science alignment are tightening the translation path from research platforms to regulated use. The European Commission Joint Research Centre (JRC) published a dedicated organ-on-chip standardisation roadmap in January 2025, and CEN/CENELEC has advanced roadmaps for comparable performance assessment and handling practices across labs. At the same time, European regulators are updating 3Rs-oriented guidance to define how MPS evidence can be accepted under a context-of-use framework, supporting cross-border comparability that affects procurement and validation strategies for chip vendors and CROs.

Competitive Landscape

The organ-on-chip market is moderately fragmented, with over a dozen platform vendors, specialized component suppliers, and analytics startups. CN Bio’s tie-up with Altis Biosystems in January 2024 merged gut epithelium modules with liver constructs, delivering a PK-PD suite that addresses first-pass metabolism. Emulate licenses its hardware under multi-year contracts and bundles cloud analytics to lock in recurring subscription revenue. MIMETAS extends its OrganoPlate catalogue to kidney models, strengthening renal-toxicity coverage.

Funding rounds fuel product roadmaps and expansion. CN Bio’s Series B and Emulate’s multi-round pool support ISO-class clean-room capacity increases. New entrants such as BMF Biotechnology apply high-resolution 3D printing to create organ scaffolds, challenging incumbents on pricing. Artificial intelligence integration forms a competitive moat; Quris-AI’s Bio-AI platform, adopted by Merck KGaA, illustrates the appeal of machine-learning-ready datasets. White-space remains in multi-organ chips for immuno-oncology and rare genetic disorders, where few validated test beds exist. Vendors that build open, modular ecosystems can capture these unmet needs.

Strategic moves in 2025 include cross-licensing of sensor technologies, OEM agreements for pump assemblies, and partnerships with electronic-health-record vendors to streamline data import. Collectively, these actions deepen switching costs, widen solution breadth, and spur consolidation as firms seek scale efficiencies.

Organ-on-chip Industry Leaders

BiomimX SRL

Elveflow

Emulate Inc.

Altis Biosystems

AxoSim

- *Disclaimer: Major Players sorted in no particular order

Organ-on-chip Market Companies Covered in this Report

- Emulate

- Mimetas

- CN Bio Innovations

- TissUse

- Hesperos

- AxoSim Technologies

- Altis Biosystems

- InSphero

- Nortis

- Kirkstall Ltd

- Netri SAS

- BiomimX

- Bi/ond BV

- Organovo

- Allevi Inc. (3D Systems)

- Elveflow (Elvesys)

- Hurel

- Valo Health (Tara Biosystems)

- SynVivo (CFD Research)

- BioChip Technologies GmbH

Market Opportunities and Future Outlook

A near-term opportunity is moving organ-on-chip from bespoke studies toward standardized, repeatable workflows that align with regulator-facing contexts of use. The creation of IAMPS in February 2026, with members including InSphero, MIMETAS, NETRI, React4Life, TissUse, AlveoliX, and BiomimX, points to an industry push to harmonize terminology, performance expectations, and engagement with European funding and standards bodies. In parallel, the Critical Path Institute launched the New Approach Methodologies Developer Coalition (NAMs-DC) in May 2026, expanding precompetitive collaboration to strengthen data robustness and qualification dialogue with regulators.

Commercial whitespace remains in high-throughput and multi-organ systems that reduce the cost per decision in early R&D and support CRO scale-up. As of 2026, organ-on-chip evidence is being used in IND packages primarily as supporting data, including in hepatotoxicity and transporter-related studies, which increases demand for platforms that generate audit-ready datasets, standardized controls, and interoperable analytics. Vendors and service providers that bundle validated assays, consumables, and data pipelines around defined use cases can capture this shift as sponsors operationalize animal-reduction policies and build internal governance for NAM-aligned study designs.

Recent Industry Developments in Organ-on-chip Market

- May 2026: Critical Path Institute launched the New Approach Methodologies Developer Coalition (NAMs-DC) to coordinate developers of human-relevant tools, including microphysiological systems used in drug development. The coalition formalizes precompetitive collaboration around data expectations and qualification dialogue with regulators, supporting broader and more consistent deployment of organ-on-chip studies across sponsors and CROs.

- November 2025: Emulate launched Brain-Chip R1 in partnership with FUJIFILM Cellular Dynamics to model the neurovascular unit for drug transport and neuroinflammation studies. The release expands commercial organ-chip coverage into higher-value neuroscience workflows, while the partnership strengthens access to standardized iPSC-derived cell inputs that improve reproducibility across sites.

- September 2024: Emulate unveiled the Chip-R1 rigid chip designed with a minimally drug-absorbing profile to improve ADME and toxicology modeling performance. This materials-focused redesign addresses a common translational limitation in microfluidic assays, improving confidence in compound exposure measurements and supporting wider use in regulated safety study packages.

Organ-on-chip Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers organ-on-chip systems that use microfluidic channels to keep living cells under controlled flow, so organ-like functions can be measured for research and testing. Revenue includes the chips themselves, supporting instruments used with the chips, essential consumables, and related study-linked services.

Scope exclusions: stand-alone organoid culture plates and static 3D cell culture products without integrated microfluidic flow are excluded.

Segments Covered in This Report

- By Organ Type

- Liver

- Heart

- Lung

- Kidney

- Intestine

- Brain & CNS

- Skin

- Multi-Organ & Other Complex Systems

- By Application

- Drug Discovery & Lead Identification

- ADME/Toxicology Screening

- Disease Modeling

- Precision Medicine & Personalized Therapy

- Other Applications

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Academic & Research Institutes

- Cosmetics & Personal Care Industry

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries for what counts as organ-on-chip revenue and to anchor the demand drivers that realistically move this market. We referred to public sources such as the US FDA (for alternative testing guidance and the broader safety testing context), NIH and EU funding portals (to track grant direction), OECD and national toxicology programs (for regulatory testing signals), and peer-reviewed journals indexed on PubMed (for adoption patterns and technology maturity). Trade association websites and reputed science press were also used to confirm common use cases in pharma labs, academic centers, and CRO workflows.

To keep company revenue mapping consistent, we reviewed filings, investor decks, product brochures, and press releases, and we used a paid subscription for company financials and intelligence when disclosures were limited. Patent databases were also checked to understand where development activity is concentrated and how multi-organ and disease-model work is progressing. These examples are not exhaustive, and many other public sources were used for data collection, clarification, and cross-checking.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with people who directly plan, run, or procure organ-on-chip studies, including platform suppliers, chip developers, reagent and consumable providers, CRO users, and lab managers in pharma, biotech, and academia. These discussions helped validate adoption pace, typical study volumes per lab, pricing movement for chips and consumables, and how often services are purchased instead of running workflows fully in-house. Since this is a global market, we balanced coverage across major demand centers so assumptions could be corrected before sign-off.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 17% | APAC: 47% |

| Mid tier: 44% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 18% | Managers: 52% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the active demand pool using research spending signals and the rate at which organ-on-chip moves from pilots into repeat study use. In practice, the model links adoption to a few observable inputs, which are then translated into revenue through typical pricing and usage patterns.

Key inputs include (illustrative) the count of research programs that require human-relevant in vitro testing, the mix of drug discovery versus toxicology use, average chips consumed per study run, the share of work outsourced to CRO services, and blended pricing for chips, consumables, and instruments. Because some disclosures are partial, we do selective bottom-up checks through sampled price points, supplier and channel checks, and a limited roll-up of visible revenues. This helps identify whether any major revenue stream is being over-counted or missed.

Forecasts rely mainly on scenario analysis supported by expert views, since adoption can shift quickly when new validation studies, funding waves, or policy signals occur. Growth paths were stress-tested by adjusting variables like penetration into pharma labs, repeat purchase frequency, and the pace of multi-organ platform uptake, then rechecked against interview feedback.

Data Validation & Update Cycle

Estimates are validated by triangulating the model output against independent signals such as funding direction, publication momentum, and how procurement behavior is changing for chips and related services. Variance checks are run across regions and use cases, and outliers are investigated through extra desk checks and targeted re-contacts when needed. Before sign-off, the work is reviewed in multiple steps so the assumptions, math, and scope treatment are consistent.

Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory guidance shifts, large funding announcements, or meaningful pricing changes. Before delivery, a final review pass is completed so clients receive the most current view available at the time.

Mordor Intelligence's Organs On Chips Market Size Compared Against Other Published Estimates

Published market sizes for organ-on-chip often do not match because scope lines are drawn differently, and the demand pool is measured using different signals. Some figures focus mainly on chips, others add instruments, consumables, and service revenue, and the year used as the current size also changes the headline value.

Evidence such as repeat purchase behavior in labs, service attachment rates to platform installs, and the mix of drug discovery versus toxicology workloads are used to check the Mo... scope, keeping Mordor Intelligence aligned to chips, supporting instruments, essential consumables, and study-linked services only (excluding stand-alone organoid plates without microfluidic flow).

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.51 B (2026) | |

| Global Consultancy A | USD 0.16 B (2024) | Uses an earlier base year and is commonly built from a narrower revenue frame, which can under-count consumables pull-through and recurring service revenue tied to ongoing study runs. |

| Industry Advisory B | USD 0.30 B (2025) | Structured as a total addressable market view with scenario bands, and it can include broader revenue buckets like software, data, and biomaterials, which shifts totals depending on the assumed adoption curve. |

The spread mainly comes from what is treated as in-scope revenue and which year is used as the current anchor. By tying pricing and volume assumptions back to observable usage patterns and cross-checking them through interviews, we keep the final number traceable and practical to update as new signals emerge.

Key Questions Answered in the Report

What is the projected value of the organ-on-chip market by 2031?

The organ-on-chip market is forecast to reach USD 1.85 billion by 2031, driven by a 29.63% CAGR.

Which organ model currently generates the highest revenue?

Lung chips lead with 34.12% of 2025 revenue, reflecting strong demand in respiratory research and inhalation toxicity testing.

Why are contract research organizations expected to grow fastest?

CROs provide outsourced microphysiological testing services that appeal to sponsors lacking in-house infrastructure, leading to a 35.07% CAGR outlook between 2026-2031.

How are regulators supporting organ-on-chip adoption?

The FDA’s ISTAND Pilot Program accepts chip-generated safety data, while the FDA Modernization Act 2.0 removes animal-test mandates, creating clear pathways for alternative methods.

What technological advances are lowering costs?

LCD 3D printing and automated thermoplastic fabrication have cut per-device production expenses, enabling mass manufacture of high-resolution chips.

Which region will expand the fastest and why?

Asia-Pacific is set for a 34.21% CAGR due to government R&D subsidies, a growing pharmaceutical base, and emerging regulatory guidance that endorses chip data in submissions.

Page last updated on: